Content

What is Polysilicon Market Size and Share?

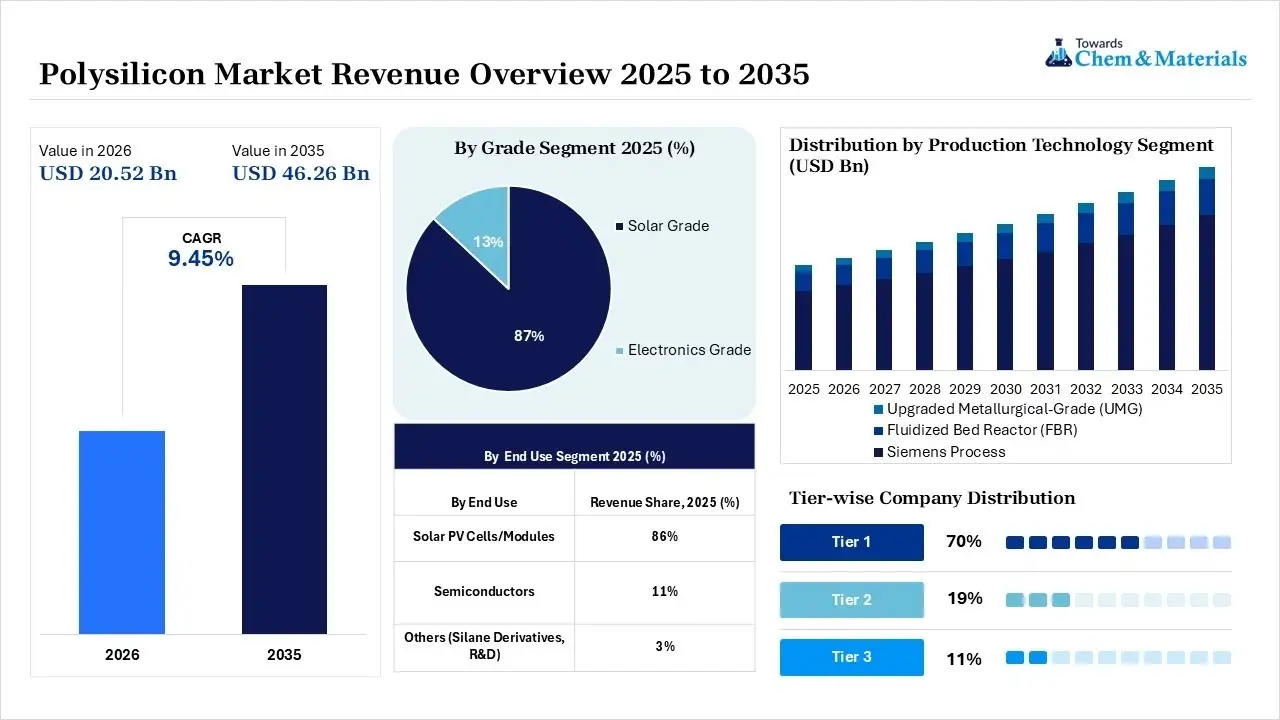

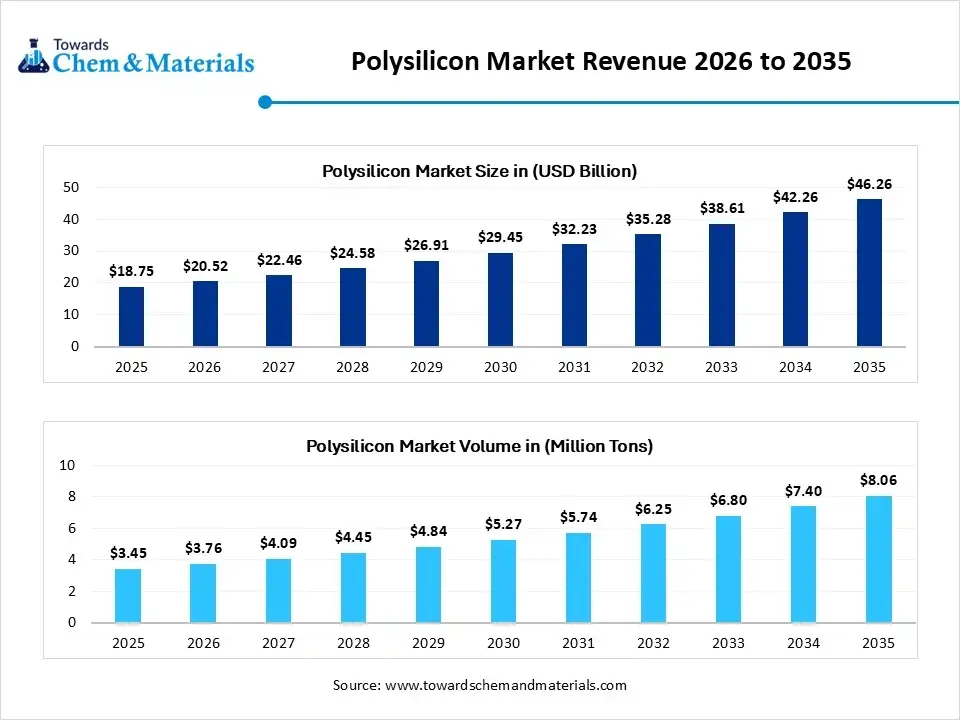

The global polysilicon market size was valued at USD 18.75 billion in 2025, is estimated to reach USD 20.52 billion in 2026, and is projected to reach USD 46.26 billion by 2035, exhibiting a compound annual growth rate (CAGR) of 9.45% over the forecast period from 2026 to 2035. Asia Pacific dominated the polysilicon market with the largest revenue share of 69.0% in 2025 and is expected to grow at the fastest CAGR of 9.53% during the forecast period. In terms of volume, the polysilicon market is projected to grow from 3.45 million tons in 2025 to 8.06 million tons by 2035, growing at a CAGR of 8.85% from 2026 to 2035.

The increasing global shift towards renewable energy is the key factor driving market growth. Also, ongoing technological innovations in high-efficiency solar cells coupled with supportive government policies can fuel market growth further. The market includes the global trade, manufacturing, and supply chain of polycrystalline silicon, a multi-crystalline and ultra-pure form of silicon. It serves as the essential raw material for both the semiconductor and solar photovoltaic (PV) industry sector. The global push towards renewable energy enables the solar PV sector to be the major driver of polysilicon demand. Polysilicon utilized within the electronics and photovoltaic industries typically requires a purity threshold of 99.99% or greater to ensure the optimal performance of semiconductor devices and solar cells. Characterized by a polycrystalline structure, this material comprises numerous microcrystalline silicon grains oriented in diverse crystallographic directions.

Polysilicon Market Key Takeaways

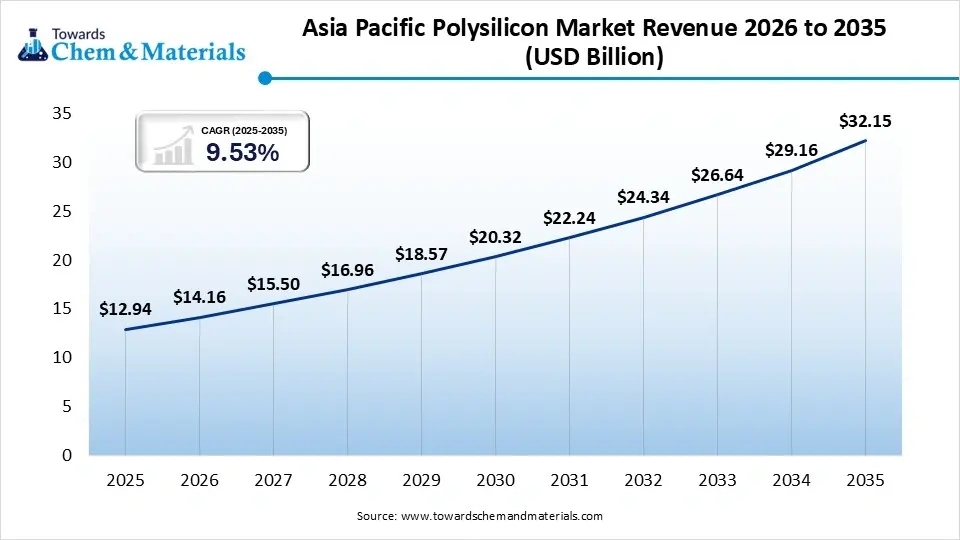

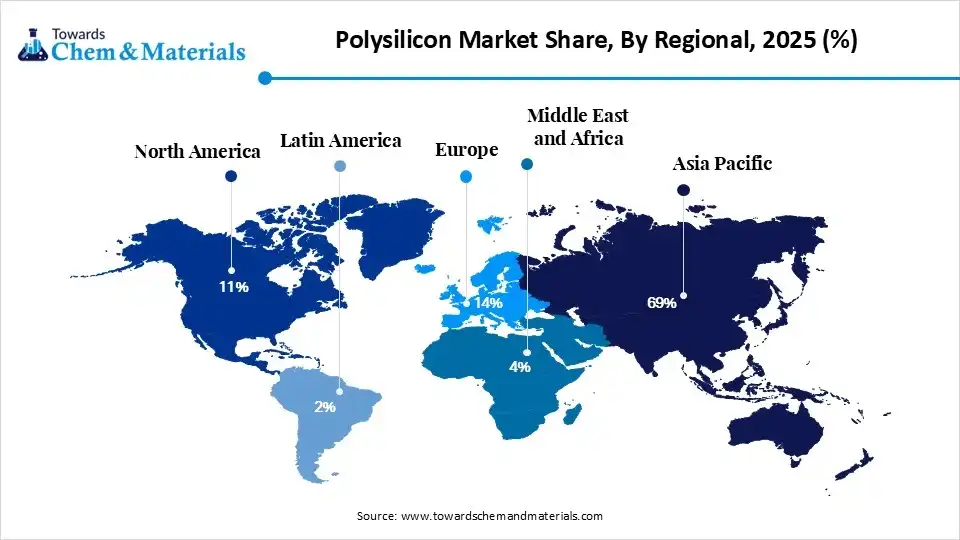

- By region, Asia Pacific dominated the market with the largest share of 69% in 2025 and is expected to grow at the fastest CAGR of 10.20% over the forecast period. The dominance and growth of the region can be attributed to the extensive scale-up of solar photovoltaic (PV) production.

- By region, Europe held the market share of 14.00% in 2025. The growth of the segment can be credited to the strategic investments improving local manufacturing capabilities.

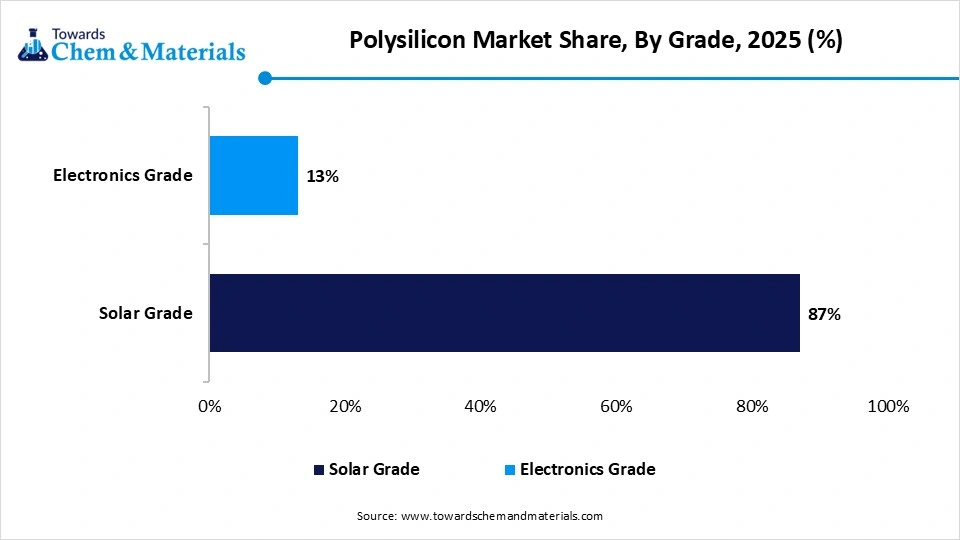

- By grade, the solar grade segment dominated the market with the largest share of 87.0% in 2025. The dominance of the segment can be attributed to the increasing global demand for solar photovoltaic (PV) installations.

- By grade, the electronics grade segment held a market share of 13.00% in 2025 and is expected to grow at the fastest CAGR of 9.80% over the forecast period. The growth of the segment can be credited to the increasing manufacturing of memory devices.

- By end use, the solar PV cells/modules segment dominated the market with the largest share of 86.0% in 2025. The dominance of the segment can be linked to the increasing consumer preference towards high-efficiency solar modules.

- By end use, the semiconductors segment held a market share of 11.00% in 2025 and is expected to grow at the fastest CAGR of 10.00% over the forecast period. The growth of the segment can be driven by ongoing purity needs.

- By production technology, the Siemens process segment dominated the market with the largest share of 76.0% in 2025. The dominance of the segment can be attributed to the surge in manufacturing of high-efficiency modules.

- By production technology, the fluidised bed reactor (FBR) segment held a market share of 18.0% in 2025 and is expected to grow at the fastest CAGR of 11.20% during the projected period. The growth of the segment can be credited to its capability to produce granular polysilicon.

Quick Stats at a Glance

- Market Estimated Size (2025): USD 18.75 Billion | CAGR (2026–2035): 9.45%

- Market Projected Size (2035): USD 46.26 Billion

- Asia Pacific: largest Market Revenue Share of 69% in 2025 | USD 12.94 Billion

- Market Estimated Volume (2025): 3.45 Million Tons | Volume CAGR (2026–2035): 8.85%

- Market Projected Volume (2035): 8.06 Million Tons

- Market Pricing (2025):

- Average Manufacturing Price (2025): USD 5.85/kg

- Average Selling Price (2025): USD 7.36/kg

- Pricing CAGR (2026–2035): 3.95%

Market Trends

- Polysilicon is extensively used in the electronics industry, as it is utilised to make semiconductor wafers, which are crucial parts of various consumer electronics, such as computers, smartphones, and other gadgets. Also, increasing demand for these devices can bring changes in consumer preferences.

- The ongoing transition towards renewable energy sources, which is being driven by the increasing need for sustainable energy solutions, is one of the major factors impacting positive market growth. The need for polysilicon, as the essential raw material used in the manufacturing of solar cells, will increase with the need for solar photovoltaic (PV) systems.

- The growth of domestic wafer and ingot manufacturing is another major factor driving market growth. Major companies are setting up complete wafer-to-module manufacturing settings, convincing that polysilicon is processed locally into ingots and wafers prior to being utilised in final applications.

Polysilicon Market Opportunity Report Scope

| Report Attributes | Details |

| Market Size 2026 | USD 20.52 Billion / 3.76 Million Tons |

| Expected size in 2035 | USD 46.26 Billion / 8.06 Million Tons |

| Growth Rate | CAGR of 9.45% |

| Base Year of Estimation | 2025 |

| Forecast Period | 2025-2035 |

| Dominant Region | Asia Pacific |

| Segment Covered | By Grade, By End Use, By Production Technology, By Regions |

| Key Companies Profiled | OCI COMPANY Ltd.,Qatar Solar Technologies,REC Silicon ASA,High-Purity Silicon America Corporation,Tongwei Group Co., Ltd,Tokuyama Corporation, DAQO NEW ENERGY CO., LTD.,GCL-TECH,Wacker Chemie AG, Xinte Energy Co., Ltd |

How Are Cutting-Edge AI Technologies Revolutionising the Polysilicon Market?

AI is transforming the market by converting it from a standard chemical commodity business into a cognitive and hyper-optimised industrial sector. Polysilicon is the essential raw material for advanced semiconductor microchips and solar photovoltaic (PV) cells. Furthermore, market players are using ML algorithms to create data-driven surrogate models of CVD reactors.

Supply Chain Analysis of the Polysilicon Market

- Feedstock Procurement :It refers to the sourcing and acquisition of essential raw materials, mainly quartz and gases like trichlorosilane (TCS) or silane needed to produce high-grade polycrystalline silicon.

- Major Players: GCL Technology Holdings Ltd., Tongwei Co., Ltd.

- Chemical Synthesis and Processing :It includes the major industrial chemistry stages needed to transform low-purity, crude metallurgical-grade silicon (MG-Si) into ultra-high-purity polycrystalline silicon (polysilicon).

- Major Players: Daqo New Energy Corp., Xinte Energy Co., Ltd.

- Packaging and Labelling :It includes the crucial, highly controlled end-of-manufacturing processes used to store, transport, and distinguish ultra-pure polycrystalline silicon.

- Major Players: OCI Company, Tokuyama Corporation

- Regulatory Compliance and Safety Monitoring :It emphasised the environmental, legal, and workplace safety frameworks that control the manufacturing of polysilicon. As polysilicon production is a highly capital-intensive and energy-consuming process.

- Major Players: Xinte Energy Co., Ltd., GCL Technology Holdings Ltd.

Polysilicon Market's Regulatory Landscape: Global Regulations

| Country/Region | Key Regulations |

| United States | Section 301 and Section 232 Tariffs: Under Section 301, the US enforces a 50% tariff on Chinese polysilicon and wafers. Additionally, following a broad Section 232 national security investigation into polysilicon and semiconductors, the administration enforces stringent Tariff-Rate Quotas (TRQs). |

| European Union | Net-Zero Industry Act (NZIA): This framework mandates that public procurement and renewable energy auctions evaluate non-price criteria, including environmental sustainability and supply-chain resilience. This effectively caps the market share of modules built using single-source, high-emission foreign polysilicon. |

| China | The Ministry of Commerce (MOFCOM) extends anti-dumping duties on solar-grade polysilicon imports coming from the US and South Korea. These measures protect domestic mega-producers from foreign competition while discouraging localized Western supply expansions. |

Market Dynamics

Driver

Growing Use of Electronic Devices

Growing use of electronic devices is one of the key factors driving market growth. Electronic devices have become a crucial part of human life, and they will remain that way. These devices, such as the television sets and smartphones, will be redundant without semiconductors. Hence, polysilicon is widely used in the manufacturing of semiconductors, and without this compound, the manufacturing of semiconductors will shrink noticeably. In addition, due to the ecological concerns surrounding conventional processing, researchers face ongoing pressure to pioneer eco-friendly methods for synthesising polysilicon.

Restraint

High Energy Intensity

Stringent industrial emission standards and carbon border mechanisms need expensive and massive upgrades in chemical and waste management, which is the major factor hindering the market expansion. Moreover, manufacturing budgets are highly sensitive to sudden spikes in quartz, metallurgical-grade silicon, and electricity costs. Conventional Siemens technology is increasingly challenged by fluidised bed reactor (FBR) methods, hampering market growth soon.

Opportunity

Increasing Adoption in Advanced Semiconductors

Ongoing innovations in semiconductor technologies such as electric vehicles, AI computing infrastructure, and high-efficiency photovoltaic systems are generating lucrative opportunities in the market. The growing need for memory devices, advanced chips, and power semiconductors is propelling investment in semiconductor fabrication facilities. Furthermore, there is a growing trend among solar manufacturers towards integrating advanced photovoltaic technologies, including TOPCon and heterojunction architectures.

Segmental Insights

Grade Insights

The Solar Grade Segment Dominated the Market with 87.0% of Market Share in 2025

The solar grade segment dominated the market with the largest share of 87.0% in 2025. The dominance of the segment can be attributed to the increasing global demand for solar photovoltaic (PV) installations and the push towards carbon neutrality. In addition, advancements in manufacturing techniques have lowered overall production costs by enhancing the economic viability of large-scale solar projects.

")

The electronics grade segment held a market share of 13.00% in 2025 and is expected to grow at the fastest CAGR of 9.80% over the forecast period. The growth of the segment can be credited to the increasing manufacturing of memory devices, microchips, and integrated circuits necessitating more electronic-grade silicon.

Polysilicon Market Share, By Grade, 2025 (%)

| By Grade | Revenue Share, 2025 (%) |

| Solar Grade | 87% |

| Electronics Grade | 13% |

End Use Insights

The solar PV cells/modules segment dominated the market with the largest share of 86.0% in 2025. The dominance of the segment can be linked to the increasing consumer preference towards high-efficiency solar modules. Also, ongoing technological advancements in polysilicon production in emerging regions have scaled supply chain capabilities.

The semiconductors segment held a market share of 11.00% in 2025 and is expected to grow at the fastest CAGR of 10.00% over the forecast period. The growth of the segment can be driven by ongoing purity needs and rapid technological innovations across global automotive and electronics sectors. The transition towards electric vehicles (EVs) is impacting positive market growth soon.

The others (silane derivatives, R&D) segment held the market share of 3.00% in 2025. The growth of the segment is owing to the increasing cost efficiency demands in solar manufacturing and the ongoing enforcement of circular economy principles. Growing emphasis on recycling end-of-life solar panels has optimised the growth of the niche processing market.

Polysilicon Market Share, By End Use, 2025 (%)

| By End Use | Revenue Share, 2025 (%) |

| Solar PV Cells/Modules | 86% |

| Semiconductors | 11% |

| Others (Silane Derivatives, R&D) | 3% |

Production Technology Insights

The Siemens process segment dominated the market with the largest share of 76.0% in 2025. The dominance of the segment can be attributed to the surge in manufacturing of high-efficiency modules and the growing emphasis on energy transition policies. Major market players are modifying Siemens variants that propel overall production yield.

The fluidised bed reactor (FBR) segment held a market share of 18.0% in 2025 and is expected to grow at the fastest CAGR of 11.20% during the projected period. The growth of the segment can be credited to its capability to produce granular polysilicon and substantially lower energy consumption. FBR creates free-flowing, granular polysilicon rather than large chunks.

The upgraded metallurgical-grade (UMG) segment held the market share of 6.00% in 2025. The growth of the segment can be linked to the increasing demand for low-carbon and cost-effective solar feedstock coupled with the transition towards more sustainable refining techniques. UMG silicon manufacturing provides a drastically cheaper alternative to conventional methods.

Polysilicon Market Share, By Production Technology, 2025 (%)

| By Production Technology | Revenue Share, 2025 (%) |

| Siemens Process | 76% |

| Fluidized Bed Reactor (FBR) | 18% |

| Upgraded Metallurgical-Grade (UMG) | 6% |

Regional Insights

How did Asia Pacific Dominate the Polysilicon Market in 2025?

The Asia Pacific polysilicon market size was estimated at USD 12.94 billion in 2025 and is projected to reach USD 32.15 billion by 2035, growing at a CAGR of 9.53% from 2026 to 2035.Asia Pacific dominated the market with the largest share of 69.0% in 2025 and is expected to grow at the fastest CAGR of 10.20% over the forecast period. The dominance and growth of the region can be attributed to the extensive scale-up of solar photovoltaic (PV) production and increasing semiconductor demand. In addition, ongoing urbanisation and digitisation of emerging nations can fuel market growth further.

China

- The rapid shift towards renewable energy and the growth of utility-scale solar installations create relentless demand for solar-grade polysilicon.

- The transition towards localising the manufacturing of electronic-grade polysilicon is fuelled by China’s booming semiconductor, 5G, AI, and electric vehicle (EV) sectors.

India

- India is heavily scaling up its solar capacity to meet renewable energy targets. The downstream push in cell and module manufacturing is driving an urgent need to onshore the entire supply chain.

- The increase in local demand for consumer electronics, 5G networking, the Internet of Things (IoT), and artificial intelligence is boosting the need for microprocessors.

The Europe polysilicon market size was estimated at USD 2.63 billion in 2025 and is projected to reach USD 6.71 billion by 2035, growing at a CAGR of 9.82% from 2026 to 2035.Europe held the market share of 14.00% in 2025. The growth of the segment can be credited to the strategic investments improving local manufacturing capabilities and sustainability goals supporting long-term demand. Furthermore, the major countries are increasingly establishing domestic electronic and solar hubs to reduce reliance on foreign imports, leading to regional expansion soon.

Germany

- The country's strong commitment to carbon neutrality and clean energy serves as the foundation for market expansion.

- Germany’s status as a heavyweight in automotive engineering fuels massive demand for microelectronics, requiring high-purity electronic-grade polysilicon for chips and sensors.

The North America polysilicon market size was estimated at USD 2.06 billion in 2025 and is projected to reach USD 5.32 billion by 2035, growing at a CAGR of 9.95% from 2026 to 2035.North America held the market share of 11.00% in 2025. The growth of the region can be linked to the increasing need for domestic semiconductor manufacturing and the ongoing transition towards high-efficiency solar technologies. Also, major policies are offering direct funding and tax credits to incentivise domestic polysilicon production.

United States

- The rapid expansion of domestic microchip foundries by major players is increasingly boosting the demand for high-grade electronic-grade polysilicon.

- North American producers are reactivating and expanding production hubs like REC Silicon's Moses Lake facility in Washington.

Canada

- Ongoing innovations in chemical vapour deposition (CVD) and silane gas phase manufacturing methods are making polysilicon manufacturing more energy-efficient and cost-effective.

- The growing adoption of 5G infrastructure, cloud computing, and automotive electronics in North America is fuelling high demand for ultra-pure silicon.

The Latin America polysilicon market size was estimated at USD 0.56 billion in 2025 and is projected to reach USD 1.39 billion by 2035, growing at a CAGR of 9.52% from 2026 to 2035.Latin America held the market share of 3.00% in 2025. The growth of the region can be driven by increasing surging solar photovoltaic (PV) installations and supportive government policies for clean energy. Solar mini-grids are increasingly becoming a crucial solution for electrifying remote, off-grid areas across major regions. This demand directly impacts a higher consumption of solar-grade polysilicon.

Polysilicon Market Share, By Regional, 2025 (%)

| Regional | Revenue Share, 2025 (%) |

| North America | 11% |

| Europe | 14% |

| Asia-Pacific | 69% |

| Latin America | 2% |

| Middle East & Africa | 4% |

Brazil

- A surge in the domestic semiconductor and consumer electronics manufacturing sector is creating consistent procurement needs for electronic-grade polysilicon.

- Brazil's extensive renewable energy targets and large-scale solar (photovoltaic) installation programmes fuel massive demand for solar-grade polysilicon to manufacture PV modules.

Argentina

- National auctions and initiatives to support energy efficiency and renewable power generation are offering clear, multi-year visibility for solar demand across the region.

- The rapidly growing electronics sector and demand for ultra-pure, electronic-grade polysilicon for semiconductors are also contributing to the broader market.

The Middle East & Africa polysilicon market size was estimated at USD 0.75 billion in 2025 and is projected to reach USD 2.08 billion by 2035, growing at a CAGR of 10.74% from 2026 to 2035.The Middle East & Africa held a market share of 3.00% in 2025. The growth of the region is owing to the regional incentives supporting green tech and foreign investment along with the robust national renewable energy targets. Moreover, regional governments are providing incentives like import duty relaxations and tax benefits for research and development (R&D).

") Saudi Arabia

Saudi Arabia

- Saudi Arabia's Public Investment Fund (PIF) has collaborated with global tech giants to build an entire solar value chain domestically, from ingots and wafers to cells and modules.

- The government is using its abundant solar resources and low power costs to attract major polysilicon manufacturers.

UAE

- Substantial financial & regulatory backing by the UAE government, that covers favourable frameworks for local manufacturing & clean energy subsidies, is driving growth of the market.

- UAE is channelling extensive capital into the renewable energy spectrum, boosting the demand for polysilicon supply-chain infrastructure.

Recent Developments

- In February 2026, United Solar Holding officially commenced operations at its polysilicon manufacturing plant located within the Sohar Freezone in Oman. The facility is projected to achieve an annual production capacity of 100,000 tonnes. This operational milestone was announced by China-based Shuangliang Hydrogen, the primary equipment supplier for the project.(Source:renewablesnow)

- In February 2026, prominent Chinese polysilicon and photovoltaic (PV) module manufacturer Tongwei Co., Ltd. disclosed a definitive strategic plan to acquire a 100% equity stake in its competitor, Qinghai Lihao Clean Energy Co., Ltd. According to the official disclosure, the transaction will be executed through a combination of share issuances and cash payments.(Source:pv-tech.org)

Polysilicon Market Companies

- GCL-Poly Energy Holdings Limited: GCL Technology Holdings Limited (formerly known as GCL-Poly Energy Holdings Limited) is one of the world's premier manufacturers of polysilicon and silicon wafers for the solar photovoltaic (PV) industry.

- Wacker Chemie AG: Wacker Chemie AG is a prominent global leader in the production of hyperpure polycrystalline silicon (polysilicon). It plays a critical role as a primary supplier for both the semiconductor (microchip) and photovoltaic (solar energy) industries

Other Companies in the Market

- OCI COMPANY Ltd. (South Korea)

- REC Silicon ASA (Norway)

- Tokuyama Corporation (Japan)

- DAQO NEW ENERGY CO,.LTD. (China)

- Hemlock Semiconductor Operations LLC (U.S.)

- activ solar Schweiz GmbH. (Switzerland)

- GCL-SI (China)

- Wuxi Suntech Power Co., Ltd. (China)

- Renesola (China)

- Yingli Solar (China)

Segment covered in the report

By Grade

- Solar Grade

- Monocrystalline Solar Grade

- N-Type Solar Grade

- P-Type Solar Grade

- Multicrystalline Solar Grade

- Standard Solar Grade

- High-Efficiency Solar Grade

- Monocrystalline Solar Grade

- Electronics Grade

- Semiconductor Grade

- Memory Chip Grade

- Logic Chip Grade

- Ultra-High Purity Grade

- Advanced Node Grade

- Specialty Electronics Grade

- Semiconductor Grade

By End Use

- Solar PV Cells/Modules

- Monocrystalline Solar Modules

- Utility-Scale Installations

- Commercial Installations

- Residential Installations

- Multicrystalline Solar Modules

- Ground-Mounted Systems

- Rooftop Systems

- Monocrystalline Solar Modules

- Semiconductors

- Integrated Circuits

- Logic Devices

- Analog Devices

- Power Semiconductors

- Automotive Electronics

- Industrial Electronics

- Memory Devices

- DRAM

- NAND Flash

- Integrated Circuits

- Others (Silane Derivatives, R&D)

- Silane Derivatives

- Specialty Chemicals

- Silicon-Based Materials

- Research & Development

- Laboratory Applications

- Pilot-Scale Production

- Silane Derivatives

By Production Technology

- Siemens Process

- Conventional Siemens Process

- High-Purity Production

- Solar-Grade Production

- Modified Siemens Process

- Energy-Efficient Systems

- Advanced Purification Systems

- Conventional Siemens Process

- Fluidized Bed Reactor (FBR)

- Granular Polysilicon Production

- Solar-Grade Granules

- High-Purity Granules

- Advanced FBR Technology

- Low-Energy Production

- High-Throughput Production

- Granular Polysilicon Production

- Upgraded Metallurgical-Grade (UMG)

- Chemical Purification Route

- Solar Applications

- Industrial Applications

- Hybrid Purification Route

- Enhanced Purity UMG

- Cost-Optimized UMG

- Chemical Purification Route

By Regional

- North America

- U.S.

- Canada

- Mexico

- Europe

- UK

- Germany

- France

- Italy

- Spain

- Sweden

- Denmark

- Norway

- Asia Pacific

- Japan

- China

- India

- Australia

- South Korea

- Thailand

- Latin America

- Brazil

- Argentina

- The Middle East and Africa

- South Africa

- Saudi Arabia

- UAE

- Kuwait

FAQ's

Select User License to Buy

Figures (6)