Content

What is the Current Agricultural Biologicals Market Size and Share?

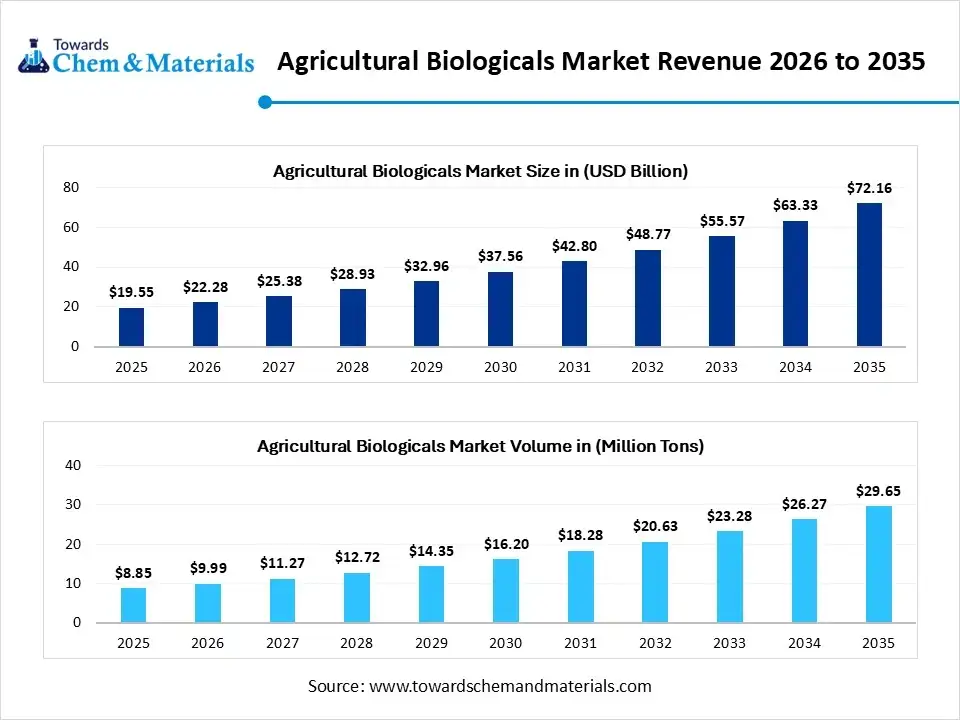

The global agricultural biologicals market size was estimated at USD 19.55 billion in 2025 and is expected to be worth around USD 72.16 billion by 2035, growing at a CAGR of 13.95% from 2026 to 2035. In terms of volume, the agricultural biologicals industry is projected to grow from 8.85 million tons in 2025 to 29.65 million tons by 2035, exhibiting a compound annual growth rate (CAGR) of 12.85% over the forecast period from 2026 to 2035. The Asia Pacific dominated the agricultural biologicals industry with the largest revenue share of 33% in 2025, reaching USD 6.45 billion, up from USD 7.35 billion in 2026. The growing demand for sustainable crop protection is the key factor driving market growth. Also, the increasing consumer demand for residue-free organic food, coupled with the stringent environmental regulations, can fuel market growth further.

The market encompasses the sector of nature-based agronomic inputs extracted from living organisms such as plants, microbes, and beneficial insects. It also includes the development, distribution, and sale of products which improve soil health, plant growth, and safeguard crops as complements or alternatives to synthetic chemicals.

These eco-friendly products leave no ecological footprint and safeguard the well-being of both farmers and consumers by mitigating the risks associated with synthetic chemicals. Furthermore, they are designed to counteract the degradation caused by historical agricultural practices, which have depleted beneficial soil microorganisms, compromised soil health, and diminished overall crop vitality. Agricultural biologicals, encompassing biopesticides, biofertilizers, and biostimulants, are frequently used with the primary objective of mitigating reliance on conventional synthetic pesticides and fertilizers.

Market Highlights

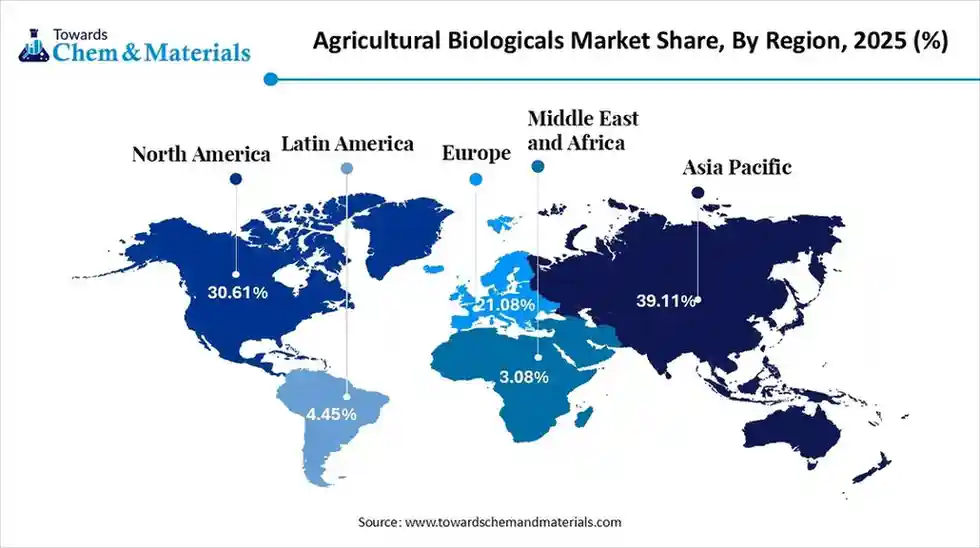

- By region, Asia Pacific dominated the market with the largest share of 33.00% in 2025 and is expected to grow at the fastest CAGR of 15.7% over the forecast period. The dominance and growth of the region can be attributed to the increasing food demand.

- By region, North America held the 27.00% market share in 2025. The growth of the region is attributed due to the growing demand for the organic food.

- By crop-type, the cereals & grains segment dominated the market with the largest share of 38.00% in 2025. The dominance of the segment can be attributed to the increasing biological input consumption across the globe.

- By crop-type, the fruits & vegetables segment is expected to grow at the fastest CAGR of 15.6% over the forecast period. The growth of the segment can be credited to the growth in organic farming, boosting product demand globally.

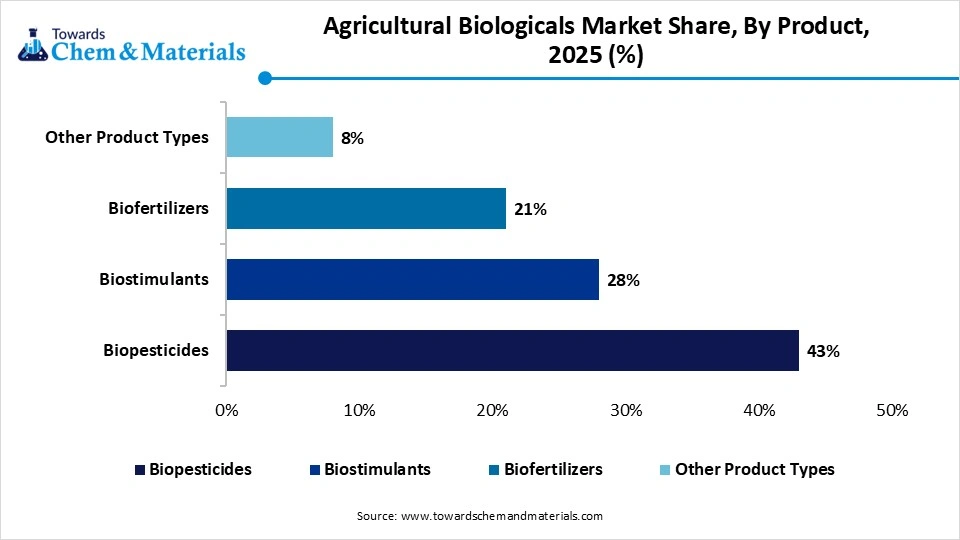

- By product, the biopesticides segment dominated the market with the largest share of 43.00% in 2025. The dominance of the segment is owing to the increasing pest resistance and growing demand for biological control products.

- By product, the biostimulants segment is expected to grow at the fastest CAGR of 15.2% over the forecast period. The growth of the segment is due to the growing demand for plant performance enhancers.

- By application method, the foliar spray segment dominated the market with the largest share of 36.00% in 2025 and is expected to grow at the fastest CAGR of 14.8% over the forecast period. The dominance and growth of the segment can be linked to the increasing foliar application demand.

Agricultural Biologicals Market Trends

- The growing emphasis on environmental sustainability is the latest trend in the market, shaping positive market growth. Due to issues about the safety of synthetic chemicals, both farmers and consumers are looking towards biological products more keenly, which in turn affects the market expansion.

- The rising incidence of resistance to pesticides in diseases and pests is a crucial factor responsible for the market growth. With the effectiveness of conventional chemical pesticides waning, there is an increasing inclination towards biological solutions among farmers.

- Major players such as Syngenta AG, Koppert Biological Systems, and Corteva Agriscience are increasingly acquiring niche biological startups to possess extensive strain libraries and global formulation assets, which is another major factor driving market growth.

Report Scope

| Report Attribute | Details |

| Market Size Value in 2026 | USD 22.28 Billion/ 9.99 Million Tons |

| Revenue Forecast in 2035 | USD 72.16 Billion/ 29.65 Million Tons |

| Growth Rate | CAGR 13.95% |

| Forecast Period | 2026 - 2035 |

| Base Year | 2025 |

| Dominant Region | Asia Pacific |

| Segments covered | By Crop-Type, By Product, By Application Method, By Regions |

| Key companies profiled | CBF China Bio-Fertilizer AG, Novozymes A/S, Mapleton Agri Biotec, Biomax, Rizobacter Argentina SA, Symborg S.L., National Fertilizers Ltd., Lallemand Inc., Agricen, Sigma Agri-Science, LLC, Agrinos Inc., and Kiwa Bio-Tech Products Group Corporation. |

How Cutting-Edge AI Technologies Are Revolutionizing the Agricultural Biologicals Market?

Advanced technologies such as AI, biotechnology, and precision agriculture are revolutionizing the market from niche alternatives to mainstream ag-inputs. These advancements can improve shelf life, fuel efficacy, and enable farmers to target specific soil and pest profiles precisely. Furthermore, next-generation sequencing is enabling agronomists to map the current soil microbiome before launching new biologicals.

Supply Chain Analysis of the Agricultural Biologicals Market

- Feedstock Procurement:It refers to the sourcing of the organic raw materials, such as plant extracts, microorganisms, and biological waste, required to produce these sustainable agricultural products.

- Major Players: Bayer AG, BASF SE

- Chemical Synthesis and Processing:It involves the technical manufacturing of biological solutions using chemical reactions and emphasizes how biochemicals, semiochemicals, and specific fermentation derivatives can be scaled, refined, and formulated.

- Major Players: BASF SE, Corteva Agriscience

- Packaging and Labeling:It refers to the specialized manufacturing, design, and regulatory compliance of containers used for biological crop inputs (like biopesticides, biostimulants, and biofertilizers).

- Major Players: Corteva, Inc, Koppert Biological Systems

- Regulatory Compliance and Safety Monitoring:It involves stringent evaluation and certification of natural crop inputs like biostimulants and biopesticides to guarantee they are safe, effective, and environmentally sound.

- Major Players: Valent BioSciences, Koppert Biological Systems

Agricultural Biologicals Market's Regulatory Landscape: Global Regulations

| Country/Region | Key Regulations |

| United States | The US lacks a unified federal definition. Products are regulated as fertilizers, plant innoculants, or soil amendments across individual states, requiring manufacturers to navigate 50 distinct state-level label approvals. |

| European Union | Regulated exactly like conventional synthetic chemicals under Regulation (EC) No 1107/2009. This involves a lengthy dual-phase review: authorization of the active substance at the EU level (EFSA), followed by zonal/national commercial authorization. |

| Brazil | The Ministry of Agriculture (MAPA), the Health Regulatory Agency (ANVISA), and the Environmental Institute (IBAMA) coordinate to fast-track biologicals. |

Market Dynamics

Driver

Surge in Organic Farming Practices

The growing adoption of organic farming is rapidly improving the market reach across the globe. Due to the transition in consumption trends towards organic produce, farmers are increasingly utilizing biological solutions for meeting certifications and enhancing output in return. In addition, this approach not only supports environmental sustainability objectives but also drives innovation in biological products, accelerating market growth further.

Restraint

Short Product Shelf Life

Living microbial formulations need specific temperature-controlled logistics, generating storage insecurities across regional distribution channels, which is the major factor hindering market growth. Biological living organisms are sensitive to field UV exposure, weather changes, and soil pH levels, which cause uneven field performance as compared to stable chemical counterparts. Moreover, biological agricultural inputs typically command a premium over conventional synthetic alternatives; targeted educational outreach is essential to demonstrating the financial return on investment to farmers.

Opportunity

Increasing Instances of Pest Infestations

The demand for safeguarding farm output from pest outbreaks and the increasing demand for better quality yields are anticipated to create lucrative opportunities in the market. Furthermore, growing concerns over the health hazards associated with chemical pesticides and evolving consumer lifestyle demands for residue-free produce are driving a substantial increase in the utilization of agricultural biologicals. Also, the market is increasingly adopting Integrated Pest Management (IPM) frameworks, successfully integrating biological products with existing agricultural and synthetic crop management strategies.

Segmental Insights

Crop-Type Insights

The cereals & grains segment dominated the market with the largest share of 38.00% in 2025. The dominance of the segment can be attributed to the increasing biological input consumption across the globe due to large cultivation acreage. Governments across the globe are promoting sustainable cereal farming and residue reduction practices. Also, farmers are increasingly adopting biologicals to enhance overall soil productivity and yield stability, leading to market growth soon.

The fruits & vegetables segment held a market share of 29.00% in 2025 and is expected to grow at the fastest CAGR of 15.6% over the forecast period. The growth of the segment can be credited to the growth in organic farming, boosting product demand globally, and the rapid adoption of residue crop protection solutions for high-value horticulture crops. Export quality standards are encouraging sustainable agriculture practices.

The oilseeds & pulses segment held a market share of 24.00% in 2025. The growth of the segment can be linked to the increasing global protein demand, expanding oilseed and pulse production, along with nitrogen-fixing biologicals strongly supporting pulse and oilseed manufacturing. Sustainable export-oriented farming increases the adoption of biological products.

The other crop types segment held a market share of 9.00% in 2025. The growth of the segment can be driven by the ongoing enforcement of soil health initiatives supporting long-term biological integration. Plantation and ornamental crop producers increase sustainable input usage. Specialty farming promotes customized biological formulation adoption.

Agricultural Biologicals Market Share, By Crop-Type, 2025 (%)

| By Crop-Type | Revenue Share, 2025 (%) |

| Cereals & Grains | 38% |

| Oilseeds & Pulses | 24% |

| Fruits & Vegetables | 29% |

| Other Crop Types | 9% |

Product Insights

The biopesticides segment dominated the market with the largest share of 43.00% in 2025. The dominance of the segment is owing to the increasing pest resistance, growing demand for biological control products, and integrated pest management practices supporting sustainable crop protection. Regulatory restrictions on synthetic pesticides can impact positive market growth.

")

The biostimulants segment held a market share of 28.00% in 2025 and is expected to grow at the fastest CAGR of 15.2% over the forecast period. The growth of the segment is due to the growing demand for plant performance enhancers due to abiotic stress management and climate variability, encouraging the adoption of crop resilience technologies.

The biofertilizers segment held a market share of 21.00% in 2025. The growth of the segment can be attributed to the soil regeneration initiatives strengthening biofertilizer consumption across the globe and government subsidies supporting sustainable nutrient management practices. Farmers are reducing chemical fertilizer dependence through microbial nutrient solutions.The other product types segment held a market share of 8.00% in 2025. The growth of the segment can be credited to the ongoing innovations in biological formulations and organic certification requirements supporting natural agriculture inputs. Botanical extracts are gaining demand in niche agriculture.

Agricultural Biologicals Market Share, By Product, 2025 (%)

| By Product | Revenue Share, 2025 (%) |

| Biopesticides | 43% |

| Biostimulants | 28% |

| Biofertilizers | 21% |

| Other Product Types | 8% |

Application Method Insights

The foliar spray segment dominated the market with the largest share of 36.00% in 2025 and is expected to grow at the fastest CAGR of 14.8% over the forecast period. The dominance and growth of the segment can be linked to the increasing foliar application demand due to rapid nutrient and biological absorption, coupled with drone spraying technologies improving overall field efficiency and precision.

The seed treatment segment held a market share of 28.00% in 2025. The growth of the segment can be driven by its cost-effective application methods, extensive farmer adoption, and improved microbial shelf stability, enhancing commercial viability. Seed-applied biologicals enhance germination and overall crop health.

The soil treatment segment held a market share of 27.00% in 2025. The growth of the segment is owing to sustainable farming practices encouraging biological soil enhancement solutions and drip irrigation compatibility, improving precision farming integration. Soil health restoration programs increase microbial soil treatment usage further.

The post-harvest segment held a market share of 9.00% in 2025. The growth of the segment is due to the increased demand for residue-free post-harvest treatment and biological preservation solutions, enhancing storage quality and shelf life. Food waste reduction initiatives prompt the adoption of biological technologies.

Agricultural Biologicals Market Share, By Application Method, 2025 (%)

| By Application Method | Revenue Share, 2025 (%) |

| Foliar Spray | 36% |

| Seed Treatment | 28% |

| Soil Treatment | 27% |

| Post-Harvest | 9% |

Regional Insights

How did Asia Pacific Dominate the Agricultural Biologicals Market in 2025?

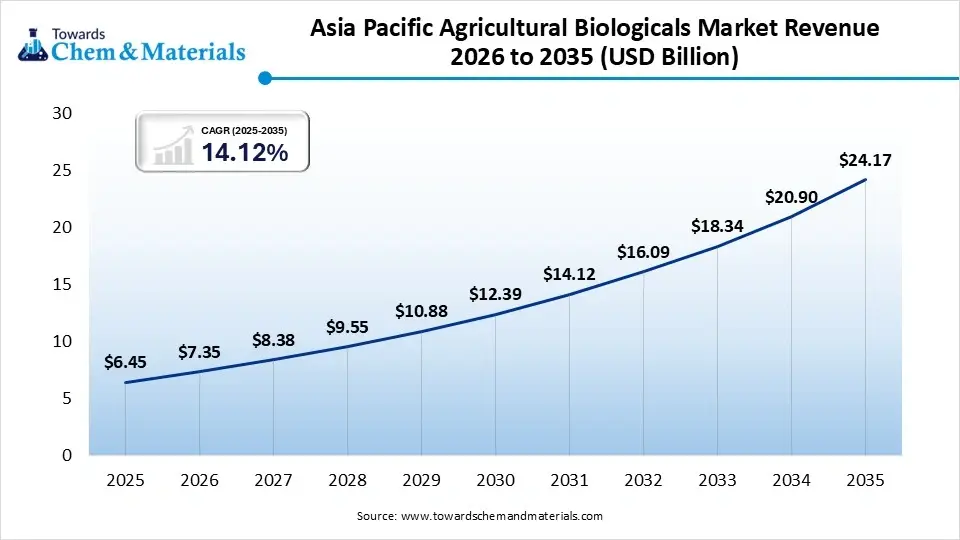

The Asia Pacific Agricultural Biologicals Market size was estimated at USD 6.45 billion in 2025 and is projected to reach USD 24.17 billion by 2035, growing at a CAGR of 14.12% from 2026 to 2035.Asia Pacific dominated the market with the largest share of 33.00% in 2025 and is expected to grow at the fastest CAGR of 15.7% over the forecast period. The dominance and growth of the region can be attributed to the increasing food demand, boosting crop productivity investments, and expanding farming practices in emerging economies. In addition, stringent export regulations on chemical residues are leading to regional expansion soon.

China

- Major companies and research institutes are using computational tools and artificial intelligence (AI) to discover functional strains and compress biological product development timelines, driving market growth.

- A surge in the middle class needs chemical-free, low-residue, and organic produce. Farmers are adopting biocontrol agents and biopesticides to ensure safety standards.

India

- Farmers are increasingly adopting biostimulants and biofertilizers to restore long-term soil fertility and revive advantageous microbial activity.

- Central and state agencies are promoting IPM programs, impelling natural biocontrol into mainstream crop protection cycles.

")

North America agricultural biologicals market size was estimated at USD 5.28 billion in 2025 and is projected to reach USD 19.84 billion by 2035, growing at a CAGR of 14.15% from 2026 to 2035.North America held a market share of 27.00% in 2025. The growth of the region can be credited to the adoption of advanced farming technologies, improving biological application efficiency and organic food demand, and supporting investments in sustainable agriculture practices. Furthermore, major market players are rapidly investing in research and strategic collaborations to commercialize highly scalable and effective biopesticides and biostimulants.

United States

- Consumer inclination towards residue-free produce is forcing retail buyers to demand sustainable practices, impelling traditional farms to incorporate biologicals into their crop protection regimens.

- Federal carbon and corporate programs reward farmers for regenerative agriculture practices; hence, biofertilizers and biostimulants are critical to these soil-health improvements.

The Europe agricultural biologicals market size was estimated at USD 4.69 billion in 2025 and is projected to reach USD 17.68 billion by 2035, growing at a CAGR of 14.19% from 2026 to 2035. Europe held a market share of 24.00% in 2025. The growth of the region can be linked to the stringent agrochemical regulations, boosting biological farming transitions and EU crop initiatives supporting sustainable farming practices. Also, major European supermarket chains are heavily demanding zero-detectable-residue, organic, and sustainable fresh produce, leading to regional growth soon.

Germany

- Consumer inclination towards organic and residue-free foods has led to a significant increase in organic cultivation land, fuelling the demand for biocontrol and biostimulant products.

- Increasing national emphasis on long-term soil health and reversing the degradation caused by chemical fertilizers fuels the need for microbial inoculants and biofertilizers.

Italy

- Ongoing innovations in microbial formulation and fermentation technologies have improved the field consistency, shelf life, and efficacy of biological products.

- Increasing consumer demand for residue-free and chemical-free food is increasingly incentivising local producers to adopt natural crop protection.

The Latin America agricultural biologicals market size was estimated at USD 1.96 billion in 2025 and is projected to reach USD 7.58 billion by 2035, growing at a CAGR of 14.48% from 2026 to 2035. Latin America held a market share of 10.00% in 2025. The growth of the region can be driven by large-scale farming operations adapting integrated biological solutions along with export-oriented agriculture, encouraging residue-free crop management. Moreover, major market players are funding regional startups specializing in biopesticides and microbes with biologicals, driving market growth shortly.

Brazil

- Brazil’s Ministry of Agriculture (MAPA) has actively optimized and fast-tracked the approval of bio-insecticidal and bio-nematicidal platforms to foster innovation.

- Brazil is among the global leaders in exporting row crops such as corn and soybeans, and farmers are adopting biologicals on a massive scale to optimize yields.

Argentina

- Large-scale commercial farms are producing grains, cereals, and soybeans to apply biofertilizers and biopesticides to maintain soil fertility.

- Farmers in emerging regions heavily depend on biocontrols and biostimulants to fulfil stringent international residue and organic standards.

The Middle East & Africa agricultural biologicals market size was estimated at USD 1.17 billion in 2025 and is projected to reach USD 4.69 billion by 2035, growing at a CAGR of 14.89% from 2026 to 2035. The Middle East & Africa held a market share of 6.00% in 2025. The growth of the region is owing to the growth in greenhouse farming, boosting biologics demand, and ongoing government security initiatives supporting soil productivity improvements. Biological alternatives provide long-term cost savings as compared to conventional synthetic chemicals, enabling farmers to reduce input costs.

Saudi Arabia

- Increasing consumer awareness regarding sustainable and chemical-free products boosts local farmers to adopt biopesticides and bio-agri inputs.

- Biofertilizers & biostimulants help crops like cereals, grains, and fruits withstand abiotic stresses.

UAE

- Agricultural biologicals are used to enhance soil health, increase water use efficiency, and build plant resilience to heat.

- The surge in modern hydroponics and advanced greenhouses in hubs like Dubai and Abu Dhabi needs sustainable and precise crop inputs suited for fertigation.

Recent Developments

- In August 2025, BioConsortia, Inc., an innovator in sustainable agricultural microbiology, secured $15 million in capital from existing investors, notably Otter Capital and its affiliates. This investment will expedite the global commercialization of Always-N™, a nitrogen-fixing seed treatment for commercial corn, and drive the expansion of the company’s R&D operations in Davis, California.(Source: www.businesswire.com)

- In May 2025, IPL Biologicals introduced six innovative soluble powder products under its new NXG Range to advance sustainable agriculture. Engineered specifically for micro-irrigation systems, these formulations support the Integrated Nutrient and Pest Management framework protocols.(Source: krishijagran.com)

Agricultural Biologicals Market Companies

- CBF China Bio-Fertilizer AG: CBF China Bio-Fertilizer AG specializes in producing and distributing microbial, bacteria-based fertilizers and agricultural biologicals within the Chinese market. Their proprietary products aim to improve soil structure, enhance nutrient uptake, and promote sustainable agriculture.

- Novozymes A/S: Novozymes A/S now operating as the biosolutions giant Novonesis following its merger with Chr. Hansen is a global pioneer in the agricultural biologicals sector. Operating a BioAg business segment, they leverage a century of biotechnology and microbial expertise to develop and supply essential biologicals to growers globally.

Other Companies in the Market

- Mapleton Agri Biotec

- Biomax

- Rizobacter Argentina SA

- Symborg S.L.

- National Fertilizers Ltd.

- Lallemand Inc.

- Agricen

- Sigma Agri-Science, LLC

- Agrinos Inc.

- Kiwa Bio-Tech Products Group Corporation

Segments Covered

By Crop-Type

-

- Cereals & Grains

- Wheat

- Rice

- Corn

- Barley

- Oilseeds & Pulses

- Soybean

- Canola

- Lentils

- Chickpeas

- Fruits & Vegetables

- Leafy Vegetables

- Tomatoes

- Citrus Fruits

- Berries

- Other Crop Types

- Plantation Crops

- Turf & Ornamentals

- Fiber Crops

- Cereals & Grains

By Product

-

- Biopesticides

- Bioinsecticides

- Biopesticides

- Bacillus thuringiensis

- Beauveria bassiana

-

- Biofungicides

-

- Trichoderma

- Bacillus subtilis

-

- Bionematicides

-

- Paecilomyces lilacinus

- Purpureocillium-based

- Biostimulants

- Seaweed Extracts

- Humic Substances

- Amino Acid-Based

- Microbial Biostimulants

- Biofertilizers

- Nitrogen Fixing

- Phosphate Solubilizing

- Potash Mobilizing

- Other Product Types

- Biological Seed Coatings

- Compost Extracts

- Botanical Extracts

- Biostimulants

By Application Method

-

- Foliar Spray

- Liquid Spray

- Drone-Based Spray

- Seed Treatment

- Seed Coating

- Seed Dressing

- Soil Treatment

- Soil Drenching

- Drip Irrigation Application

- Granular Soil Application

- Post-Harvest

- Biological Storage Protection

- Shelf-Life Enhancement Treatments

- Foliar Spray

By Region

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Asia Pacific

- China

- India

- Japan

- South Korea

- Latin America

- Brazil

- Argentina

- Middle East & Africa

- Saudi Arabia

- South Africa

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

Tags

FAQ's

Select User License to Buy

Figures (5)