Content

What is Mechanical & Chemical Recycling of Polyethylene Market Size and Share?

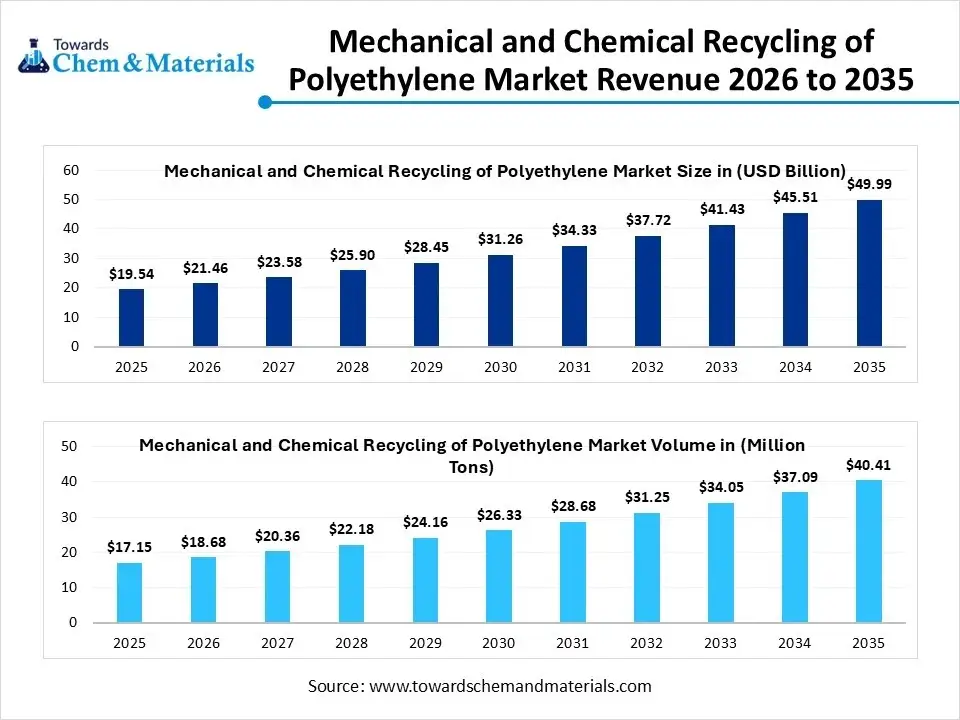

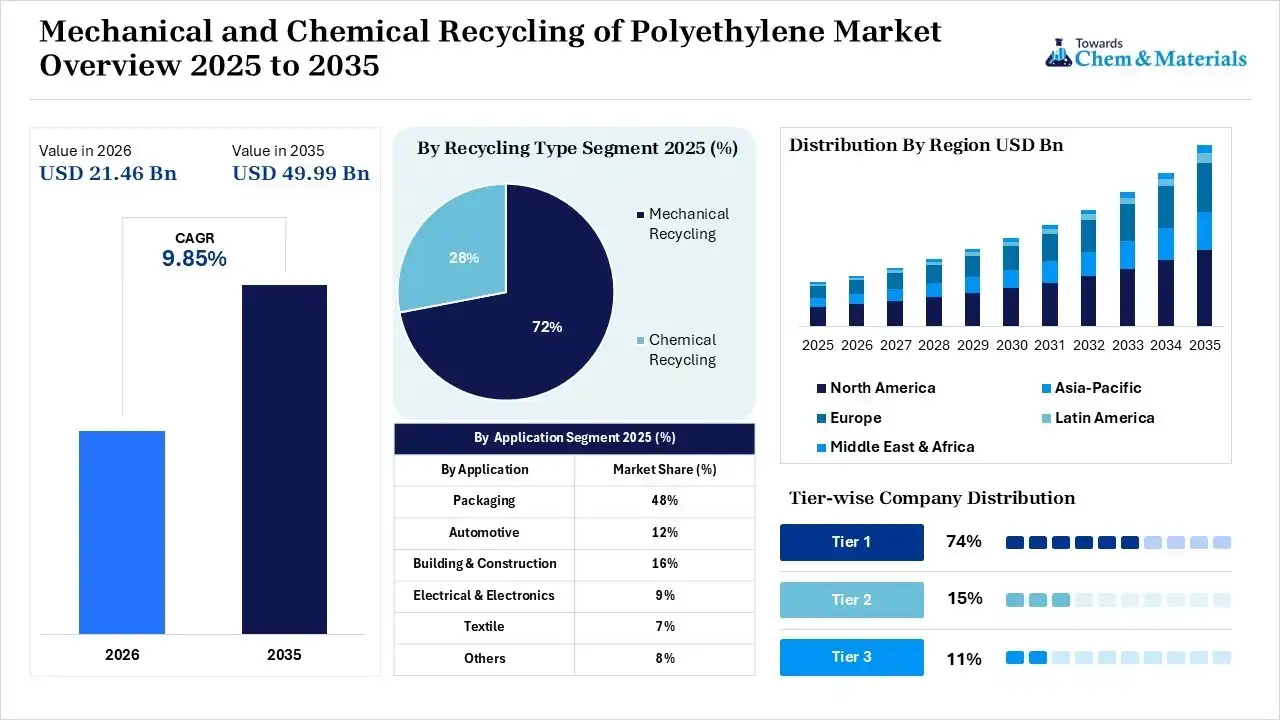

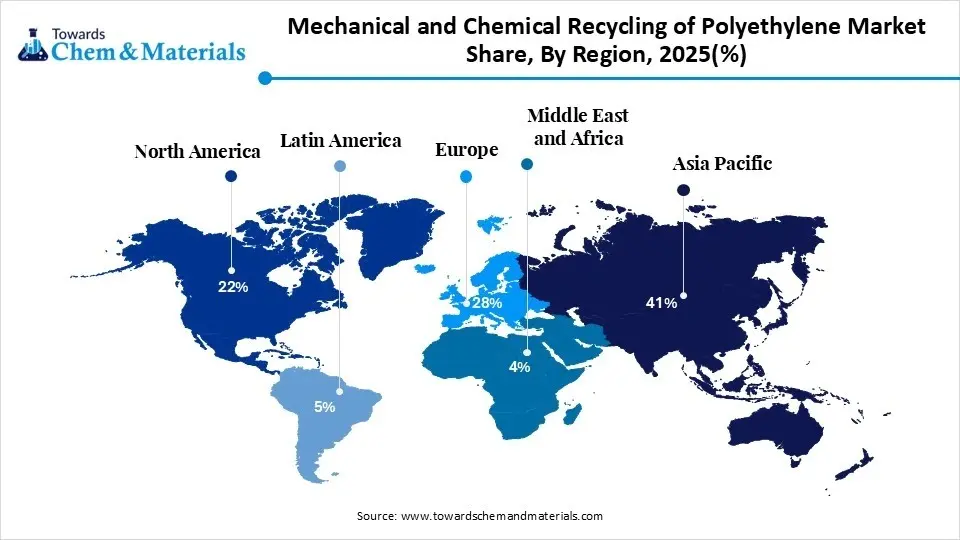

The global mechanical & chemical recycling of polyethylene market market size was valued at USD 19.54 billion in 2025, is estimated to reach USD 21.46 billion in 2026, and is projected to reach USD 49.99 billion by 2035, exhibiting a compound annual growth rate (CAGR) of 9.85% over the forecast period from 2026 to 2035. Asia Pacific dominated the mechanical & chemical recycling of the polyethylene market with the largest revenue share of 41% in 2025 and is expected to grow at the fastest CAGR of 9.99% during the forecast period.

The surge in corporate sustainability commitments is the key factor driving market growth. Also, ongoing enhancements in sorting and purification technologies coupled with the rapid innovations in automated optical sorting techniques can fuel market growth further.

Market Highlights

- By region, Asia Pacific dominated the market with the largest share of 41% in 2025. The dominance of the region can be credited to the ongoing urbanization and extensive corporate sustainability commitments.

- By region, Europe held a market share of 28% in 2025 and is expected to grow at the fastest CAGR of 10.20% over the forecast period. The growth of the region can be linked to rapid investments in innovative recycling infrastructure.

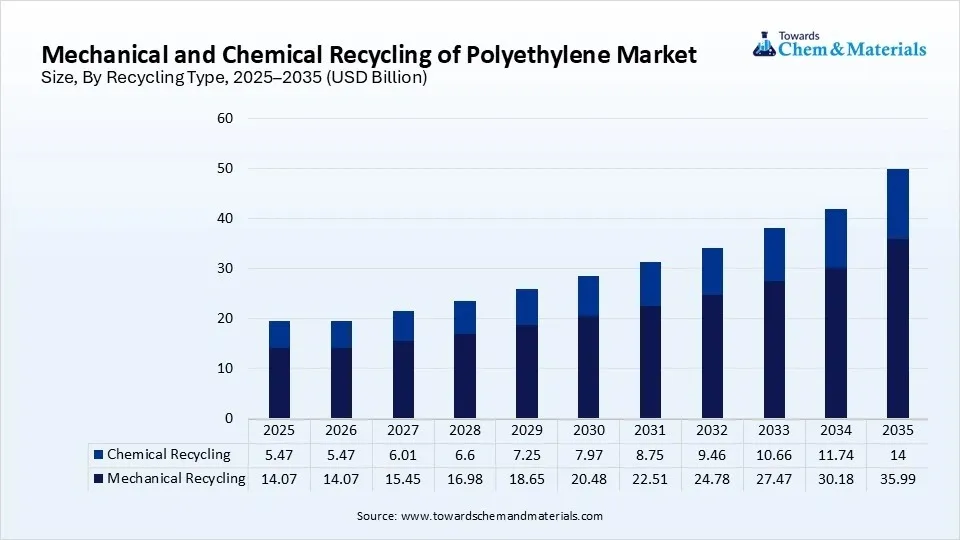

- By technology, the mechanical recycling segment dominated the market with a largest share of 72.0% in 2025. This dominance is primarily driven by its established infrastructure and cost-effective processing capabilities for standard plastic waste streams.

- By technology, the chemical recycling segment held a market share of 28% in 2025 and is expected to grow at the fastest CAGR of 12.80% over the forecast period. This rapid growth is fueled by increasing demands for high-purity recycled resins.

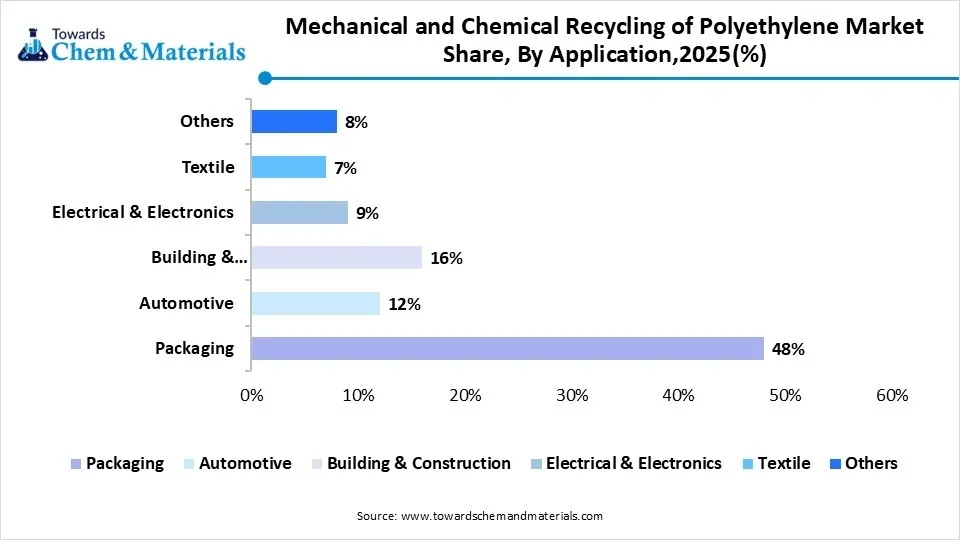

- By application, the packaging segment dominated the market with the largest share of 48.0% in 2025. The dominance of the segment can be credited to stringent global regulations on single-use plastics.

- By application, the textile segment held a market share of 7% in 2025 and is expected to grow at the fastest CAGR of 10.3% over the forecast period. The growth of the segment can be attributed to the rising fashion industry demand for circular materials.

According to Towards Chemicals and Materials Analytics and Consulting, the global mechanical & chemical recycling of polyethylene market volume was valued at 17.15 million tons in 2025 and is expected to surpass around 40.41 million metric tons by 2035, accelerating a compound annual growth rate (CAGR) of 3.85% over the forecast period from 2026 to 2035.

Growing Demand for Recycled Plastics Supports Market Growth

The rising need for recycled plastics across different sectors, with a surge in environmental concerns, presents lucrative opportunities in the market. This transition towards sustainable practices facilitates the adoption of various alternatives to virgin plastics.

- In February 2026, NOVA Chemicals Corporation advanced its circular economy initiatives through the commercialization of SYNDIGO rPE-IN3 and SYNDIGO rPE-IN4. These new grades expand the companys SYNDIGO portfolio, introducing resins manufactured entirely from 100% post-consumer recycled (PCR) films. The products are created for general-purpose, non-food-grade applications across North America.(Source: www.indianchemicalnews.com)

Recycled plastics offer a cost-efficient and sustainable solution, fueling their adoption in different sectors.

Market Trends

- The sudden shift toward monomaterial packaging designs, particularly in the flexible packaging segment, is spearheading industry growth in the current period. Moreover, brands and converters are increasingly adopting single-polymer solutions to simplify recycling processes and reduce contamination in waste streams. This change supports both mechanical and chemical recycling pathways by improving quality and processing efficiency. The trend is particularly strong in FMCG and e-commerce packaging, where demand for recyclable materials is high.

- Advanced sorting systems using AI, near-infrared (NIR) spectroscopy, and robotics are driving the mechanical & chemical recycling of polyethylene market growth while reshaping how polyethylene waste is identified and separated in the current period. Technologies enable higher purity rates and better segregation of high- and low-density polyethylene streams, which directly improves recycling efficiency. This trend is enabling recyclers to reduce contamination and increase output quality, aligning with brand demand for high-grade recycled content. As adoption grows, operational costs are gradually declining, making high-tech sorting a viable investment in the future, as per observation.

- Decentralized recycling, where small- to medium-scale facilities process polyethylene waste locally, is gaining traction in the current period. Also, this model reduces transportation emissions, creates localized supply chains, and strengthens feedstock access in some of the regions. Moreover, these setups often focus on mechanical recycling and serve localized industries such as agriculture or regional packaging.

- Chemical recycling technologies such as pyrolysis and solvolysis have gained heavy attention in recent years. These methods enable the breakdown of complex and contaminated plastics into virgin-equivalent polymers or fuels. With growing support from petrochemical firms and packaging giants, pilot facilities are now transitioning into commercial operations.

Market Scope

| Report Attributes | Details |

| Market Size in 2026 | USD 21.46 Billion/ 18.68 Million Tons |

| Expected size by 2035 | USD 49.99 Billion/ 40.41 Million Tons |

| Growth Rate from 2025 to 2035 | CAGR 9.85% |

| Base Year of Estimation | 2025 |

| Forecast Period | 2025 -2035 |

| Segment Covered | By Recycling Type, By Application, By Region |

| Key Companies Profiled | KW Plastics, Veolia, Biffa, Plastipak, MBA Polymers, Loop Industries, Brightmark, Plastic Energy, Eastman Chemical, Agilyx, Dow Inc. |

Supply Chain Analysis of the Mechanical & Chemical Recycling of Polyethylene Market

Production & Processing

- It includes the methods used to convert plastic waste into secondary raw materials. It also dictates the processing yields, conversion phase, and the final quality of the recycled resin. This method has high operational efficiency, serving as a primary revenue generator, especially as localized processing capacity scales across regions like Southeast Asia.

- BASF SE: A major player in chemical recycling; their ChemCycling process converts mixed plastic waste into pyrolysis oil used for new plastics.

- Other Key Players: Banyan Nation, Dalmia Polypro

Quality Testing and Certification

- It ensures that recycled polyethylene matches virgin-grade specifications through rigorous mechanical and chemical processing. These validation procedures verify physical performance, chemical purity, and the exact percentage of Post-Consumer Recycled (PCR) content. These protocols are crucial for brand owners to achieve regional sustainability targets and maintain stringent regulatory compliance.

- SABIC: A leader in advanced recycling, utilizing mass-balance-certified polymers that maintain the same performance properties as traditional fossil-based polyethylene.

- Other Key Players: Banyan Nation, Intertek

Distribution to Industrial Users

- It refers to the supply chain tier where processed recycled resins (rPE) are delivered to manufacturers. These market users, such as construction, automotive, and consumer goods companies, used recycled material to make new products and packaging. The distribution network connects major recycling processers directly to end-product manufacturers.

- Indorama Ventures: A global leader specializing in closed-loop recycling and providing raw resin pellets for packaging applications.

- Other Key Players: Plastic Energy, Agilyx ASA.

Market Opportunity

Strategic Integration and Material Advancements Reshape the Recycled Polyethylene Industry

Integration of recycled polyethylene into high-performance applications such as automotive components, industrial containers, and durable consumer goods is expected to create significant opportunities for mechanical & chemical recycling of polyethylene market in the coming years. Advances in purification and blending technologies have improved the consistency and mechanical strength of recycled material, making it suitable for demanding environments.

Vertical integration presents a strategic opportunity for manufacturers to control quality, cost, and supply continuity in recycled polyethylene in the future as per industry observation. By investing in or acquiring sorting, washing, and pelletizing operations, companies can ensure a steady supply of raw material while optimizing downstream processing, which can create significant growth opportunities for the market.

Market Challenge

Quality Gaps in Input Materials Undermine Recycled Polyethylene Output Standards

The inconsistency of feedstock quality and availability is expected to hamper the mechanical & chemical recycling of polyethylene market potential in the coming years. For mechanical recyclers, inconsistent input quality can result in inferior end-products, affecting customer satisfaction. For chemical recyclers, unpredictable volumes of suitable waste challenge the economics of scaling. This lack of feedstock is forcing recyclers to invest more in sorting and preprocessing, raising costs and reducing margins.

Segmental Insights

Recycling Type Insights

The mechanical recycling segment held the largest share of the mechanical & chemical recycling of polyethylene market in 2025, akin to its established infrastructure, lower operational costs, and simpler processing methods. Moreover, industries prefer this method for post-consumer packaging waste, as it retains polymer properties while reducing environmental impact. The process is energy-efficient and cost-effective, supporting economic initiatives without significant technological investments, which is driving the segment growth in the current period. Also, it remains the preferred choice for rigid and flexible polyethylene applications where purity and performance are less stringent, particularly in packaging and agricultural films.

") The chemical recycling segment is seen to grow at a notable rate during the predicted timeframe due to its addressing key limitations of mechanical methods, specifically with contaminated, multi-layered, or degraded polyethylene waste. It breaks plastics down into monomers or fuels, enabling the production of virgin-quality materials. As regulatory initiatives push for higher recycling rates, chemical recycling offers an ideal solution for hard-to-recycle plastics in the future. Investments in depolymerization and pyrolysis technologies are growing, driven by demand for sustainability in high-performance applications like food-grade packaging, which is expected to contribute to segment growth in the future.

The chemical recycling segment is seen to grow at a notable rate during the predicted timeframe due to its addressing key limitations of mechanical methods, specifically with contaminated, multi-layered, or degraded polyethylene waste. It breaks plastics down into monomers or fuels, enabling the production of virgin-quality materials. As regulatory initiatives push for higher recycling rates, chemical recycling offers an ideal solution for hard-to-recycle plastics in the future. Investments in depolymerization and pyrolysis technologies are growing, driven by demand for sustainability in high-performance applications like food-grade packaging, which is expected to contribute to segment growth in the future.

Mechanical & Chemical Recycling of Polyethylene Market Share,By Recycling Type, 2025(%)

| By Recycling Type | Market Share (%) |

| Mechanical Recycling | 72% |

| Chemical Recycling | 28% |

Application Insights

The packaging segment dominated the mechanical & chemical recycling of polyethylene market with the largest share in 2025, akin to its massive consumption of polyethylene in both flexible and rigid formats in the current period. Moreover, consumer goods, food, and e-commerce sectors drive this demand, generating large volumes of recyclable waste. Mechanical recycling technologies allow the processing of packaging waste, making collection and processing economically viable. Regulatory initiatives and brand commitments toward sustainable packaging further incentivize recycling in this segment. As a result, packaging remains a prominent driver for recycled polyethylene use, offering consistent end-use demand.

") The automotive segment is expected to experience notable mechanical & chemical recycling of polyethylene market growth in the future, owing to its sudden shift toward lightweighting and sustainability. As electric vehicle adoption rises, automakers are increasingly using high-performance recycled plastics for interior and other components. Chemical recycling also enables the production of high-purity resins with mechanical strength and thermal stability suitable for automotive standards. Moreover, rising governmental regulatory pressures on vehicle recyclability and carbon footprint reduction can accelerate material innovation in the future.

The automotive segment is expected to experience notable mechanical & chemical recycling of polyethylene market growth in the future, owing to its sudden shift toward lightweighting and sustainability. As electric vehicle adoption rises, automakers are increasingly using high-performance recycled plastics for interior and other components. Chemical recycling also enables the production of high-purity resins with mechanical strength and thermal stability suitable for automotive standards. Moreover, rising governmental regulatory pressures on vehicle recyclability and carbon footprint reduction can accelerate material innovation in the future.

Mechanical & Chemical Recycling of Polyethylene Market Share, By Application,2025(%)

| By Application | Market Share (%) |

| Packaging | 48% |

| Automotive | 12% |

| Building & Construction | 16% |

| Electrical & Electronics | 9% |

| Textile | 7% |

| Others | 8% |

Regional Analysis

How Did Asia Pacific dominate the Mechanical & Chemical Recycling of Polyethylene Market in 2025?

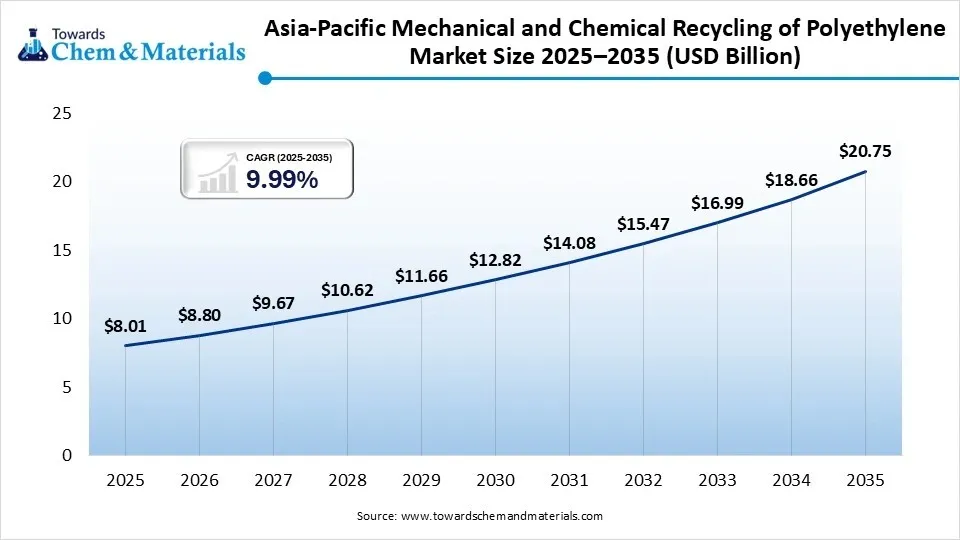

The Asia Pacific mechanical and chemical recycling of polyethylene market size was estimated at USD 8.01 billion in 2025 and is projected to reach USD 20.75 billion by 2035, growing at a CAGR of 9.99% from 2026 to 2035.Asia Pacific dominated the market with the largest share of 41% in 2025. The dominance of the region can be credited to the ongoing urbanization and extensive corporate sustainability commitments. Furthermore, governments and regional bodies in the region are imposing Extended Producer Responsibility (EPR) regulations and legal mandates regarding minimum recycled content.

")

China

- The Chinese government enforces stringent rules on plastic waste disposal. The "National Sword" policy banned the import of foreign plastic waste.

- The ongoing push to achieve carbon neutrality needs industries to decrease their environmental impact, which favors both chemical and mechanical recycling over dumping waste.

India

- India is enforcing stringent guidelines that need brands to take responsibility for the plastic waste they create.

- This is called Extended Producer Responsibility (EPR).

- The government is updating rules to require minimum levels of recycled plastic in new products, boosting the demand for both mechanical and chemical processes.

Europe held the market share of 28% in 2025 and was expected to grow at the fastest CAGR of 10.20% over the forecast period. The growth of the region can be linked to rapid investments in innovative recycling infrastructure and an increase in consumer demand for sustainable packaging. Also, major food, beverage, and consumer packaged goods enterprises are actively re-engineering their product portfolios to incorporate elevated volumes of recycled polyethylene.

Germany

- The country has a great "dual bin" system and a deposit-return setup for bottles and containers. This offers clean trash (feedstock) for recycling.

- Major German chemical and material companies are investing heavily in innovative technologies to meet climate-neutral goals by 2045.

France

- The EU Circular Economy Action Plan impels countries to meet high recycling targets and ban certain types of landfill waste.

- Major local waste companies (like Veolia and Suez SA) are working directly with big brands (like Nestle and Mars) to build better recycling factories.

North America held a market share of 22% in 2025. The growth of the region can be attributed to the increasing capital investments in chemical processing and ambitious corporate sustainability initiatives by consumer brands. In addition, major petrochemical market players are heavily investing in cutting-edge recycling capabilities, leading to market growth soon.

United States

- State policies mandating higher recycled content in packaging and single-use plastic bags are impelling manufacturers to secure sustainable feedstocks.

- Major market players are committing to stringent ESG targets, fueling consistent, long-term demand for recycled PE.

Canada

- Major market players and packaging converters are making public pledges to raise the volume of recycled content in their products.

- Partnerships between municipal waste authorities and global chemical market players have facilitated multi-million-dollar pilots and commercial-scale advanced recycling plants across the globe.

Latin America held a market share of 5% in 2025. The growth of the region can be driven by increasing plastic waste and corporate goals for sustainable packaging. The region generates an escalating volume of polyethylene (PE) waste, largely derived from packaging and consumer commodities. Hence, recycling initiatives play a critical role in mitigating this accumulation and alleviating the burden on municipal landfills.

")

Brazil

- Brazil has a well-established and mature informal waste collection sector. This offers a steady, cost-effective stream of waste material used as basic raw feed by recycling facilities.

- Major automakers, consumer brands, and packaging companies in the country are setting voluntary goals to include post-consumer recycled (PCR) content in their products.

Argentina

- Companies are now facing stricter targets for reducing pollution. This forces industries to buy recycled polyethylene rather than always using brand new plastic.

- The major companies now demand large amounts of recycled polyethylene for their boxes and wrappers. This high demand boosts overall market value.

The Middle East & Africa held a market share of 4% in 2025. The growth of the region can be attributed to the increasing sustainability mandates, along with the heavy investments by a major global circular plastics hub. Furthermore, Middle Eastern nations, including the UAE and Saudi Arabia, are making substantial investments in recycling infrastructure. This strategic effort aims to build a circular economy and diversify their national revenues beyond traditional crude oil exports.

Saudi Arabia

- Chemical recycling changes complex plastics into basic chemicals to be reused. This process is expanding quickly because it can handle dirty, mixed, or hard-to-recycle PE plastics.

- Major petrochemical and waste management companies in the region are partnering to fund advanced recycling technologies.

UAE

- The UAE government aims to divert most of all waste away from landfills, encouraging heavy investments in recycling infrastructure.

- Key local vendors such as the BEEAH Group are scaling their capabilities, supported by partnerships between petrochemical firms and recycling tech providers.

Recent Developments

- In March 2025, Agilyx and Carlos Monreal created a partnership for the development of the Chemical recycling feedstock called Plastyx. Moreover, the main focus of Plastyx is to secure plastic waste of 200,000 tons by the end of 2025, as per the report published by the company. (Source- chemanalyst)

- In January 2025, PolyCycl introduced its latest patented technology for plastic recycling in India. According to the report published by the company, this technology is secured by multiple international patents. (Source: thehindu )

- In January 2026, the European Commission introduced a novel suite of circular economy pilot initiatives, primarily designed to reinforce the European plastics recycling sector against escalating economic and competitive challenges.(Source: www.letsrecycle.com)

Top Companies List

- KW Plastics

- Veolia

- Biffa

- Plastipak

- MBA Polymers

- Loop Industries

- Brightmark

- Plastic Energy

- Eastman Chemical

- Agilyx

- Dow Inc.

Segment Covered in the Report

By Recycling Type

- Mechanical Recycling

- Primary Recycling (Closed-Loop)

- Secondary Recycling (Post-Consumer & Post-Industrial)

- HDPE Recycling

- LDPE Recycling

- LLDPE Recycling

- Chemical Recycling

- Pyrolysis

- Gasification

- Solvolysis

- Catalytic Depolymerization

By Application

- Packaging

- Flexible Packaging

- Rigid Packaging

- Industrial Packaging

- Automotive

- Interior Components

- Exterior Components

- Under-the-Hood Components

- Building & Construction

- Pipes & Fittings

- Insulation Materials

- Geomembranes & Sheets

- Electrical & Electronics

- Cable Insulation

- Electronic Casings

- Consumer Electronics Components

- Textile

- Fibers & Yarns

- Nonwoven Fabrics

- Industrial Textiles

- Others

- Agriculture

- Consumer Goods

- Household Products

By Region

- North America

- U.S.

- Canada

- Mexico

- Europe

- UK

- Germany

- France

- Italy

- Spain

- Sweden

- Denmark

- Norway

- Asia Pacific

- Japan

- China

- India

- Australia

- South Korea

- Thailand

- Latin America

- Brazil

- Argentina

- The Middle East and Africa

- South Africa

- Saudi Arabia

- UAE

- Kuwait

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

Tags

Select User License to Buy

Figures (6)