Content

Specialty Resins Market Trends, Growth and Market Size Analysis

The global Specialty Resins market size was estimated at USD 98.19 billion in 2025 and is expected to be worth around USD 201.43 billion by 2035, growing at a CAGR of 7.45% from 2026 to 2035. In terms of volume, the Specialty Resins market is projected to grow from 21.85 million tons in 2025 to 40.44 million tons by 2035. growing at a CAGR of 6.35% from 2026 to 2035. Heavy shift towards the specialty application, which needs tailored solutions, has accelerated the industry's growth in recent years.

Market Highlights

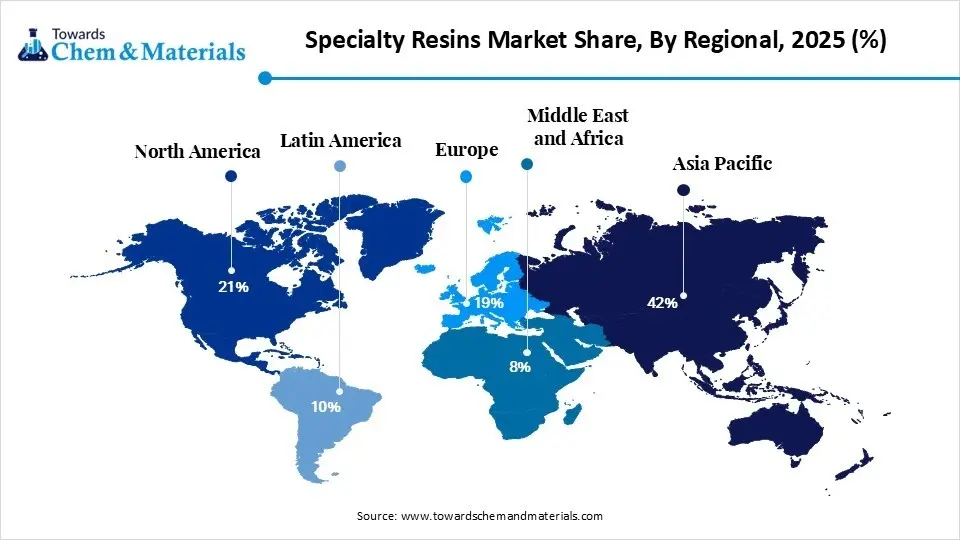

- By region, Asia Pacific dominated the market with a share of 44% in 2025 and is expected to be the fastest-growing region in the market, with a CAGR of 8.1% in the forecast period.

- By region, North America is notably growing with 20% market share in 2025.

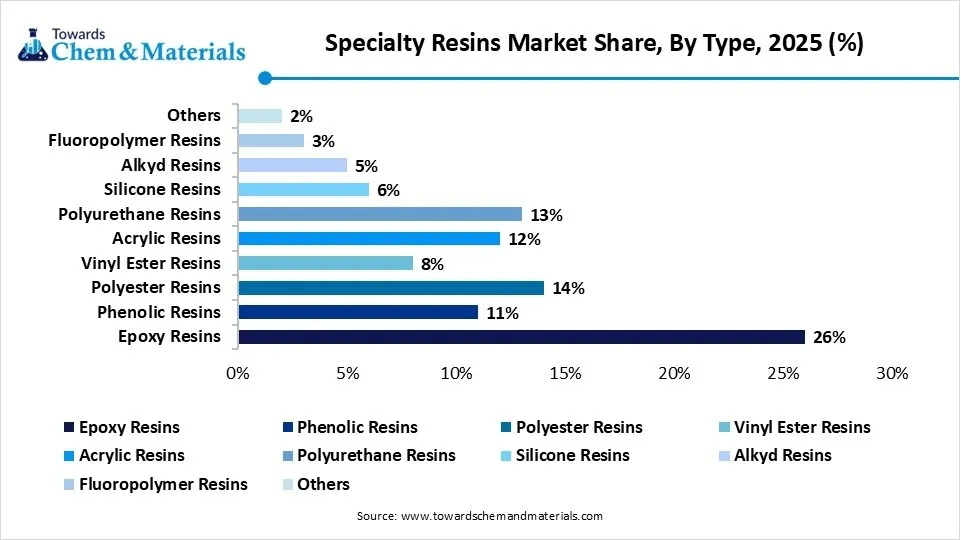

- By type, the epoxy resins segment dominated the market with 26% share in 2025.

- By type, the acrylic resins segment held the 12% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 7.9% in the forecast period.

- By form, the liquid segment dominated the market with 48% share in 2025.

- By form, the powder segment held the 20% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 7.8% in the forecast period.

- By application, the coatings segment dominated the market with 38% share in 2025.

- By application, the composites segment held the 16% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 8.1% in the forecast period.

- By end-use industry, the building and construction segment dominated the market with 28% share in 2025.

- By end-use industry, the electrical and electronics segment held the 15% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 7.8% in the forecast period in 2025.

Market Size and Volume Forecast

- Market Estimated Size (2025): USD 98.19 Billion | CAGR (2026–2035): 7.45%

- Market Projected Size (2035): USD 201.43 Billion

- Market Volume (2025): 7.45% Million Tons | Volume CAGR (2026–2035): 6.35%

- Market Projected Volume (2035): 40.44 Million Tons

- Market Pricing (2025):

- Average Manufacturing Price: USD 3.95/kg

- Average Selling Price: USD 5.36/kg

- Pricing CAGR (2025–2035): 3.65%

Engineered Resins for Critical Applications

The refined category of resins produced with clear, specific purposes, high quality, and high performance is known as specialty resins. Moreover, owing to their specific properties, such as heat resistance, high strength, chemical stability, and electrical performance, specialty resins have gained major industry attention in recent times

Market Trends:

- Heavy need for high-performance applications has elevated the earning potential for the industry in recent years. Also, the industries are looking for the material which with stand extreme conditions such as pressure and high temperatures.

- The heavy trend towards sustainability and smarter materials is driving substantial financial gains in the current period. The major companies are actively developing resins with energy-efficient processes and using recycled materials nowadays.

- The ongoing need for tailored and customized resins is likely to lead to robust revenue growth across the sector. Also, heavy manufacturers are in demand for very specific resin designs for very specific work.

Report Scope

| Report Attribute | Details |

| Market Size and Volume in 2026 | USD 105.51 Billion / 23.24 Million Tons |

| Expected Size and Volume by 2035 | USD 201.43 Billion / 40.44 Million Tons |

| Growth Rate from 2026 to 2035 | CAGR 7.45% |

| Forecast Period | 2026 - 2035 |

| Dominant Region | Asia-Pacific |

| Segment Covered | By Type, By Form, By Application, By End-Use Industry, By Region |

| Key companies profiled | SABIC, Covestro AG, LyondellBasell, Solvay S.A., LANXESS, Sumitomo Chemical Co., Ltd., Mitsubishi Chemical Group |

Molecular Control Enhancing Resin Performance

The industry has seen a move toward precision engineering at the molecular level in the current period. Also, modern technologies allow scientists to control the structure of resins during development, resulting in highly consistent and predictable properties. Moreover, the advanced processing methods, simulation tools, and digital monitoring systems are also improving production efficiency.

Supply Chain Analysis of the Specialty Resins Market:

Distribution to Industrial Users

Specialty resins are efficiently funneled to industrial users through streamlined distribution networks that prioritize technical support and bulk logistics.

Distributors ensure consistent supply for specialized applications like aerospace and electronics, providing tailored formulations and just-in-time delivery. This localized access enables manufacturers to maintain production cycles while meeting rigorous material specifications

Chemical Synthesis and Processing

Chemical synthesis of specialty resins involves precise polymerization techniques, such as step-growth or chain-growth reactions, to achieve specific molecular architectures.

Processing typically utilizes controlled thermal curing or UV irradiation to crosslink polymers. These meticulously engineered methods ensure the resulting materials exhibit exceptional durability, thermal stability, and chemical resistance for performance.

Regulatory Compliance and Safety Monitoring

Regulatory compliance for specialty resins involves adhering to strict international standards like REACH and OSHA to manage chemical risks. Continuous safety monitoring throughout production prevents hazardous exposure and environmental leaks.

Rigorous documentation and regular audits ensure that these high-performance materials meet legal safety thresholds and worker protection protocols.

Specialty Resins Market Regulatory Landscape: Regulations

| Country Region | Regulatory Body | Key Regulations | Focus Areas |

| United States | Environmental Protection Agency (EPA) | Toxic Substances Control Act (TSCA): Section 5 Requires Pre-Manufacture Notification for new specialty resins before they enter the market. | Risk evaluation of "high-priority" substances (e.g., acrylonitrile used in resins), pre-market safety reviews, and limiting hazardous emissions from finished products |

| Europe | European Chemicals Agency (ECHA) |

REACH Regulation Registration: Mandatory for substances manufactured/imported over 1 tonne/year. | Phasing out hazardous substances, promoting "green" chemical alternatives, and ensuring detailed safety data communication throughout the supply chain |

| China | Ministry of Emergency Management (MEM) |

Articles 15 & 37: Mandatory GHS-compliant labelling and Safety Data Sheets (SDS) for hazardous resins |

Strict licensing for production and operation, comprehensive hazardous chemical inventories (Catalogue of Hazardous Chemicals), and GHS enforcement at customs for imported resins. |

Market Dynamics

Driver

Strong Durable Materials Fuel Market Expansion

The growing need for strong, durable, and lightweight materials across industries is driving the industry growth nowadays. Also, modern products, from vehicles to electronics, require materials that perform better and last longer.

Restraint

Expensive Processes Restrict Small Manufacturers Across

The high cost of production compared to standard materials is likely to hinder industry growth during the forecast period. This can make specialty resins less accessible for small manufacturers. Also, the complexity of processing, as these materials often require specific conditions and expertise.

Opportunity

Eco-Friendly Materials Unlock New Market Potential

The development of sustainable and bio-based resins is expected to emerge as an ideal opportunity during the project period. As industries move toward environmentally responsible practices, there is increasing demand for materials that reduce environmental impact.

Segmental Insights

Type Insights

The Epoxy Resins Segment Dominated the Specialty Resins Market with 26% Market Share in 2025

The epoxy resins segment dominated the market with 26% share in 2025, as they offer a strong balance of properties. They provide excellent adhesion, high strength, and resistance to heat and chemicals. These qualities make them suitable for a wide range of applications, including coatings, adhesives, and electronics.

The polyester resins segment held the 14% market share in 2025, owing to they offer a cost-effective solution with good performance. They are easier to process and require less complex handling compared to some other resins. This makes them attractive for industries looking to balance cost and quality.

The acrylic resins segment held the 12% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 7.9% in the forecast period, owing to their excellent clarity, weather resistance, and environmental advantages. They are widely used in applications where appearance and durability are important, such as coatings and transparent materials.

Form Insights

The Liquid Segment Dominated the Market with 48% Market Share in 2025

The liquid segment dominated the market with 48% share in 2025, akin to they are easy to handle and widely applicable. They can be applied smoothly in coatings, adhesives, and casting processes. Their flexibility in use makes them suitable for both large-scale and detailed applications. Another advantage is their ability to mix easily with additives, allowing customization.

The solid segment held the 32% market share in 2025 due to its advantages in storage, transportation, and stability. Unlike liquid resins, they are less sensitive to temperature changes and have a longer shelf life. This makes them suitable for industries that require reliable material handling over time

The powder segment held the 20% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 7.8% in the forecast period, due to its support for cleaner and more efficient processes. They do not require solvents, which reduces environmental impact and improves safety. Powder coatings, for example, produce less waste and provide strong, durable finishes.

Application Insights

The Coatings Segment Dominated the Specialty Resins Market with 38% Market Share in 2025

The coatings segment dominated the market with 38% share in 2025 as they are essential for protecting and enhancing surfaces. Specialty resins used in coatings provide durability, resistance to corrosion, and improved appearance. These coatings are widely used in construction, automotive, and industrial equipment.

The adhesives and sealants segment held the 18% market share in 2025 due to the industries are moving toward lightweight and efficient assembly methods. Instead of using traditional fasteners like screws or bolts, manufacturers are using adhesives to join materials. This reduces weight and improves design flexibility.

The composites segment held the 16% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 8.1% in the forecast period, owing to the they combine strength with low weight. Specialty resins are a key component in composite materials used in industries like aerospace, automotive, and renewable energy. These materials help improve fuel efficiency and overall performance.

End-Use Industry Insights

The Building and Construction Segment Dominated the Market with 28% Market Share in 2025

The building and construction segment dominated the market with 28% share in 2025 owing to it requires large volumes of durable and reliable materials. Specialty resins are used in coatings, flooring, insulation, and structural components. These materials improve the strength, safety, and longevity of buildings.

The automotive segment held the 17% market share in 2025 owing to the increasing focus on lightweight and energy-efficient vehicles. Specialty resins are used to replace heavier materials, helping improve fuel efficiency and performance. They are also important in electric vehicles, where advanced materials are required for batteries and components.

The electrical and electronics segment held the 15% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 7.8% in the forecast period in 2025, owing to rapid technological advancement. Specialty resins are used for insulation, protection, and miniaturization of electronic components. As devices become smaller and more powerful, the need for reliable materials increases.

Regional Insights

How will Asia Pacific Dominate the Specialty Resins Market in 2025?

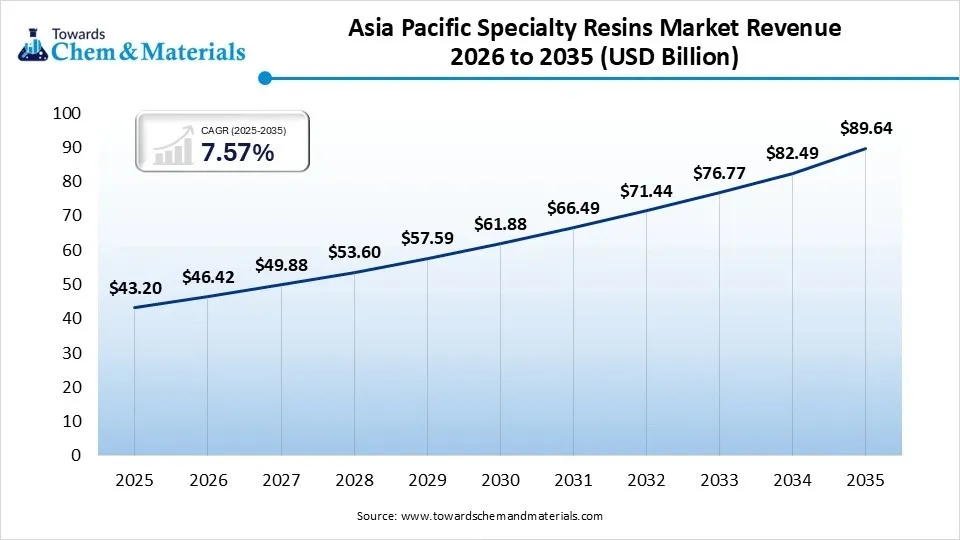

The Asia Pacific Specialty Resins market size was estimated at USD 43.20 billion in 2025 and is projected to reach USD 89.64 billion by 2035, growing at a CAGR of 7.57% from 2026 to 2035 .Asia Pacific dominated the market with a share of 44% in 2025 and is expected to be the fastest-growing region in the market, with a CAGR of 8.1% in the forecast period, due to strong industrial growth, large manufacturing capacity, and increasing infrastructure development. Countries in this region produce and consume a high volume of specialty resins. Cost advantages, availability of raw materials, and skilled labor also support this position.

China Leading Global Specialty Resins Market

China maintained its dominance in the market, owing to its large-scale manufacturing and strong industrial base. The country has a well-developed supply chain, allowing efficient production and distribution. Government support for infrastructure and industrial growth further drives demand. China is also investing in advanced materials and sustainable solutions.

Specialty Resins Market Evaluation in North America

North America is notably growing with 20% market share in 2025, owing to the region's investment in research and development, leading to the creation of high-performance and sustainable resins. Strong demand from industries such as aerospace, electronics, and renewable energy supports growth. In simple terms, the region’s strength lies in innovation rather than volume.

Strong Innovation Driving the United States Specialty Resins Growth

The United States is expected to emerge as a prominent country for the specialty resins market in the coming years, due to its advanced industrial ecosystem and strong emphasis on research and development. The country leads in innovation, particularly in high-performance and sustainable materials. Industries such as aerospace, automotive, and electronics create consistent demand for specialty resins.

Recent Development

- In December 2025, SABIC unveiled its latest fluorine-free polycarbonate resin. Also, the newly launched resin is specifically designed to enhance medical device safety and is named LNP ELCRES NPCRX9612U, as per the company's claim.(Source: www.indianchemicalnews.com)

Top Vendors in the Specialty Resins Market & Their Offerings:

- Huntsman Corporation: Huntsman is a global leader in differentiated chemicals, specifically renowned for its high-performance epoxy and polyurethane systems. By focusing on high-growth sectors like aerospace and automotive, the company provides innovative bonding and insulation solutions. Their strategy emphasizes sustainable chemistry, developing lightweight materials that improve energy efficiency across modern industrial applications.

- SABIC: Based in Saudi Arabia, SABIC is a diversified chemical giant that excels in high-heat specialty resins and engineering thermoplastics. Their portfolio, featuring advanced polyetherimides, serves the rigorous demands of electronics and healthcare. SABIC prioritizes a circular economy by integrating chemically recycled feedstocks, ensuring their performance materials meet modern sustainability standards.

- Covestro AG: Covestro is a pioneer in premium polymer materials, specializing in high-tech polycarbonates and polyurethane precursors. The company focuses heavily on a fully circular future, engineering resins for electric vehicle components and energy-efficient building insulation. Their commitment to innovation drives the development of sustainable coatings and adhesives for diverse global markets.

Other Key Players

- LyondellBasell

- Solvay S.A.

- LANXESS

- Sumitomo Chemical Co., Ltd.

- Mitsubishi Chemical Gro

Segments Covered in the Report

By Type

- Epoxy Resins

- Bisphenol A Epoxy

- Bisphenol F Epoxy

- Novolac Epoxy

- Phenolic Resins

- Resol

- Novolac

- Polyester Resins

- Unsaturated Polyester

- Saturated Polyester

- Vinyl Ester Resins

- Acrylic Resins

- Thermoplastic Acrylics

- Thermosetting Acrylics

- Polyurethane Resins

- Flexible PU

- Rigid PU

- Coatings Grade PU

- Silicone Resins

- Alkyd Resins

- Fluoropolymer Resins

- Others

- Amino Resins

- Furan Resins

By Form

- Liquid

- Solid

- Powder

By Application

- Coatings

- Industrial Coatings

- Automotive Coatings

- Protective Coatings

- Adhesives & Sealants

- Structural Adhesives

- Non-Structural Adhesives

- Composites

- Fiber Reinforced Plastics

- Carbon Fiber Composites

- Electrical & Electronics

- Encapsulation

- Insulation

- Construction

- Flooring

- Concrete Repair

- Others

By End-Use Industry

- Building & Construction

- Automotive

- Electrical & Electronics

- Marine

- Aerospace

- Wind Energy

- Consumer Goods

- Others

By Region

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Asia Pacific

- China

- India

- Japan

- South Korea

- Latin America

- Brazil

- Argentina

- Middle East & Africa

- Saudi Arabia

- South Africa

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

FAQ's

Select User License to Buy

Figures (4)