Content

What is the Current Offshore Lubricants Market Size and Share?

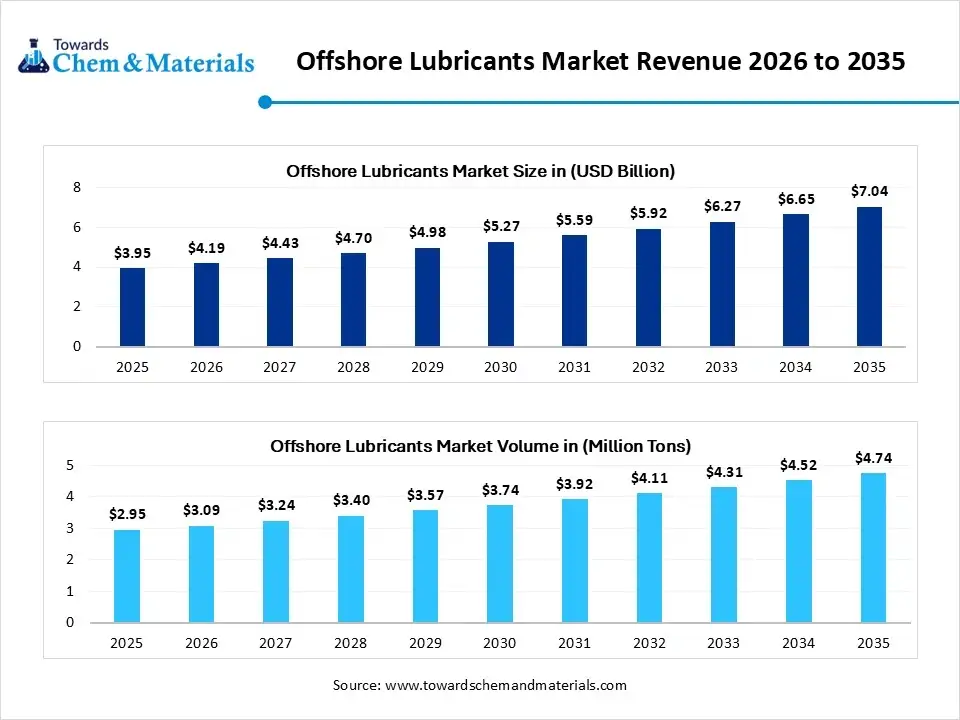

The offshore lubricants market size was valued at USD 3.95 billion in 2025, is estimated to reach USD 4.19 billion in 2026, and is projected to reach USD 7.04 billion by 2035, exhibiting a compound annual growth rate (CAGR) of 5.95% over the forecast period from 2026 to 2035. In terms of volume, the offshore lubricants market is projected to grow from 2.95 million tons in 2025 to 4.74 million tons by 2035. growing at a CAGR of 4.85% from 2026 to 2035. The growing offshore oil exploration and deepwater drilling operations are major factors in boosting the demand for high-performance offshore lubrication solutions.

The offshore lubricants market includes specialized oils, greases, and hydraulic fluids made for drilling rigs, at sea production platforms, offshore support vessels (OSVs), and subsea equipment that need to work in rough marine surroundings. In practice, these lubricants help keep machinery reliable, offer anti-corrosion protection, maintain thermal balance, and support smoother operation even when there is extreme pressure, saltwater contact, and constantly shifting temperatures. Demand keeps moving because offshore oil & gas exploration is growing, deepwater drilling work is increasing, maritime trade is becoming more active, and environmental rules are getting tighter, which pushes buyers toward biodegradable and low-toxicity lubricants. Another factor is the wider take-up of synthetic lubricants, since they tend to last longer and deliver better overall results.

AI-enabled predictive maintenance, IoT lubricant monitoring, and improved additive packages are making operations more efficient and cutting down on unplanned downtime. Also, money is flowing into offshore renewable energy builds, especially offshore wind projects, and that creates extra openings for high-performance, eco-compliant offshore lubrication solutions across many regions globally.

Market Highlights

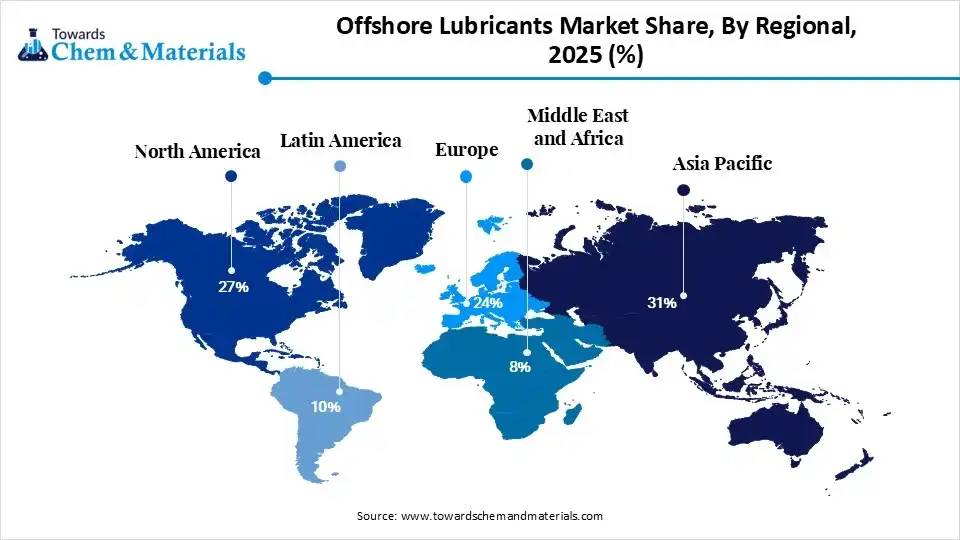

- By region, Asia Pacific dominated the Offshore Lubricants Market by holding 31% share in 2025 and is expected to grow at the fastest with a CAGR of 7.1% during the forecast period due to rising offshore wind investments.

- By region, North America held the 27% market share in 2025 and expects notable growth in the market with 5.3% CAGR during the forecast period, driven by stringent regulatory standards.

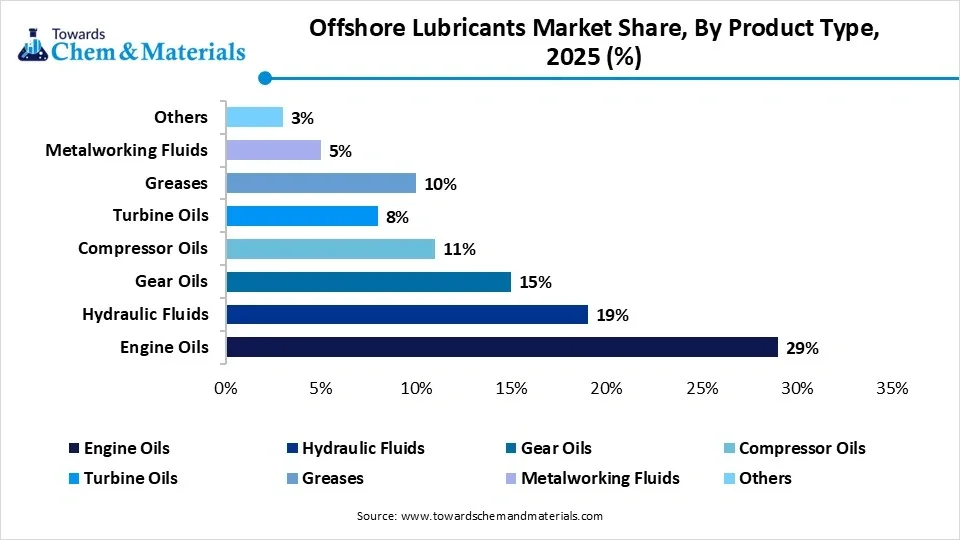

- By product type, the engine oils segment dominated the market with the largest share of 29% in 2025, driven by high-performance lubrication demand.

- By product type, the greases segment held the 10% market share in 2025 and is expected to grow at the fastest CAGR of 6.8% over the forecast period due to increased use of specialty greases for corrosion resistance and heavy-load protection.

- By base oil type, the mineral oils segment dominated the market with the largest share of 48% in 2025, driven by established supply chains supporting widespread deployment in mature offshore assets.

- By base oil type, the synthetic oil segment held the 39% market share in 2025 and is expected to grow at the fastest CAGR of 7.2% over the forecast period, as deepwater and ultra-deepwater operations require high-performance synthetic lubricants with superior thermal stability.

- By application, the drilling operations segment dominated the market with the largest share of 32% in 2025, driven by rising offshore investments in frontier basins.

- By application, the renewable offshore operations segment held the 7% market share in 2025, and is expected to grow at the fastest CAGR of 8.3% over the forecast period, as offshore wind farm expansion significantly increases lubricant demand for turbines and installation vessels

- By end-use industry, the oil & gas operators industry segment dominated the market with the largest share of 41% in 2025 due to extensive offshore production assets requiring continuous lubrication.

- By end-use industry, the offshore wind operators segment held the 10% market share in 2025, and is expected to grow at the fastest CAGR of 8.5% over the forecast period as operators prioritize long-drain synthetic lubricants for remote offshore assets.

- By distribution channel, the Direct Sales segment dominated the market with the largest share of 46% in 2025, as major lubricant suppliers maintain direct contracts with offshore operators and drilling companies

- By distribution channel, the OEM partnerships segment held the 15% market share in 2025, and is expected to grow at the fastest CAGR of 6.4% over the forecast period, as equipment manufacturers increasingly recommend certified lubricants for warranty compliance and performance optimization.

- By offshore water depth, the shallow water segment dominated the market with the largest share of 44% in 2025, driven by existing infrastructure that supports long-term operational continuity.

- By offshore water depth, the ultra-deepwater segment held the 22% market share in 2025, and is expected to grow at the fastest CAGR of 7.4% over the forecast period, as technological advances enable new offshore developments in challenging reservoirs.

At a Glance

- Market Estimated Size (2025): USD 3.95 Billion | CAGR (2026–2035): 5.95%

- Market Projected Size (2035): USD 7.04 Billion

- Asia Pacific: largest Market Revenue Share of 31% in 2025.

- Market Estimated Volume (2025): 2.95 Million Tons | Volume CAGR (2026–2035): 4.85%

- Market Projected Volume (2035): 4.74 Million Tons

- Market Pricing (2025):

- Average Manufacturing Price (2025): USD 1,989/Ton

- Average Selling Price (2025): USD 2,769/Ton

- Pricing CAGR (2025–2035): 3.11%

Offshore Lubricants Market Trends

- Environmental Regulation & Sustainability: More strict environmental rules, including IMO emission standards, are basically pushing up the need for biodegradable and environmentally acceptable lubricants (EALs). Offshore operators care more and more they care about low-toxicity, low-emission lubricant options. It helps reduce ecological exposure, makes compliance easier, and also backs broader sustainability aims while still keeping operational efficiency steady in sensitive marine ecosystems and offshore production zones.

- Rise of Synthetic Lubricants: Synthetic lubricants are seeing a lot of traction, mainly because they have better oxidation resistance, solid thermal stability, and strong overall performance in deep-sea offshore work. In many cases, they allow longer drain intervals, lower equipment wear, and improve dependability even when conditions get rough, high pressure, and colder temperatures. That means operators can cut down on maintenance spending and also stretch machinery lifespan, noticeably.

- Increasing Demand for High-Performance Grease : The demand for high-performance offshore grease is increasing rapidly, with operators looking for improved protection from corrosion, water contamination, and heavy mechanical loads. The equipment lasts longer, and unexpected failures are limited in cranes, winches, bearings, and subsea systems, ensuring continuous operations offshore and fewer and less frequent maintenance visits.

Report Scope

| Report Attribute | Details |

| Market Size and Volume in 2026 | USD 4.19 Billion/ 3.09 Million Tons |

| Revenue Forecast in 2035 | USD 7.04 Billion/ 4.74 Million Tons |

| Growth Rate | CAGR 5.95% |

| Forecast Period | 2026 - 2035 |

| Base Year | 2025 |

| Dominant Region | Asia Pacific |

| Segment Covered | By Product Type, By Base Oil, By Application, By End User, By Distribution Channel, By Offshore Water Depth, By Region |

| Key companies profiled | Exxon Mobil, Shell, Aegean Marine Petroleum, Idemitsu Kosan Co. Ltd., Chevron Corporation, Gulf Oil Corporation, BP Plc, Total S.A., Fuchs |

Key Technological Shifts and AI in the Offshore Lubricants Market

Artificial intelligence, along with newer digital tools, is turning how people manage lubricant use, with predictive maintenance, real-time condition tracking, and more tuned lubricant formulations. In practice, AI systems scan lubricant viscosity, oxidation levels, contamination, and wear particles by reading data from IoT sensors, then running machine learning models. This makes early fault detection easier, so unexpected stoppages go down, and machines stay productive for longer.

At the same time, advanced analytics can guide operators toward better oil replacement timing, so lubricant waste drops and overall operating costs come down too. AI is also speeding up work on additive and synthetic lubricant development, because it can estimate molecular behavior and performance traits before costly testing.

And on top of that, digital supply chain optimization supports better inventory prediction, plus smoother lubricant availability across various offshore sites. All these changes together boost equipment reliability, help extend machinery lifespan, strengthen environmental compliance, and cut operational risks that tend to show up in offshore conditions.

Supply Chain Analysis of the Offshore Lubricants Market

- Feedstock Procurement: The ability to choose high-quality additives, and to guarantee supply stability and regulatory compliance, cost effectiveness, and the quality of offshore-grade lubricants.

- Key Players: ExxonMobil, Shell, BP

- Chemical Synthesis and Processing: Using crude-derived materials to make synthetic or mineral base stocks that are specifically designed to operate under extreme pressure and temperature conditions.

- Key Players: BASF, Evonik, Lubrizol

- Quality Testing and Certification of Offshore Lubricants: Viscosity, Thermal stability, Water separation, and wear resistance testing to API, ISO, and offshore operations standards.

- Key Players: Chevron, SGS, Intertek

Regulatory Framework: Offshore Lubricants Market

Region Key Regulation Regulatory Focus

- Asia Pacific China Marine Environmental Protection Law

- Increasingly, offshore operators use biodegradable and environmentally acceptable lubricants to minimise marine pollution and meet offshore environmental standards.

- North America U.S. EPA Vessel General Permit (VGP) Regulations Offshore vessels and marine equipment used in environmentally sensitive waters should use environmentally acceptable lubricants (EALs), which are required by regulations.

- European Union EU Ecolabel for Lubricants & REACH Regulations

- The use of biodegradable offshore lubricants is encouraged under European regulations, which help to ensure sustainable offshore drilling and marine operations.

Offshore Lubricants Market Dynamics

Drivers:

The expanding market for Offshore Support Vessels (OSVs)

The demand for lubricants is significantly growing due to the growing use of offshore shipping vessels for the transport of equipment, personnel, and lubricants to offshore platforms. Engine oils, hydraulic fluids, and greases with superior performance capabilities are essential for the operation of OSVs in challenging marine environments, ensuring efficient and reliable performance.

High-Performance Lubricant Demand

Offshore machinery does its work in extreme temperatures, high-pressure conditions, and corrosive saltwater surroundings, so the need for advanced lubricants is getting sharper, with better thermal endurance and wear protection. In practice, high-performance synthetic lubricants help extend the service life of the equipment, cut down on how often maintenance shows up, and support smoother operational efficiency.

Restraints

Volatile Petrochemical Prices

Crude oil and petrochemical feedstock prices have a direct impact on the manufacturing costs and product pricing, thus directly influencing the offshore lubricants market. A sudden rise in the cost of raw materials negatively impacts the profitability of the producer of lubricants and causes uncertainty in the price of lubricants for the offshore operators.

Stringent Environmental Regulations

Compliance is becoming a challenge for manufacturers and offshore operators due to the increasingly strict environmental controls for chemical emissions, lubricant disposal, and limits on volatile organic compounds (VOCs). Environmental standards for the regulation of lubricants call for the use of less harmful, less biodegradable lubricants, sometimes at a high added cost for production and certification.

Opportunities

Bio-based Alternatives

Environmental concerns and tougher marine sustainability regulations are providing a good opportunity for bio- and biodegradable offshore lubricants. These products help operators meet environmental standards and minimize ecological risks from spills and leakage. The rise of the use of environmentally acceptable lubricants (EALs) in the offshore drilling industry, as well as in marine vessels and subsea equipment, has led to investments by manufacturers in renewable feedstocks and sustainable formulations.

Lubricant Technology Advancements

Some interesting technology advancements in synthetic lubricant formulations, especially for Group IV and Group V base oils, are creating real growth paths in offshore use. These newer lubes deliver noticeably better oxidation resistance and thermal stability, plus longer run times than the older conventional products. Also, there's a stronger emphasis on operational efficiency, predictive maintenance, and improving equipment life, which is pushing demand for fresh lubricant technologies that are tuned for rough offshore conditions and even deeper water operations.

Segmental Insights

Product Type Insights

The Engine Oils Segment Dominated the Offshore Lubricants Market with 29% of Market Share in 2025

The engine oils segment dominated the market with the largest share of 29% in 2025, which is widely used in offshore vessels, drilling rigs, and production equipment. Offshore operations are in constant operation and demand superior lubrication to protect the engine, save fuel usage, and achieve longer drain cycles. The surge in deepwater exploration and the growing use of offshore fleets are further driving the need for durable engine lubrication solutions worldwide.

")

The greases segment held the 10% market share in 2025 and is expected to grow at the fastest CAGR of 6.8% over the forecast period. Increasing installation of offshore wind and greater maintenance needs of heavy offshore equipment are driving the growth of greases. Specialty greases offer enhanced corrosion protection, water resistance, and load-carrying ability in severe marine environments. Demand for sophisticated offshore grease formulations is still rising, driven by continued growth in subsea infrastructure and the need for turbine maintenance.

The hydraulic fluids segment held the 19% market share in 2025, as automation levels in offshore drilling rigs and systems are increasing. These fluids are used for operations under high pressure, corrosion protection, and equipment performance in marine applications. Worldwide demand for biodegradable hydraulic fluids remains robust amid the rising production of offshore infrastructure.

Offshore Lubricants Market Share, By Product Type, 2025 (%)

| By Product Type | Revenue Share, 2025 (%) |

| Engine Oils | 29% |

| Hydraulic Fluids | 19% |

| Gear Oils | 15% |

| Compressor Oils | 11% |

| Turbine Oils | 8% |

| Greases | 10% |

| Metalworking Fluids | 5% |

| Others | 3% |

Base Oil Insights

The Mineral Oil Segment Dominated the Offshore Lubricants Market with 48% of Market Share in 2025

The mineral oils segment dominated the market with the largest share of 48% in 2025. Mineral oil is the most important due to its low cost and widespread application in conventional offshore operations. Existing supply chains and compatibility with existing offshore equipment facilitate widespread adoption. In the mature oilfields, operators still favor mineral-based lubricants for their day-to-day drilling, production, and maintenance operations, where budget is a primary concern.

The synthetic oil segment held the 39% market share in 2025 and is expected to grow at the fastest CAGR of 7.2% over the forecast period. Synthetic oils are expanding in popularity because of their longer service life, greater thermal stability, and resistance to oxidation in extreme offshore conditions. The high-performance lubricants required for deep water and ultra-deep water projects are evolving and demanding greater performance under extreme pressure and temperature. Advanced synthetic lubrication technology is even more in demand worldwide due to offshore wind installations.

The bio-based oil segment held the 13% market share in 2025. As they are biodegradable, they pose less risk of pollution and comply with the standards that apply to lubricants that are acceptable to the environment. The pressure from regulatory bodies and sustainability programs for offshore drilling, subsea operations, and offshore wind power will remain as factors to drive demand for eco-friendly lubrication solutions.

Offshore Lubricants Market Share, By Base Oil, 2025 (%)

| By Base Oil | Revenue Share, 2025 (%) |

| Mineral Oil | 48% |

| Synthetic Oil | 39% |

| Bio-based Oil | 13% |

Application Insights

The Drilling Operations Segment Dominated the Offshore Lubricants Market with 32% of Market Share in 2025

The drilling operations segment dominated the market with the largest share of 32% in 2025. The biggest market share comes from drilling operations as they require constant lubricant usage across the rigs, drill strings, pumps, and heavy mechanical systems. Premium lubricants are needed to meet high pressure and extreme operating conditions in deepwater and frontier basins. Consumption of lubricants for drilling continues to grow in all offshore projects around the world.

The renewable offshore operations segment held the 7% market share in 2025 and is expected to grow at the fastest CAGR of 8.3% over the forecast period. For the dependable offshore operation of wind turbines, installation vessels, and infrastructure, long-life lubricants are needed. The government's renewable energy targets, sustainability efforts, and investments in offshore wind farms are contributing to a major increase in the demand for lubricants in this new application area.

The production operations segment held the 24% market share in 2025 because of the regular lubrication needs of FPSOs, offshore platforms, and rotating equipment. Offshore fields require more maintenance and lubricant changes as they get older. Operators focus on operation reliability, equipment uptime, and corrosion protection, and manage their lubricant usage equally across all offshore production facilities around the world.

Offshore Lubricants Market Share, By Application, 2025 (%)

| By Application | Revenue Share, 2025 (%) |

| Drilling Operations | 32% |

| Production Operations | 24% |

| Marine Support Operations | 16% |

| Subsea Equipment | 12% |

| Maintenance & Repair | 9% |

| Renewable Offshore Operations | 7% |

End User Insights

The Oil & Gas Operators Segment Dominated the Offshore Lubricants Market with 41% of Market Share in 2025

The oil & gas operators segment dominated the market with the largest share of 41% in 2025. Engines, turbines, hydraulic systems, and subsea equipment must be constantly lubricated to ensure the proper function of large offshore asset portfolios. Continued funding for deepwater exploration and efficiency gains in production drive lubricant procurement volume growth worldwide.

The offshore wind operators segment held the 10% market share in 2025 and is expected to grow at the fastest CAGR of 8.5% over the forecast period. Maintenance frequency must be reduced, and the synthetic lubricants must be high-performing enough to endure extremely harsh marine conditions to make offshore wind turbines viable. Lubricant demand in this segment is growing strongly, thanks to the support the government has provided for the development of renewable energy infrastructure and the growth of offshore wind.

The offshore drilling contractors segment held the 24% market share in 2025, because of increasing exploration drilling campaigns and the modernization of offshore drilling rig fleets. Specialized lubricants are needed for advanced drilling systems for reasons of operational reliability and to minimize downtime. As investments in offshore exploration rise and drilling activity gets extended, strong lubricant demand from drilling contractors around the world continues.

Offshore Lubricants Market Share, By End User, 2025 (%)

| By End User | Revenue Share, 2025 (%) |

| Oil & Gas Operators | 41% |

| Offshore Drilling Contractors | 24% |

| Marine Service Providers | 17% |

| Offshore Wind Operators | 10% |

| Subsea Engineering Companies | 8% |

Distribution Channel Insights

The Direct Sales Segment Dominated the Offshore Lubricants Market with 46% of Market Share in 2025

The direct sales segment dominated the market with the largest share of 46% in 2025, with the major suppliers having long-term agreements with the offshore operators and drilling companies. Bulk agreements guarantee supply reliability, technical assistance, and tailored lubricant solutions for vital operations in the offshore industry. Direct sourcing and supplier relationships continue to be the preferred approach for large-scale offshore projects and complex lubrication requirements around the world.

The OEM partnerships segment held the 15% market share in 2025 and is expected to grow at the fastest CAGR of 6.4% over the forecast period, because of equipment manufacturers' push for using certified products to ensure optimal system performance and warranty compliance. Offshore operators also appreciate OEM-recommended formulations for critical machinery reliability and efficiency. Lubricant supplier relationships with equipment manufacturers around the world are expanding yet again due to the increased automation of offshore operations, the advancement of equipment integration, and opportunities for aftermarket service.

The distributor network segment held the 31% market share in 2025, due to its role in making lubricants more readily available in offshore hubs and offshore areas. Regional Distributors offer quick delivery, local stocking, and technical support to offshore operators. First, this is driven by the ongoing expansion of oil and gas exploration efforts into the oceans, and second, by increasing logistics operations in the marine sector.

Offshore Lubricants Market Share, By Distribution Channel, 2025 (%)

| By Distribution Channel | Revenue Share, 2025 (%) |

| Direct Sales | 46% |

| Distributor Network | 31% |

| OEM Partnerships | 15% |

| Online & E-Procurement Platforms | 8% |

Offshore Water Depth Insights

The Shallow Water Segment Dominated the Offshore Lubricants Market with 44% of Market Share in 2025

The shallow water segment dominated the market with the largest share of 44% in 2025, as the market is dominated by existing offshore infrastructure and the stable production activity in the mature oilfields. Drilling rigs, production, and marine support systems continue to consume lubricants due to reduced operating and maintenance costs. In shallow water areas around the world, steady demand for lubricants keeps going for long-term offshore field operations.

The ultra-deepwater segment held the 22% market share in 2025 and is expected to grow at the fastest CAGR of 7.4% over the forecast period, as exploration continues to grow in these hard-to-explore offshore reservoirs. The lubricants used in these operations must be very special and be able to operate under extreme pressure and temperature. Lubricant demand is continuing to rise in the offshore segment at an even higher pace than in the past, thanks to technological developments in offshore drilling and investment in frontier deepwater reserves.

The deepwater segment held the 34% market share in 2025. With the expansion of energy companies in the search for offshore reserves in complex marine environments, deepwater operations account for the second-largest share. Lubricant usage is expected to remain steady in global offshore operations as the deepwater production projects continue to expand, and offshore investment increases.

Offshore Lubricants Market Share, By Offshore Water Depth, 2025 (%)

| By Offshore Water Depth | Revenue Share, 2025 (%) |

| Direct Sales | 46% |

| Distributor Network | 31% |

| OEM Partnerships | 15% |

| Online & E-Procurement Platforms | 8% |

Regional Insights

How did the Asia Pacific dominate the Offshore Lubricants Market in 2025?

Asia Pacific Offshore Lubricants market size was estimated at USD 1.22 billion in 2025 and is projected to reach USD 2.22 billion by 2035, growing at a CAGR of 6.17% from 2026 to 2035.Asia Pacific dominated the market by holding 31% share in 2025 and is expected to grow at the fastest with a CAGR of 7.1% during the forecast period, as the offshore exploration activities in China, India, and Southeast Asia are high. Demand for lubricants remains on the rise with the growth of offshore wind investments, increasing marine infrastructure development, and government support for domestic energy production. Rapid industrialization and growing energy development offshore further consolidate the growth of regional markets.

India Offshore Lubricants Market Growth Trends

The offshore lubricants market in India is growing steadily with the rise in offshore exploration activities. Investment in offshore wind energy and growing marine logistics activities are driving increased demand for lubricants, and government efforts to support domestic energy production are also driving growth. The use of synthetic lubricants and biodegradable lubricants is increasing, which will further support the market growth over the years.

North America Offshore Lubricants Market Growth Trends

North America held the 27% market share in 2025 and is expected to experience notable growth in the market with 5.3% CAGR during the forecast period. Market growth is being supported by deepwater exploration projects, modernization of the offshore fleet, and growth in investments in advanced lubrication technologies. Equipment reliability, production efficiency, and predictive maintenance strategies are still high priorities for offshore operators across offshore assets and marine operations.

")

U.S. Offshore Lubricants Market Growth Trends

Offshore drilling and production activities are strong, which propels the United States offshore lubricants market. Market expansion is helped by increasing deepwater exploration, modernization of the offshore fleet, and demand for high-performing synthetic lubricants. The trend toward sustainable offshore lubrication solutions is also being driven by advanced predictive maintenance technologies and the increasingly tight regulations imposed on the environment.

Recent Developments

- In May 2026, Motul launched the IPONE brand in India, targeting the premium motorcycle engine oil market. The range features four tiers named after judo belts, with the Black Belt – Racing Range prioritizing protection for high-performance riding.(Source: www.team-bhp.com)

- In December 2025, Renault Group partnered with Castrol and launched the co-branded Renault Castrol GTX range using Re-Refined Base Oils, becoming the first manufacturer to implement this technology in RN17 (5W-30) for over 50% of its European vehicles.(Source: media.renaultgroup.com)

Top Companies in the Market

- Exxon Mobil

- Shell

- Aegean Marine Petroleum

- Idemitsu Kosan Co. Ltd.

- Chevron Corporation

- Gulf Oil Corporation

- BP Plc

- Total S.A.

- Fuchs

Segment Covered in the Report

By Product Type

- Engine Oils

- Trunk Piston Engine Oil

- Crosshead Engine Oil

- Gas Engine Oil

- Hydraulic Fluids

- Mineral-based Hydraulic Fluids

- Synthetic Hydraulic Fluids

- Biodegradable Hydraulic Fluids

- Gear Oils

- Industrial Gear Oil

- Extreme Pressure Gear Oil

- Compressor Oils

- Rotary Compressor Oil

- Reciprocating Compressor Oil

- Turbine Oils

- Steam Turbine Oil

- Gas Turbine Oil

- Greases

- Lithium Grease

- Calcium Sulfonate Grease

- Aluminum Complex Grease

- Metalworking Fluids

- Cutting Fluids

- Corrosion Preventive Fluids

- Others

- Wire Rope Lubricants

- Heat Transfer Fluids

By Base Oil

- Mineral Oil

- Synthetic Oil

- Polyalphaolefin (PAO)

- Ester-based

- Polyalkylene Glycol (PAG)

- Bio-based Oil

By Application

- Drilling Operations

- Offshore Jack-up Rigs

- Drillships

- Semi-submersible Rigs

- Production Operations

- Floating Production Storage and Offloading (FPSO)

- Offshore Platforms

- Marine Support Operations

- Anchor Handling Tug Supply Vessels

- Platform Supply Vessels

- Offshore Support Vessels

- Subsea Equipment

- Blowout Preventers

- Subsea Trees

- Control Systems

- Maintenance & Repair

- Equipment Servicing

- Corrosion Protection

- Renewable Offshore Operations

- Offshore Wind Installation Vessels

- Offshore Wind Turbine Systems

By End User

- Oil & Gas Operators

- National Oil Companies

- International Oil Companies

- Offshore Drilling Contractors

- Marine Service Providers

- Offshore Wind Operators

- Subsea Engineering Companies

By Distribution Channel

- Direct Sales

- Distributor Network

- OEM Partnerships

- Online & E-Procurement Platforms

By Offshore Water Depth

- Shallow Water

- Deepwater

- Ultra-Deepwater

By Region

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Asia Pacific

- China

- India

- Japan

- South Korea

- Latin America

- Brazil

- Argentina

- Middle East & Africa

- Saudi Arabia

- South Africa

FAQ's

Select User License to Buy

Figures (4)