Content

What is PFAS Treatment Market Size and Share?

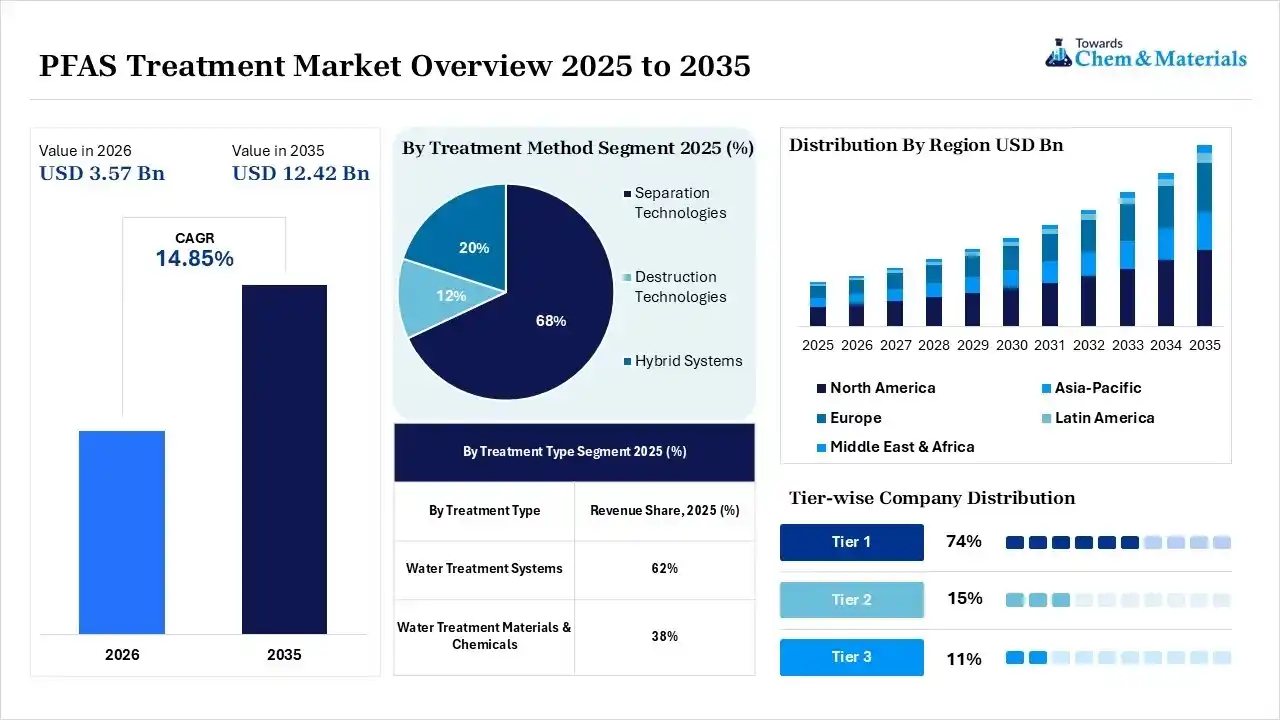

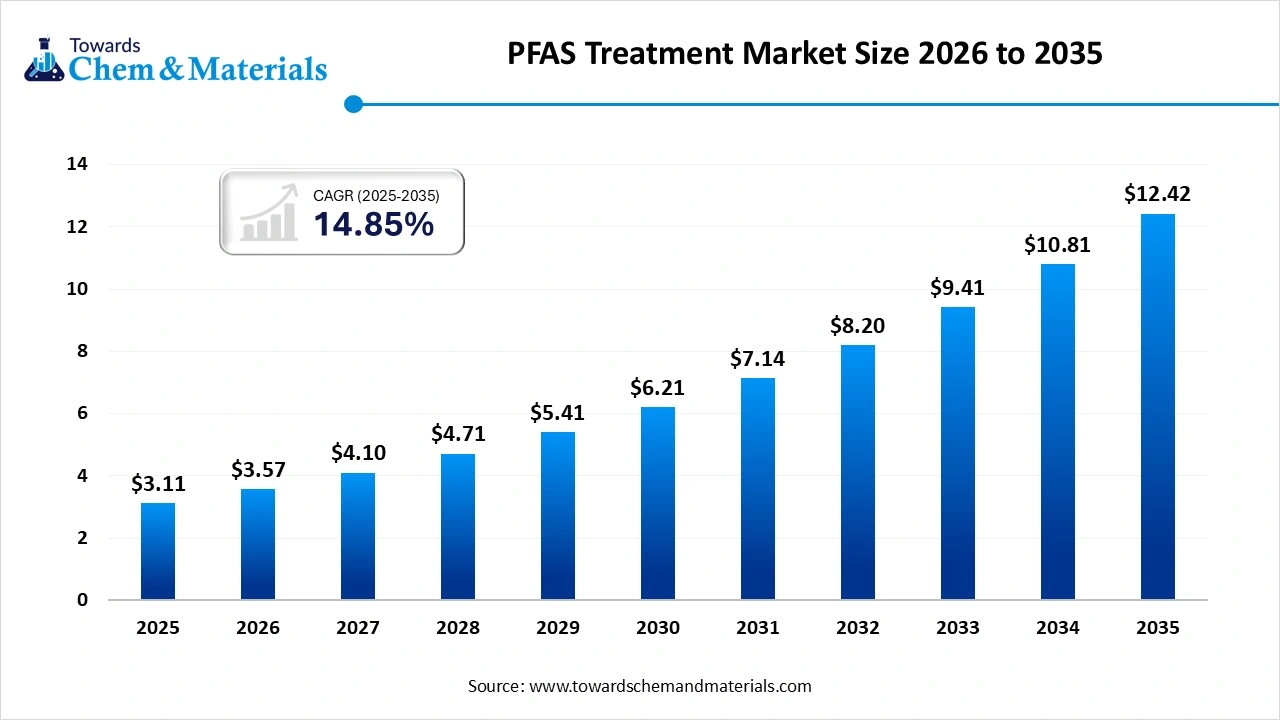

The global PFAS treatment market size was valued at USD 3.11 billion in 2025, is estimated to reach USD 3.57 billion in 2026, and is projected to reach USD 12.42 billion by 2035, exhibiting a compound annual growth rate (CAGR) of 14.85% over the forecast period from 2026 to 2035.North America dominated the PFAS treatment market with the largest revenue share of 43% in 2025 and is expected to grow at the fastest CAGR of 14.96% during the forecast period.The need for safer water supplies and ongoing sustainability initiatives is actively providing huge attention to the industry. Also, the greater and advanced technologies are going to major part of the industry, where all the participants are likely to depend on them during the projected time period.

Market Highlights

- By region, North America dominated the market with a share of 43% in 2025, due to the region having introduced some of the world's strictest regulations for PFAS monitoring and water treatment.

- By region, Asia Pacific is notably growing with a 21% market share in 2025 and is expected to be the fastest-growing region in the market, with a CAGR of 16.50% in the forecast period, owing to many countries increasing investments in clean water infrastructure and industrial wastewater treatment.

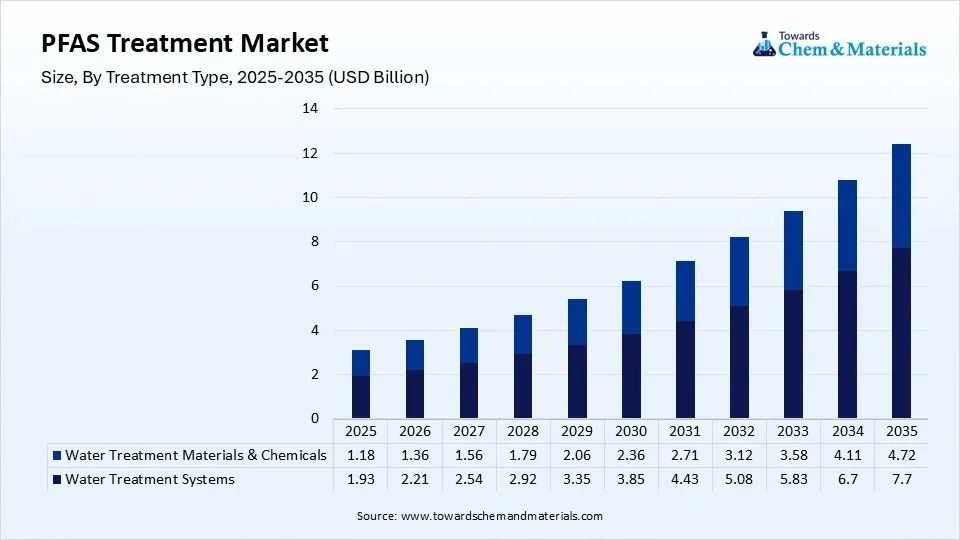

- By treatment type, the water treatment systems segment dominated the market with a 62% share in 2025, as they provide complete treatment solutions for municipal water plants, industrial facilities, and contaminated groundwater sites.

- By treatment type, the water treatment materials & chemicals segment held the 38% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 15.80% in the forecast period, owing to treatment media requiring regular replacement during operation.

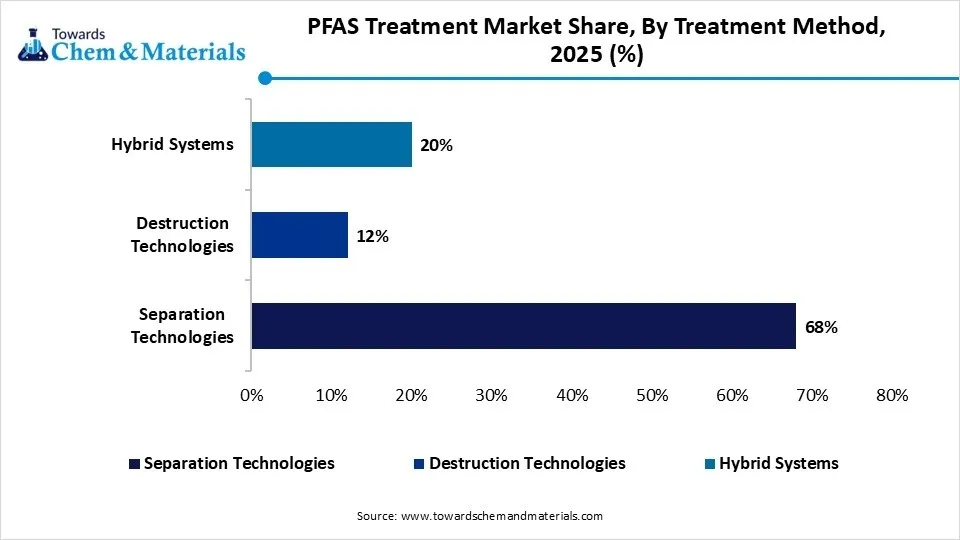

- By treatment method, the separation technologies segment dominated the market with 68% share in 2025, owing to its widespread provenness, commercial availability, and being trusted by water treatment operators.

- By treatment method, the hybrid systems segment held a 20% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 19.20% in the forecast period, owing to they combine multiple technologies within a single treatment process.

- By contamination source, the industrial discharge segment dominated the market with 31% share in 2025, owing to manufacturing industries having been major sources of PFAS contamination for many years.

- By contamination source, the firefighting foam (AFFF) sites segment held the 26% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 17.10% in the forecast period, owing to many airports, military facilities, oil and gas sites, and industrial plants replacing older PFAS-based firefighting foam systems.

- By application, the drinking water treatment segment dominated the market with 39% share in 2025, owing to clean drinking water is the first responsibility of every water utility and government authority.

- By application, the groundwater remediation segment held a 18% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 16.10% in the forecast period, owing to PFAS pollution often remaining underground for many years before it is discovered.

")

The heavy awareness and push for global water treatment has created greater advantages for the treatment provider nowadays. Also, the major industries and regional governments are playing a major role in the industry expansion by taking important designs and throwing regulations for water safety. Health consciousness is another factor leading the market potential. Moreover, the emergence of advanced and better filtration systems has been observed with more sophisticated destruction technologies, as per the reports.

- For instance, in June 2026, the PRM has unveiled the latest PFAS removal system. Also, the system is named PFAS-Snare™, and it is a containerized system as per the published report.(Source: www.prmfiltration.com)

The water utilities, manufacturing facilities, airports, and defense sites are among the major users of PFAS treatment systems. Furthermore, companies are introducing better filtration and destruction technologies to improve treatment performance. As environmental standards continue to become stricter across many regions, the need for efficient PFAS treatment solutions is likely to drive industry sales in the coming years.

Global Investment Flow for the PFAS Treatment Market 2026

Governments are allocating larger budgets for upgrading drinking water facilities with advanced PFAS treatment technologies to meet new environmental standards.

Industrial companies are investing in modern treatment systems to reduce PFAS discharge, improve environmental compliance, and strengthen sustainable manufacturing operations.

Technology developers are increasing research programs & commercial projects to introduce more efficient PFAS removal and destruction solutions while lowering treatment costs for customers.

- For instance, in 2025, Gradient introduced the latest PFAS destruction platform. Also, the platform is called ForeverGone and aims behind the innovation to establish cost-effective and sustainable solutions for water cleaning by removing PFAS.(Source: www.gradiant.com)

Market Trends

- The greater shift towards safer drinking water has emerged as a catalyst for unlocking the sector's full potential in recent years. Furthermore, as consumers become more aware, investment in filtration standards has increased.

- The focus on permanent PFAS removal solutions has allowed stakeholders to capitalize on growth opportunities in the current period. Several major treatment providers are increasingly seen investing in research and development activities nowadays.

- The major industrial participation in PFAS management is likely to strengthen the foundation of future sector growth. Also, several water treatment projects from the major industrial areas are in the pipeline, which is likely to provide greater advantage for the PFAS treatment providers.

Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 3.11 Billion |

| Expected Size in 2035 | USD 12.42 Billion |

| Growth Rate | CAGR of 14.85% |

| Base Year of Estimation | 2025 |

| Forecast Period | 2025-2035 |

| Dominant Region | North America |

| Segment Covered | By Treatment Type, By Treatment Method, By Contamination Source, By Application, By Region |

| Key Companies Profiled | Xylem, Veolia, Evoqua Water Technologies, Calgon Carbon, Clean Harbors, Regenesis, AECOM, Battelle, De Nora, Jacobs Solutions, Aquatech International |

Quick Technology Updations

The industry is aggressively moving from traditional filtration methods toward technologies that can completely break down PFAS chemicals instead of simply separating them from water. In addition, companies have increased research into advanced destruction methods that reduce secondary waste and improve environmental performance. Furthermore, treatment systems are becoming more automated through digital monitoring and smart process controls, allowing operators to improve efficiency and reduce maintenance needs.

Supply Chain Analysis of the PFAS Treatment Market:

- Production & Processing:Treating PFAS involves two main stages: separation and destruction. First, filters like activated carbon or ion exchange resins trap and concentrate the toxic chemicals from water.

Next, advanced technologies like electro-oxidation or extreme heat break the ultra-strong carbon-fluorine bonds, safely converting PFAS into harmless, natural byproducts. - Veolia: Veolia is a global environmental leader providing large-scale PFAS remediation. They deploy advanced activated carbon, ion exchange, and membrane filtration systems to clean municipal and industrial water supplies.

- Key players: 3M, DuPont, Chemours, and AECOM

- Quality Testing and Certification:Testing means checking the water both before and after it hits the filters to ensure every single drop is genuinely clean.

- Labs look for even microscopic traces of these stubborn chemicals, hunting for total fluorine to catch hidden variations.Independent watchdogs then run intense trials on the equipment to stamp it with an official seal of safety, proving to the public that the technology actually delivers on its promises.

Eurofins Scientific is a massive global laboratory network that specializes in hunting down PFAS down to single-digit parts per trillion.- Key agencies: EPA (U.S. Environmental Protection Agency), NSF International, ANSI (American National Standards Institute), and ECHA (European Chemicals Agency)

- Distribution to Industrial Users:Getting treatment systems to factories requires a mix of specialized engineering firms and heavy machinery distributors.

- They supply tailored, large-scale filtration rigs directly to chemical plants, airports, and manufacturing sites.

Brenntag: Brenntag is a massive global chemical and ingredients distributor that connects industrial facilities with crucial water treatment products. T

- Key players: Xylem, Kurita Water Industries, De Nora, and Aquatech International

PFAS Treatment Market Regulatory Landscape: Regulations?

| Country Region? | Regulatory Body? | Key Regulations? | Focus Areas? |

| United States | EPA (Environmental Protection Agency) | Safe Drinking Water Act (SDWA) — National Primary Drinking Water Regulations: Imposes legally binding limits (Maximum Contaminant Levels) restricting PFOA and PFOS to just 4 parts per trillion each, alongside limits on PFHxS, PFNA, and GenX. | Public Drinking Water Supplies: Upgrading local water plants with heavy-duty filtration setups like granulated carbon beds and ion-exchange filters to scrub tap water clean. |

| Europe | ECHA (European Chemicals Agency) | REACH Regulation (EC No 1907/2006) Annex XVII: Drives active restrictions on chemical use, including a firm phase-out of toxic firefighting foams and an active proposal to completely ban non-essential PFAS products across the continent. | Upstream Pollution Bans: Stopping the problem at the source by forcing manufacturers to swap out raw chemicals for eco-friendly alternatives before items ever hit the shelves. |

| China | Ministry of Ecology and Environment (MEE) | The Environmental and Ecological Code Article 645: Establishes a fresh national framework to actively track, register, and regulate "new pollutants"—putting a sharp legislative spotlight directly on tracking hidden PFAS lifecycles. | Industrial District Filtration: Concentrating heavy cleanup tech inside dedicated chemical manufacturing hubs, textile mills, and metal plating plants to trap toxic runoff at the source. |

Market Dynamics

Driver

Clean Water Demand with Local Government Support

The growing focus on clean and safe water is actively enhancing industry readiness and future industry capabilities. Also, governments are introducing stricter rules to reduce PFAS contamination in drinking water, groundwater, and industrial wastewater. This is encouraging municipalities and industries to install advanced treatment systems that can remove these harmful chemicals effectively. In addition, companies are investing in modern treatment technologies to comply with environmental standards and avoid penalties.

Restraint

Higher Cost and Lower Awareness

The high cost of treatment technologies is expected to hinder growth in the coming years. Also, the advanced filtration systems, destruction technologies, and regular maintenance require significant investment, making adoption difficult for small industries and municipalities with limited budgets. Furthermore, PFAS compounds are difficult to remove completely, which increases operating expenses and replacement costs for treatment materials.

Opportunity

Permanent Solution Approaches

The demand for technologies that permanently destroy PFAS chemicals is expected to create lucrative opportunities in the upcoming period. In recent years, industries and water utilities have started looking beyond traditional filtration systems because these methods only separate PFAS instead of eliminating them. In addition, companies developing advanced destruction technologies are attracting new investments and commercial partnerships. Governments are also supporting pilot projects to evaluate innovative treatment methods that reduce long-term environmental impact.

Segmental Insights

Treatment Type Insights

The water treatment systems segment dominated the market with 62% share in 2025, as they provide complete treatment solutions for municipal water plants, industrial facilities, and contaminated groundwater sites. These systems combine several treatment technologies to remove PFAS efficiently while meeting environmental regulations. Furthermore, many governments are upgrading existing water treatment infrastructure instead of building entirely new facilities, increasing demand for integrated treatment systems.

") The water treatment materials & chemicals segment held the 38% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 15.80% in the forecast period, owing to treatment media requiring regular replacement during operation. Activated carbon, ion exchange resins, specialty adsorbents, and treatment chemicals are consumed over time, creating continuous product demand. Furthermore, companies are developing improved materials with higher PFAS removal efficiency and longer service life. As more treatment plants become operational worldwide, the need for replacement materials will continue increasing.

The water treatment materials & chemicals segment held the 38% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 15.80% in the forecast period, owing to treatment media requiring regular replacement during operation. Activated carbon, ion exchange resins, specialty adsorbents, and treatment chemicals are consumed over time, creating continuous product demand. Furthermore, companies are developing improved materials with higher PFAS removal efficiency and longer service life. As more treatment plants become operational worldwide, the need for replacement materials will continue increasing.

PFAS Treatment Market Share, By Treatment Type, 2025 (%)

| By Treatment Type | Revenue Share, 2025 (%) |

| Water Treatment Systems | 62% |

| Water Treatment Materials & Chemicals | 38% |

Treatment Method Insights

The separation technologies segment dominated the market with 68% share in 2025, owing to it is widely proven, commercial availability, and trusted by water treatment operators. Technologies such as activated carbon filtration, membrane filtration, and ion exchange can effectively remove many PFAS compounds from contaminated water. Furthermore, these solutions are already installed in thousands of municipal and industrial treatment facilities, making adoption easier than newer technologies.

") The hybrid systems segment held a 20% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 19.20% in the forecast period, owing to they combine multiple technologies within a single treatment process. Instead of depending on one method, hybrid systems improve PFAS removal efficiency while reducing operating limitations. Furthermore, these systems allow operators to treat different PFAS compounds more effectively under changing water conditions.

The hybrid systems segment held a 20% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 19.20% in the forecast period, owing to they combine multiple technologies within a single treatment process. Instead of depending on one method, hybrid systems improve PFAS removal efficiency while reducing operating limitations. Furthermore, these systems allow operators to treat different PFAS compounds more effectively under changing water conditions.

PFAS Treatment Market Share, By Treatment Method, 2025 (%)

| By Treatment Method | Revenue Share, 2025 (%) |

| Separation Technologies | 68% |

| Destruction Technologies | 12% |

| Hybrid Systems | 20% |

Contamination Source Insights

The Industrial discharge segment dominated the market with 31% share in 2025, owing to manufacturing industries having been major sources of PFAS contamination for many years. Chemical manufacturing, metal finishing, electronics production, textile processing, and several other industries use PFAS-containing materials during production. Furthermore, governments are increasing monitoring of industrial wastewater, encouraging companies to install treatment systems before wastewater is released into the environment.

The firefighting foam (AFFF) sites segment held the 26% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 17.10% in the forecast period, owing to many airports, military facilities, oil and gas sites, and industrial plants replacing older PFAS-based firefighting foam systems. Furthermore, governments are identifying contaminated land and groundwater around these locations, creating significant demand for remediation projects. Environmental agencies are also introducing stricter regulations regarding firefighting foam use and disposal.

PFAS Treatment Market Share, By Contamination Source, 2025 (%)

| By Contamination Source | Revenue Share, 2025 (%) |

| Industrial Discharge | 31% |

| Firefighting Foam (AFFF) Sites | 26% |

| Landfills & Leachate | 14% |

| Wastewater Treatment Plants | 17% |

| Surface & Groundwater | 12% |

Application Insights

The drinking water treatment segment dominated the market with 39% share in 2025, owing to clean drinking water is the first responsibility of every water utility and government authority. Whenever PFAS contamination is detected, drinking water systems receive immediate attention to protect public health. This has encouraged faster installation of advanced treatment technologies in municipal water plants compared with many other applications.

The groundwater remediation segment held a 18% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 16.10% in the forecast period, owing to PFAS pollution often remains underground for many years before it is discovered. As environmental investigations continue, more contaminated sites are being identified near airports, industrial facilities, military locations, and landfill areas. Cleaning these water sources requires long-term remediation projects, creating sustained demand for advanced treatment technologies.

PFAS Treatment Market Share, By Application, 2025 (%)

| By Application | Revenue Share, 2025 (%) |

| Drinking Water Treatment | 39% |

| Wastewater Treatment | 24% |

| Groundwater Remediation | 18% |

| Soil Remediation | 8% |

| Industrial Process Water Treatment | 11% |

Regional Analysis

How will North America Dominate the PFAS Treatment Market in 2025?

North America dominated the market with a share of 43% in 2025, due to the region having introduced some of the world's strictest regulations for PFAS monitoring and water treatment. In the current period, governments are investing heavily in upgrading drinking water systems, cleaning contaminated sites, and supporting PFAS research. Furthermore, the region has many leading water treatment companies that continuously develop advanced treatment technologies.

United States

- The government has introduced stricter drinking water standards and increased funding for PFAS cleanup projects, while water utilities are upgrading treatment plants, and industries are investing in advanced treatment systems to meet environmental requirements.

- The technology companies are introducing new PFAS removal and destruction solutions to support growing demand in the country.

Canada

- Provincial governments and local authorities are working to identify PFAS-contaminated sites and strengthen drinking water protection, and municipalities are investing in modern treatment technologies to improve long-term water safety.

- Industrial companies are also upgrading wastewater treatment systems to reduce environmental impact and comply with changing environmental expectations.

PFAS Treatment Market Evaluation in Asia Pacific

Asia Pacific is notably growing with a 21% market share in 2025 and is expected to be the fastest-growing region in the market, with a CAGR of 16.50% in the forecast period, owing to many countries increasing investments in clean water infrastructure and industrial wastewater treatment. Rapid industrialization, urban population growth, and rising environmental awareness are creating strong demand for PFAS treatment solutions. Furthermore, governments are strengthening environmental regulations and encouraging industries to adopt advanced treatment technologies.

China

- The country continues to strengthen environmental protection and industrial wastewater management, and local governments are also investing in water treatment infrastructure while increasing inspections of industrial facilities.

- Also, companies in China are expanding production of advanced filtration materials and water treatment equipment to meet rising domestic demand.

Japan

- The country is increasing water quality monitoring while supporting research on efficient PFAS removal methods. In addition, companies in Japan are developing innovative filtration materials, membranes, and treatment systems to improve water purification performance.

- The municipal utilities are also upgrading treatment facilities to maintain safe drinking water supplies.

Europe Engineering Plastics Industry Conditions

Europe held the 27% market share in 2025, owing to environmental protection remaining a major priority across the region. Governments are introducing stricter PFAS regulations while increasing investments in water treatment infrastructure and contaminated site remediation. Furthermore, industries are improving wastewater management to comply with changing environmental standards. European companies are also investing in sustainable treatment technologies that reduce environmental impact while improving treatment efficiency.

Germany

- Manufacturing industries are investing in advanced wastewater treatment systems to reduce PFAS discharge and improve regulatory compliance, while German technology companies continue to develop innovative filtration and water purification solutions for both domestic and international markets.

- Continuous investment in environmental technologies and industrial modernization has been observed.

Italy

- Local authorities in Italy have strengthened water monitoring programs while encouraging investments in modern treatment infrastructure, and industries are adopting better wastewater treatment practices to reduce environmental pollution and meet European environmental requirements.

- Also, research institutions and water technology companies are supporting the development of more effective PFAS treatment solutions.

PFAS Treatment Market Survey in Latin America

Latin America held a 5% market share in 2025 as several countries are paying greater attention to protecting rivers, lakes, and underground water resources. Industries are realizing that untreated PFAS contamination can create future environmental & legal challenges. This is encouraging companies to upgrade their water treatment processes before stricter regulations become widespread. At the same time, cities are investing in cleaner water infrastructure to improve public health and support long-term development.

Brazil

- Industries such as mining, chemicals, pulp and paper, and manufacturing are placing greater importance on improving wastewater quality before discharge, while several water utilities are modernizing treatment facilities to meet the growing demand for clean drinking water in expanding urban areas.

- The companies are also increasing investments in sustainable production practices to improve environmental performance.

Argentina

- Many manufacturing facilities are reviewing their wastewater treatment processes to improve operational sustainability and prepare for future environmental requirements, while the local authorities are giving more attention to protecting freshwater resources that support agriculture and nearby communities.

- Also, universities and environmental organizations are increasing research related to water pollution and treatment.

Middle East and Africa Engineering Plastics Sector Observation

The Middle East and Africa held a 4% market share in 2025, akin to water has become one of the region's most valuable resources. Instead of relying only on freshwater supplies, many countries are expanding water recycling and reuse projects for industries and cities. This shift is encouraging the use of advanced treatment technologies that can remove difficult contaminants such as PFAS. At the same time, industrial expansion and new infrastructure projects are increasing the need for better wastewater management.

Saudi Arabia

- The country is making water security a long-term national priority, while large investments in industrial cities, energy projects, and manufacturing facilities are increasing the demand for reliable water treatment systems.

- The new industrial developments require better wastewater treatment solutions to improve environmental performance and operational efficiency.

UAE

- The country is investing heavily in smart and sustainable water management, while rapid urban development, tourism projects, and industrial expansion are increasing the need for high-quality treated water throughout the country.

- Also, the country is also encouraging innovation in water treatment through partnerships with international technology companies.

Competitive Analysis

The market is becoming more competitive as companies focus on developing technologies that remove or permanently destroy PFAS compounds more efficiently. Also, instead of competing only on equipment sales, leading companies are expanding engineering services, pilot testing, monitoring solutions, and complete treatment systems.

Xylem is increasing its PFAS treatment capabilities by combining advanced filtration technologies with digital water management solutions and establishing strategic collaborations with other key players. It is also investing in research to improve treatment efficiency while reducing operating costs for customers. (Source: www.businesswire.com)

- Ovivo continues improving membrane filtration and advanced water purification technologies for industrial and municipal applications with the nomination of 2025 Water Technology Company of the Year. Also, the company is focusing on increasing treatment performance while reducing maintenance requirements.

(Source:ovivowater.com)

Top Vendors in the PFAS Treatment Market & Their Offerings

| Company | Company Type/Position | Major Headquarters | Geographic Presence | Offerings | Key Strength |

| Veolia | Global Environmental Leader | Paris, France | Active across all 5 continents with a heavy footprint in Europe and North America | Large-scale water filtration setups, mobile treatment trailers, and hazardous filter destruction services. | Massive infrastructure capacity to manage entire city water supplies and complex industrial waste networks. |

| Evoqua Water Technologies | Specialized Water Solutions Provider | Washington, D.C., USA | Deeply rooted across North America with expanding operations in Europe and Asia-Pacific. | Advanced carbon tanks, ion-exchange resin filters, and dedicated services to reactivate spent carbon media | Rapid deployment of emergency mobile treatment trailers to communities facing sudden water contamination crises. |

| Calgon Carbon | Carbon Material Specialist | Pennsylvania, USA | Strong operational hubs in the United States, Europe, and major industrial centers in Asia. | High-grade granular activated carbon (GAC) media and thermal destruction furnaces for safe chemical recycling. | Industry pioneer in designing high-surface-area carbon particles that maximize the trapping of stubborn chemicals. |

Other Key Players

Recent Development

- In June 2025, Veolia introduced its latest PFAS treatment, which is designed for hazardous waste with the removal of persistent pollutants. Also, the newly launched technology is called Drop® technology and is promoted across the entire European region, as per the published report.(Source: www.veolia.com)

Segments Covered in the Report

By Treatment Type

- Water Treatment Systems

- Granular Activated Carbon (GAC) Systems

- Ion Exchange (IX) Systems

- Reverse Osmosis (RO) Systems

- Membrane Filtration Systems

- Advanced Oxidation Systems

- Electrochemical Treatment Systems

- Water Treatment Materials & Chemicals

- Activated Carbon Media

- Ion Exchange Resins

- Coagulants & Flocculants

- Oxidizing Agents

- Adsorbents

- Specialty PFAS Removal Chemicals

By Treatment Method

- Separation Technologies

- Granular Activated Carbon

- Ion Exchange

- Reverse Osmosis

- Nanofiltration

- Membrane Adsorption

- Destruction Technologies

- Electrochemical Oxidation

- Plasma Treatment

- Supercritical Water Oxidation

- Photocatalytic Oxidation

- Thermal Destruction

- Hybrid Systems

- GAC + RO

- IX + RO

- Adsorption + Oxidation

- Multi-Barrier Treatment Systems

By Contamination Source

- Industrial Discharge

- Chemical Manufacturing

- Semiconductor Manufacturing

- Textile Processing

- Metal Finishing

- Firefighting Foam (AFFF) Sites

- Airports

- Military Bases

- Fire Training Facilities

- Landfills & Leachate

- Municipal Landfills

- Industrial Landfills

- Wastewater Treatment Plants

- Municipal WWTPs

- Industrial WWTPs

- Surface & Groundwater

- Rivers & Lakes

- Aquifers

- Reservoirs

By Application

- Drinking Water Treatment

- Municipal Drinking Water

- Rural Water Systems

- Wastewater Treatment

- Municipal Wastewater

- Industrial Wastewater

- Groundwater Remediation

- In-Situ Treatment

- Ex-Situ Treatment

- Soil Remediation

- Excavation & Treatment

- Stabilization Methods

- Industrial Process Water Treatment

- Electronics Industry

- Chemical Industry

- Manufacturing Industry

By Regional

- North America

- Europe

- Asia Pacific

- Middle East & Africa

- Latin America

FAQ's

Select User License to Buy

Figures (4)