Content

What is the Advanced Composites Market Size and Share?

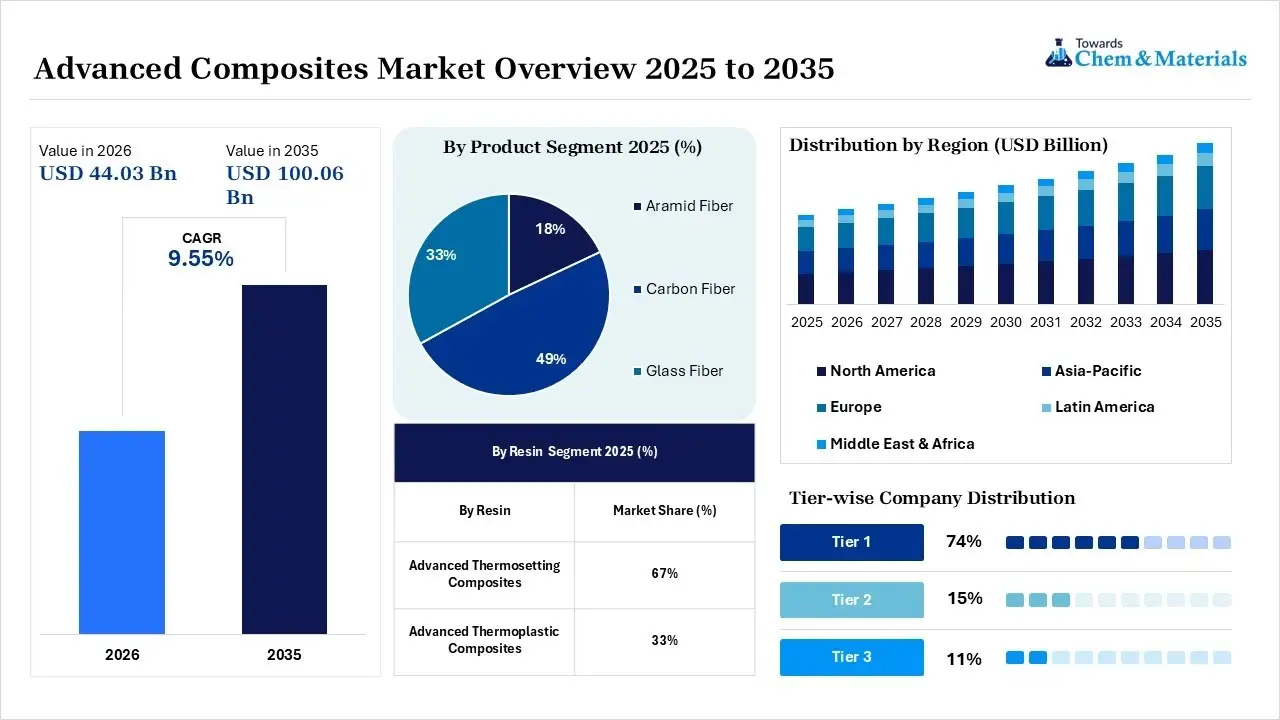

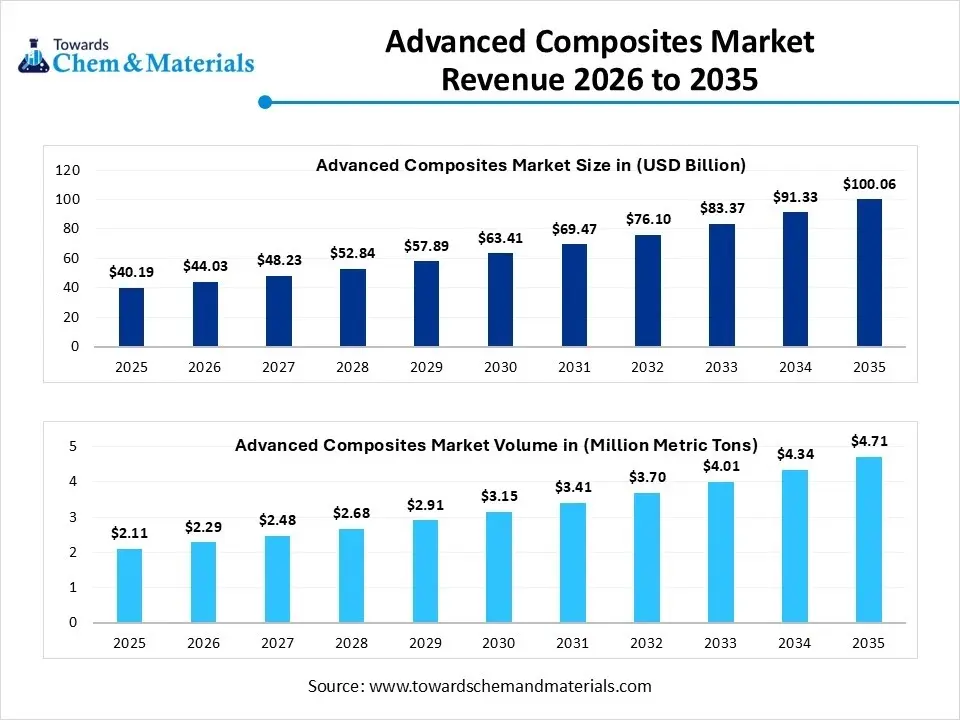

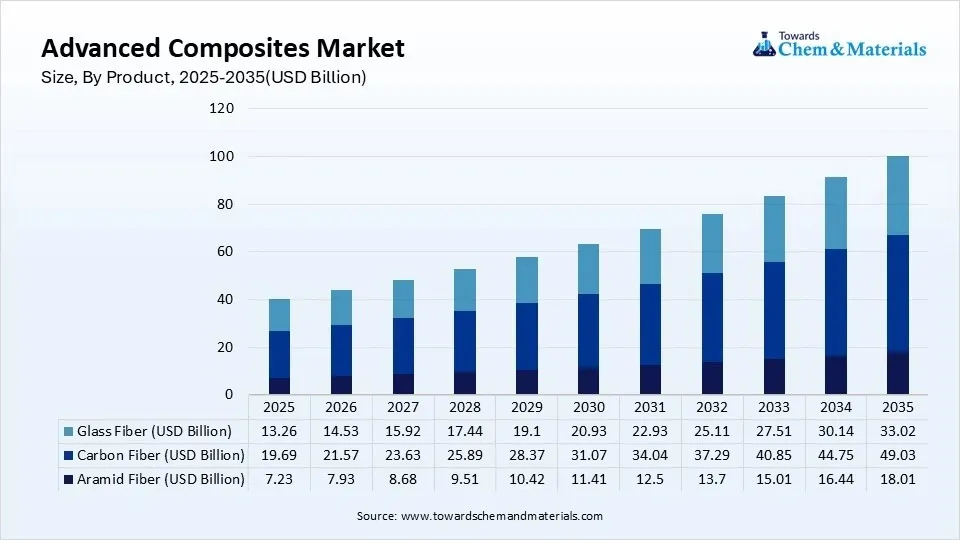

The global advanced composites market size was valued at USD 40.19 billion in 2025, is estimated to reach USD 44.03 billion in 2026, and is projected to reach USD 100.06 billion by 2035, exhibiting a compound annual growth rate (CAGR) of 9.55% over the forecast period from 2026 to 2035.Asia Pacific dominated the advanced composites market with the largest revenue share of 34% in 2025 and is expected to grow at the fastest CAGR of 9.71% during the forecast period. The market is highly significant because it produces ultra-lightweight, high-strength materials essential for modern engineering. The Advanced Composites partners with leading firms across the aerospace, automotive, and industrial sectors; similarly, Hexcel works with FIDAMC (Foundation for Research, Development, and Application of Composite Materials) to shape the future of advanced materials according to the report.

Market Highlights

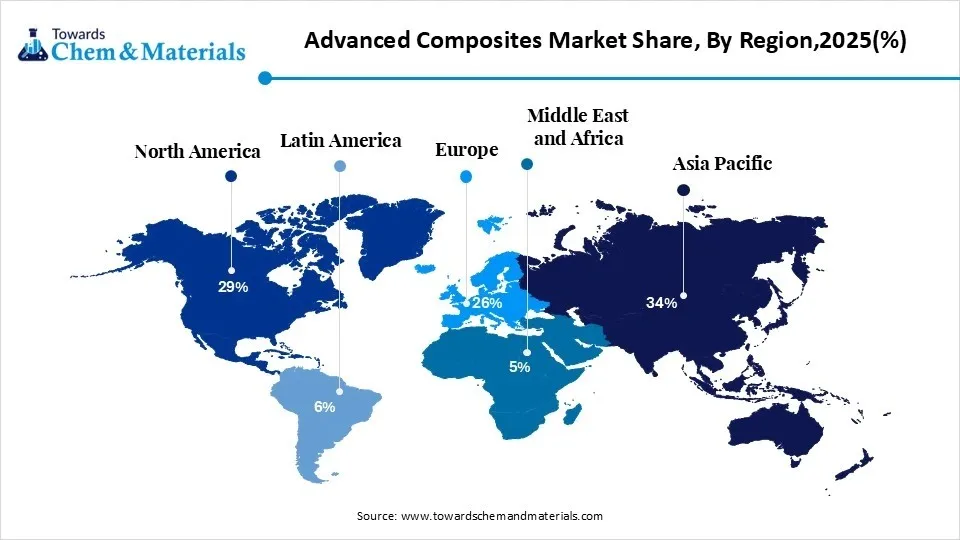

- By region, Asia Pacific dominated the market with a share of 34% in 2025. Industrialization accelerates composite manufacturing.

- By region, North America held 29% market share in 2025 and is expected to experience the fastest growth with a CAGR of 11.34% in the forecast period. Strong aerospace manufacturing supports composite consumption.

- By product, the carbon fiber segment dominated the market with 49% share in 2025. Aerospace and EV manufacturers are increasingly replacing metals with carbon composites.

- By product, the glass fiber segment held 33% market share in 2025 and is expected to have the fastest growth with a CAGR of 10.88% in the forecast period. Wind energy installations accelerate demand for structural composites.

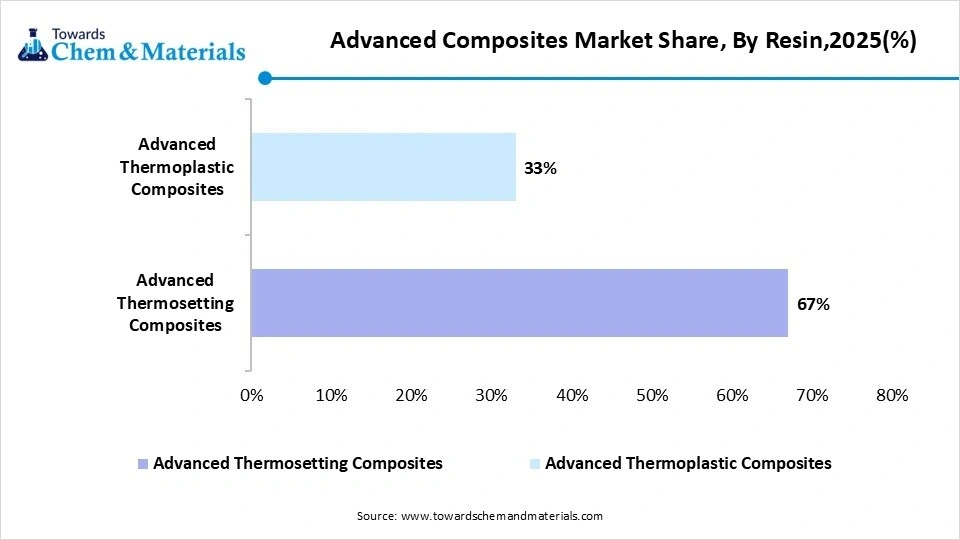

- By resin, the advanced thermosetting composites segment dominated the market with 67% share in 2025. Superior mechanical strength supports aerospace and wind blade production.

- By resin, the advanced thermoplastic composites segment held 33% market share in 2025 and is expected to have the fastest growth with a CAGR of 11.46% in the forecast period. Recyclability and rapid molding accelerate automotive adoption.

The advanced composites market is the industry responsible for creating high-performance, lightweight materials made by combining two or more distinct substances. These materials matter globally because they offer extreme strength while weighing significantly less than traditional metals, making them essential for saving fuel and reducing emissions across aerospace, automotive, and renewable energy sectors.

Advanced composites are foundational to modern aircraft and spacecraft. Because these materials are exceptionally strong yet lightweight, they enable planes to carry heavier loads while using less fuel. They are used to build airplane wings, fuselages, and defense systems. Wind turbines require massive, lightweight, and durable blades to catch the wind. Advanced composites allow for longer blades that spin easily and produce more electricity.

In the automotive industry, lightweighting is critical. Every pound saved in a vehicles body extends its battery range. Advanced composites are increasingly used for EV battery enclosures, providing excellent crash protection, heat resistance, and structural stability. Compared to normal metals, these high-tech materials do not rust easily and can withstand intense heat and physical stress.

- For instance, Merlinhawk Composites and Engineering Pvt. Ltd. officially launched its advanced composites aerospace manufacturing facility in Shoolagiri, Tamil Nadu, located within the Tamil Nadu Defence Industrial Corridor.(Source: www.tribuneindia.com)

Advanced Composites Market Trends

- The increasing adoption in the automotive sector is driving advanced composites market growth in the current period. As automakers are increasingly shifting toward lightweight materials like carbon fiber and glass fiber composites to improve fuel efficiency and meet stringent emission regulations. As electric vehicles (EVs) gain traction, demand for advanced composites in battery enclosures, structural frames, and interior components is rising.

- The aerospace industry continues to be a major consumer of advanced composites, particularly for structural components that require high strength-to-weight ratios. Aircraft manufacturers are incorporating carbon fiber composites in fuselage, wings, and interior panels to reduce weight and enhance fuel economy.

- Rapid expansion of the renewable energy sector is fueling demand for advanced composites, especially in wind energy. Composite materials such as glass fiber are extensively used in wind turbine blades due to their strength, corrosion resistance, and long service life. As countries increase their wind power capacities, manufacturers are developing longer, lighter blades using advanced molding technologies.

- Advanced composites are gaining attention in the construction industry for use in infrastructure, bridges, and building components. Fiber-reinforced polymers (FRPs) offer corrosion resistance, low maintenance, and high strength, making them ideal for long-term applications in harsh environments. With rising demand for durable, lightweight building materials, the construction sector is integrating smart composite technologies for structural reinforcement in the current period.

Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 44.03 Billion/ 2.29 Million Metric Tons |

| Expected Size by 2035 | USD 100.06 Billion/ 4.71 Million Metric Tons |

| Growth Rate | CAGR 9.55% |

| Base Year of Estimation | 2025 |

| Forecast Period | 2025 - 2035 |

| Dominant Region | Asia Pacific |

| Segment Covered | By Product, By Resin, By Application, By Region |

| Key Companies Profiled | Toray Industries, Inc., Koninklijke Ten Cate NV Teijin Limited, Hexcel Corporation, SGL Group, Cytec Solvay Group, Owens Corning, E. I. Dupont De Nemours and Company, Huntsman Corporation, Momentive Performance Materials Inc., WS Atkins plc, AGY Holdings Corp., Formosa Plastics Corporation, Plasan Carbon Composites, Strata Manufacturing |

Supply Chain Analysis of the Advanced Composites Market:

Composite Material Production & Processing

- Advanced composites are produced by combining high-performance fibers such as carbon fiber, glass fiber, and aramid fiber with polymer resin systems to create lightweight materials with superior strength, stiffness, and durability.

- Toray Industries: Toray Industries manufactures carbon fiber and advanced composite materials used in aerospace, automotive, wind energy, and industrial applications. The company focuses on lightweight solutions that improve fuel efficiency and structural performance.

- Key Players: Hexcel Corporation, Toray Industries, Solvay, Teijin Limited.

Quality Testing & Certification

- Advanced composites must comply with standards for tensile strength, fatigue resistance, fire performance, impact resistance, and structural reliability before use in critical applications.

- Hexcel Corporation: Hexcel Corporation develops aerospace-grade composite materials, prepregs, and honeycomb structures that meet stringent certification requirements for commercial aircraft, defense systems, and space applications.

- Key Authorities & Standards: International Organization for Standardization, ASTM International, Federal Aviation Administration, European Union Aviation Safety Agency.

Distribution to End-Use Industries

- Advanced composites are supplied to aerospace manufacturers, automotive companies, wind turbine producers, marine industries, and sporting goods manufacturers for high-performance lightweight applications.

- Solvay: Solvay supplies advanced composite materials and resin systems for aerospace, automotive, and industrial markets, helping manufacturers reduce weight while maintaining high mechanical performance and durability.

- Key Suppliers: Hexcel Corporation, Toray Industries, Solvay.

Advanced Composites Market Opportunity

Precision Performance : Composites for Every Application

Product customization and targeting niche markets in several regions is expected to create significant opportunities for the advanced composites market during the forecast period. From sports equipment and medical devices to marine and robotics applications, end-users are seeking tailored solutions that meet specific performance criteria. This demand is opening new opportunities for specialized composite formulations with unique mechanical, thermal, and aesthetic properties. Manufacturers who can offer design flexibility and small-batch production capabilities stand to capture high margins in the coming years.

Advanced Composites Market Challenge

High-Tech, High Cost

High production costs and limited production volume are expected to hamper the advanced composites market growth during the forecast period. The complexity of processing materials like carbon fiber and the need for specialized equipment can produce production expenses in the coming years. Moreover, scaling operations while maintaining consistent quality creates a challenge, specifically for small and mid-sized investors or producers. Also, these cost barriers can hinder wider adoption in price-sensitive sectors such as automotive or construction.

Regional Insights

How did Asia Pacific dominate the Advanced Composites Market in 2025?

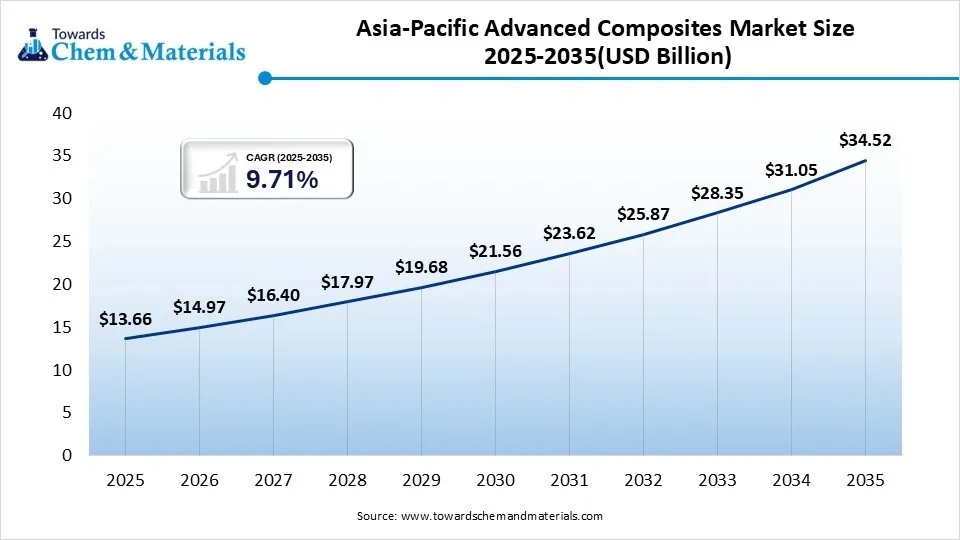

The Asia Pacific advanced composites market size was estimated at USD 13.66 billion in 2025 and is projected to reach USD 34.52 billion by 2035, growing at a CAGR of 9.71% from 2026 to 2035.Asia Pacific dominated the market with the largest share of 34% in 2025.Asia Pacific dominated the market with the largest share of 34% in 2025. This leadership was driven by mass-scale automotive manufacturing, major wind energy projects, and rapid industrialization in countries like China, Japan, and South Korea. Governments backed massive renewable energy installations, which require massive composite blades for wind turbines. The region utilized high-volume, cost-effective glass-fiber and carbon-fiber production lines to supply global electronics and industrial markets.

")

China

- China builds many large wind farms. Wind turbine blades use strong composites to catch more wind and survive harsh weather.

- Chinas national goals push for cleaner energy and greener manufacturing. This forces industries to use modern, energy-saving materials.

India

- Government policies encourage local production and the setup of carbon fiber value chains. This helps the country rely less on imported materials.

- India is building a large hub for defense and aviation manufacturing. States like Gujarat have big auto and defense clusters that drive local demand.

North America Advanced Composites Market Growth Factor

North America held a market share of 29% in 2025and is expected to grow at the fastest CAGR of 11.34% over the forecast period, driven by its use in making high-strength, lightweight, and durable parts. The region holds a significant market share, fueled by the aerospace, defense, electric vehicle (EV), and wind energy industries. Aerospace and defense are the largest user of advanced composites. Companies use these materials to build lighter aircraft and military equipment, which improves fuel efficiency and performance. Innovations in bio-based materials and recyclable thermoplastics also support eco-friendly manufacturing goals, driving growth in the region.

United States

- The United States has a massive aerospace and defense sector. Aircraft and military equipment require advanced composites to reduce weight, which saves fuel and increases range.

- Strict government rules push companies to reduce pollution. Using composite materials helps meet these goals by making machines run more efficiently.

Canada

- Canada has large aerospace hubs in cities like Montreal and Toronto. Companies use advanced composites to make airplanes lighter. This lowers fuel use and cuts down pollution.

- Advanced composites are widely used in wind turbine blades. Canadas push for clean energy infrastructure helps drive this demand.

Europe Advanced Composites Market Growth Factor

Europe held a market share of 26% in 2025, driven by the strong demand for lightweight, high-strength materials. Key sectors like aerospace, automotive, renewable energy (wind turbines), and defense are leading this growth, fueled by strict environmental regulations and sustainability targets. European countries enforce strict limits on carbon emissions from vehicles. Automotive makers use advanced composites to make cars lighter. Lighter cars need less fuel and emit fewer greenhouse gases.

")

Germany

The German advanced composites market is growing rapidly due to the rising demand for lightweight materials, strict carbon emission rules, and a strong push for electric vehicles (EVs).

Germanys massive automotive industry, like BMW and Volkswagen, heavily uses composites to replace heavy metals, offsetting the weight of heavy battery packs and increasing range

France

European climate policies like the European Green Deal and Fit-for-55 pressure industries to shift toward lower-carbon materials.

France is expanding its wind energy sector. Advanced composites are crucial for making massive, highly durable turbine blades.

Companies are actively creating bio-based and recyclable composite materials to meet future waste rules.

Latin America Advanced Composites Market Growth Factor

Latin America held a market share of 6% in 2025. This growth is powered by three main factors: rising demand for lightweight vehicles to improve fuel efficiency, investments in renewable energy like wind turbines, and upgrades in the regional automotive and aerospace industries. These modern, man-made materials combine different substances to create a product that is both very strong and very light. They are used instead of traditional metals to lower the weight and prevent rust.

Brazil

- Car companies in Brazil use these materials to build lighter cars. Lighter cars use less gas and go further on a charge. This helps meet strict environmental laws.

- The rising middle class in Brazil is buying more luxury vehicles. These cars use high-performance glass and carbon fibers to improve both design and safety.

Argentina

- Argentina is investing heavily in renewable energy infrastructure. Advanced composites are the preferred material for manufacturing large, durable, and lightweight wind turbine blades.

- The countrys aerospace and defense sectors demand high-performance materials like aramid and carbon fibers.

- These composites are chosen for their heat resistance, impact resistance, and ability to handle extreme stress.

Middle East & Africa Advanced Composites Market Growth Factor

The Middle East & Africa held a market share of 5% in 2025, growing rapidly due to rising demands for lightweight, durable, and corrosion-proof materials. Key growth factors include the booming aerospace and defense sectors, high infrastructure and construction investments, and a regional shift toward renewable energy. Governments are shifting away from relying only on oil. They are funding massive wind and solar power projects. Composites are essential for building massive, durable wind turbine blades.

Saudi Arabia

- The Saudi Arabia advanced composites market is growing due to Vision 2030, which brings massive government investments in aerospace, defense, and urban infrastructure.

- These specialized, lightweight materials are highly valued for being strong, stiff, and resistant to harsh environments, which helps cut costs and save fuel.

- The Kingdom is expanding its aerospace manufacturing and investing in aramid fibers for defense.

UAE

- Advanced composites like carbon fiber help build lighter aircraft. Lighter planes use less fuel. Government investments in UAVs, drones, and the space industry are also boosting demand.

- The UAEs booming construction and real estate sectors drive massive material needs. Advanced composites are favored because they resist extreme heat and corrosion, require low maintenance, and last longer than traditional metals.

Segmental Insights

Product Insights

The carbon fiber segment dominated the advanced composites market with the largest share in 2025, akin to its exceptional strength-to-weight ratio, fatigue resistance, and stiffness, making it indispensable in aerospace, defense, and high-end automotive applications. It enables lightweight structures that significantly enhance fuel efficiency and performance. Demand surged from sectors prioritizing weight reduction without compromising mechanical strength in the current period. Also, carbon fibres compatibility with various resin systems and solid high-performance end uses has maintained its leading position.

") The glass fiber segment is expected to experience notable advanced composites market growth in the future, owing to its cost-effectiveness, versatility, and expanding use in industries like wind energy, construction, and consumer goods. From the carbon fibre, glass fibre offers a more economical solution for applications that require moderate strength but high durability and corrosion resistance. Its compatibility with various resins and ease of manufacturing make it suitable for mass production. As sustainability gains traction, glass fibres recyclability and lower environmental footprint are also gaining importance. The growing demand for affordable lightweight materials in emerging economies is further driving their adoption across industries in the future.

The glass fiber segment is expected to experience notable advanced composites market growth in the future, owing to its cost-effectiveness, versatility, and expanding use in industries like wind energy, construction, and consumer goods. From the carbon fibre, glass fibre offers a more economical solution for applications that require moderate strength but high durability and corrosion resistance. Its compatibility with various resins and ease of manufacturing make it suitable for mass production. As sustainability gains traction, glass fibres recyclability and lower environmental footprint are also gaining importance. The growing demand for affordable lightweight materials in emerging economies is further driving their adoption across industries in the future.

Resin Type Insights

The advanced thermosetting composites segment held the dominating share of the advanced composites market in 2025 due to its widespread use in high-performance applications such as wind energy, aerospace, and automotive sectors. Also, these composites offer excellent heat resistance, dimensional stability, and superior strength-to-weight ratio, making them ideal for structural components.

Epoxy, phenolic, and polyester resins are extensively used due to their strong bonding and lightweight properties. Furthermore, established manufacturing techniques like filament winding and resin transfer molding have supported large-scale production. Their long-standing reliability in mission-critical applications has driven steady demand, specifically where mechanical strength and thermal stability are crucial.

")

The advanced thermoplastic composites segment is seen to grow at a notable rate during the predicted timeframe owing to increasing preferences for materials that support faster production cycles, recyclability, and easy repair. Industries are shifting towards thermoplastics like Polyether Ether Ketone (PEEK), Polyphenylene Sulfide (PPS), and Polyetherimide (PEI) due to their reprocessability and superior impact resistance. Moreover, these composites are gaining traction in electric vehicles and aerospace for lightweighting without compromising structural performance. Additionally, advancements in automated processing methods such as automated fiber placement (AFP) are enabling mass production, which is contributing to segment growth.

Application Insights

The automotive segment dominated the advanced composites market with the largest share in 2025, akin to its increasing need for lightweight, high-strength materials that enhance fuel economy and reduce emissions. Composites are increasingly used in structural components, body panels, and interiors to meet regulatory and performance standards. OEMs have integrated advanced composites into both luxury and mass market vehicles to boost efficiency without compromising safety. Additionally, electric vehicle production has increased composite usage for battery enclosures and aerodynamic designs in the current period.

The aerospace & defense segment is expected to grow at the fastest rate in the advanced composites market during the forecast period due to rising air travel demand, lightweight aircraft needs, and stringent fuel-efficiency goals. Advanced composites significantly reduce aircraft weight while enhancing performance, safety, and operational life. Aircraft manufacturers are increasingly adopting carbon fiber and thermoplastics in airframes, interiors, and engine components. With the rapid expansion of commercial aviation and space exploration programs, composites offer strategic advantages in reducing maintenance costs and increasing design versatility. As production scales and material technologies mature, aerospace applications will become the primary growth driver for the market.

Recent Developments in Advanced Composites Market

- In October 2025, Aeromech opened the Aeromech Training Centre in Brisbane, Australia, to deliver specialized advanced composites training for the aerospace and defense sectors. Alongside the facilitys opening, the company launched its flagship "Advanced Composites Aerospace Manufacturing and Repair" training program.(Source: www.compositesworld.com)

- In January 2026, Bharat Petroleum Corporation Ltd (BPCL) launched Bharatgas Lite, a lightweight composite LPG cylinder, in Goa, marking a shift toward alternative cylinder materials aimed at improving safety, convenience, and consumer experience. Advanced composites resist high-pressure conditions and do not fragment upon high-velocity impact.(Source: energy.economictimes.indiatimes.com)

- In November 2025, German coated fiber technology developer FibreCoat GmbH and Spanish advanced materials company Lofith Composites formed a strategic partnership to launch next-generation thermoplastic composites into space. The partnership combines FibreCoats specialized aluminum fiber coating technology with Lofiths high-performance thermoplastic tape and composite manufacturing.(Source: www.aero-mag.com)

Top Companies list

- Toray Industries, Inc.

- Koninklijke Ten Cate NV

- Teijin Limited

- Hexcel Corporation

- SGL Group

- Cytec Solvay Group

- Owens Corning

- E. I. Dupont De Nemours and Company

- Huntsman Corporation

- Momentive Performance Materials Inc.

- WS Atkins plc

- AGY Holdings Corp.

- Formosa Plastics Corporation

- Plasan Carbon Composites

- Strata Manufacturing

Segment Covered in the Report

By Product

- Aramid Fiber

- Para-Aramid

- Meta-Aramid

- Carbon Fiber

- PAN-Based Carbon Fiber

- Pitch-Based Carbon Fiber

- Glass Fiber

- E-Glass

- S-Glass

- C-Glass

By Resin

- Advanced Thermosetting Composites

- Epoxy

- Polyester

- Vinyl Ester

- Phenolic

- Advanced Thermoplastic Composites

- PEEK

- PPS

- PEI

- PA

- PP

- Others

By Application

- Aerospace & Defense

- Commercial Aircraft

- Military Aircraft

- Space Systems

- Automotive

- Passenger Vehicles

- Commercial Vehicles

- Electric Vehicles

- Wind Energy

- Turbine Blades

- Nacelles

- Sporting Goods

- Bicycles

- Golf Equipment

- Tennis Equipment

- Others

- Others

- Marine

- Construction

- Industrial Equipment

- Medical

By Region

- North America

- U.S.

- Canada

- Mexico

- Europe

- UK

- Germany

- France

- Italy

- Spain

- Sweden

- Denmark

- Norway

- Asia Pacific

- Japan

- China

- India

- Australia

- South Korea

- Thailand

- Latin America

- Brazil

- Argentina

- The Middle East and Africa

- South Africa

- Saudi Arabia

- UAE

- Kuwait

FAQ's

Select User License to Buy

Figures (6)