Content

Isocyanates Market Size and Forecast 2026 - 2035

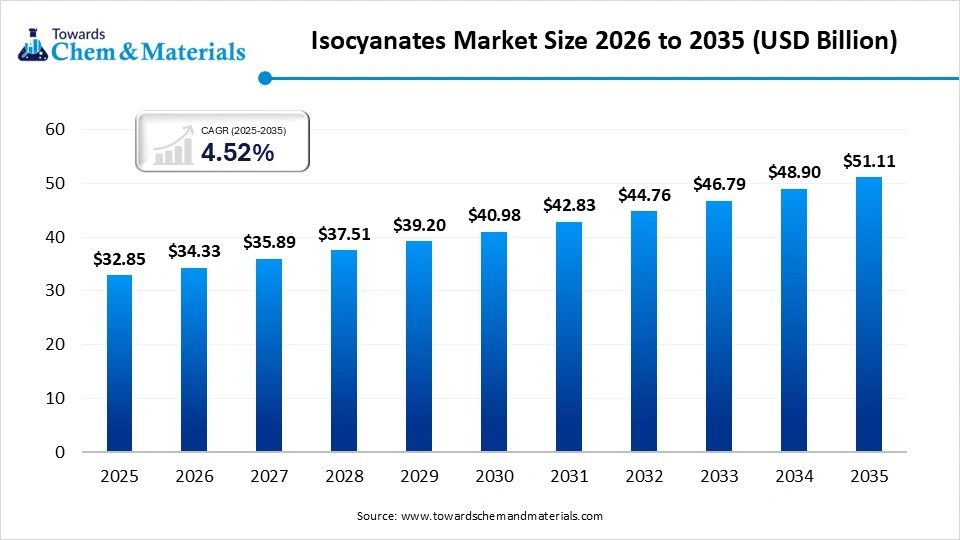

The global isocyanates market size was estimated at USD 32.85 billion in 2025 and is expected to increase from USD 34.33 billion in 2026 to USD 51.11 billion by 2035, growing at a CAGR of 4.52% from 2026 to 2035. North America dominated the isocyanates market with the largest revenue share of 49.00% in 2025.The growth of the market is driven by the surging demand for polyurethane-based products, including rigid and flexible foams, coatings, and adhesives in the construction, automotive, and furniture industries")

Market Highlights

- North America dominated the market share 49.00% in 2025. There’s a notable shift towards sustainable, bio-based products

- By region, Europe is expected to have the fastest growth in the market in the forecast period between 2026 and 2035. The construction industry's growth, especially in Germany, is fueling demand for isocyanate-based rigid PU foam for insulation.

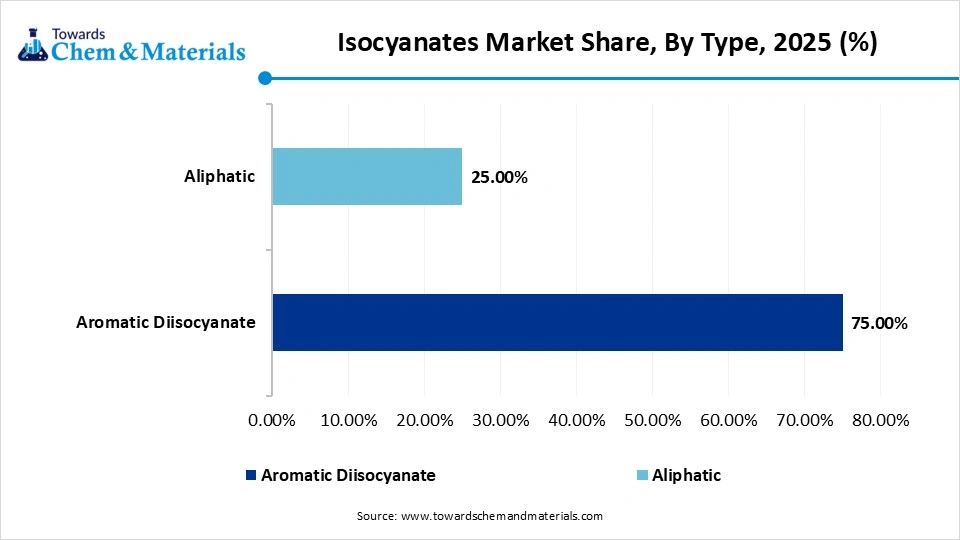

- By type, the aromatic diisocyanate segment dominated the market share 75.00% in 2025. Aromatic isocyanates are critical in producing lightweight polyurethane foams and composites.

- By type, the aliphatic segment is projected to grow at the fastest CAGR between 2026 and 2035. The segment is driven by increasing demand for automotive clearcoats and high-performance industrial coatings.

- By application, the rigid foam segment dominated the market share 41.00% in 2025. The expansion of cold-storage warehouses and temperature-sensitive shipping significantly increased the demand.

- By application, the flexible foam segment is projected to grow at the fastest CAGR between 2026 and 2035. The growing demand for cushioning in bedding, furniture, and automotive sector.

- By end use, the building and construction segment dominated the market share 38.00% in 2025. An increasing focus on energy efficiency led to widespread renovations and a surge in cold-storage infrastructure

- By end use, the furniture segment is projected to grow at the fastest CAGR between 2026 and 2035. The rapid growth of the online furniture market is fueling the demand.

What Is the Significance of the Isocyanates Market?

The isocyanates market plays a key role in the global polyurethane (PU) industry, vital for manufacturing flexible and rigid foams, coatings, adhesives, and sealants. Its importance stems from delivering essential insulation solutions for construction and lightweighting materials for the automotive industries, fueled by rapid urbanization and energy efficiency demands. The rising need for lightweight vehicles to enhance fuel efficiency further drives the demand for PU components.

Key Technological Shifts In The Isocyanates Market:

Major technological changes in the market are mainly motivated by sustainability, environmental safety, and high-performance needs in the automotive and construction industries. The industry is shifting toward low-emission products, non-phosgene manufacturing methods, and bio-based options. It is also abandoning traditional phosgenation, a hazardous process, in favor of greener synthesis techniques like using dimethyl carbonate or direct carboxylation to produce MDI and TDI.

Trade Analysis Of Isocyanates Market: Import & Export Statistics

According to Global Export Data, the world exported 20 Aliphatic Isocyanate shipments between April 2024 and March 2025 (TTM) through 6 verified exporters and 7 buyers, marking a 67% YoY change.

India, Russia, and Vietnam lead as the top Aliphatic Isocyanate importers, while the United States with 35 shipments, China with 10 shipments and Japan with 3 shipments rank as the largest global Aliphatic Isocyanate exporters.

Top-performing Global Aliphatic Isocyanate Exporters by volume:

- Allnex USA Inc: 4 shipments (22%)

- PPG Industries: 4 shipments (22%)

- CHEMICAL MARKETING CONCEPTS EUROPE: 3 shipments (17%)

Market Growth Trends:

- Circular Economy Initiatives: Rising focus on chemical recycling, such as glycolysis and aminolysis, to convert polyurethane waste back into usable raw materials.

- Regulatory Pressures: Strict environmental regulations on volatile organic compound (VOC) emissions are forcing a shift towards safer chemical handling and improved, low-emission formulations.

- Sustainability & Green Chemistry: Growing adoption of bio-based isocyanates and phosgene-free production methods to address ecological concerns, including developments like bio-based alternatives derived from castor oil.

Report Scope

| Report Attribute | Details |

| Market Size in 2026 | USD 34.33 Billion |

| Revenue Forecast in 2035 | USD 51.11 Billion |

| Growth Rate | CAGR 4.52% |

| Forecast Period | 2026 - 2035 |

| Base Year | 2025 |

| Dominant Region | North America |

| Segment Covered | By Type, By End-Use, By Application, By Regions |

| Key companies profiled | Mitsui Chemicals, Inc., Tosoh Corporation, Kumho Mitsui Chemicals, Vencorex, Asahi Kasei Corporation, Anderson Development Company, BASF SE, Bayer AG, Cangzhou Dahua Group Co., Ltd., Covestro AG, Evonik Industries AG, Huntsman Corporation, Mitsui Chemicals, The Dow Chemical Company, Wanhua Chemical Group Co., Ltd. |

Isocyanates Market - Supply Chain Analysis

Chemical Production and Processing

- Isocyanates such as MDI, TDI, and HDI are produced through phosgenation of amines followed by purification and formulation for use in polyurethane production across industrial and consumer applications.

- Key players BASF, Covestro, Dow, Huntsman Corporation

Quality Testing and Certification

- Isocyanates must meet strict chemical purity standards, hazardous material handling regulations, and environmental safety compliance before industrial uses.

- Key players: Chemicals Agency, U.S. Environmental Protection Agency, International Organization for Standardization, Occupational Safety and Health Administration

Distribution to Industrial Users

- Isocyanates are supplied to polyurethane foam manufacturers, automotive component producers, construction material companies, coating and adhesive manufacturers, and insulation producers.

- Key players: BASF, Covestro, Dow.

Isocyanates Regulatory Landscape: Global Regulations

| Country / Region | Regulatory Body | Key Regulations | Focus Areas | Notable Notes |

| US | Environmental Protection Agency (EPA); Occupational Safety and Health Administration (OSHA) | Toxic Substances Control Act (TSCA); OSHA Hazard Communication Standard; Clean Air Act | Chemical safety, occupational exposure limits, and industrial emissions | Isocyanates used in polyurethane production are strictly regulated due to respiratory health risks and workplace exposure hazards. |

| Europe | European Chemicals Agency (ECHA); European Commission | REACH Regulation; CLP Regulation; Worker Protection Directive | Chemical registration, hazard classification, and worker safety training | The EU introduced mandatory training requirements for workers handling diisocyanates to reduce occupational exposure risks. |

| China | Ministry of Ecology and Environment (MEE); Ministry of Emergency Management (MEM) | Environmental Protection Law; Work Safety Law | Industrial chemical safety, emissions monitoring | China regulates isocyanate production and handling due to the hazardous nature of the compounds and industrial safety concerns. |

| India | Ministry of Environment, Forest and Climate Change (MoEFCC); Central Pollution Control Board (CPCB) | Environment Protection Act; Manufacture, Storage, and Import of Hazardous Chemicals Rules | Hazardous chemical management, industrial safety | Isocyanates are categorized as hazardous chemicals and must follow strict storage, handling, and transportation rules. |

| Japan | Ministry of Economy, Trade and Industry (METI); Ministry of Health, Labour and Welfare (MHLW) | Chemical Substances Control Law (CSCL); Industrial Safety and Health Act | Chemical risk management, workplace safety | Japan regulates isocyanates through strict occupational exposure limits and chemical management systems. |

| Brazil | Brazilian Institute of Environment and Renewable Natural Resources (IBAMA); Ministry of Labor | National Chemical Safety Regulations; Occupational Safety Standards | Worker protection, environmental monitoring | Brazil enforces occupational safety and environmental regulations for industrial use of isocyanates in polyurethane manufacturing. |

Segmental Insights

Type Insights

How did the Aromatic Diisocyanate Segment Dominate the Isocyanates Market in 2025?

The aromatic diisocyanate segment dominated the market share 75.00% in 2025, driven by its extensive, cost-effective use in producing rigid polyurethane foam for construction insulation, rising demand for energy-efficient appliances, and expanding applications in the automotive sector, particularly electric vehicles. Aromatic isocyanates are critical in producing lightweight polyurethane foams and composites that improve fuel efficiency and extend electric vehicle (EV) battery ranges, with the automotive sector anticipated to expand rapidly.

")

The aliphatic segment is projected to have the fastest CAGR in the market between 2026 and 2035, expanding rapidly due to their superior performance in specialized applications. The coatings are expected to be a major contributor, driven by the need for non-yellowing, weather-resistant surfaces in outdoor applications, increasing demand for automotive clearcoats and high-performance industrial coatings, particularly for electric vehicles.

Isocyanates Market Share, By Type, 2025 (%)

| By Type | Revenue Share, 2025 (%) |

| Aromatic Diisocyanate | 75.00% |

| Aliphatic | 25.00% |

- The Aromatic Diisocyanate Segment shares 75.00% of the market, driven by its widespread use in polyurethane production for construction, automotive, and insulation applications, benefiting from high demand and cost efficiency."

- The aliphatic segment share of 25.00% is limited by higher costs and niche usage in coatings and specialty applications, though valued for superior UV resistance and durability."

Application Insights

Which Application Dominated the Isocyanates Market in 2025?

The rigid foam segment dominated the market share 38.00% in 2025, driven heavily by its critical role in building insulation, refrigeration, and cold-chain logistics. The segment's dominance is primarily supported by its superior thermal resistance, lightweight nature, and durability, which align with global trends towards energy efficiency and stricter building codes. Tightening building energy codes globally spurred high demand for spray foam insulation and rigid panels, valued for their durability and superior insulation performance.

The flexible foam segment is projected to have the fastest CAGR in the market between 2026 and 2035, fueled by rising demand in furniture, bedding, and automotive cushioning. Flexible foam is emerging as a high-growth segment due to its extensive use in consumer goods, such as cushions and mattresses, as well as automotive interiors. Flexible polyurethane foams are in high demand for automotive seating, providing comfort and noise reduction, with a specific focus on electric vehicle applications.

Isocyanates Market Share, By Application, 2025 (%)

| By Application | Revenue Share, 2025 (%) |

| Rigid Foam | 38.00% |

| Flexible Foam | 18.00% |

| Paints and Coatings | 14.00% |

| Adhesives and Sealants | 12.00% |

| Elastomers | 7.00% |

| Binders | 5.00% |

| Others | 6.00% |

- The Rigid Foam Segment shares 38.00% in 2025 of the market, driven by strong demand in insulation applications across construction and refrigeration industries, supported by energy efficiency regulations and infrastructure growth."

- The flexible foam segment shares 18.00%, supported by usage in furniture, bedding, and automotive seating, but is limited compared to rigid foam due to lower volume intensity and slower growth in end-use sectors."

- The Paints and Coatings Segment shares 14.00% of the market, constrained by its role in specialized protective and decorative applications, with demand tied to industrial and automotive coating cycles."

- The Adhesives and Sealants segment shares 12.00%, driven by construction and packaging needs, but remains secondary due to competition from alternative chemistries and moderate consumption volumes."

- The elastomer segment shares 7.00% of the market, limited by niche applications in automotive and industrial components, with relatively lower consumption compared to foam segments."

- The Binders segment shares 5.00% of the market restricted to specific uses such as wood panels and foundry applications, resulting in comparatively lower demand."

- The Others segment shares 6.00% of the market, consisting of diverse minor applications with fragmented demand and limited large-scale industrial adoption."

End Use Insights

How did the Budlings and Construction Segment Dominate the Isocyanates Market in 2025?

The building and construction segment dominated the market share 41.00% in 2025, driven by massive demand for rigid polyurethane foam in insulation retrofits, energy-efficient building codes, and cold-storage warehouses. Increased use of spray foam for superior air-sealing and durability accelerated this leadership. Rising global adoption of green building initiatives requires high-performance insulation, driving demand for rigid polyurethane foams derived from MDI. The need for durable bonding materials in modern construction projects has increased the use of polyurethanes.

The furniture segment is projected to have the fastest CAGR in the market between 2026 and 2035. Growth is largely fueled by rising demand for flexible polyurethane foam, which is crucial for cushioning, durability, and comfort in residential and commercial furniture. Increased consumer demand for comfortable and high-quality aesthetic furniture is driving the need for better-performing flexible foam, which uses isocyanates. The rapid growth of online furniture is fueling the demand for durable and easily transportable foam products, contributing to the sector's fast growth.

Isocyanates Market Share, By End-Use, 2025 (%)

| By End-Use | Revenue Share, 2025 (%) |

| Building & Construction | 41.00% |

| Furniture | 10.00% |

| Automotive | 12.00% |

| Electronics | 8.00% |

| Packaging | 7.00% |

| Footwear | 6.00% |

| Others | 16.00% |

- Rigid Foam (38.00%) Why it dominates: "Accounts for 38.00% of the market, driven by strong demand in insulation applications across construction and refrigeration industries, supported by energy efficiency regulations and infrastructure growth."

- Flexible Foam (18.00%) Why it is gaining momentum: "Holds 18.00% share, supported by increasing demand in furniture, bedding, and automotive seating, with steady expansion across comfort and cushioning applications."

- Paints and Coatings (14.00%) Why it is gaining momentum: "Represents 14.00% of the market, driven by rising demand for high-performance protective and decorative coatings in automotive and industrial sectors."

- Adhesives and Sealants (12.00%) Why it is gaining momentum: "Captures 12.00% share, fueled by growing applications in construction, packaging, and infrastructure development projects."

- Elastomers (7.00%) Why it is gaining momentum: "Accounts for 7.00% of the market, supported by expanding use in automotive and industrial components requiring durability and flexibility."

- Binders (5.00%) Why it is gaining momentum: "Holds 5.00% share, driven by consistent demand in wood panels, composites, and specialty industrial applications."

- Others (6.00%) Why it is gaining momentum: "Comprises 6.00% of the market, supported by emerging niche applications and gradual adoption across diverse end-use industries."

Regional Insights

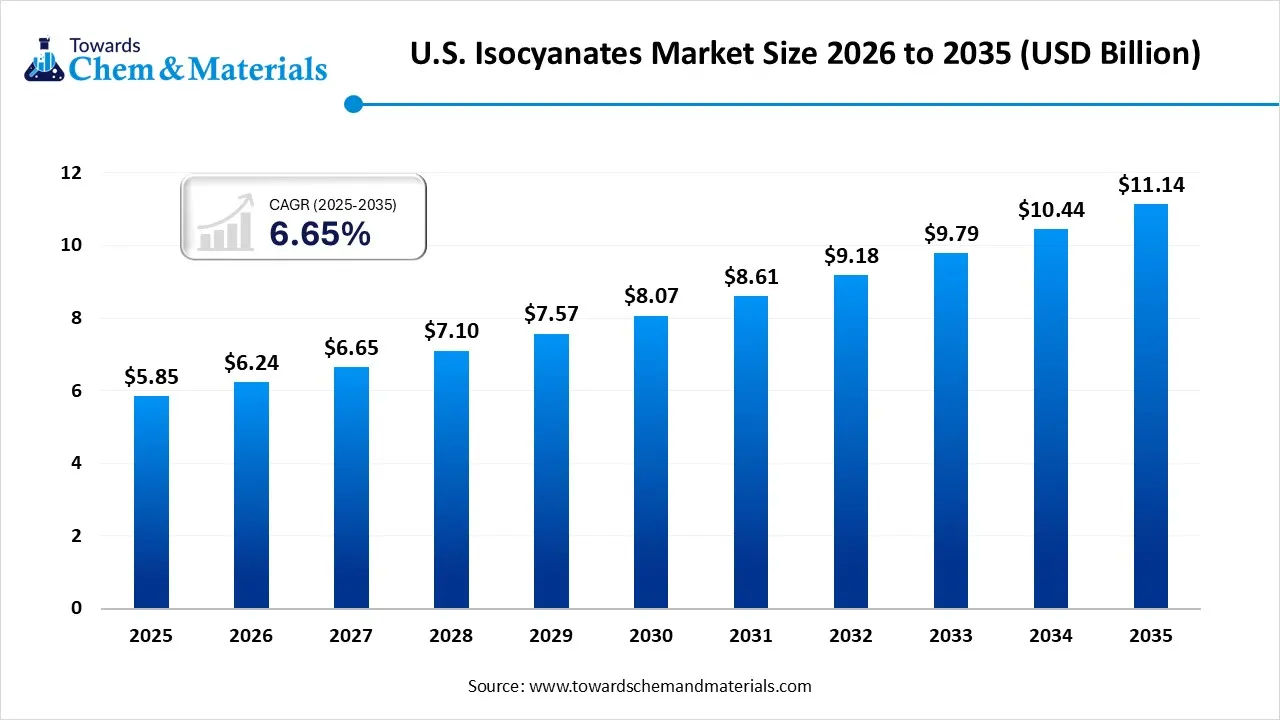

The U.S. Isocyanates market size was valued at USD 12.07 billion in 2025 and is expected to be worth around USD 19.10 billion by 2035, exhibiting at a compound annual growth rate (CAGR) of 4.70% over the forecast period from 2026 to 2035. The U.S. isocyanates market is fueled by strong demand for polyurethane in construction, especially insulation, and in the automotive sector for lightweighting and EVs, as well as increasing furniture and bedding needs. Major growth drivers include increased demand for energy-efficient materials, technological advancements, and a significant shift toward bio-based, sustainable, low-VOC options to comply with strict regulations. Growing consumer awareness and government restrictions on emissions are further accelerating the adoption of eco-friendly isocyanates, particularly those derived from bio-based feedstocks.")

North America Isocyanates Market Growth Factor

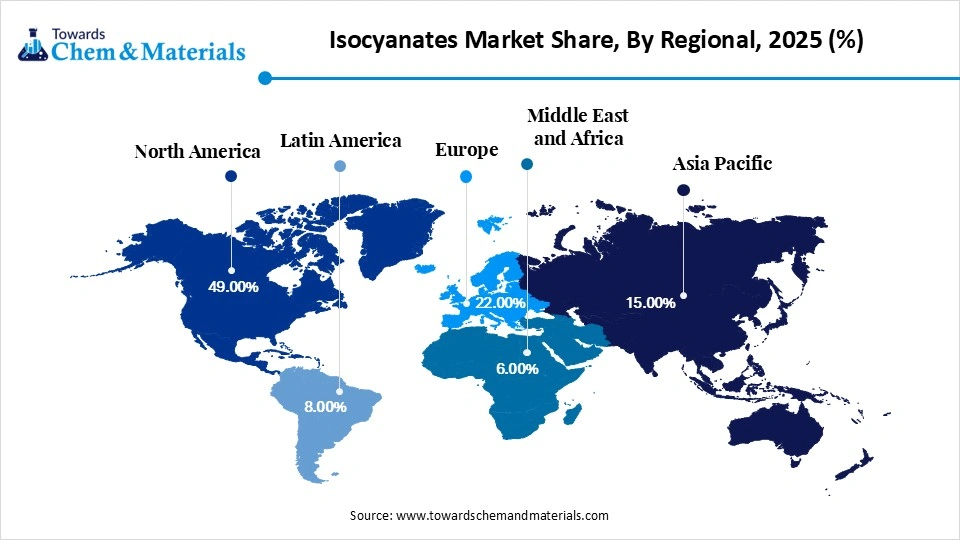

The North America isocyanates market size was valued at USD 16.10 billion in 2025 and is expected to be worth around USD 25.30 billion by 2035, exhibiting at a compound annual growth rate (CAGR) of 4.62% over the forecast period from 2026 to 2035. North America dominated the market share 49.00% in 2025, driven by increasing demand for polyurethane (PU) in construction, especially insulation, and in the automotive sector. Additionally, there’s a notable shift towards sustainable, bio-based products. Major growth drivers include government investments in energy-efficient buildings, the adoption of lightweight materials, and tighter environmental regulations that favor low-VOC options. Regulations from the EPA and other U.S. environmental agencies are also encouraging the market to favor water-based coatings and safer crosslinking agents.

Europe Isocyanates Market Growth Factor

Europe isocyanates market segment accounted for the major revenue share of 22.00% in 2025. Europe is expected to have the fastest growth in the market in the forecast period between 2026 and 2035, due to growing demand for polyurethane (PU) foams in construction, insulation, and automotive lightweighting, as well as increased renovation projects aimed at improving energy efficiency. The construction industry's growth, especially in Germany, is fueling demand for isocyanate-based rigid PU foam for insulation. Additionally, the EU's emphasis on energy-efficient, eco-friendly buildings greatly supports this sector.")

Germany Isocyanates Market Growth Factor

The German isocyanates market is rapidly growing, fueled by the strong manufacturing sector, especially in automotive and construction. Advances in sustainable and high-performance materials also contribute to this growth. The construction industry is a key user of rigid polyurethane foam, supported by Germany’s strict energy building codes and net-zero-energy objectives. Growing investments in residential and commercial infrastructure, along with renovation projects needing efficient insulation, greatly increase the demand for MDI-based insulation materials.

Asia Pacific Isocyanates Market Growth Factor

Asia Pacific isocyanates market segment accounted for the major revenue share of 15.00% in 2025. Asia Pacific expects the notable growth in the market, driven by robust manufacturing growth and rising polyurethane demand in China, India, and Southeast Asia. Rapid urbanization, large-scale construction projects, and increased automotive production, along with capacity expansions by industry giants such as Wanhua Chemical and Covestro in China, have strengthened the region's dominance. The large manufacturing sector, particularly in furniture, automotive seating, and rigid foams used in cold-chain logistics, contributed significantly to high consumption levels.

Isocyanates Market Share, By Regional, 2025 (%)

| Regional | Revenue Share, 2025 (%) |

| North America | 49.00% |

| Europe | 22.00% |

| Asia Pacific | 15.00% |

| Latin America | 8.00% |

| Middle East & Africa | 6.00% |

- North America (49.00%) Why it dominates: "Accounts for 49.00% of the market, driven by advanced manufacturing infrastructure, high demand across construction and automotive sectors, and strong presence of key industry players."

- Europe (22.00%) Why it is gaining momentum: "Holds 22.00% share, supported by increasing focus on sustainable materials, energy-efficient construction, and well-established automotive and industrial sectors."

- Asia Pacific (15.00%) Why it is gaining momentum: "Represents 15.00% of the market, driven by rapid industrialization, expanding construction activities, and growing demand from emerging economies."

- Latin America (8.00%) Why it is gaining momentum: "Accounts for 8.00% share, supported by steady growth in construction, automotive production, and infrastructure development."

- Middle East & Africa (6.00%) Why it is gaining momentum: "Captures 6.00% of the market, driven by increasing investments in infrastructure, construction projects, and industrial diversification initiatives."

India Isocyanates Market Growth Factor

The Indian isocyanates market is growing rapidly, driven mainly by strong demand for polyurethane (PU) in the construction, automotive, and furniture industries. Major growth factors include increased infrastructure spending, higher demand for rigid foam insulation, wider use of lightweight materials in electric vehicles (EVs), and ongoing urbanization. Large infrastructure and urban housing projects in India are increasing demand for rigid polyurethane foam, which is widely used for thermal insulation, sealants, and roofing.

Recent Developments

- In August 2025, Algenesis Labs, a pioneer in sustainable materials science, announced the commissioning of its Bio-Iso pilot plant. This facility creates the world’s first 100% biogenic carbon isocyanate entirely derived from plants, marking a significant breakthrough in polyurethane chemistry.(Source: worldbiomarketinsights.com)

- In December 2025, Pflaumer Brothers introduced TERACURE® HP-47, an aliphatic polyisocyanate hardener designed to bridge the performance gap between waterborne and solvent-borne high-performance 2K polyurethane systems. The new product offers high chemical and abrasion resistance for applications in heavy-duty flooring, transportation, and industrial coatings. For more details, visit Coatings World.(Source: www.coatingsworld.com)

Top players in the Isocyanates Market & Their Offerings:

- Mitsui Chemicals, Inc.: Mitsui Chemicals produces MDI, TDI, and modified isocyanates used in electronics, automotive components, and industrial polyurethane systems. The company maintains strong production capacity in Asia and focuses on advanced material development.

- Tosoh Corporation: Tosoh manufactures isocyanates for polyurethane foams, coatings, and elastomers. The company operates production facilities in Asia and supplies materials used in construction, insulation, appliances, and automotive parts.

- Kumho Mitsui Chemicals: Kumho Mitsui Chemicals produces MDI used primarily in polyurethane foam applications such as insulation panels, refrigerators, and automotive components. The company focuses on high-quality products and expanding production capacity in Asia.

- Vencorex: Vencorex manufactures specialty isocyanates and derivatives used in coatings, adhesives, elastomers, and advanced composite materials. The company emphasizes innovation in specialty polyurethane chemicals for industrial and aerospace applications.

- Asahi Kasei Corporation: Asahi Kasei supplies specialty chemicals, including isocyanate-based materials used in coatings, adhesives, and engineering plastics. The company focuses on sustainable chemical manufacturing and advanced material solutions.

- Anderson Development Company

- BASF SE

- Bayer AG

- Cangzhou Dahua Group Co., Ltd.

- Covestro AG

- Evonik Industries AG

- Huntsman Corporation

- Mitsui Chemicals

- The Dow Chemical Company

- Wanhua Chemical Group Co., Ltd.

Segments Covered:

By Type

- Aromatic Diisocyanate

- Aliphatic

By End-Use

- Building & Construction

- Furniture

- Automotive

- Electronics

- Packaging

- Footwear

- Others

By Application

- Rigid Foam

- Flexible Foam

- Paints and Coatings

- Adhesives and Sealants

- Elastomers

- Binders

- Others

By Regions

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Asia Pacific

- China

- India

- Japan

- South Korea

- Latin America

- Brazil

- Argentina

- Middle East & Africa

- Saudi Arabia

- South Africa

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

FAQ's

Select User License to Buy

Figures (4)