Content

Base Oil Market Size and Forecast 2026 – 2035

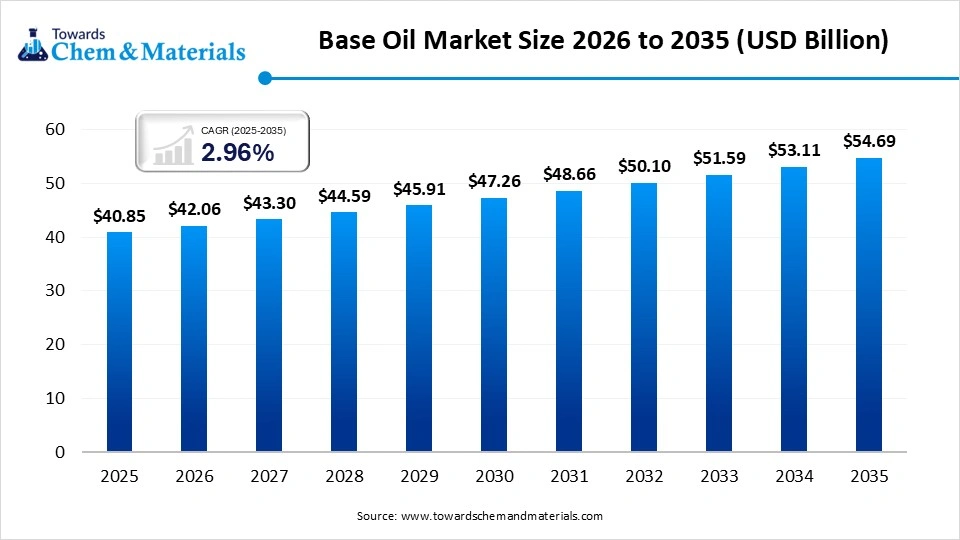

The global base oil size was estimated at USD 40.85 billion in 2025 and is expected to increase from USD 42.06 billion in 2026 to USD 54.69 billion by 2035, growing at a CAGR of 2.96% from 2026 to 2035. Asia Pacific dominated the base oil with the largest revenue share of 51.00% in 2025.The increasing demand for better lubrication and heavy oils has accelerated the industry's growth in recent years. Beyond traditional engines, we're seeing a real pivot toward bio-based oils and specialized fluids for EV thermal management. These innovations aren't just trends; they are fundamentally changing how the sector approaches long-term growth and sustainability. As Group II and III oils become the new standard, the market is moving toward a much cleaner, high-performance future

Market Highlights

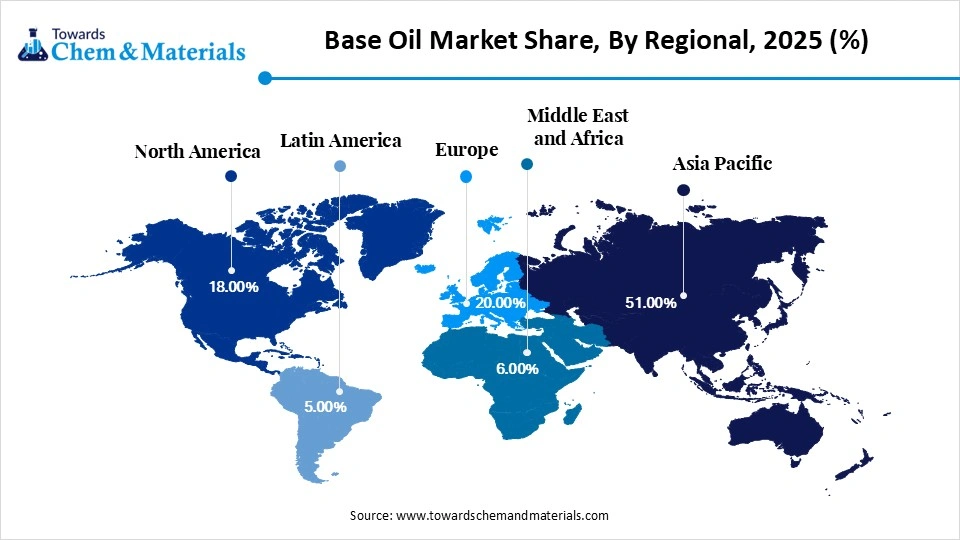

- The Asia Pacific dominated base oil market with the largest revenue share of 51.00% in 2025. due to its strong industrial growth, large transport demand, and expanding manufacturing activity.

- By region, Europe is anticipated to capture a greater portion of the market with a significant CAGR in the future due to buyers increasingly focus on oil quality machine efficiency, and long-term lubricant performance.

- By product, the group I segment dominated the market and accounted for the largest revenue share of 45.14% in 2025, owing to its being widely available and easy to produce in existing refineries, as many countries built refining systems around Group I production long ago, so industries became familiar with it.

- By product, the group V segment is expected to grow during the forecast period, due to it includes special oils designed for advanced and demanding uses.

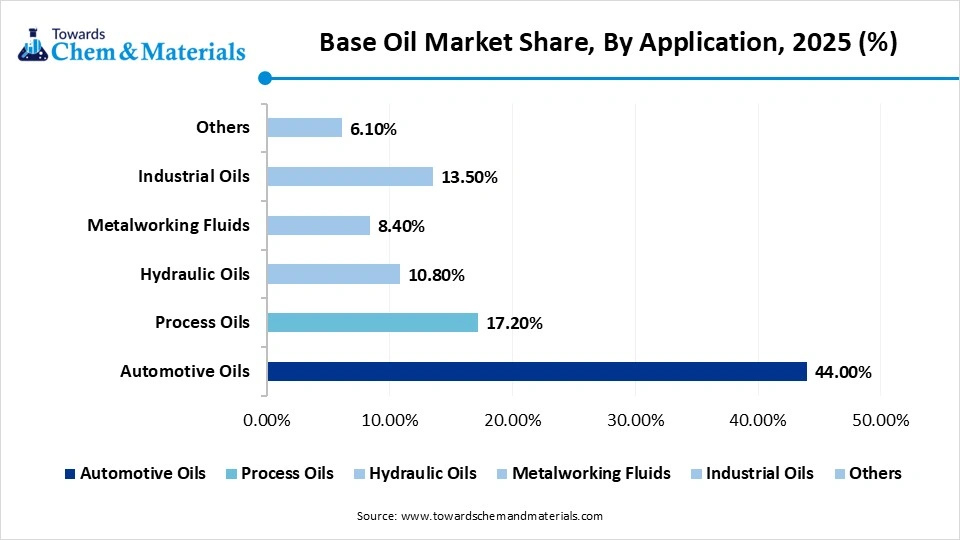

- By application, the automotive oils segment led the market with the largest revenue share of 44.00% in 2025, owing to vehicles' use of large amounts of lubricants regularly.

- By application, the process oils segment is expected to grow during the forecast period, due to many manufacturing industries expanding and using oils in their production, not only for lubrication, but also for process oil, which is used in rubber, plastics, chemicals, textiles, and many material-making operations.

Defining the Essence of Next-Generation Lubrication

The primary liquid that is used to make lubricants is known as the base oil. Also, by helping in the reduction of friction while controlling heat and protecting machinery, the base oil has allowed stakeholders to capitalize on growth opportunities in recent years. Moreover, the widespread usage in all machinery and products from the heavy industries, the base oil is likely to gain major industry attention in the coming years.

Trade Analysis of the Base Oil Market:

Import, Export, Consumption, and Production Statistics

- The world has observed the greater export of the base oil through 6,804 buyers and 5,705 exporters with 85,761 shipments. Also, these exports were done between July 2024 to June 2025 as per the published report.

- South Korea has emerged as the heavy exporter of the base oil with 35,781 shipments, while the United States (34,160 shipments) and Colombia (30,672 shipments) are actively following the exports.

- Russia has been seen in heavy import of base oil these days, with 56,049 shipments, while Vietnam (38,118) and India (36,935) are also importing a heavy amount of base oil with Russia.

Recent Market Trends:

- The replacement of the older oils with the better quality oils has positioned the industry for long-term expansion. Moreover, as engines and machines become more advanced and modern, the requirements of oil have changed from basic to pure quality oil in the past few years.

- The increased demand for long-life oils has driven the strategic transformation and sectoral scalability in the current period. Several major manufacturers are releasing long-lasting oils for the solution of frequent replacements.

- The industrial buyers are now choosing oils based on specific machine needs instead of buying one general product for everything is likely to create lucrative opportunities in the coming years. Different machines now run under different pressure, heat, and speed conditions, so oil selection has become more precise.

Report Scope

| Report Attribute | Details |

| Market Size in 2026 | USD 42.06 Billion |

| Revenue Forecast in 2035 | USD 54.69 Billion |

| Growth Rate | CAGR 2.96% |

| Forecast Period | 2026 - 2035 |

| Base Year | 2025 |

| Dominant Region | Asia Pacific |

| Segment Covered | By Product, By Application, By Region |

| Key companies profiled | CNOOC Limited, Petro-Canada Lubricants Inc., Petroleum & Chemical Corp. (SINOPEC), PETRONAS Lubricants International (PLI), Chevron Corporation, Shell plc, Indian Oil Corporation Ltd, BP p.l.c, Saudi Arabian Oil Co., Sepahan Oil, Bahrain Lube Base Oil Company, LUKOIL, SK Lubricants Co., Ltd. |

Precision Refining for Superior Oil Performance

The industry is actively shifting towards cleaner refining and more controlled molecular quality. Earlier, many oils were accepted even if their molecular structure was less uniform. Now, refining technology is designed to produce oils with more consistent molecules, which improves stability, oxidation resistance, and long-term performance. The modern base oil is becoming more engineered than before.

Supply Chain Analysis of the Base Oil Market:

Distribution to Industrial Users

- The distribution of base oil to industrial users involves a streamlined supply chain where refined stocks are transported from refineries to manufacturers and blenders via seagoing tankers, railroad tank cars, or pipelines.

- These users incorporate base oils into finished lubricants, hydraulic fluids, and greases for critical machinery.

Chemical Synthesis and Processing

- Chemical synthesis and processing of base oil involves vacuum distillation to separate heavy fractions, followed by solvent extraction or hydrocracking to remove impurities.

- Advanced hydroisomerization then rearranges molecular structures to enhance viscosity and thermal stability. These processes ensure high-purity feedstocks for manufacturing high-performance lubricants and industrial fluids.

Regulatory Compliance and Safety Monitoring

- Regulatory compliance for base oil involves adhering to REACH, TSA, and GHS standards to manage chemical risks. Safety monitoring focuses on Flash Point and VOC testing to prevent fire hazards and respiratory exposure.

- Strategic Safety Data Sheets (SDS) and spill prevention protocols ensure environmental protection and workplace safety throughout the supply chain.

Base Oil Market Regulatory Landscape: Global Regulations

| Country Region | Regulatory Body | Key Regulations | Focus Areas |

| United States | Environmental Protection Agency (EPA) | Toxic Substances Control Act (TSCA): Section 6 governs the manufacturing, processing, and distribution of chemical substances | Risk evaluation of existing chemicals, pre-manufacture notification for new substances, and strict limits on persistent, bioaccumulative, and toxic (PBT) chemicals. |

| European Union | European Chemicals Agency (ECHA). | REACH Regulation (EC) No 1907/2006: The primary framework for Registration, Evaluation, Authorisation, and Restriction of Chemicals | Ensuring high levels of protection for human health and the environment, promoting alternative testing methods, and maintaining a transparent database of all chemicals used in the EU. |

| China |

Ministry of Ecology and Environment (MEE). |

China REACH (MEE Order No. 12): Formally known as the Measures on Environmental Management of New Chemical Substances. |

Management of new chemical notifications, control of hazardous air and climate pollutants (China 6a/6b standards), and the establishment of Domestic Emission Control Areas (DECA) to limit sulfur content. |

Segmental Insights

Product Insights

How did the Group I Segment Dominate the Base Oil Market in 2025?

The group I segment dominated the market share 45.14% in 2025, due to it was widely available and easy to produce in existing refineries. Moreover, many countries built refining systems around Group I production long ago, so industries became familiar with it. It also remained popular because many industrial applications did not require very advanced oil quality. For basic lubrication needs, Group I was often good enough and affordable.

The group V segment is expected to grow with a rapid CAGR, owing to it includes special oils designed for advanced and demanding uses. Moreover, these oils are often chosen when ordinary oils cannot give enough stability, temperature control, or chemical performance. As machines become more specialized and high-performance systems become common, demand for special oils rises. Group V also supports applications where exact oil behavior matters more than cost alone.

Base Oil Market Share, By Product , 2025 (%)

| By Product | Revenue Share, 2025 (%) |

| Group I | 45.14% |

| Group II | 28.26% |

| Group III | 16.50% |

| Group IV | 5.30% |

| Group V | 4.80% |

- Group I (45.14%) Why it dominates: "Accounts for 45.14% of the market, driven by its widespread availability, cost-effectiveness, and extensive use in conventional lubricant formulations across multiple industries."

- Group II (28.26%) Why it is gaining momentum: "Holds 28.26% share, supported by increasing demand for higher purity base oils with improved performance and efficiency in modern engine oils."

- Group III (16.50%) Why it is gaining momentum: "Represents 16.50% of the market, driven by rising adoption in premium lubricants offering enhanced oxidation stability and longer service life."

- Group IV (5.30%) Why it is gaining momentum: "Accounts for 5.30% share, supported by growing use in high-performance synthetic lubricants for demanding automotive and industrial applications."

- Group V (4.80%) Why it is gaining momentum: "Captures 4.80% of the market, driven by specialized applications requiring unique properties such as biodegradability and extreme temperature performance."

Application Insights

How did the Automotive Oils Segment Dominate the Base Oil Market in 2025?

The automotive oils segment dominated the market share 44.00% in 2025, due to vehicles' regular use of large amounts of lubricants. Furthermore, the cars, trucks, buses, and commercial vehicles all need engine oil, transmission oil, and other lubricants for daily operation. Since transport exists everywhere and vehicles need repeated oil changes, this creates huge regular demand. Also, vehicle numbers increased continuously over many years, especially in developing economies.

")

The process oils segment is expected to grow with a rapid CAGR, owing to many manufacturing industries expanding and using oils in their production, not only for lubrication. Furthermore, the process oil is used in rubber, plastics, chemicals, textiles, and many material-making operations. As manufacturing becomes more specialized, process oils become more important because they directly affect product quality.

Base Oil Market Share, By Application, 2025 (%)

| By Application | Revenue Share, 2025 (%) |

| Automotive Oils | 44.00% |

| Process Oils | 17.20% |

| Hydraulic Oils | 10.80% |

| Metalworking Fluids | 8.40% |

| Industrial Oils | 13.50% |

| Others | 6.10% |

- Automotive Oils (44.00%) Why it dominates: "Accounts for 44.00% of the market, driven by high vehicle population, continuous lubricant consumption, and strong demand for engine and transmission oils."

- Process Oils (17.20%) Why it is gaining momentum: "Holds 17.20% share, supported by increasing use in rubber processing, textiles, and chemical manufacturing applications."

- Industrial Oils (13.50%) Why it is gaining momentum: "Represents 13.50% of the market, driven by expanding industrial activities and demand for reliable lubrication in machinery and equipment."

- Hydraulic Oils (10.80%) Why it is gaining momentum: "Accounts for 10.80% share, supported by growing use in construction, mining, and industrial hydraulic systems."

- Metalworking Fluids (8.40%) Why it is gaining momentum: "Captures 8.40% of the market, driven by increasing machining and manufacturing activities requiring cooling and lubrication solutions."

- Others (6.10%) Why it is gaining momentum: "Comprises 6.10% of the market, supported by diverse applications across niche and specialized lubricant uses."

Regional Insights

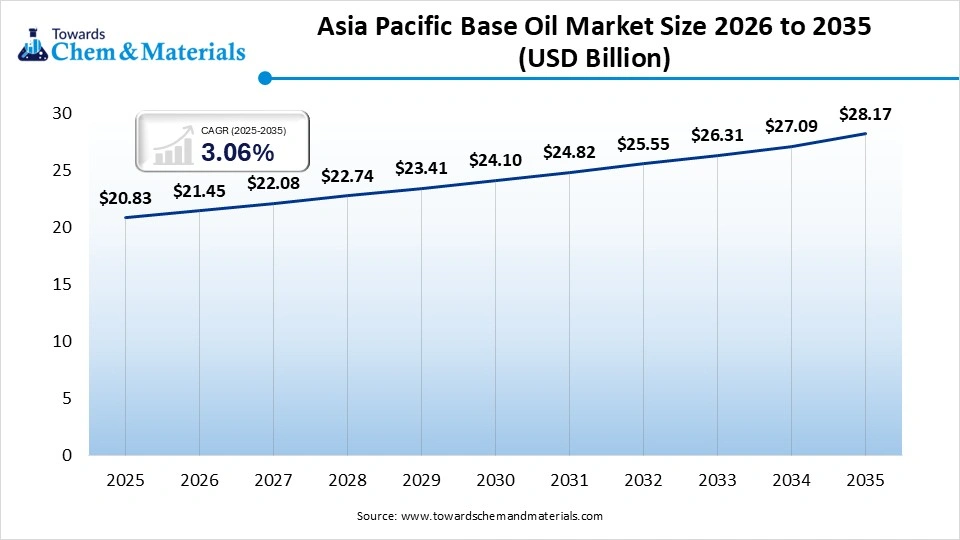

The Asia Pacific base oil market size was valued at USD 20.83 billion in 2025 and is expected to be worth around USD 28.17 billion by 2035, exhibiting at a compound annual growth rate (CAGR) of 3.06% over the forecast period from 2026 to 2035.Asia Pacific dominated the base oil market share 51.00% in 2025, due to its strong industrial growth, large transport demand, and expanding manufacturing activity. Many countries in the region have growing vehicle populations, large factories, and rising machinery use. This creates strong demand for both automotive and industrial oils. Another reason is that many manufacturing industries are concentrated here, so lubricant demand spreads across many sectors at once.

China Driving Global Base Oil Demand

China maintained its dominance in the market, owing to it combines huge manufacturing activity with large vehicle demand. The country uses large volumes of lubricants in factories, transport fleets, construction equipment, and industrial systems. Furthermore, the many products made in China require process oils during production. Also, because industrial output is very large, base oil demand stays strong across many sectors at the same time.

Base Oil Market Evaluation in Europe

Europe base oil market segment accounted for the major revenue share of 20.00% in 2025. Europe is expected to capture a major share of the base oil market with a rapid CAGR, owing to buyers there increasingly focus on oil quality machine efficiency, and long-term lubricant performance. As machines become more advanced, higher-quality oils become more important. Europe also has many industries where stable lubricant performance matters more than low price alone. This creates demand for advanced oil types and specialty oils.

Precision Performance Fuels Oil Selection in Germany

Germany is expected to emerge as a prominent country for the base oil market in the coming years, due to its strong automotive engineering and advanced industrial systems. Moreover, the many machines and engines there require precise lubrication quality. This means oil selection often depends on performance, not just availability. Germany also has strong manufacturing sectors such as machinery, automotive parts, and industrial processing, all of which use different lubricant grades.

")

North America Base Oil Market Examination

North America base oil market accounting for 18.00% of total revenue,North America is notably growing in industry, owing to many industries are upgrading equipment and paying more attention to maintenance efficiency. Buyers increasingly prefer oils that protect machines longer and reduce maintenance frequency. Also, the transport, industrial logistics, and energy-related operations still create strong lubricant demand because many sectors now focus on longer equipment life, and base oil quality becomes more important, actively supporting market growth.

Base Oil Market Share, By Regional, 2025 (%)

| Regional | Revenue Share, 2025 (%) |

| North America | 18.00% |

| Europe | 20.00% |

| Asia Pacific | 51.00% |

| Latin America | 5.00% |

| Middle East & Africa | 6.00% |

- Asia Pacific (51.00%) Why it dominates: "Accounts for 51.00% of the market, driven by strong industrial growth, high automotive production, and increasing demand for lubricants across manufacturing and transportation sectors."

- Europe (20.00%) Why it is gaining momentum: "Holds 20.00% share, supported by advanced refining capabilities and growing demand for high-quality and sustainable lubricant formulations."

- North America (18.00%) Why it is gaining momentum: "Represents 18.00% of the market, driven by steady demand from automotive and industrial sectors along with technological advancements in lubricant production."

- Middle East & Africa (6.00%) Why it is gaining momentum: "Accounts for 6.00% share, supported by expanding refining capacity and increasing industrial and transportation activities."

- Latin America (5.00%) Why it is gaining momentum: "Captures 5.00% of the market, driven by gradual growth in automotive usage and industrial development."

Transport Networks Powering the Oil Market in the United States

The United States is expected to gain a significant industry share owing to its large transport networks, industrial machinery use, and strong lubricant replacement demand. Trucks, industrial systems, manufacturing plants, and heavy equipment all use significant lubricant volumes. Also, many buyers now prefer oils that improve efficiency and reduce downtime. This keeps both basic and advanced base oils in demand across many industries. Also, the heavy trucks, industrial plants, farming equipment, logistics systems, aviation support machinery, and construction equipment all use large lubricant volumes regularly. Additionally, many buyers now prefer oils that reduce maintenance stops because machine downtime costs money.

Recent Developments

- In January 2026, Castrol India created a strategic collaboration with HPCL. Also, the main motive behind this partnership is to develop and investigate the re-refined base oil systems with the creation of a circular model for gathering, as per the company's claim.(Source: scanx.trade)

- In July 2025, Vibra introduced its latest self-branded base oil called Vibra Base Oil. Moreover, the company is likely to expand its offerings, which primarily include group III and some of the specialty base oils in the coming years.(Source: www.lubesngreases.com)

Top Vendors in the Base Oil Market & Their Offerings:

- CNOOC Limited: CNOOC Limited, a subsidiary of China National Offshore Oil Corp, is China's largest producer of offshore crude oil and natural gas. While historically focused on exploration and production, it has expanded into the downstream sector with a major base oil plant in Taizhou. This facility produces 400,000 metric tons per year of Group II-plus and 200,000 tons of naphthenic oils, supporting a strategy to increase value-added oil products.

- Petro-Canada Lubricants Inc.: Owned by HollyFrontier Corporation, Petro-Canada Lubricants operates one of the world's largest refineries in Mississauga, Ontario, with an annual capacity exceeding one billion litres. The company is renowned for producing 99.9% pure base oils using a specialized hydro-clearing process. Their portfolio includes high-margin Group III base oils and over 350 specialized lubricants distributed to more than 80 countries.

- Petroleum & Chemical Corp. (SINOPEC): SINOPEC is a dominant global force, producing over 2.4 million metric tons of Group I, II, and III base oils annually. As China's largest lubricant manufacturer, its flagship "GreatWall" series is widely used in automotive, industrial, and marine sectors. Recent strategic shifts include the 2023 launch of advanced synthetic base oils specifically tailored for electric vehicles and high-performance applications.

- PETRONAS Lubricants International (PLI): The global lubricants arm of Malaysia’s PETRONAS, PLI is a top-tier player in the premium Group III and III+ markets. It is particularly known for its ETRO+ base oil, which enhances fuel efficiency and reduces emissions. Operating in over 100 markets, PLI leverages high-paraffinic Tapis crude to produce base stocks used by the Mercedes-AMG PETRONAS Formula One Team.

- Chevron Corporation

- Shell plc

- Indian Oil Corporation Ltd

- BP p.l.c

- Saudi Arabian Oil Co.

- Sepahan Oil

- Bahrain Lube Base Oil Company

- LUKOIL

- SK Lubricants Co., Ltd.

Segments Covered in the Report

By Product

- Group I

- Group II

- Group III

- Group IV

- Group V

By Application

- Automotive Oils

- Process Oils

- Hydraulic Oils

- Metalworking Fluids

- Industrial Oils

- Others

By Region

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Asia Pacific

- China

- India

- Japan

- South Korea

- Latin America

- Brazil

- Argentina

- Middle East & Africa

- Saudi Arabia

- South Africa

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

FAQ's

Select User License to Buy

Figures (4)