Content

Polyurethane Foam Market Size, Volume, Share, Growth, Report 2026 to 2035

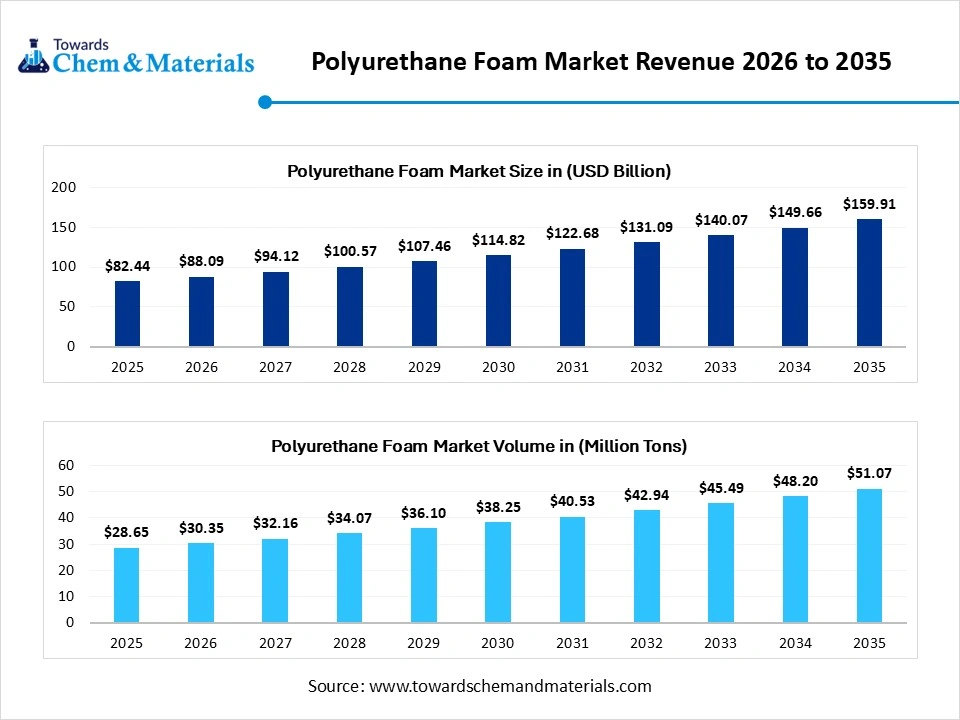

The global polyurethane foam market size was estimated at USD 82.44 billion in 2025 and is expected to be worth around USD 159.91 billion by 2035, growing at a CAGR of 6.85% from 2026 to 2035. In terms of volume, the polyurethane foam industry is projected to grow from 28.65 million tons in 2025 to 51.07 million tons by 2035, exhibiting a compound annual growth rate (CAGR) of 5.95% over the forecast period from 2026 to 2035. The heavy demand for lightweight materials and convenient packaging has accelerated the industry's growth in recent years.

Market Highlights

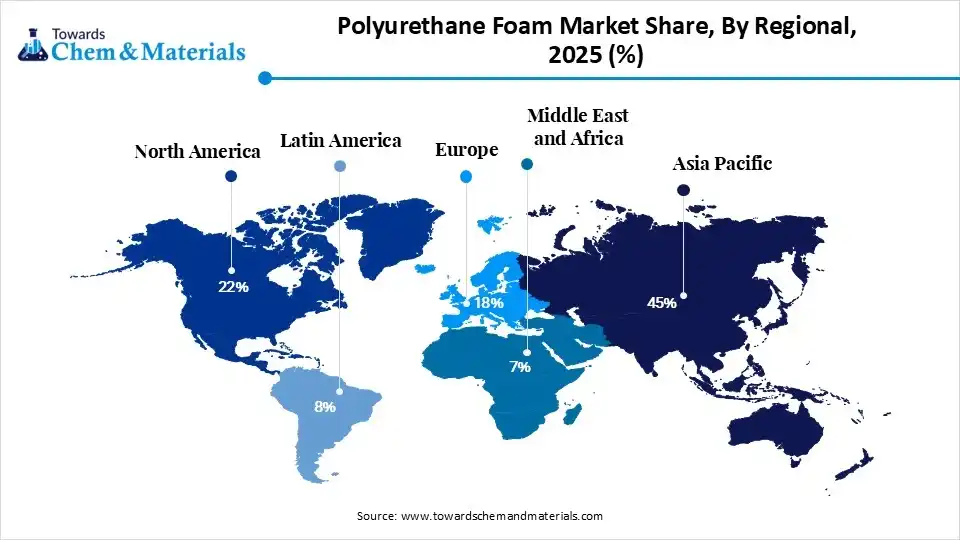

- By region, Asia Pacific dominated the market with a share of 45% in 2025 and is expected to be the fastest-growing region in the market, with a CAGR of 7.6% in the forecast period.

- By region, North America is notably growing with 22% market share in 2025.

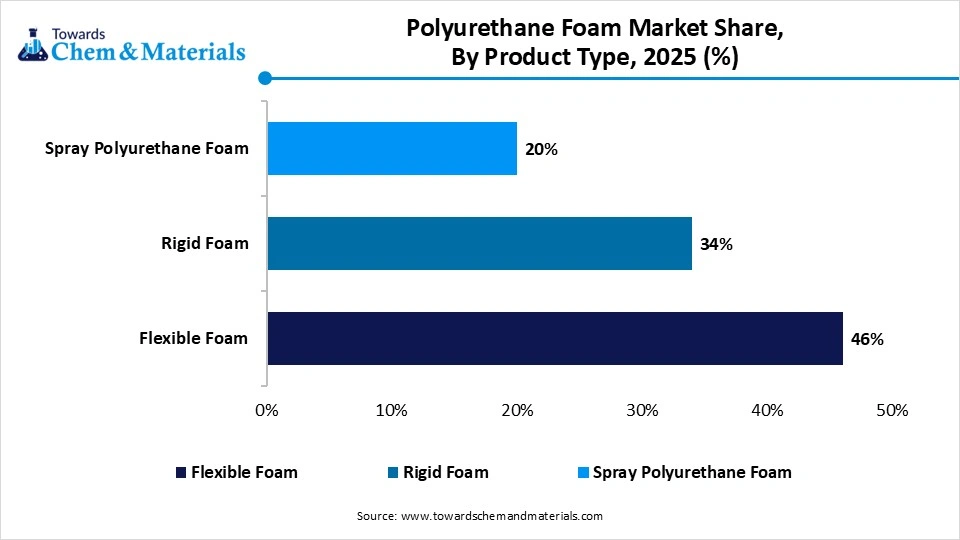

- By product type, the flexible foam segment dominated the market with 46% share in 2025.

- By product type, the rigid foam segment held the 34% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 7.2% in the forecast period.

- By raw material, the MDI segment dominated the market with 52% share in 2025 and is expected to be the fastest-growing segment in the market, with a CAGR of 7.1% in the forecast period.

- By application, the furniture and bedding segment dominated the market with 32% share in 2025.

- By application, the building and construction segment held the 27% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 7.5% in the forecast period.

- By end-use industry, the residential segment dominated the market with 48% share in 2025.

- By end-use industry, the commercial segment held the 30% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 7.0% in the forecast period in 2025.

- By density, the low-density segment dominated the market with 38% share in 2025.

- By density, the high-density segment held the 28% market share in 2025and is expected to be the fastest-growing in the market, with a CAGR of 7.3% in the forecast period.

Market Size and Volume Forecast

- Market Estimated Size (2025): USD 82.44 Billion | CAGR (2026–2035): 6.85%

- Market Projected Size (2035): USD 159.91 Billion

- Market Volume (2025): 28.65 Million Tons | Volume CAGR (2026–2035): 5.95%

- Market Projected Volume (2035): 51.07 Million Tons

- Market Pricing (2025):

- Average Manufacturing Price: USD 2,160 per ton

- Average Selling Price: USD 2,790 per ton

- Pricing CAGR (2025–2035): 3.25%

Next Generation Material for Better Living

The material, which is made by mixing two liquid chemicals that have the ability to react and expand into foams, is known as the polyurethane foam. Moreover, having major factors like lightweight, ability to trap air inside, and durability, the polyurethane foam has gained major industry attention in the past few years. Also, it's commonly seen used in sofas, refrigerators, packaging, and mattresses over the years.

Recent Market Trends:

- The heavy expansion in energy-saving building development has driven substantial financial gains in the manufacturing sector in the past few years. The polyurethane foams have been seen acting as a strong barrier against the heat flow.

- The increased usage of polyurethane foam in the automotive industry for the minimization of vehicle weight has attracted increased capital and investment in manufacturing in the current period.

- The shift towards sustainable and reusable materials is anticipated to elevate earning potential for the producers during the forecast period. Also, the major manufacturers are observed to be changing from traditional methods where the chemical usage is higher to more sustainable and lower chemical usage nowadays.

Report Scope

| Report Attribute | Details |

| Market Size and Volume in 2026 | USD 88.09 Billion / 30.35 Million Tons |

| Revenue Size and Volume Forecast in 2035 | USD 159.91 Billion / 51.07 Million Tons |

| Growth Rate | CAGR 6.85% |

| Forecast Period | 2026 - 2035 |

| Base Year | 2025 |

| Dominant Region | Asia Pacific |

| Segment Covered | By Product Type, By Raw Material, By Application, By End-Use Industry, By Density, By Region |

| Key companies profiled | The Dow Chemical Company , BASF SE , Huntsman Corporation ,Covestro AG, Wanhua Chemical Group Co., Ltd., Sekisui Chemical Co., Ltd., Saint-Gobain S.A., Recticel S.A., Rogers Corporation |

Precision Foam Engineering for Modern Applications

The industry is actively moving toward smarter and more controlled production. Also, earlier, foam was made in bulk with limited customization. Now, manufacturers use advanced machines and digital systems to control density, strength, and shape precisely. This allows them to create foam for very specific uses, such as medical support or high-performance insulation.

Supply Chain Analysis of the Polyurethane Foam Market:

Distribution to Industrial Users

- The distribution of polyurethane foam to industrial users involves a specialized supply chain focused on bulk logistics and technical support. Manufacturers provide large-scale formats like blocks or rolls directly to sectors like automotive, construction, and furniture.

- This ensures precise material specifications and cost-efficiency for high-volume production and specialized manufacturing requirements.

Chemical Synthesis and Processing

- Polyurethane foam is synthesized through the exothermic reaction of liquid polyols and diisocyanates. When mixed with catalysts and blowing agents, the chemicals react to form a cellular structure that expands rapidly.

- The resulting foam is then cured, shaped, and processed into various densities to meet specific industrial performance standards.

Regulatory Compliance and Safety Monitoring

- Regulatory compliance for polyurethane foam focuses on stringent safety standards regarding flammability, chemical emissions, and environmental impact.

- Manufacturers must adhere to REACH and OSHA guidelines, monitoring VOC levels and fire-retardant properties. Rigorous testing and regular audits ensure the material remains safe for industrial use while minimizing occupational health risks.

Polyurethane Foam Market Regulatory Landscape: Regulations

| Country Region | Regulatory Body | Key Regulations | Focus Areas |

| United States | Environmental Protection Agency (EPA) | Water Reuse Action Plan (WRAP) 2.0 (Released April 2026) | Scaling up recycling across industrial, technology, and energy sectors, including water for AI data centers and critical mineral extraction |

| Europe | European Commission (EC) |

Regulation (EU) 2020/741 on minimum requirements for water reuse (Effective June 2023). | Harmonizing water quality classes (A–D) primarily for agricultural irrigation, while also promoting circular economy goals in industrial processes. |

| China | Ministry of Ecology and Environment (MEE) | Regulations on Water Conservation (Effective May 2024) is the first national-level framework of its kind. | Targeting 25% wastewater reuse in water-scarce cities by 2025 and mandating water-saving technological upgrades for high-intensity industrial enterprises |

Market Dynamics

Driver

Comfort and Efficiency Fuel Market Expansion

The increasing demand for comfort, insulation, and lightweight materials results in an increased return on investment for manufacturers. Also, the consumer wants better mattresses, sofas, and temperature-controlled homes, which increases foam use. Growing construction activities also push demand because foam helps in insulation and energy saving. The automotive industry is another driver, as companies want lighter vehicles for better efficiency. Urbanization and rising income levels are also important, as more people can afford better-quality products.

Restraint

Sustainability Issues Restraining Foam Production

Environmental concerns related to chemicals used in foam production are expected to hamper the industry's growth during the forecast period. Also, some raw materials can release harmful gases, which creates strict government regulations. This increases production cost and slows down growth. Recycling polyurethane foam is also difficult, which creates waste management problems.

Opportunity

Green Innovations Creating Future Market Opportunities

More opportunities are in electric vehicles nowadays, where lightweight and thermal insulation materials are highly needed. Growing smart cities and energy-efficient buildings also create new demand. There is also potential in healthcare applications, such as special support foam for patients. Emerging markets offer huge growth because construction and lifestyle standards are improving quickly. The developing eco-friendly and recyclable foam is expected to create significant opportunities for manufacturers in the projected period. Also, companies that focus on green solutions aim to gain a strong market advantage.

Segmental Insights

Product Type Insights

The Flexible Foam Segment Dominated the Polyurethane Foam Market with 46% Market Share in 2025

The flexible foam segment dominated the market with 46% share in 2025, as it is widely used in daily life products like mattresses, cushions, and furniture. People need comfort and softness, which this foam provides very well. It is also easy to shape and affordable, making it suitable for mass production.

")

The rigid foam segment held the 34% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 7.2% in the forecast period, owing to its strong insulation properties. As energy saving becomes more important, industries prefer materials that reduce heat loss. Rigid foam is widely used in walls, roofs, and refrigerators for insulation.

The spray polyurethane foam segment held the 20% market share in 2025 owing to its easy application and providing excellent sealing. It expands after application and fills small gaps, which makes it very effective for insulation. It is widely used in buildings for roofs and walls to prevent air leakage.

Polyurethane Foam Market Share, By Product Type, 2025 (%)

| By Product Type | Revenue Share, 2025 (%) |

| Flexible Foam | 46% |

| Rigid Foam | 34% |

| Spray Polyurethane Foam | 20% |

Raw Material Insights

The MDI Segment Dominated the Market with 52% Market Share in 2025

The MDI segment dominated the market with 52% share in 2025 and is expected to be the fastest-growing segment in the market, with a CAGR of 7.1% in the forecast period, as it is mainly used in rigid foam production, which is highly demanded for insulation. It provides strong bonding and better thermal performance compared to other materials. It is also safer to handle compared to some alternatives, which makes it preferred by manufacturers.

The TDI segment held the 28% market share in 2025, due to it is mainly used in flexible foam production, especially for furniture and bedding. As demand for comfort products increases, the use of TDI also rises. It helps create soft and elastic foam, which is important for cushions and mattresses.

The polyols segment held the 20% market share in 2025, owing to they are a key component in all types of polyurethane foam. Demand increases automatically as foam production increases. New types of polyols are being developed to improve foam quality and reduce environmental impact. Bio-based polyols are also gaining attention because they are more sustainable.

Application Insights

The Furniture and Bedding Segment Dominated the Polyurethane Foam Market with 32% Market Share in 2025

The furniture and bedding segment dominated the market with 32% share in 2025, as they use a large amount of flexible foam. Every home, hotel, and office needs sofas, chairs, and mattresses. These products require comfort, durability, and affordability, which polyurethane foam provides. Demand is continuous because people regularly replace or upgrade furniture.

The building and construction segment held the 27% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 7.5% in the forecast period, owing to the increasing focus on energy efficiency. Polyurethane foam is used for insulation in roofs, walls, and floors. Governments are promoting green buildings, which increases demand for insulation materials. Rapid urban development also supports this growth.

The automotive segment held the 15% market share in 2025, akin to manufacturers want lightweight and comfortable vehicles. Polyurethane foam is used in seats, interiors, and insulation parts. It reduces vehicle weight, which improves fuel efficiency and battery performance in electric vehicles.

End-Use Industry Insights

The Residential Segment Dominated the Market with 48% Market Share in 2025

The residential segment dominated the market with 48% share in 2025, owing to most foam products are used in homes. Furniture, mattresses, insulation, and appliances all require polyurethane foam. As the population increases, housing demand also increases. People also focus more on comfort and energy saving in their homes.

The commercial segment held the 30% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 7.0% in the forecast period in 2025, owing to rapid growth in offices, malls, hotels, and hospitals. These buildings require large-scale insulation and furniture solutions. Energy efficiency is very important in commercial spaces because of high electricity usage.

The industrial segment held the 22% market share in 2025, owing to polyurethane foam being used in packaging, machinery insulation, and cold storage. Industries need strong and reliable materials to protect goods and maintain temperature. Foam helps in the safe transportation and storage of products.

Density Insights

The Low-Density Segment Dominated the Market with 38% Market Share in 2025

The low-density segment dominated the market with 38% share in 2025, owing to it is mainly used in furniture and bedding products. It is soft, lightweight, and cost-effective, making it suitable for mass use. It provides comfort and is widely preferred in mattresses and cushions. Since these products are used daily, demand is very high.

The medium density segment held the 34% market share in 2025 as it offers a balance between comfort and durability. It is stronger than low-density foam but still provides good softness. It is used in furniture, automotive seats, and some construction applications.

The high-density segment held the 28% market share in 2025and is expected to be the fastest-growing in the market, with a CAGR of 7.3% in the forecast period, owing to its strength and long lifespan. It is used in construction, industrial applications, and high-performance products. It can handle heavy loads and provides better insulation. As industries move toward durable and high-quality materials, demand for high-density foam increases.

Regional Insights:

How will Asia Pacific Dominate the Polyurethane Foam Market in 2025?

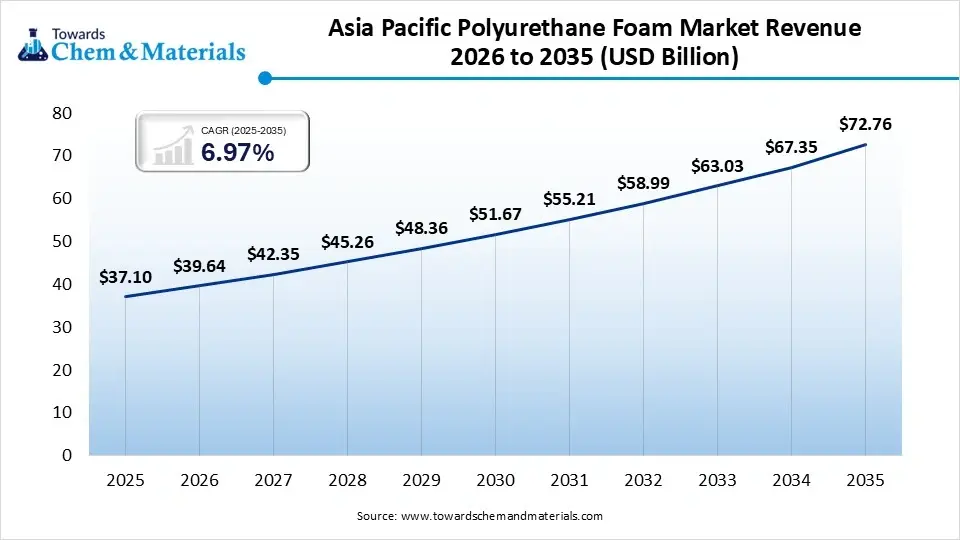

The Asia Pacific polyurethane foam market size was estimated at USD 37.10 billion in 2025 and is projected to reach USD 72.76 billion by 2035, growing at a CAGR of 6.97% from 2026 to 2035. Asia Pacific dominated the market with a share of 45% in 2025 and is expected to be the fastest-growing region in the market, with a CAGR of 7.6% in the forecast period, due to rapid industrial growth and a large population. Countries in this region have a high demand for housing, furniture, and vehicles. Construction activities are increasing quickly, which boosts foam usage. The region also has low manufacturing costs, attracting many companies. Rising income levels are improving living standards, increasing demand for comfort products.

China Dominates with Massive Production Strength

China maintained its dominance in the market, owing to its strong manufacturing base and the production of a wide range of foam products. The country has massive construction activities, including residential and commercial buildings. It is also a major producer of furniture and automotive products. Government support for industrial growth further boosts demand. China also focuses on exports, supplying foam products worldwide.

Polyurethane Foam Market Evaluation in North America

North America is notably growing with 22% market share in 2025, owing to advanced technology and a strong focus on sustainability. The region is investing heavily in energy-efficient buildings and smart infrastructure. High awareness about environmental issues is pushing demand for eco-friendly foam. Industries are adopting advanced production methods and high-performance materials.

")

Innovation Powering the United States Foam Industry Expansion

The United States is expected to emerge as a prominent country for the polyurethane foam market in the coming years, due to its advanced industries and high demand for insulation and comfort products. The country focuses on energy-efficient buildings and increasing foam usage. It also has a strong automotive and furniture market. Companies invest heavily in research and development, leading to innovation. There is also growing demand for eco-friendly materials. The construction sector is stable and continuously developing.

Recent Development

- In December 2025, BASF introduced the latest product line of spray polyurethane foam insulation called WALLTITE RSB, which is a closed-cell spray. Also, the main purpose of this product launch is to enhance sustainability in advanced construction materials and fulfil global sustainable construction material demands as per the published report.(Source: www.basf.com)

Top Vendors in the Polyurethane Foam Market & Their Offerings:

- BASF SE: BASF SE is a German chemical giant and the world’s leading chemical producer, operating in over 80 countries. It supplies critical polyols and isocyanates for flexible and rigid foams used in automotive and construction. The company focuses on sustainability through innovations like biomass-balanced polyurethane systems.

- The Dow Chemical Company: The Dow Chemical Company, an American subsidiary of Dow Inc., is a major global manufacturer of diverse chemical products. In the polyurethane sector, Dow offers tailored isocyanates, polyols, and silicone additives that enhance foam performance in bedding, footwear, and energy-efficient building insulation.

- Huntsman Corporation: Huntsman Corporation is a publicly traded American manufacturer specializing in differentiated and specialty chemicals. A global leader in MDI-based polyurethanes, it provides essential materials for energy-saving thermal insulation, lightweight automotive components, and comfort foams for furniture. The company serves over 3,000 customers worldwide.

Other Key Players

- Covestro AG

- Wanhua Chemical Group Co., Ltd.

- Sekisui Chemical Co., Ltd.

- Saint-Gobain S.A.

- Recticel S.A.

- Rogers Corporation

Segments Covered in the Report

By Product Type

- Flexible Foam

- Slabstock Foam

- Molded Foam

- High Resilience Foam

- Rigid Foam

- Spray Foam

- Boardstock Foam

- Structural Foam

- Spray Polyurethane Foam (SPF)

- Open-Cell SPF

- Closed-Cell SPF

By Raw Material

- MDI (Methylene Diphenyl Diisocyanate)

- Polymeric MDI

- Pure MDI

- TDI (Toluene Diisocyanate)

- TDI 80/20

- TDI 65/35

- Polyols

- Polyether Polyols

- Polyester Polyols

By Application

- Furniture & Bedding

- Mattresses

- Upholstery

- Building & Construction

- Insulation

- Sealants

- Roofing

- Automotive

- Seating

- Interior Components

- Electronics & Appliances

- Refrigeration Insulation

- Appliance Cushioning

- Packaging

- Protective Packaging

- Industrial Packaging

- Footwear

- Soles

- Insoles

By End-Use Industry

- Residential

- Commercial

- Industrial

By Density

- Low Density

- Medium Density

- High Density

By Region

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Asia Pacific

- China

- India

- Japan

- South Korea

- Latin America

- Brazil

- Argentina

- Middle East & Africa

- Saudi Arabia

- South Africa

FAQ's

Select User License to Buy

Figures (4)