Content

What is the Thermal Interface Materials Market Size and Share?

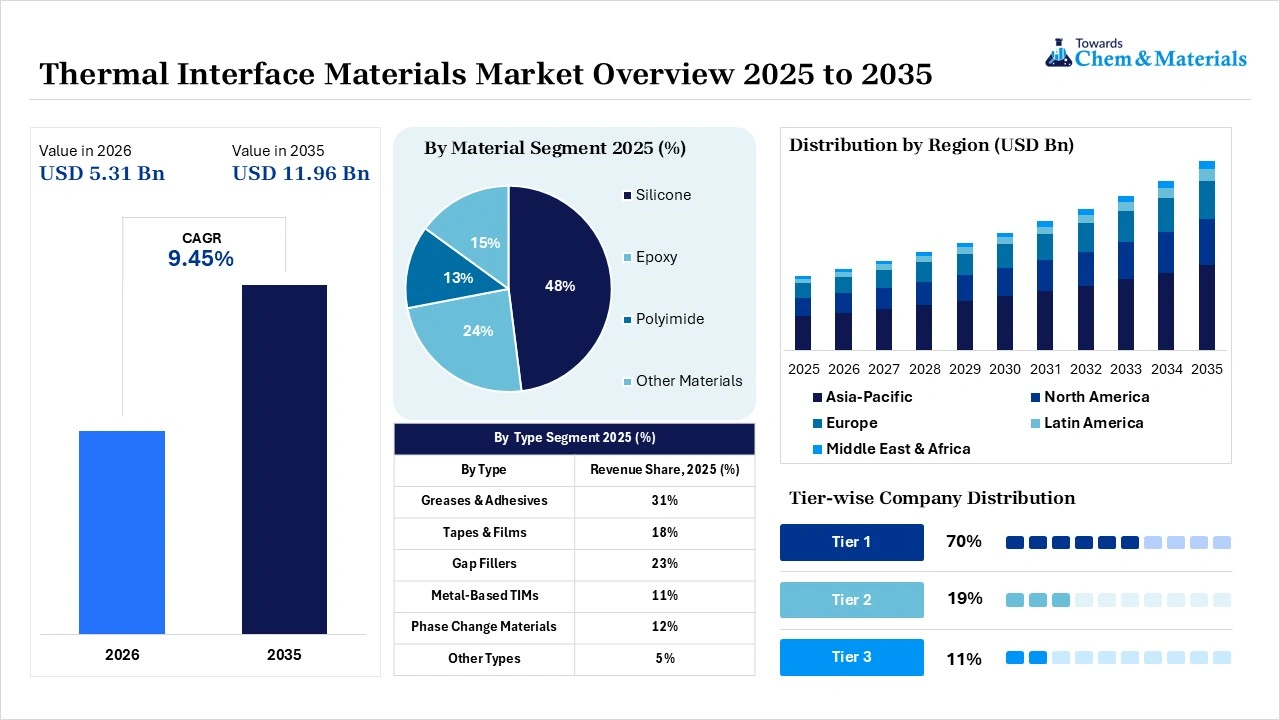

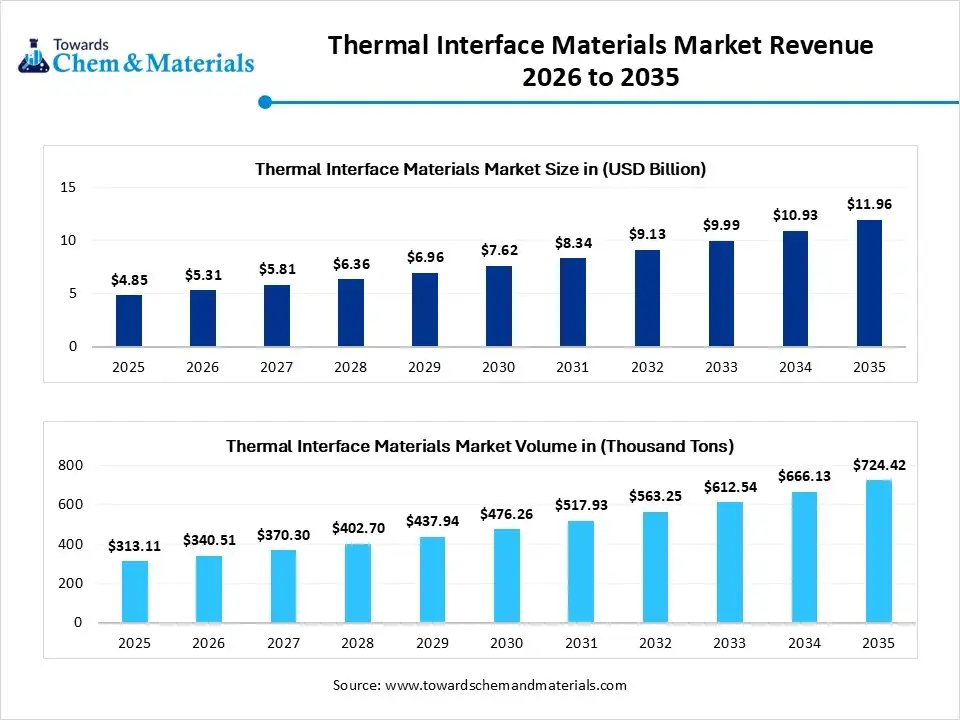

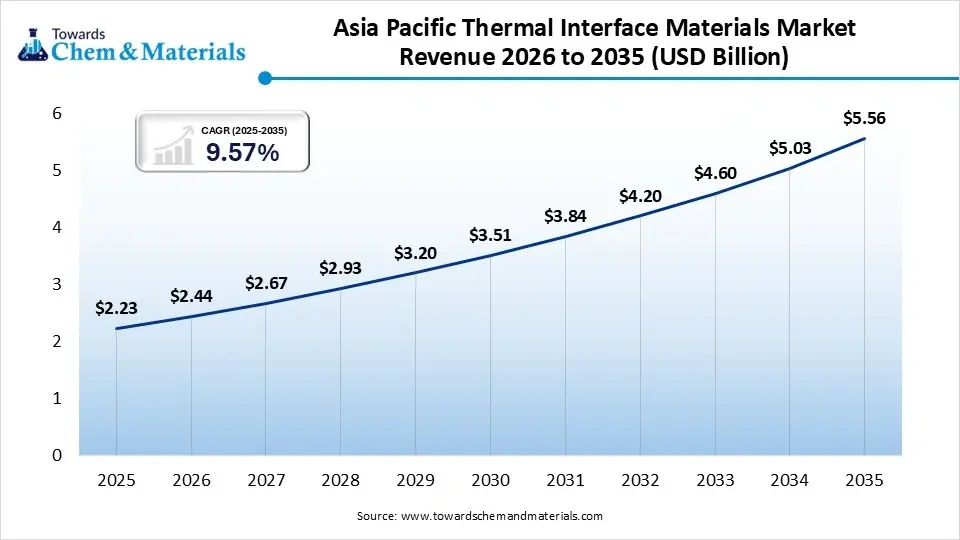

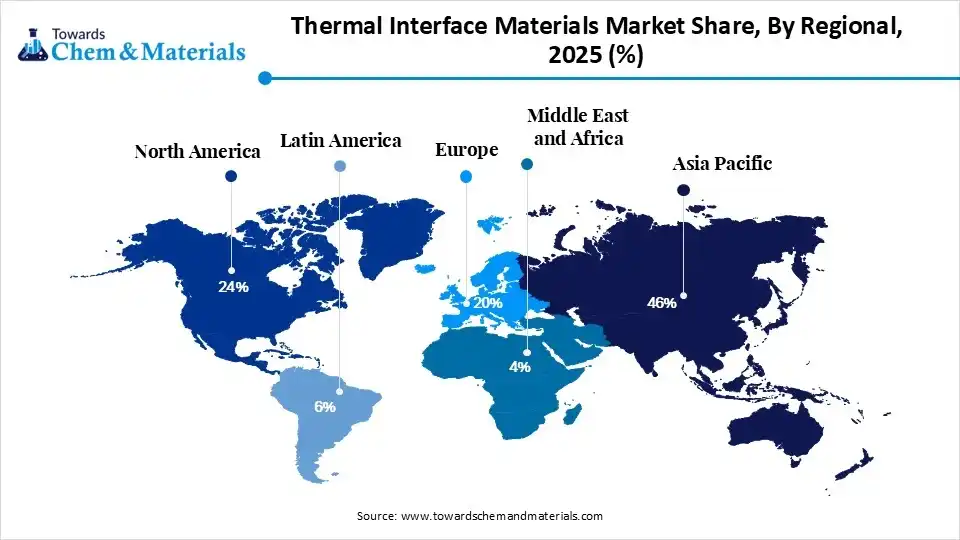

The thermal interface materials market size was valued at USD 4.85 billion in 2025, is estimated to reach USD 5.31 billion in 2026, and is projected to reach USD 11.96 billion by 2035, exhibiting a compound annual growth rate (CAGR) of 9.45% over the forecast period from 2026 to 2035.Asia Pacific dominated the thermal interface materials market with the largest revenue share of 46% in 2025 and is expected to grow at the fastest CAGR of 9.57% during the forecast period. In terms of volume, the thermal interface materials market is projected to grow from 313.11 thousand tons in 2025 to 724.42 thousand tons by 2035. growing at a CAGR of 8.75% from 2026 to 2035.The market expansion is boosted by the development of data centers, investment in industrial automation, and demand for thermal management systems and thermal cycling performance in automotive, electronics, and telecommunication, integrated by industrial automation. The advancement in 5G infrastructure and renewable energy electronics supports the next-generation thermal solution

Market Highlights

- By region, Asia Pacific dominated the thermal interface materials market by holding a 46% share in 2025, driven by strong electronics manufacturing practices and industrial expansion.

- By region, North America held the 24% market share in 2025 and is expected to grow at the fastest with a CAGR of 10.30% during the forecast period due to data center investments and advancement in semiconductor infrastructure.

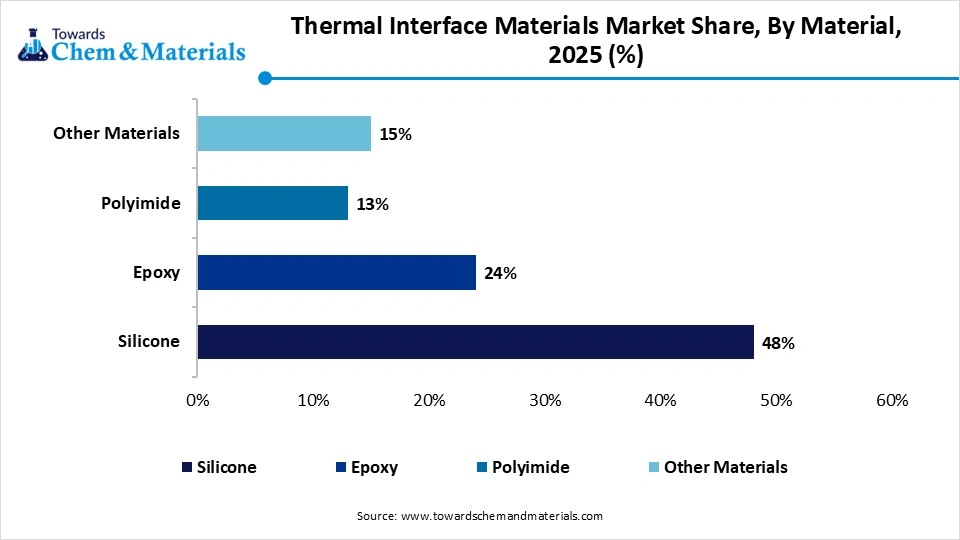

- By material, the silicone segment dominated the market with the largest share of 48% in 2025 due to its thermal stability and reliability in EV battery and power module cooling.

- By material, the polyimide segment held 13% market share in 2025 and is expected to grow at the fastest CAGR of 10.2% over the forecast period, driven by its demand in advanced semiconductor packaging and flexible electronics manufacturing.

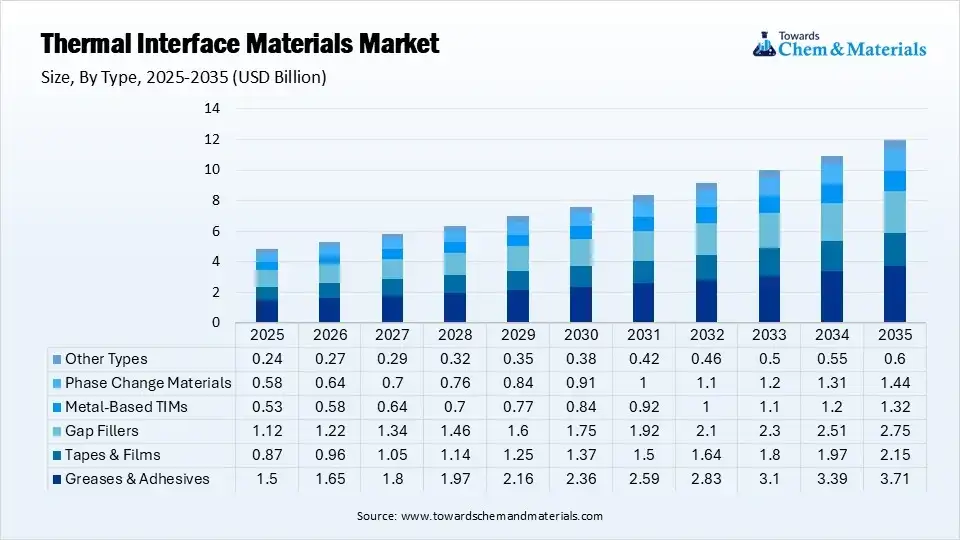

- By type, the greases & adhesives segment dominated the market with the largest share of 31% in 2025, used in CPUs, Industrial electronics, and GPUs for large-scale electronics manufacturing.

- By type, the gap fillers segment held 23% market share in 2025 and is expected to grow at the fastest CAGR of 10.5% over the forecast period because it offers higher thermal transfer efficiency. And demand for power electronics systems.

- By application, the computers & data centers segment dominated the market with the largest share of 28% in 2025, driven by AI servers expansion and advanced processing materials.

- By application, the automotive segment held 24% market share in 2025 and is expected to grow at the fastest CAGR of 11.3% over the forecast period accelerated by demand for thermal management in EV battery system and power electronics.

Quick Stats at a Glance

- Market Estimated Size (2025): USD 4.85 Billion | CAGR (2026–2035): 9.45%

- Market Projected Size (2035): USD 11.96 Billion

- Asia Pacific: largest Market Revenue Share of 46% in 2025|USD 2.23 Billion

- Market Estimated Volume (2025): 313.11 Thousand Tons | Volume CAGR (2026–2035): 8.75%

- Market Projected Volume (2035): 724.42 Thousand Tons

- Market Pricing (2025):

- Average Manufacturing Price: USD 10.50/kg

- Average Selling Price: USD 13.90/kg

- Pricing CAGR (2026–2035): 2.95%

- Average Manufacturing Price: USD 10.50/kg

The thermal interface material sector grows through research on improving material stability and performance. The global Thermal Interface Materials Market is developing because of its increased demand for electronic miniaturization, industrial automation, and high-density power management systems. Chemical companies are increasingly undergoing strategic partnerships by developing mediums and highly conductive materials with low thermal resistance and superior conductivity, setting a standard for value chain resilience.

- In October 2025, Henkel Adhesive Technologies advances its sustainable manufacturing efforts through a broadened strategic partnership with Dow. This collaboration integrates low-carbon feedstocks into its commercial adhesive and thermal production lines by improving emission reductions. The initiative promotes strict, multi-enterprise net-zero manufacturing practices.

The growing consumer electronics and telecommunication infrastructure is fueling the market. As manufacturers seek greater equipment longevity and thermal stability to prevent components such as microprocessors and graphics units from shrinking. Advancements in materials eliminate microscopic air pockets between the hot semiconductor and the cooling components, reducing heat spikes. The silicone-based materials maintain their dominance due to their flexibility, which accelerates the transition toward non-silicone polymers and advanced epoxies in cleanrooms.

Manufacturers utilized high-performance thermal greases for thin, speedy GPU connections and automated gap fillers for production batch assembly. The innovation focuses on phase-change material stability and rework.

The inventors are integrating graphene and carbon nanotubes into polymers to produce highly sustainable electronic systems. The modern procurement of advanced cooling media, the booming data-driven industry, is integrated with sustainable agility. The expansion driven by high-performance computing and AI capabilities demands efficient heat dissipation to shield data and improve energy efficiency. Additionally, the rise of modern electronics and 5G base stations requires effective, weather-resistant thermal interface solutions by combining nanotechnology.

Global Investment Flow for Thermal Interface Materials Market in 2026

A substantial investment is driving the expansion of automated production infrastructures optimized for a high-volume liquid delivery system in the market. Venture capital into specialized material science startups to scale the commercialization of nano-driven materials, providing liquidity.

- In January 2026, Vertiv Group launched Vertiv™ MegaMod™ HDX, a hybrid liquid-cooling system optimized for AI and high-performance computing processing units in North America and EMEA. This investment integrates direct-to-chip liquid cooling with air-cooled designs to meet thermal demand.

The compounding initiatives fund domestic manufacturing hubs and regional application-testing laboratories to deliver modified, fast-curing thermal interface materials to regional electronics packaging hubs. This investment focuses on corporate decarbonization to integrate bio-based feedstocks and green energy assets through strategic collaboration.

Recent Market Trends

- Move Towards Thermal Upgradation: The integration of deep learning algorithms and computing models boosts silicon hardware development, driving the need for innovative materials by offering superior reliability of thermal components.

- Adoption of Automated Fluid Formulations: The shift towards high-speed electronic manufacturing lines is adopting disposable liquid gap fillers and gels through precise rheological properties, enabling robotic nozzle systems to proficiently in multi-layer circuit boards.

- Process Engineering Focused on High Thermal Yields: The large-scale manufacturers focus on manufacturing compatibility and superior thermal efficiency. for clean debonding and simple rework production cycles.

Report Scope

| Report Attributes | Details |

| Market Size and Volume in 2026 | USD 5.31 Billion / 340.51 Thousand Tons |

| Revenue Forecast in 2035 | USD 11.96 Billion / 724.42 Thousand Tons |

| Growth Rate | CAGR 9.45% |

| Base Year of Estimation | 2025 |

| Forecast Period | 2025 - 2035 |

| High Impact Region | Asia Pacific |

| Segment Covered | By Material, By Type, By Application, By regions |

| Key Companies Profiled | Henkel AG & Co. KGaA, Dow, 3M Company, Indium Corporation, Fujipoly, Honeywell International Inc., SIBELCO, Shin-Etsu |

Key Technological Shifts and AI in the Thermal Interface Materials Market

The thermal interface materials market is transforming as Artificial Intelligence computer hardware redesigns thermal pathways. Deep learning microprocessors and high-wattage devices generate heat spikes, making novel materials essential for reliability. The technological shift ensures a stable value chain by controlling filler distribution in the thermal system.

Formulation companies are using neural networks and machine learning to simulate molecular interactions to develop advanced phase-change materials and ultra-thin thermal greases. The merging of hyperscale cloud and autonomous systems creates workflows that generate next-generation, low-resistance cooling mediums capable of managing heat waves.

Supply Chain Analysis of the Thermal Interface Materials Market

- Synthesis and Feedstock Procurement: The stage of sourcing ultra-pure conductive fillers and isolating chemicals, raw silicone fluids, epoxies, and non-silicone acrylic monomers used in the production of thermal interface materials. It involves supplying conductive mineral fillers via surface treatments with coupling agents within a viscous polymer base.

- Dow (Dow Silicones): They provide vinyl-functionalized polydimethylsiloxane fluids, ultra-pure silicone base polymers, and cross-linkers specifically engineered for compounding thermal interface materials. These chemical operators controlled molecular weight distribution in cleanroom computing assemblies.

- Key Players: Momentive Performance Materials, Shin-Etsu Chemical Co., Ltd., Wacker Chemie AG, and Evonik Industries AG

- Quality Analysis and Certification: The stage focuses on operational validation by ensuring functional safety and mechanical longevity. Technicians evaluate performance variables, including bulk thermal conductivity and contact thermal resistance.

- UL Solutions (Underwriters Laboratories): The leading global organization for material testing, validation, and safety certification of advanced thermal engineering materials. UL Solutions focuses on safety assessments and performance verification programs for thermal interface infrastructure.

- Key Players: TÜV SÜD, Intertek Group plc., Anritsu Corporation, and SGS S.A.

- Material Distribution to End Users: The logistical stage of formulation, with specialized temperature-controlled shipping and storage logistics. These materials are integrated with electronic and automotive assembly by maintaining shelf-life preservation and a precise delivery system.

- Arrow Electronics, Inc.: Global industrial distributors offer specialized supply chain management programs and climate-controlled storage infrastructure for pre-cut elastomeric pads and syringes of thermal grease to electronics manufacturers.

- Key Players: Avnet, Inc., Euro Technologies, DigiKey Electronics and Mouser Electronics, Inc

Regulatory Framework: Thermal Interface Materials Market

| Region | Key Regulations | Regulatory Focus |

| European Union | REACH and RoHS standards | Restriction on the volume of cyclic siloxanes and halogenated additives in polymeric base. The standard or flame-retardant pads are included with the pre-cut pads. |

| North America | TSCA, EPA Standards, and UL 94 Standards | Standard focus on tracking novel carbon allotropes and testing thermal materials in computing and automotive applications. |

| Asia Pacific | K-REACH, China RoHS, and CSCL | Thermal material classification disclosure labels and mandates for novel formulation mineral filler in electronic assembly pipelines. |

Thermal Interface Materials Market Dynamics

Driver

Transition Towards Electric Mobility

The thermal interface materials market is expanding as the move towards sustainable e-mobility drives growth. The increased demand for conformable, fast-curing gap fillers and fluid-driven gels to fill complex spaces within battery thermal management and cooling systems, boosting the adoption of thermal interface materials. The consumer demand for electric vehicles with high-voltage powertrains, densely packed batteries, and fast chargers that generate significant heat. To avoid thermal runaway and protect safety and battery performance, manufacturers require thermal management systems. Additionally, as automotive players increasingly integrate automation, the need for these specialized, quick-dispensing thermal compounds.

Restraint

Volatility in Raw Material Cost and Supply Chain Limitations

The market growth is restrained by the fluctuations in feedstock prices and the limited supply of key polymers and fillers. The development of thermal systems requires pure raw materials, such as silicone fluids and nitrides, but geopolitical tensions and logistical uncertainty limit continuous market growth. Electronic manufacturers with compelling suppliers to absorb high operation costs, which lowers the R&D funding and investment in new cooling solutions.

Opportunity

Integration of Cutting-edge Nanotechnology and Graphene Fillers

The key opportunity in the market is accelerated by a new commercial route that is emerging by combining engineered carbon allotropes into chemical frameworks. The modernization of industrial infrastructure by adding coarse fillers to boost heat transfer, especially in automotive and electronic assembly.

The formulation experts increasingly utilize nanotechnology by integrating graphene-based fillers and multi-walled carbon nanotubes into fluid polymers. These nanostructures create conductive pathways by reducing thermal resistance through thin, lightweight materials. This advancement enables suppliers to gain a competitive edge in engineering heat-dissipation solutions for sensors, mobile devices, and telecommunications modules.

Segmental Insights

Material Insights

The silicone segment dominated the market with the largest share of 48% in 2025. It is essential in the thermal industry because of its elasticity, dielectric stability, and thermal resilience. The formulators preferred silicone polymers for their ability to incorporate conductive fillers, maintain good surface wetting, and withstand mechanical strain and thermal cycling. Standard silicones are experiencing oil separation and outgassing in enclosed environments, accelerating the development of low-volatile alternatives for greases, pads, and gap fillers based on silicone components. The purified, novel silicone prevents oil migration, shielding optical sensors, laser components, and electrical components, providing resilience in tough industrial infrastructure.

The polyimide segment held the 13% market share in 2025 and is expected to grow at the fastest CAGR of 10.2% over the forecast period. They represent as protective dielectric barriers, isolating high-voltage components by offering superior mechanical resilience and higher electrical insulation. The polyimide films and thermally conductive polyimide composites ensure higher tensile strength and puncture resistance, enabling production and assembly.

Their slim structure ensures uniformity, reducing thermal resistance and meeting electrical safety standards. Aerospace and industrial engineers demand polyimide materials crucial for high-frequency power modules, high-voltage circuits, and high-precision applications.

")

Type Insights

The greases & adhesives segment dominated the market with the largest share of 31% in 2025.These thermal greases, pastes, and thermal adhesives are vital for minimal bond-line thickness amongst microchips and cooling assemblies. These fluid preparations wet rough metal surfaces and fill microscopic valleys, allowing fast heat transfer. The expansion and contraction cycles boost the requirement for superior thermal interface materials. In recent years, advances in R&D have led to cross-linked polymers and anti-pump-out additives for cooling joints, enabling long-term use in industrial applications.

The gap fillers segment held the 23% market share in 2025 and is expected to grow at the fastest CAGR of 10.5% over the forecast period. The gap fillers are categorized into pads and dispensed gap fillers serve as conformable, pre-cured pads and liquid compounds by providing low-stress interface compatibility pads, complex multi-component electrical components. Gap fillers are crucial in automation because they can be applied quickly with robotic dispensers, enabling streamlined assembly of multi-layered electronic modules by removing manual pad application. Additionally, its strong damping properties ensure shock and vibration resistance for rugged industrial controllers, outdoor telecommunication enclosures, and dense power management units.

") Application Insights

Application Insights

The computers & data centers segment dominated the market with the largest share of 28% in 2025, driven by AI training and cloud platforms, where thermal interface materials are vital for high-volume processing and hyperscale infrastructure workloads. Engineers are moving towards high-performance phase-change solutions and carbon-filled matrices that improve heat dissipation, maintaining safety in processing units and ensuring safe, efficient operation under heavy workloads. Modern hyperscale servers, AI accelerators, and storage systems align with advanced cooling systems, which are essential to maintaining speed, uptime, and cost-effectiveness.

The automotive segment held the 24% market share in 2025 and is expected to grow at the fastest CAGR of 11.3% over the forecast period.due to the global move towards next-generation electric mobility and autonomous systems. The demand for thermal interface materials in high-voltage inverters, ADAS systems, charging units, and lithium-ion batteries. Using ultra-stable thermal compounds is vital for high-voltage safety and to avoid thermal runaway. Automotive interface materials are driving manufacturers to seek long-lasting thermal compounds for vehicle longevity and performance.

Regional Insights

How Did the Asia Pacific Dominated the Thermal Interface Materials Market in 2025?

The Asia Pacific thermal interface materials market size was estimated at USD 2.23 billion in 2025 and is projected to reach USD 5.56 billion by 2035, growing at a CAGR of 9.57% from 2026 to 2035.Asia Pacific dominated the market by holding a 46% share in 2025, defined by its role as a global logistics and finance hub. Governments' investments in digital infrastructure and green energy boost the need for advanced cooling solutions and hyper-scale electronics sourcing. It includes a regional integrated silicon ecosystem, consumer electronics plants, and lithium-ion battery infrastructure. Asia Pacific's surge towards quick-dispensing formulations for robotic assembly lines is fueling domestic growth. Regional chemical companies focus on building large facilities for semiconductor packaging networks.

China

China

- China continues to dominate in the adoption of thermal interface materials, driven by domestic evolution in electric vehicle powertrain manufacturing, the electronics sector, and high-end consumer devices.

- Additionally, the country is undergoing an expanding trend in advanced semiconductor packaging engineering and the commercialization of lithium-ion battery systems.

Japan

- Focus on speeding up the production of advanced medical imaging devices and high-resolution optical sensors to comply with strict regulatory standards and ecological toxicity assessments.

- Japan is described as a supplier of raw minerals and a leader in precision electronics, boosting the move toward advanced printable phase-change formulations.

The North America thermal interface materials market size was estimated at USD 1.16 billion in 2025 and is projected to reach USD 2.93 billion by 2035, growing at a CAGR of 9.71% from 2026 to 2035.North America held the 24% market share in 2025 and is expected to grow at the fastest with a CAGR of 10.30% during the forecast period, valued for its advanced technology, stringent environmental standards, and early leadership in processing platforms. The regional development is driven by hyperscale cloud, defense electronics, and aerospace firms. A domestic move towards computational infrastructure for localized semiconductor packaging and microelectronics testing makes thermal interface materials for durable, ultra-low-outgassing insulation. North America's major players invest in R&D to develop high-performance formulations, including advanced carbon allotrope blends and premium phase-change media.

United States

- The United States is defined by its advanced thermal compounding hub and the integration of molecular nanotechnology, where manufacturers need cross-linking of graphene sheets and multi-walled carbon nanotubes.

- The supportive regulatory framework and government backing are accelerating the deployment of hyperscale data centers engineered for AI and high-power graphics processing units.

The Europe thermal interface materials market size was estimated at USD 0.97 billion in 2025 and is projected to reach USD 2.45 billion by 2035, growing at a CAGR of 9.71% from 2026 to 2035.Europe held the 20% market share in 2025. It is a specialized, engineering-driven region largely supported by the precision automotive hub. Regional manufacturers require highly reliable battery thermal materials that withstand vibrations, moisture, and seasonal changes. Europe's focus on advanced circular economy mandates aligns with electric and automated systems. Additionally, regional manufacturers and local suppliers are moving towards developing halogen-free, bio-based matrices with stringent chemical safety and sustainability goals

Germany

- The country's focus on circular economy sustainability commitments and regulatory compliance is driving improved capital investment in utility-scale clean energy projects and power modules.

- Germany is progressing towards implementing polyurethane- and silicon-free polymer bases and developing high-voltage electric vehicle propulsion infrastructure.

France

- France is focusing on highly advanced formulation in thermal interface materials and green chemical engineering that boosting the innovation of bio-based resin alternatives.

- The country experiences steady growth via integrated smart factory hardware & industrial Internet-of-Things nodes in localized aerospace electronics and defense systems.

The Latin America thermal interface materials market size was estimated at USD 0.29 billion in 2025 and is projected to reach USD 0.78 billion by 2035, growing at a CAGR of 10.40% from 2026 to 2035.Latin America held the 5% market share in 2025. The regional manufacturers focus on formulating silicone-based materials as nearshoring and electrification progress. The electronic wiring and consumer electronics manufacturing hubs boost demand for high-performance thermal interface materials in automotive and electronic assembly. Latin America's shift towards automation and renewable formulations to protect high-power electrical inverters, in line with strict regulations and sustainability efforts, improves production precision and eco-friendliness.

Brazil

- Driven by technological advancement in the automotive and consumer electronics assembly that promoted by regulatory support for infrastructure modernization.

- The domestic manufacturing of slim consumer hardware and capital investment in clean energy to insulate high-power electrical inverters.

The Middle East & Africa thermal interface materials market size was estimated at USD 0.19 billion in 2025 and is projected to reach USD 0.54 billion by 2035, growing at a CAGR of 11.01% from 2026 to 2035.The Middle East & Africa held the 5% market share in 2025, influenced by infrastructure upgradation and modernization investments. Regional industrial diversification enables the adoption of thermal interface materials focused on protecting electronic and communication equipment. MEA is adopting premium, non-silicone materials that resist dry-out and fluid separation during outdoor deployments. The government's fund for smart-city and grid upgrades requires durable, weatherproof interface pads for 5G base stations and data hubs across the MEA region.

")

Saudi Arabia

- The country is following infrastructure-led modernization, supported by national funding for digital transformation and smart city initiatives.

- Saudi Arabia's innovator is evolving towards commercializing hyperscale cloud data units to improve processor efficiency through improved thermal interface materials.

Competitive Analysis in the Thermal Interface Materials Market

- The global thermal interface materials market is highly competitive, with top chemical companies reformatting to develop high-performance, automation-ready thermal compounds.

- Henkel dominates in innovation with silicone-free liquid gap fillers and adhesives that ensure reliability under challenging AI workloads.

- Dow advances semiconductor packaging by creating ultra-pure silicone matrices and ultra-high conductivity thermal gel to cool next-generation optical and enhance thermal performance.(Source:indianchemicalnews.com)

- Parker Hannifin offers cure-in-place gels for robotic administration and stabilizing logistics with decentralized manufacturing. Honeywell and Shin-Etsu supply advanced phase-change materials and silicone solution directly to data centers and fabrication units.

Recent Developments

- In May 2026, Henkel announced the launch of new thermal interface materials to enhance EV battery thermal management. They released two products, Bergquist TGF 2030APS and Loctite TLB 9270APS, designed for use in electric vehicle batteries and supporting high-volume, cost-efficient production.(Source: www.henkel.com)

- In November 2025, Parker Hannifin's Chomerics division officially commercialized THERM-A-GAP GEL 120, expanding its automation footprint. This new gap-filler gel formulation provides a high-thermal-conductivity solution optimized to eliminate heat dissipation and maintain performance.(Source: electropages.com)

Top Companies in the Thermal Interface Materials Market and Their Offerings

- Henkel AG & Co. KGaA: The company delivers specialized elastomeric sheets and high-conductivity liquids, supplies cooling media for general circuit assemblies, and uses automated dispensing for high-speed processing units.

- Dow: The global leader focuses on producing low-volatile thermal pads, non-curing greases, dispensable gels, and cure-in-place compounds, which are designed to protect automotive sensors and aerospace electronics.

Other Major Players

- 3M Company

- Indium Corporation

- Fujipoly

- Honeywell International Inc.

- SIBELCO

- Shin-Etsu

Segments Covered in the Report

By Material

- Silicone

- Silicone Greases

- Silicone Gap Fillers

- Silicone Pads

- Epoxy

- Thermally Conductive Epoxy Adhesives

- Epoxy Encapsulants

- Polyimide

- Polyimide Films

- Thermally Conductive Polyimide Composites

- Other Materials

- Acrylic-Based TIMs

- Graphite-Based Materials

- Hybrid Polymer Materials

By Type

- Grease & Adhesives

- Thermal Greases

- Thermal Adhesives

- Tapes & Films

- Thermal Tapes

- Thermal Films

- Gap Fillers

- Pads

- Dispensed Gap Fillers

- Metal-Based TIMs

- Liquid Metal TIMs

- Metal Foils

- Phase Change Materials

- Waxed-Based PCM

- Polymer-Based PCM

- Other Types

- Thermal Gels

- Graphite Sheets

By Application

- Computers & Data Centers

- Servers

- AI Accelerators

- Storage Systems

- Automotive

- Electric Vehicles

- ADAS Systems

- Power Electronics

- Telecommunications

- 5G Infrastructure

- Networking Equipment

- Industrial Applications

- Automation Systems

- Power Modules

- Industrial Electronics

- Healthcare & Medical Devices

- Diagnostic Equipment

- Imaging Systems

- Consumer Durables

- Smartphones

- Laptops

- Gaming Consoles

- Home Electronics

- Other Applications

- Aerospace

- Defense

- Renewable Energy Systems

By Regional

- North America

- U.S.

- Canada

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Sweden

- Denmark

- Norway

- Asia Pacific

- China

- Japan

- India

- South Korea

- Thailand

- Latin America

- Brazil

- Mexico

- Argentina

- Middle East and Africa (MEA)

- South Africa

- UAE

- Saudi Arabia

- Kuwait

FAQ's

Select User License to Buy

Figures (7)