Content

What is the Current Biodegradable Electronics Polymers Market Size and Share?

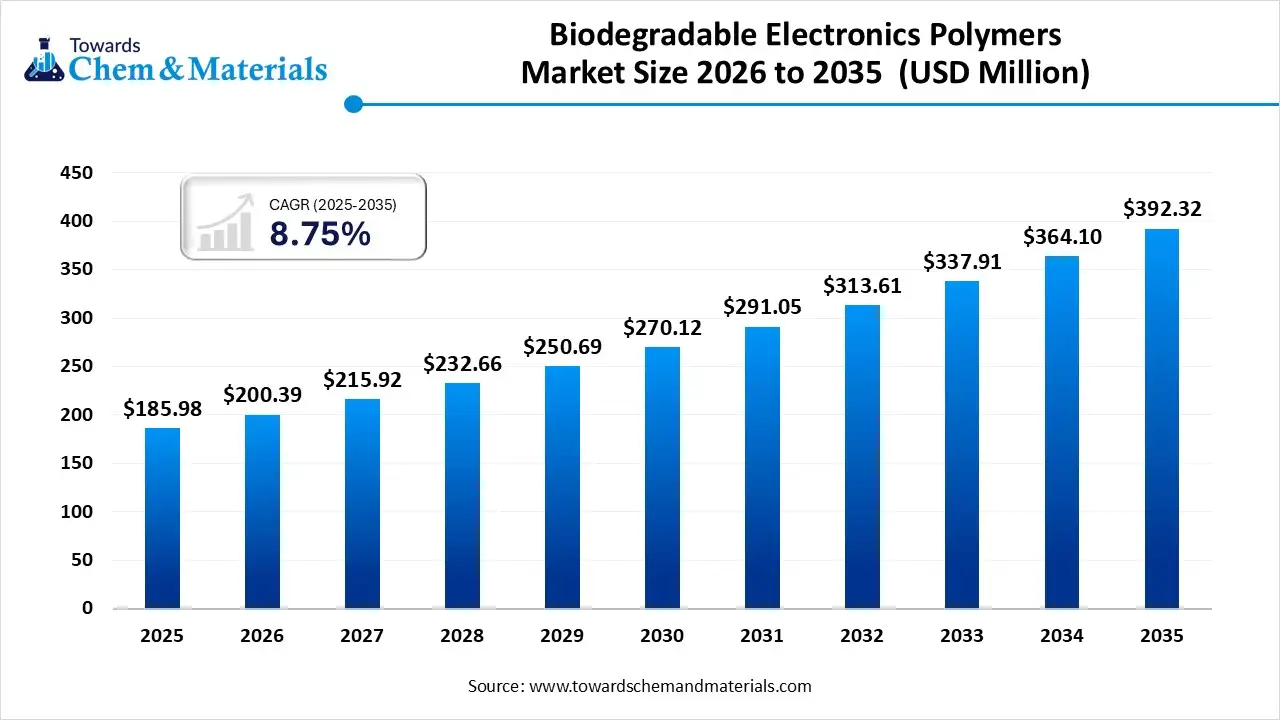

The global biodegradable electronics polymers market size was estimated at USD 185.98 million in 2025 and is expected to increase from USD 200.39 million in 2026 to USD 392.32 million by 2035, growing at a CAGR of 7.75% from 2026 to 2035. North America dominated the biodegradable electronics polymers market with the largest revenue share of 41.00% in 2025. Driven by rising e-waste concerns and demand for sustainable materials, key polymers like PLA, PCL, and PHA are replacing traditional plastics in flexible circuits, sensors, and transient electronics.

")

Market Highlights

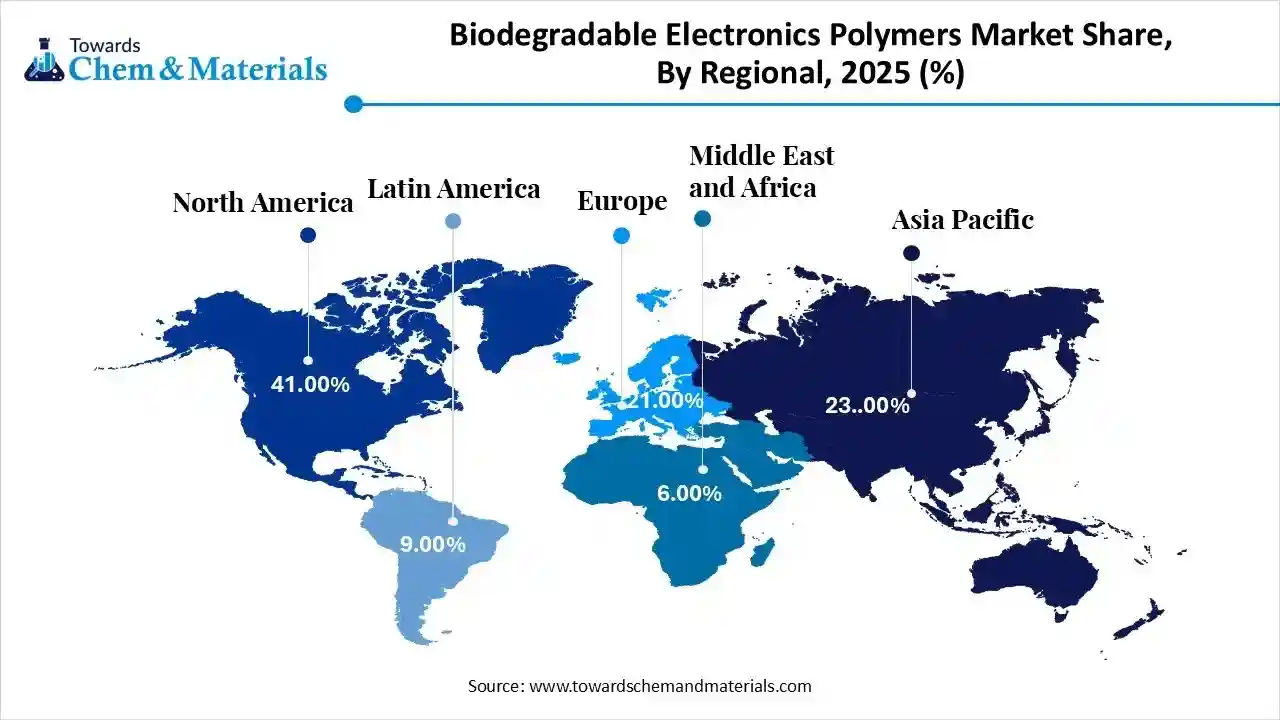

- The North America dominated the biodegradable electronics polymers market with the largest share of 41.00% in 2025.

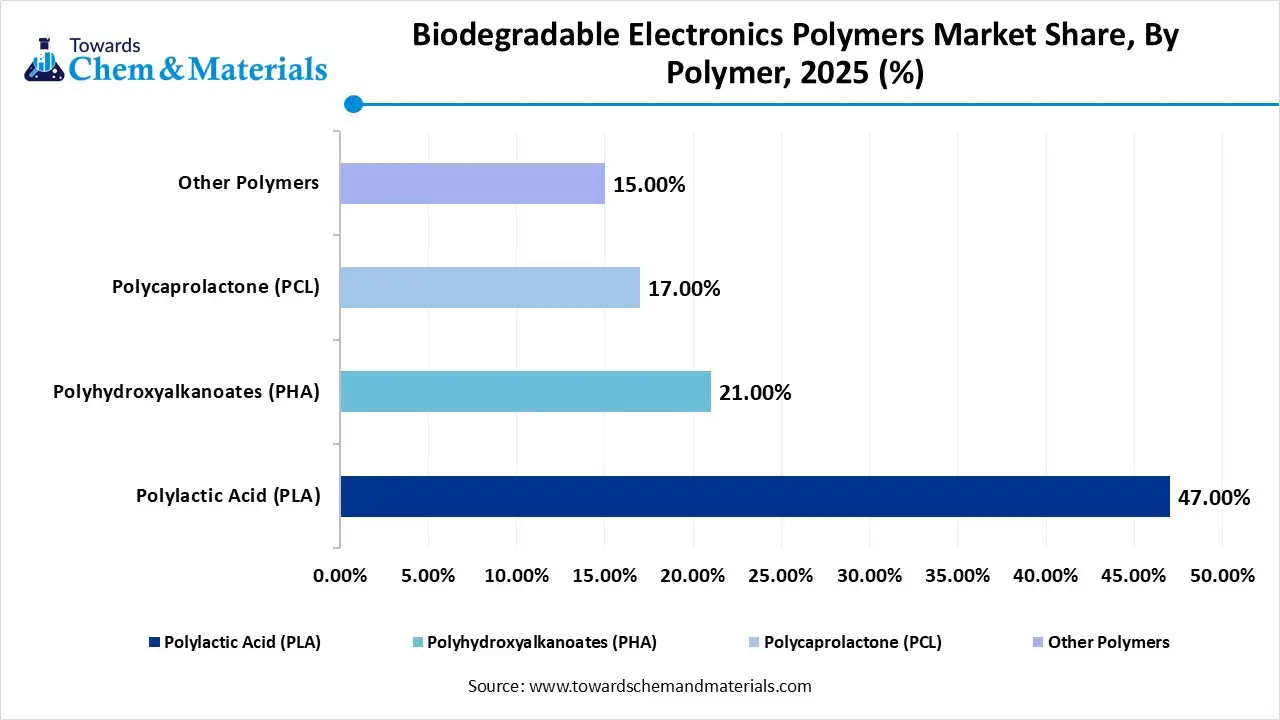

- By polymer, the polylactic acid segment dominated the market and accounted for the largest share of 47.00% in 2025.

- By polymer, the Polyhydroxyalkanoates (PHA) segment is anticipated to grow at a substantial CAGR of 8.85% from 2026 to 2035..

- By application, the flexible electronics segment led the market with the largest revenue share of 38.00% in 2025 and is forecasted to grow at the fastest CAGR of 8.25% from 2026 to 2035.

- By application, the printed electronics segment is projected to grow at a substantial CAGR of 7.95% from 2026 to 2035.

Market Overview

What Is the Significance of the Biodegradable Electronics Polymers Market?

The market is crucial for mitigating global electronic waste (e-waste) by enabling the creation of transient, eco-friendly, and wearable devices. These materials, including PLA, PCL, and conductive polymers, are transforming sectors like healthcare and consumer electronics by providing sustainable, dissolvable, or biodegradable alternatives to traditional plastic components.

Biodegradable Electronics Polymers Market Growth Trends:

- Rise of Transient Electronics: Development is increasing for devices that dissolve or degrade after use, particularly for environmental monitoring and medical implants.Technological Shift: Shift from "price-focused" to "performance-driven" adoption in electronics, agriculture, and healthcare.

- Key Material Trends: PLA remains in high demand, but there is increasing use of Polyhydroxyalkanoates (PHA) and conductive polymers like polyaniline (PANI) for functional, transient electronics.

Report Scope

| Report Attribute | Details |

| Market Size and Volume in 2026 | USD 200.39 Million |

| Revenue Forecast in 2035 | USD 392.32 Million |

| Growth Rate | CAGR 7.75% |

| Forecast Period | 2026 - 2035 |

| Base Year | 2025 |

| Dominant Region | North America |

| Segment Covered | By Polymer, By Application, By Regions |

| Key companies profiled | BASF SE, NatureWorks LLC, Mitsubishi Chemical Corporation, Novamont S.p.A., TotalEnergies Corbion, Biodegradable Electronics Polymers, Daicel ChemTech, Polysciences, Inc., Lubrizol, CD Bioparticles, Evonik Industries, Biome Bioplastics,Danimer Scientific |

Key Technological Shifts in the Biodegradable Electronics Polymers Market:

The biodegradable electronics polymers market is undergoing a significant transformation, moving from early-stage research to commercial-scale, driven by the urgent need for sustainable e-waste solutions. Key technological shifts and advancements are enhancing the performance, processing, and application of these materials. The use of 3D printing (FDM and SLS) with biodegradable materials is enabling customized production of electronic components, such as sensors, circuits, and casings.

Trade Analysis Of Biodegradable Electronics Polymers Market: Import & Export Statistics

- According to Global Export Data, from July 2024 to June 2025 (TTM), the world exported 339 shipments of Biodegradable Resin through 87 verified exporters and 99 buyers.

- The leading importers are India, Chile, and Vietnam, while the largest exporters are China with 614 shipments, India with 157 shipments, and Vietnam with 61 shipments.

- Additionally, during the same period, 451 shipments of Biodegradable Plastic were exported globally via 124 verified exporters and 126 buyers.

- The top importers are the United States, Vietnam, and Colombia, while China with 650 shipments, Vietnam with 112 shipments, and Italy with 59 shipments, are the leading exporters.

Biodegradable Electronics Polymers Market Value Chain Analysis

Polymer Synthesis & Electronic Material Processing

- Biodegradable electronic polymers are produced through controlled polymerization and functional modification of biodegradable backbones, followed by compounding with conductive fillers, film formation, printing, coating, and flexible substrate integration for transient electronics, wearable sensors, medical implants, and eco-friendly electronic components.

- Key players: Evonik Industries, BASF SE, NatureWorks LLC, Corbion

Quality Testing and Certification

- Biodegradable electronic polymers require certifications ensuring electrical conductivity stability, biodegradation safety, biocompatibility, and regulatory compliance. Key certifications include ISO quality standards, ISO 10993 biocompatibility standards, ASTM biodegradability testing standards, REACH compliance, and FDA approvals for implantable or medical electronic applications.

- Key players: ISO (International Organization for Standardization), ASTM International, FDA (U.S. Food and Drug Administration), TÜV SÜD.

Distribution to Industrial Users

- Biodegradable electronic polymers are supplied to wearable electronics manufacturers, medical device companies, research institutions, flexible electronics developers, and sustainable consumer electronics producers.

Key players: Evonik Industries, NatureWorks LLC, BASF SE.

Biodegradable Electronics Polymers Regulatory Landscape: Global Regulations

| Country / Region | Regulatory Body / Agency | Key Regulations / Policies | Focus Areas |

| United States | FDA (Food and Drug Administration) EPA (Environmental Protection Agency) OSHA (Occupational Safety and Health Administration) |

FDA medical device regulations (for implantables and bioelectronics) EPA chemical/biodegradability guidance OSHA nanomaterial & polymer handling guidance |

Biocompatibility & clinical safety Chemical safety and environmental compliance Workplace hazard communication |

| European Union | European Medicines Agency (EMA) European Chemicals Agency (ECHA) European Commission (DG Environment / DG GROW) |

Medical Device Regulation (MDR 2017/745) REACH (Registration, Evaluation, Authorization & Restriction of Chemicals) CLP (Classification, Labelling & Packaging) EU Circular Economy / Waste Framework rules |

Clinical/medical safety & performance Chemical registration & hazard labeling Environmental sustainability & EOL performance Eco-design standards |

| China | National Medical Products Administration (NMPA) Ministry of Ecology and Environment (MEE) Standardization Administration of China (SAC) |

Medical device registration & safety standards Environmental protection laws (air/water quality) Product standards for biodegradable plastics |

Clinical safety & approval Chemical and environmental compliance Standards development |

| Middle East & Africa | UAE: Ministry of Climate Change & Environment (MOCCAE) Saudi Standards, Metrology & Quality Org. (SASO) South Africa: Department of Forestry, Fisheries and the Environment (DFFE) |

Environmental protection & chemical safety laws Hazard communication aligned with GHS Consumer product standards |

Environmental compliance Worker hazard communication Equipment/product safety |

Segmental Insights

Polymer Insights

How did Polylactic Acid Segment Dominate the Biodegradable Electronics Polymers Market in 2025?

The polylactic acid segment dominated the market in 2025 accounting for 47.00% of total revenue and is forecasted to grow at a 7.15% CAGR from 2026 to 2035. driven by its high versatility, transparency, and superior moldability for sustainable, eco-friendly, and compostable packaging and consumer electronics. The market dominance was fueled by increased regulatory pressure to reduce electronic waste and technological advancements, such as high-heat-resistant PLA, which made the material more durable and versatile for advanced applications.

")

The polyhydroxyalkanoates segment is projected to grow at the fastest CAGR of 8.88% between 2026 and 2035 in the market, driven by their superior marine biodegradability and mechanical properties. PHAs are expected to see significant demand due to increasing environmental regulations and the shift toward sustainable, eco-friendly materials. The demand is fueled by the need for sustainable alternatives to traditional plastics, particularly in packaging and agriculture.

Biodegradable Electronics Polymers Market Share, By Polymer, 2025 (%)

| By Polymer Type | Revenue Share, 2025 (%) |

| Polylactic Acid (PLA) | 47.00% |

| Polyhydroxyalkanoates (PHA) | 21.00% |

| Polycaprolactone (PCL) | 17.00% |

| Other Polymers | 15.00% |

Application Insights

Which Application Segment Dominates the Biodegradable Electronics Polymers Market in 2025?

The flexible electronics segment dominated the market in 2025 accounting for 38.00% of total revenue,and is forecasted to grow at the fastest CAGR of 8.25% from 2026 to 2035 driven by high demand for eco-friendly, wearable, and comfortable devices. This dominance was propelled by advancements in Polyhydroxyalkanoates (PHA) and PLA materials, allowing for biodegradable foldable screens, sensors, and sustainable IoT devices. Rapid adoption of fitness trackers, smartwatches, and health-monitoring devices requires flexible, lightweight, and eco-friendly substrates.

The printed electronics segment is projected to grow at the fastest CAGR 7.95% between 2026 and 2035 in the market, driven by demand for sustainable, flexible, and transient devices to reduce e-waste. This sector is experiencing rapid innovation in conductive inks and substrates. Strong growth is fueled by stricter environmental regulations and increased adoption of biodegradable materials like PLA, PCL, and PHA in electronics manufacturing.

Biodegradable Electronics Polymers Market Share, By Application, 2025 (%)

| Application | Revenue Share, 2025 (%) |

| Flexible Electronics | 38.00% |

| Printed Electronics | 24.00% |

| Disposable Electronics | 16.00% |

| Consumer Electronics Components | 13.00% |

| Other Applications | 9.00% |

Regional Insights

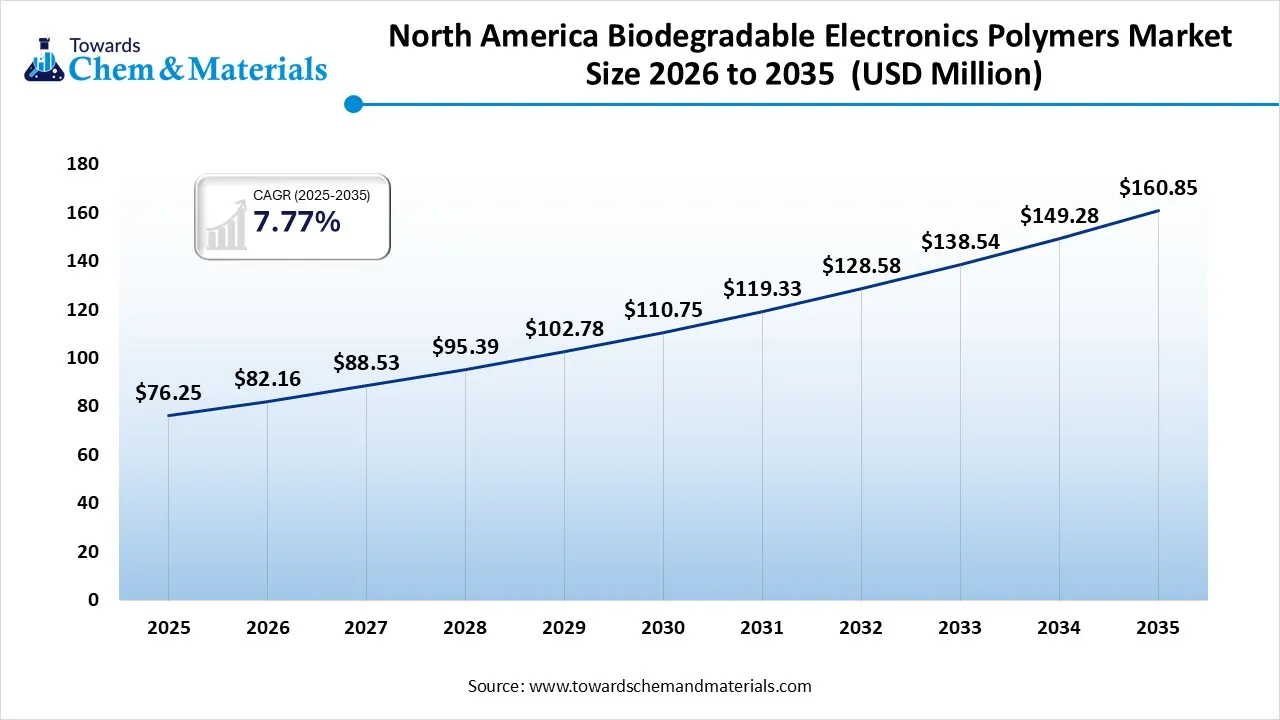

The North America biodegradable electronics polymers market size was valued at USD 76.25 million in 2025 and is expected to be worth around USD 160.85 million by 2035, exhibiting at a compound annual growth rate (CAGR) of 7.77% over the forecast period from 2026 to 2035. North America biodegradable electronics polymers market held the largest revenue share of 44% in 2025 .

")

North America dominated the market in 2025, due to the presence of strict regulations for the environment amid growing concerns regarding e-waste, increased demand for medical devices and wearable and increased investment in research and development by key players in the region like Dow, DuPont, and Lubrizol supports growth. The region benefited from advanced research facilities and partnerships, specifically developing biodegradable substrates and sensors for medical and IoT applications. North America's focus on integrating biodegradable polymers, such as PLA and PBS, into high-performance, sustainable electronic applications solidified its top market position.

U.S. Biodegradable Electronics Polymers Market Growth Factor

The U.S. biodegradable electronics polymers market is driven by rising environmental concerns, strict regulations on electronic waste, and the demand for sustainable, transient, and flexible components. Key growth factors include increasing adoption in medical and consumer electronics, with significant R&D in materials like PLA, PHA, and PCL. There is a surge in demand for biodegradable, flexible, and, in some cases, transient (temporary) electronic components in consumer devices and medical applications.

Asia Pacific Biodegradable Electronics Polymers Market Growth Factor

Asia Pacific is expected to the fastest growth in the market in the forecast period, driven by strict environmental regulations against single-use plastics, rising demand for sustainable and flexible wearables, and heavy investment in R&D by countries like China, Japan, and India. The shift towards a circular economy and the need to reduce electronic waste are key drivers for the adoption of materials like PLA and PHA in electronics, despite the high production costs compared to traditional plastics.

")

India Biodegradable Electronics Polymers Market Growth Factor

The Indian biodegradable electronics polymers market is primarily driven by strict government regulations on e-waste, rising environmental concerns, and the demand for sustainable, flexible, and transient electronic components. Growing awareness among Indian consumers about environmental impact is driving demand for green electronics, leading companies to adopt sustainable materials to enhance brand reputation. The development of durable, cost-effective bio-based materials is enabling their use in advanced electronic applications, overcoming previous performance limitations.

Biodegradable Electronics Polymers Market Share, By Regional, 2025 (%)

| Regional | Revenue Share, 2025 (%) |

| North America | 41.00% |

| Europe | 21.00% |

| Asia Pacific | 23.00% |

| Latin America | 9.00% |

| Middle East & Africa | 6.00% |

Europe Biodegradable Electronics Polymers Market Growth Factor

The European biodegradable electronics polymers market is driven by strict environmental regulations regarding e-waste, rising demand for sustainable, flexible, and wearable devices, and a shift toward circular economy initiatives. Key materials like Polylactic Acid (PLA) and Polyhydroxyalkanoates (PHA) are gaining traction, supported by advancements in electronics packaging and components.

Germany Biodegradable Electronics Polymers Market Growth Factor

The German biodegradable electronics polymers market is experiencing significant growth, driven by the country's stringent environmental regulations, a strong focus on sustainability, and the need to reduce electronic waste. Germany's strict policies regarding waste management and the EU's focus on circular economy initiatives are major drivers. The need to reduce electronic waste (e-waste) is pushing manufacturers to adopt biodegradable polymers in place of traditional, non-degradable plastics.

Recent Developments

- In July 2025, Balrampur Chini Mills Limited (BCML) introduced "Bioyug," India’s first industrial-scale brand for Polylactic Acid (PLA) biopolymers. This initiative represents a strategic move into green manufacturing, utilizing a fully integrated, sugarcane-to-PLA facility located in Kumbhi, Uttar Pradesh.(Source: thebetterindia.com)

- In March 2025, TotalEnergies Corbion and Benvic announced a strategic partnership to expand the use of low-carbon Luminy® PLA compounds in durable applications, specifically targeting the automotive and electronics sectors.(Source: totalenergies-corbion.com)

Top players in the Biodegradable Electronics Polymers Market & Their Offerings:

- BASF SE: BASF develops biodegradable polymer solutions, including polylactic acid (PLA) and other sustainable polymers used as substrates, encapsulants, and structural components in flexible electronics, printed sensors, and transient device applications.

- NatureWorks LLC: NatureWorks supplies Ingeo™ PLA and related biopolymer grades that are increasingly used in eco-friendly electronic components such as wearable gadgets, flexible circuits, and disposable sensors where controlled biodegradation is desired.

- Mitsubishi Chemical Corporation: Mitsubishi Chemical produces biodegradable polymer materials and compounds compatible with electronic manufacturing processes, targeting sustainable material integration in IoT and wearable devices.

- Novamont S.p.A.: Novamont focuses on biobased and biodegradable polymer technologies like Mater-BIO® products, offering materials suitable for eco-friendly electronic components and low-impact polymer systems.

- TotalEnergies Corbion: TotalEnergies Corbion supplies PLA and other biodegradable polymers tailored for electronics applications, and collaborates on low-carbon polymer formulations with industry partners to enhance performance in sustainable devices.

- Daicel ChemTech

- Polysciences, Inc.

- Lubrizol

- CD Bioparticles

- Evonik Industries

- Biome Bioplastics

- Danimer Scientific

Segments Covered:

By Polymer

- Polylactic Acid (PLA)

- Polyhydroxyalkanoates (PHA)

- Polycaprolactone (PCL)

- Other Polymers

By Application

- Flexible Electronics

- Printed Electronics

- Disposable Electronics

- Consumer Electronics Components

- Other applications

By Regions

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Asia Pacific

- China

- India

- Japan

- South Korea

- Latin America

- Brazil

- Argentina

- Middle East & Africa

- Saudi Arabia

- South Africa

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

FAQ's

Select User License to Buy

Figures (4)