Content

What is the Current Size of the Fumed Silica Market and its Projected Growth?

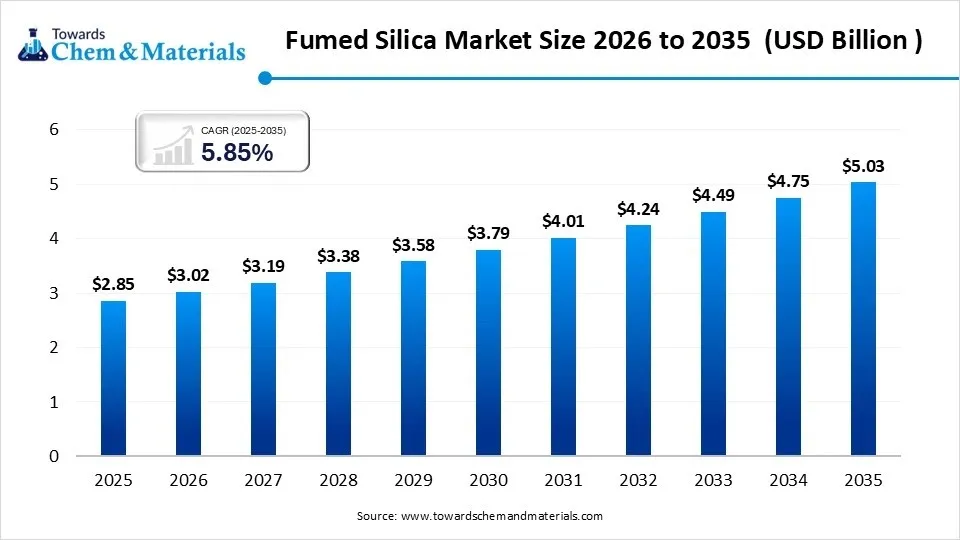

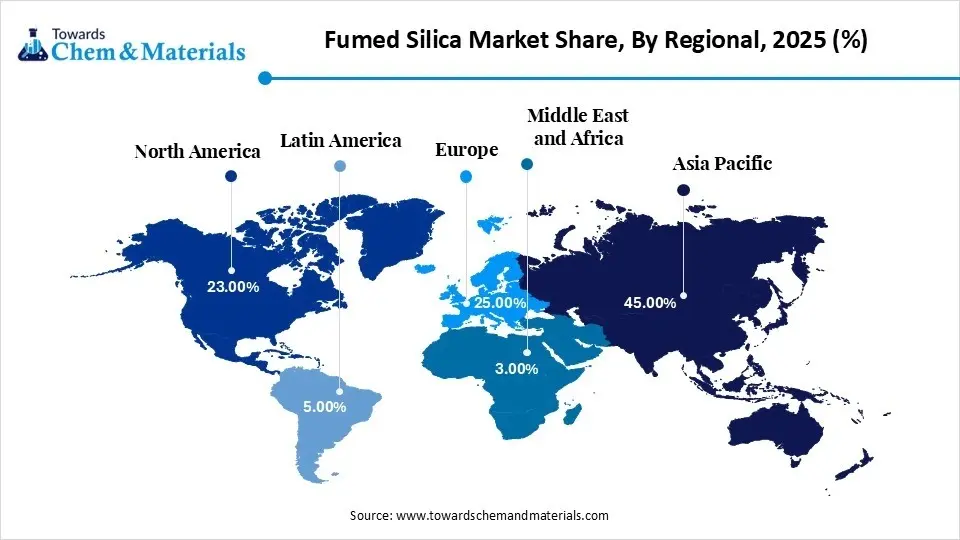

The global fumed silica size was estimated at USD 2.85 billion in 2025 and is expected to increase from USD 3.02 billion in 2026 to USD 5.03 billion by 2035, growing at a CAGR of 5.85% from 2026 to 2035. Asia Pacific dominated the fumed silica with the largest revenue share of 45.00% in 2025. Increasing product demand from the construction and automotive industries is the key factor driving market growth. Also, ongoing innovations in production processes coupled with the rapid urbanisation across the globe, can fuel market growth further.

")

Market Highlights

- Asia Pacific dominated the market with the largest share 45.00% in 2025. The dominance of the segment can be attributed to the growing demand for paints, coatings, and sealants.

- By region, North America is expected to grow at the fastest CAGR over the forecast period. The growth of the region can be credited to the ongoing innovations in manufacturing processes.

- By region, Europe is expected to grow at a notable CAGR over the forecast period. The growth of the region can be driven by the growing demand for high-purity additives in cosmetics.

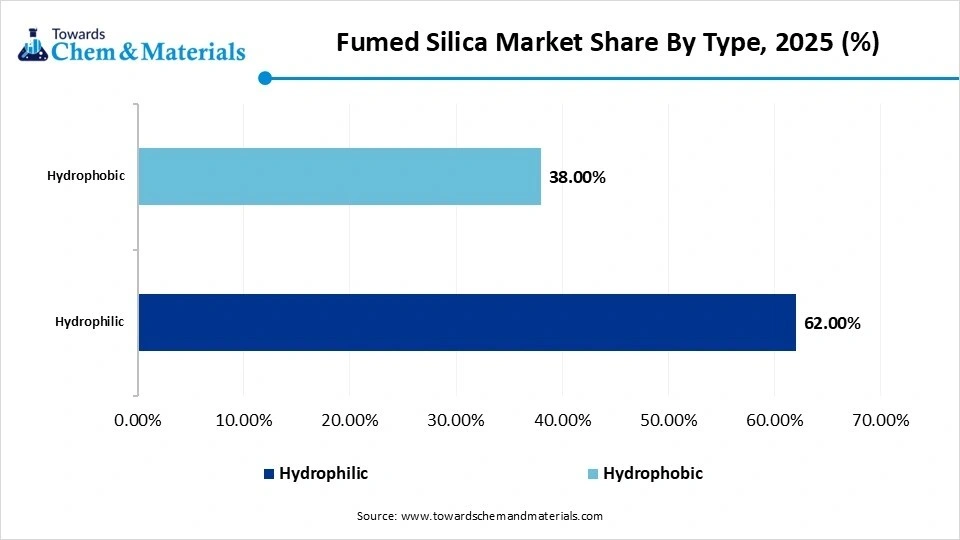

- By type, the hydrophilic segment dominated the market with the largest share 62.00% in 2025. The dominance of the segment can be attributed to its increasing demand as an anti-settling, thickening, and reinforcing agent.

- By type, the hydrophobic segment is expected to grow at the fastest CAGR over the forecast period. The growth of the segment can be credited to the rising demand for durable construction applications.

- By application, the silicone rubber segment held the largest market share 38.00% in 2025. The dominance of the segment can be linked to the ongoing trend towards specialized and high-purity silicone rubber.

- By application, the adhesives and sealants segment is expected to grow at the fastest CAGR over the projected period. The growth of the segment can be driven by the growing demand for rheology control.

What is Fumed Silica Market?

The market involves the manufacturing, distribution, and application of a high-grade, nano-sized, fluffy white amorphous silicon dioxide powder produced through flame hydrolysis. It acts as an important thickening agent, rheology modifier, and reinforcing filler. Major end-uses include paints and coatings, silicon rubber reinforcement, pharmaceuticals, and adhesives and sealants. The market is crucial for improving product stability and performance in different consumer sectors.

Recent Market Trends

- The market is experiencing substantial growth due to its increasing applications in the electronics sector. Fumed silica is used in different electronic components, such as capacitors, insulators, and circuit boards, due to its exceptional thermal stability and dielectric properties.

- The rapid advancements in production processes to improve the quality and efficiency of fumed silica are the latest trend in the market, shaping positive market growth. These developments can increase product demand across different sectors, aligning with sustainability goals by reducing overall waste and energy consumption.

- Growing demand for high-performance materials in microelectronic devices and semiconductor encapsulation is another major factor driving market expansion. Also, there is an ongoing transition towards hydrophobic (treated) fumed silica, which is favoured for its moisture-sensitive applications such as automotive and sealant refinishing.

Report Scope

| Report Attribute | Details |

| Market Size in 2026 | USD 3.02 Billion |

| Revenue Forecast in 2035 | USD 5.03 Billion |

| Growth Rate | CAGR 5.85% |

| Forecast Period | 2026 - 2035 |

| Base Year | 2025 |

| Dominant Region | Asia Pacific |

| Segment Covered | By Type, By Application, By Region |

| Key companies profiled | Cabot Corporation, Dongyue Group, Evonik Industries AG, Gelest Inc., Hubei Xingfa Chemicals Group Co., Ltd., Henan Xunyu Chemical Co., Ltd., Nouryon, Shin-Etsu Chemical Co., Ltd., China National Bluestar (Group) Co., Ltd., Guangdong Polysil Co., Ltd., Tata Chemicals Ltd., Heraeus Holding GmbH, Wynca Group, Shandong Bangde Chemical Co., Ltd., Yichang CSG Polysilicon Co., Ltd. |

How Cutting-Edge Technologies Are Revolutionizing the Fumed Silica Market?

Advanced technologies such as nanotechnology, plasma-based synthesis, and cutting-edge surface modification are transforming the market by facilitating greener production, lowering energy consumption, and enabling specialized, high-purity applications. Furthermore, nanotechnology allows to produce ultra-fine particles with controlled porosity, which are necessary for high-performance sectors such as aerospace and electronics.

Trade Analysis of the Fumed Silica Market: Import & Export Statistics

According to U.S. import data, 310 shipments of fumed silica were imported into the United States between June 2024 and May 2025 (TTM). via 98 international exporters supplying 88 global buyers.

South Korea, China, and Thailand dominate global fumed silica exports, while the United States, India, and Vietnam are the top three importing countries.

In 2024, China's imports of silica and quartz sands totaled $269,291.35K. The supply was led by Indonesia ($96,758.74K, 2,659,900,000 Kg), Australia ($69,050.75K, 1,289,010,000 Kg), Malaysia ($53,664.02K, 1,443,590,000 Kg), United States ($17,182.45K, 2,726,100 Kg), Other Asia, nes ($12,914.69K, 59,085,200 Kg).

According to India import data, 7 shipments of Chemical Silica were imported between May 2024 and Apr 2025 (TTM), showcasing a 40% year-on-year growth. These transactions involved 4 exporters supplying 3 verified global buyers, highlighting increased market activity.

- The top three chemical silica importers are Vietnam, Colombia, and the U.S., while the leading exporters are China, Germany, and the UK.

- According to India Export data, 106 shipments of Colloidal Silica were exported from India between June 2024 and May 2025 (TTM), involving 14 verified Indian exporters and 46 buyers.

- Japan (499 shipments), China (411 shipments), and India (360 shipments) are the top global exporters of colloidal silica. Conversely, Bangladesh, Australia, and Sri Lanka dominate the import market.

Fumed Silica Market Supply Chain Analysis

Feedstock Procurement

- It involves the strategic sourcing of high-grade raw materials, mainly silicon tetrachloride and hydrogen/oxygen gases, crucial for the energy-intensive flame hydrolysis production process.

- Major Players: Evonik Industries AG, Cabot Corporation

Chemical Synthesis and Processing

- It involves the high-temperature flame hydrolysis technique used to manufacture high-purity, ultra-fine, amorphous silicon dioxide. The resulting fumed silica is then processed through surface treatment.

- Major Players: Wacker Chemie AG, Tokuyama Corporation

Packaging and Labelling

- It includes the catering materials, sizes, and safety documentation used to transport and store this high-surface area and low-density material.

- Major Players: Tokuyama Corporation, OCI Company Ltd

Regulatory Compliance and Safety Monitoring

- It includes the strict, mandatory adherence to international and national standards regarding the manufacturing, handling, and environmental impact of synthetic amorphous silica.

- Major Players: Kemitura A/S, Dongyue Group Ltd.

Fumed Silica Market's Regulatory Landscape: Global Regulations

| Country/Region | Key Regulations |

| European Union (EU) | Circular Economy Act (2026): Scheduled for proposal in late 2026, this landmark legislation aims to create a Single Market for secondary raw materials, doubling the EU's circularity rate to 24% by 2030. |

| India | Import Duty Exemptions: Revised rates effective February 2, 2025, provide duty exemptions for various metal waste and scrap (e.g., copper, tin, tungsten) to support domestic recycling. |

| China | New rules effective August 1, 2025, clarify that high-quality recycled steel and lithium-ion battery materials (black mass) are not classified as "solid waste," allowing them to be imported more freely to support domestic manufacturing. |

| United States | Current policies favor domestic processing of scrap metal to support industries like electric vehicle manufacturing and aerospace. |

Segmental Insights

Type Insights

How Much Share Did Hydrophilic Segment Held in Fumed Silica Market in 2025?

The hydrophilic segment dominated the market with the largest share in 2025. The dominance of the segment can be attributed to its increasing demand as an anti-settling, thickening, and reinforcing agent in paints, coatings, adhesives, and sealants. In addition, this type of silica is extensively used in gelcoats and fiberglass-reinforced plastics (FRP) to improve viscosity control during manufacturing, contributing to segment growth soon.

")

The hydrophobic segment is expected to grow at the fastest CAGR over the forecast period. The growth of the segment can be credited to the rising demand for durable construction, automotive, and electronics applications, along with the rapid innovations in specialized applications. Additionally, hydrophobic silica is favoured as a rheology modifier for automotive and premium refinishing coatings as it is effective in preventing sagging on vertical surfaces.

Fumed Silica Market Share By Type, 2025 (%)

| By Type | Revenue Share, 2025 (%) |

| Hydrophilic | 62.00% |

| Hydrophobic | 38.00% |

- Hydrophilic type segment accounts for 62% of the market share, dominating due to its widespread use in various applications like coatings, sealants, and adhesives, where moisture absorption is less of a concern.

- Hydrophobic type segment holds 38% of the market share, gaining momentum in specialized applications such as silicone-based products and hydrophobic coatings, but not dominating due to its more niche applications.

Application Insights

Which Application Dominated the Fumed Silica Market in 2025?

The silicone rubber segment held the largest market share in 2025. The dominance of the segment can be linked to the ongoing trend towards specialized and high-purity silicone rubber in consumer goods and the medical sector. Moreover, silicone rubber is indispensable for implants, medical tubing, and artificial heart valves because of its high thermal stability and biocompatibility y at temperatures up to 200°C.

The adhesives and sealants segment is expected to grow at the fastest CAGR over the projected period. The growth of the segment can be driven by growing demand for rheology control, high-performance bonding, and thixotropic properties in the automotive and construction sectors. Furthermore, the push toward low-VOC in architectural coatings and sealants optimizes the use of fumed silica to keep peak performance without compromising the regulatory standards.

Fumed Silica Market Share By Application , 2025 (%)

| By Application | Revenue Share, 2025 (%) |

| Silicone Rubber | 38.00% |

| Plastics and Composites | 15.00% |

| Food and Beverages | 8.00% |

| Paints, Coatings & Inks | 12.00% |

| Adhesives and Sealants | 14.00% |

| Others | 13.00% |

- Silicone Rubber segment accounts for 38% of the market share, dominating due to its high demand in the production of elastomers and sealants, where fumed silica enhances strength and viscosity.

- Plastics and Composites segment holds 15% of the market share, used to improve the mechanical properties and stability of materials, but not dominating due to competition with other fillers and additives.

- Food and Beverages segment represents 8% of the market share, used as an anti-caking agent, but not dominating due to its specialized role and smaller market size compared to other applications.

- Paints, Coatings & Inks segment accounts for 12% of the market share, widely used to improve thixotropy and consistency in formulations, but not dominating due to the presence of other functional additives.

- Adhesives and Sealants segment holds 14% of the market share, used to enhance bonding and durability, but not dominating due to its competition with other strengthening agents and fillers.

- Others segment represents 13% of the market share, covering various niche uses, but not dominating due to its relatively fragmented and smaller share in comparison to major applications.

Regional Insights

The Asia Pacific fumed silica market size was valued at USD 1.28 billion in 2025 and is expected to be worth around USD 2.29 billion by 2035, exhibiting at a compound annual growth rate (CAGR) of 5.99% over the forecast period from 2026 to 2035.Asia Pacific dominated the market with the largest share 45.00% in 2025. The dominance of the segment can be attributed to the growing demand for paints, coatings, and sealants, coupled with the surge in production adoption in personal care and pharmaceutical products. In addition, the growth in electronics production in emerging economies such as China and India propels the demand for fumed silica in protective coatings and potting compounds.

")

China Fumed Silica Market Trends

In the Asia Pacific, China dominated the market owing to the rise in investments in green technologies and high-tech industries, along with the substantial expansion in the automotive, construction, and electronics industries. Also, market players are increasingly adopting cutting-edge technologies such as AI and automation to enhance efficiency and fulfil environmental standards.

North America Fumed Silica Market Trends

North America is expected to grow at the fastest CAGR over the forecast period. The growth of the region can be credited to the ongoing innovations in manufacturing processes and the growing emphasis on energy-efficient and sustainable materials. Additionally, the strong presence of major market players like Wacker Chemie AG offers a consistent and robust domestic supply, leading to further regional growth.

U.S. Fumed Silica Market Trends

In North America, the U.S. led the market due to the increasing demand for personal care products and a surge in infrastructure investment in different regions of the country. Fumed silica is crucial for manufacturing lightweight components and advanced coatings. Major market players have expanded their U.S. facilities to ensure a consistent domestic supply.

")

Europe Fumed Silica Market Trends

Europe is expected to grow at a notable CAGR over the forecast period. The growth of the region can be driven by the growing demand for high-purity additives in cosmetics and pharmaceutical sectors, coupled with the strict EU regulations regarding the trade of fumed silica. In addition, governments in the region are introducing new R&D initiatives to optimise the production process of smart coatings using advanced technology, which is increasing their adoption in the highly developed aerospace sector.

Fumed Silica Market Share, By Regional, 2025 (%)

| Regional | Revenue Share, 2025 (%) |

| North America | 23.00% |

| Europe | 25.00% |

| Asia Pacific | 45.00% |

| Latin America | 5.00% |

| Middle East & Africa | 3.00% |

- The Asia Pacific share of 45.00% in 2025 Why it dominates: Rapid industrialization, increasing demand for fumed silica in industries like coatings, electronics, and automotive, particularly in China and India."

- The North America share of 23.00% in 2025 Why it does not dominate: While it has a notable share, the market is relatively mature, and growth is slower compared to Asia Pacific."

- The Europe share of 25.00% in 2025 Why it does not dominate: Despite a strong share, Europe faces slower growth due to established industrial sectors and limited expansion opportunities."

- The Latin America share of 5.00% in 2025 Why it does not dominate: Limited industrialization and slower adoption of fumed silica technology, contributing to a smaller market share."

- The Middle East & Africa share of 3.00% in 2025 Why it does not dominate: Economic and industrial challenges in the region hinder the growth of the fumed silica market."

Germany Fumed Silica Market Trends

The growth of the market in the country is due to growing demand for high-grade additives in manufacturing and the rise in adoption of electric vehicles (EVs). Moreover, the country's robust pharmaceutical industry uses fumed silica as a high-purity stabilizer and glidant for tablet formulations, to ensure dosage uniformity and prevent clumping.

Recent Developments

- In February 2026, North American specialty chemical distributor LBB Specialties (LBBS) announced a partnership with Kemitura to distribute its fumed silica products across the United States and Canada. This agreement adds KemituraSil® to LBBS's portfolio, strengthening their presence, especially within the C.A.S.E. (coatings, adhesives, sealants, and elastomers)markets.(Source: www.thailand-business-news.com )

- In August 2025, Bharat Heavy Electricals Limited (BHEL) partnered with DRDO’s (Defence Research and Development Organisation) DMRL (Defence Metallurgical Research Laboratory), Hyderabad, via a License Agreement for Transfer of Technology (LAToT) to manufacture Fused Silica Radar Domes. Utilizing the Cold Isostatic Pressing and Sintering route, this agreement promotes indigenous production of critical seeker-based missile guidance systems.(Source: www.business-standard.com)

Market Companies

- Cabot Corporation: Cabot Corporation is a leading global producer in the fumed silica market, renowned for its CAB-O-SIL® branded products used as critical performance additives in adhesives, sealants, coatings, and silicone elastomers. With a strong manufacturing footprint, including major expansions in China and the US.

- Dongyue Group: Dongyue Group (specifically its subsidiary, Shandong Dongyue Silicone Material Co., Ltd.) is a major global player in the fumed silica market, leveraging its position as one of China's largest silicone producers to maintain a highly integrated value chain.

- Evonik Industries AG: Evonik Industries AG is a dominant "Star" player in the global fumed silica market, holding a leading position through its flagship AEROSIL® brand. The company's predecessor, Degussa, invented the flame hydrolysis process for fumed silica in 1942, giving Evonik over 80 years of expertise in the sector.

- Gelest Inc.

- Hubei Xingfa Chemicals Group Co., Ltd.

- Henan Xunyu Chemical Co., Ltd.

- Nouryon

- Shin-Etsu Chemical Co., Ltd.

- China National Bluestar (Group) Co., Ltd.

- Guangdong Polysil Co., Ltd.

- Tata Chemicals Ltd.

- Heraeus Holding GmbH

- Wynca Group

- Shandong Bangde Chemical Co., Ltd.

- Yichang CSG Polysilicon Co., Ltd.

Segments Covered in the Report

By Type

- Hydrophilic

- Hydrophobic

By Application

- Silicone Rubber

- Plastics and Composites

- Food and Beverages

- Paints, Coatings & Inks

- Adhesives and Sealants

- Others

By Region

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Asia Pacific

- China

- India

- Japan

- South Korea

- Latin America

- Brazil

- Argentina

- Middle East & Africa

- Saudi Arabia

- South Africa

FAQ's

Select User License to Buy

Figures (4)