Content

What is the Current Oil & Gas Market Size and Share?

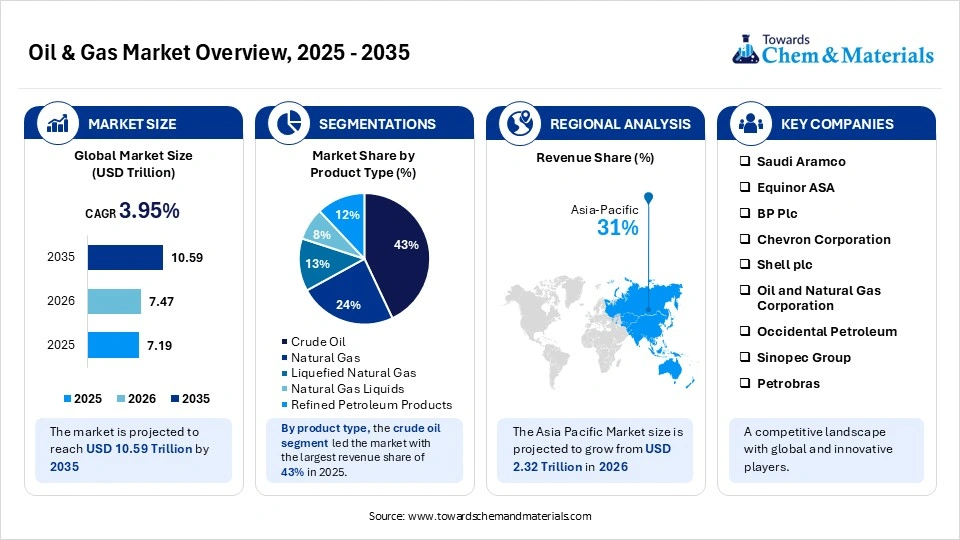

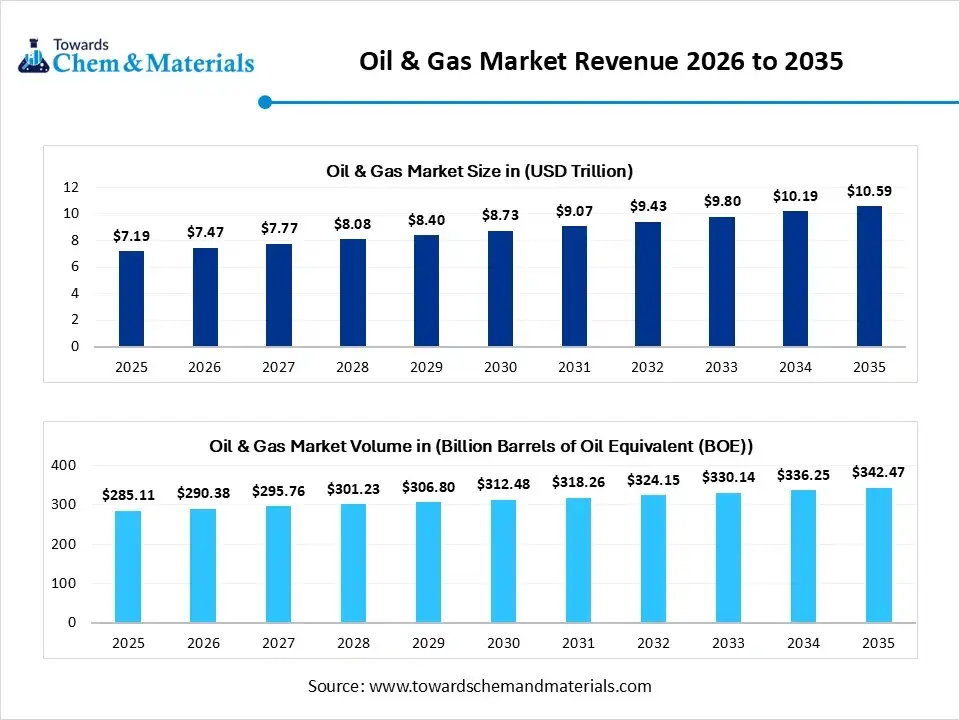

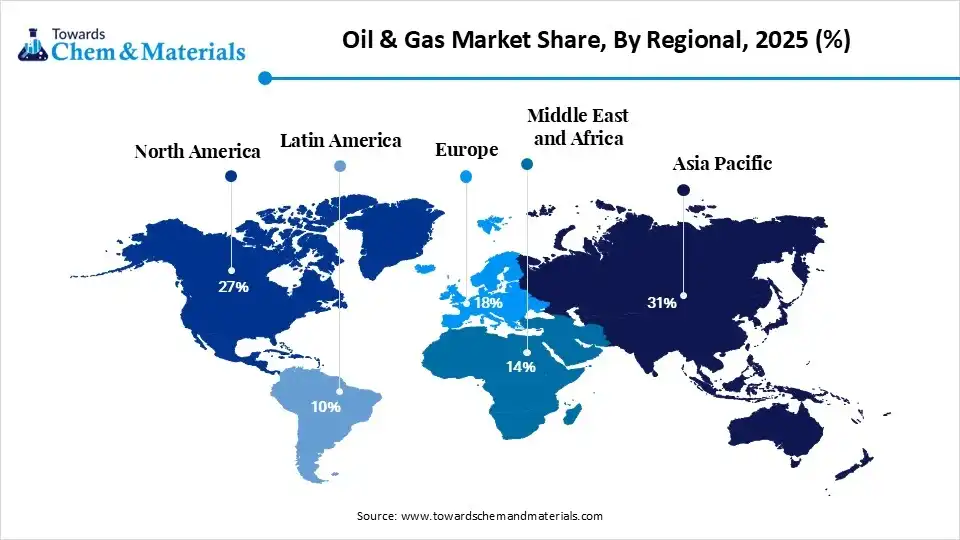

The global oil & gas market size was valued at USD 7.19 trillion in 2025, is estimated to reach USD 7.47 trillion in 2026, and is projected to reach USD 10.59 trillion by 2035, exhibiting a compound annual growth rate (CAGR) of 3.95% over the forecast period from 2026 to 2035. Asia Pacific dominated the oil & gas market with the largest revenue share of 31% in 2025 and is expected to grow at the fastest CAGR of 4.59% during the forecast period. In terms of volume, the oil & gas industry is projected to grow from 285.11 billion barrels of oil equivalent in 2025 to 342.47 billion barrels of oil equivalent by 2035. growing at a CAGR of 1.85% from 2026 to 2035. The market expansion is propelled by decarbonization goals, a focus on supply chain resilience, mega-mergers & corporate alliances, industrial automation, and renewable energy expansion.

The oil & gas market is defined by its complex industrial ecosystem, balancing economic productivity and geopolitical framework. The market is characterized by three major stages includes upstream exploration and manufacturing, midstream transportation infrastructure, and downstream processing operations, that driving the demand for oil & gas in petrochemical and transit fuels. The rising focus on clean technology is boosting the scaling of blue hydrogen manufacturing as an alternative fuel, which is driving the market expansion. The global suppliers transition towards localized sourcing and strategic oilfield contracts for a stable supply chain.

The regulatory compliance for decarbonization and energy transition enables the carbon capture and utilization installations and renewable energy as a green alternative. The strategic collaboration and agreement governed by commodity benchmarking indexes boost the trade dynamics and supply chain resilience. The market focus expansion of liquefaction facilities that enhance the scaling of maritime LNG transit infrastructure to meet social, environmental, and governance standards. The operators preferred institutional financial exclusion through specialized cryogenic transport containers for clean-burning and electricity generation.

The oil & gas sector is deploying field automation and digital operations that offer protection against natural field degradation and diminishing reservoir yields. The commercial integration of subsurface machine learning and a cloud-driven virtualization platform that eliminates unnecessary field downtime. The implementation of autonomous drilling and robotic extraction drives down the extraction cost and improves operational field safety. Additionally, technological innovation is boosting the continuous methane emission monitoring by ensuring legal precision and corporate financial reporting.

Market Highlights

- By region, Asia Pacific dominated the oil & gas market by holding 31% share in 2025 and is expected to grow at the fastest with a CAGR of 5.10% during the forecast period, driven by industrialization and urban consumer demand for hydrocarbon and domestic energy security.

- By region, North America held the 27% market share in 2025 and expects notable growth in the market with 3.70% CAGR during the forecast period due to its shale production and expanding LNG export capacity.

- By value chain, the upstream segment dominated the market with the largest share of 41% in 2025, driven by exploration and production activities.

- By value chain, the midstream segment held 27% market share in 2025 and is expected to grow at the fastest CAGR of 4.3% over the forecast period due to pipeline and storage infrastructure investment with expanding LNG trade.

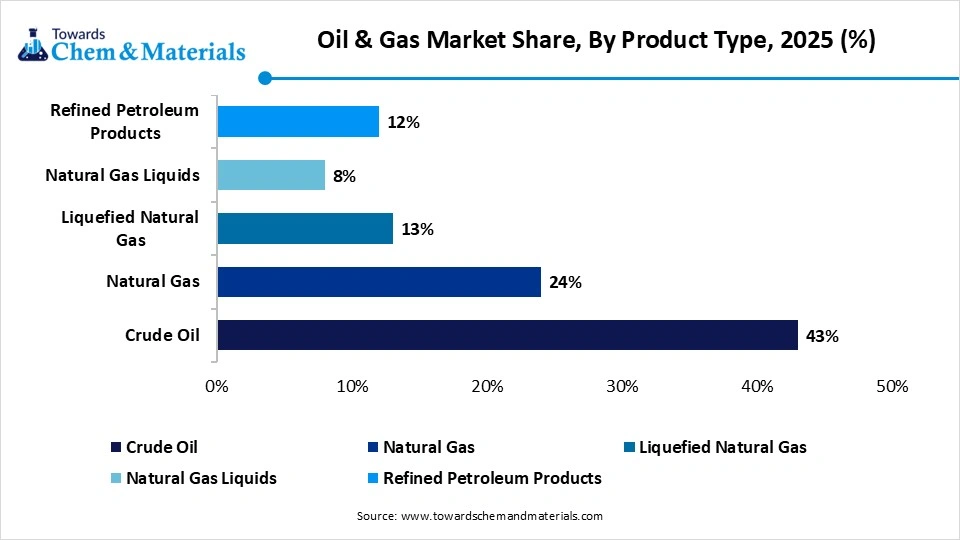

- By product type, the crude oil segment dominated the market with the largest share of 43% in 2025, driven by OPEC production strategies and refining expansion in logistics and petrochemical sectors.

- By product type, the liquefied natural gas segment held 13% market share in 2025 and is expected to grow at the fastest CAGR of 6.7% over the forecast period, driven by the marine fuel transition and energy diversification approach.

- By application, the transportation fuels segment dominated the market with the largest share of 46% in 2025 due to expanding vehicle fleets' demand for gasoline, liquid fuel, and diesel.

- By application, the petrochemicals and specialty products segment held 8% market share in 2025 and is expected to grow at the fastest CAGR of 5.3% over the forecast period due to investment in hydrocarbon feedstock and demand for plastic and synthetic materials.

From Exploration to Distribution: Inside the Oil & Gas Value Chain

At its core, the oil and gas sector is about getting hydrocarbons crude oil and natural gas out of the ground and delivering them to the global market. Because it powers everything from manufacturing to daily transportation, this industry acts as a major anchor for global economies and geopolitics. The entire process is traditionally split into three distinct phases: upstream (finding and extracting the resource), midstream (moving and storing it), and downstream (refining and selling the final products).

Today, the industry is balancing traditional demands with new pressures. While global energy needs and breakthroughs in drilling tech like deepwater exploration and advanced fracturing continue to push production forward, the focus is visibly shifting. Companies are navigating a tight rope between meeting current fuel needs and adapting to strict environmental regulations. This has sparked a massive wave of digital automation on the ground, alongside major investments in LNG, hydrogen, and carbon reduction strategies as the sector maps out its long-term future.

Which Factor Is Driving the Oil & Gas Market?

The global need for energy is spearheading the industry growth in the current period. Moreover, oil & gas are considered the major fuel option in the heavy manufacturing industries or their machinery. Furthermore, even with the release of renewable energy, oil and gas remain crucial due to factors such as reliability and easy transportation in recent years, as per the latest market survey.

Market Trends

- Industrial Shift Towards Decarbonization: The upstream and downstream industry focuses on a carbon capture, utilization, and storage ecosystem through substantial corporate investment to meet low-carbon hydrogen and net-zero commitments.

- Automation in Methane Emission Monitoring: The operators focus on orbital satellite imaging and sensor-driven airborne drones by offering instantaneous detection of greenhouse gas leaks in active pipelines.

Market Report Scope

| Report Attribute | Details |

| Market Size and Volume in 2026 | USD 7.47 Trillion/ 290.38 Billion Barrels of Oil Equivalent |

| Revenue Forecast in 2035 | USD 10.59 Trillion/ 342.47 Billion Barrels of Oil Equivalent |

| Growth Rate | CAGR 3.95% |

| Base Year of Estimation | 2025 |

| Forecast Period | 2025 - 2035 |

| Dominant Region | Asia Pacific |

| Segment Covered | By Value Chain, By Product Type, By Application, By Regions |

| Key Companies Profiled | Saudi Aramco, Equinor ASA, BP Plc, Chevron Corporation, Shell plc, Oil and Natural Gas Corporation, Occidental Petroleum, Sinopec Group, Petrobras, Eni S.p.A, Gazprom, Repsol S.A., Woodside Energy, Rosneft Oil Company, TotalEnergies SE |

Key Technological Shifts and AI in the Oil & Gas Market

Technological integration is revolutionizing oil & gas field engineering into data-driven infrastructure via digital asset optimization & subsurface robotic learning. The cloud-driven network runs real-time monitoring. The predictive digital twin enables geological precision and high-yield hydrocarbon synthesis in well-established basins.

The autonomous drilling rigs align with robotic pipe-handling arrays lowers per-barrel operational cost.

Manufacturers are increasingly integrating orbital satellite imaging with computer intelligence for methane emission monitoring. Artificial Intelligence optimizes the maritime pathway of the specialized LNG ecosystem by enabling refinery yield and quality of oil.

Supply Chain Analysis of the Oil & Gas Market

- Exploration and Manufacturing: The upstream sector utilizes high-resolution three-dimensional seismic surveying, gravity modeling, and magnetics focus on hydrocarbon and fluid extraction from subsurface geological identification, reservoir quality, and supply chain interdependence.

- Key Players: ExxonMobil Corporation, Chevron Corporation, Shell plc., SLB (Schlumberger), and Baker Hughes

- Logistics and Storage: The stage focuses on logistical vascular network, long-distance transit, and high-volume storage of unrefined resources. The LNG transport vessels are monitored by a supervisory control and data acquisition infrastructure.

- Key Players: Kinder Morgan, Inc., Enbridge Inc., Cheniere Energy, Inc., Mitsui O.S.K. Lines, and Enterprise Products Partners L.P.

- Refinery Processing and Marketing: The stage of refining yields through fluid catalytic crackers and chemical reactors. The diversified chemical manufacturing and retail marketing infrastructure to meet strict carbon emission taxes.

- Key Players: TotalEnergies SE, Reliance Industries Limited, Marathon Petroleum Corporation, BASF SE, and Valero Energy Corporation

Regulatory Framework: Oil & Gas Market

| Region | Key Regulations | Regulatory Focus |

| European Union | EU REACH Standards, EU Methane Emissions Regulation, and Carbon Border Adjustment Mechanism | Strict import standards and decarbonization mandates for carbon tracking, detection, and repair of the oil & gas network. The standards focus on legal binding nature of net-zero alignment. |

| North America | Environmental Protection Agency, BLM, Bureau of Safety and Environmental Enforcement, Federal Energy Regulatory Commission. | Focus on safety and regulation for interstate pipeline and LNG export terminal approvals. Strict methane fee penalties and financial-grade ESG disclosure tracking. |

| Middle East and Africa | Organization of the Petroleum Exporting Countries orders, Saudi Ministry of Energy, ADNOC in Aramco | Regulation for preservation of domestic hydrocarbon and state-driven flaring bans of industrial carbon capture and utilization system, and local fuel pricing controls |

| Asia Pacific | Ministry of Petroleum and Natural Gas, Natural Gas Regulatory Board, and Directorate General of Hydrocarbons | Standards of open acreage licensing policies for domestic filling and deepwater gas pricing. The strict safety audits for complex deepwater offshore infrastructure. |

| Latin America | National Agency of Petroleum, ANP in Brazil, National Hydrocarbons Commission | Management for deepwater pre-salt blocks and structuring offshore production contracts surrounding resource nationalism. |

Market Dynamics

Driver

Expanded LNG Infrastructure and Supply Chain Resilience

The global energy transition is driving the oil & gas market growth. The rising focus on implementing the liquefied natural gas value chain. Liquefaction hubs and export facilities are increasingly investing in gas export infrastructure for superior logistics and transit. The surge for supply chain resilience enables the reengineering and fabrication of advanced and high-capacity specialized LNG transport vessels integrated with modern cryogenic containment systems. To replace emission-heavy coal and eliminate single-source supply lines fueling the rapid scaling of flexible transit fuel infrastructure by offering a reliable, stable solution for a modern energy shift to meet carbon-neutrality targets.

Restraints

Falling Reservoir Quality and Asset Geology

The oil & gas market key refiners and manufacturers are focusing on geological limitation which enable the production decline curves. The oilfield requires water-separation technologies and an ultra-deepwater environment for drilling and hydrocarbon products, which drives the technical complexity and operational risks that restrain the market expansion.

Opportunity

Scaling of CCU and Blue Hydrogen

The market demand for decarbonization in logistics and the maritime sector is driving the diversified opportunity for an industrial-scale carbon capture & utilization ecosystem. The cement manufacturing, chemical refining, and steel fabrication sector shift towards new establishments of infrastructure-driven low-carbon revenue streams to create high-margin carbon credits and separate greenhouse gases. Additionally, manufacturers are rapidly scaling blue hydrogen production by integrating advanced carbon capture technologies for heavy industries. The domestic hydrogen hubs utilize blue hydrogen as a clean energy asset to end-user industries.

Segmental Insights

Value Chain Insights

The upstream segment dominated the market with the largest share of 41% in 2025, driven by exploration and production activities that make the upstream key for supply chain resilience and baseline ecosystem. The rising implementation of advanced seismic imaging and geophysical surveys in modern energy security, data centers, and power grids. The offshore and onshore exploration shift towards natural gas extraction by integrating digital oilfield technologies, boosting the production of shale oil, conventional products, and tight gas.

")

The midstream segment held the 27% market share in 2025 and is expected to grow at the fastest CAGR of 4.3% over the forecast period. It represents a key segment of transportation, storage, and processing of raw petroleum and natural gas by implementing smart manufacturing. The transportation includes the pipeline and LNG carriers, and rail transport. The midstream sector comprises initial processing include gas fractionation facilities and dehydration. The oil & gas operators focus on the expansion of LNG liquefaction and high-value NGL through tank farms, storage terminal and underground storage.

The downstream segment held the 32% market share in 2025, serving as a key stage for raw hydrocarbon transformation into high-value industrial and commercial sectors. The downstream segment involves crude oil refining, retail fuel, and bulk distribution and marketing by using advanced petrochemical plants. The modern downstream operators are investing in refinery configuration modernization to manufacture cleaners and low-emission fuels. Wholesale marketing and distribution allow fuel terminals and gas stations to integrate digital optimization by ensuring superior operational efficiency.

Oil & Gas Market Share, By Value Chain, 2025 (%)

| By Value Chain | Revenue Share, 2025 (%) |

| Upstream | 41% |

| Midstream | 27% |

| Downstream | 32% |

Product Type Insights

The crude oil segment dominated the market with the largest share of 43% in 2025, serving as a key liquidity catalyst and petrochemical feedstock for manufacturing and logistic framework. The crude oil offers superior density and ideal chemical compositions like light sweet crude, heavy crude, and sour crude that enhance refining profitability and oil & gas product yield. The shift towards superior maritime logistics efficiency and optimizing feedstock blending makes crude oil key for modern downstream petrochemical manufacturing.

The natural gas segment held the 24% market share in 2025. The rising focus on modern energy transition fuel and low-carbon alternative make natural gas key for petrochemical, fertilizers ad plastics manufacturing. The natural gas offers higher operation resilience and versatility that is processed to remove impurities and isolate valuable natural gas liquids and liquified natural gas. This product acts as a chemical feedstock that is utilized in residential heating, power grids, industrial manufacturing, and to stabilize renewable energy intermittency.

The liquefied natural gas segment held the 13% market share in 2025 and is expected to grow at the fastest CAGR of 6.7% over the forecast period. It is a high-liquidity seaborne commodity asset that transforms super-cooling natural gas into a liquid state to compress its volume by 600 times. The substantial investment in liquefaction facilities for export and domestic regasification terminals for import makes LNG a key for high-growth maritime and baseload energy transition.

The refined petroleum products segment held 12% market share in 2025, driven by its versatility as a chemical feedstock utilized in the transportation sector and industrial manufacturing. The refined petroleum products are produced using the processing of crude oil in refineries through catalytic cracking and fractional distillation. The segment is divided into light distillate, heavy residue, and middle distillate, like diesel, jet fuels, which are accelerating the demand in the petroleum and industrial sectors.

The natural gas liquids segment held 8% market share in 2025, defined by low-cost chemical feedstock required for the manufacturing of plastics, household resins, and synthetic rubbers. The NGL is non-methane hydrocarbons that contain ethane, propane, and butane, which are co-extracted during gas production as a liquidity driver separated at specialized fractionation hubs, which is crucial for upstream extraction and consumer goods production.

Oil & Gas Market Share, By Product Type, 2025 (%)

| By Product Type | Revenue Share, 2025 (%) |

| Crude Oil | 43% |

| Natural Gas | 24% |

| Liquefied Natural Gas | 13% |

| Natural Gas Liquids | 8% |

| Refined Petroleum Products | 12% |

Application Insights

The transportation fuels segment dominated the market with the largest share of 46% in 2025. The oil & gas industry is a mobility driver and key to stable supply chain logistics. The operators focus on advancing refinery configuration to create ultra-low sulfur diesel and sustainable aviation fuel to meet stringent emissions targets, driving the market growth. The transportation application utilized LPG, gasoline, jet fuel, and diesel by integrating with advanced crude oil refineries.

The petrochemicals and specialty products segment held the 8% market share in 2025 and is expected to grow at the fastest CAGR of 5.3% over the forecast period. The rising downstream sector focuses on converting refined chemical feedstock into key industrial components by utilizing chemical crackers in olefins and aromatics production. The shift towards the adoption of specialty products involves industrial solvents, advanced lubricants, asphalt ad specialized waxes for chemical manufacturing, boosting the market expansion. The integration of the refinery-to-chemical process to maximize operational efficiency.

The industrial energy segment held the 21% market share in 2025, acting as a heavy-duty operational catalyst that supplies stable thermal power and reliable baseload electricity, key for mining operations, modern manufacturing, and heavy chemical processing. The industrial energy sector demands petroleum coke, natural gas, and fuel oil for industrial operations to meet carbon-neutral commitments. The industry is implementing combined heat and power systems and automated energy management to maximize industrial productivity.

The power generation segment held 18% market share in 2025, because it converts raw hydrocarbons into flexible electricity that is key for gas-fired power and diesel-based backup infrastructure. The power generation sector is installing advanced combined-cycle gas turbine systems and artificial intelligence data centers. The oil & gas market is key for a higher grid-stabilisation mechanism by balancing renewable energy intermittency & carbon-neutral goals.

Oil & Gas Market Share, By Application, 2025 (%)

| By Application | Revenue Share, 2025 (%) |

| Transportation Fuels | 46% |

| Power Generation | 18% |

| Industrial Energy | 21% |

| Residential and Commercial Heating | 7% |

| Petrochemicals and Specialty Products | 8% |

Regional Insights

How Did the Asia Pacific Dominated the Oil & Gas Market in 2025?

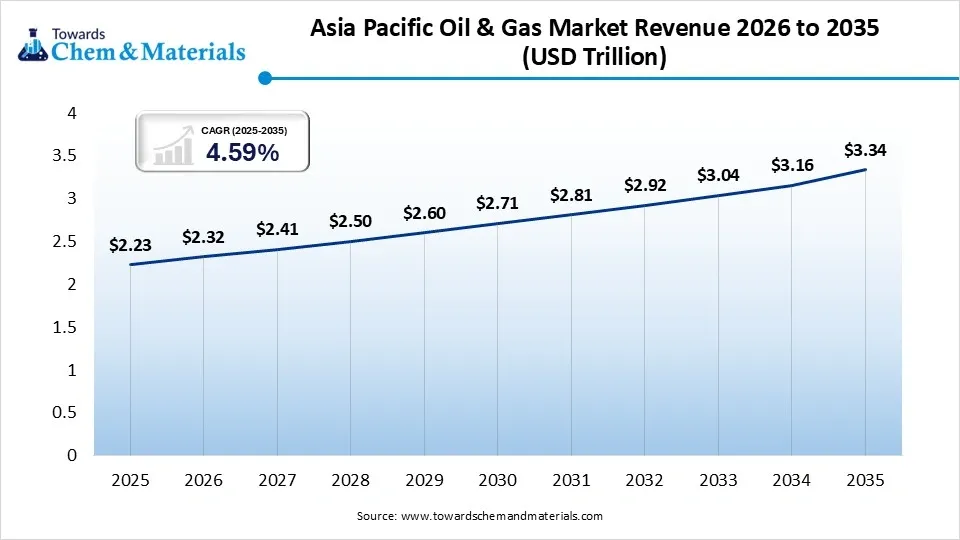

The Asia Pacific oil & gas market size was estimated at USD 2.23 trillion in 2025 and is projected to reach USD 3.34 trillion by 2035, growing at a CAGR of 4.59% from 2026 to 2035.Asia Pacific dominated the market by holding 31% share in 2025 and is expected to grow at the fastest with a CAGR of 5.10% during the forecast period. The regional transformation is driven by industrial oil capacity development and a rising urban population. The domestic focus on deepwater drilling and LNG infrastructure to support the energy transition is accelerating market growth. The Asia Pacific carbon-reduction initiative and clean transition mandates enable rapid scaling of oil production. Additionally, the region integrating digital oilfield technologies strengthen their dominance.

China

- Driven by their transition towards unconventional tight gas and deep shale exploitation to meet stringent industrial emission caps and green hydrogen blending compliance.

- China is focused on expanding underground gas storage capacity in the domestic landscape and industrial power consumption.

India

- Supported by their diversified downstream refining expansion infrastructure and city gas distribution ecosystem, construct domestic export hubs.

- The government support for revenue-sharing contracts and strict biofuel blending mandates is boosting their natural gas demand in the middle-class consumer base.

The North America oil & gas market size was estimated at USD 1.94 trillion in 2025 and is projected to reach USD 2.91 trillion by 2035, growing at a CAGR of 4.14% from 2026 to 2035. North America held the 27% market share in 2025 and is expected to experience notable growth in the market with a 3.70% CAGR during the forecast period, supported by its export-driven hubs that align with domestic fuel requirements. The regional operators utilize automated drilling rigs and advanced hydraulic fracturing infrastructure in the oil & gas sectors. The shift of the Permian basin and gulf coast driving the growth of liquefaction facilities. North America focuses on corporate consolidation, its mega-corporation and increasingly invests in methane emissions monitoring and carbon capture systems.

United States

- Represented by their stringent capital discipline and corporate consolidation that accelerating the development of LNG liquefaction facilities to meet strict pipeline safety

- The global demand for US light sweet crude is driving the integration of highly efficient horizontal drilling techniques to meet methane emission standards and economic public-interest audits.

Canada

- Due to its large-scale LNG export hubs and expanding heavy crude export capacity, supported by stringent carbon pricing mechanisms and real-time tailing pond emission real-time monitoring.

- Canada selects crude by opening a direct pathway to Asia refining infrastructure and the expansion of trans-continental pipelines.

The Europe oil & gas market size was estimated at USD 1.29 trillion in 2025 and is projected to reach USD 1.96 trillion by 2035, growing at a CAGR of 4.27% from 2026 to 2035. Europe held 18% market share in 2025, driven by its stable supply chain and shift towards liquefied natural gas imports in the maritime ecosystem. The regional players are investing in floating regasification terminals and building interconnected hydrogen-ready pipeline networks. Europe's climate-neutral mandates are reinforcing oil operators to implement advanced CCU and real-time methane monitoring. The regulatory compliance focuses on industrial energy security that driving Europe's leadership in green transition.

Norway

- Due to its zero-tolerance regulation on routine flaring and the highest carbon taxes enable corporate investment in field-electrification projects.

- Norway maintains its leadership in the transformation of depleted offshore reservoirs into a commercial carbon capture and storage hub promoted by its strong continental export pricing.

United Kingdom

- The UK is shifting towards decommissioning services and offshore wind integration to meet net-zero compliance pathways.

- The demand for domestic heating & industrial electricity assists the phase-out of fossil fuel infrastructure by imposing volatile energy profits taxes.

The Latin America oil & gas market size was estimated at USD 0.72 trillion in 2025 and is projected to reach USD 1.11 trillion by 2035, growing at a CAGR of 4.42% from 2026 to 2035. Latin America held 10% market share in 2025, accelerated by its economic realignment and geological activities driving the innovation in deepwater extraction. Domestic operators employ automated subsea robotics and real-time reservoir through foreign direct investment. Latin America adopts FPSO vessels and ultra-deep pre-salt oil in regional facilities by integrating with low-carbon extraction technologies.

")

Brazil

- Driven by their surge in ultra-deepwater crude manufacturing and non-OPEC global oil supply by monitoring associated gas flaring limits and strict deepwater environmental licensing protocols.

- Brazil dominated in its profitable reserves within sub-salt layers and the implementation of standardized high-volume FPSO vessels.

The Middle East and Africa oil & gas market size was estimated at USD 1.01 trillion in 2025 and is projected to reach USD 1.54 trillion by 2035, growing at a CAGR of 4.31% from 2026 to 2035. The Middle East & Africa held 14% market share in 2025. The domestic development is fostered by their cost-effective upstream production.MEA is maintaining its leadership in monumental natural gas innovation and deploying remote subsea robotics. The regional zero-routine flaring initiatives and carbon-mitigation mandates are driving the rapid expansion of spare production capacity and AI-driven reservoir management.

Oil & Gas Market Share, By Regional, 2025 (%)

| Regional | Revenue Share, 2025 (%) |

| North America | 27% |

| Europe | 18% |

| Asia-Pacific | 31% |

| Latin America | 10% |

| Middle East & Africa | 14% |

Saudi Arabia

- The domestic advancement is boosted by their integrated petrochemical mega-complexes and expansion in sustainable crude capacity by maintaining cost-effectiveness in upstream extraction.

- Saudi Arabia's substantial investment in large-scale circular carbon economy technologies and the Vision 2030 framework to meet domestic clean hydrogen compliance.

Recent Developments

- In March 2026, ST LNG selected Baker Hughes as the technology provider for its offshore LNG export terminal project in Texas. The agreement focuses on supplying gas compression and power generation technology near Matagorda.(Source: www.marinelink.com)

- In December 2025, ExxonMobil, Aramco, and Samref signed a Venture Framework Agreement to evaluate a significant upgradation of the Samref refinery and the construction of a new petrochemical complex. The key focus is to reduce emissions and improve the refinery's energy efficiency.(Source: www.aramco.com)

- In October 2025, Honeywell, Aramco, and KAUST signed a joint agreement to develop technology for the advancement of crude-to-chemicals (CTC) technology. This partnership focuses on scaling up the CTC process and reducing operational cost that helping to advance economic diversification.(Source: www.honeywell.com)

Top Companies in the Oil & Gas Market

- Saudi Aramco

- Equinor ASA

- BP Plc

- Chevron Corporation

- Shell plc

- Oil and Natural Gas Corporation

- Occidental Petroleum

- Sinopec Group

- Petrobras

- Eni S.p.A

- Gazprom

- Repsol S.A.

- Woodside Energy

- Rosneft Oil Company

- TotalEnergies SE

Segment Covered

By Value Chain

- Upstream

- Exploration

- Seismic Surveys

- Offshore Exploration

- Onshore Exploration

- Exploration

- Production

- Conventional Production

- Unconventional Production

- Shale Oil

- Tight Gas

- Midstream

- Transportation

- Pipelines

- LNG Carriers

- Rail Transport

- Storage

- Tank Farms

- Underground Storage

- Processing

- Gas Processing Plants

- Fractionation Facilities

- Transportation

- Downstream

- Refining

- Fuels Refining

- Petrochemical Refining

- Distribution

- Retail Fuel Stations

- Bulk Distribution

- Marketing

- Industrial Sales

- Commercial Sales

- Refining

By Product Type

- Crude Oil

- Light Crude

- Heavy Crude

- Sour Crude

- Natural Gas

- Conventional Gas

- Shale Gas

- Coal Bed Methane

- Liquefied Natural Gas

- Export LNG

- Bunkering LNG

- Small-scale LNG

- Natural Gas Liquids

- Ethane

- Propane

- Butane

- Refined Petroleum Products

- Gasoline

- Diesel

- Jet Fuel

- Lubricants

By Application

- Transportation Fuels

- Road Transportation

- Aviation

- Marine Transport

- Power Generation

- Gas-fired Power Plants

- Diesel-based Backup Systems

- Industrial Energy

- Manufacturing

- Mining

- Heavy Industries

- Residential and Commercial Heating

- Space Heating

- Water Heating

- Petrochemicals and Specialty Products

- Olefins Production

- Aromatics Production

- Specialty Chemicals

By Region

- North America

- U.S.

- Mexico

- Canada

- Europe

- Germany

- UK

- France

- Italy

- Asia Pacific

- China

- India

- Japan

- South Korea

- Central & South America

- Brazil

- Argentina

- Middle East & Africa

- Saudi Arabia

- UAE

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

FAQ's

Select User License to Buy

Figures (7)