Content

What is the Europe Iron and Steel Market Size and Share?

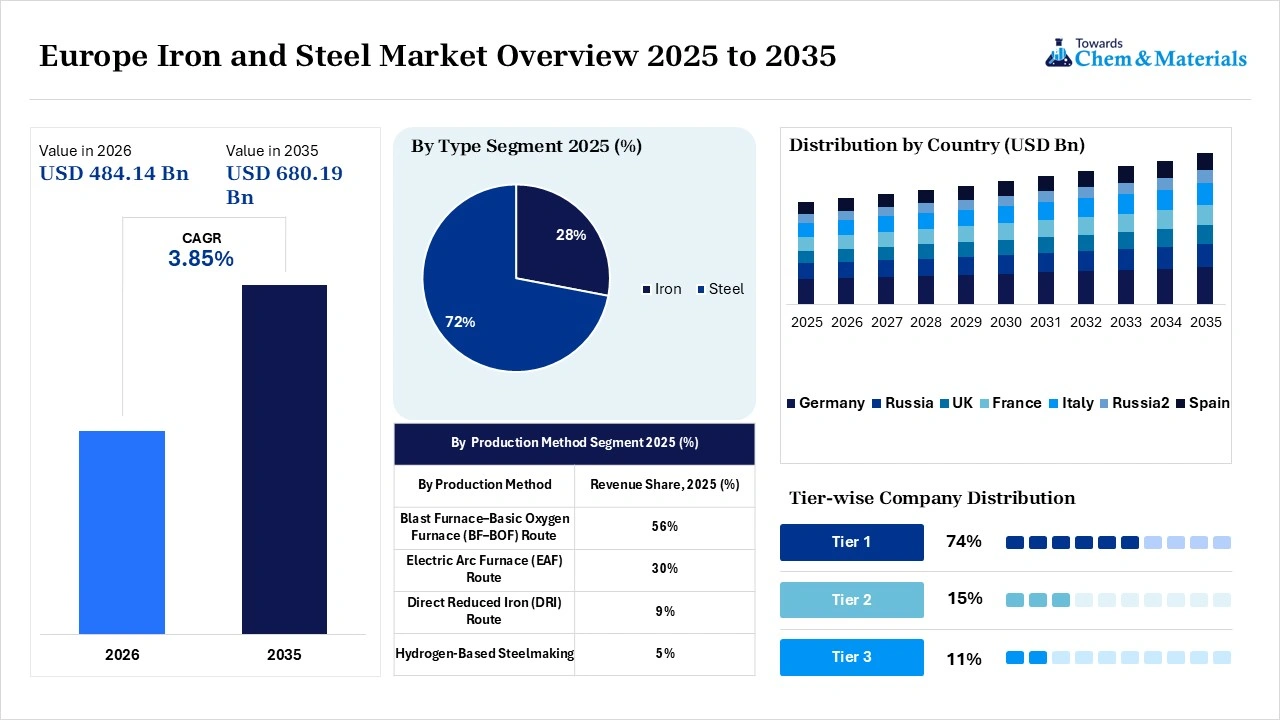

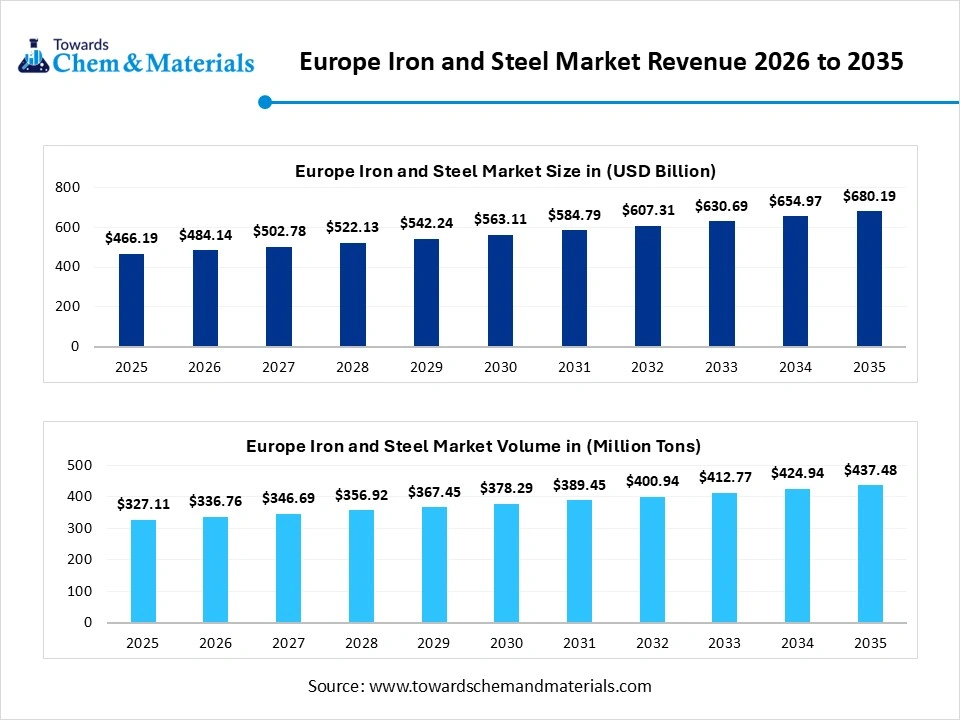

The Europe iron and steel market size was valued at USD 466.19 billion in 2025, is estimated to reach USD 484.14 billion in 2026, and is projected to reach USD 680.19 billion by 2035, exhibiting a compound annual growth rate (CAGR) of 3.85% over the forecast period from 2026 to 2035.Germany dominated the iron and steel market with the largest revenue share of 24.80% in 2025 and is expected to grow at the fastest CAGR of 3.87% during the forecast period. In terms of volume, the iron and steel market is projected to grow from 327.11 million tons in 2025 to 437.48 million tons by 2035. growing at a CAGR of 2.95% from 2026 to 2035. The ongoing transition to green steel is the key factor driving market growth. Also, push towards lightweight and high-strength materials coupled with the rapid urbanisation in the region can fuel market growth further.

Market Highlights

- By country, Germany dominated the market with the largest share of 24.80% in 2025. The dominance of the country can be attributed to the surge in investment in green steel.

- By country, France is expected to grow at the fastest CAGR of 5.14% over the forecast period. The growth of the country can be credited to the increasing speciality demand from the automotive and aerospace sectors.

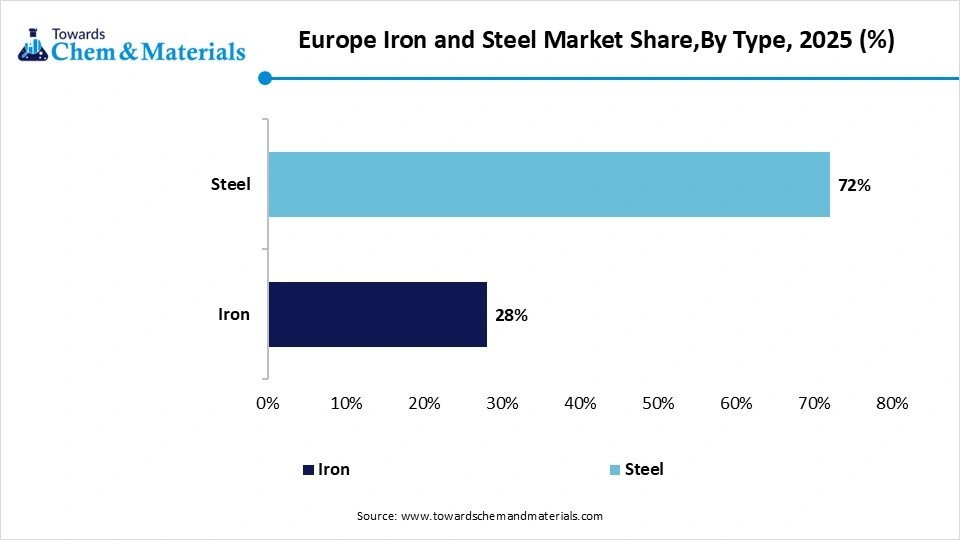

- By type, the steel segment dominated the market with the largest share of 71.60% in 2025 and is expected to grow at the fastest CAGR of 5.28% over the forecast period. The dominance and growth of the segment can be attributed to the increasing demand for high-performance steel grades.

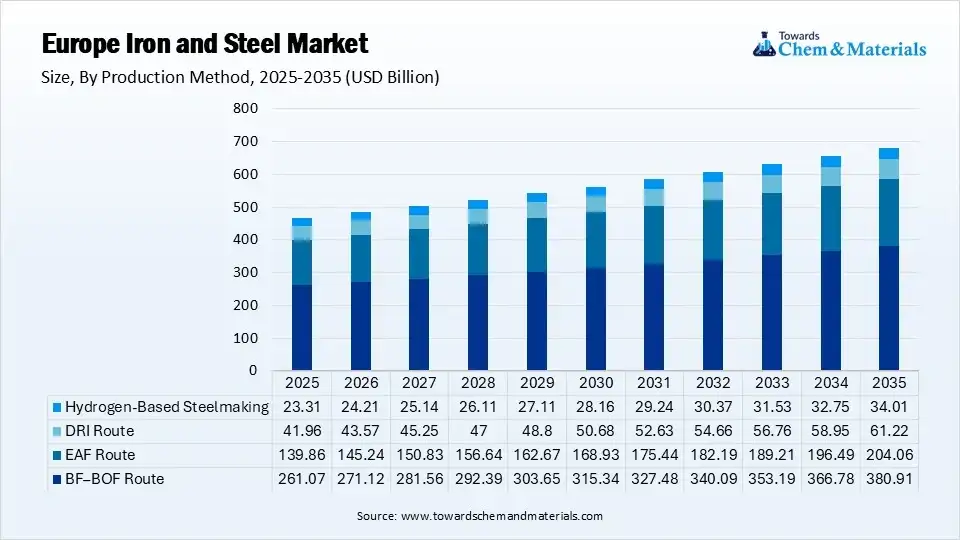

- By production method, the blast furnace–basic oxygen furnace (BF–BOF) route segment dominated the market with the largest share of 56.20% in 2025. The dominance of the segment can be linked to the established infrastructure.

- By production method, the hydrogen-based steelmaking segment is expected to grow at the fastest CAGR of 11.48% over the forecast period. The growth of the segment can be driven by green hydrogen investment supporting low-emission steel production.

- By form, the finished segment dominated the market with the largest share of 65.30% in 2025 and is expected to grow at the fastest CAGR of 5.22% during the projected period. The dominance and growth of the segment is owed to the increasing demand for value-added steel grades.

- By application, the construction & infrastructure segment dominated the market with the largest share of 35.60% in 2025. The dominance of the segment can be attributed to the green building standards promoting durable steel materials.

- By application, the energy & utilities segment is expected to grow at the fastest CAGR of 5.88% over the forecast period. The growth of the segment can be credited to the increasing demand for speciality steel products.

Quick Stats at a Glance

- Market Estimated Size (2025): USD 466.19 Billion | CAGR (2026–2035): 3.85%

- Market Projected Size (2035): USD 680.19 Billion

- Germany: Revenue Share of 24.80% in 2025|USD 115.62 Billion

- Market Estimated Volume (2025): 327.11 Million Tons | Volume CAGR (2026–2035): 2.95%

- Market Projected Volume (2035): 437.48 Million Tons

- Market Pricing (2025):

- Average Manufacturing Price (2025): USD 1,090/Ton

- Average Selling Price (2025): USD 1,370/Ton

- Pricing CAGR (2026–2035): 2.45%

The market covers the manufacturing, processing, and trade of semi-finished products, crude steel, and ferroalloys across the region. It is a widely regulated and highly integrated sector, central to the European economy and greatly aligned with the region's climate goals. The market is rapidly undergoing a massive transformation toward decarbonization, replacing carbon-intensive blast furnaces with green hydrogen-based direct reduced iron (DRI) and EAF processes.

Trade policies and tariffs significantly influence market dynamics, reflecting shifting international relations. Furthermore, technological advancements like automation and digitalization are about to revolutionize industry operations. As this landscape changes, stakeholders must remain resilient to adapt to these changes and capitalize on emerging opportunities.

Recent Market Trends

- The increasing product demand from the automotive sector is the latest trend in the market, shaping positive market growth. The demand for lightweight, high-strength steel and iron is increasing due to a surge in production of electric vehicles (EVs) across the region.

- The availability and pricing of essential raw materials are a crucial driver for the market expansion. Europe depends heavily on imports for key raw materials like scrap steel and iron ore. Also, the geopolitical tensions can make raw materials availability a crucial factor impacting manufacturing costs and market stability.

- Technological advancements in manufacturing processes are another major factor driving market growth.

- Innovations such as artificial intelligence, automation, and data analytics are improving operational efficiencies and reducing overall costs. The integration of smart production techniques enables real-time monitoring and optimization of manufacturing lines.

Report Scope

| Report Attributes | Details |

| Market Size and Volume in 2026 | USD 484.14 Billion / 336.76 Million Tons |

| Revenue Forecast in 2035 | USD 680.19 Billion / 437.48 Million Tons |

| Growth Rate | CAGR 3.85% |

| Base Year of Estimation | 2025 |

| Forecast Period | 2025 - 2035 |

| High Impact Country | Germany |

| Segment Covered | By Type, By Production Method, By Form, By Application, By Country |

| Key Companies Profiled | ArcelorMittal, Tata Steel, SSAB, voestalpine, Salzgitter AG, CELSA Group, Outokumpu, Acerinox, Aperam, LKAB |

How Cutting-Edge Technologies Are Revolutionizing the Europe Iron and Steel Market?

Advanced technologies are transforming the market mainly through automation, deep decarbonization, and digitalization. To fulfil stringent climate-neutrality goals, major players in the region are rapidly adopting hydrogen-based production and AI-driven process optimizations. Furthermore, AI algorithms can process production data in real time to optimize furnace temperatures and enhance the quality of specialized steel grades.

Supply Chain Analysis of the Europe Iron and Steel Market

- Feedstock Procurement :It refers to the sourcing of raw materials required to produce iron and steel. It also involves acquiring inputs like metallurgical coal, recycled steel scrap, iron ore, and Direct Reduced Iron (DRI).

- Major Players: Voestalpine, SSAB

- Chemical Synthesis and Processing :It includes the core chemical engineering methods, thermodynamic reduction reactions, and gas synthesis technologies used to extract pure iron from iron ore and refine it into steel.

- Major Players: Salzgitter AG, Voestalpine

- Packaging and Labeling :It refers to the digital technologies and standards, materials used to safeguard, track, and market steel products and the production of finished steel packaging (like cans, drums, and aerosols).

- Major Players: Tata Steel, Thyssenkrupp Rasselstein

- Regulatory Compliance and Safety Monitoring :It refers to the legally binding frameworks, occupational health standards, and environmental mandates that steelmakers must follow to operate, trade, and protect workers within the European Union.

- Major Players: SSAB, Voestalpine

Europe Iron and Steel Market 's Regulatory Landscape: Regulations

| Country | Key Regulation |

| Germany | The Federal Ministry for Economic Affairs and Climate Action heavily regulates and finances the transition from traditional blast furnaces to Hydrogen-based Direct Reduced Iron (DRI) and Electric Arc Furnaces (EAFs). |

| France | The French government closely monitors industrial emissions under the EU Green Deal, forcing operators like ArcelorMittal to aggressively modernize legacy facilities to lower carbon output. |

| Italy | Energy Relief Interventions: Because Italian rebar and long-product manufacturers operate on highly volatile electric grids, the state frequently revises short-term energy subsidies to insulate domestic mills from structural spikes. |

Market Dynamics

Drivers

Surge in Energy Demand

The increase in energy demand, especially for renewable energy, is the major factor driving the growth of the market. The construction of solar panels, wind turbines, and other renewable energy infrastructures needs significant amounts of steel. The transition towards sustainable energy solutions is likely to fuel the market expansion soon. In addition, as organizations adapt to the dynamic demands of the modern industrial landscape, the transition from fossil fuels to renewable energy sources is anticipated to drive substantial investments in energy infrastructure, hence accelerating steel consumption within this sector.

Restraint

Raw Material Volatility

High-grade coking coal required for conventional blast furnaces confronts severe regional shortages, forcing many countries to import substantial amounts of their metallurgical coal needs, which is the major factor hindering market growth. Moreover, conventional steelmaking processes require an extensive amount of power. Frequent inconsistencies in the power grid and elevated electricity tariffs directly threaten operational continuity.

Opportunity

Rapid Infrastructure Development

The rapid growth of infrastructure projects across the region is the key factor creating lucrative opportunities in the market. Governments are heavily investing in transportation bridges, networks, and urban development, which requires significant quantities of steel. Furthermore, these investments are set to significantly benefit the global iron and steel industry, where the demand for durable materials remains critical. Rising urbanization will further drive steel demand as expanding cities require robust infrastructure to support growing populations.

Segmental Insights

Type Insights

The steel segment dominated the market with the largest share of 71.60% in 2025 and is expected to grow at the fastest CAGR of 5.28% over the forecast period. The dominance and growth of the segment can be attributed to the increasing demand for high-performance steel grades and green steel initiatives, boosting advanced steel investments in the region.

") The iron segment held the market share of 28.40% In 2025. The growth of the segment can be credited to the ongoing infrastructure projects supporting pig iron consumption and growing iron demand from foundry and industrial applications. Metallurgical sectors are maintaining iron processing activities across Europe.

The iron segment held the market share of 28.40% In 2025. The growth of the segment can be credited to the ongoing infrastructure projects supporting pig iron consumption and growing iron demand from foundry and industrial applications. Metallurgical sectors are maintaining iron processing activities across Europe.

Europe Iron and Steel Market Share,By Type, 2025 (%)

| By Type | Revenue Share, 2025 (%) |

| Iron | 28% |

| Steel | 72% |

Production Method Insights

The blast furnace–basic oxygen furnace (BF–BOF) route segment dominated the market with the largest share of 56.20% in 2025. The dominance of the segment can be linked to the established infrastructure and persistence of BF-BOF operations in the region. Also, integrated steel plants maintain large steel manufacturing capacity.

The hydrogen-based steelmaking segment held the market share of 4.70% in 2025 and is expected to grow at the fastest CAGR of 11.48% over the forecast period. The growth of the segment can be driven by green hydrogen investment supporting low-emission steel production and the enforcement of decarbonization policies, fuelling hydrogen steel project development.

")

The electric arc furnace (EAF) route segment held the market share of 29.80% in 2025. The growth of the segment is owed to the lower emissions, encouraging investment in electric steelmaking technologies and renewable energy integration, boosting sustainable production strategies. Scrap availability supports efficient EAF steel production.

Europe Iron and Steel Market Share,By Production Method, 2025 (%)

| By Production Method | Revenue Share, 2025 (%) |

| Blast Furnace–Basic Oxygen Furnace (BF–BOF) Route | 56% |

| Electric Arc Furnace (EAF) Route | 30% |

| Direct Reduced Iron (DRI) Route | 9% |

| Hydrogen-Based Steelmaking | 5% |

Form Insights

The finished segment dominated the market with the largest share of 65.30% in 2025 and is expected to grow at the fastest CAGR of 5.22% during the projected period. The dominance and growth of the segment is owed to the increasing demand for value-added steel grades from the automotive and infrastructure sectors. Coating and rolling technologies are improving finished product quality further.

The semi-finished segment held the market share of 34.70% in 2025. The growth of the segment is due to export demand supporting semi-finished steel trade flows and integrated mills maintaining steady intermediate product output. Steel processors need slabs and billets for downstream operations.

Europe Iron and Steel Market Share, By Form, 2025 (%)

| By Form | Revenue Share, 2025 (%) |

| Semi-Finished | 35% |

| Finished | 65% |

Application Insights

The construction & infrastructure segment dominated the market with the largest share of 35.60% in 2025. The dominance of the segment can be attributed to the green building standards promoting durable steel materials and public investments supporting bridges and transport construction. Urban development will soon drive steel demand.

The energy & utilities segment held the market share of 11.80% in 2025 and is expected to grow at the fastest CAGR of 5.88% over the forecast period. The growth of the segment can be credited to the increasing demand for speciality steel products due to a surge in energy transition investments. Renewable energy installations increase steel requirements substantially.

The automotive & transportation segment held the market share of 20.10% in 2025. The growth of the segment can be linked to the green building standards promoting durable steel materials and heavy public investments supporting bridges and transport construction. Urban development can drive demand further.

Europe Iron and Steel Market Share, By Application, 2025 (%)

| By Application | Revenue Share, 2025 (%) |

| Construction & Infrastructure | 36% |

| Automotive & Transportation | 20% |

| Mechanical Equipment | 15% |

| Energy & Utilities | 12% |

| Defense & Aerospace | 7% |

| Consumer Appliances | 10% |

Country Insights

How did Germany Dominate the Europe Iron and Steel Market in 2025?

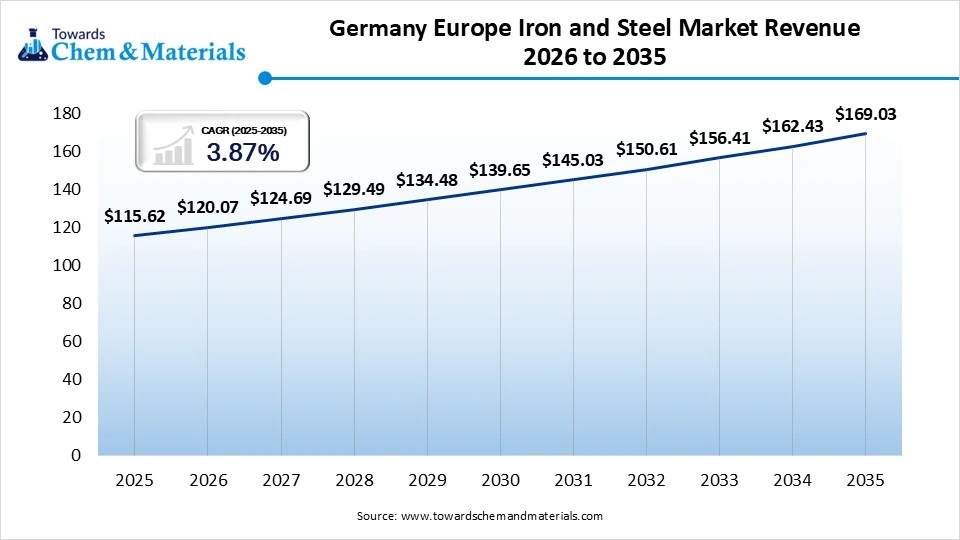

The Germany iron and steel market size was estimated at USD 115.62 billion in 2025 and is projected to reach USD 169.03 billion by 2035, growing at a CAGR of 3.87% from 2026 to 2035.Germany dominated the market with the largest share of 24.80% in 2025. The dominance of the country can be attributed to the surge in investment in green steel and the strong presence of major industrial and automotive players in the emerging region. In addition, government initiatives aim to establish a surge in demand by focusing on low-emission steel in public procurement, like rail, road, and renewable energy infrastructure.

The France iron and steel market size was estimated at USD 62.00 billion in 2025 and is projected to reach USD 93.87 billion by 2035, growing at a CAGR of 4.23% from 2026 to 2035.France held the market share of 13.30% in 2025 and is expected to grow at the fastest CAGR of 5.14% over the forecast period. The growth of the country can be credited to the increasing speciality demand from the automotive and aerospace sector, coupled with the government's decarbonisation policies, boosting market expansion. The conversion towards EVs needs advanced & lightweight high-strength steels (AHSS) for battery enclosures and safety-critical structural components.

The France iron and steel market size was estimated at USD 62.00 billion in 2025 and is projected to reach USD 93.87 billion by 2035, growing at a CAGR of 4.23% from 2026 to 2035.France held the market share of 13.30% in 2025 and is expected to grow at the fastest CAGR of 5.14% over the forecast period. The growth of the country can be credited to the increasing speciality demand from the automotive and aerospace sector, coupled with the government's decarbonisation policies, boosting market expansion. The conversion towards EVs needs advanced & lightweight high-strength steels (AHSS) for battery enclosures and safety-critical structural components.

Recent Development

- In January 2026, the European Union and India proposed the elimination of tariffs on iron and steel products, a development that will yield substantial advantages for manufacturers operating across both jurisdictions. This zero-tariff framework would eliminate trade barriers and elevate the global competitiveness of multinational conglomerates such as Tata Steel.(Source: scanx.trade)

Europe Iron and Steel Market Companies

- ArcelorMittal: ArcelorMittal is a Luxembourg-headquartered multinational and the largest steel producer in the European Union. Operating in 8 European countries with over 48,000 employees, the company commands a dominant share of the continent's automotive, construction, and flat steel markets.

- Tata Steel: Tata Steel is Europe's second-largest steel producer, operating primary steelmaking facilities in the UK (Port Talbot) and the Netherlands (IJmuiden). The company supplies premium flat and strip steel to major European sectors, navigating a market recently shaped by CBAM regulations, safeguard duties, and green-steel transitions.

Other Companies in the Market

- SSAB

- voestalpine

- Salzgitter AG

- CELSA Group

- Outokumpu

- Acerinox

- Aperam

- LKAB

- Would you

Segments Covered in the Report

By Type

- Iron

- Pig Iron

- Direct Reduced Iron

- Cast Iron

- Steel

- Carbon Steel

- Low Carbon Steel

- Medium Carbon Steel

- High Carbon Steel

- Alloy Steel

- Stainless Steel

- Tool Steel

- High-strength Alloy Steel

- Carbon Steel

By Production Method

- Blast Furnace–Basic Oxygen Furnace (BF–BOF) Route

- Integrated Steel Plants

- Coke-based Ironmaking

- Electric Arc Furnace (EAF) Route

- Scrap-based EAF

- DRI-fed EAF

- Direct Reduced Iron (DRI) Route

- Gas-based DRI

- Coal-based DRI

- Hydrogen-Based Steelmaking

- Green Hydrogen DRI

- Pilot Hydrogen Steel Projects

By Form

- Semi-Finished

- Slabs

- Billets

- Blooms

- Finished

- Flat Products

- Hot Rolled Products

- Cold Rolled Products

- Coated Products

- Long Products

- Rebars

- Wire Rods

- Structural Sections

- Flat Products

By Application

- Construction & Infrastructure

- Buildings

- Bridges

- Rail Infrastructure

- Automotive & Transportation

- Passenger Vehicles

- Commercial Vehicles

- Railway Equipment

- Mechanical Equipment

- Industrial Machinery

- Heavy Equipment

- Machine Tools

- Energy & Utilities

- Power Generation

- Oil & Gas Infrastructure

- Renewable Energy Equipment

- Defense & Aerospace

- Military Equipment

- Aerospace Components

- Naval Applications

- Consumer Appliances

- White Goods

- Kitchen Appliances

- HVAC Equipment

By Country

- Germany

- UK

- France

- Russia

- Spain

- Italy

- Rest of Europe

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

Tags

FAQ's

Select User License to Buy

Figures (6)