Content

What is Mild Steel Market Size and Share?

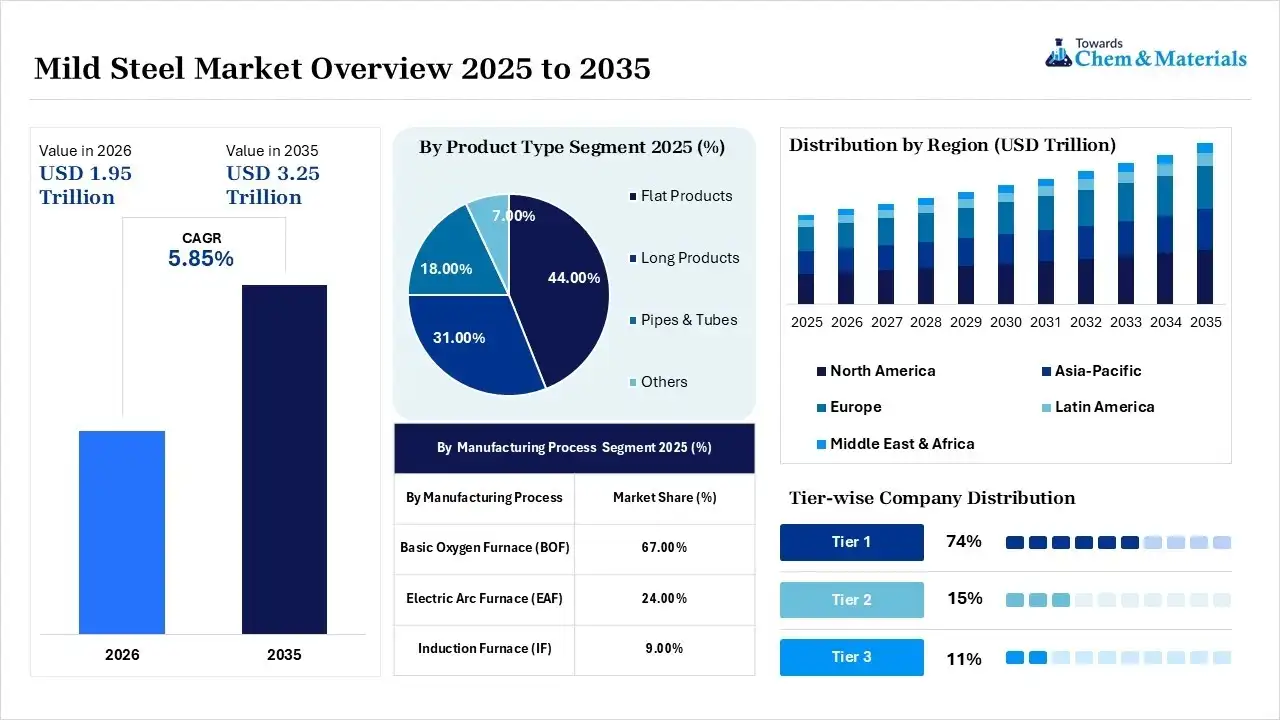

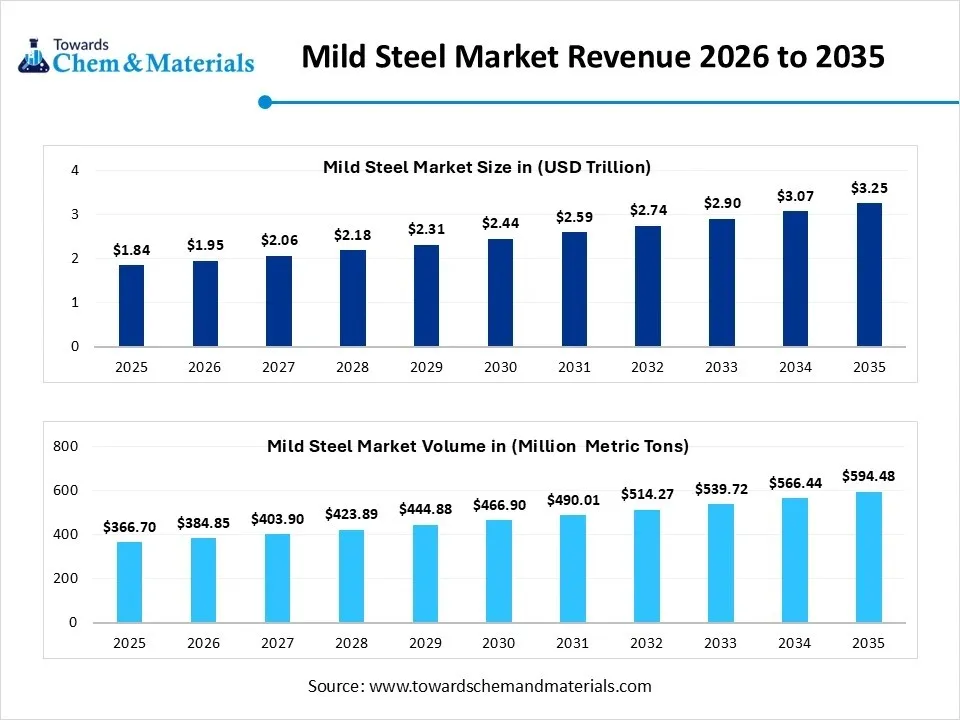

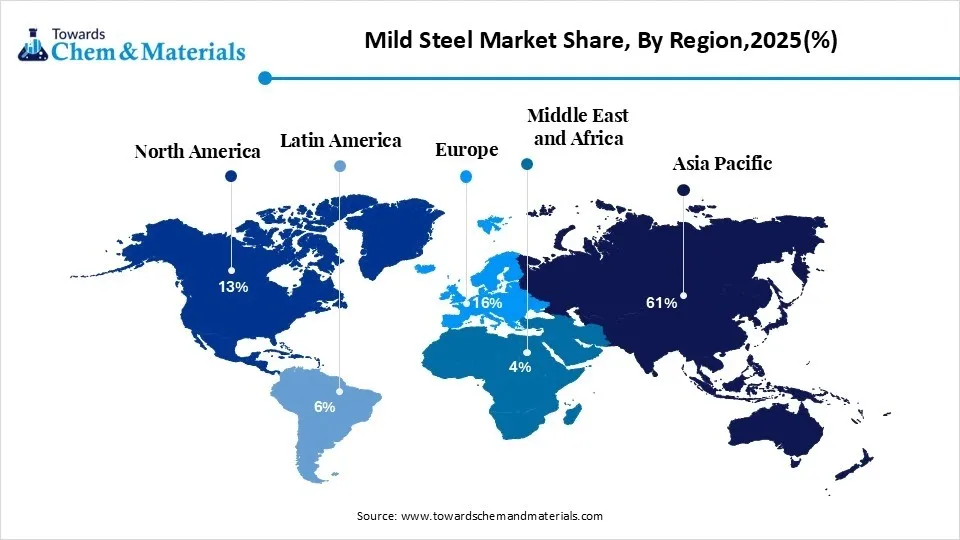

The global mild steel market size was valued at USD 1.84 trillion in 2025, is estimated to reach USD 1.95 trillion in 2026, and is projected to reach USD 3.25 trillion by 2035, exhibiting a compound annual growth rate (CAGR) of 5.85% over the forecast period from 2026 to 2035.Asia Pacific dominated the mild steel market with the largest revenue share of 61% in 2025 and is expected to grow at the fastest CAGR of 5.95% during the forecast period. In terms of volume, the mild steel market is projected to grow from 366.7 million metric tons in 2025 to 594.5 million metric tons by 2035. growing at a CAGR of 4.95% from 2026 to 2035.The ongoing growth of machinery, equipment, and fabrication sectors is a major factor leading market growth. Also, supportive government policies and investments coupled with the soaring manufacturing and industrial activity across the globe can create new market avenues soon in the future.

Market Highlights

- By region, Asia Pacific dominated the market with a share of 61.00% in 2025 and is expected to grow at a CAGR of 4.80% over the forecast period.

- By region, North America held a market share of 13.00% in 2025 and was expected to grow at the fastest CAGR of 5.80% over the forecast period.

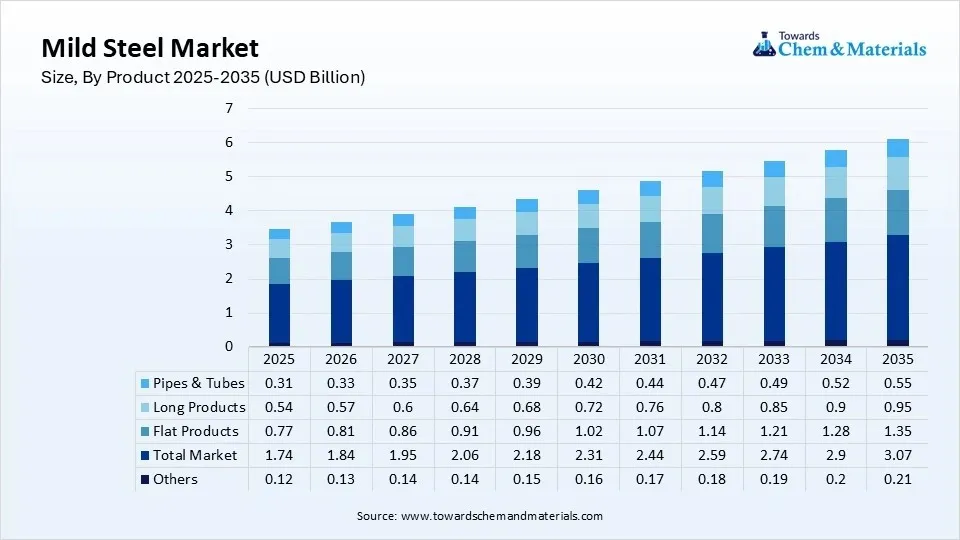

- By product, the flat products segment dominated the market with the largest share of 44.00% in 2025 and is expected to grow at a CAGR of 5.20% over the forecast period.

- By product, the pipes & tubes segment held a market share of 18.00% in 2025 and is expected to grow at the fastest CAGR of 5.80% over the forecast period.

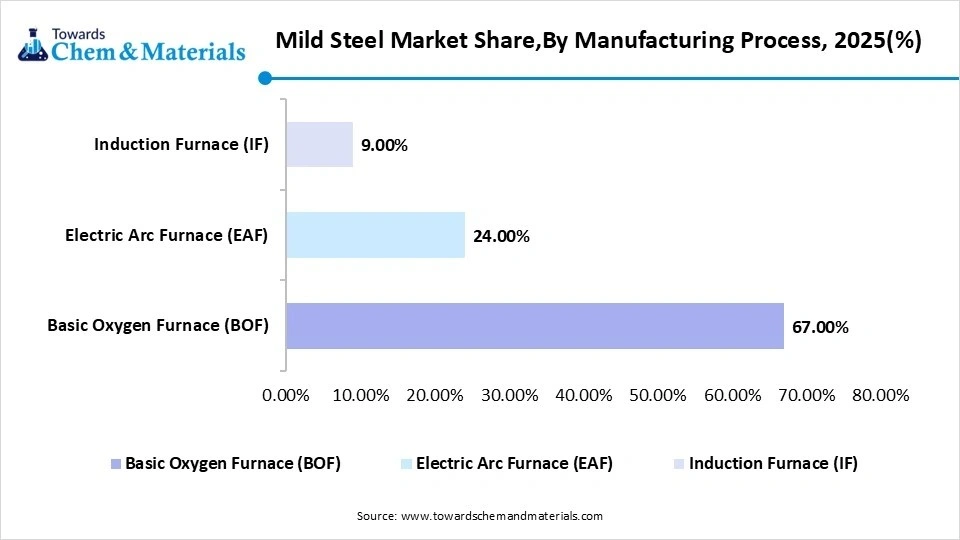

- By manufacturing process, the basic oxygen furnace (BOF) segment dominated the market with the largest share of 67.00% in 2025 and is expected to grow at a CAGR of 4.70% over the forecast period.

- By manufacturing process, the electric arc furnace (EAF) segment held a market share of 24.00% in 2025 and is expected to grow at the fastest CAGR of 6.40% over the forecast period.

- By form, the coil segment dominated the market with the largest share of 33.00% in 2025 and is expected to grow at a CAGR of 5.20% over the forecast period.

- By form, the pipe & tube segment held a market share of 9.00% in 2025 and is expected to grow at the fastest CAGR of 5.90% over the forecast period.

- By thickness, the 3–6 mm segment dominated the market with the largest share of 38.00% in 2025 and is expected to grow at a CAGR of 5.20% over the forecast period.

- By thickness, the 6–12 mm segment held a market share of 24.00% in 2025 and is expected to grow at the fastest CAGR of 5.70% over the forecast period.

- By application, the building & construction segment dominated the market with the largest share of 36.00% in 2025 and is expected to grow at a CAGR of 5% over the forecast period.

- By application, the energy & power segment held a market share of 9.00% in 2025 and is expected to grow at the fastest CAGR of 6.20% during the projected period.

- By distribution channel, the direct sales segment dominated the market with the largest share of 52.00% in 2025 and is expected to grow at a CAGR of 5.10% over the forecast period.

- By distribution channel, the steel service centers segment held a market share of 24.00% in 2025 and is expected to grow at the fastest CAGR of 5.90% during the study period.

The ongoing shift towards clean and renewable energy is creating an increase in demand for mild steel, including solar farm mounting structures, wind turbine towers, offshore platform foundations, and grid modernization equipment, presenting lucrative opportunities in the market.

- In January 2026, China's first million-ton-level near-zero carbon steel facility is fully operational in Zhanjiang, Guangdong. Operated by a subsidiary of Baosteel, the plant pioneers hydrogen-based smelting to minimize fossil fuel reliance. This infrastructure integrates a 1 Mt capacity hydrogen shaft furnace, an electric arc furnace, and a continuous casting sequence.(Source: mexicobusiness.news)

- Therefore, the incorporation of threaded globe valves and other components in energy infrastructure installations further boosts demand for mild steel across the upstream and midstream energy industries over the projected period.

Global Investment Flow for Mild Steel 2025

The global investment flow for the market is undergoing a significant geographical and structural reallocation, transitioning away from standard blast furnace expansions in emerging economies such as China and increasingly transitioning towards low-carbon "green steel" technologies and developing market infrastructure.

- In June 2026, China's steel exports reached 10.341 million tonnes in May, reflecting an 8.9% month-over-month increase. However, cumulative shipments for the first five months of the year totaled 44.554 million tons.(Source: www.sunsirs.com)

The investment flows are specifically targeting emerging economies like Vietnam, Egypt, and Saudi Arabia. These countries are positioning themselves as new regional manufacturing hubs by drawing cross-border investments to build out local construction supply chains.

Mild Steel Market Trends

- The increase in automotive manufacturing across the globe is the latest trend in the market, shaping positive market growth. As advanced high-strength steels (AHSS) and aluminum alloys are replacing conventional mild steel in some structural applications and closure panels, mild steel retains growth in underbody components, brackets, and fuel tanks.

- In recent years, there has been a growing demand for steel in manufacturing military aircraft. Military aircraft need materials with excellent durability, strength, and resistance to extreme conditions. Steel, with its high reliability and strength, is a first choice for different components within these aircraft.

- Ongoing technological innovations are the future trend in the market, driving market expansion. These advancements include an extensive range of innovations, from automotive developments and artificial intelligence to the development of cutting-edge materials and production processes.

Report Scope

| Report Attributes | Details |

| Market Size in 2026 | USD 1.95 Triilion/ 384.9 Million Metric Tons |

| Market Size by 2035 | USD 3.25 Trillion/ 594.5 Million Metric Tons |

| Growth Rate from 2026 to 2035 | CAGR 5.85% |

| Base Year of Estimation | 2025 |

| Forecast Period | 2026 - 2035 |

| Dominant Region | Asia Pacific |

| Segment Covered | By Product Type, By Manufacturing Process, By Form, By Thickness, By Application, By Distribution Channel, By Region |

| Key Profiled Companies | POSCO Holdings, Nucor Corporation, HBIS Group, Ansteel Group, Jiangsu Shagang Group, Tata Steel Limited, JSW Steel |

AI-Powered Predictive Formulations in the Mild Steel Market

AI-powered predictive formulations in the market use data-driven and machine learning models to forecast, simulate, and optimize the microstructural properties and overall performance of low-carbon steels. Furthermore, AI frameworks are able to precisely predict key metrics such as Ultimate Tensile Strength (UTS), Yield Strength, and elongation before the steel even reaches a physical testing lab.

Supply Chain Analysis of the Mild Steel Market

Production & Processing

- It includes the creation of raw steel from iron ore via a blast furnace/basic oxygen furnace or melting scrap (via an electric arc furnace).

- The processing includes shaping and refining this steel through hot rolling, cold rolling, and coating.

ArcelorMittal: One of the world's leading steel and mining companies, operating globally with a strong presence in the Americas, Europe, and Africa. - Other Key Players: Tata Steel, Nucor Corporation

Quality Testing and Certification

- It includes standardized inspection protocols and verifies documentation utilized to prove a steel batch's physical, chemical, and mechanical properties.

These crucial steps guarantee the material's durability, load-bearing capacity, and industrial compliance with safety standards. - JSW Steel: One of India's largest integrated steel companies, utilizing modern methods of testing steel quality for structural and commercial applications.

- Other Key Players: Tata Steel, ArcelorMittal

Distribution to Industrial Users

- It includes the supply chain channels that connect major steel market players directly with downstream B2B consumers, including manufacturing, automotive, energy, and construction firms.

Distributors bypass retail traders to offer customized, bulk, and processed steel products directly to these industrial facilities. - Tata Steel: A historic legacy brand providing high-quality, flat, and long mild-steel products to construction and automotive sectors.

- Other Key Players: APL Apollo Tubes, Shyam Metalics

Mild Steel Market’s Regulatory Landscape: Global Regulations

| Country / Region | Regulatory Body | Key Regulations & Standards | Focus Areas |

| Global / International | International Organization for Standardization (ISO) | ISO 630, ISO 4950, ISO 14001, ISO 5001 | Structural steel specs, environmental management, energy efficiency |

| United States | Environmental Protection Agency (EPA), OSHA, ASTM International | Clean Air Act, ASTM A36, ASTM A513, OSHA 29 CFR | Carbon emissions, structural steel grading, workplace safety |

| European Union | European Committee for Standardization (CEN), European Commission | EN 10025, EU ETS, CBAM, Construction Products Regulation (CPR) | Structural steel standards, carbon trading, import carbon tax |

What are the Types of Mild Steel?

- Hot Rolled Mild Steel:This steel is shaped at very high temperatures (over 927°C). It is rougher and generally used for heavy structural components, like I-beams and railway tracks.

- Cold Rolled Mild Steel:Hot-rolled steel that is further processed at room temperature. It has a smoother surface finish and tighter dimensional tolerances, which makes it ideal for automotive panels and consumer appliances.

- Galvanized Mild Steel:It is coated with a protective layer of zinc to prevent rust and corrosion. It is the major choice for outdoor frameworks, sheds, and agricultural equipment.

Market Dynamics

Driver

Surge in Investments in Energy Sector

Investments in renewable energy infrastructure are the major factor driving the growth of the market. The shift towards sustainable energy sources, like solar and wind power, needs significant amounts of steel for the construction of solar panels, turbines, and other infrastructure. In addition, this transition also aligns well with many extensive sustainability goals. As major countries are focusing on minimizing carbon emissions, the need for mild steel in energy projects is likely to rise.

Restraint

Severe Raw Material Volatility

Input costs for iron scrap, ore, and coking coal fluctuate unpredictably, which fuels structural pricing shifts, increasing mild steel prices. This is the major factor hindering the growth of the market. Moreover, growing trade barriers, retaliatory tariffs, and quotas globally complicate international trade flows and limit export prospects. Adopting clean technologies such as green hydrogen needs huge upfront investment, which is difficult for businesses to cope with.

Opportunity

Rise in Green Steel Initiatives

The ongoing investment in Electric Arc Furnaces (EAF) and hydrogen-based manufacturing addresses stringent low-carbon regulatory environments, creating lucrative opportunities in the market while fulfilling global B2B procurement needs for sustainable manufacturing materials. Furthermore, implementing Industry 4.0 standards such as real-time supply chain monitoring and AI-driven predictive maintenance allows companies to capture major market share in the near future.

Segmental Insights

Product Type Insight

The flat products segment dominated the market with the largest share of 44.00% in 2025 and is expected to grow at a CAGR of 5.20% over the forecast period. The dominance of the segment can be attributed to the ongoing urbanization, expanding infrastructure, and automotive production investments. In addition, the construction industry heavily relies on flat steel for roofing, cladding, and modular design because of its ease of flexibility and assembly.

")

The pipes & tubes segment held a market share of 18.00% in 2025 and is expected to grow at the fastest CAGR of 5.80% over the forecast period. The growth of the segment can be credited to its growing demand in water management and energy pipeline networks along with its cost-effectiveness. Mild steel offers exceptional ductility and weldability at a lower price point as compared to stainless or alloy steels.

Mild Steel Market Share, By Product, 2025(%)

| By Product Type | Market Share (%) |

| Flat Products | 44.00% |

| Long Products | 31.00% |

| Pipes & Tubes | 18.00% |

| Others | 7.00% |

Manufacturing Process Insight

The basic oxygen furnace (BOF) segment dominated the market with the largest share of 67.00% in 2025 and is expected to grow at a CAGR of 4.70% over the forecast period. The growth of the segment can be linked to the ongoing urbanization and advent of mega-construction projects in emerging economies. The extensive usage of mild steel sheets, bars, and long steel in shipbuilding, machinery, and consumer goods propels steady baseline growth.

The electric arc furnace (EAF) segment held a market share of 24.00% in 2025 and is expected to grow at the fastest CAGR of 6.40% over the forecast period. The growth of the segment can be driven by its lower operational costs, sustainability mandates, and scrap metal abundance. In addition, EAFs rely mainly on recycled ferrous scrap. Increasing urbanization and scrap collection infrastructures are offering a cost-effective and steady supply of raw materials.")

- In February 2026, ArcelorMittal confirmed a strategic €1.3 billion investment to construct an electric arc furnace (EAF) at its Dunkirk facility. Scheduled to launch in 2029, the two-million-tonne EAF will reduce CO₂ emissions by two-thirds compared to traditional blast furnaces, utilizing a mix of scrap, HBI/DRI, and hot metal.

(Source: corporate.arcelormittal.com)

Mild Steel Market Share,By Manufacturing Process, 2025(%)

| By Manufacturing Process | Market Share (%) |

| Basic Oxygen Furnace (BOF) | 67.00% |

| Electric Arc Furnace (EAF) | 24.00% |

| Induction Furnace (IF) | 9.00% |

Form Insight

The coil segment dominated the market with the largest share of 33.00% in 2025 and is expected to grow at a CAGR of 5.20% over the forecast period. The dominance of the segment is owing to the growing need for durable and lightweight materials across various sectors along with the surge in infrastructure investments globally. Mild steel coils are generally used in shipbuilding and consumer appliances because of their benefits.

The pipe & tube segment held a market share of 9.00% in 2025 and is expected to grow at the fastest CAGR of 5.90% over the forecast period. The growth of the segment is due to extensive infrastructure development and heavy industrialization coupled with the rise in urbanization in emerging economies. The cost-effective and abundant availability of carbon and mild steel makes it the most preferred choice for large-scale projects.

Mild Steel Market Share,By Form, 2025(%)

| By Form | Market Share (%) |

| Coil | 33.00% |

| Sheet | 18.00% |

| Plate | 16.00% |

| Bar | 12.00% |

| Rod | 8.00% |

| Pipe & Tube | 9.00% |

| Structural Steel | 4.00% |

Thickness Insight

The 3–6 mm segment dominated the market with the largest share of 38.00% in 2025 and is expected to grow at a CAGR of 5.20% over the forecast period. The growth of the segment can be attributed to the ongoing shift towards cost-effective and lightweight manufacturing. Moreover, this segment offers the crucial balance of tensile strength and weight. Mild steel in this thickness range is more formable, weldable, and inexpensive as compared to other alloys.

The 6–12 mm segment held a market share of 24.00% in 2025 and is expected to grow at the fastest CAGR of 5.70% over the forecast period. The growth of the segment can be credited to the growing demand in residential housing and extensive use of these dimensions for concrete reinforcement stirrups. Furthermore, extensive regional infrastructure, including expressways and metro rail networks, is increasingly fueling bulk procurement of this thickness still.

Mild Steel Market Share,By Thickness, 2025(%)

| By Thickness | Market Share (%) |

| Up to 3 mm | 26.00% |

| 3–6 mm | 38.00% |

| 6–12 mm | 24.00% |

| Above 12 mm | 12.00% |

Application Insight

The building & construction segment dominated the market with the largest share of 36.00% in 2025 and is expected to grow at a CAGR of 5% over the forecast period. The dominance of the segment can be linked to the increasing transition towards prefabricated modular construction and rising adoption of green building standards. Also, government spending on public infrastructure such as railways, bridges, and utilities boosts demand further.

The energy & power segment held a market share of 9.00% in 2025 and is expected to grow at the fastest CAGR of 6.20% during the projected period. The growth of the segment can be driven by growing investments in grid modernization and electric vehicle (EV) component manufacturing. Moreover, the push towards zero-emission generation technologies mainly depends on magnetic and structural steels to facilitate performance and structural integrity.

Mild Steel Market Share,By Application, 2025(%)

| By Application | Market Share (%) |

| Building & Construction | 36.00% |

| Automotive | 16.00% |

| Machinery & Equipment | 14.00% |

| Shipbuilding | 6.00% |

| Energy & Power | 9.00% |

| Railways | 5.00% |

| Consumer Goods | 8.00% |

| Agriculture | 4.00% |

| Others | 2.00% |

Distribution Channel Insight

The direct sales segment dominated the market with the largest share of 52.00% in 2025 and is expected to grow at a CAGR of 5.10% over the forecast period. The dominance of the segment can be attributed to the growing demand for smooth and large-volume supply chains coupled with the ongoing urbanization. Major market players form direct procurement contracts to ensure consistent material availability, which helps consumers to sidestep logistics delays.

The steel service centers segment held a market share of 24.00% in 2025 and is expected to grow at the fastest CAGR of 5.90% during the study period. The growth of the segment can be credited to the growing need for customized processing and localized inventory management. Also, steel service centers are crucial in bridging the gap between raw steel mills and end-users.

Mild Steel Market Share, By Distribution Channel, 2025(%)

| By Distribution Channel | Market Share (%) |

| Direct Sales | 52.00% (Dominating) |

| Steel Service Centers | 24.00% |

| Distributors & Wholesalers | 18.00% |

| Online Sales | 6.00% |

What are the Benefits of Mild Steel?

Mild steel is a highly versatile, affordable, and durable material preferred in construction and manufacturing. Its low carbon content offers exceptional malleability, high tensile strength, and better weldability, which makes it easy to cut, shape, and machine without fracturing.

The low carbon content enables electrical current to pass through smoothly without changing the structural integrity of the metal. It can be precisely and easily joined using standard welding methods without needing special preheating or expensive equipment.

Regional Analysis

How did Asia Pacific dominate the Mild Steel Market in 2025?

The Asia Pacific mild steel market size was estimated at USD 1.01 trillion in 2025 and is projected to reach USD 1.80 trillion by 2035, growing at a CAGR of 5.95% from 2026 to 2035. Asia Pacific dominated the market with a share of 61.00% in 2025 and is expected to grow at a CAGR of 4.80% over the forecast period. The dominance of the region can be attributed to the increasing product demand from the automotive, construction, and heavy machinery sectors along with the government investments in transportation networks. In addition, mild steel remains the material of choice because of its exceptional ductility, weldability, and high affordability.

") China

China

The Chinese government is heavily pumping capital into major public works, railway expansions, and green energy such as wind and solar infrastructure, which creates baseline structural steel demand. In addition, a surge in domestic and international demand for Chinese-manufactured vehicles and appliances fuels steel consumption further.

India

The integration of Industry 4.0, automation, and AI in domestic rolling mills is reducing production costs and improving product precision. Increasing incomes and domestic manufacturing pushes like the PLI scheme for specialty steel substantially increase consumption in automotive chassis manufacturing.

North America

The North America mild steel market size was estimated at USD 0.29 trillion in 2025 and is projected to reach USD 0.54 trillion by 2035, growing at a CAGR of 6.41% from 2026 to 2035.North America held a market share of 13.00% in 2025 and was expected to grow at the fastest CAGR of 5.80% over the forecast period. The growth of the region can be credited to the stringent energy-efficient building codes and huge government spending on public infrastructure. Robust domestic reshoring efforts and industrial automation demand equipment parts, heavy machinery, and sheet metal components.

United States

Major players in the country, such as United States Steel Corp., are investing billions in new mills and Electric Arc Furnaces (EAF), which aligns well with green production goals. Moreover, regional manufacturing is highly impacted by nationwide trade policies and tariffs.

Canada

Major domestic market players are shifting from traditional blast furnaces to sustainable electric arc furnaces (EAF) to hit environmental targets, propelling investment into modernized, high-quality production. To counter global tariffs and supply chain vulnerabilities, the federal government consistently supports projects that utilize Canadian-made steel.

Europe

The Europe mild steel market size was estimated at USD 0.33 trillion in 2025 and is projected to reach USD 0.60 trillion by 2035, growing at a CAGR of 6.16% from 2026 to 2035.Europe held a market share of 16.00% in 2025 and was expected to grow at a CAGR of 4.40% over the forecast period. The growth of the region can be linked to the rapid implementation of decarbonization mandates and supply chain realignments along with the shift towards green steel. Market growth is majorly reliant on customizable cutting and processing capabilities for various production demands.

Germany

Extensive investments in Germany's renewable energy targets, specifically wind turbine components, solar panel support structures, and power grid frames, are creating localized demand for structural steel and coils. Moreover, the integration of automated roll-forming, 3D modeling, and advanced metallurgical alloys is facilitating overall manufacturing efficiency.

France

An increasing shift toward modular and prefabricated steel frameworks to minimize construction times and carbon footprints is one of the major factors driving country growth. The shift to EAF production increases the industry’s reliance on electricity, which makes operations highly sensitive to energy price fluctuations.

Latin America

The Latin America mild steel market size was estimated at USD 0.11 trillion in 2025 and is projected to reach USD 0.21 trillion by 2035, growing at a CAGR of 6.68% from 2026 to 2035.Latin America held a market share of 5.00% in 2025 and was expected to grow at the fastest CAGR of 5% during the projected period. The growth of the region can be driven by the ongoing shift towards electric vehicles and lighter automotive components along with the rapid urbanization in the major countries. Moreover, growing demand for automotive structural parts is fuelling the consumption of hot-rolled and cold-rolled mild steel products.

Brazil

The costly Brazilian agricultural sector needs constant production and maintenance of farm equipment, storage silos, and transport, creating steady regional demand for steel plates, beams, and bars. Major players are increasingly investing billions into local downstream capacity, enhancing the scalability and precision of domestically manufactured steel products.

Argentina

Mild steel consumption is witnessing strong backing from local manufacturing, automotive production, and expanding energy operations. Also, major companies in the country are using Argentina's abundant renewable resources to manufacture green, sustainable products and reduce operational costs.")

Middle East & Africa

The Middle East & Africa mild steel market size was estimated at USD 0.09 trillion in 2025 and is projected to reach USD 0.18 trillion by 2035, growing at a CAGR of 7.18% from 2026 to 2035.The Middle East & Africa held a market share of 5.00% in 2025 and was expected to grow at a CAGR of 5.30% over the forecast period. The growth of the region can be attributed to the extensive smart city and infrastructure investments along with the transition towards modular construction methods. Furthermore, substantial investment by major regional players is increasing domestic steel production.

Saudi Arabia

The shift towards renewable energy needs significant mild steel fabrication for utility-scale solar and wind infrastructure. New local production hubs for the defense, automotive, and heavy machinery segments are generating flat-steel consumption streams away from conventional construction, leading to country growth soon.

UAE

The UAE government has enforced policies that encourage the use of locally sourced and produced steel. This impels domestic mills and processing hubs based in strategic manufacturing zones such as Dubai to scale their operations and fulfil regional demands.

Competitive Analysis

The market remains highly consolidated yet fiercely competitive, fuelled by strong infrastructure demand and increasing manufacturing compliance costs. Major market players are transitioning their emphasis towards electric arc furnace (EAF) manufacturing, 'green steel' investments, and localized scrap policies.

ArcelorMittal is strategically allocating capital toward high-return opportunities to drive sustainable growth. The corporation is advancing its high-quality renewable energy portfolio, scaling Electric Arc Furnace (EAF) capacity to satisfy the growing demand for low-carbon steel.

- Nippon Steel Corporation is highlighting its mild steel strategy for expanding its global production footprint, transitioning to integrated electric arc furnace (EAF) "green steel" production.(Source: cdn.arcelormittal.com )

(Source:gmk.center )

Recent Developments

- In October 2025, Steel Dynamics, Inc. introduced BIOEDGE™ and EDGE™, two new lower-embodied-carbon steel product lines designed to assist clients in meeting their greenhouse gas reduction and sustainability objectives. Both product offerings are manufactured using electric arc furnace (EAF) technology.(Source: www.prnewswire.com)

Strategic Profiles of Key Players Shaping the Mild Steel Market

| Company | Company Type / Position | Headquarters | Geographic Presence | Offerings | Key Offering / Strength |

| ArcelorMittal | Integrated Global Tier-1 Producer / Market Leader | Luxembourg | Europe, Americas, Asia, Africa | Hot-rolled, cold-rolled, and galvanized mild steel sheets, coils, and structural sections | Massive global supply chain scale and advanced automotive-grade low-carbon mild steel variants |

| China Baowu Steel Group | State-Owned Enterprise / World's Largest Steelmaker by Volume | Shanghai, China | Asia-Pacific dominance with an expanding global export footprint | Heavy mild steel plates, commercial sheets, wire rods, and structural profiles for infrastructure | Unmatched production capacity, cost-leadership, and high-volume supply reliability |

| Nippon Steel Corporation | Premium Integrated Manufacturer / Technological Innovator | Tokyo, Japan | Asia manufacturing base with joint ventures in the Americas and Europe | High-purity mild steel sheets, formable cold-rolled coils, and specialized structural steels | Superior material consistency, strict quality control, and advanced formability for manufacturing |

Other Key Players

- POSCO Holdings

- Nucor Corporation

- HBIS Group

- Ansteel Group

- Jiangsu Shagang Group

- Tata Steel Limited

- JSW Steel

Segments Covered in the Report

By Product Type

- Flat Products

- Hot-Rolled Coil (HRC)

- Cold-Rolled Coil (CRC)

- Steel Plates

- Steel Sheets

- Long Products

- Rebars

- Wire Rods

- Merchant Bars

- Structural Sections

- Pipes & Tubes

- Seamless Pipes

- Welded Pipes

- Hollow Sections

- Others

- Strips

- Flats

- Profiles

By Manufacturing Process

- Basic Oxygen Furnace (BOF)

- Electric Arc Furnace (EAF)

- Induction Furnace (IF)

By Form

- Coil

- Sheet

- Plate

- Bar

- Rod

- Pipe & Tube

- Structural Steel

By Thickness

- Up to 3 mm

- 3–6 mm

- 6–12 mm

- Above 12 mm

By Application

- Building & Construction

- Automotive

- Machinery & Equipment

- Shipbuilding

- Energy & Power

- Railways

- Consumer Goods

- Agriculture

- Others

By Distribution Channel

- Direct Sales

- Steel Service Centers

- Distributors & Wholesalers

- Online Sales

By Regions

- North America

- U.S.

- Canada

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Sweden

- Denmark

- Norway

- Asia Pacific

- China

- Japan

- India

- South Korea

- Thailand

- Latin America

- Brazil

- Mexico

- Argentina

- Middle East & Africa

- South Africa

- UAE

- Saudi Arabia

- Kuwait

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

FAQ's

Select User License to Buy

Figures (6)