Content

What is the current Purified Terephthalic Acid (PTA) Market Size and Share?

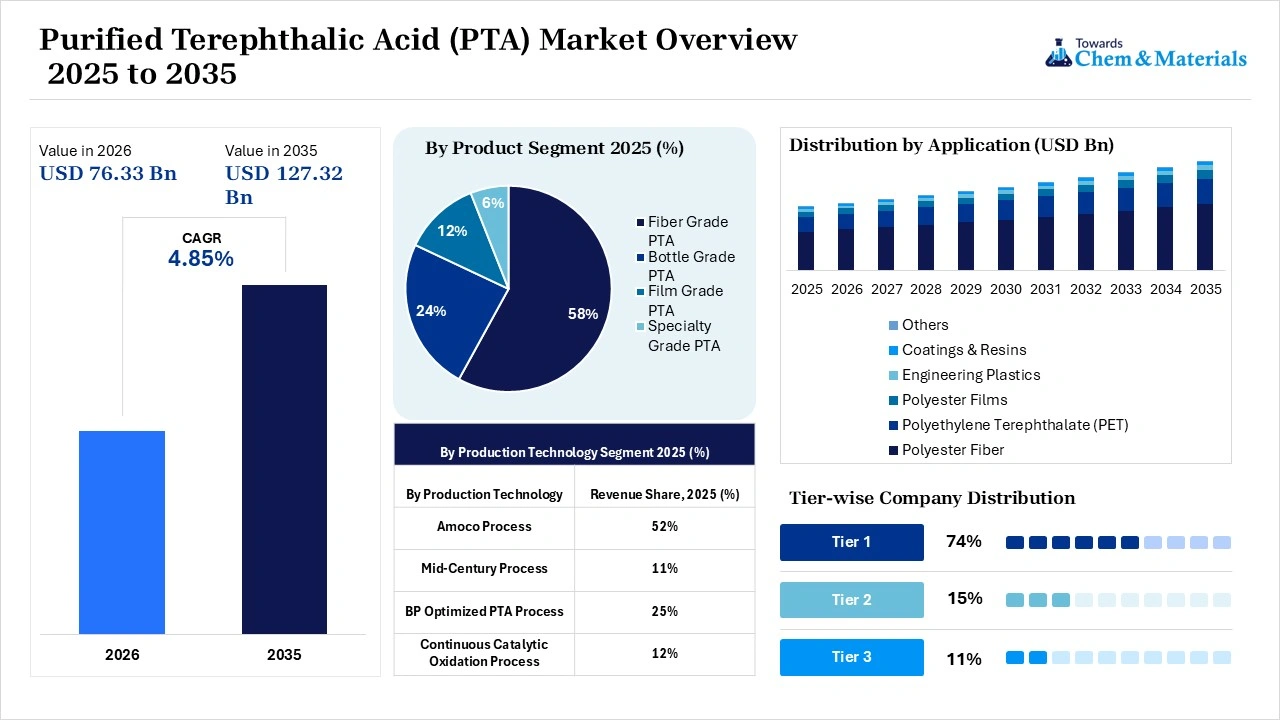

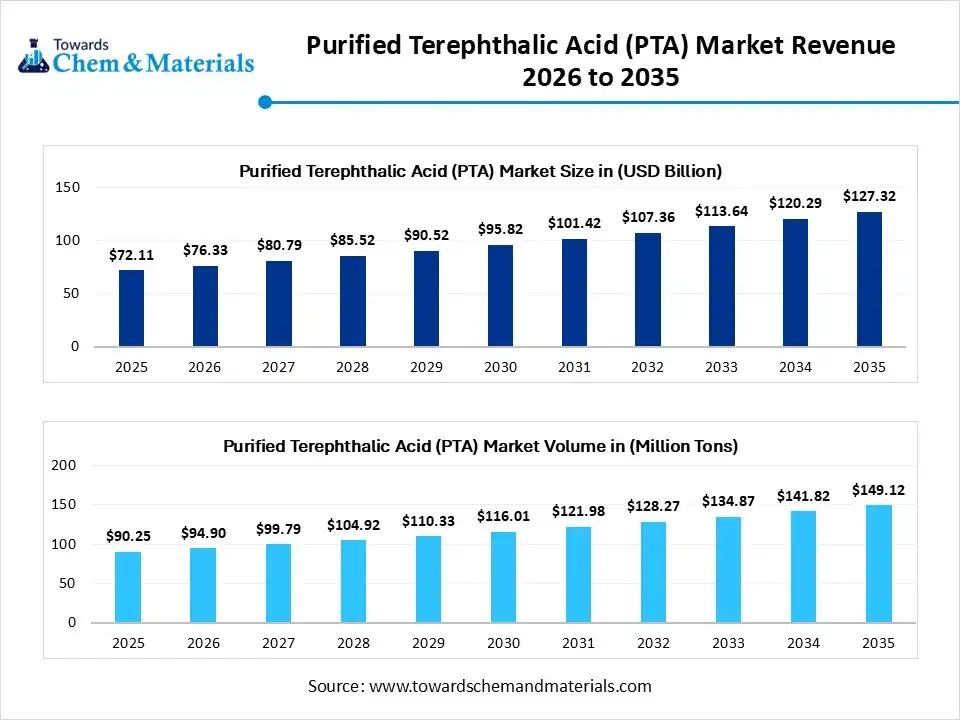

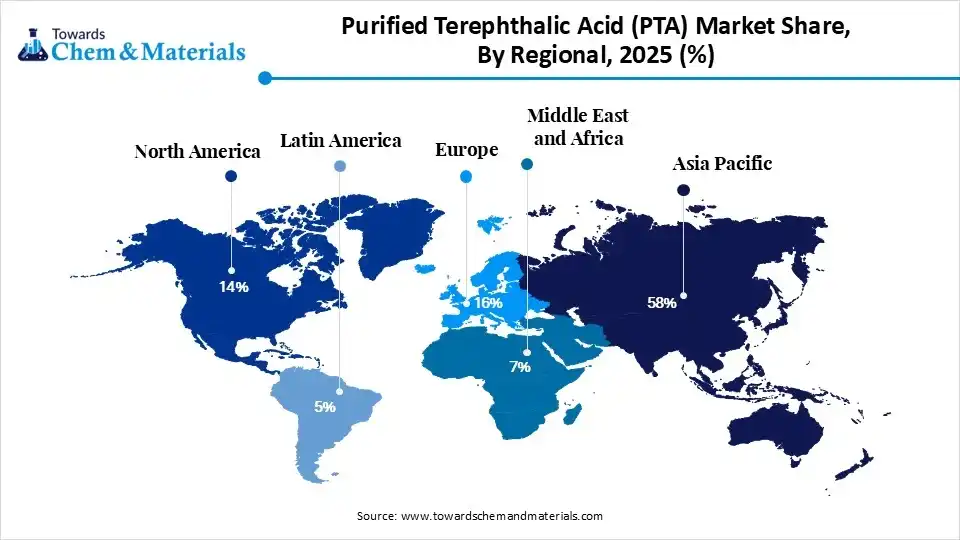

The purified terephthalic acid (PTA) market size was valued at USD 72.11 billion in 2025, is estimated to reach USD 76.33 billion in 2026, and is projected to reach USD 127.32 billion by 2035, exhibiting a compound annual growth rate (CAGR) of 5.85% over the forecast period from 2026 to 2035.Asia Pacific dominated the purified terephthalic acid (PTA) market with the largest revenue share of 58% in 2025 and is expected to grow at the fastest CAGR of 5.94% during the forecast period. In terms of volume, the purified terephthalic acid (PTA) market is projected to grow from 90.25 million tons in 2025 to 149.12 million tons by 2035. growing at a CAGR of 5.15% from 2026 to 2035. The market growth is driven by innovation for specialty PTA development, rapid urbanization, demand for optimized oxidation technologies, and large-scale PTA consumption.

Market Overview")

Market Highlights

- By region, Asia Pacific dominated the purified terephthalic acid (PTA) market by holding 58% share in 2025 and is expected to grow at the fastest with a CAGR of 6.7% during the forecast period due to PET manufacturing practices and rising urban demand for domestic PTA production capacity.

- By region, Europe held the 16% market share in 2025 and expects notable growth in the market with 5.10% CAGR during the forecast period, driven by sustainability-driven regulation and advancement & recycling for specialty polyester manufacturing.

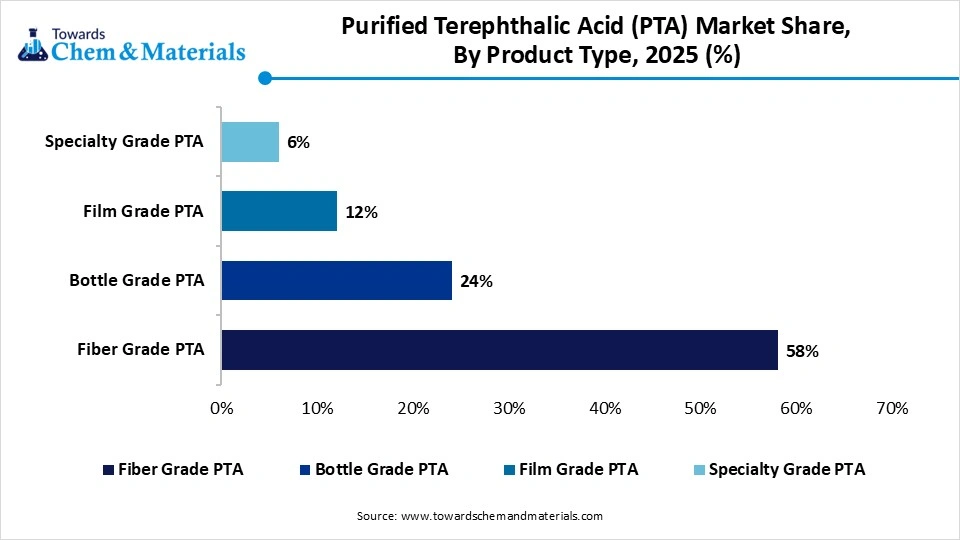

- By product type, the fiber grade PTA segment dominated the market with the largest share of 58% in 2025 due to its large-scale textile capacity expansion and fast-fashion demand.

- By product type, the bottle grade PTA segment held 24% market share in 2025 and is expected to grow at the fastest CAGR of 6.3% over the forecast period, driven by its lightweight and recyclability in food and packaging to meet sustainability mandates.

- By production technology, the Amoco process segment dominated the market with the largest share of 52% in 2025, driven by its operational efficiency and scalability in PTA manufacturing facilities.

- By production technology, the continuous catalytic oxidation process segment held 12% market share in 2025 and is expected to grow at the fastest CAGR of 6.8% over the forecast period due to rising investment for cleaner manufacturing operations and process automation.

- By application, the polyester fiber segment dominated the market with the largest share of 61% in 2025 due to demand for cost-effective synthetic fiber and emerging economies for textile manufacturing.

- By application, the polyethylene terephthalate (PET) segment held 23% market share in 2025 and is expected to grow at the fastest CAGR of 6.7% over the forecast period, driven by urban and consumer food and packaged sector demand for lightweight and recyclable solutions.

- By end user industry, the textile industry segment dominated the market with the largest share of 54% in 2025 due to fast-fashion trends and market players' investment in textile manufacturing expansion.

- By end user industry, the packaging industry segment held 25% market share in 2025 and is expected to grow at the fastest CAGR of 6.8% over the forecast period, driven by sustainability initiatives and e-commerce growth in consumer goods packaging.

- By purity level, the standard purity PTA segment dominated the market with the largest share of 68% in 2025 due to large-scale demand for conventional polyester fiber and PET manufacturing hubs.

- By purity level, the ultra-high purity PTA segment held 8% market share in 2025 and is expected to grow at the fastest CAGR of 7.1% over the forecast period, driven by advancements in specialty engineering plastics, optical films, and electronics to support premium product commercialization.

- By distribution channel, the direct sales segment dominated the market with the largest share of 49% in 2025 due to major PTA manufacturers' supply agreements with integrated PET and polyester producers.

- By distribution channel, the online commodity platforms segment held 6% market share in 2025 and is expected to grow at the fastest CAGR of 7.0% over the forecast period, driven by digital commodity trading platforms and e-commerce integration.

Market Revenue 2026 to 2035")

The global purified terephthalic acid (PTA) market is key for global petrochemical sectors as a chemical pillar for the synthesis of polyester polymers. The shift towards sustainability commitments fosters the innovation of bio-based phthalic acid. The growing industrial demand for polyester fabrics in the modern textile industry is due to its higher durability and wrinkle resistance, providing cost-effectiveness. The corporate green initiatives are accelerating the integration of closed-loop mechanical recycling solutions in chemical manufacturing practices.

PTA is a key component in a high-performance engineering framework. Recently, fast-moving consumer goods infrastructure has been driving the adoption of PET bottles and rigid container packaging because of their lightweight nature and superior gas barrier capabilities utilized in liquid food storage and carbonated beverages. As the market focuses on the consumer goods ecosystem, where catalytic esterification is utilized in the manufacturing of polyethylene terephthalate resins and high-strength polyester fibers.

Its ability to provide dielectric insulation layers is the form of specialized polyester films make them key for the electrical and electronics sector. The emerging trends towards renewable energy, where PTA provides solar cell backsheets, make it a crucial eco-conscious alternative. The global and domestic market players emphasize navigation of complex structural headwinds, accelerating the sub-structural investment to prevent upstream supply chain disruption. Additionally, R&D and government focus on technological advancement that strengthens the PTA adoption with continuous market growth.

Purified Terephthalic Acid (PTA) Market Trends

- Rising Focus on Recycling Practices: The global shift towards circular economy values is reshaping the substantial investment and implementation of mechanical and chemical recycling technologies in PTA. This trend focuses on innovation in purified recovery.

- Strict Environmental Regulations: The PTA market expansion is driven by enforcing stringent laws regarding plastic waste, and regulatory pressure pushes manufacturers to invest in continuous catalytic oxidation technologies and R&D activities.

Report Scope

| Report Attributes | Details |

| Market Size and Volume in 2026 | USD 76.33 Billion / 94.90 Million Tons |

| Revenue Forecast in 2035 | USD 127.32 Billion / 149.12 Million Tons |

| Growth Rate | CAGR 5.85% |

| Base Year of Estimation | 2025 |

| Forecast Period | 2025 - 2035 |

| High Impact Region | Asia Pacific |

| Segment Covered | By Product Type, By Production Technology, By Application, By End User Industry, By Purity Level, By Distribution Channel, By Region |

| Key Companies Profiled | Reliance Industries (IN), Indorama Ventures (TH), SABIC (SA), Mitsubishi Chemical (JP), Lotte Chemical (KR), Eastman Chemical (US), BASF (DE), Formosa Plastics (TW), PetroChina (CN), China National Petroleum Corporation (CN) |

Key Technological Shifts and AI in the Purified Terephthalic Acid (PTA) Market

The technological revolution in the purified terephthalic acid (PTA) market is propelled by digital intelligence, which is transforming high-performance polymers through artificial intelligence. This technological advancement accelerates precision and automated manufacturing processes. Predictive modeling simulates terephthalic acid (PTA) purification under stress conditions, thereby reducing manufacturing timelines and facilitating large-scale optimized manufacturing.

Additionally, digital twin technology allows dimensional precision in advanced electronics components and minimizes material waste. Machine learning ensures these resins have responsiveness to environmental impact, which supports sophisticated autonomous and high-frequency PTA systems for future development.

Supply Chain Analysis of the Purified Terephthalic Acid (PTA) Market

- Feedstock Procurement: The stage of refining crude oil to extract mixed xylene and then processing it into high-purity paraxylene by using catalytic reforming and isomerization.

- Key Players: Saudi Aramco, ExxonMobil Chemical, Sinopec, Reliance Industries Ltd., and GS Caltex

- PTA Synthesis and Formulation: The stage of paraxylene oxidized in liquid phase acetic acid using catalytic oxidation to manufacture crude terephthalic acid, and then hydrogenated and purified into PTA.

- Key Players: Yisheng Petrochemical, Hengli Petrochemical, INEOS Aromatics, Indorama Ventures, Hanwha Impact, and Alpek Polyester

- End-User Integration: the stage consumer PTA in solid powder in react with Monoethylene glycol to create polyethylene terephthalate resin, fibers, and managing materials.

- Key Players: Indroma Ventures, Sinopec Yizheng Chemical Fibre, CR Chemical Materials

Regulatory Framework: Purified Terephthalic Acid (PTA) Market

| Region | Key Regulations | Regulatory Focus |

| Global | ISO 10993, NSF/ANSI standards 61 | Focus on the biocompatibility of PTA in medical tubing, and focus on the health effects of PTA |

| European Union | EU MDR, RoHS, BfR Recommendation XV, Directive (EU) mandates for Sustainability and migration limits | Standards for food processing equipment, PTA-based medical components, and mandates for recyclability and reduced environmental impact of plastic products. |

| United States | EPA standards, NHTSA, FDA 21 CFR, USP Class VI | Standards for VOC release and commercial framework. Focus on safety and emission reduction. |

| Asia Pacific | BIS Standards, GB 4806 | National regulations focus on safety, quality, and structural consolidation by restrictive self-contained aromatics. |

Purified Terephthalic Acid (PTA) Market Dynamics

Driver

Innovation and R&D

Innovation in the production of bio-based PTA and specialty polyester formulations gives rise to the development of high-performance purified terephthalic acid (PTA) that enhances flexibility and barrier performance. The increasing focus on reducing environmental impact and lowering waste generation is driving the adoption of green chemistry principles. Regulatory compliance and large-scale manufacturing demand are accelerating the R&D activities in purified terephthalic acid (PTA).

Restraints

Availability of alternatives to limit PTA adoption

Purified terephthalic acid (PTA) shows chemical purity, durability, operational efficiency, and low cost, boosting the demand. But the PP and PET offer superior clarity, flexibility, and heat resistance, integrate with the circular economy strategy, and focus on the reduction of carbon footprint. Thus, PTA alternatives represent a key restraining factor due to their higher cost for process automation and modernization activities.

Opportunity

Rising Consumer Concerns for Environmental and Sustainability

The growing consumer environmental concern and hygiene emphasis on sustainable practices are major opportunities that include bio-based purified terephthalic acid (PTA) and advanced recycling infrastructure. The rising focus on the sustainable alternative fueling market towards PTA derived from renewable feedstock. The rising investment and innovation in chemical and mechanical recycling technologies can convert impure PTA waste into high-quality purified terephthalic acid feedstock for the end-user industry sector.

Segmental Insights

Product Type Insights

The fiber grade PTA segment dominated the market with the largest share of 58% in 2025. It is key for high-speed industrial spinning by offering superior ultra-high chemical purity and high-tenacity. The fiber grade PTA acts as a key feedstock for manufacturing polyester fibers utilized in the textile sector to meet consumer hygiene compliance. This segment maintains durability and wrinkle resistance that make it key in the automotive and apparel sectors.

Market Share, By Product Type, 2025 (%)")

The bottle grade PTA segment held the 24% market share in 2025 and is expected to grow at the fastest CAGR of 6.3% over the forecast period, driven by its optical transparency and structural strength for manufacturing high-performance packaging resins and food-grade containers. The consumer's increasing demand for bottle-grade PTA is utilized in pharmaceutical, cosmetic, and beverage products to ensure consumer hygiene and safety.

The film grade PTA segment held the 12% market share in 2025, due to its demand in extrusion processes by offering a clean molecular structure and net-zero contamination. Film grade PTA is a key raw material for the production of biaxially-oriented polyester films, maintaining superior electrical insulation and heat resistance. It is ideal for flexible electronics and high-barrier food packaging.

The specialty grade PTA segment held 6% market share in 2025. It functions as a key reactant for specialized copolymer formulation and high-performance engineering by stabilizing molecular reactivity. Specialty grade PTA is utilized in automotive, aerospace, heat-resistant engineering plastics, and microelectronics.

Purified Terephthalic Acid (PTA) Market Share, By Product Type, 2025 (%)

| By Product Type | Revenue Share, 2025 (%) |

| Fiber Grade PTA | 58% |

| Bottle Grade PTA | 24% |

| Film Grade PTA | 12% |

| Specialty Grade PTA | 6% |

Production Technology Insights

The Amoco process segment dominated the market with the largest share of 52% in 2025. The technology is key for oxidizing paraxylene feedstock into crude acid mixture by utilizing a cobalt-manganese-bromide catalytic system. Amoco technology depends on a secondary, high-temperature palladium-catalysed hydrogenation phase to destroy impurity of 4-carboxybenzaldehyde. This process enables high feedstock yield and ultra-pure crystals for downstream polyester polymerization.

The BP optimized PTA process segment held the 25% market share in 2025 due to its ability to eliminate intermediate solid handling, where crude terephthalic acid slurry is transferred into the hydrogenation purification stage. It is a highly advanced manufacturing technology that integrates direct waste heat recovery by lowering greenhouse gas emissions and operating water usage in the chemical sector.

The continuous catalytic oxidation process segment held the 12% market share in 2025 and is expected to grow at the fastest CAGR of 6.8% over the forecast period. It utilizes a homogeneous cobalt-manganese-bromide catalyst in a continuously stirred tank reactor to convert paraxylene feedstock into a crude acid mixture. It integrates a liquid-phase system to capture exothermic reaction heat for optimal processing efficiency.

The mid-century process segment held 11% market share in 2025, serving as a multi-stage oxidation technology that oxidizes paraxylene using cobalt-manganese-bromide catalyst. To overcome the intermediate esterification stage, a highly efficient crude acid pathway for the advancement of secondary hydrogenation for modern Amoco technology licensing.

Purified Terephthalic Acid (PTA) Market Share, By Production Technology, 2025 (%)

| By Production Technology | Revenue Share, 2025 (%) |

| Amoco Process | 52% |

| Mid-Century Process | 11% |

| BP Optimized PTA Process | 25% |

| Continuous Catalytic Oxidation Process | 12% |

Application Insights

The polyester fiber segment dominated the market with the largest share of 61% in 2025 because it offers a structural monomer to produce high-tenacity polymer chains through melt condensation polymerization. The polyester fiber is extruded into staple fibers for the textile and apparel sector. The sportswear and garment industry demands polyester fiber due to its durability and cost-effectiveness. It is key for high-tenacity industrial yarn and heavy-duty industrial conveyor systems.

The polyethylene terephthalate (PET) segment held the 23% market share in 2025 and is expected to grow at the fastest CAGR of 6.7% over the forecast period, represent as thermoplastic resin that is synthesized through polycondensation reaction that combines with purified acid monomer to create a highly stable, recyclable polymer chain. PET is key for the packaging and bottling sector due to its superior oxygen barrier property, impact-resistance durability, and optical clarity. Additionally, it is processed into high-performance dielectric electronic films and lightweight automotive components.

The polyester films segment held the 8% market share in 2025 due to its superior tensile strength, dielectric resistance, and thermal stability that synthesized using polymer extrusion and mechanical stretching. It is essential in electronics, flexible packaging, and photovoltaic sectors, utilized to achieve an advanced state of biaxial orientation and manufacturing of multi-layer barrier laminates.

The engineering plastics segment held 4% market share in 2025, driven by its ability to synthesize specialized thermoplastics like polybutylene terephthalate by offering superior mechanical strength and thermal resistance while maintaining dimensional stability. The automotive and electric industry demands engineered plastics that are molded into under-the-hood components, circuit breakers, and high-voltage connectors.

Purified Terephthalic Acid (PTA) Market Share, By Application, 2025 (%)

| By Application | Revenue Share, 2025 (%) |

| Polyester Fiber | 61% |

| Polyethylene Terephthalate (PET) | 23% |

| Polyester Films | 8% |

| Engineering Plastics | 4% |

| Coatings & Resins | 3% |

| Others | 1% |

End User Industry Insights

The textile industry segment dominated the market with the largest share of 54% in 2025 due to the high-volume need for upstream chemical processing, where structural PTA polymerized and extruded covert into polyester staple fibers and textured filament yarns. The modern textile infrastructure demands high-speed mechanical looms where PTA provides superior shape retention and stain resistance.

The packaging industry segment held the 25% market share in 2025 and is expected to grow at the fastest CAGR of 6.8% over the forecast period. This sector focuses on chemical structural stability, where PTA offers superior carbon dioxide barrier performance and impact resistance. As consumer demand for food preservation and high-performance polyethylene terephthalate packaging resin increases, ensuring safety during long-haul transit is driving the market growth.

The electrical & electronics industry segment held the 7% market share in 2025, driven by demand for superior dielectric strength and structural integrity. PTA is key for synthesizing ultra-thin dielectric insulation films and heat-resistant engineering thermoplastics. The growth is propelled by next-generation hardware manufacturing practices where PTA is used in capacitors, flexible printed circuit boards, weather-resistant photovoltaic solar cell backsheets, and automotive wiring.

The automotive industry segment held 5% market share in 2025 due to major consumers within the vehicle manufacturing infrastructure, where PTA is key for synthesize crash resistant airbags, vehicle safety belts, and tire cord reinforcement by offering dimensional stability and superior strength -to-weight ratio. As the automotive sector focuses on modern lightweighting and safety compliances boosting the market expansion.

Purified Terephthalic Acid (PTA) Market Share, By End User Industry, 2025 (%)

| By End User Industry | Revenue Share, 2025 (%) |

| Textile Industry | 54% |

| Packaging Industry | 25% |

| Automotive Industry | 5% |

| Electrical & Electronics Industry | 7% |

| Consumer Goods Industry | 4% |

| Construction Industry | 3% |

| Chemical Industry | 2% |

Purity Level Insights

The standard purity PTA segment dominated the market with the largest share of 68% in 2025. It is key for the high-volume manufacturing sector, which set standard for producing general-purpose textile staple fibers and cost-effective PET container resins. It undergoes domestic filtration and crystallization during large-scale industrial polymerization.

The high purity PTA segment held the 24% market share in 2025, driven by demand for quality specifications in advanced polymer manufacturing. The high-purity PTA fosters secondary hydrogenation and a precise recrystallization cycle that drives 4-CBA to net-zero practices. The rising focus on higher polymerization kinetics and uniform molecular weight distribution to maintain chemical integrity. It is used in optical-grade dielectric polyester films, high-tenacity industrial filament, and crystal-clear food packaging.

The ultra-high purity PTA segment held the 8% market share in 2025 and is expected to grow at the fastest CAGR of 7.1% over the forecast period, fueled by its hyper-refined crystal structure that undergoes specialized multi-stage catalytic reduction and continuous supercritical fluid extraction. This segment offers higher thermal degradation and superior molecular consistency to synthesize advanced liquid crystal polymers and semiconductor encapsulation resins.

Purified Terephthalic Acid (PTA) Market Share, By Purity Level, 2025 (%)

| By Purity Level | Revenue Share, 2025 (%) |

| Standard Purity PTA | 68% |

| High Purity PTA | 24% |

| Ultra-high Purity PTA | 8% |

Distribution Channel Insights

The direct sales segment dominated the market with the largest share of 49% in 2025, serving as a B2B commercial high-volume industrial commodity that focuses on establishing long-term multi-year supply agreements directly with downstream consumer facilities. The direct commercial ensures a reliable supply for producers and buyers to eliminate intermediary handling fees and stabilize procurement costs.

The distributors & traders segment held the 24% market share in 2025, driven by primary manufacturers and fragmented downstream end-user spot-market transactions in the chemical ecosystem. In this segment, trading houses inject commercial flexibility and manage domestic warehouse facilities by offering credit facilities and short-term financing. Distributors & trades ensure cross-border logistics and execute price arbitrage.

The long-term supply contracts segment held the 21% market share in 2025 due to demand from downstream industrial hubs that preferred multi-year corporate agreements. This contract offers price-indexation formulas and adjustment of paraxylene feedstocks. Chemical manufacturers ensure a predictable and stable flow of raw materials.

The online commodity platforms segment held the 6% market share in 2025 and is expected to grow at the fastest CAGR of 7.0% over the forecast period. The segment is a specialized electronic exchanger with instantaneous real-time price discovery. The online commodity platforms eliminate administrative friction and provide transparency in chemical liquidity. Additionally, the segment executes automated future contract hedging by monitoring live assets and digital transaction clearing.

Purified Terephthalic Acid (PTA) Market Share, By Distribution Channel, 2025 (%)

| By Distribution Channel | Revenue Share, 2025 (%) |

| Direct Sales | 49% |

| Distributors & Traders | 24% |

| Long-term Supply Contracts | 21% |

| Online Commodity Platforms | 6% |

Regional Insights

How Did the Asia Pacific Dominated the Purified Terephthalic Acid (PTA) Market in 2025

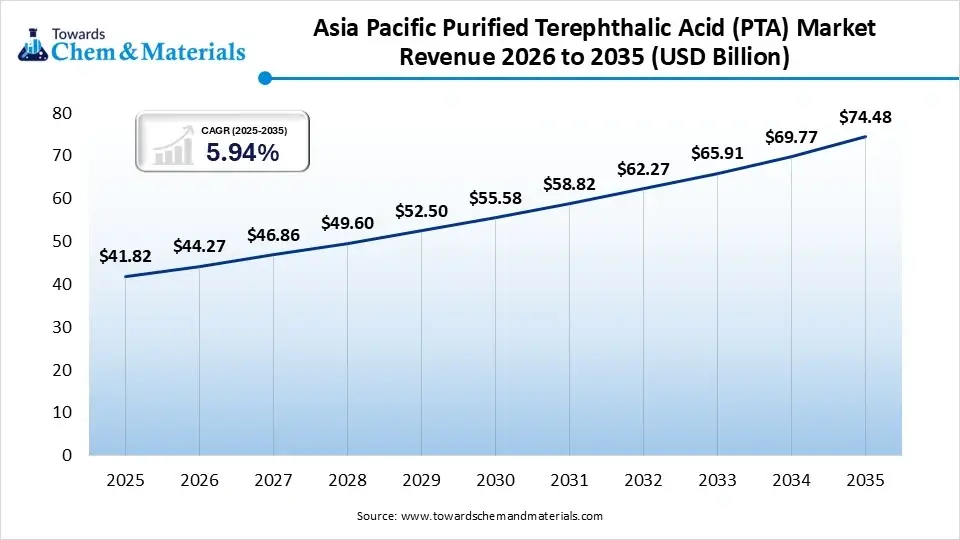

The Asia Pacific purified terephthalic acid market size was estimated at USD 3.40 billion in 2025 and is projected to reach USD 6.14 billion by 2035, growing at a CAGR of 6.09% from 2026 to 2035.Asia Pacific dominated the market by holding 58% share in 2025 and is expected to grow at the fastest with a CAGR of 6.7% during the forecast period. It is a key hub for production capacity expansion and downstream consumption of PTA with government support. The domestic industry is growing through its textile apparel manufacturing hubs and emerging fast-moving consumer goods. The region focuses on a closed-loop recycling system and recycled polyester material to meet sustainability commitments.

Market Revenue 2026 to 2035")

China Purified Terephthalic Acid (PTA) Market Growth Trends

China is witnessing significant growth in the PTA market due to its rising adoption on textile apparel industries and expanding rigid beverage packaging. The domestic facility focuses on automated infrastructure to supply high-speed polyester spinning lines and clear PET resins. China's stringent sustainability mandate and transition towards circular plastic recycling are driving the growth.

The Europe purified terephthalic acid market size was estimated at USD 2.15 billion in 2025 and is projected to reach USD 3.91 billion by 2035, growing at a CAGR of 6.16% from 2026 to 2035.Europe held the 16% market share in 2025 and expects notable growth in the market with 5.10% CAGR during the forecast period. The regional stringent environmental standards and substantial investment in a chemical recycling framework are boosting the market expansion. Europe downstream consumers focus on specialized PTA in high-performance automotive engineering plastic, premium medical packaging, and protective electronic films. Additionally, leading layers are integrating low-emission chemical refining and scaling up industrial chemical recycling.

Purified Terephthalic Acid (PTA) Market Share, By Regional, 2025 (%)

| Regional | Revenue Share, 2025 (%) |

| North America | 14% |

| Europe | 16% |

| Asia-Pacific | 58% |

| Latin America | 5% |

| Middle East & Africa | 7% |

Germany Purified Terephthalic Acid (PTA) Market Growth Trends

Germany market is a key region for technological and heavy engineering manufacturing hubs. The regional domestic manufacturers focus on downstream consumption for advanced automotive engineering plastics and specialized high-dielectric electronic films. Germany's shift towards decarbonization and chemical recycling infrastructure through corporate investment.

Market Share, By Regional, 2025 (%)")

Recent Developments

- In November 2025, Lotte Chemical complete sale of its 75.01% stake in the manufacturing subsidiary LCPL of Pakistani PTA production. LCPL is a company that creates 500,000 tons per year of high-purity terephthalic acid (PTA), utilized in polyester fibers, industrial yarns, and PET bottles.(Source: www.lottechem.com)

- In August 2025, Jiangxi Jiujiang Petrochemicals signed the contract for the seventh batch of major projects in 2025 and the 3 million tons/year PTA project. The project is a crucial step towards an integrated refining and aromatic hydrogen industry chain.(Source: www.seetaoe.com)

Top Companies in the Purified Terephthalic Acid (PTA) Market

Market Companies")

- Reliance Industries (IN)

- Indorama Ventures (TH)

- SABIC (SA)

- Mitsubishi Chemical (JP)

- Lotte Chemical (KR)

- Eastman Chemical (US)

- BASF (DE)

- Formosa Plastics (TW)

- PetroChina (CN)

- China National Petroleum Corporation (CN)

Segment Covered in the Report

By Product Type

- Fiber Grade PTA

- Textile-Grade PTA

- Industrial Fiber-Grade PTA

- Bottle Grade PTA

- Beverage Bottle Grade

- Food Packaging Grade

- Film Grade PTA

- Packaging Film Grade

- Electrical Film Grade

- Specialty Grade PTA

- High Purity PTA

- Modified PTA

By Production Technology

- Amoco Process

- Mid-Century Process

- BP Optimized PTA Process

- Continuous Catalytic Oxidation Process

By Application

- Polyester Fiber

- Apparel Fiber

- Home Textile Fiber

- Industrial Fiber

- Polyethylene Terephthalate (PET)

- Bottles & Containers

- Food Packaging

- Thermoforming Sheets

- Polyester Films

- Flexible Packaging Films

- Electrical & Electronics Films

- Optical Films

- Engineering Plastics

- Automotive Components

- Electrical Components

- Coatings & Resins

- Powder Coatings

- Unsaturated Polyester Resins

- Others

- Adhesives

- Specialty Chemicals

By End User Industry

- Textile Industry

- Packaging Industry

- Automotive Industry

- Electrical & Electronics Industry

- Consumer Goods Industry

- Construction Industry

- Chemical Industry

By Purity Level

- Standard Purity PTA

- High Purity PTA

- Ultra-High Purity PTA

By Distribution Channel

- Direct Sales

- Distributors & Traders

- Long-term Supply Contracts

- Online Commodity Platforms

By Region

- North America

- U.S.

- Canada

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Sweden

- Denmark

- Norway

- Asia Pacific

- China

- Japan

- India

- South Korea

- Thailand

- Latin America

- Brazil

- Mexico

- Argentina

- Middle East and Africa (MEA)

- South Africa

- UAE

- Saudi Arabia

- Kuwait

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

Tags

FAQ's

Select User License to Buy

Figures (6)