Content

What is Regenerative Agriculture Market Size and Share?

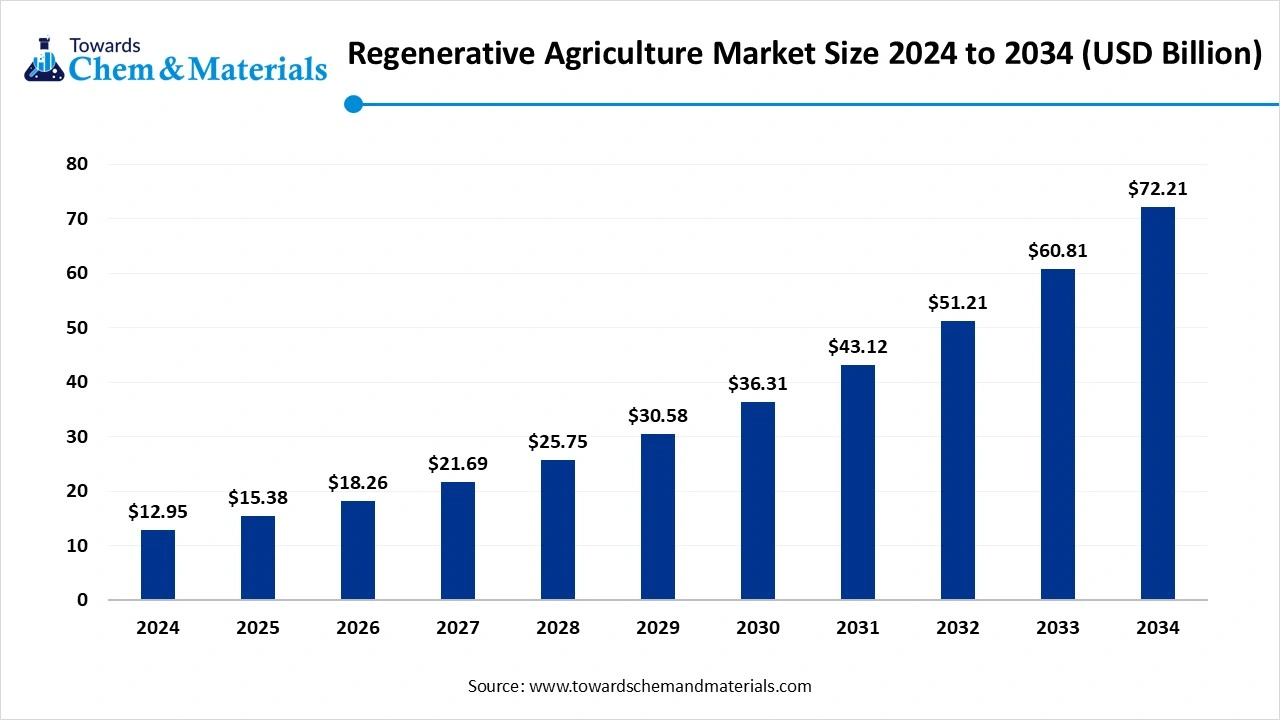

The global regenerative agriculture market size was valued at USD 15.19 billion in 2025, is estimated to reach USD 17.42 billion in 2026, and is projected to reach USD 59.61 billion by 2035, exhibiting a compound annual growth rate (CAGR) of 14.65% over the forecast period from 2026 to 2035 .North America dominated the regenerative agriculture market with the largest revenue share of 34.0% in 2025 and is expected to grow at the fastest CAGR of 34% during the forecast periperiod. easing consumer demand for sustainably sourced food is the key factor in driving market growth. Also, volatile agrochemical costs coupled with the technological innovations in farming can fuel market growth further.

")

The market is an industry emphasis on outcome-based farming systems that improve biodiversity, restore soil health, and sequester atmospheric carbon. It reverses climate change by restoring degraded soil biodiversity and rebuilding soil organic matter. Unlike conventional sustainability, which focuses on reducing harm, the market emphasizes active environmental restoration while keeping overall agricultural productivity.

Regenerative agriculture represents a holistic and conservation-driven approach to food production and farming systems, mainly focusing on restoring soils degraded by the intensive application of chemical pesticides and fertilizers. By prioritizing the rehabilitation of agricultural ecosystems, this methodology seeks to optimize the water cycle, restore topsoil, enhance biodiversity, increase nutrient density, and strengthen soil vitality.

Key Takeaways

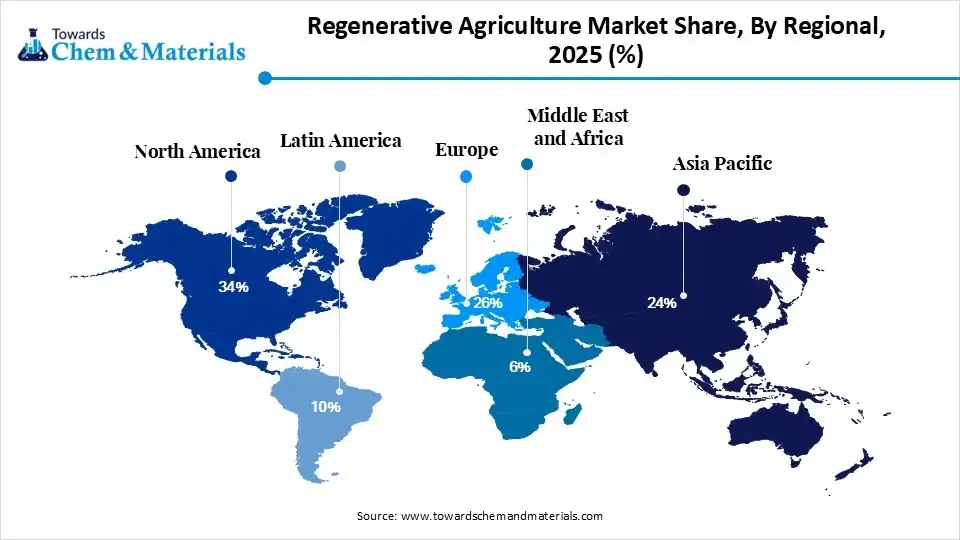

- By region, North America dominated the market with the largest share of 34.0% in 2025. The dominance of the region can be attributed to the increasing consumer willingness to pay a premium for regeneratively sourced foods.

- By region, Asia Pacific held a market share of 24.0% in 2025 and is expected to grow at the fastest CAGR of 16.40% over the forecast period. The growth of the region can be credited to the growing disposable incomes across emerging nations.

- By component, the solutions segment dominated the market with the largest share of 63.0% in 2025. The dominance of the segment can be attributed to the increasing demand for verified carbon sequestration.

- By component, the services segment held a market share of 37.00% in 2025 and is expected to grow at the fastest CAGR of 15.4% over the forecast period. The growth of the segment can be credited to the growing demand for specialized education.

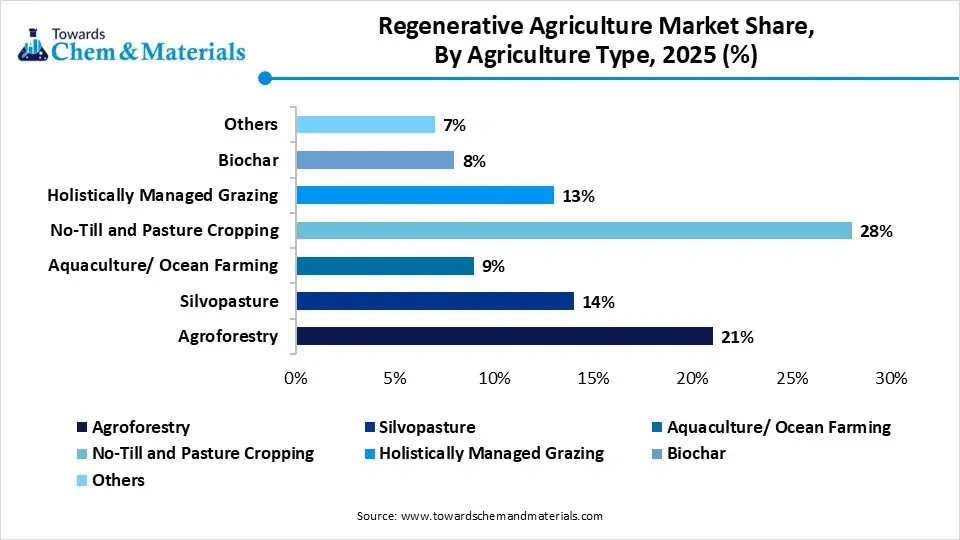

- By agriculture type, the no-till and pasture cropping segment dominated the market with the largest share of 28.0% in 2025. The dominance of the segment can be linked to the growing demand for climate mitigation.

- By agriculture type, the aquaculture/ocean farming segment held the market share of 9.00% in 2025 and is expected to grow at the fastest CAGR of 16.1% over the forecast period. The growth of the segment can be driven by a rise in corporate investment for ESG mandates.

- By end user, the farmers segment dominated the market with the largest share of 46.0% in 2025. The dominance of the segment can be attributed to the increasing corporate commitments to sustainable sourcing.

- By end user, the financial institutions segment held the market share of 12.00% in 2025 and is expected to grow at the fastest CAGR of 16.3% during the projected period. The growth of the segment can be credited to increasing ESG investments.

Market Trends

- Increasing demand for sustainable agriculture is the latest trend in the market, shaping positive market growth. Consumers are more concerned regarding environmental issues like soil degradation, climate change, and loss of biodiversity. They search for products that are created in eco-friendly ways.

- Consumer engagement and education act as one of the key drivers for market growth. Educational campaigns are bridging the gap between consumers and sources of their food. This surge in consumer awareness is increasing the need for more convenient farming practices.

- The growing focus on climate change mitigation is another major factor driving growth in the market. Moreover, regenerative strategies such as rotational grazing and cover cropping, along with carbon sequestration in soils, facilitate minimizing overall greenhouse gas emissions

Report Scope

| Report Attributes | Details |

| Market Size and Volume in 2026 | USD 17.42 Billion |

| Revenue Forecast in 2035 | USD 59.61 Billion |

| Growth Rate | CAGR 14.65% |

| Base Year of Estimation | 2025 |

| Forecast Period | 2025 - 2035 |

| Dominant Region | North America |

| Segment Covered | By Component), By Agriculture Type, By End User, By Regional |

| Key Companies Profiled | Agreed. Earth, Aker Technologies, Inc, Astanor Ventures, Biotrex, Carbon Robotics, Cargill, Incorporated, Continuum Ag, Ecorobotix SA, Indigo Ag, Inc., Ruumi, SATELLIGENCE, Terramera Inc., Tortuga Agricultural Technologies, Inc., Vayda |

How Are Cutting-Edge AI Technologies Revolutionizing the Regenerative Agriculture Market?

Advanced technologies are transforming the market by precisely managing resources and automating complex soil health tracking. Predictive analytics and machine learning enable farmers to shift away from reactive and chemical-heavy farming to proactive and data-driven ecosystems. Furthermore, AI analyzes layers of local data such as oil microbiota and moisture levels to map microclimates.

Supply Chain Analysis of the Regenerative Agriculture Market

- Feedstock Procurement :It refers to the sourcing of essential raw biological materials and inputs grown or derived using methods that restore biodiversity, soil health, and ecosystem resilience.

- Major Players: Unilever, Nestlé

- Chemical Synthesis and Processing :It refers to the manufacturing and strategic application of inputs within the agricultural ecosystem. While traditional farming depends on synthetically manufactured chemicals, the market transition shifts the focus towards sustainable alternatives.

- Major Players: Corteva Agriscience, BASF SE

- Packaging and Labeling :It is a crucial step that addresses how sustainably produced goods are contained, certified, and presented to consumers. It covers the use of biodegradable, sustainable, and recyclable packaging.

- Major Players: Alter Eco, Unilever PLC

- Regulatory Compliance and Safety Monitoring :It includes the frameworks, technologies, and certifications utilized to verify ecological outcomes and ensure food safety.

- Major Players: Nestle SA, Danone S,

Regenerative Agriculture Market's Regulatory Landscape: Global Regulations

| Country/Region | Key Regulations |

| United States | The Natural Resources Conservation Service administers a $700 million whole-farm conservation fund. It splits allocations across the Environmental Quality Incentives Program ($400M) and the Conservation Stewardship Program ($300M). |

| European Union | Nature Restoration Law: This binding mandate forces member states to [rehabilitate at least 20% of degraded terrestrial ecosystems by 2030](1.1.3, 1.4.6). It explicitly focuses on reversing pollinator decline and increasing soil organic carbon. |

| India | The federal government uses technology-driven programs like PMKSY (irrigation efficiency) and PMFBY (climate risk insurance) to stabilize farms transitioning away from input-intensive methods. |

Market Dynamics

Driver

Increasing Demand for Organic Food Products

The increasing need for chemical-free and sustainable food is the major factor driving the growth of the market. Farmers have increasingly adopted new regenerative agriculture practices such as rotational cropping and the no-till method due to the rise in awareness about soil health and biodiversity across the globe. In addition, partnerships between food enterprises and agricultural producers, aimed at fostering sustainable food networks, are generating new avenues for market expansion.

Restraint

High Transition Costs

The process of shifting from traditional to regenerative farming is a much costlier process for changing farming and training practices, which is the major factor hindering market growth. Moreover, a lack of standardized certification and quantifiable outcomes creates uncertainty regarding market value, hampering the adoption of regenerative agriculture despite growing consumer demand.

Opportunity

Technological Innovations in Agriculture

Technological innovations are transforming the market by offering advanced solutions that improve farming practices, creating lucrative opportunities in the market. Precision agriculture technologies, like drones and soil sensors, allow farmers to monitor and manage their land more efficiently. Furthermore, the ongoing advancement and integration of agricultural technologies are expected to drive operational efficiency and productivity. This technological progression will improve the economic viability of regenerative farming methods and ensure ongoing market growth.

Segmental Insights

Component Insights

The solutions segment dominated the market with the largest share of 63.0% in 2025. The dominance of the segment can be attributed to the increasing demand for verified carbon sequestration and ongoing digital transformation. In addition, major food and beverage market players are aggressively funding regenerative agricultural solutions within their supply chains.

The services segment held a market share of 37.00% in 2025 and is expected to grow at the fastest CAGR of 15.4% over the forecast period. The growth of the segment can be credited to the growing demand for specialized education, consulting, and data tracking along with the shift towards sustainable models. Major market players are heavily investing in tech-driven services to track agricultural inputs.

Regenerative Agriculture Market Share, By Component, 2025 (%)

| By Component | Revenue Share, 2025 (%) |

| Solutions | 63% |

| Services | 37% |

Agriculture Type Insights

The no-till and pasture cropping segment dominated the market with the largest share of 28.0% in 2025. The dominance of the segment can be linked to the growing demand for climate mitigation, enhanced soil health, and long-term farm profitability. Also, consumer awareness about organically produced and sustainable food is compelling the supply chains to source ingredients from regenerative farms.

The aquaculture/ocean farming segment held the market share of 9.00% in 2025 and is expected to grow at the fastest CAGR of 16.1% over the forecast period. The growth of the segment can be driven by a rise in corporate investment for ESG mandates and zero-input crop requirements. Consumers are increasingly demanding ethically sourced blue foods.

")

The agroforestry segment held the market share of 21.00% in 2025. The growth of the segment is owing to the increasing focus on climate change mitigation and growing consumer awareness about sustainability. Public policies across the globe are heavily supporting ecological transitions. Taxes, incentives, and green subsidies encourage the shift toward sustainable grazing.

The silvopasture segment held a market share of 14.00% in 2025. The growth of the segment is due to improved carbon sequestration techniques and lucrative new carbon credit revenues. Moreover, farmers are rapidly adopting silvopasture to diversify revenue streams. Selling carbon credits for ecosystem services (PES) adds direct income, leading to segment growth further.

Regenerative Agriculture Market Share, By Agriculture Type, 2025 (%)

| By Agriculture Type | Revenue Share, 2025 (%) |

| Agroforestry | 21% |

| Silvopasture | 14% |

| Aquaculture/ Ocean Farming | 9% |

| No-Till and Pasture Cropping | 28% |

| Holistically Managed Grazing | 13% |

| Biochar | 8% |

| Others | 7% |

End User Insights

The farmers segment dominated the market with the largest share of 46.0% in 2025. The dominance of the segment can be attributed to the increasing corporate commitments to sustainable sourcing and the surge in demand to minimize synthetic input costs. Farmers are rapidly monetizing their shift through carbon credit marketplaces.

The financial institutions segment held the market share of 12.00% in 2025 and is expected to grow at the fastest CAGR of 16.3% during the projected period. The growth of the segment can be credited to the increasing ESG investments and sustainable finance initiatives supporting climate-smart farming expansion. Carbon credit markets are attracting institutional agriculture investment heavily.

The service organization segment held a market share of 18.00% in 2025. The growth of the segment can be linked to the growing adoption of sustainability verification services, and improvements in digital farm advisory platforms. NGOs and agritech firms are increasingly expanding regenerative agriculture support programs.

The consumer packaged goods manufacturers segment held a market share of 13.00% in 2025. The growth of the segment can be driven by increasing demand for traceable products and ongoing investments in regenerative sourcing. Furthermore, sustainable packaging solutions and ingredient sourcing fuel segment growth soon.

Regenerative Agriculture Market Share, By End User, 2025 (%)

| By End User | Revenue Share, 2025 (%) |

| Farmers | 46% |

| Service Organization | 18% |

| Financial Institutions | 12% |

| Advisory Bodies | 11% |

| Consumer Packaged Goods Manufacturers | 13% |

Regional Insights

How did North America Dominate the Regenerative Agriculture Market in 2025?

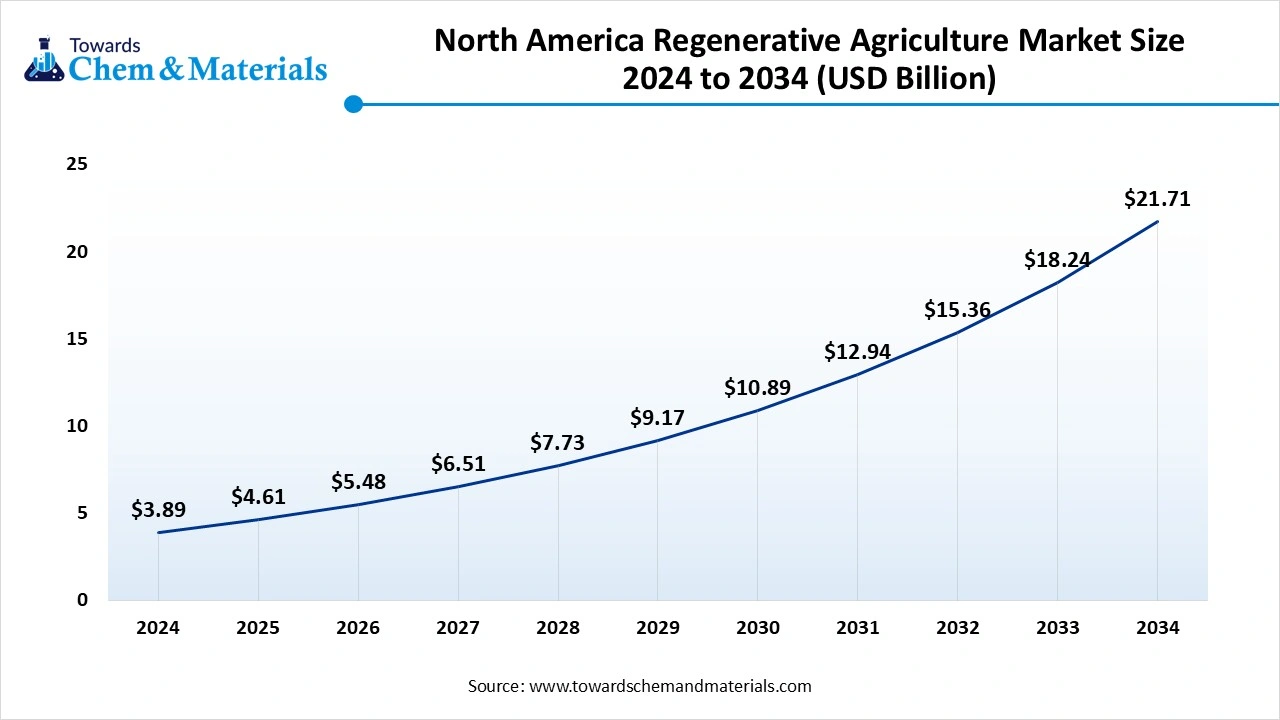

The North America Regenerative Agriculture market size was estimated at USD 5.16 billion in 2025 and is projected to reach USD 20.57 billion by 2035, growing at a CAGR of 14.83% from 2026 to 2035.North America dominated the market with the largest share of 34.0% in 2025. The dominance of the region can be attributed to the increasing consumer willingness to pay a premium for regeneratively sourced foods and favorable government policies. In addition, major food, beverage, and consumer goods market players are making heavy sustainable sourcing commitments, fueling market growth further.

")

United States

- There is an increasing conscious-consumer demographic willing to pay a premium for sustainable and regeneratively agricultural products and sourced foods.

- Farmers are rapidly adopting these practices to tackle soil degradation and minimize reliance on expensive synthetic fertilizers.

Canada

- Federal initiatives are offering funding to farmers for adopting sustainable practices, and farmers are monetizing carbon sequestration.

- Farmers are using AI monitoring, IoT sensors, and precision tools to measure soil health and substantiate sustainability claims.

The Asia Pacific regenerative agriculture market size was estimated at USD 3.65 billion in 2025 and is projected to reach USD 14.60 billion by 2035, growing at a CAGR of 14.87% from 2026 to 2035.Asia Pacific held the market share of 24.0% in 2025 and was expected to grow at the fastest CAGR of 16.40% over the forecast period. The growth of the region can be credited to the growing disposable incomes across emerging nations along with the growing need for organic fuel. The continous development of mobile-based advisory platforms is enhancing the efficiency of regenerative farming.

China

- A growing middle class with higher disposable incomes has increased demand for sustainably sourced, healthy, and organic food options.

- The growing adoption of AI-driven soil monitoring, precision agriculture, and IoT devices allows farmers to optimize resource use and shift to regenerative practices.

India

- Advanced startups and agricultural platforms use AI and remote sensing to measure carbon sequestration.

- A surge in disposable income and urbanization have boosted domestic demand for chemical-free, nutrient-dense, and sustainably produced food.

The Europe regenerative agriculture market size was estimated at USD 3.95 billion in 2025 and is projected to reach USD 15.80 billion by 2035, growing at a CAGR of 14.87% from 2026 to 2035.Europe held a market share of 26.00% in 2025. The growth of the region can be linked to the increasing consumer demand for sustainable food and sustainability policies encouraging regenerative farming transitions rapidly. Also, major market players in the region are investing rapidly to fulfill internal climate and sustainability goals.

Germany

- A surge in environmental and health awareness has driven extensive consumer adoption of organic and sustainable products.

- Traditional farmers are introducing resilient alternative crops, such as sunflowers, soybeans, and nitrogen-fixing legumes, to stabilize crop rotation.

The Latin America regenerative agriculture market size was estimated at USD 1.52 billion in 2025 and is projected to reach USD 6.26 billion by 2035, growing at a CAGR of 5.38% from 2026 to 2035. Latin America held a market share of 10.00% in 2025. The growth of the region can be driven by a surge in regional investment activities boosting carbon farming opportunities coupled with the rising adoption of regenerative agriculture pilot programs. The region's extensive arable land and need for climate resilience can fuel regional growth soon.

Brazil

- There is an increase in emphasis on the dual benefits of improved soil fertility and carbon sequestration.

- Brazil is at the top of the agricultural biologics revolution. Bio-inputs such as biofertilizers and biopesticides help farmers minimize reliance on environmentally hazardous chemical fertilizers.

Argentina

- Ranchers and farmers are actively shifting to regenerative grazing and diversified crop rotations to combat severe soil erosion and drought.

- Major market players and cooperatives are funding regenerative shifts to secure sustainable supply chains.

The Middle East and Africa regenerative agriculture market size was estimated at USD 0.91 billion in 2025 and is projected to reach USD 3.87 billion by 2035, growing at a CAGR of 15.58% from 2026 to 2035.The Middle East & Africa held a market share of 6.00% in 2025. The growth of the segment is owing to the ongoing innovation in regenerative farming practices and international sustainability collaboration driving regional regenerative initiatives. The utilization of AI-driven monitoring services and biological inputs is growing overall resource efficiency and minimizing agricultural waste across harsh terrains.

")

Saudi Arabia

- Saudi Arabia is heavily dependent on food imports. To tackle this, the government is prioritizing sustainable local farming systems.

- Major regional buyers and agribusinesses are adopting carbon-neutral supply chains, fueling the demand for services and solutions.

UAE

- Increasing health awareness is increasing local demand for sustainably produced, organic food, which commands a premium price.

- The country battles high temperatures, minimal rainfall, and saline soils. Regenerative solutions emphasize soil health and agroforestry.

Recent Developments

- In January 2026, JDE Peet’s, the premier pure-play coffee enterprise globally, introduced its "Grounded in Nature" Nature Transition Plan. This initiative serves as a scientifically grounded framework designed to safeguard ecosystems, enhance agricultural resilience, and guarantee the long-term sustainability of global coffee cultivation.(Source: www.globenewswire.com)

- In May 2026, Standard Bank Business and Commercial Banking (BCB), in partnership with Orizon Agriculture, has launched South Africa’s first bank-backed regenerative agriculture carbon credit program to assist farmers in generating supplemental revenue through carbon markets.(Source: iol.co.za)

Regenerative Agriculture Market Companies

- Agreed. Earth: Agreed. Earth is a prominent, niche AgTech company that accelerates the mass adoption of regenerative agriculture by remotely monitoring nitrogen flow. They leverage machine learning, open-source models, and satellite data via a specialized SaaS platform to reduce synthetic input dependencies and scale carbon farming.

- Aker Technologies, Inc.: Aker Technologies, Inc. is a prominent technology provider in the global regenerative agriculture market, recognized for delivering advanced field sensing, data analytics, and automated crop monitoring tools.

Other Companies in the Market

- Astanor Ventures

- Biotrex

- Carbon Robotics

- Cargill, Incorporated

- Continuum Ag

- Ecorobotix SA

- Indigo Ag, Inc.

- Ruumi

- SATELLIGENCE

- Terramera Inc.

- Tortuga Agricultural Technologies, Inc.

- Vayda

Segments covered in the report

By Component

- Solutions

- Soil Health Management Solutions

- Cover Crop Systems

- Compost and Organic Amendments

- Carbon Monitoring Platforms

- Satellite Monitoring

- IoT-based Monitoring

- Farm Management Software

- Crop Analytics

- Water Optimization Tools

- Soil Health Management Solutions

- Services

- Consulting Services

- Farm Transition Planning

- Sustainability Auditing

- Carbon Credit Verification Services

- Soil Carbon Assessment

- Emissions Reporting

- Training and Education Services

- Farmer Workshops

- Digital Learning Programs

- Consulting Services

By Agriculture Type

- Agroforestry

- Alley Cropping

- Forest Farming

- Windbreak Systems

- Silvopasture

- Livestock Grazing Integration

- Tree-Livestock Systems

- Aquaculture / Ocean Farming

- Regenerative Seaweed Farming

- Shellfish Farming

- No-Till and Pasture Cropping

- Conservation Tillage

- Crop Rotation Systems

- Holistically Managed Grazing

- Rotational Grazing

- Adaptive Multi-Paddock Grazing

- Biochar

- Wood-based Biochar

- Agricultural Waste Biochar

- Others

- Permaculture

- Integrated Crop-Livestock Systems

- Organic Regenerative Farming

By End User

- Farmers

- Small-scale Farmers

- Commercial Farms

- Cooperative Farming Groups

- Service Organizations

- NGOs

- Sustainability Certification Bodies

- Agritech Service Providers

- Financial Institutions

- Carbon Credit Investors

- Agricultural Banks

- ESG-focused Investment Firms

- Advisory Bodies

- Government Agencies

- Research Institutions

- Agricultural Extension Services

- Consumer Packaged Goods Manufacturers

- Food and Beverage Companies

- Personal Care Product Manufacturers

- Sustainable Packaging Producers

By Region

- North America

- U.S.

- Canada

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Sweden

- Denmark

- Norway

- Asia Pacific

- China

- Japan

- India

- South Korea

- Thailand

- Latin America

- Brazil

- Mexico

- Argentina

- Middle East and Africa (MEA)

- South Africa

- UAE

- Saudi Arabia

- Kuwait

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

Tags

FAQ's

Select User License to Buy

Figures (5)