Content

What is the Martensitic Stainless Steels Market Size and Share?

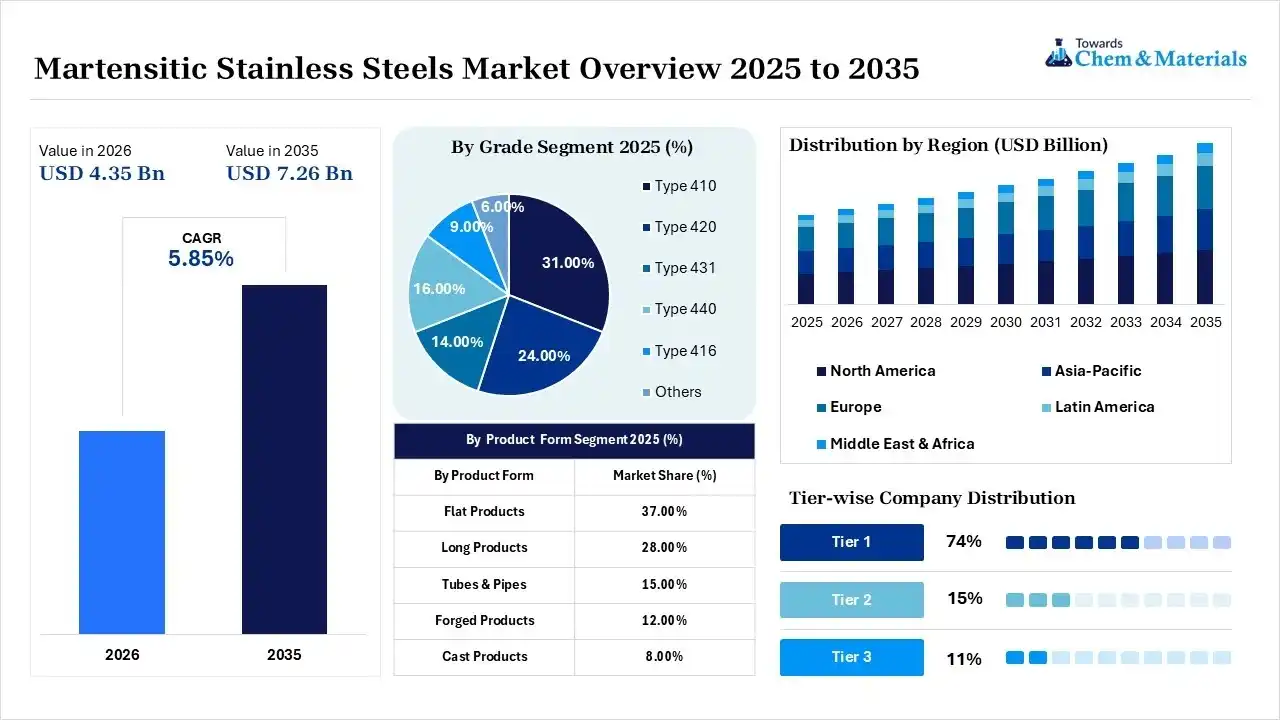

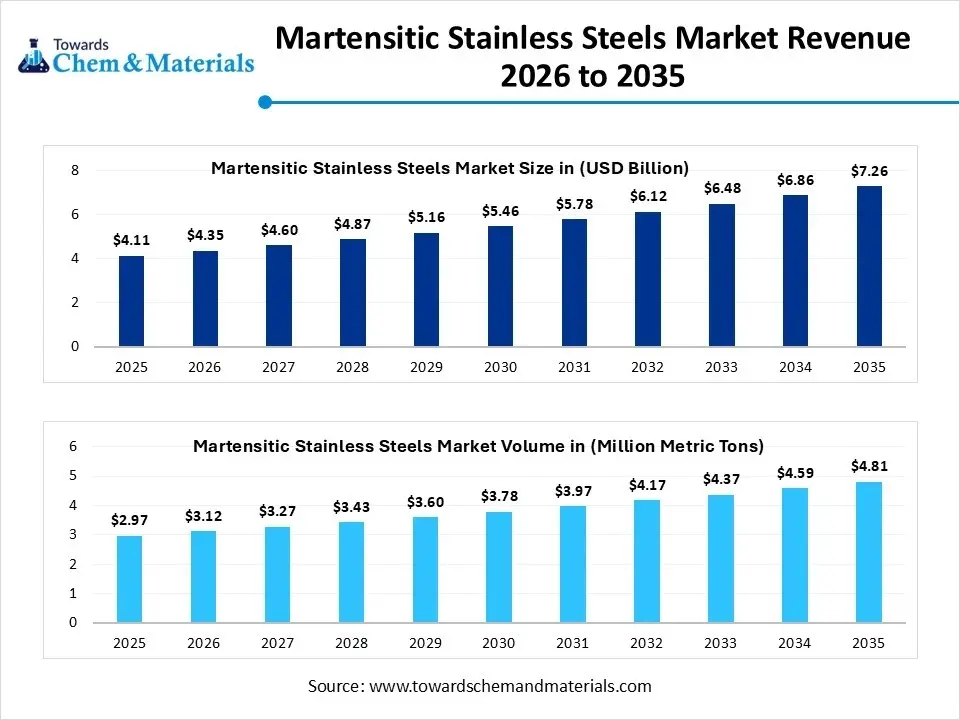

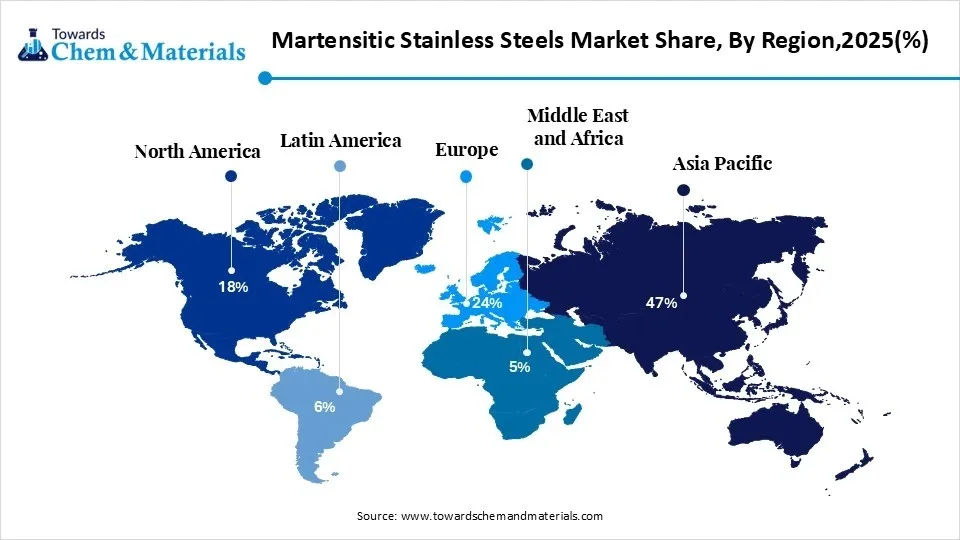

The global martensitic stainless steels market size was valued at USD 4.11 billion in 2025, is estimated to reach USD 4.35 billion in 2026, and is projected to reach USD 7.26 billion by 2035, exhibiting a compound annual growth rate (CAGR) of 5.85% over the forecast period from 2026 to 2035.Asia Pacific dominated the martensitic stainless steels market with the largest revenue share of 47% in 2025 and is expected to grow at the fastest CAGR of 5.98%during the forecast period. In terms of volume, the martensitic stainless steels industry is projected to grow from 2.97 million metric tons in 2025 to 4.81 million metric tons by 2035. growing at a CAGR of 4.95% from 2026 to 2035.The applications in automotive, oil and gas, architecture, building and construction, and aerospace, due to its high mechanical and corrosion resistance, are the core advantages of this product. The key collaborations between companies such as JFE Steel and local partners, POSCO and Nippon Steel, are primarily aimed at developing advanced recycled steel for its applications. This expansion and development are expected to create a strong presence of the product in the upcoming time.

Market Highlights

- By region, Asia Pacific dominated the market with a share of 47% in 2025, due to expanding manufacturing hubs in the region.

- By region, North America held 18% market share in 2025 and is expected to experience the fastest growth with a CAGR of 6.5% in the forecast period. The growing oil and gas investment in the region drives growth.

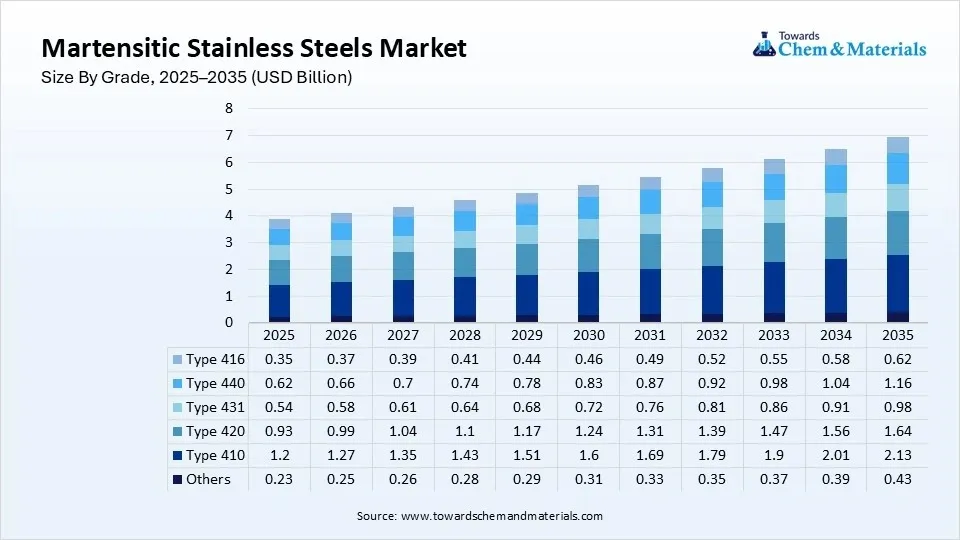

- By grade, the type 410 segment dominated the market with a 31% share in 2025. Widely used across industrial machinery.

- By grade, the type 420 segment held 24% market share in 2025 and is expected to have the fastest growth with a CAGR of 6.60% in the forecast period. Demand rises for surgical instruments.

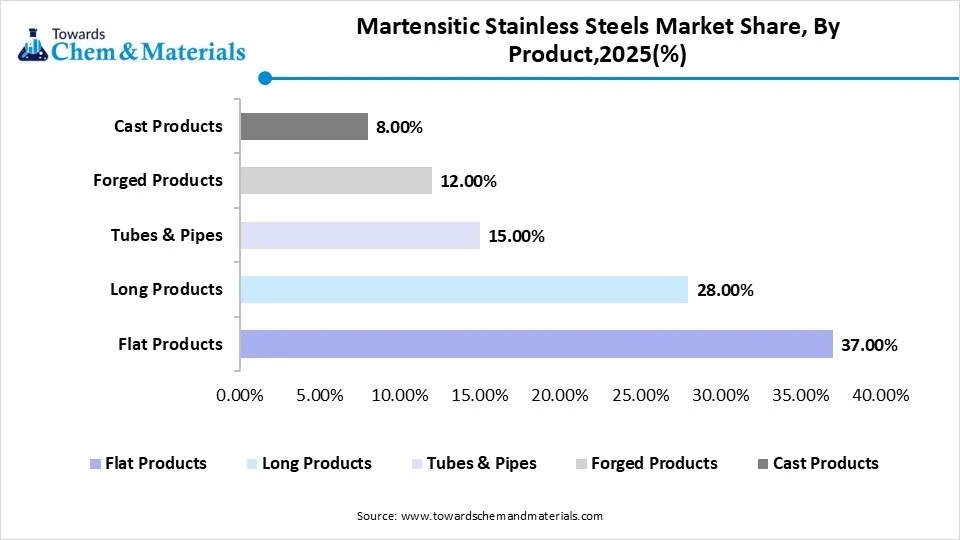

- By product form, the flat products segment dominated the market with a 37% share in 2025. Strong demand from fabrication industries.

- By product form, the tubes and pipes segment held 15% market share in 2025 and is expected to have the fastest growth with a CAGR of 6.4% in the forecast period. Oil & gas investments increase.

- By heat treatment, the Hardened & Tempered segment dominated the market with a 39% share in 2025. Provides balanced toughness and hardness.

- By heat treatment, the Quenched & Tempered segment held 21% market share in 2025 and is expected to have the fastest growth with a CAGR of 6.3% in the forecast period. Heavy-duty equipment adoption rises.

- By manufacturing process, the hot-rolled segment dominated the market with a 35% share in 2025. Cost-efficient production supports volume demand.

- By manufacturing process, the cold-rolled segment held 26% market share in 2025 and is expected to have the fastest growth with a CAGR of 6.4% in the forecast period. Precision industries require a superior finish.

- By end use industry, the automotive segment dominated the market with a 27% share in 2025. Engine efficiency improvements drive adoption

- By end use industry, the aerospace segment held 11% market share in 2025 and is expected to have the fastest growth with a CAGR of 6.8% in the forecast period. Aircraft production expands globally.

- By distribution channel, the direct sales segment dominated the market with a 46% share in 2025. Large industrial contracts drive procurement.

- By distribution channel, the online sales segment held 6% market share in 2025 and is expected to have the fastest growth with a CAGR of 8.2% in the forecast period. Digital procurement platforms expand.

The martensitic stainless steels are magnetic steels that primarily consist of 11.5% to 18% chromium and 0.1 to 1.2% carbon, which helps make hardenable steel. The chromium and carbon contents help in balancing the structure of the stainless steel. It is preferred by most of the sectors due to its advantageous properties, such as its exceptional tensile strength, wear resistance, and durability, which are used and helpful in making materials for turbine parts, tools, and surgical instruments. Commonly used grades are type 410, type 420, type 431, type 440A, type 440B, and type 440C. The application of martensitic stainless steels depends on the carbon content and is used for its corrosion resistance, wear resistance, and high-strength properties.

- For instance, the recent launch of the UGIMA®-X third-generation high-performance machinable stainless steels by the Swiss Steel Group introduces newly optimized martensitic grades designed for demanding industrial applications. The key martensitic grades launched include UGIMA-X 4021 and UGIMA-X 4028

(Source: swisssteel-group.com)

They are used for their mechanical properties, up to about 0.4% C in applications such as valves, shafts, and pumps, and above 0.4 C, it is used for their wear resistance in surgical blades, nozzles, cutlery, and plastic injection molds, which increases the demand for the product, helping in expanding the business. Martensitic stainless steels help in providing a low-maintenance product life, which helps manufacturers due to their profitable recycling rate, which aligns with sustainability initiatives due to rising environmental concerns, which attracts manufacturers due to growing awareness.

The main application lies in 3 major sectors, that is, aerospace, power generation, and oil and gas recovery, due to its application, which propels the growth and expansion of the market. In aerospace, it is used for its high strength, reliability, stiffness, and corrosion resistance. The ESP process in this helps in achieving the top performance level. In power generation, creep-resistant materials in the martensitic stainless steels allow steam power to operate at 650°C, which is important in electricity produced by steam. In oil and gas recovery, used for moderate temperatures and CO2 and H2S pressure, new grades are more resistant to stress corrosion cracking and sulfide stress cracking, which help bridge the gap between martensitic and the expensive high corrosion-resistant duplex grades.

Global Investment Flow for Martensitic Stainless Steels Market 2026

The growing investments by major companies like Outokumpu (Finland), Sandvik (Sweden), and Carpenter Technology (US), and the government's domestic production and expansion through policies like the Production-Linked Incentive (PLI) Scheme are key investors and promising leads in the manufacturing of products.

- India's leading stainless-steel manufacturer, Jindal Stainless, operates 16 stainless steel manufacturing and production units in India, Spain, and Indonesia. The company's product line makes it’s a largest facility in India. The sustainability and green energy focus of the company makes it a valuable asset.(Source: www.jindalstainless.com)

- Shyam Metalics and Energy plans to pledge an additional ₹2,700-crore investment focusing heavily on specialty and value-added steel products, aimed at driving import substitution by 2029.(Source: infra.economictimes.indiatimes.com)

- Jindal Stainless Limited is planning a massive ₹40,000-crore investment to set up a new facility in Maharashtra. Supported by the state government, this facility will focus on specialized grades including martensitic stainless steels for critical applications like defense, mobility, and nuclear energy.(Source: www.manufacturingtodayindia.com)

Recent Market Growth Trends:

- The growing demand from the automotive sector due to its lightweight application, which helps in maintaining fuel efficiency, and demand for martensitic stainless steels in battery and powertrain components due to the rapid shift towards electric vehicles is a growing trend.

- The need for components capable of undergoing and handling extreme stress and temperature in the aerospace and defence sector, especially in the major hubs like Japan and the US demand for heat resistant and precipitation-hardened martensitic grade steels.

- The growing industrial and medical expansion due to its applications and properties, which are ideal for precision tools, turbine blades, and cutting instruments due to its efficient hardness, which makes it ideal for use.

Report Scope

| Report Attributes | Details |

| Market Size in 2026 | USD 4.35 Biilion/ 3.12 Million Metric Tons |

| Market Size by 2035 | USD 7.26 Billion/ 4.81 Million Metric Tons |

| Growth Rate from 2026 to 2035 | CAGR 5.85% |

| Base Year of Estimation | 2025 |

| Forecast Period | 2026 - 2035 |

| Dominant Region | Asia Pacific |

| Segment Covered | By Grade, By Product Form, By Heat Treatment,By Manufacturing Process, By End-use Industry, By Distribution Channel, By Region |

| Key Profiled Companies | Tata Steel Group, China Baowu Steel Group, ThyssenKrupp, Outokumpu, Jindal Stainless, Aperam, ATI (Allegheny Technologies), Sandvik AB, Cleveland-Cliffs (AK Steel), Valbruna, Tsingshan Holding Group, Dongkuk Steel Mill, HBIS Group, Gerdau, Voestalpine |

Martensitic Stainless Steels Through AI: Reactive Manufacturing To Data-Driven Manufacturing

The integration of AI in the production of martensitic stainless steels is a very efficient and productive way for the manufacturing of steel, which shifts production from reactive and traditional manufacturing to data-driven and precision engineering. This key technological shift, which includes AI, is microstructure and property prediction, digital twins for heat treatment, AI-enabled defect detection, predictive maintenance, and optimized additive manufacturing, which helps in increasing the yield and also helps in efficiently lowering the carbon emissions in high-end and high-performance applications in major sectors, which propels the growth and demand for the market, supporting expansion.

Supply Chain Analysis of Martensitic Stainless Steels Market

Production and Processing

- The martensitic stainless steels are produced through melting and casting, and the primary process includes hot working and cold working.

- Signature core processing that includes heat treatment includes austenitizing, quenching, and tempering. These techniques help in the production of high-strength and hard products.

- Nippon Steel Corporation is the largest steel producer in Japan, supplying high-performance steel and advanced metals for various sectors like energy, automotive, and electronics. They supply steel like Prostruct building materials for industrial plants.

- Key players: Nippon Steel Corporation, POSCO, ArcelorMittal, JFE Steel Corporation, Baosteel Group, and Outokumpu.

Quality Testing and Certification

- The martensitic stainless steels require standards to verify specific mechanical strength, which are evaluated through various testing standards as per ASTM E112 and ASTM E8. Certifications and standards that are mandatory are material test certification, industrial standards, issued per EN 10204.

- POSCO produces martensitic stainless steels, which are high carbon and chromium, as per the grade and standards, and have superior hardness, wear and tear resistance, and corrosion resistance. It is known for manufacturing durable and high-end products, which increases the demand.

- Key players: ASTM International and UL Solutions, AEME, ISO, BIS Certification

Distribution to Industrial Users

- Martensitic stainless steels are extensively used due to their properties of high strength, wear resistance, and hardness in industries like aerospace, automotive, medical, oil and gas, power generation, and food processing for components.

- Outokumpu supplies martensitic and precipitation-hardening (PH) stainless steels primarily under its Dura product range. Outokumpu provides these materials in various flat-rolled and long product forms, optimized for different heat-treatment conditions and machinability requirements.

- Key players: SAIL, Ambica Steels Limited, and Dipti Metal Industries.

Martensitic stainless steels Regulatory Landscape

| Country / Region | Regulatory Body | Key Regulations | Focus Areas | Notable Notes |

| United States | American Society for Testing and Materials; Occupational Safety and Health Administration | ASTM Stainless Steel Standards; OSHA Workplace Safety Standards | Material quality, industrial safety | The U.S. promotes the use of martensitic stainless steels in aerospace, automotive, medical, and energy applications requiring high strength and wear resistance. |

| European Union | European Committee for Standardization; European Chemicals Agency | EN Stainless Steel Standards; REACH Regulation | Product quality, sustainable manufacturing | Europe emphasizes high-performance stainless steels for engineering, tooling, and industrial equipment while ensuring environmental compliance. |

| China | Ministry of Industry and Information Technology; State Administration for Market Regulation | GB/T Stainless Steel Standards; Environmental Protection Law | Advanced steel production, industrial modernization | China is expanding martensitic stainless steel production to support automotive, machinery, and infrastructure industries. |

| India | Bureau of Indian Standards, Ministry of Steel | IS Stainless Steel Standards; National Steel Policy | Specialty steel production, manufacturing quality | India is strengthening domestic production of martensitic stainless steels for engineering, defense, and industrial applications. |

| Japan | Japanese Industrial Standards Committee; Ministry of Economy, Trade and Industry | JIS Stainless Steel Standards | High-performance alloys, precision manufacturing | Japan focuses on premium martensitic stainless steels for automotive, aerospace, and precision engineering applications. |

| Germany | German Institute for Standardization; Federal Ministry for Economic Affairs and Energy | DIN Stainless Steel Standards; REACH Compliance | Advanced metallurgy, lightweight engineering | Germany is a leading producer of high-quality martensitic stainless steels for automotive, industrial machinery, and aerospace sectors. |

What are the Key Product Types of Martensitic stainless steels?

The martensitic stainless steels are magnetic alloys and highly hardenable products that are known for their exceptional strength and wear resistance. The products offered are made up of compositions consisting of iron-chromium-carbon steels, creep-resisting grades, nickel-bearing grades, and precipitation-hardening steels. The key product grades offered are:

Iron-Chromium-Carbon (Fe-Cr-C) Steels: Type 410, Type 420, Type 440 (ABC), used for fasteners, pins, and machine parts, surgical tools, dental instruments, cutlery, knife blades, ball bearings, and valve components. They are the most widely used martensitic steels due to their offering of great strength and wear resistance, which relies on the carbon content, making them hard during heat treatment.

Nickel-Bearing Grades: Type 431, Type 248SV (EN 1.4418) used in e hardware, shafts, and aircraft fasteners for its metal toughness, which absorbs energy without breaking, corrosion resistance, and also the manufacturers substitute the carbon and nickel and add molybdenum, which is a major factor in the production.

Precipitation Hardening (PH) Steels: 17-4 PH (Type 630) is used in aerospace hardware, turbine blades, and nuclear components. They generally use copper, aluminum, or titanium; the precipitate is formed by heating and forms a microscopic precipitate which intact the structure, matching strength and toughness.

Creep-Resisting Grades: use in gas turbines and jet engines. They are made of niobium, cobalt, boron, and vanadium, which makes them rigid and strong, which stays intact also in pressure environments like stretching or deforming of metal under stress and high temperature.(Source: worldstainless.org)

Market Dynamics

Driver

What Are the Key Growth Drivers in the Martensitic Stainless Steels Market?

Martensitic stainless steels market growth is driven by the growing shift of consumers towards EVs and the industrial shift to improve fuel efficiency and lower emissions, which increases the demand for lightweight materials from the automotive sectors is, a major factor responsible for growth. Other key growth drivers include demand from aerospace and defence, advanced manufacturing techniques, and demand from the health and medical device industry due to its properties and applications, which expand the market growth.

Restraint

What Are the Key Growth Challenges in the Martensitic Stainless Steels Market?

The market is experiencing extensive challenges due to high volatility of raw material costs, especially chromium, nickel, and molybdenum; stringent environmental regulations due to growing awareness, and growing competition, which hinders the growth of the market. Other key growth restraints are corrosion resistance limitations, intense competition from alternatives, hindrance in the supply chain, and ESG and regulatory pressures, which face increasing compliance, challenging the growth and expansion of the market.

Opportunity

What Are the Key Growth Opportunities in the Martensitic Stainless Steels Market?

The martensitic stainless steels market is experiencing growth driven by key opportunities like key technological innovation, including ongoing metallurgical advancements, which include advanced heat treatment processes, which help in improving previous challenges like brittleness. This factor and innovation increase and broaden the scope of material use in the manufacturing of equipment and heavy machinery. This is a major growth factor that will help the market to grow in the coming time and also play a significant role in the advancement of the market.

Segmental Insights

Grade Insights

The Type 410 Segment Dominated the Martensitic stainless steels Market With 31% Market Share In 2025.

The Type 410 segment dominated the market with a 31% share in 2025, due to advanced manufacturing and advanced technology like heat treatment processing and increased demand for components from sectors like automotive and mechanical engineering applications. The cost efficiency of 410 as it is processed through carbon content and thermal processing rather than tradition method propels the growth of the market.

")

The Type 420 segment held 24% market share in 2025 and is expected to have the fastest growth with a CAGR of 6.60% in the forecast period, due to its high hardness, precision manufacturing, and excellent edge, which increases demand. The manufacturing advancements in metal processing, such as metal injection molding, help manufacturers to produce the complex 420 stainless steel. The consumer food and cutlery industry's demand for medical and surgical instruments is a major factor that supports the growth of the market.

Martensitic Stainless Steels Market Share, By Grade, 2025(%)

| By Grade | Market Share (%) |

| Type 410 | 31% |

| Type 420 | 24.00% |

| Type 431 | 14.00% |

| Type 440 | 16.00% |

| Type 416 | 9.00% |

| Others | 6.00% |

Product Form Insights

The Flat Products segment dominated the market with a 37% share in 2025, due to its properties like high strength, magnetic properties of materials, and wear resistance, which are widely used in various sectors like industrial applications, automotive, and cutlery. The research, development, and innovation in the designing and production of products to improve toughness, corrosion resistance, and wearability, while keeping the traditional strength, increase the demand and help in promoting the product in the market.

")

The Tubes and Pipes segment held 15% market share in 2025 and is expected to have the fastest growth with a CAGR of 6.4% in the forecast period, due to the exceptional mechanical properties, which increase demand and are ideal for high-pressure and corrosive environments, especially in industries such as aerospace and automotive, where high-strength components are used. The other major and key drivers include oil and gas sector dominance, seamless tube manufacturing innovation, and the rise of super martensitic grades. The continuous production and processing by major companies for high alloy pipes and tubes boosts the market supply.

Martensitic Stainless Steels Market Share, By Product,2025(%)

| By Product Form | Market Share (%) |

| Flat Products | 37.00% |

| Long Products | 28.00% |

| Tubes & Pipes | 15.00% |

| Forged Products | 12.00% |

| Cast Products | 8.00% |

Heat Treatment Insights

The hardened & tempered segment dominated the market with a 39% share in 2025, due to its demand for wear resistance and structural durability, balancing the high hardness of the materials for high-stress applications. The hardened and tempered are extensively used to withstand corrosive environments and mechanical wear, supporting growth. This also helps in strengthening the manufacturing and heat treatment through advanced processing, supporting the growth of the market.

The quenched & tempered segment held 21% market share in 2025 and is expected to have the fastest growth with a CAGR of 6.3% in the forecast period, due to growing demand for steel in the broader specialty stainless steel sector. Rapid cooling and then tempering it is a foundational processing route for martensitic stainless steel. Energy sector applications, industrial tooling, cutlery, advanced heating treatment, and regional dominance for heat-treated steel plates and specialty grades, especially in India and China, further propel the expansion of the market.

Manufacturing Process Insights

The hot-rolled segment dominated the market with a 35% share in 2025 due to robust and exceptional demand from industrial manufacturing, rapid infrastructure development, and the need for high-strength and wear-resistant components due to their properties and applications. The other key growth drivers are industrial machinery dominance, application in heavy-duty components, infrastructure, and shipbuilding, which create industrial dominance and support the growth of the market.

The cold-rolled segment held 26% market share in 2025 and is expected to have the fastest growth with a CAGR of 6.4% in the forecast period, due to exceptional demand from the industry for blades, shafts and valves, which increases the consumption of cold-rolled martensitic flats. The advanced processing through integrating continuous lines, tempering the tight tolerance, and improving weldability also meets the market demand. The hardness level over HRC 55, which his achieved by the cold rolling, makes it a preferred choice for surgical instruments and premium cutlery, which further increases the demand.

Martensitic Stainless Steels Market Share, By Heat Treatment,2025(%)

| By Heat Treatment | Market Share (%) |

| Annealed | 19.00% |

| Hardened | 21.00% |

| Hardened & Tempered | 39.00% |

| Quenched & Tempered | 21.00% |

End Use Industry Insights

The automotive segment dominated the market with a 27% share in 2025, due to its exceptional and superior strength, wear resistance, and high hardness, as it is used in disc brakes and powertrain components, due to its high hardness and moderate corrosion resistance, which expands its application and demand. The push for better fuel efficiency and longer EV ranges increases the demand for lightweight materials, maintaining structural lightweighting without compromising crash safety, expanding the growth of the market.

The aerospace segment held 11% market share in 2025 and is expected to have the fastest growth with a CAGR of 6.8% in the forecast period, due to rising demand for materials offering exceptional strength-to-weight ratios, high tensile strength, and corrosion resistance under extreme operating conditions. It is a vital material for critical aircraft parts, including turbine blades, engine components, and landing gear. The expanding forgings market, which is driven by the aerospace and commercial aviation needs, drives growth.

Martensitic Stainless Steels Market Share, By End-use Industry, 2025(%)

| By End-use Industry | Market Share (%) |

| Automotive | 27% |

| Oil & Gas | 18.00% |

| Aerospace | 11.00% |

| Power Generation | 12.00% |

| Industrial Machinery | 17.00% |

| Medical | 6.00% |

| Consumer Goods | 6.00% |

| Others | 3% |

Distribution Channel Insights

The Direct Sales Segment Dominated the Martensitic Stainless Steels Market With 46% Market Share In 2025

The direct sales segment dominated the market with a 46% share in 2025. It is largely driven by original equipment manufacturers (OEMs) in aerospace, automotive, and heavy industry bypassing distributors to establish long-term supply contracts for high-strength, lightweight, and heat-resistant components. Martensitic steels offer an exceptional strength-to-weight ratio. Direct sales to automotive OEMs are surging as the shift toward electric vehicles (EVs) requires highly durable, crash-resistant chassis parts and battery enclosures.

The online sales segment held 6% market share in 2025 and is expected to have the fastest growth with a CAGR of 8.2% in the forecast period, driven by the broader B2B shift toward digital procurement and e-commerce. B2B metal marketplaces allow buyers to instantly compare grades, prices, and delivery terms, replacing traditional, time-intensive RFQ processes. Platforms like Metalbook App on Google Play, OfBusiness, and SteelonCall facilitate transparent price discovery, instant quotations, and logistics for industrial metals.

Martensitic Stainless Steels Market Share, By Distribution Channel,2025(%)

| By Distribution Channel | Market Share (%) |

| Direct Sales | 46.00% |

| Distributors & Service Centers | 33.00% |

| Online Sales | 6.00% |

| OEM Supply Contracts | 15.00% |

Regional Analysis

How did Asia Pacific dominate the Martensitic Stainless Steels Market in 2025?

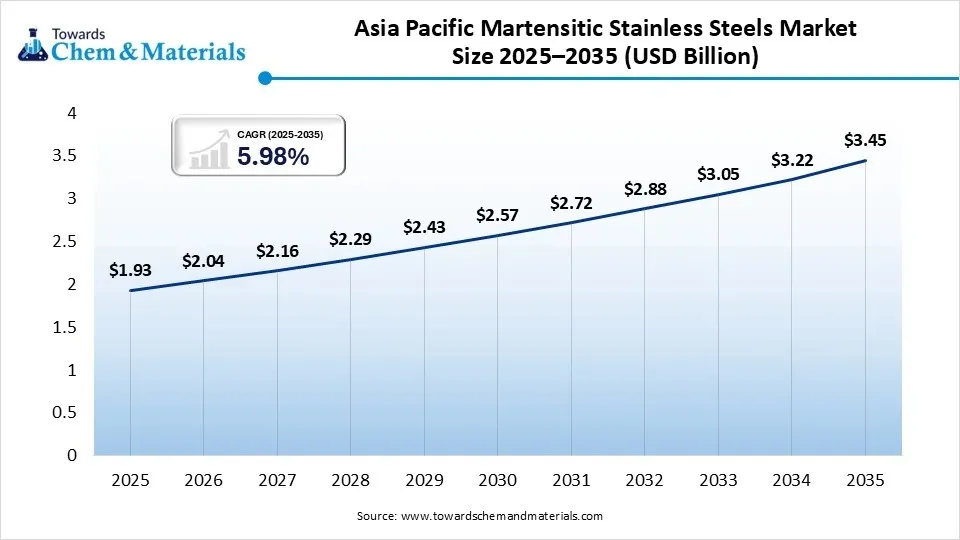

The Asia Pacific martensitic stainless steels market size was estimated at USD 1.93 billion in 2025 and is projected to reach USD 3.45 billion by 2035, growing at a CAGR of 5.98% from 2026 to 2035. Asia Pacific dominated the market with a share of 47% in 2025, due to massive government initiatives for development of infrastructure development, rising production from major industry players like Baosteel and Tsingshan, and rapid urbanization, which supports the growth in the region. Policies such as India's national stainless-steel policy and massive regional smart city projects increase the consumption and further expand the market growth. The cost-effective local production and energy and power generation are the reasons for the dominance of the market in the region.

") India

India

India's martensitic stainless steels market is driven by booming demand for high-strength, wear-resistant materials in the automotive, aerospace, and healthcare industries. Government initiatives like Make in India and rapid infrastructure development are propelling overall consumption, making the Asia-Pacific region the fastest-growing hub for specialty steels.

China

China's martensitic stainless-steel market is primarily driven by expanding automotive manufacturing, large-scale infrastructure and energy projects, and rising demand for industrial machinery. Technological advancements enhancing material wear and corrosion resistance are further boosting adoption in critical, high-strength applications.

North America Martensitic Stainless Steels Market Growth Factor

North America martensitic stainless steels market size was estimated at USD 0.74 billion in 2025 and is projected to reach USD 1.34 billion by 2035, growing at a CAGR of 6.12% from 2026 to 2035. North America held the market share of 18% in 2025 and is expected to have the fastest growth with a CAGR of 6.5% in the forecast period, due to growing hubs of aerospace, automotive, and energy sectors, which increase demand and sale strengthen the production and manufacturing in the region. The regional infrastructure development, increased medical device production, and heavy investment in the region propel the growth further. The heavy investment in the development of bridges, highways, and public transportation supports and adds to the growth of the market.

United States

The US Martensitic stainless steels market is rapidly expanding, driven by the aerospace, automotive, and medical device sectors. Growth is fueled by the material's high strength-to-weight ratio and exceptional wear resistance. Upgrading aging infrastructure and expanding renewable energy facilities which rely heavily on these corrosion-resistant and highly durable alloys are major catalysts.

Canada

Canada's martensitic stainless-steel market This growth is primarily fueled by infrastructure upgrades, an expanding domestic energy sector, robust automotive manufacturing, and high-demand applications like industrial machinery and surgical instruments. Canadian automotive supply chains rely on martensitic grades for gears, shafts, and exhaust lines. The push for durable, lightweight materials to improve fuel efficiency directly accelerates local demand.

Europe Martensitic Stainless Steels Market Growth Factor

The Europe martensitic stainless steels market size was estimated at USD 0.99 billion in 2025 and is projected to reach USD 1.78 billion by 2035, growing at a CAGR of 6.04% from 2026 to 2035. Europe held a market share of 24% in 2025, due to regional shift towards adoption of Ev which increases the demand for lightweight materials to increase the fuel efficiency especially in countries like Germany, France, and the U.K. the major growth driver in the regions market is stringent regional eco-friendly manufacturing mandates like EUs carbon Border Adjustment Mechanism pushes the manufacturers to adopt more cleaner and greener production practice with the help of key players in the region like Outokumpu and Acerinox, accelerating the shift toward recycled scrap usage.

Germany

Germany's martensitic stainless steels market is driven by robust demand from the automotive sector, especially exhaust lines and engine components and the manufacturing of surgical tools, kitchen knives, and industrial blades. The regional market is supported by advanced engineering and green steel initiatives. Germany is a global hub for high-precision medical devices. The exceptional hardenability and corrosion resistance of martensitic stainless steel make it the gold standard for surgical instruments.

Italy

The market for martensitic stainless steels in Italy is primarily driven by strong demand from domestic manufacturing and export-oriented sectors like automotive like Ferrari, Lamborghini, and Fiat components, aerospace, and high-end kitchenware. Because these alloys are prized for their high strength, wear resistance, and hardness, they are frequently utilized in critical components such as engine valves, turbine blades, bearings, and cutting tools.

Latin America Martensitic Stainless Steels Market Growth Factor

The Latin America martensitic stainless steels market size was estimated at USD 0.25 billion in 2025 and is projected to reach USD 0.47 billion by 2035, growing at a CAGR of 6.52% from 2026 to 2035. Latin America held a market share of 6% in 2025, driven by infrastructure development in heavy industry, booming automotive manufacturing in countries like Mexico and Brazil, and rising demand for corrosion-resistant materials in the regional energy sector. The region, particularly Brazil, is seeing heavy adoption of high-strength martensitic stainless steel for lightweight, durable components like gears, shafts, and cutting tools, which helps automakers improve fuel efficiency.

Brazil

The Brazilian martensitic stainless-steel market is primarily driven by expanding automotive manufacturing, localized heavy industrial operations, and the energy/oil & gas sectors. This specific material is highly valued for its superior hardness, wear resistance, and ability to withstand extreme conditions. Rapid urbanization and infrastructure projects require durable construction equipment and industrial machinery. Martensitic steel is uniquely suited for tools, blades, valves, and mining equipment that demand exceptional wear resistance.

Argentina

Argentina's martensitic stainless-steel market is primarily driven by expanding oil and gas operations (Vaca Muerta), automotive manufacturing, and infrastructure upgrades. These sectors rely on the material's exceptional hardness, wear resistance, and high-temperature durability.

Middle East and Africa Martensitic Stainless Steels Market Growth Factor

The Middle East and Africa martensitic stainless steels market size was estimated at USD 0.21 billion in 2025 and is projected to reach USD 0.40 billion by 2035, growing at a CAGR of 6.66% from 2026 to 2035. The Middle East and Africa held a market share of 5% in 2025, primarily driven by expanding oil and gas infrastructure, automotive manufacturing, and large-scale industrial projects within the GCC region and South Africa. Its high strength, hardness, and wear resistance make it essential for engineering applications such as turbine blades, shafts, and valves. Extensive upstream and downstream development in energy hubs, particularly in Saudi Arabia and the UAE, requires martensitic stainless steel for its resistance to corrosion and high-stress environments.

")

Saudi Arabia

Saudi Arabia's martensitic stainless-steel market is predominantly within the 400 Series Market and is driven by government Vision 2030 initiatives, investments in petrochemical and oil and gas infrastructure, and high-tech manufacturing localization. Key growth factors include high-stress industrial applications requiring superior wear resistance, corrosion defense, and high tensile strength.

UAE

The UAE's martensitic stainless steels market is expanding due to heavy investments in the oil & gas sector, petrochemical processing, and rapid infrastructure development. High-strength and wear-resistant martensitic grades like 410 and 420 are highly sought after for equipment requiring extreme durability in harsh environments.

Competitive Analysis

The martensitic stainless-steel production is heavily focused on by domestic and major players due to high demand for agile production from automotive, aerospace, and medical industries, from players like Nippon Steel Corporation, POSCO, Acerinox, and Jindal Stainless.

- EcoACX® is a highly sustainable grade of stainless steel manufactured by Acerinox Europa. It is designed to help industrial clients directly and verifiably reduce their Scope 3 supply chain emissions without sacrificing material quality, performance, or corrosion resistance.(Source: www.acerinox.com)

- At Blechexpo 2025, thyssenkrupp Steel showcased five distinct material lines under its "Material of Mobility" banner and broader industrial portfolio. The core materials include MBW, CH-W, bluemint® Steel, ZM Ecoprotect® Solar, and High-Strength Cut-to-Length Sheet.(Source: www.thyssenkrupp-steel.com)

Recent Developments

- In April 2026, Jindal Stainless, a top stainless-steel producer in India, introduced its stainless steel rebars, called ‘Jindal Infinity’, in retail outlets in Punjab. This move aims to make advanced construction materials more accessible to end consumers. ‘Jindal Infinity’ rebars are known for their enhanced durability, resistance to corrosion, and long-term value.(Source: www.jindalstainless.com)

- In June 2026, JFE Holdings is expanding its global supply footprint by targeting joint ventures in the United States, JSW JFE Steel Limited, an integrated steelworks venture with local partner JSW Steel. and doubling its steel production capacity in India by 2030.(Source: www.vibetrader.com)

Top players in the Martensitic stainless steels market & Their Offerings

| Company | Company Type/Position | Major Headquarters | Geographic Presence | Martensitic stainless steels: Offerings | Key Offering/Strength of Martensitic stainless steels |

| Nippon Steel Corporation | Publicly traded, multinational manufacturing company | Tokyo, Japan | Asia, North America, and Europe | Nippon Steel's Martensitic Stainless Series includes custom-engineered solutions for high-stress environments like NSSC 550, NSSC WR-1, and NSSC HT980. | Key strengths offered include superior quench hardening, corrosion resistance, and magnetic properties. |

| POSCO | Public Company (Traded on the KRX and NYSE as POSCO Holdings Inc.) | Pohang, South Korea | Asia, the Americas, Europe, and Africa | POSCO manufactures several distinct martensitic stainless-steel grades tailored for industrial and consumer use, like grade 410/ 410B and Grade 450 | Core strength and advantages like tunable strength and hardness, high wear resistance, and integrated manufacturing |

| ArcelorMittal | The world's leading steel and mining company. It operates as a global public corporation. | Luxembourg | Europe, the Americas, Africa, and Asia | Key strength in martensitic steels lies in its martINsite® and Industeel product lines. Ultra-high strength, super weldability, and toughness | Offers a diverse range of martensitic steels, SOLEIL C5, VIRGO 39, and VIRGO 17.4 PH |

| Acerinox | Publicly traded multinational holding company. Leading stainless steel and high-performance alloy producer | Madrid, Spain | Pacific, Europe, North America, Africa | Premium martensitic stainless steels, ACX 390, ACX 360 | Provides outstanding mechanical strength and high hardness levels of stainless steel |

| JFE Steel Corporation | The largest steel manufacturer is a publicly traded, multinational corporation. | Chiyoda, Tokyo, Japan. | Europe, North America, Asia Pacific | Oil & Gas (OCTG) Pipes, JFE410DB-ER for motorcycle, JFE410RW for coal and iron | advanced proprietary grades like UHP TM-15CR-125 and HP13Cr for deep, high-pressure wells |

Other Top Players Are

- Tata Steel Group

- China Baowu Steel Group

- ThyssenKrupp

- Outokumpu

- Jindal Stainless

- Aperam

- ATI (Allegheny Technologies)

- Sandvik AB

- Cleveland-Cliffs (AK Steel)

- Valbruna

- Tsingshan Holding Group

- Dongkuk Steel Mill

- HBIS Group

- Gerdau

- Voestalpine

Segments Covered:

By Grade

- Type 410

- Standard 410

- Modified 410

- Type 420

- 420A

- 420B

- 420C

- Type 431

- Type 440

- 440A

- 440B

- 440C

- Type 416

- Others

- Type 403

- Type 414

- Proprietary Martensitic Grades

By Product Form

- Flat Products

- Plates

- Sheets

- Coils

- Long Products

- Bars

- Rods

- Wire Rods

- Tubes & Pipes

- Seamless

- Welded

- Forged Products

- Cast Products

By Heat Treatment

- Annealed

- Hardened

- Hardened & Tempered

- Quenched & Tempered

By Manufacturing Process

- Hot Rolled

- Cold Rolled

- Forged

- Cast

- Powder Metallurgy

By End-use Industry

- Automotive

- Engine Components

- Exhaust Components

- Transmission Parts

- Oil & Gas

- Valves

- Pumps

- Downhole Equipment

- Aerospace

- Structural Components

- Landing Gear Components

- Power Generation

- Steam Turbine Parts

- Gas Turbine Components

- Industrial Machinery

- Bearings

- Shafts

- Gears

- Medical

- Surgical Instruments

- Dental Instruments

- Consumer Goods

- Knives

- Scissors

- Hand Tools

- Others

- Defense

- Marine

- Mining

By Distribution Channel

- Direct Sales

- Distributors & Service Centers

- Online Sales

- OEM Supply Contracts

By Regions

- North America

- U.S.

- Canada

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Sweden

- Denmark

- Norway

- Asia Pacific

- China

- Japan

- India

- South Korea

- Thailand

- Latin America

- Brazil

- Mexico

- Argentina

- Middle East & Africa

- South Africa

- UAE

- Saudi Arabia

- Kuwait

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

FAQ's

Select User License to Buy

Figures (6)