Content

What is the Methanol market Size and Share?

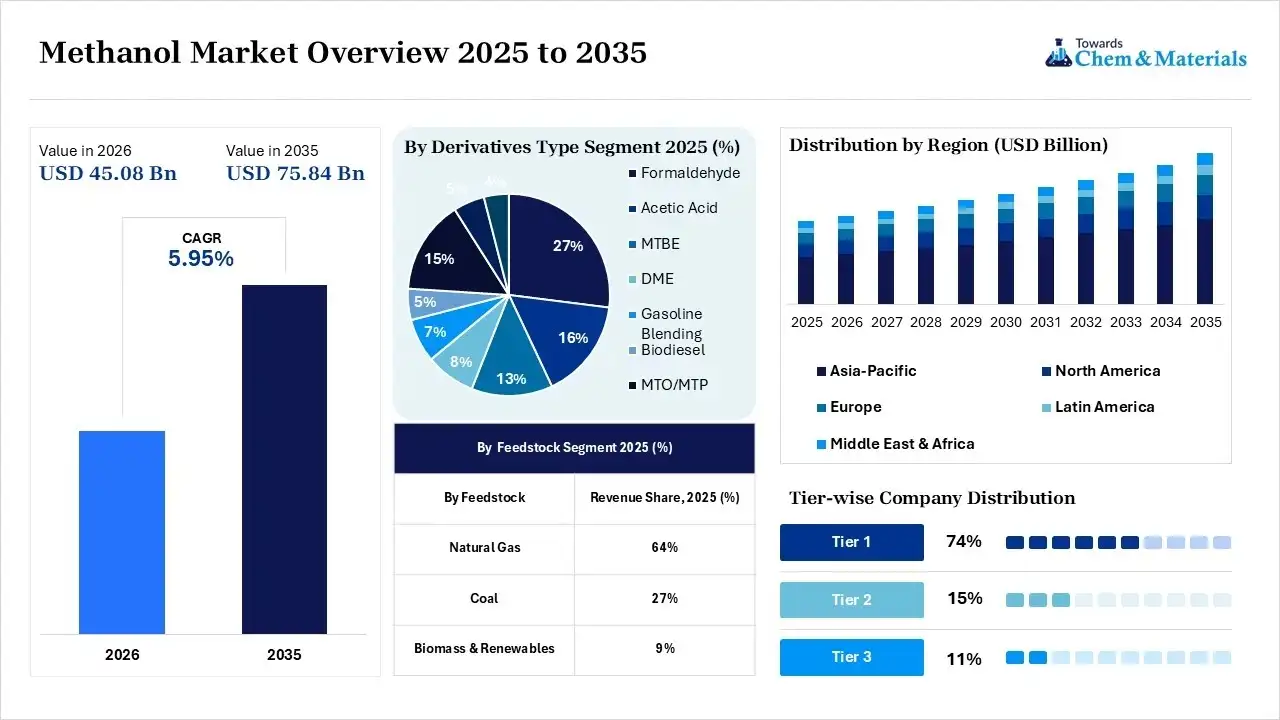

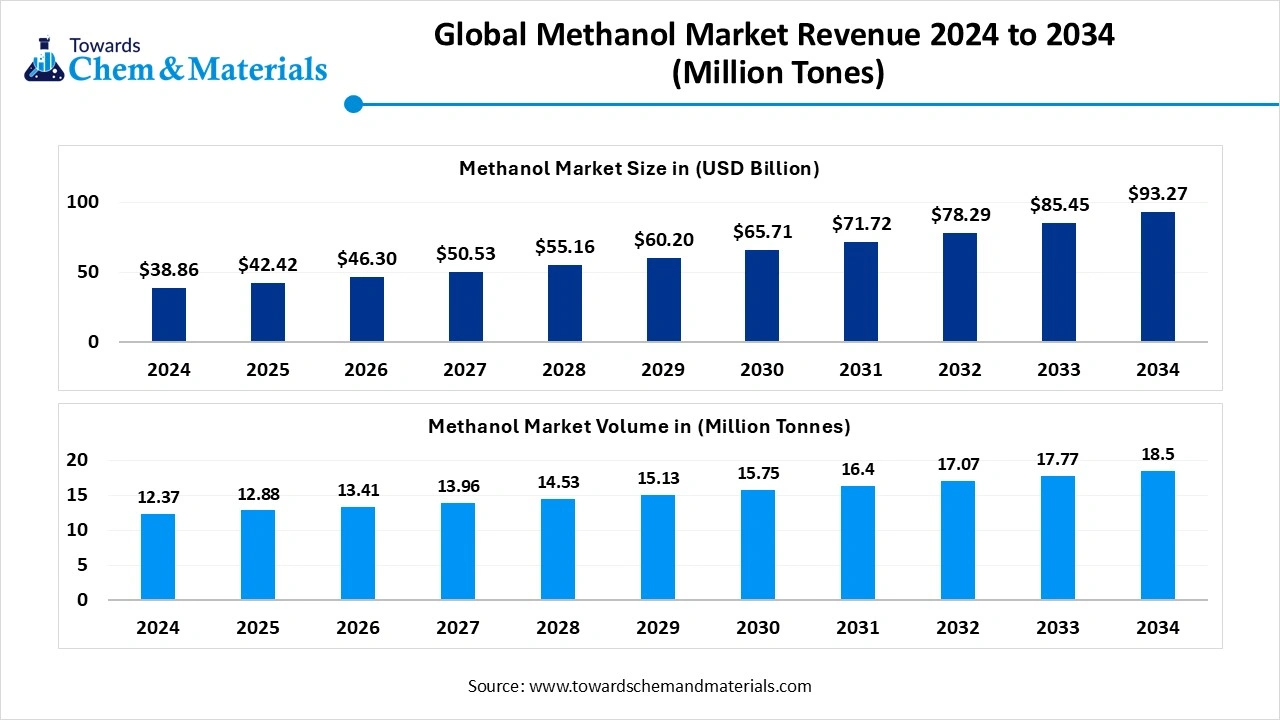

The methanol market size was valued at USD 42.55 billion in 2025, is estimated to reach USD 45.08 billion in 2026, and is projected to reach USD 75.84 billion by 2035, exhibiting a compound annual growth rate (CAGR) of 5.95% over the forecast period from 2026 to 2035.Asia Pacific dominated the methanol market with the largest revenue share of 57% in 2025 and is expected to grow at the fastest CAGR of 6.04% during the forecast period. In terms of volume, the methanol market is projected to grow from 120.45 million metric tons in 2025 to 195.27 million metric tons by 2035. growing at a CAGR of 5.95% from 2026 to 2035.Methanol becomes the center element of modern industrialization while manufacturers are actively looking for better supply chain statistics. Also, with the push for eco-friendly materials, the methanol industry is likely to create brighter industry capabilities during the forecast period.

Market Highlights

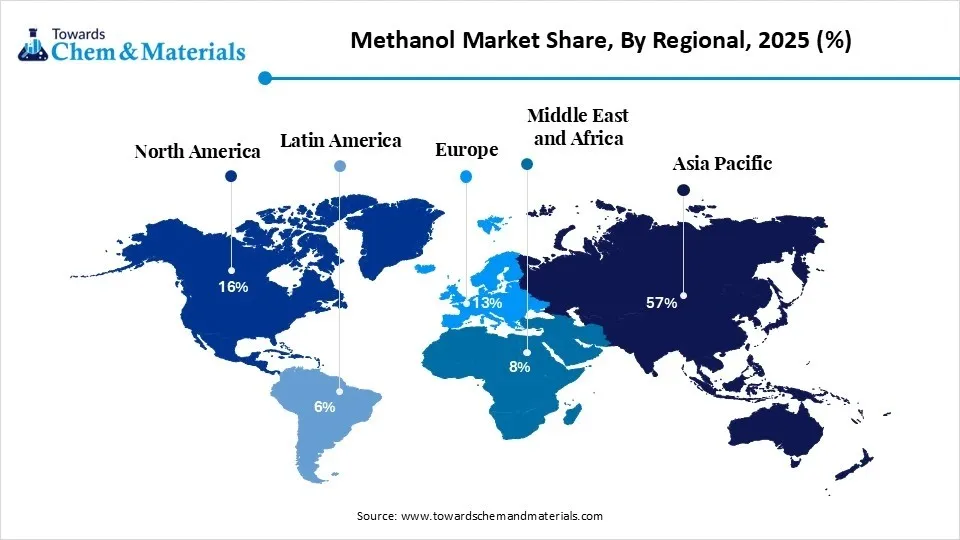

- By region, Asia Pacific dominated the market with a share of 57% in 2025, due to the it is home to some of the world's largest chemical manufacturing industries.

- By region, Europe held 13% market share in 2025 and is expected to be the fastest-growing region in the market, with a CAGR of 7.2% in the forecast period, owing to many countries investing in renewable and low-carbon methanol production.

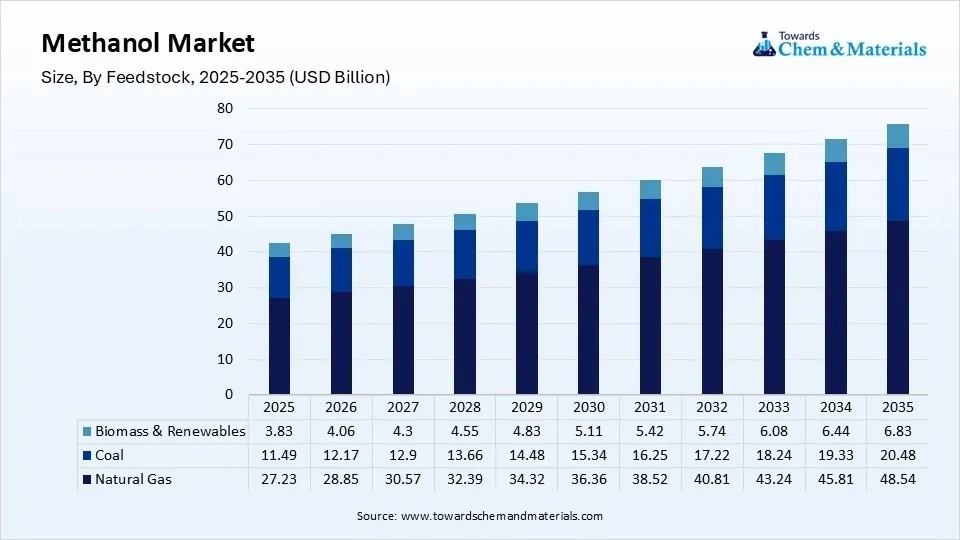

- By feedstock, the natural gas segment dominated the market with 64% share in 2025, as the increasing development of green and renewable methanol.

- By feedstock, the biomass & renewables segment held the 9% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 12.80% in the forecast period, owing to the increasing development of green and renewable methanol.

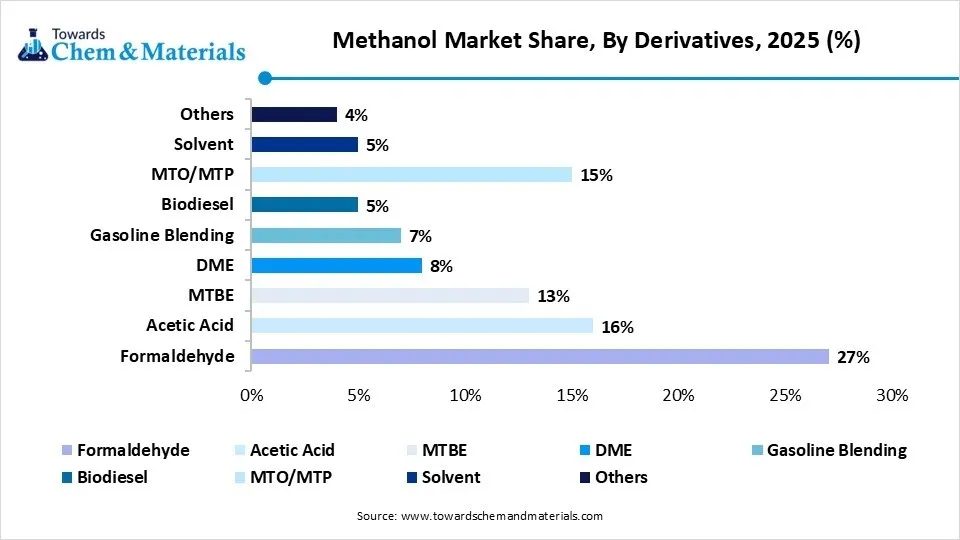

- By derivatives, the formaldehyde segment dominated the market with 27% share in 2025, owing to it being one of the most widely used products made from methanol.

- By derivatives, the MTO/MTP segment held a 15% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 8.90% in the forecast period, owing to they allow manufacturers to convert methanol into valuable petrochemical products.

- By application, the construction segment dominated the market with a 39% share in 2025, owing to many construction materials depending on methanol-based chemicals during manufacturing.

- By application, the electronics segment held the 18% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 7.10% in the forecast period, owing to demand for electronic devices across the world.

The greater involvement of methanol in major industrial sectors such as plastics, paints, adhesives, and several other chemical products has already provided huge attention to the industry in recent years. As manufacturers are actively thinking beyond hazardous chemicals usage, trying to switch cleaner fuel alternatives and energy solutions, methanol is expected to create its own presence in the upcoming period as standard research analysis. Also, the quick investments in technology innovations, international trades, and production capacity expansions have supported supply reliability.

- For instance, in June 2026, Evonik established methanol pipelines in collaboration with regional partners while sharing infrastructure information. According to the company, the main motive of this establishment is to secure long-term raw material supply in Europe, as per the published report.

(Source: www.evonik.com)

The industry is now benefiting from continuous investment in production capacity, international trade, and technological innovation. Also, several companies are expanding manufacturing facilities to meet rising global demand while strengthening supply reliability. Research activities are supporting the development of renewable and low-carbon methanol using sustainable feedstocks and carbon capture technologies.

Global Investment Flow for the Methanol Market 2026

Companies are investing in new methanol plants to meet rising demand from the chemical, fuel, and marine industries, where manufacturers are likely to invest in the latest technologies.

Manufacturers are increasing investment in low-carbon and renewable methanol projects to support global decarbonization goals, while several regional governments are actively implementing sustainable manufacturing practices.

- Strategic partnerships are helping companies strengthen feedstock supply, improve production efficiency, and expand into new international markets, which further strengthens the industry as per the industry analysis.

- For instance, in 2026, Mitsubishi Gas Chemicals expanded its investment in a green methanol project by signing an MOU with Gold Hydrogen in South Australia.(Source: www.mgc.co.jp)

Methanol Market Trends

- Focus areas for low-carbon methanol have aligned with consumer preferences, offering fresh prospects in recent years. Also, industrial manufacturers and energy producers are actively looking to reduce greenhouse gas emissions as per the recent survey.

- Expansion into the marine fuel category is resulting in stronger policy support for the manufacturers in the current period. Also, the shipping companies are actively investing and seeking methanol-powered vessels while following the international environmental requirements.

- The greater expansion of production capacities and establishing local refineries with sophisticated imports is likely to strengthen the foundation for the future sector growth during the forecast period. Also, several manufacturers are trying to reduce dependance form the regular and limited regional production.

Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 45.08 Billion/ 126.41 Million Metric Tons |

| Expected Size in 2035 | USD 75.84 Billion/ 195.27 Million Metric Tons |

| Growth Rate | CAGR of 5.95% |

| Base Year of Estimation | 2025 |

| Forecast Period | 2025-2035 |

| Dominant Region | Asia Pacific |

| Segment Covered | By Feedstock, By Derivatives, By Application, By Region |

| Key Companies Profiled | OCI Global, Celanese Corporation, BASF, Petronas Chemicals Group, Mitsubishi Gas Chemical Company, Zagros Petrochemical Company, Sinopec, Methanex Corporation, Proaman, SABIC |

Sustainable Production with Technology

The methanol industry is heavily moving from conventional natural gas-based production toward cleaner and more sustainable manufacturing technologies. Also, the companies are investing in renewable methanol production using biomass, captured carbon dioxide, and green hydrogen. Modern process technologies are also improving production efficiency while reducing emissions and energy consumption. Digital monitoring systems and advanced process control are helping manufacturers improve plant performance and operational reliability.

Supply Chain Analysis of the Methanol Market

Production & Processing

- Making standard methanol looks like cooking compressed gases over a metallic catalyst. Factories blast natural gas with white-hot steam inside heavy steel reactors to smash the molecules into a blended vapor called syngas.

- They pump this vapor over specialized copper plates under immense pressure, forcing the carbon and hydrogen to lock together and condense into clear, liquid alcohol.

- Methanex Corporation: Methanex Corporation stands as the world's absolute largest producer and distributor of commercial methanol.

- Key players: SABIC, Proman, OCI Global, Yanzhou Coal Mining Company, and Celanese Corporation

Quality Testing and Certification

- Testing industrial methanol means confirming the chemical is totally pure, completely dry, and perfectly transparent. Techs shoot chemical samples through specialized laboratory sensors to track down even tiny drops of hidden water or rogue organic oils that could ruin an industrial batch.

- Independent testing networks then verify these metrics against global baselines, stamping the cargo with a formal safety seal before it ever loads onto cargo ships.

- SGS: SGS acts as a premier global inspection giant for the chemical commodities sector. Their field technicians operate advanced testing laboratories directly inside major shipping hubs to independently certify that bulk methanol shipments are completely free of contaminants.

- Key agencies: ASTM International, International Methanol Producers and Consumers Association (IMPCA), and ISO (International Organization for Standardization)

Distribution to Industrial Users

- Moving bulk methanol to industrial plants relies on a tight network of specialized chemical tankers, railcars, and dedicated pipelines.

- Because the liquid alcohol catches fire easily and burns with an invisible flame, distributors utilize highly secure, sealed steel containers. Logistics managers track these shipments continuously to ensure seamless, safe factory delivery.

- Stolt-Nielsen: Stolt-Nielsen is a premier global logistics leader specializing in transporting hazardous liquid chemicals. They operate a massive fleet of deep-sea parcel tankers and thousands of specialized tank containers to safely move methanol across worldwide shipping lanes.

- Key players: Brenntag, Univar Solutions, Helm AG, and Odfjell

Methanol Market Regulatory Landscape: Regulations

| Country Region | Regulatory Body | Key Regulations | Focus Areas |

| United States | U.S. Environmental Protection Agency (EPA) | Clean Air Act (CAA) Amendments [Section 112(b)]: Classifies industrial methanol directly as a Hazardous Air Pollutant (HAP). | Industrial Leak Containment: Mandating the use of heavy-duty, double-walled storage tanks and advanced optical sensors to instantly flag hidden liquid or vapor leaks at manufacturing facilities. |

| Europe | European Chemicals Agency (ECHA) | REACH Regulation [(EC) No 1907/2006] Annex XVII Entry 69: Imposes a strict consumer ban on the chemical. | Maritime Carbon Rules: Driving the shipping industry to swap dirty heavy fuel oil for certified green e-methanol to hit aggressive decarbonisation targets set by regional maritime laws. |

| China | Ministry of Emergency Management (MEM | Regulations on the Safe Management of Hazardous Chemicals [Decree No. 591] Chapter 2: Places methanol on China's Catalog of Hazardous Chemicals. | Coal-to-Chemical Security: Imposing tight environmental checks on inland mega-refineries that bake raw coal into syngas to ensure they do not pollute local regional river basins with chemical wastewater. |

Methanol Market Dynamics

Driver

Essential Feedstock Rise

The industries that depend on methanol as an important raw material for daily production are actively driving the industry demand in recent years. It is widely used to manufacture chemicals, plastics, paints, adhesives, fuels, and several industrial products. In the current period, demand is also increasing from the energy sector as methanol gains attention as a cleaner fuel option. Many manufacturers are expanding production to meet rising industrial requirements while improving supply reliability. Furthermore, growing industrial activity in developing countries is creating additional demand for methanol.

Restraint

Price Uncertainty Pressure

Frequent changes in raw material prices are expected to hinder industry growth during the forecast period. Natural gas, coal, and other feedstocks used for methanol production often experience price fluctuations because of supply conditions, geopolitical events, and energy market changes. When production costs increase, manufacturers may face lower profit margins or higher product prices. Smaller producers are affected more because they have limited flexibility to absorb rising costs.

Opportunity

Green Innovation Fuels Industry Momentum

The increasing development of green and renewable methanol is anticipated to create exceptional opportunities in the industry during the projected time period. Also, many companies are investing in cleaner production methods that use biomass, captured carbon dioxide, and green hydrogen instead of traditional fossil-based feedstocks. These projects are attracting attention from industries that want to reduce carbon emissions while maintaining reliable fuel and chemical supplies. Shipping companies, energy producers, and industrial manufacturers are showing growing interest in renewable methanol.

Segmental Insights

Feedstock Insights

The natural gas segment dominated the market with 64% share in 2025, as the increasing development of green and renewable methanol. Many companies are investing in cleaner production methods that use biomass, captured carbon dioxide, and green hydrogen instead of traditional fossil-based feedstocks. These projects are attracting attention from industries that want to reduce carbon emissions while maintaining reliable fuel and chemical supplies. Shipping companies, energy producers, and industrial manufacturers are showing growing interest in renewable methanol.

")

The biomass & renewables segment held a 9% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 12.80% in the forecast period, owing to industries working to reduce their environmental impact. Companies are looking for cleaner raw materials that support low-carbon manufacturing while meeting future sustainability targets. Renewable feedstocks also help producers reduce dependence on fossil resources and create products with a lower carbon footprint.

Methanol Market Share, By Feedstock, 2025 (%)

| By Feedstock | Revenue Share, 2025 (%) |

| Natural Gas | 64% |

| Coal | 27% |

| Biomass & Renewables | 9% |

Derivatives Insights

The formaldehydes segment dominated the market with 27% share in 2025, owing to its being one of the most widely used products made from methanol. It is an essential material for manufacturing wood panels, furniture, construction materials, insulation products, automotive components, and many household goods. Since these industries produce goods in very large quantities throughout the year, formaldehyde demand remains consistently strong.

")

The MTO/MTP segment held a 15% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 8.90% in the forecast period, owing to they allow manufacturers to convert methanol into valuable petrochemical products. Demand for plastics and packaging materials continues to increase worldwide, encouraging investment in these advanced production routes. Many chemical producers are expanding MTO and MTP projects to improve raw material flexibility while supporting growing petrochemical demand.

Methanol Market Share, By Derivatives, 2025 (%)

| By Derivatives | Revenue Share, 2025 (%) |

| Formaldehyde | 27% |

| Acetic Acid | 16% |

| MTBE | 13% |

| DME | 8% |

| Gasoline Blending | 7% |

| Biodiesel | 5% |

| MTO/MTP | 15% |

| Solvent | 5% |

| Others | 4% |

Application Insights

The construction segment dominated the market with 39% share in 2025, owing to many construction materials depending on methanol-based chemicals during manufacturing. Products such as plywood, laminates, insulation materials, paints, coatings, adhesives, and engineered wood all require methanol derivatives. As urban development and infrastructure projects continue worldwide, demand for these building materials remains high. Construction activities in both developed and developing countries also support continuous consumption of methanol-based products.

The electronics segment held the 18% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 7.10% in the forecast period, owing to demand for electronic devices across the world. Methanol and its derivatives are used during the production of electronic components, specialty materials, and semiconductor-related products. As technologies such as artificial intelligence, electric vehicles, and advanced communication systems expand, manufacturers are increasing investment in electronics production. This growth is creating additional demand for methanol-based chemicals used in precision manufacturing.

Methanol Market Share, By Application, 2025 (%)

| By Application | Revenue Share, 2025 (%) |

| Construction | 39% |

| Automotive | 26% |

| Electronics | 18% |

| Others | 17% |

Regional Analysis

How did Asia Pacific Dominated the Methanol Market in 2025?

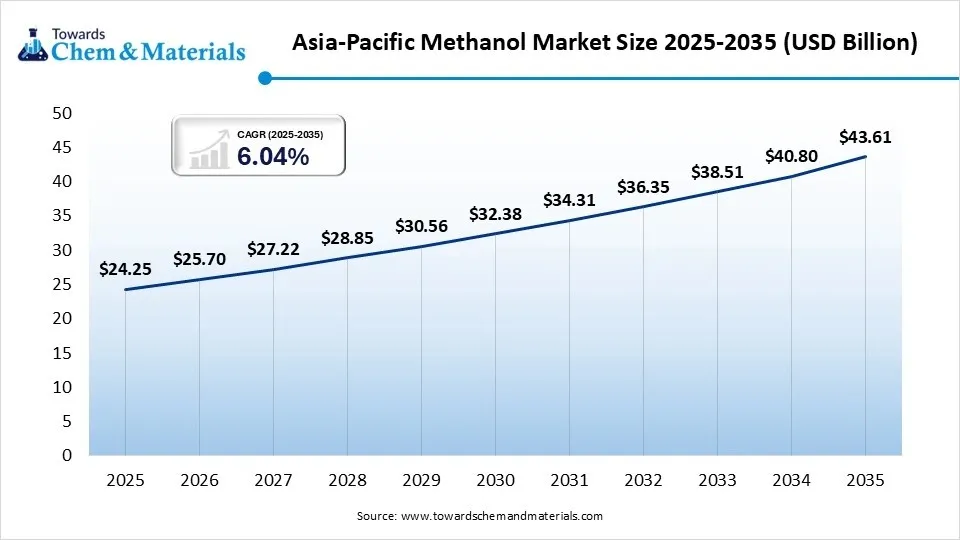

The Asia Pacific methanol market size was estimated at USD 24.25 billion in 2025 and is projected to reach USD 43.61 billion by 2035, growing at a CAGR of 6.04% from 2026 to 2035. Asia Pacific dominated the market with a share of 57% in 2025, due to the it is home to some of the world's largest chemical manufacturing industries. Many countries in the region produce methanol-based products on a large scale to meet both domestic and international demand. Rapid industrial growth, expanding manufacturing activities, and increasing investment in chemical production continue to support methanol consumption.

")

China

- The country has invested heavily in methanol production and downstream chemical manufacturing, while many chemical companies are expanding facilities that convert methanol into valuable industrial products, helping meet growing domestic demand.

- The country is also increasing the use of methanol in fuel applications and advanced chemical processes to support industrial development.

Japan

- Companies in Japan are increasing research on low-carbon methanol while exploring its use in shipping and sustainable fuel projects, while the country's strong specialty chemical industry is also creating demand for high-quality methanol products used in advanced manufacturing.

- The collaboration between industrial companies to develop environmentally friendly production methods in the country nowadays.

Methanol Market Evaluation in Europe

The Europe methanol market size was estimated at USD 5.53 billion in 2025 and is projected to reach USD 10.24 billion by 2035, growing at a CAGR of 6.35% from 2026 to 2035. Europe held 13% market share in 2025 and is expected to be the fastest-growing region in the market, with a CAGR of 7.2% in the forecast period, owing to many countries investing in renewable and low-carbon methanol production. The region is placing greater emphasis on reducing industrial emissions while encouraging the development of cleaner fuels for transportation and manufacturing. Many companies are also building partnerships to produce sustainable methanol using renewable resources and captured carbon dioxide. This transition toward cleaner production methods is creating new investment opportunities throughout Europe.

Germany

- Germany is strengthening its methanol industry through investment in green technologies and industrial innovation, while many producers are exploring renewable methanol for use in chemical manufacturing and sustainable energy projects.

- Also, the country's advanced engineering sector is supporting the development of modern production technologies that improve efficiency while lowering emissions.

Italy

- Major companies are exploring methanol as an alternative fuel while improving manufacturing processes that depend on methanol-based chemicals, while the country's ports and shipping activities are also encouraging discussions around cleaner marine fuels for future operations.

- Chemical manufacturers are modernizing production facilities to improve efficiency and reduce environmental impact in the country nowadays.

North America Enzyme Industry Conditions

The North America methanol market size was estimated at USD 6.81 billion in 2025 and is projected to reach USD 12.51 billion by 2035, growing at a CAGR of 6.27% from 2026 to 2035. North America held a 16% market share in 2025, owing to industries increasing investment in advanced chemical manufacturing and cleaner fuel technologies. Many companies are expanding methanol production while exploring new industrial applications beyond traditional chemical processing. Growing interest in carbon reduction is encouraging research into renewable methanol and carbon capture technologies. The region also benefits from a reliable natural gas supply, supporting competitive methanol production.

United States

- The United States is expanding its methanol market through increasing investment in low-emission fuels and modern chemical production, while manufacturers are developing projects that support renewable methanol while improving production efficiency at existing facilities.

- Also, the country's shipping, energy, and industrial sectors are also exploring methanol as an alternative fuel for future operations.

Canada

- Canada is bolstering its methanol market by making greater use of its natural resource base while investing in cleaner industrial development, & producers are evaluating renewable methanol projects that use sustainable feedstocks and lower-carbon production methods.

- Also, the country's focus on clean energy and environmental innovation is encouraging investment in advanced fuel technologies.

Methanol Market Survey in Latin America

The Latin America methanol market size was estimated at USD 2.55 billion in 2025 and is projected to reach USD 4.93 billion by 2035, growing at a CAGR of 6.81% from 2026 to 2035. Latin America held a 6% market share in 2025 as industrial production continues to expand across several countries. Manufacturers are increasing the production of paints, plastics, construction materials, and chemical products that depend on methanol and its derivatives. At the same time, governments and private companies are investing in industrial development to improve manufacturing capacity and support economic growth.

")

Brazil

- Brazil is leading the regional market because its large manufacturing and agricultural industries create strong demand for methanol-based products, while chemical producers are increasing the use of methanol to manufacture resins, adhesives, and industrial chemicals used across different sectors.

- The country is also expanding industrial production to support growing domestic demand for consumer and construction products.

Argentina

- The country's chemical sector is improving production efficiency and expanding downstream manufacturing activities, while companies are increasing the use of methanol in industrial processing and improving supply chains for chemical products.

- Also, the growing demand for methanol-based materials used in automotive components, coatings, and industrial manufacturing in Argentina in the current period.

Middle East and Africa Methanol Sector Observation

The Middle East and Africa methanol market size was estimated at USD 3.40 billion in 2025 and is projected to reach USD 6.45 billion by 2035, growing at a CAGR of 6.61% from 2026 to 2035. The Middle East and Africa held an 8% market share in 2025, as several countries have abundant natural gas resources that support competitive methanol production. Many producers are expanding manufacturing capacity while increasing exports to international markets. Governments are also encouraging industrial diversification by investing in downstream chemical industries that use methanol as a key raw material. At the same time, growing infrastructure development is increasing regional demand for methanol-based construction materials.

Saudi Arabia

- The country continues strengthening its methanol industry by expanding its petrochemical sector and increasing production of value-added chemical products, and many manufacturers are investing in integrated industrial projects that convert methanol into higher-value downstream products.

- The country is also focusing on industrial diversification by reducing dependence on crude oil exports and expanding chemical manufacturing.

UAE

- The UAE is expanding its methanol market by increasing investment in modern chemical manufacturing and industrial infrastructure, while companies are exploring new opportunities to improve production efficiency while supporting future energy transition projects.

- Also, the growing interest in sustainable industrial technologies that improve resource efficiency in the country.

Recent Development

- In May 2026, Thermax has created a strategic collaboration with Ankur Scientific regarding the establishment of the green methanol plant in India. Also, the capacity of these future plants is likely to be 18000 tons of methanol production per year, as per the published report.(Source: energy.economictimes.indiatimes.com)

Competitive Analysis

The market is highly competitive because companies are focusing on expanding production capacity, improving manufacturing efficiency, and developing lower-carbon methanol solutions. Instead of competing only through production volume, many manufacturers are investing in technology, sustainability, and global supply chain expansion, as per the recent industry survey.

Methanex Corporation, which continues expanding its global methanol business through production optimization, supply reliability, and low-carbon methanol initiatives, with the introduction of bunkering operations. The company is actively investing in projects that support future sustainable methanol demand while strengthening its position in international markets. (Source: www.methanex.com) https://www.methanex.com/news/release/methanex-launches-global-methanol-bunkering-operations-with-strategic-partnerships-in-the-ara-region-and-south-korea/

Top Vendors in the Methanol Market & Their Offerings:

| Company | Company Type/Position | Major Headquarters | Geographic Presence | Offerings | Key Strength |

| Methanex Corporation | Global Production Leader | Vancouver, Canada | Massively widespread across North America, South America, Europe, the Middle East, and the Asia-Pacific region. | Millions of tons of commercial-grade liquid methanol annually, along with a growing supply of low-carbon bio-methanol. | Total supply chain ownership, backed by a massive, dedicated fleet of transoceanic chemical shipping vessels. |

| Proaman | Integrated Energy & Petrochemical Giant | Wollerau, Switzerland | Highly concentrated production hubs in Trinidad and Tobago, the United States, and Oman, with global export routes. | High-purity industrial methanol, green methanol variants, fertilizer products, and melamine. | Deep vertical integration, managing everything from natural gas extraction to processing and downstream transport. |

| SABIC | Diversified Chemical Heavyweight | Riyadh, Saudi Arabia | Strong distribution networks across the Middle East, Europe, the Americas, and major manufacturing hubs in Asia. | Bulk chemical building blocks including methanol, advanced polymers, industrial plastics, and agri-nutrients. | Vast financial backing and low-cost access to regional raw natural gas feedstocks for highly competitive manufacturing. |

- Proman is currently focusing on strengthening its position in the global methanol industry by expanding its production capabilities and supporting the transition toward lower-carbon methanol investments.(Source: www.guardian.co.tt)

Other Key Players

- OCI Global

- Celanese Corporation

- BASF

- Petronas Chemicals Group

- Mitsubishi Gas Chemical Company

- Zagros Petrochemical Company

- Sinopec

Segments Covered in the Report

By Feedstock

- Natural Gas

- Conventional Natural Gas

- Associated Gas

- Shale Gas

- Coal

- Bituminous Coal

- Lignite Coal

- Biomass & Renewables

- Biomass Gasification

- Municipal Solid Waste

- Renewable Hydrogen + Captured CO₂

- Biomethane

By Derivatives

- Formaldehyde

- Urea Formaldehyde Resins

- Phenol Formaldehyde Resins

- Melamine Formaldehyde Resins

- Acetic Acid

- Vinyl Acetate Monomer

- Purified Terephthalic Acid

- Acetate Esters

- MTBE

- DME

- LPG Blending

- Clean Cooking Fuel

- Gasoline Blending

- Biodiesel

- MTO/MTP

- Ethylene Production

- Propylene Production

- Solvent

- Others

- Methylamines

- Chloromethanes

- Dimethyl Sulfate

By Application

- Construction

- Insulation Materials

- Adhesives & Resins

- Paints & Coatings

- Automotive

- Fuel Applications

- Engineering Plastics

- Coatings

- Electronics

- Semiconductor Chemicals

- Electronic Resins

- Display Materials

- Others

- Pharmaceuticals

- Agriculture

- Marine

- Textile

By Region

- North America

- Europe

- Asia Pacific

- Middle East & Africa

- Latin America

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

Tags

FAQ's

Select User License to Buy

Figures (6)