Content

Renewable Ethanol Market Size, Share, Analysis and Forecast 2035

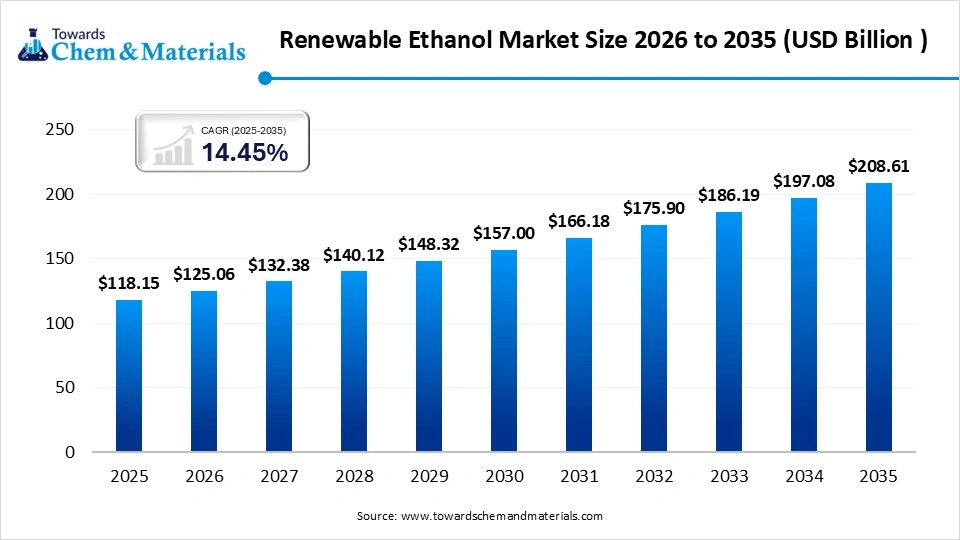

The global renewable ethanol market size was estimated at USD 118.15 billion in 2025 and is expected to increase from USD 125.06 billion in 2026 to USD 208.61 billion by 2035, growing at a CAGR of 14.45% from 2026 to 2035. Asia Pacific dominated the renewable ethanol market with the largest revenue share of 14.45% in 2025.The growth of the market is driven by the global decarbonization, strict blending mandates, and its role in sustainable aviation fuel, which fuels the growth of the market.

The renewable ethanol market plays an essential role in decreasing greenhouse gas emissions by 52% lower than gasoline, while boosting energy security by replacing imported oil and generating economic value through bio-based fuel production. Its rapid growth is fueled by mandatory blending policies, decarbonization targets, and increasing use in sustainable aviation fuels. Ethanol greatly reduces harmful tailpipe emissions like particulate matter and carbon monoxide, as well as greenhouse gases. It is regarded as a key instrument for reaching carbon neutrality in transportation, with notable improvements in production efficiency.

")

Market Highlights

- The North America dominated renewable ethanol market with the largest revenue share of 41.00% in 2025. increasing demand for low-carbon fuels, and technological progress

- By feedstock/type, the corn-based ethanol segment dominated the market and accounted for the largest revenue share of 38.00% in 2025. high availability, and strong policy mandates

- By feedstock/type, the cellulosic ethanol segment is projected to grow at the fastest CAGR between 2026 and 2035, driven by its sustainable nature and technological advancements.

- By production process, the fermentation of starch crops segment led the market with the largest revenue share of 36.00% in 2025, driven by its commercial viability and widespread adoption

- By production process, the cellulosic conversion segment is projected to grow at the fastest CAGR between 2026 and 2035. sustainability benefits and utilization of non-food biomass.

- By application, the transportation fuel segment dominated the market and accounted for the largest revenue share of 41.00% in 2025, maintain its dominance and experience rapid growth

- By application, the industrial solvents & chemicals segment is projected to grow at the fastest CAGR between 2026 and 2035, driven by its high demand in applications.

- By end-use industry, the automotive / transportation led the market with the largest revenue share of 48.00% in 2025, Driven by the urgent need to reduce greenhouse gas emissions

- By end-use industry, the chemical industry segment is projected to grow at the fastest CAGR between 2026 and 2035. Driven by its increasing use in sustainable aviation fuel.

Key Technological Shifts In The Renewable Ethanol Market:

The renewable ethanol market is moving toward second-generation (2G) cellulosic ethanol, which uses non-food biomass such as agricultural residue to enhance sustainability. Major advancements include cutting-edge enzymatic hydrolysis, improved fermentation techniques, the integration of Carbon Capture, Utilization, and Storage, and AI-powered process optimization to reduce carbon footprint and boost yields, supporting net-zero targets. Additionally, Artificial Intelligence and the Internet of Things are being employed for real-time monitoring and enhancement of fermentation, distillation, and supply chain operations, thus increasing overall efficiency.

What is Renewable Ethanol Used for?

- Fuel: One of its biggest uses is as a biofuel, particularly in vehicles. It's blended with gasoline to create a cleaner alternative to traditional fossil fuels. This blend, commonly called ethanol fuel (such as E10, E15, or E85), helps reduce greenhouse gas emissions and can be more sustainable than petroleum-based fuels.

- Energy Production: Renewable ethanol can be used in power plants to generate electricity. It provides an alternative to burning coal or natural gas, contributing to cleaner energy solutions.

- Industrial Solvent: In industries, renewable ethanol is used as a solvent for cleaning, extracting flavors, or even in products like perfumes, cosmetics, and pharmaceuticals.

- Chemical Production: It serves as a starting material for producing chemicals like acetic acid, ethyl acetate, and other solvents, which are used in everything from food preservation to plastics.

- Alcoholic Beverages: Renewable ethanol is the main ingredient in the production of alcoholic drinks like beer, wine, and spirits.

- Disinfectants and Sanitizers: Ethanol is used in products like hand sanitizers, as it’s effective at killing bacteria and viruses, especially in health and hygiene applications.

Trade Analysis of the Renewable Ethanol Market: Import & Export Statistics

According to Global Export Data, the world exported 25,612 Ethanol Alcohol shipments through 2,229 verified exporters and 2,718 buyers

Top-performing Global Ethanol Alcohol Exporters by volume:

- CONG TY TNHH TM-SX NONG SAN THUC PHAM QUOC TE QUAN: 2,345 shipments (38%)

- TRICON ENERGY LTD: 1,171 shipments (19%)

- CV VIETNAM TRADING SERVICE IMPORT AND EXPORT COMPANY LTD.: 553 shipments (9%)

Market Growth Trends:

- Advanced/Cellulosic Ethanol Shift: There is a significant transition from first-generation to second-generation, cellulosic ethanol produced from agricultural waste.

- Sustainability & Low Carbon Focus: Producers are heavily investing in technology to reduce the carbon intensity of ethanol to meet stricter environmental regulations.

- SAF and Green Chemicals: Beyond transportation, ethanol is increasingly used in producing sustainable aviation fuel (SAF), bio-plastics, and green solvents.

Report Scope

| Report Attribute | Details |

| Market Size in 2026 | USD 125.06 Billion |

| Revenue Forecast in 2035 | USD 208.61 Billion |

| Growth Rate | CAGR 14.45% |

| Forecast Period | 2026 - 2035 |

| Base Year | 2025 |

| Dominant Region | Asia Pacific |

| Segment Covered | By Feedstock / Type, By Production Process, By Application, By End-Use Industry, By Regions |

| Key companies profiled | COFCO Corporation, CropEnergies AG, BlueFire Renewables, Iogen Corporation, Alto Ingredients, POET LLC, Archer Daniels Midland Company, Green Plains Inc., Valero Energy Corporation, Royal Dutch Shell PLC, Cargill Inc., DuPont de Nemours Inc., Abengoa Bioenergy, Advanced Biofuels USA, NutraSweet Company, Biofuel Energy Corp., Raízen S.A., BP Bunge Bioenergia, The Andersons Inc., Tereos Group, Processing. |

Renewable Ethanol Market - Supply Chain Analysis

Biofuel Production & Processing

- Renewable ethanol is produced through fermentation of biomass feedstocks such as corn, sugarcane, wheat, and cellulosic materials, followed by distillation and dehydration to obtain fuel-grade ethanol.

- Key Players: POET, Archer Daniels Midland, Valero Energy, Raízen.

Quality Testing & Certification

- Renewable ethanol must meet fuel purity standards, environmental sustainability criteria, and transportation fuel regulations before blending or distribution.

Key Authorities & Standards: U.S. Environmental Protection Agency, ASTM International, International - Organization for Standardization, European Commission.

Distribution to End-Use Industries

- Renewable ethanol is supplied to fuel blending companies, transportation fuel distributors, chemical manufacturers, and energy providers for use as a renewable fuel and industrial feedstock.

- Key Suppliers: POET, Archer Daniels Midland, Valero Energy.

Renewable Ethanol Regulatory Landscape: Global Regulations 5x6

| Country / Region | Regulatory Body | Key Regulations | Focus Areas | Notable Notes |

| US | Environmental Protection Agency (EPA); Department of Energy (DOE) | Renewable Fuel Standard (RFS); Clean Air Act | Biofuel blending mandates, emission reduction, and renewable fuel certification | The U.S. promotes renewable ethanol production through blending mandates and renewable identification number (RIN) credits to reduce transportation emissions. |

| Europe | European Commission; European Environment Agency (EEA) | Renewable Energy Directive (RED II); Fuel Quality Directive | Renewable fuel targets, sustainability criteria, and carbon reduction | The EU supports renewable ethanol through biofuel mandates and sustainability certification to lower greenhouse gas emissions in the transport sector. |

| Brazil | National Agency of Petroleum, Natural Gas and Biofuels (ANP); Ministry of Mines and Energy | RenovaBio Policy; National Biofuels Policy | Biofuel production incentives, carbon intensity reduction | Brazil is a global leader in sugarcane-based ethanol and promotes production through decarbonization credits and fuel blending mandates. |

| China | National Development and Reform Commission (NDRC); Ministry of Ecology and Environment (MEE) | Biofuel Development Plan; Renewable Energy Law | Ethanol blending, energy security, and emission control | China encourages fuel ethanol blending and production to reduce dependence on fossil fuels and support agricultural resource utilization. |

| India | Ministry of Petroleum and Natural Gas (MoPNG); Ministry of New and Renewable Energy (MNRE) | National Biofuel Policy; Ethanol Blended Petrol (EBP) Programme | Ethanol blending targets, renewable fuel adoption | India promotes ethanol production through blending targets in petrol and incentives for biofuel production from agricultural feedstocks. |

Segmental Insights

Feedstock / Type Insights

How did the Corn-Based Ethanol Segment Dominate the Renewable Ethanol Market in 2025?

The corn-based ethanol segment dominated the market share 38% in 2025, driven by record production levels of approximately 16.3 billion gallons, particularly in the United States. This dominance is underpinned by established infrastructure, high availability, and strong policy mandates, such as the Renewable Fuel Standard (RFS). Increased demand for cleaner, renewable fuels to reduce greenhouse gas emissions is boosting bio-based feedstock utilization.

The cellulosic ethanol segment is projected to grow at the fastest CAGR between 2026 and 2035 in the market, driven by its sustainable nature and technological advancements. The broader renewable fuel market, including advanced biofuels, is growing due to rising environmental regulations, decarbonization targets, and increased investments in biorefineries. Cellulosic ethanol, often derived from non-food agricultural waste, is becoming a priority for sustainable energy solutions.

Renewable Ethanol Market Share, By Feedstock / Type, 2025 (%)

| By Feedstock / Type | Revenue Share, 2025 (%) |

| Corn-Based Ethanol | 38.00% |

| Sugarcane-Based Ethanol | 27.00% |

| Cellulosic Ethanol | 16.00% |

| Algae-Based Ethanol | 8.00% |

| Others | 11.00% |

- Corn-Based Ethanol – Dominating with a 38.00% share, abundant feedstock availability, established production infrastructure, and cost efficiency drive widespread adoption.

- Sugarcane-Based Ethanol – With a 27.00% share, higher conversion efficiency and strong presence in sugarcane-rich regions support significant market contribution.

- Cellulosic Ethanol – Holding a 16.00% share, increasing focus on sustainable and non-food-based feedstocks is driving growth, though technological and cost challenges limit scale.

- Others – With an 11.00% share, diverse feedstock sources provide flexibility, but lack of standardization restricts broader market dominance.

- Algae-Based Ethanol – With an 8.00% share, high potential for sustainability supports innovation, but early-stage commercialization and high production costs limit adoption.

Production Process Insights

Which Production Process Dominated the Renewable Ethanol Market in 2025?

The fermentation of starch crops segment dominated the market share 36.00% in 2025. This dominance is driven by the mature, cost-effective, and large-scale production technology available for starch-based ethanol. Starch-based ethanol, with corn as the primary feedstock, holds the largest share of the market, driven by its commercial viability and widespread adoption.

The cellulosic conversion segment is projected to grow at the fastest CAGR between 2026 and 2035 in the market, driven by its sustainability benefits and utilization of non-food biomass. While overall ethanol markets are growing, this sector is specifically a high-growth area for advanced biofuels. Cellulosic conversion uses non-food feedstocks like agricultural waste, which reduces environmental impact and competition with food supplies.

Renewable Ethanol Market Share, By Production Process, 2025 (%)

| By Production Process | Revenue Share, 2025 (%) |

| Fermentation of Sugar Crops | 36.00% |

| Fermentation of Starch Crops | 33.00% |

| Cellulosic Conversion (Lignocellulosic Biomass) | 19.00% |

| Other Advanced Processes | 12.00% |

- Fermentation of Sugar Crops – Dominating with a 36.00% share, high conversion efficiency, lower processing complexity, and strong availability in sugarcane-rich regions drive leading adoption.

- Fermentation of Starch Crops – With a 33.00% share, abundant feedstock supply (especially corn) and well-established production infrastructure support widespread usage.

- Cellulosic Conversion (Lignocellulosic Biomass) – Holding a 19.00% share, increasing focus on sustainable, non-food-based feedstocks is driving growth, though high costs and technological challenges limit scale.

- Other Advanced Processes – With a 12.00% share, emerging technologies offer innovation potential, but limited commercialization and scalability restrict broader market dominance.

Application Insights

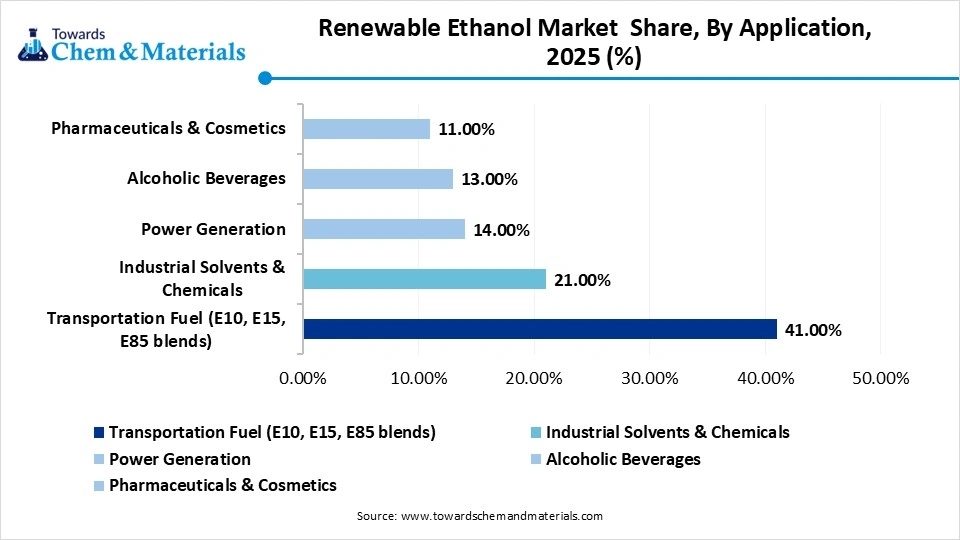

How did the Transportation Fuel Segment Dominate the Renewable Ethanol Market in 2025?

The transportation fuel segment dominated the market in 2025, driven by global mandates for E10/E85 blending and decarbonization goals. This segment is expected to maintain its dominance and experience rapid growth, with expanding production capacities for bio-based feedstock ethanol to meet high-octane fuel demand. Growth is propelled by increased blending mandates, the rise of Flexible Fuel Vehicles, and technological advancements in cellulosic ethanol, which fuel the growth.

")

The industrial solvents & chemicals segment is projected to grow at the fastest CAGR between 2026 and 2035 in the market, poised for rapid growth in the market, driven by its high demand in applications like paints, coatings, and pharmaceutical formulations, as industries pivot toward sustainable alternatives. The shift is supported by increasing regulatory pressure to move away from petroleum-based solvents and the versatility of ethanol in high-purity applications.

Renewable Ethanol Market Share, By Application, 2025 (%)

| By Application | Revenue Share, 2025 (%) |

| Transportation Fuel (E10, E15, E85 blends) | 41.00% |

| Industrial Solvents & Chemicals | 21.00% |

| Power Generation | 14.00% |

| Alcoholic Beverages | 13.00% |

| Pharmaceuticals & Cosmetics | 11.00% |

- Transportation Fuel (E10, E15, E85 blends) – Dominating with a 41.00% share, strong regulatory mandates, widespread fuel blending practices, and rising demand for low-emission fuels drive the highest consumption.

- Industrial Solvents & Chemicals – With a 21.00% share, extensive use in chemical manufacturing and solvent applications supports significant industrial demand.

- Power Generation – Holding a 14.00% share, growing use of renewable fuels for electricity generation contributes to steady market expansion.

- Alcoholic Beverages – With a 13.00% share, consistent demand from beverage production maintains stable consumption levels.

- Pharmaceuticals & Cosmetics – With an 11.00% share, increasing use in sanitizers, formulations, and personal care products supports moderate growth, though limited volume restricts higher share.

End-Use Industry Insights

Which End-Use Industry Dominated the Renewable Ethanol Market in 2025?

The automotive / transportation segment dominated the market share 48.00% in 2025, driven by the urgent need to reduce greenhouse gas emissions and comply with government mandates for biofuel blending in gasoline, such as India's 20% ethanol blending (E20) goal and the U.S. Renewable Fuel Standard. The market for fuel ethanol is anticipated to continue growing as countries prioritize energy security and environmental regulations.

The chemical industry segment is projected to grow at the fastest CAGR between 2026 and 2035 in the market, driven by its increasing use in sustainable aviation fuel (SAF), green solvents, and biodegradable plastics. This segment aligns with industrial decarbonization goals, with ethanol derivatives showing high potential for replacing fossil-based feedstocks. Rising demand for eco-friendly products and sustainable, bio-based chemicals is accelerating the use of renewable ethanol in chemical manufacturing.

Renewable Ethanol Market Share, By End-Use Industry, 2025 (%)

| By End-Use Industry | Revenue Share, 2025 (%) |

| Automotive / Transportation | 48.00% |

| Chemical Industry | 18.00% |

| Food & Beverage | 13.00% |

| Pharmaceutical & Healthcare | 11.00% |

| Energy & Power | 10.00% |

- Automotive / Transportation – Dominating with a 48.00% share, widespread fuel blending adoption, strong policy support, and rising demand for low-emission fuels drive the largest consumption.

- Chemical Industry – With an 18.00% share, extensive use as a solvent and feedstock in chemical manufacturing supports significant industrial demand.

- Food & Beverage – Holding a 13.00% share, steady demand from beverage production and food processing maintains consistent market contribution.

- Pharmaceutical & Healthcare – With an 11.00% share, increasing use in disinfectants, sanitizers, and medical formulations supports stable growth.

- Energy & Power – With a 10.00% share, growing use of ethanol in power generation contributes to moderate demand, though limited scale restricts higher share.

Regional Insights

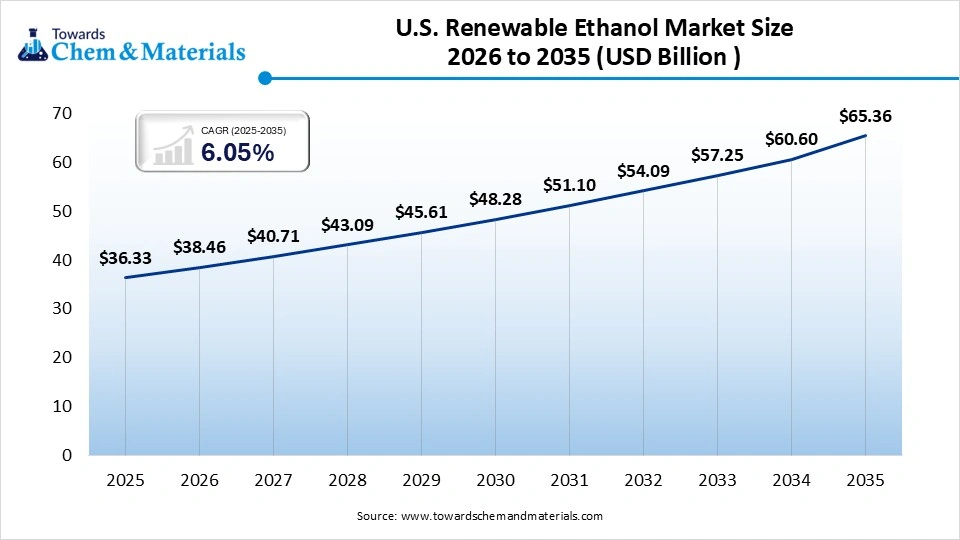

U.S. renewable ethanol market size was valued at USD 36.33 billion in 2025 and is expected to be worth around USD 65.36 billion by 2035, exhibiting at a compound annual growth rate (CAGR) of 6.05% over the forecast period from 2026 to 2035The U.S. renewable ethanol market is experiencing robust growth, driven mainly by federal policies such as the Renewable Fuel Standard (RFS), rising international demand, and the adoption of higher-octane blends like E15. Ethanol's key role as a low-carbon octane enhancer in transportation fuels this growth. The EPA's RFS requires high levels of renewable fuel blending, ensuring steady demand. Additionally, increased consumer awareness and corporate sustainability efforts focused on cutting greenhouse gas emissions are contributing to this upward trend.

")

North America Renewable Ethanol Market Growth Factor

The North America renewable ethanol market size was valued at USD 48.44 billion in 2025 and is expected to be worth around USD 86.57 billion by 2035, exhibiting at a compound annual growth rate (CAGR) of 5.98% over the forecast period from 2026 to 2035. North America dominated the market in 2025, due to the U.S. Renewable Fuel Standard (RFS) mandates, extensive corn-based production capacity, and modern infrastructure. Strong government incentives, increasing demand for low-carbon fuels, and technological progress in cellulosic ethanol all contributed to this leadership. The U.S., in particular, leveraged its large agricultural sector and advanced biorefineries, especially in the Midwest, to produce substantial amounts of corn ethanol.

Asia Pacific Renewable Ethanol Market Growth Factor

Asia Pacific is expected to have the fastest growth in the market in the forecast period, due to government blending mandates, such as India's E20 target, in China and Thailand, which are key drivers, along with rising fuel consumption driven by increasing vehicle ownership and initiatives to cut carbon emissions. The growth is supported by abundant agricultural resources such as sugarcane and corn, rising industrial demand in sectors like pharmaceuticals and cosmetics, and investments in advanced second-generation ethanol technology, supporting growth.

India Renewable Ethanol Market Growth Factor

India's renewable ethanol market is rapidly expanding. Key drivers include the government's ambitious target to achieve 20% ethanol blending (E20), which aims to enhance energy security, cut crude oil imports, reduce emissions, and boost rural incomes. The National Policy on Biofuels and the Ethanol Blended Petrol program offer vital incentives. Market growth is expected to accelerate further due to rising infrastructure investments, especially from the sugar industry, which has invested around ₹40,000 crore to expand production capacity.

")

Europe Renewable Ethanol Market Growth Factor

The renewable ethanol market in Europe is expected to expand considerably, driven by strict EU decarbonization targets, the requirement to blend E10, and rising demand for sustainable aviation fuel. Major growth factors encompass industrial demand, investments in second-generation bioethanol, and energy security policies. The main catalyst is the European Union’s commitment to achieving carbon neutrality, which has led to mandatory biofuel blending in transportation, particularly the adoption of E10 (10% ethanol) petrol.

Germany Renewable Ethanol Market Growth Factor

The German renewable ethanol market is growing rapidly, supported by strict EU decarbonization goals, high E10 blending requirements, and advanced sustainable production methods. Growth is driven by abundant agricultural feedstock, rising demand for low-carbon fuels, and investment in second-generation, residue-based biofuels. Germany's strong commitment to achieving carbon neutrality fuels the demand for biofuels through binding quotas on greenhouse gas reductions in transportation, which also boosts ethanol blending rates.

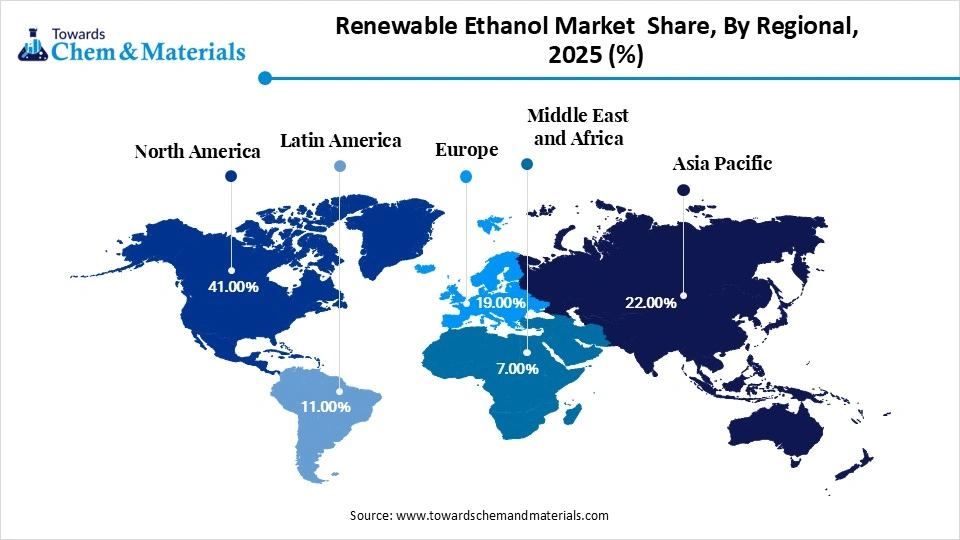

Renewable Ethanol Market Share, By Regional, 2025 (%)

| Regional | Revenue Share, 2025 (%) |

| North America | 41.00% |

| Europe | 19.00% |

| Asia Pacific | 22.00% |

| Latin America | 11.00% |

| Middle East & Africa | 7.00% |

North America – Dominating with a 41.00% share, strong government mandates, large-scale corn-based ethanol production, and well-established fuel blending infrastructure drive market leadership.

Asia Pacific – With a 22.00% share, rising energy demand, growing biofuel adoption, and supportive policies contribute to steady market expansion.

Europe – Holding a 19.00% share, stringent emission regulations and increasing renewable fuel usage support consistent demand, though growth remains moderate.

Latin America – With an 11.00% share, strong sugarcane-based ethanol production and export capabilities support significant regional contribution.

Middle East & Africa – Making up 7.00% of the market, emerging renewable initiatives and limited production infrastructure result in a smaller overall market presence.

Recent Developments

- In January 2024, Brazil inaugurated its 22nd corn-based ethanol facility, marking a significant expansion in the country's biofuel industry. The new facility, part of a surge that has seen production jump to over 7.7 billion litres in 2024, reinforces a strategic shift towards utilizing "second-crop" corn for year-round production.(Source: www.chemanalyst.com)

Top players in the Renewable Ethanol Market & Their Offerings:

- COFCO Corporation: COFCO plays a major role in Asia’s renewable ethanol production through vertically integrated operations, including grain processing, ethanol manufacturing, and distribution. The company supports China’s biofuel blending policies and expanding domestic ethanol demand.

- CropEnergies AG: CropEnergies produces sustainable ethanol primarily from cereals and sugar crops. The company supplies renewable ethanol for fuel blending, food and beverage industries, and industrial chemical applications across Europe.

- BlueFire Renewables: BlueFire Renewables develops advanced technologies for producing ethanol from biomass such as agricultural residues and municipal waste. The company focuses on second-generation cellulosic ethanol solutions to reduce greenhouse gas emissions.

- Iogen Corporation: Iogen specializes in advanced cellulosic ethanol technology using enzymatic hydrolysis to convert agricultural residues into renewable fuel. The company has invested heavily in R&D and has developed multiple patents for advanced biofuel production.

- Alto Ingredients: Alto Ingredients operates several ethanol production facilities producing renewable ethanol and specialty alcohols for fuel, food, and industrial markets. The company is also investing in carbon capture projects to reduce emissions from ethanol production.

- POET LLC

- Archer Daniels Midland Company

- Green Plains Inc.

- Valero Energy Corporation

- Royal Dutch Shell PLC

- Cargill Inc.

- DuPont de Nemours Inc.

- Abengoa Bioenergy

- Advanced Biofuels USA

- NutraSweet Company

- Biofuel Energy Corp.

- Raízen S.A.

- BP Bunge Bioenergia

- The Andersons Inc.

- Tereos Group

- Grain Processing Corporation (Kent Corporation)

Segments Covered:

By Feedstock / Type

- Corn-Based Ethanol

- Sugarcane-Based Ethanol

- Cellulosic Ethanol

- Algae-Based Ethanol

By Production Process

- Fermentation of Sugar Crops

- Fermentation of Starch Crops

- Cellulosic Conversion (Lignocellulosic Biomass)

- Other Advanced Processes

By Application

- Transportation Fuel (E10, E15, E85 blends)

- Industrial Solvents & Chemicals

- Power Generation

- Alcoholic Beverages

- Pharmaceuticals & Cosmetics

By End-Use Industry

- Automotive / Transportation

- Chemical Industry

- Food & Beverage

- Pharmaceutical & Healthcare

- Energy & Power

By Regions

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Asia Pacific

- China

- India

- Japan

- South Korea

- Latin America

- Brazil

- Argentina

- Middle East & Africa

- Saudi Arabia

- South Africa

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

FAQ's

Select User License to Buy

Figures (4)