Content

What is the Floor Adhesives Market Size and Share?

The global floor adhesives market size was valued at USD 9.11 billion in 2025, is estimated to reach USD 9.65 billion in 2026, and is projected to reach USD 16.24 billion by 2035, exhibiting a compound annual growth rate (CAGR) of 5.95% over the forecast period from 2026 to 2035.Asia Pacific dominated the floor adhesives market with the largest revenue share of 34% in 2025 and is expected to grow at the fastest CAGR of 6.09% during the forecast period. In terms of volume, the floor adhesives market is projected to grow from 4.19 million tons in 2025 to 6.99 million tons by 2035. growing at a CAGR of 5.25% from 2026 to 2035.The growth of the market is driven by the construction and renovation activities, demand for eco-friendly products, and growing consumer preference, which fuel the growth. The government initiatives and advanced technology align with the company's pathway, like Pidilite and Saint-Gobain Weber, which support the growth of the market, as per the latest reports.

Market Highlights

- By region, Asia Pacific dominated the market with a share of 34% in 2025 and is expected to sustain its position while growing with a CAGR of 7.20% in the forecast period. Benefits from infrastructure development

- By region, Europe held 28% market share in 2025. Maintains a strong flooring industry.

- By resin, the acrylic segment dominated the market with 36% share in 2025. Provides strong bonding performance.

- By resin, the polyurethane segment held 26% market share in 2025 and is expected to have the fastest growth with a CAGR of 7.20% in the forecast period. Supports premium flooring applications.

- By application, the resilient flooring segment dominated the market with 31% share in 2025. Gains demand from vinyl flooring growth.

- By application, the wooden flooring segment held 29% market share in 2025 and is expected to have the fastest growth with a CAGR of 6.80% in the forecast period. Expands through premium housing projects.

- By end-use, the commercial segment dominated the market with 45% share in 2025. Benefits from office and retail construction.

- By end-use, the industrial segment held 17% market share in 2025 and is expected to have the fastest growth with a CAGR of 6.50% in the forecast period. Requires heavy-duty flooring systems.

Quick Stats at a Glance

- Market Estimated Size (2025): USD 9.11 Billion | CAGR (2026–2035): 5.95%

- Market Projected Size (2035): USD 16.24 Billion

- Asia Pacific: largest Market Revenue Share of 34% in 2025|USD 3.10 Billion

- Market Estimated Volume (2025): 4.19 Million Tons| Volume CAGR (2026–2035): 5.25%

- Market Projected Volume (2035):4.19 Million Tons

- Market Pricing (2025):

- Average Manufacturing Price (2025):USD 1,820/Ton

- Average Selling Price (2025): USD 2,440/Ton

- Pricing CAGR (2026–2035): 2.15%

The global floor adhesives market is vital to modern construction and remodeling. It plays a key role by ensuring structural stability, speeding up installation processes, and promoting eco-friendly solutions. Driven by increasing urbanization worldwide and rising demand in commercial and residential sectors, adhesives are used to bond materials such as vinyl, carpet, ceramic tiles, and hardwood to subfloors. High-performance adhesives are essential for evenly distributing weight, handling heavy foot traffic, and resisting moisture damage under environmental stress.

It ensures the structural integrity, safety, and longevity of flooring across residential, commercial, and industrial spaces while driving trends toward sustainability. Rising global housing development and smart city infrastructure projects continually propel the need for reliable, rapid-installation subfloor bonding.

For Instances,

- MAPEI S.p.A. supplies tile adhesives for residential and commercial flooring installations.

These adhesives provide strong bonding, moisture resistance, and durability for ceramic and stone tiles. - Henkel is one of the most trusted of all water-based adhesive manufacturers.

The products improve installation efficiency, flexibility, and long-term floor stability.

The DIY home improvement trend also boosts demand for easy-to-use, reliable adhesive systems to achieve professional results. Acrylic and polyurethane resins dominate due to their quick curing, strong bonding, and versatility. The market remains highly competitive, led by global giants like Henkel, 3M, and H.B. Fuller, with regional companies like Pidilite Industries leading in India.

Global Investment Flow for Floor Adhesives 2026

- Investment focuses heavily on supply-chain localization and domestic production plants to bypass import dependencies. Represents the growing demand for resilient surfaces and luxury vinyl tile installations.

- Capitalize heavily on renovation and refurbishment, prioritizing strict low-VOC standards and single-component wood adhesive advancements across Asia Pacific, North America, Europe and Latin America.

- The market is experiencing robust merger-and-acquisition activity, localized infrastructure supply-chain investments, and a major shift toward sustainable, low-emission, and bio-based resin formulations.

- For instance, H.B. Fuller completes a $20 million phased investment in India, starting a business office in Pune and a state-of-the-art R&D center at its existing 24,000-metric-tons-per-annum manufacturing plant in Shirwal.

Market Growth Trends:

- Technological Advancements: Manufacturers are actively investing in R&D to develop adhesives with quicker curing times, better bonding strengths, and moisture-mitigating properties.

- Resilient Flooring & Luxury Vinyl Tile: Increasing consumer preference for LVT & resilient flooring is skyrocketing the demand for specialized glue-down adhesives which provides moisture resistance and durability.

- Sustainable & Low-VOC Formulations: Tightening environmental regulations in regions have driven a massive shift from traditional solvent-based adhesives to eco-friendly, water-based, and bio-based alternatives.

Floor Adhesives Market Report Scope

| Report Attribute | Details |

| Market Size and Volume in 2026 | USD 9.65 Billion / 4.41 Million Tons |

| Revenue Forecast in 2035 | USD 16.24 Billion / 6.99 Million Tons |

| Growth Rate | CAGR of 5.95% |

| Base year for estimation | 2025 |

| Forecast period | 2025-2035 |

| Segments covered | By Resin, By Application, By End-Use, By Regions |

| Dominat Region | Asia Pacific |

| Key companies profiled | Sika AG, MAPEI, H.B. Fuller, 3M Company, Henkel, Bison, Bostik, Pro Flooring, Cattie Adhesives, DAP Global Inc., Dow, Forbo, H.B. Fuller, Henkel Adhesives, Jowat Adhesives, Magicrete, Mapei, Pidilite, Saint-Gobain Weber, Sika Group, WW Henry |

Key Technological Shifts in the Floor Adhesives Market with AI-Driven Solutions

The floor adhesives market is fundamentally evolving to meet demands for sustainability, installation efficiency, and superior durability. Key shifts include the widespread adoption of low-VOC/solvent-free formulas to improve indoor air quality, the rise of moisture-resistant technologies for concrete subfloors, and the popularity of pressure-sensitive adhesives for modular flooring. Artificial intelligence and machine learning are fundamentally reshaping Industry 4.0 shifts by cutting formulation development cycles by up to 70% and balancing mechanical strength with environmental compliance.

Floor Adhesives Market Regulatory Landscape

| Country / Region | Regulatory Body | Key Regulations | Focus Areas | Notable Notes |

| United States | Environmental Protection Agency (EPA); Occupational Safety and Health Administration (OSHA) | Clean Air Act; VOC Emission Standards; OSHA Chemical Safety Standards | Low-VOC adhesives, indoor air quality | The U.S. promotes environmentally friendly floor adhesives with increasing adoption of water-based and solvent-free technologies. |

| European Union | European Chemicals Agency (ECHA); European Commission | REACH Regulation; Construction Products Regulation (CPR); EU Green Deal | Chemical safety, sustainable construction | Europe strongly regulates VOC emissions and hazardous chemicals in flooring adhesive formulations. |

| China | Ministry of Ecology and Environment (MEE); Ministry of Housing and Urban-Rural Development (MOHURD) | Green Building Standards; VOC Emission Regulations | Sustainable construction materials, low-emission adhesives | China is expanding adoption of eco-friendly flooring adhesives in residential and commercial construction projects. |

| India | Bureau of Indian Standards (BIS); Central Pollution Control Board (CPCB) | BIS Adhesive Standards; Environmental Protection Rules | Construction quality, sustainable adhesives | India is witnessing increasing demand for low-VOC floor adhesives driven by urbanization and infrastructure growth. |

| Japan | Ministry of Economy, Trade and Industry (METI) | Chemical Substances Control Law (CSCL); Indoor Air Quality Standards | High-performance adhesives, indoor environmental safety | Japan focuses on advanced low-emission adhesive technologies for premium flooring applications. |

| Germany | Federal Environment Agency (UBA) | Blue Angel Eco-label Standards; REACH Compliance | Eco-friendly flooring systems | Germany is a major market for sustainable flooring adhesives and green building materials. |

Supply Chain Analysis of the Floor Adhesives Market

Adhesive Production & Formulation

- Floor adhesive production involves compounding polymer emulsions or cementitious bases using automated dry-mix systems. Floor adhesives are produced through the formulation of acrylic, epoxy, polyurethane, and vinyl-based resins combined with additives to provide strong bonding, moisture resistance, and durability for flooring installations.

- The manufacturing process differs based on whether the adhesive is a dry powder or a liquid paste. Production requires precision mixing tanks, tried-and-true ratios, and strict raw material sequencing.

Henkel AG & Co. KGaA is the first global adhesive manufacturer, renowned for heavy-duty commercial epoxy and sub-floor solutions.

- Key Players: Henkel, Sika, MAPEI, H.B. Fuller.

Quality Testing & Certification

- Floor adhesives must comply with standards for bonding strength, VOC emissions, moisture resistance, durability, and indoor air quality safety before commercial use. Testing laboratories measure tensile adhesion (≥ 1.0 MPa) under heat aging and water immersion to ensure structural reliability.

- In India, mandatory regulations require specific BIS Certification for Adhesives (IS 15477:2019) to guarantee structural safety and prevent installation failures.

- FloorScore Certifies low VOC (Volatile Organic Compound) emissions for indoor air quality, whereas Intertek Flooring Services performs comprehensive physical properties testing for wood, vinyl, and carpet flooring underlayments.

- Key Authorities & Standards: International Organization for Standardization, ASTM International, European Chemicals Agency, U.S. Environmental Protection Agency.

Distribution to End-Use Industries

- Floor adhesives are supplied to residential and commercial construction projects, flooring manufacturers, renovation contractors, industrial facilities, and infrastructure development sectors. Distribution channels heavily prioritize direct-to-site supply for large projects and retail/distributor networks for DIY renovations.

- Targets factories, warehouses, and production units. Products require heavy-duty chemical and machinery resistance. Distribution occurs through specialized industrial distributors or directly from leading manufacturers like Henkel.

- Key Suppliers: Henkel, Sika, MAPEI.

Floor Adhesives Market Dynamics

| Drivers | Restrains | Opportunities |

| Eco-Friendly & Low-VOC Formulations:Stringent health, safety, and environmental mandates have shifted consumer and builder preferences away from solvent-borne systems toward water-borne, non-toxic adhesives that ensure safer indoor air quality. | Volatile Raw Material Prices:Supply chain disruptions and currency fluctuations directly inflate production costs, squeezing manufacturer profit margins and forcing contractors to delay projects awaiting price relief. | Residential Remodeling & DIY Culture:Rising disposable incomes are fueling residential renovation trends. Homeowners frequently upgrade to hardwood, ceramic, and luxury vinyl tiles, which require specialized adhesives. |

| Renovation & Remodeling:Increased disposable income and a cultural shift toward upgrading, refinishing, and modernizing older residential and commercial buildings are major catalysts. | Strict Environmental Regulations:Regulatory bodies globally enforce rigorous constraints on Volatile Organic Compound emissions. Compliance requires shifts toward water-based or bio-attributed technologies. | Market Consolidation & Diversification:Leading global players such as Henkel AG & Co. KGaA, Sika AG, Pidilite Industries Limited, and H.B. Fuller Company are strategically leveraging direct e-commerce and dealership networks to capture regional momentum. |

| Material Versatility & Ease of Application:Adhesives that bond seamlessly across diverse substrates while offering swift curing times and reduced labor downtime are highly favored in fast-paced construction. | Moisture and Subfloor Sensitivity:Certain advanced formulations are highly sensitive to temperature and humidity. Poor subfloor conditions can cause bond failures. The need for extra primers or moisture barriers inflates overall project costs. | Technological Advancements in Chemistry:R&D efforts focus on high-performance solutions like polyurethane & acrylic systems, that provides rapid curing under UV light & excellent heat or water resistance. |

Segmental Insights

Resin Insights

The acrylic segment dominated the market with 36% share in 2025, driven by rapid urbanization, infrastructure development, and a shift toward eco-friendly low-VOC materials. The segment is expanding rapidly due to rising urbanization, eco-friendly low-VOC regulations, and booming luxury vinyl tile installations. Quick-drying properties significantly reduce project timelines and labor costs for contractors. his makes them highly preferred for strict green building standards and indoor-sensitive environments like schools and hospitals.

")

The polyurethane segment held 26% market share in 2025 and is expected to have the fastest growth with a CAGR of 7.20% in the forecast period. This growth is heavily driven by increasing construction, urbanization, and a strong shift toward high-performance, durable, and moisture-resistant bonding solutions. Polyurethane bonds remain highly elastic, preventing cupping, warping, or squeaking in humid environments. Surging installation of demanding materials like luxury vinyl tiles and engineered hardwood requires resilient, moisture-resistant bonding. These factors further propelled the growth of the market.

Floor Adhesives Market Share, By Resin, 2025 (%)

| By Resin | Revenue Share, 2025 (%) |

| Acrylic | 36% |

| Polyvinyl Acetate | 22% |

| Polyurethane | 26% |

| Conventional Phenolic (Alkyd/Epoxy) | 10% |

| Other Resin | 6% |

Application Insights

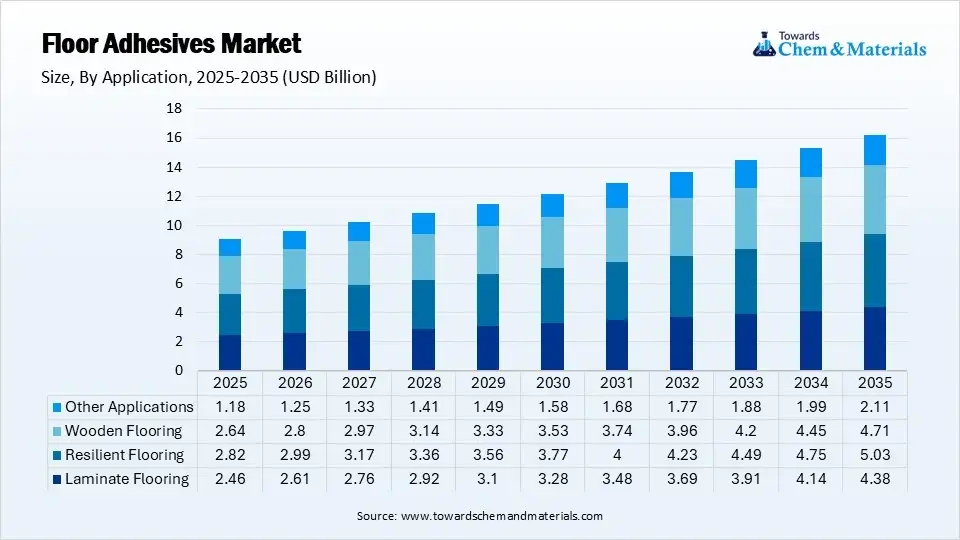

The resilient flooring segment dominated the market with 31% share in 2025, due to booming demand for waterproof, durable, and low-maintenance surfaces in residential and commercial spaces. Healthcare and education renovations specify modular solutions like carpet tiles and vinyl planks, driving the need for releasable adhesives that allow easy swaps without subfloor damage, alongside epoxy formulations with antimicrobial additives. Aging infrastructure and commercial renovations across retail, healthcare, and hospitality drive continuous replacement cycles.

")

The wooden flooring segment held 29% market share in 2025 and is expected to have the fastest growth with a CAGR of 6.80% in the forecast period. Rising disposable incomes, booming construction, and increased home renovations drive the wooden flooring segment's expansion. Premium aesthetics and property value boosts push demand. The rise of multilayer and engineered floating floor systems requires specialized bonding. Strenuous green building regulations and consumer health awareness are shifting the Flooring Adhesives Market toward solvent-free, water-free, and ultra-low-emission formulations.

Floor Adhesives Market Share,By Application, 2025 (%)

| By Application | Revenue Share, 2025 (%) |

| Laminate Flooring | 27% |

| Resilient Flooring | 31% |

| Wooden Flooring | 29% |

| Other Applications | 13% |

End-Use Insights

The commercial segment dominated the market with 45% share in 2025. Growth is propelled by rapid urbanization, office remodeling, retail expansion, and post-pandemic renovations requiring high-performance adhesives that withstand heavy foot traffic. Commercial spaces like corporate offices, shopping malls, and hospitality venues need flooring to withstand massive daily wear. Installers heavily rely on robust bonding technologies such as Epoxy Adhesives for extreme durability and chemical resistance.

The industrial segment held 17% market share in 2025 and is expected to have the fastest growth with a CAGR of 6.50% in the forecast period, growing rapidly due to rising manufacturing infrastructure, stringent regulatory safety standards, and heavy-duty operational demands requiring fast-curing, chemical-resistant bonding solutions that minimize operational downtime. Rising utilization of impermeable, chemically resistant epoxy containment flooring ensures structural integrity and prevents hazardous seepage during chemical spills which increases the demand for the market.

Floor Adhesives Market Share,By End-use, 2025 (%)

| By End-use | Revenue Share, 2025 (%) |

| Commercial | 45% |

| Residential | 38% |

| Industrial | 17% |

Regional Analysis

How did Asia Pacific dominate the Floor Adhesives Market in 2025?

The Asia Pacific floor adhesives market size was estimated at USD 3.10 billion in 2025 and is projected to reach USD 5.60 billion by 2035, growing at a CAGR of 6.09% from 2026 to 2035.Asia Pacific dominated the market with a share of 34% in 2025 and is expected to sustain its position while growing with a CAGR of 7.20% in the forecast period. The growth of the market is driven by rapid urbanization and the growing demand for flooring solutions. The increasing disposable incomes of the middle class facilitated the expansion of home improvement projects, fueling the growth. Government initiatives promoting infrastructure development further reinforced the demand for flooring adhesives.

India

India

- Consumers and regulatory bodies are increasingly conscious of the environmental impact of their choices, leading to a surge in demand for adhesives with lower Volatile Organic Compounds (VOC) emissions. This shift towards eco-friendly products is driving the market.

- The ongoing evolution of technology and shifting market dynamics are continuously driving the floor adhesive industry. Innovations in adhesive technology are ensuring that adhesives meet the demands of various applications, including commercial and residential settings.

China

- China's continuous urbanization push and immense state-level construction spending drive flooring installations.

Strict government emission caps, such as GB 33372-2020, limit volatile organic compounds. This shifts market preference toward eco-friendly, water-based, and acrylic formulations. - While Tier-1 cities remain foundational, rapid commercial and residential development in emerging Tier-2 and Tier-3 cities provides a fresh wave of consumption demand.

Japan

- Stringent government policies like the Air Pollution Control Act force manufacturers away from solvent-based glues, accelerating the shift toward water-based, eco-friendly adhesive formulations.

- Modern bonding techniques provide enhanced durability, moisture resistance, and heavy-load bearing capacities, aligning with high-end luxury home builds and commercial spaces.

Europe Floor Adhesives Market Growth Factor

The Europe floor adhesives market size was estimated at USD 2.55 billion in 2025 and is projected to reach USD 4.63 billion by 2035, growing at a CAGR of 6.15% from 2026 to 2035.Europe held the market share of 28% in 2025. Increasing construction activities and urban development are driving the demand for resilient flooring materials and high-performance adhesives, fueling the growth of the market. Rapid urbanization and rising demand for modern interior designs are expanding the use of flooring adhesives in both residential and commercial projects. The regulatory shift and eco-friendly formulations are shaping product innovation in Europe, fueling further growth of the market.

Germany

- Stringent European Union & domestic environmental mandates limit Volatile Organic Compounds. This drives a major inclination toward water-based, sustainable, and solvent-free adhesive technologies.

- Rising consumer disposable income and living standards have increased the uptake of luxury vinyl tiles, modular carpet tiles, and engineered wood. These sophisticated materials require advanced, high-performance bonding agents.

Italy

- Tightening European Union regulations regarding Volatile Organic Compounds and REACH diisocyanate rules compel a shift toward water-borne and silane-terminated systems.

- R&D investments by industry leaders like Henkel have yielded formulations with faster curing times and superior durability.

France

- The France floor adhesives market is primarily driven by a robust renovation-led construction rebound and energy-retrofit pipelines. The broader French adhesives sector, alongside specific flooring adhesive valuations, reflects strong market momentum.

- Stringent European mandates like REACH and RE2020 are accelerating the shift toward eco-friendly water-borne and bio-based adhesive platforms.

North America Floor Adhesives Market Growth Factor

The North America floor adhesives market size was estimated at USD 2.28 billion in 2025 and is projected to reach USD 4.14 billion by 2035, growing at a CAGR of 6.15% from 2026 to 2035.North America held the market share of 25% in 2025, driven by robust construction and renovation activity, strict environmental regulations favoring low-VOC water-based formulations, and a strong consumer preference for resilient flooring like luxury vinyl tiles (LVT). The massive commercial real estate and residential construction base in the U.S. and Canada heavily boosts demand. Growing middle-class populations and rising disposable incomes have further accelerated residential remodeling.

U.S.

- Sustained investments in residential housing and commercial infrastructure, alongside trends in retrofitting and modernizing older buildings, directly boost adhesive consumption.

- Tightening environmental laws like stricter VOC limits in North America are forcing manufacturers to pivot toward water-borne, bio-based, and eco-friendly systems, driving premium product sales

Canada

- Strict federal volatile organic compound limits are compelling manufacturers like Henkel Canada Corp. to innovate sustainable, low-emission, and fast-curing water-based or acrylic adhesives.

- Increased residential & commercial infrastructure projects, with the innovations in mass-timber construction, heavily accelerate domestic demand.

Latin America Floor Adhesives Market Growth Factor

The Latin America floor adhesives market size was estimated at USD 0.73 billion in 2025 and is projected to reach USD 1.38 billion by 2035, growing at a CAGR of 6.58% from 2026 to 2035.Latin America held the market share of 8% in 2025, driven by expanding residential and commercial construction, rising urbanization, and increased renovation activities. Ongoing development in housing and infrastructure upgrades, particularly in major economies like Brazil and Mexico, fuels the need for reliable bonding solutions. A growing middle class and rising disposable incomes are increasing the adoption of modern flooring materials, including vinyl tiles, ceramics, and laminates.

")

Brazil

- Tighter solvent-emission caps by ANVISA are pushing formulators away from traditional solvents and toward water-borne, bio-based, and low-VOC adhesives.

- Industry leaders like Mapei S.p.A., Sika AG, and Henkel AG & Co. KGaA are introducing rapid-curing, high-moisture-resistant formulations that minimize labor costs and accelerate project timelines.

Argentina

- Growth in Latin American infrastructure and residential building projects directly scales up the need for advanced bonding and flooring solutions. Increased middle-class housing developments drive the demand for high-performance tile, stone, and resilient flooring.

- There is a strong industry shift away from solvent-borne products toward water-based and acrylic formulations. Stricter limits on emissions mandate the use of low-VOC adhesives in modern buildings.

Middle East and Africa Floor Adhesives Market Growth Factor

The Middle East and Africa floor adhesives market size was estimated at USD 0.46 billion in 2025 and is projected to reach USD 0.89 billion by 2035, growing at a CAGR of 6.82% from 2026 to 2035.The Middle East and Africa held the market share of 5% in 2025. This growth is propelled by mega-infrastructure projects, urban expansion, and stringent sustainability mandates across the region. Rapid urbanization and large-scale government initiatives such as Saudi Vision 2030 and commercial developments in the UAE are heavily driving building activities. This directly fuels the consumption of flooring materials and their corresponding adhesives.

Floor Adhesives Market Share, By Regional, 2025 (%)

| Regional | Revenue Share, 2025 (%) |

| North America | 25% |

| Europe | 28% |

| Asia-Pacific | 34% |

| Latin America | 8% |

| Middle East & Africa | 5% |

Saudi Arabia

Vision 2030 initiatives, including giga-projects like NEOM, the Red Sea developments, and extensive residential expansions in Riyadh, are driving massive demand for resilient flooring and advanced installation materials.

The implementation of strict regulations by the Saudi Standards, Metrology, and Quality Organization mandates the reduction of VOCs. This has shifted the market toward eco-friendly, water-borne, and green adhesive solutions.

UAE

- Ongoing large-scale commercial, residential, and mixed-use developments in Dubai and Abu Dhabi drive immense flooring material consumption.

- UAE's stringent sustainability visions, such as the Estidama Pearl Rating System and Dubai Green Building Regulations, are shifting contractors away from solvent-based adhesives.

Competitive Analysis

- The competition in the industry is shifting towards high-performance, low-VOC (Volatile Organic Compounds) bonding systems. The industry is moderately concentrated, driven by megacities urbanization, strict eco-regulations.

- Floor adhesives are evaluated on bond strength, elasticity, and moisture resistance. Leading global manufacturers like Henkel GmbH & Co. KGaA produce distinct adhesive formulations tailored to specific flooring materials, balancing mechanical loads with workability and environmental regulations.

- Driven by a massive boom in local real estate, commercial infrastructure, and residential construction, India's industrial and tile adhesive sectors are expanding rapidly. Major global & domestic manufacturers dominate this landscape, balancing traditional cementitious formulas with advanced, low-emission elastic polymers such as Sika India Pvt. Ltd., Pidilite Industries Limited, Henkel Adhesive Technologies India Pvt. Ltd., Bostik India Pvt. Ltd., Jyoti Resins & Adhesives, H.B. Fuller India, 3M India Ltd.

Recent Developments

- In April 2026, SikaBond®-5700 is the latest addition to Sika's resilient adhesive portfolio, following the 2025 rollouts of SikaBond-5800 and SikaBond-5900. Engineered as a high-performance, problem-solving solution under the SikaBond umbrella, this versatile glue is formulated for both residential and commercial interior installations.(Source: www.floorcoveringweekly.com)

- In April 2025, Trinseo, a global leader in specialty material solutions, announced the commercial launch of LIGOS™ A 9210. This advanced all-acrylic latex binder is engineered to elevate the adhesion, durability, and processing efficiency of flexible flooring adhesives. The introduction expands Trinseo’s Coatings, Adhesives, Sealants, and Elastomers (CASE) portfolio to meet the shifting demands of the building and construction industries.(Source: www.chemanalyst.com)

- In February 2026, TotalWorx Accessories, the dedicated installation accessories division of Shaw Industries, officially introduced its high-performance RockHold resilient flooring adhesive. Positioned as a versatile addition to its LokWorx locking systems catalog, the product functions as a single source solution designed to replace multiple specialty adhesives on a single job site.(Source: www.fcnews.net)

Top players in the Floor Adhesives Market & Their Offerings:

- Sika AG: Specializes in high-performance polyurethane and epoxy flooring adhesives prioritizing durability, movement accommodation, and chemical resistance.

- MAPEI: Offers an extensive range of eco-sustainable, technologically advanced adhesives for ceramic, resilient, and wood installations.

- H.B. Fuller: Provides permanently flexible overlays and sub-flooring solutions designed to accommodate movement and ensure long-term structural integrity.

- 3M Company: Focuses on heavy-duty liquid adhesives and tape systems designed for adhering rigid floor coverings and specialty subflooring.

- Henkel: Delivers robust structural adhesives for residential, commercial, and specialty sport/transportation flooring applications.

Other Top Players Are

- Bison

- Bostik Pro Flooring

- Cattie Adhesives

- DAP Global Inc.

- Dow

- Forbo

- H.B. Fuller

- Henkel Adhesives

- Jowat Adhesives

- Magicrete

- Mapei

- Pidilite

- Saint-Gobain Weber

- Sika Group

- WW Henry

Segments Covered

By Resin

- Acrylic

- Water-Based Acrylic

- Solvent-Based Acrylic

- Pressure-Sensitive Acrylic

- Polyvinyl Acetate

- Standard PVA

- Cross-Linked PVA

- Modified PVA

- Polyurethane

- One-Component Polyurethane

- Two-Component Polyurethane

- Moisture-Cure Polyurethane

- Conventional Phenolic (Alkyd/Epoxy)

- Alkyd-Based

- Epoxy-Based

- Modified Phenolic Systems

- Other Resin

- Silicone-Based

- Rubber-Based

- Hybrid Resin Systems

By Application

- Laminate Flooring

- Residential Laminate Installation

- Commercial Laminate Installation

- Resilient Flooring

- Vinyl Flooring

- Linoleum Flooring

- Rubber Flooring

- Wooden Flooring

- Solid Wood Flooring

- Engineered Wood Flooring

- Parquet Flooring

- Other Applications

- Carpet Tiles

- Sports Flooring

- Specialty Flooring

By End-Use

- Commercial

- Offices

- Retail Facilities

- Hospitality Facilities

- Educational Institutions

- Residential

- New Residential Construction

- Renovation & Remodeling

- Industrial

- Manufacturing Facilities

- Warehouses

- Logistics Centers

By Regional

- North America

- Europe

- Asia Pacific

- Middle East & Africa

- South America

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

FAQ's

Select User License to Buy

Figures (7)