Content

PFAS Filtration Market Size, Share, Growth and Forecast 2026-2035

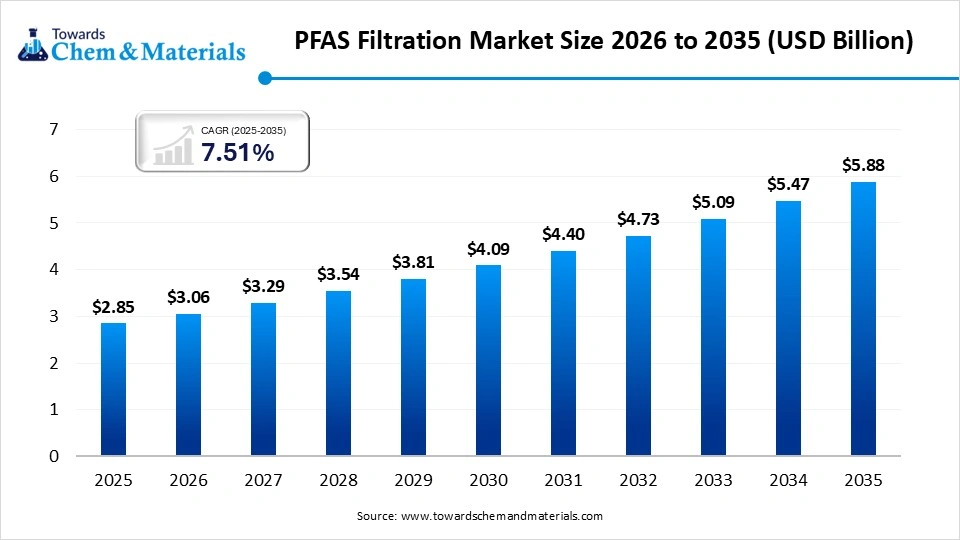

The global PFAS filtration size was estimated at USD 2.85 billion in 2025 and is expected to increase from USD 3.06 billion in 2026 to USD 5.88 billion by 2035, growing at a CAGR of 7.51% from 2026 to 2035. North America dominated the PFAS filtration with the largest revenue share of 43.00% in 2025.The heavy demand for clean water in every sector has fueled the industry's growth in recent years.The removing of the PFAS chemicals from the water before it is used for some work is known as the PFAS filtration. Moreover, helping to remove chemicals with ordinary filtration does not stop; the PFAS filtration has gained major industry attention in recent years. Also, the chemicals that are primarily used in these filtration processes are difficult to break down and are seen to remain in water for a longer period, as per recent observations.

")

Market Highlights

- North America dominated PFAS filtration market with the largest revenue share of 43.00% in 2025., due to PFAS becoming a public issue there earlier than in many other places.

- By region, Europe is anticipated to capture a greater portion of the market with a significant CAGR in the future due to its increasing link with preventive water policy rather than only contamination response.

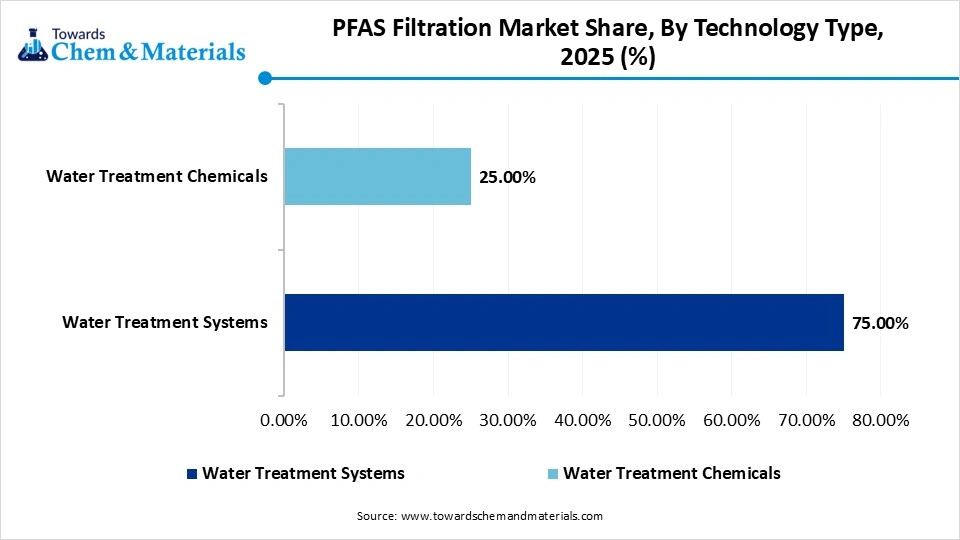

- By technology, the water treatment systems segment dominated the market and accounted for the largest revenue share of 75.00% in 2025, owing to full treatment equipment was the first practical solution when PFAS concerns became serious.

- By technology, the water treatment chemicals segment is expected to grow during the forecast period, due to buyers increasingly wanting flexible treatment options rather than full equipment replacement.

- By place of treatment, the ex-situ segment led the market with the largest revenue share of 65.00% in 2025, owing to it is easier to control over water when it is removed from the source and treated in a separate system.

- By place of treatment, the in-situ segment is expected to grow during the forecast period, due to its ability to clean contamination directly where it exists without moving large volumes of water.

- By end use, the municipal segment dominated the market and accounted for the largest revenue share of 38.00% in 2025, owing to full city water systems affecting large numbers of people every day.

- By end use, the industrial segment is expected to grow during the forecast period, due to PFAS contamination, which first became strongly visible around industrial operations.

Beyond Single Filters Toward Layered Systems

The market has seen a move from single-stage filtration to layered treatment systems. Also, earlier, one filter material was often expected to solve the problem alone. Now, treatment systems increasingly combine multiple stages such as adsorption, membrane separation, and selective polishing materials in one treatment sequence. This happens because PFAS molecules vary in size and chemical behavior, so one method may remove some types better than others. New systems are being designed to treat PFAS in steps rather than relying on one barrier.

Market Trends:

- The increasing usage of daily water filtration instead of only industrial processing has strengthened the bottom line for the production firms in recent years. Also, these initiatives have been increasingly observed in business, modern cities, and households in the past few years.

- The trend towards awareness and evidence-based cleaning services has attracted increased capital and investment in manufacturing nowadays. Also, several consumers are demanding measurable proof that PFAS removal actually works.

- The targeting of smaller contaminated spaces is expected to present new business models for forward-thinking manufacturers during the projected period. Also, in recent years, the manufacturers are targeting only large industrial spaces and military areas, but in recent years, the need for filtration has gained heavy attention in smaller places too, like households, local manufacturing zones, and commercial laundry.

Report Scope

| Report Attribute | Details |

| Market Size in 2026 | USD 3.06 Billion |

| Revenue Forecast in 2035 | USD 5.88 Billion |

| Growth Rate | CAGR 7.51% |

| Forecast Period | 2026 - 2035 |

| Base Year | 2025 |

| Dominant Region | Asia Pacific |

| Segment Covered | By Technology Type, By Place of Treatment, By End Use Industry, By Region |

| Key companies profiled | Veolia, AECOM, Xylem, Pentair, WSP, Jacobs, TRC Companies, Inc., Cyclopure, Inc., Mineral Technologies, Inc., CDM Smith, Inc. |

Supply Chain Analysis of the PFAS Filtration Market:

Distribution to Industrial Users

- Industrial distributors supply PFAS filtration systems such as Granular Activated Carbon (GAC), Ion Exchange (IX) resins, and Reverse Osmosis (RO) units directly to sectors like chemical manufacturing, metal finishing, and electronics.

- These distributors provide specialized logistics, technical integration, and replacement media to help plants meet stringent EPA and local discharge limits. By bridging the gap between OEMs and end-users, they ensure continuous compliance and operational safety in high-volume water treatment.

Chemical Synthesis and Processing

- Chemical synthesis of PFAS filtration media involves engineering specialized surfaces, such as fluorinated functional groups on ion-exchange resins or high-surface-area activated carbons.

- Processing focuses on optimizing pore size distribution and surface charge to maximize adsorption kinetics. These advanced materials are then thermally or chemically treated to ensure durability against aggressive industrial solvents.

Regulatory Compliance and Safety Monitoring

- Regulatory compliance requires adhering to strict EPA Health Advisories and NPDES discharge permits to mitigate environmental risks.

- Safety monitoring involves frequent liquid chromatography-mass spectrometry (LC-MS) testing to detect "breakthrough" points in filtration media. Ensuring high removal efficiency protects workers and local ecosystems from the bioaccumulative effects of PFAS.

PFAS Filtration Market Regulatory Landscape: Global Regulations

| Country Region | Regulatory Body | Key Regulations | Focus Areas |

| United States | Environmental Protection Agency (EPA) | Safe Drinking Water Act (SDWA): National Primary Drinking Water Regulation (NPDWR) (finalized April 2024). It sets Maximum Contaminant Levels (MCLs) at 4.0 ppt for PFOA and PFOS individually. | Public water systems (monitoring and treatment), hazardous waste remediation, and industrial discharge permits (NPDES). |

| European Union | European Chemicals Agency (ECHA). | REACH Regulation (EC 1907/2006): Annex XVII includes specific restrictions on PFOA and PFHxS. A Universal PFAS Restriction Proposal (submitted in 2023) aims to ban nearly all ~10,000 PFAS substances with limited "essential use" derogations. | Eliminating non-essential uses in consumer goods (textiles, food packaging), strict groundwater quality standards, and transitioning to PFAS-free industrial alternatives. |

| China |

Ministry of Ecology and Environment (MEE). |

Several PFAS groups are now subject to Environmental Impact Assessment (EIA) requirements and discharge limits. |

Industrial wastewater management in high-density chemical parks, animal-derived food safety (GB 5009.253), and alignment with the Stockholm Convention on Persistent Organic Pollutants. |

Segmental Insights

Technology Insights

How did the Water Treatment Systems Segment Dominate the PFAS Filtration Market in 2025?

The water treatment systems segment dominated the market share 75.00% in 2025, due to full treatment equipment was the first practical solution when PFAS concerns became serious. Also, the Large treatment systems are likely to be installed directly into municipal water plants, industrial discharge lines, or facility treatment units without redesigning the entire water infrastructure. Moreover, the operators preferred complete systems because they offered immediate operational control and could be integrated into existing treatment processes. Also, when PFAS became important, the users wanted visible installed solutions instead of separate treatment components nowadays.

")

The water treatment chemicals segment is expected to grow with a rapid CAGR, owing to buyers increasingly wanting flexible treatment options rather than full equipment replacement. Moreover , in the many cases, changing adsorbents, resins, or treatment chemicals inside existing systems is easier than building entirely new infrastructure. This lowers cost and speeds up adaptation when PFAS standards become stricter. Furthermore, the treatment materials can be upgraded more frequently as PFAS improves in the coming years.

PFAS Filtration Market Share, By Technology Type , 2025 (%)

| By Technology Type | Revenue Share, 2025 (%) |

| Water Treatment Systems | 75.00% |

| Water Treatment Chemicals | 25.00% |

- Water Treatment Systems (75.00% Why it dominates: "Accounts for 75.00% of the market, driven by widespread adoption of advanced filtration technologies such as activated carbon and membrane systems for effective PFAS removal and regulatory compliance."

- Water Treatment Chemicals (25.00%) Why it is gaining momentum: "Holds 25.00% share, supported by increasing use of chemical treatment solutions to enhance filtration efficiency and complement system-based purification processes."

Place of Treatment Insights

How did the Ex-Situ Segment Dominate the PFAS Filtration Market in 2025?

The ex-situ segment dominated the market accounting for 65.00% of total revenue in 2025, due to it is easier to control over water when it is removed from the source and treated in a separate system. In simple terms, water is taken out, cleaned in a treatment unit, and then reused or released. This gives operators better control because they can monitor the water closely and change filters when needed. Many early PFAS projects used this method because it gave quick and visible results. Also, the industries and water plants already had treatment units where ex-situ systems could be added easily.

The in-situ segment is expected to grow with a rapid CAGR, owing to it cleans contamination directly where it exists without moving large volumes of water. Moreover, this saves time, space, and often reduces long-term operating effort. Instead of pumping water out continuously, treatment happens underground or inside the affected area itself. This becomes attractive when contamination spreads across large land areas because moving all the water becomes expensive. In the future, many users may prefer solving PFAS problems closer to the source rather than building larger external systems.

PFAS Filtration Market Share, By Place of Treatment, 2025 (%)

| By Place of Treatment | Revenue Share, 2025 (%) |

| Ex-Situ | 65.00% |

| In-Situ | 35.00% |

- Ex-Situ (65.00%) Why it dominates: "Accounts for 65.00% of the market, driven by its effectiveness in treating contaminated water through centralized systems with controlled processing and high removal efficiency."

- In-Situ (35.00%) Why it is gaining momentum: "Holds 35.00% share, supported by increasing adoption of on-site treatment solutions offering cost efficiency and minimal disruption to existing infrastructure."

End Use Insights

How did the Municipal Segment Dominate the PFAS Filtration Market in 2025?

The municipal segment dominated the market share 38.00% in 2025, due to city water systems affecting large numbers of people every day. Also, when PFAS is found in public water, local authorities usually act quickly because drinking water safety directly affects communities. Municipal treatment also often covers schools, homes, hospitals, and public buildings together, so one treatment decision affects thousands of users. Furthermore, the public water systems are expected to meet strong quality standards, so they often adopt filtration early when new water concerns appear because municipal systems serve many people at once, they have become one of the strongest drivers in PFAS filtration demand.

The industrial segment is expected to grow with a rapid CAGR, owing to PFAS contamination, which first became strongly visible around industrial operations. Also, many manufacturing activities traditionally use PFAS-containing materials in coatings, processing chemicals, firefighting foams, and industrial cleaning systems. This created direct pressure for factories to install filtration systems before releasing water. Industries are always ready to act first when they face operational risk if contamination affects permits, discharge compliance, or nearby water sources. Moreover, the industrial users usually manage high water volumes, making treatment investment necessary earlier than in many smaller sectors.

PFAS Filtration Market Share, By End Use Industry, 2025 (%)

| By End Use Industry | Revenue Share, 2025 (%) |

| Commercial | 16.00% |

| Agriculture | 12.00% |

| Municipal | 38.00% |

| Industrial | 21.00% |

| Healthcare | 13.00% |

- Municipal (38.00%) Why it dominates: "Accounts for 38.00% of the market, driven by large-scale public water treatment needs, strict regulatory standards, and increasing investments in safe drinking water infrastructure."

- Industrial (21.00%) Why it is gaining momentum: "Holds 21.00% share, supported by rising focus on wastewater treatment and regulatory compliance across manufacturing and processing industries."

- Commercial (16.00%) Why it is gaining momentum: "Represents 16.00% of the market, driven by growing adoption of water filtration systems in offices, hospitality, and retail facilities."

- Healthcare (13.00%) Why it is gaining momentum: "Accounts for 13.00% share, supported by increasing demand for high-purity water in hospitals, laboratories, and pharmaceutical applications."

- Agriculture (12.00%) Why it is gaining momentum: "Captures 12.00% of the market, driven by rising awareness of water quality for irrigation and livestock, along with adoption of treatment solutions in farming operations."

Regional Insights

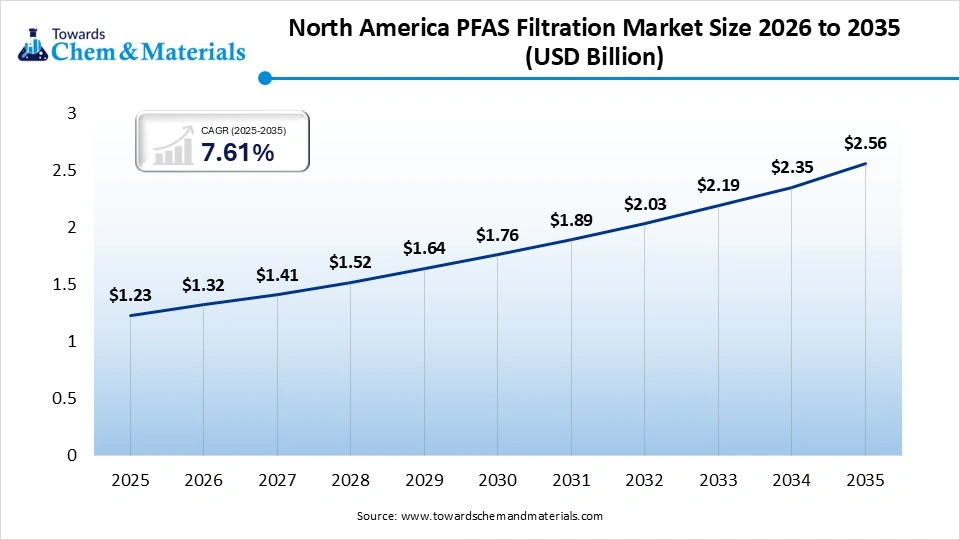

The North America PFAS filtration market size was valued at USD 1.23 billion in 2025 and is expected to be worth around USD 2.56 billion by 2035, exhibiting at a compound annual growth rate (CAGR) of 7.61% over the forecast period from 2026 to 2035. North America dominated the PFAS filtration market in 2025, due to PFAS became a public issue there earlier than in many other places. Water testing increased, people became more aware, and many local areas started improving water treatment systems. Industries, public water systems, and communities all began looking for solutions. This early attention created strong market potential, while many older industrial areas need water upgrades. Because awareness came early and North America became the biggest market in recent years, as per the observation.

")

United States PFAS Filtration Market Trends

The United States maintained its dominance in the market, owing to PFAS, which gained major industry attention across many cities and industries. Different areas found different water concerns, so demand appeared in many places at the same time in the country nowadays. Some places needed industrial treatment, while others focused on public water systems. The country also has many separate local water systems, which means many individual projects happen together. This creates a broad and active market. Also, water safety awareness has become very important in many regions, and PFAS filtration continues to grow across the United States in the coming years.

PFAS Filtration Market Evaluation in Europe

Europe is expected to capture a major share of the PFAS filtration market with a rapid CAGR, owing to its increasing link with preventive water policy rather than only contamination response. Also, many European systems often act early when a contaminant shows long-term environmental persistence. This creates market growth not only where contamination already exists but also where future treatment standards are anticipated. Moreover, the water systems in many European regions are highly structured, making filtration upgrades easier to implement systematically.

Precision Filtration Backed By German Expertise

Germany is expected to emerge as a prominent country for the PFAS filtration market in the coming years, due to because water treatment is taken very seriously and often planned for long-term use. Moreover, the industries and public systems both focus on high-quality treatment methods. Germany also has strong technical knowledge in filtration and industrial water systems. As these advanced infrastructures, PFAS filtration fits well into existing water improvement work. The country is likely to become a greater market due to both industry and public water systems are likely to adopt advanced treatment step by step.

")

Asia Pacific PFAS Filtration Market Examination

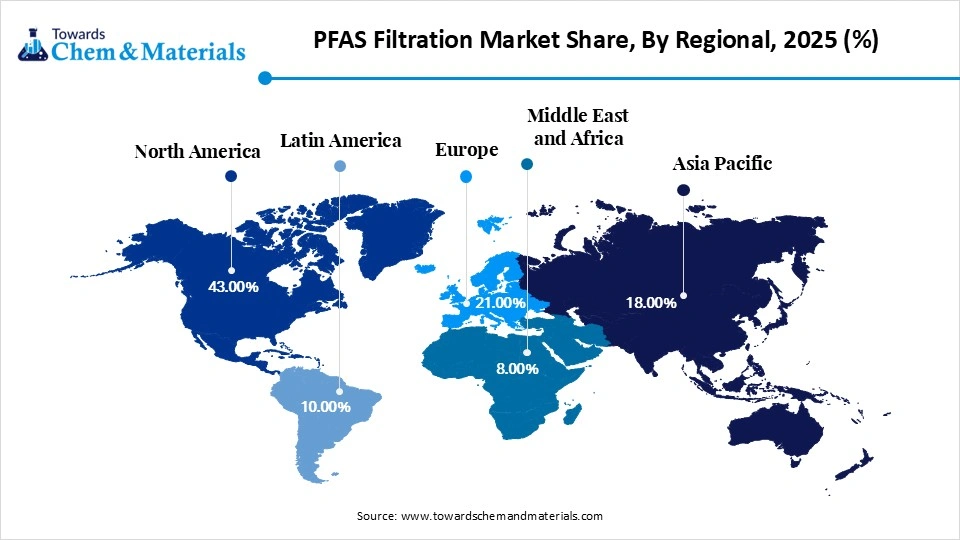

Asia Pacific filtration market segment accounted for the major revenue share of 18.00% in 2025. Asia Pacific is notably growing in industry, owing to PFAS treatment demand is now expanding alongside industrial modernization and urban water quality. Also, in many parts of the region, rapid industrial growth happened before advanced contaminant monitoring became common. As monitoring improves, more water systems are beginning to identify PFAS-related treatment needs. Moreover, the urban populations are expanding quickly, making water quality more politically and socially important.

PFAS Filtration Market Share, By Regional, 2025 (%)

| Regional | Revenue Share, 2025 (%) |

| North America | 43.00% |

| Europe | 21.00% |

| Asia Pacific | 18.00% |

| Latin America | 10.00% |

| Middle East & Africa | 8.00% |

- North America (43.00% Why it dominates: "Accounts for 43.00% of the market, driven by stringent regulatory frameworks, high awareness of PFAS contamination, and strong investments in advanced water treatment infrastructure."

- Europe (21.00%) Why it is gaining momentum: "Holds 21.00% share, supported by increasing environmental regulations and growing adoption of sustainable water purification technologies."

- Asia Pacific (18.00%) Why it is gaining momentum: "Represents 18.00% of the market, driven by rapid industrialization, urbanization, and rising focus on water quality management."

- Latin America (10.00%) Why it is gaining momentum: "Accounts for 10.00% share, supported by expanding water treatment initiatives and improving infrastructure development."

- Middle East & Africa (8.00%) Why it is gaining momentum: "Captures 8.00% of the market, driven by increasing investments in water security and adoption of filtration solutions in water-scarce regions."

Industrial Growth Fuels Water Filtration Demand in China

China is expected to gain a significant industry share owing to water treatment increasingly connecting with industrial upgrading and environmental efficiency in the country nowadays. As industries modernize, water quality standards become part of production competitiveness. This creates filtration demand not only for public systems but also inside industrial supply chains. Also, the large urban regions require stable water quality across growing populations, which encourages investment in advanced treatment technologies in China for the upcoming years, as per the future industry expectations.

Recent Developments

- In October 2025, Cleanova unveiled its PFAS-Free Media Coalescing Filters. Also, these filters are specifically designed for sustainable gas filtration and launched under the series named the Dollinger GP-198 series, as per the published report by the company recently.(Source: www.cleanova.com)

- In September 2025, Kurita America created a strategic collaboration with Cyclopure. Also, the motive behind these partnership establishments is to deliver the PFAS solution, which is more sustainable and advanced with DEXSORB technology of Cyclopure, as per the published report.(Source: www.indianchemicalnews.com)

Top Vendors in the PFAS Filtration Market & Their Offerings:

- Veolia: French transnational giant specializing in optimized resource management. In the PFAS sector, they provide end-to-end water treatment solutions, including advanced incineration services for contaminated waste and mobile water treatment units.

- AECOM: Global infrastructure consulting firm that leads the market in PFAS remediation and site assessment. They offer specialized engineering services to identify contamination plumes and design custom filtration systems.

- Xylem: leading American water technology provider famous for its Leopold and Wedeco brands. They manufacture high-efficiency filtration systems, including ozone oxidation and advanced carbon adsorption units.

- Pentair: Diversified water treatment company that focuses on both industrial and residential filtration solutions. They produce high-performance membrane technologies and specialized point-of-entry (POE) systems certified to reduce

- PFOA/PFOS.

- WSP

- Jacobs

- TRC Companies, Inc.

- Cyclopure, Inc.

- Mineral Technologies, Inc.

- CDM Smith, Inc.

Segments Covered in the Report

By Technology Type

- Water Treatment Systems

- Water Treatment Chemicals

By Place of Treatment

- Ex-Situ

- In-Situ

By End Use Industry

- Commercial

- Agriculture

- Municipal

- Industrial

- Healthcare

By Region

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Asia Pacific

- China

- India

- Japan

- South Korea

- Latin America

- Brazil

- Argentina

- Middle East & Africa

- Saudi Arabia

- South Africa

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

FAQ's

Select User License to Buy

Figures (4)