Content

Chemical Intermediate Market Analysis, Demand and Growth Rate Forecast

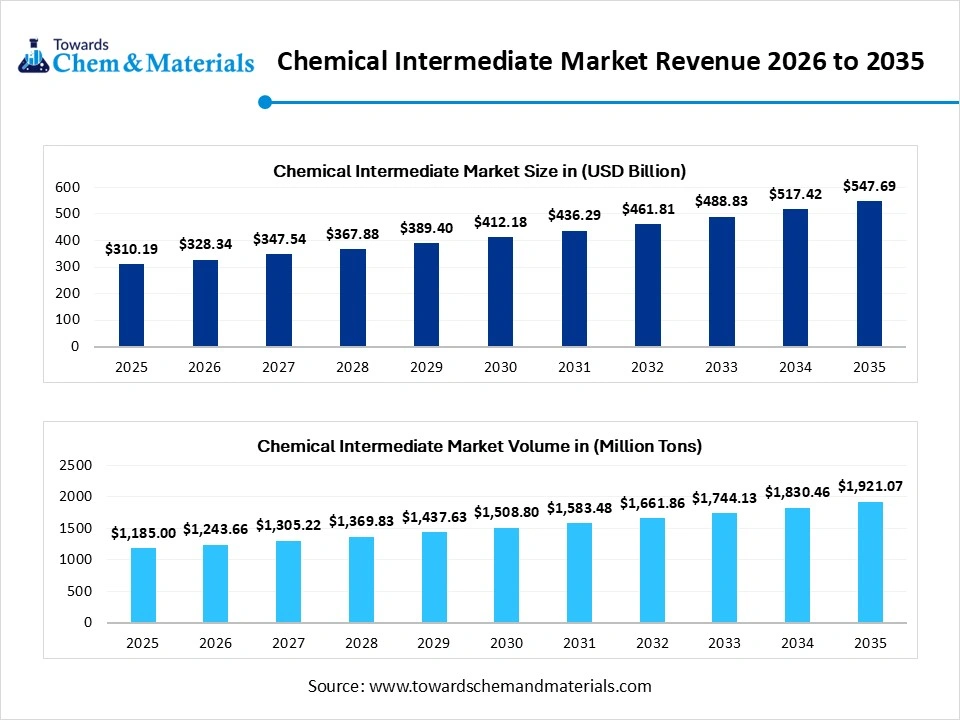

The global chemical intermediate market was valued at USD 310.19 billion in 2025, is estimated to reach USD 328.34 billion in 2026, and is projected to reach USD 547.69 billion by 2035, growing at a CAGR of 5.85% from 2026 to 2035. In terms of volume, the chemical intermediate market is projected to grow from 1185 million tons in 2025 to 1921.07 million tons by 2035. growing at a CAGR of 4.95% from 2026 to 2035.

Key Takeaways

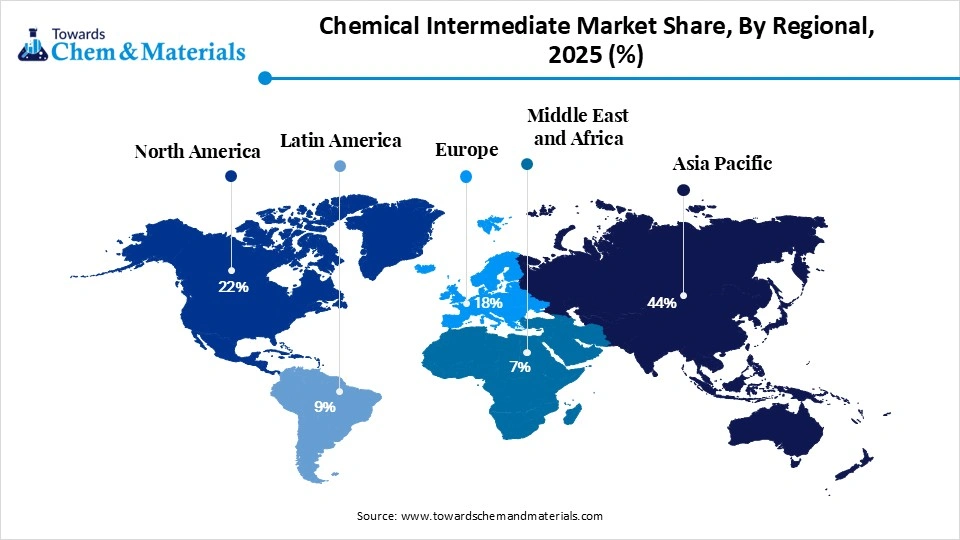

- By region, Asia Pacific dominated the market with a share of 44% in 2025 and is expected to sustain its position while growing with a CAGR of 6.5% in the forecast period.

- By region, North America held 22% market share in 2025.

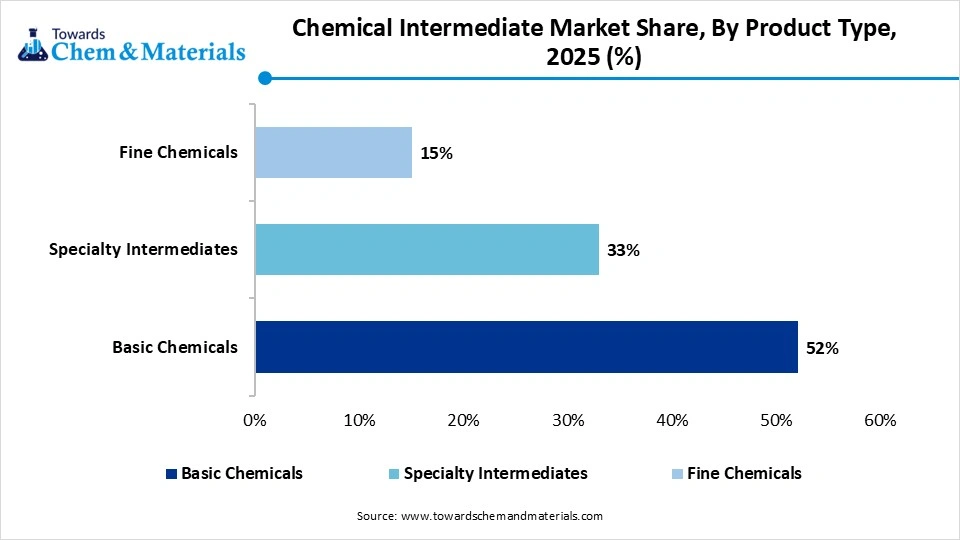

- By product type, the basic chemicals segment dominated the market with 52% share in 2025.

- By product type, the specialty intermediates segment held 33% market share in 2025 and is expected to have the fastest growth with a CAGR of 6.7% in the forecast period.

- By application, the plastics and polymers segment dominated the market with 26% share in 2025.

- By application, the pharmaceutical segment held the 28% market share in 2025 and is expected to have the fastest growth with a CAGR of 6.8% in the forecast period.

- By end-use industry, the consumer goods segment dominated the market with 24% share in 2025.

- By end-use industry, the healthcare segment held the 15% market share in 2025 and is expected to have the fastest growth with a CAGR of 6.9% in the forecast period.

- By production process, the batch processing segment dominated the market with 48% share in 2025.

- By production process, the continous processing segment held 37% market share in 2025 and is expected to have the fastest growth with a CAGR of 6.4% in the forecast period.

- By raw material source, the fossil-based segment dominated the market with 72% share in 2025.

- By raw material source, the bio-based segment held the 28% market share in 2025 and is expected to have the fastest growth with a CAGR of 7.2% in the forecast period.

Market Size and Volume Forecast

- Market Estimated Size (2026): USD 328.34 Billion | CAGR (2026–2035): 5.85%

- Market Projected Size (2035): USD 547.69 Billion

- Market Volume (2025): 1,185.00 Million Tons (MT) | Volume CAGR (2026–2035): 4.95%

- Market Projected Volume (2035): 1,921.07 Million Tons (MT)

- Market Pricing (2025):

- Average Manufacturing Price: USD 825/ton

- Average Selling Price: USD 1,055/ton

- Pricing CAGR (2025–2035): 3.8%

Market Overview

What Is the Significance of the Chemical Intermediate Market?

The market for chemical intermediates is crucial because it supplies key components like solvents, reagents, and precursors used to produce final products in sectors such as pharmaceuticals, agrochemicals, plastics, and automotive industries. Valued for supporting efficient, high-yield manufacturing, this market is propelled by growing demand for specialty chemicals, a rise in chronic diseases increasing pharmaceutical needs, and the urgent push for sustainable, bio-based solutions.

Recent Market Growth Trends:

- Sustainability & Green Chemistry: Environmental regulations are forcing a shift away from traditional hazardous chemicals toward eco-friendly, biodegradable, and bio-based alternatives.

- Production Technology Shifts: There is a strong industry trend towards continuous-flow manufacturing and automated, data-driven, or "smart" manufacturing, reducing the reliance on traditional batch processes.

- High-Growth Sectors: The pharmaceutical and agrochemical industries are major drivers, demanding high-purity intermediates to meet growing, complex product requirements.

Report Scope

| Report Attribute | Report Attribute |

| Market Size and Volume in 2026 | USD 328.34 Billion / 1243.66 Million Metric Tons |

| Expected Size and Volume by 2035 | USD 547.69 Billion / 1921.07 Million Metric Tons |

| Growth Rate from 2026 to 2035 | CAGR 5.85% |

| Forecast Period | 2026 - 2035 |

| Dominant Region | Asia Pacific |

| Segment Covered | By Product Type, By Application, By End-Use Industry, By Production Process, By Raw Material Source and By Regions |

| Key companies profiled | Weyerhaeuser, Dewitt Products LLC, Arauco, Gemini Particleboard Pvt Ltd, Norbord, Pine Wood Canada, Wood Resources International LLC, Finsa, Shannon Wood Products, Sukup Manufacturing Co, Kronospan, Biesse SpA, Veneer Products Ltd, Panel Processing Inc, INEOS Group, Mitsubishi Chemical Group Corporation, Sumitomo Chemical Co., Ltd., LG Chem Ltd., Reliance Industries Limited |

Key Technological Shifts in the Chemical Intermediate Market

The chemical intermediate market is shifting rapidly towards sustainability, digitalization, and efficiency, driven by green chemistry, AI-driven synthesis, and bio-based feedstocks. Advancements in recycling technologies are turning chemical waste into reusable intermediates, with projects focused on recovering polyurethane waste. The shift toward electrifying chemical reactors for critical steps like oxidation and nitration is reducing dependence on fossil fuels.

Trade Analysis of Chemical Intermediate Market: Import & Export Statistics

- According to Global Export Data, the world exported 561 Chemical Intermediates shipments between June 2024 and May 2025 (TTM) via 126 verified exporters and 35 buyers.

- Colombia, the United States, and China lead as the top Chemical Intermediates importers, while the United States with 2,951 shipments, Mexico with 365 shipments, and India with 339 shipments are the leading exporters of Chemical Intermediates.

Top-performing Global Chemical Intermediates Exporters by volume

- TETRA PAK GLOBAL SUPPLY S A: 51 shipments (20%)

- Firmeneich Inc.: 44 shipments (17%)

- Firmenich of Mexico S.A. de C.V.: 28 shipments (11%)

Supply Chain Analysis of Chemical Intermediate Market

Chemical Synthesis and Processing

Chemical intermediates are produced through various synthesis processes, including oxidation, reduction, alkylation, and catalytic reactions, to serve as key building blocks in the production of end-use chemicals and materials.

- Key players: BASF, Dow, Lanxess, Eastman Chemical Company

Quality Testing and Certification

Chemical intermediates must comply with purity standards, safety regulations, and environmental guidelines to ensure suitability for downstream manufacturing processes.

- Key players: International Organization for Standardization, European Chemicals Agency, U.S. Environmental Protection Agency, and Occupational Safety and Health Administration.

Distribution to Industrial Users

Chemical intermediates are supplied to pharmaceutical manufacturers, agrochemical companies, polymer producers, coatings and dyes industries, and specialty chemical manufacturers.

- Key players: BASF, Dow, Lanxess

Chemical Intermediate Regulatory Landscape: Global Regulations

| Country / Region | Regulatory Body | Key Regulations | Focus Areas | Notable Notes |

| U.S. | Environmental Protection Agency (EPA); Occupational Safety and Health Administration (OSHA) | Toxic Substances Control Act (TSCA); OSHA Hazard Communication Standard; Clean Air Act | Chemical safety, worker protection, emissions control | Chemical intermediates must comply with strict safety, labeling, and environmental regulations due to their hazardous nature and industrial usage. |

| Europe | European Chemicals Agency (ECHA); European Commission | REACH Regulation; CLP Regulation | Chemical registration, classification, safe industrial use | The EU mandates detailed registration and hazard assessment for chemical intermediates under REACH, with strict labeling requirements. |

| China | Ministry of Ecology and Environment (MEE); Ministry of Emergency Management (MEM) | Environmental Protection Law; | Work Safety Law Industrial chemical safety, environmental compliance | China regulates chemical intermediates production with strict safety and pollution control standards. |

| India | Ministry of Environment, Forest and Climate Change (MoEFCC); Central Pollution Control Board (CPCB) | Environment Protection Act; Manufacture, Storage and Import of Hazardous Chemicals Rules | Hazardous chemical management, emissions monitoring | India enforces regulations for safe handling, storage, and disposal of chemical intermediates. |

| Japan | Ministry of Economy, Trade and Industry (METI); Ministry of Health, Labour and Welfare (MHLW) | Chemical Substances Control Law (CSCL); Industrial Safety and Health Act | Chemical risk management, occupational safety | Japan requires strict compliance for chemical intermediates related to industrial and pharmaceutical production. |

| South Korea | Ministry of Environment (MoE); Ministry of Trade, Industry and Energy (MOTIE) | K-REACH; Chemicals Control Act | Chemical registration, hazardous substance management | South Korea regulates chemical intermediates through comprehensive chemical safety and registration frameworks. |

Market Dynamics

Drivers

What are the Key Growth Drivers of the Chemical Intermediate Market?

The chemical intermediate market is primarily driven by surging demand from the pharmaceutical, agrochemical, and polymer industries, alongside rapid industrialization, particularly in the Asia-Pacific region. Key factors include the adoption of green chemistry and bio-based alternatives, high-value manufacturing, process intensification technologies, and strategic capacity expansions. Developing nations are boosting demand for raw materials to support infrastructure, construction, and consumer goods manufacturing.

Restrains

What are the Key Growth Restraints of the Chemical Intermediate Market?

Key growth restraints for the chemical intermediate market include stringent environmental regulations requiring costly compliance, high raw material price volatility, specifically petrochemical feedstocks, and global supply chain disruptions. Additionally, the shift toward sustainable/bio-based alternatives, geopolitical tensions, and high capital investment requirements limit market expansion.

Opportunities

What are the Key Growth Opportunities of the Chemical Intermediate Market?

Key growth opportunities in the chemical intermediate market are driven by sustainability-focused bio-based products, rising demand for customized specialty chemicals in pharmaceuticals and agrochemicals, and expanding manufacturing in Asia Pacific and the Middle East. Rising demand for advanced materials, adhesives, and polymers is opening up new revenue streams for specialty intermediates.

Segmental Insights

Product Type Insights

The Basic Chemicals Segment Dominated The Market With 52% Market Share In 2025

The basic chemicals segment dominated the market with 52% share in 2025, driven by high-purity, versatile products such as ethylene amines and caustic products, which are critical to expanding downstream industries like pharmaceuticals and electronics. Growth is further fueled by rapid industrialization, the adoption of sustainable alternatives, and a strong rebound in demand across Asia Pacific.

The specialty intermediates segment held 33% market share in 2025 and is expected to have the fastest growth with a CAGR of 6.7% in the forecast period, driven by surging demand from pharmaceuticals, agrochemicals, and high-performance materials. This growth is catalyzed by the shift towards green chemistry, supply chain diversification, and the adoption of advanced manufacturing technologies. The adoption of continuous-flow production and biocatalysis is enhancing productivity, lowering costs, and driving market development.

The fine chemicals segment held 15% market share in 2025, driven by surging demand for high-purity intermediates in pharmaceuticals and advanced agrochemicals. Growth is accelerated by increased outsourcing to Contract Development and Manufacturing Organizations (CDMOs) and adoption of green chemistry. Increasing adoption of green chemistry to minimize environmental impact attracts regulatory support and meets demand for eco-friendly products.

Application Insights

The Plastics And Polymers Segment Dominated The Market With 26% Market Share In 2025

The plastics and polymers segment dominated the market with 26% share in 2025, driven by surging demand for lightweight, durable materials in packaging, automotive, and construction, alongside a massive shift toward sustainable, bio-based polymers. Increased regulatory pressure and environmental awareness are driving demand for biodegradable, bio-based plastics and circular polymers.

Chemical Intermediate Market Share, By Application, 2025 (%)

| By Application | Revenue Share, 2025 (%) |

| Pharmaceuticals | 28% |

| Agrochemicals | 22% |

| Plastics & Polymers | 26% |

| Textiles | 14% |

| Electronics | 10% |

The pharmaceuticals segment held 28% market share in 2025 and is expected to have the fastest growth with a CAGR of 6.8% in the forecast period, due to surging demand for active pharmaceutical ingredients (APIs), rising chronic disease prevalence, and increased outsourcing to Contract Manufacturing Organizations (CMOs). The market is further boosted by advancements in drug delivery, generic expansion, and the need for specialty, high-purity intermediates.

The agrochemicals segment held 22% market share in 2025, due to surging demand for food, increasing pest resistance necessitating new formulations, and a shift toward sustainable, precision agriculture. Increasing consumption of cereals and grains requires higher crop yields, boosting the consumption of crop protection chemicals. There is strong growth in bio-pesticides and bio-fertilizers, aligned with global sustainability goals, alongside AI-integrated precision farming.

The textiles segment held 14% market share in 2025, driven by a strong shift toward sustainable "green" chemistry, the expansion of technical textiles in industries like automotive and healthcare, and the rapid rise of digital printing technologies. Technical textiles, such as those used for protective clothing, medical applications (PPE), and automotive, are growing faster than traditional apparel. These materials require specialized chemical treatments, including antimicrobial agents, flame retardants, and water repellents.

End-Use Industry Insights

The Consumer Goods Segment Dominated The Market With 24% Share In 2025

The consumer goods segment dominated the market with 24% share in 2025. The chemical intermediate market plays a crucial role in consumer goods by supplying essential raw materials used to produce products like plastics, cosmetics, detergents, and textiles. These intermediates enable efficient large-scale manufacturing, improve product quality, and support innovation, helping companies meet consumer demand while maintaining cost-effectiveness and consistent performance across industries.

Chemical Intermediate Market Share, By End-Use Industry, 2025 (%)

| By End-Use Industry | Revenue Share, 2025 (%) |

| Healthcare | 15% |

| Agriculture | 20% |

| Automotive | 14% |

| Construction | 17% |

| Electronics & Electrical | 10% |

| Consumer Goods | 24% |

The healthcare segment held the 15% market share in 2025 and is expected to have the fastest growth with a CAGR of 6.9% in the forecast period. The chemical intermediate market is vital in healthcare, providing key compounds used in the production of pharmaceuticals, vaccines, and medical supplies. These intermediates enable precise drug formulation, ensure consistency and safety, and support large-scale manufacturing, helping improve treatment effectiveness, accelerate drug development, and meet the growing global demand for reliable healthcare solutions.

Production Process Insights

The Batch Processing Segment Dominated The Market With 48% Market Share In 2025

The batch processing segment dominated the market with 48% share in 2025, driven by a surge in demand for specialty chemicals, personalized pharmaceuticals, and high-purity intermediates. While continuous manufacturing is gaining traction, batch processing is rapidly evolving through digitalization and modularization to meet needs for flexibility, traceability, and stringent regulatory compliance. Batch processes are being transformed by Industry 4.0 technologies. The integration of IoT, artificial intelligence (AI), and advanced process control (APC) is reducing human error and boosting efficiency.

Chemical Intermediate Market Share, By Production Process, 2025 (%)

| By Production Process | Revenue Share, 2025 (%) |

| Batch Processing | 48% |

| Continuous Processing | 37% |

| Bioprocessing | 15% |

The continuous processing segment held 37% market share in 2025 and is expected to have the fastest growth with a CAGR of 6.4% in the forecast period, driven by the need for higher production efficiency, reduced waste, and improved safety. The shift toward flow chemistry allows for superior process control, optimized heat transfer, and faster product development cycles compared to traditional batch methods, notably in specialty chemical and pharmaceutical manufacturing.

The bioprocessing segment held 15% market share in 2025, driven by a rapid shift toward sustainable, bio-based alternatives and the surging demand for biologics. The market is transforming from traditional petroleum-based synthetic methods to industrial bioprocessing using microorganisms, enzymes, and cell cultures to produce chemicals, to achieve lower carbon emissions, better production efficiency, and improved product sustainability.

Raw Material Source Insights

The Fossil-Based Segment Dominated The Market With 72% Market Share In 2025

The fossil-based segment dominated the market with 72% share in 2025, due to established infrastructure, cost efficiency, and high-volume demand in petrochemicals. The growth of the market supports large-scale petrochemical production due to increased demand. The industry also benefits from established supply chains, which increase exports to consumers. Maintains cost competitiveness, further fuels the growth and expansion of the market.

Chemical Intermediate Market Share, By Raw Material Source, 2025 (%)

| By Raw Material Source | Revenue Share, 2025 (%) |

| Fossil-based | 72% |

| Bio-based | 28% |

The bio-based segment held 28% market share in 2025 and is expected to have the fastest growth with a CAGR of 7.2% in the forecast period, driven by rising demand for sustainable alternatives, advancements in biotechnology (fermentation/enzyme engineering), and stringent environmental regulations. Key growth factors include increased investment in biomass refineries, favorable government policies, and a strategic shift from petro-based to renewable feedstocks.

Regional Insights

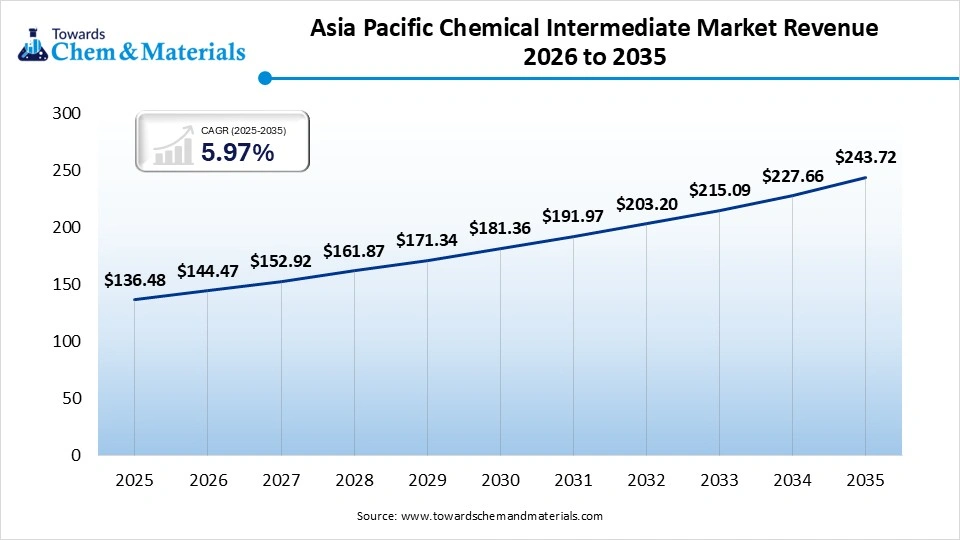

How did Asia Pacific Dominate the Chemical Intermediate Market in 2025?

The Asia Pacific chemical intermediate market size was estimated at USD 136.48 billion in 2025 and is projected to reach USD 243.72 billion by 2035, growing at a CAGR of 5.97% from 2026 to 2035, driven by rapid industrialization, strong manufacturing demand in China and India, and expanding pharmaceutical, agrochemical, and automobile sectors. Growth is propelled by low production costs, supportive government policies, and the adoption of advanced technologies like AI and continuous-flow manufacturing.

India Chemical Intermediate Market Growth Factor

The Indian chemical intermediate market is driven by booming demand in pharmaceuticals and agrochemicals, shifting global manufacturing to India, and robust investment in petrochemicals. Key drivers include the "Make in India" initiative, high demand for specialty chemicals, and increasing exports. Manufacturers are moving to India to diversify supply chains, supported by Government policies like Production Linked Incentive (PLI) schemes.

North America Chemical Intermediate Market Growth Factor

North America held 22% market share in 2025, driven by high demand from the pharmaceutical, agrochemical, and automotive sectors, paired with advanced manufacturing infrastructure and shale gas feedstock advantages. Robust R&D investments and a shift toward sustainable, bio-based chemical production are fueling market growth. The region’s dominance in pharmaceutical R&D, coupled with rapid growth in Contract Manufacturing Organizations (CMOs) and Contract Research Organizations (CROs), drives high demand for specialized intermediates.

U.S. Chemical Intermediate Market Growth Factor

The U.S. chemical intermediate market is growing, driven by robust demand in pharmaceuticals, agrochemicals, and specialized manufacturing, alongside a strong shift toward sustainable, bio-based alternatives. Growth is supported by increased industrial infrastructure investment and the need for high-performance specialty chemicals, despite challenges from regulatory pressures and geopolitical uncertainties.

Recent Developments

- In February 2026, NEXTCHEM launched the NXPand suite, a technological platform featuring NX CONSER PolyFlex technology for producing spandex fiber, marking its entry into the sustainable textile market. The technology enables the production of PTMEG using conventional or bio-based feedstock, with application in technical apparel and sportswear.

- In October 2025, Chemetall and Londian Wason have partnered to introduce Gardolene® D, the industry's first chromium- and fluoride-free passivation solution for copper foils used in lithium batteries. The main aim of this technology is to improve the capacity of battery retention, which makes upto 6% this initiative is to meet the environmental regulations amid growing concerns.

Top players in the Chemical Intermediate Market & Their Offerings

- BASF SE: BASF is one of the largest global producers of chemical intermediates, supplying a wide range of products, including amines, alcohols, acids, and solvents. The company benefits from its integrated Verbund production system, ensuring efficiency and cost optimization.

- Dow Inc.: Dow produces a diverse portfolio of chemical intermediates, including ethylene derivatives, propylene derivatives, and specialty chemicals.

- Eastman Chemical Company: Eastman manufactures a broad range of intermediates such as acetyl chemicals, solvents, and plasticizers.

- Huntsman Corporation: Huntsman produces intermediates used in polyurethanes, performance products, and advanced materials. Its offerings support industries including construction, automotive, textiles, and industrial manufacturing.

- SABIC: SABIC supplies key chemical intermediates derived from petrochemical processes, including olefins, aromatics, and glycols.

Chemical Intermediate Market Top Players

- Weyerhaeuser

- Dewitt Products LLC

- Arauco

- Gemini Particleboard Pvt Ltd

- Norbord

- Pine Wood Canada

- Wood Resources International LLC

- Finsa

- Shannon Wood Products

- Sukup Manufacturing Co

- Kronospan

- Biesse SpA

- Veneer Products Ltd

- Panel Processing Inc

- INEOS Group

- Mitsubishi Chemical Group Corporation

- Sumitomo Chemical Co., Ltd.

- LG Chem Ltd.

- Reliance Industries Limited

Chemical Intermediate Market Segments Covered

By Product Type

- Basic Chemicals

- Petrochemical Intermediates

- Ethylene Derivatives

- Propylene Derivatives

- Inorganic Intermediates

- Acids

- Alkalis

- Petrochemical Intermediates

- Specialty Intermediates

- Pharmaceutical Intermediates

- API Intermediates

- Custom Intermediates

- Agrochemical Intermediates

- Herbicide Intermediates

- Pesticide Intermediates

- Polymer Additives Intermediates

- Pharmaceutical Intermediates

- Fine Chemicals

- Electronic Chemicals

- Flavors & Fragrances Intermediates

By Application

- Pharmaceuticals

- Generic Drugs

- Specialty Drugs

- Agrochemicals

- Fertilizers

- Crop Protection Chemicals

- Plastics & Polymers

- Packaging

- Automotive Plastics

- Textiles

- Dyes

- Finishing Chemicals

- Electronics

- Semiconductors

- Display Materials

By End-Use Industry

- Healthcare

- Agriculture

- Automotive

- Construction

- Electronics & Electrical

- Consumer Goods

By Production Process

- Batch Processing

- Continuous Processing

- Bioprocessing

By Raw Material Source

- Fossil-based

- Oil-derived

- Gas-derived

- Bio-based

- Plant-based Feedstock

- Waste-derived Feedstock

By Regions

- North America

- U.S.

- Canada

- Mexico

- U.S.

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Germany

- Asia Pacific

- China

- India

- Japan

- South Korea

- China

- Latin America

- Brazil

- Argentina

- Brazil

- Middle East & Africa

- Saudi Arabia

- South Africa

- Saudi Arabia

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

Tags

FAQ's

Select User License to Buy

Figures (4)