Content

What is the Current Size and Volume of the Lithium-Ion Battery Solvent Market and Its Projected Growth?

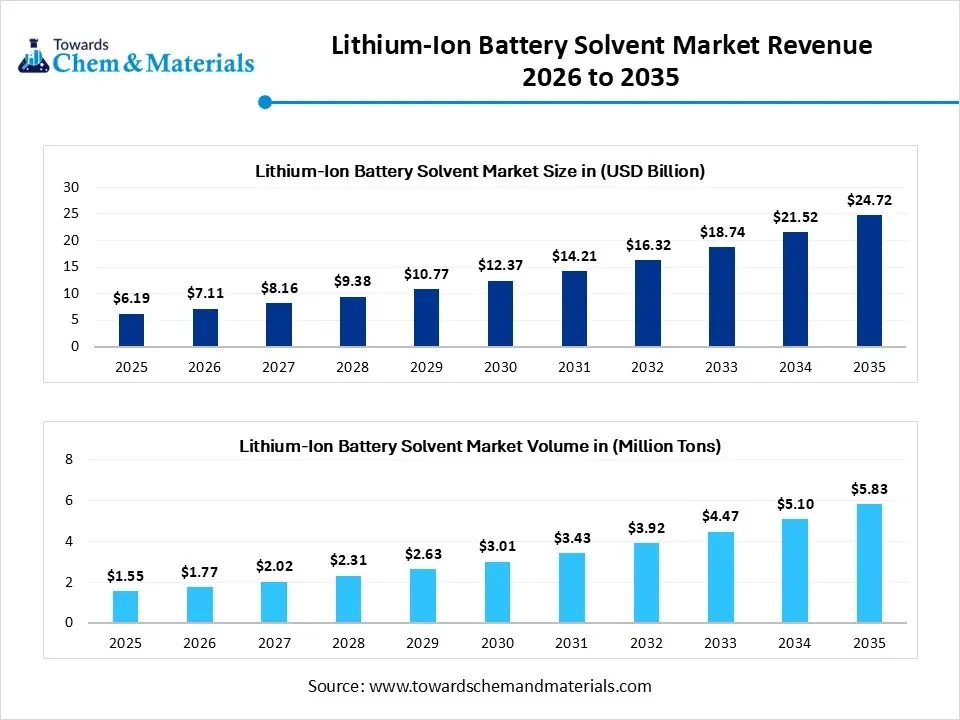

The global lithium-ion battery solvent market size was estimated at USD 6.19 billion in 2025 and is expected to increase from USD 7.11 billion in 2026 to USD 24.72 billion by 2035, growing at a CAGR of 14.85% from 2026 to 2035 Asia Pacific dominated the lithium-ion battery solvent market with the largest revenue share of 54% in 2025. In terms of volume, the market is projected to grow from 1.55 million tons in 2025 to 5.83 million tons by 2035. growing at a CAGR of 14.16% from 2026 to 2035. The rapid growth in the electric vehicle (EV) production is the key factor driving market growth. Also, ongoing innovations in battery technology coupled with the growing demand for wearable and smartphones can fuel market growth further.

Market Highlights

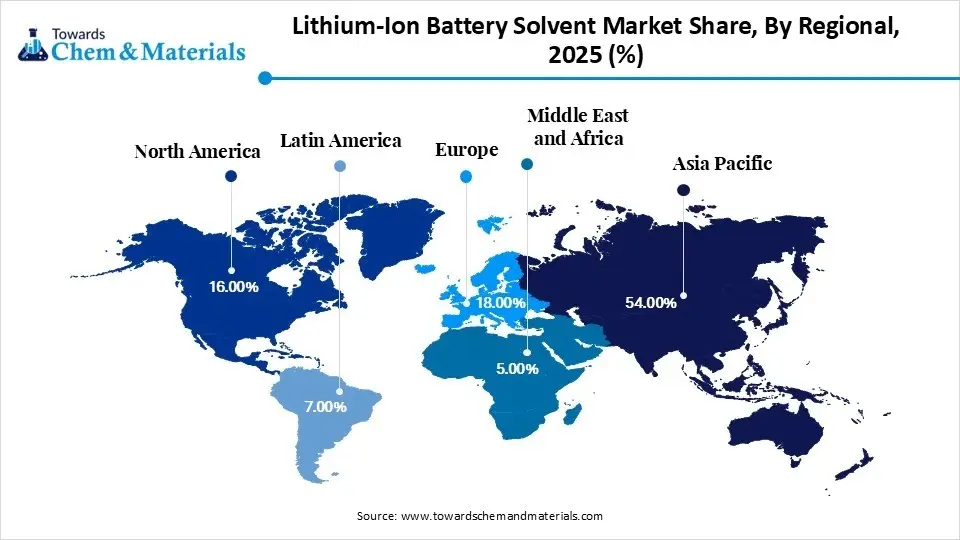

- By region, Asia Pacific dominated the market with 54% share in 2025 and is expected to sustain its position in the market with 15.8% CAGR during the forecast period. The dominance and growth of the region can be attributed to the increasing consumer electronics sales.

- By region, Europe held the second largest share of 18% in 2025 is expected to experience notable growth in the market with 14.60% CAGR during the forecast period. The growth of the region can be credited to the rapid enforcement of stringent emission regulations.

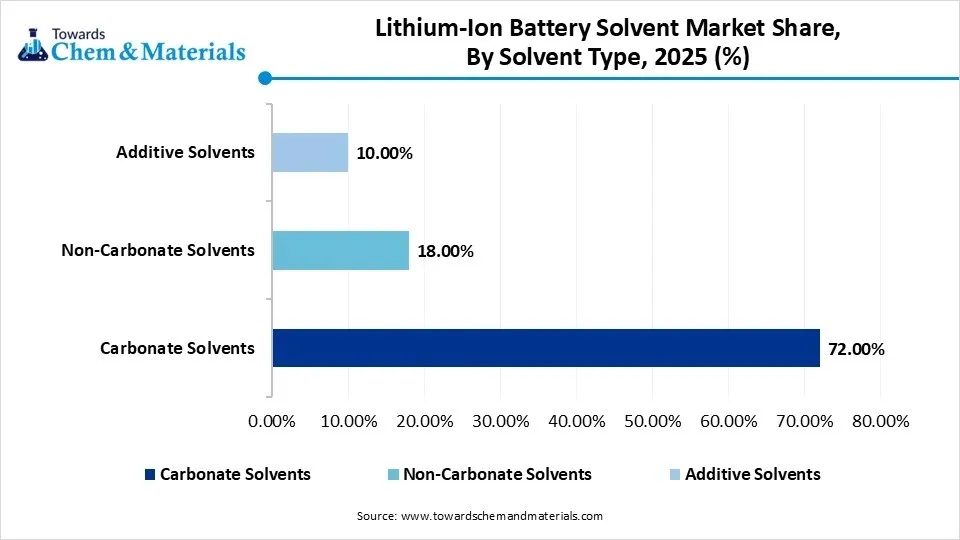

- By solvent type, the carbonate solvents segment dominated the market with 72% share in 2025. The dominance of the segment can be attributed to its key role in electrolyte performance.

- By solvent type, the non-carbonate solvents segment is expected to grow at the fastest CAGR of 15.6% over the forecast period. The growth of the segment can be credited to the increasing EV adoption globally.

- By battery chemistry, the Lithium Nickel Manganese Cobalt Oxide (NMC) segment dominated the market with 34% share in 2025. The dominance of the segment is owing to the transition towards high-nickel formulations.

- By battery chemistry, the Solid-State Lithium Batteries segment is expected to grow at the fastest CAGR of 22.4% over the forecast period. The growth of the segment can be driven by increasing demand for EVs.

- By application, the electric vehicles segment dominated the market with 52% share in 2025 and is expected to grow at the fastest CAGR of 16.8% during the forecast period. The dominance of the segment can be linked to the rising demand for high-performance batteries.

- By end user, the battery manufacturers segment dominated the market with 38% share in 2025 and is expected to grow at the fastest CAGR of 15.9% over the forecast period. The dominance and growth of the segment can be credited to the ongoing technological innovations.

What is Lithium-Ion Battery Solvent Market?

The market encompasses the manufacturing, distribution, and sale of high-grade organic compounds, mainly dimethyl carbonate (DMC), ethylene carbonate (EC), and ethyl methyl carbonate (EMC), utilised to dissolve lithium salts in battery electrolytes. There is a robust industry transition towards low-molecular-weight, high-purity, and "battery-grade" solvents with a surge in research into non-flammable and fluorinated alternatives for higher performance.

Recent Market Trends

- The growing adoption of electric vehicles across the globe is the latest trend in the market, shaping positive market growth. As many consumers are opting for electric mobility, the demand for high-quality battery solvents is increasing rapidly. This trend suggests a strong growth potential for the market, as market players strive to fulfil the demands of this sector.

- A surge in investment in renewable energy sources is driving the growth of the market. As various countries strive to shift to clean energy systems, the need for energy storage solutions is increasing. The industry is also experiencing a rise in funding for the development of battery technology, with investments expected to exceed several billion dollars in the upcoming years.

- The market is witnessing a key trend towards innovations and integration of cutting-edge electrolyte formulations, especially for high-performance batteries. The growing demand for high-performance electrolytes is boosting innovations in the energy and automotive sectors, solidifying their position in battery technology evolution.

Report Scope

| Report Attribute | Details |

| Market Size in 2026 | USD 7.11 Billion |

| Revenue Forecast in 2035 | USD 24.72 Billion |

| Growth Rate | CAGR 14.85% |

| Forecast Period | 2026 - 2035 |

| Base Year | 2025 |

| Dominant Region | Asia Pacific |

| Segment Covered | By Solvent Type, By Battery Chemistry, By Application, By Purity Level, By End User, By Region |

| Key companies profiled | UBE Corporation, OUCC, Dongwha Electrolyte, Shenzhen Capchem Technology Co., Ltd. (“Capchem”), BASF SE, Mitsubishi Chemical Corporation, Zhangjiagang Guotai Huarong New Chemical Materials Co., Ltd., Huntsman International LLC, Shandong Lixing Advanced Material Co., Ltd., Lotte Chemical |

How Cutting-Edge Technologies Are Revolutionizing the Lithium-Ion Battery Solvent Market?

Advanced technologies are transforming the market by transitioning it away from commodity-driven petrochemicals toward sustainable, high-performance, and smart formulations. Furthermore, researchers are increasingly developing solvents directly derived from biomass, which are simple, cheap, and biodegradable, providing a new frontier in sustainable battery production and contributing to market growth soon.

Trade Analysis of the Lithium-Ion Battery Solvent Market: Import & Export Statistics

- Based on 2024 U.S. import data, the total value of lithium imports reached $432.36 million. This highlights significant activity in the lithium supply chain.

During the first six months of 2025, the United States recorded a total of $205.29 million in imports for lithium cells and batteries. - From January to September 2025, China's lithium battery exports experienced significant growth, totaling USD 55.38 billion in value, a 26.75% year-on-year increase, and 3.4 billion units in volume, a 19% rise over the previous year.

- Germany has become China's top lithium-ion battery export market as of May 2025, overtaking the U.S.From January to September 2025, exports to Germany surged to USD 10.265 billion, a 29.87% year-on-year increase, representing 18.5% of China's total export value.

- In May 2025, India's lithium battery imports surged to 4,267 shipments, marking a robust 37% increase over the previous month and a 40.3% year-over-year rise compared to May 2024.

- Indian lithium battery imports surged by 24% in the year ending May 2025 (TTM), with 39,710 shipments recorded. These shipments involved 1,316 foreign suppliers and 863 verified buyers.

China, Vietnam, and Japan dominate global lithium battery exports, while Vietnam, India, and the United States lead in imports.

Lithium-Ion Battery Solvent Market Supply Chain Analysis

Feedstock Procurement

- It involves the sourcing and supply chain management of essential raw materials needed to produce high-grade battery organic solvents, and electrolyte salts.

- Major Players: BASF SE, UBE Corporation

Chemical Synthesis and Processing

- It includes the industrial manufacturing and high-grade refinement of organic carbonate solvents such as DMC, EC, and EMC that optimizes ion transport within a battery.

- Major Players: Shenzhen Capchem Technology Co., Ltd, Shandong Shida Shenghua Chemical Group

Packaging and Labelling

- It is a crucial, highly regulated process created to ensure the purity, stability, and safe transport of volatile chemical compounds utilized in the production of electrolytes.

- Major Players: Lotte Chemical, Dongwha Electrolyte

Regulatory Compliance and Safety Monitoring

- It refers to the stringent adherence to environmental, legal, and safety standards, monitoring the manufacturing, transport, and use of electrolyte solvents.

- Major Players: Arkema, BASF SE

Lithium-Ion Battery Solvent Market's Regulatory Landscape: Global Regulations

| Country/Region | Key Regulations |

| European Union (EU) | By 2026, a digital "battery passport" will be mandatory to track material origin, carbon footprint, and performance, directly affecting the solvent supply chain. |

| United States | The EPA announced a proposed rule in June 2024 to protect workers from NMP, which is linked to miscarriages and liver damage. It seeks to ban some uses and establish a Workplace Chemical Protection Program (WCPP) for others. |

| China | In late 2024, China passed its first energy law to promote carbon neutrality, further driving demand for high-performance and regulated battery materials. |

| South Korea | As of January 1, 2025, the threshold for simple notification (vs. full registration) was raised to 1 ton/year, streamlining compliance for low-volume specialty solvents. |

Segmental Insights

Solvent Type Insights

The Carbonate Solvents Segment Dominated The Market With 72% Share In 2025

The carbonate solvents segment dominated the market with 72% share in 2025. The dominance of the segment can be attributed to its key role in electrolyte performance and growing adoption of silicon-rich anodes, which require high-purity carbonate solvents. In addition, major market players are incorporating upstream to secure raw materials.

")

The non-carbonate solvents segment held the second largest share of 18% and is expected to grow at the fastest CAGR of 15.6% over the forecast period. The growth of the segment can be credited to the increasing EV adoption globally, along with the availability of sustainable electrolyte alternatives to conventional carbonates. Non-carbonate components significantly expand battery life.

The additive solvent segment held the third largest share of 10% in 2025. The growth of the segment can be attributed to the growing demand for high-purity, specialized solvents and additives that facilitate fast charging and innovative cathode chemistries. Additives also play a crucial role in improving battery safety.

Lithium-Ion Battery Solvent Market Share, By Solvent Type, 2025 (%)

| By Solvent Type | Revenue Share, 2025 (%) |

| Carbonate Solvents | 72.00% |

| Non-Carbonate Solvents | 18.00% |

| Additive Solvents | 10.00% |

- Carbonate Solvents hold the largest share of the market with a significant 72.00%. This category dominates due to its effectiveness and widespread use in lithium-ion battery production.

- Non-Carbonate Solvents account for 18.00% of the market. Their growing adoption stems from advancements in battery performance and sustainability considerations.

- Additive Solvents make up 10.00% of the market. These solvents are used to enhance the overall performance and longevity of lithium-ion batteries.

Battery Chemistry Insights

The Lithium Nickel Manganese Cobalt Oxide (NMC) Segment Dominated The Market With 34% Share In 2025

The Lithium Nickel Manganese Cobalt Oxide (NMC) segment dominated the market with 34% share in 2025. The dominance of the segment is owing to the transition towards high-nickel formulations and growth in energy storage systems. Furthermore, NMC batteries are rapidly being used in large-scale stationary storage for the integration of renewable energy.

The Solid-State Lithium Batteries segment held a 5% market share in 2025 is expected to grow at fastest CAGR of 22.4% over the forecast period. The growth of the segment is due to the rapid innovations in electric vehicles (EVs), developments in solid electrolyte materials and substantial heavy investments in scaling manufacturing.

The Lithium Iron Phosphate (LFP) segment held the second largest share of 28% in 2025. The growth of the segment can be driven by increasing adoption of LFP in electric vehicles (EVs) for high thermal safety and cost efficiency, coupled with its better lifecycle compared to nickel-based batteries.

The Lithium Cobalt Oxide (LCO) segment held the third largest share of 14% in 2025. The growth of the segment can be linked to the growing need for high-energy-density batteries in consumer electronics like laptops and the rising adoption in lightweight and specialized applications.

The Lithium Nickel Cobalt Aluminium Oxide (NCA) segment held the fourth largest share of 12% in 2025. The growth of the segment can be attributed to growing investment in recycling technologies to recover valuable metals and ongoing research and development in battery design techniques.

Lithium-Ion Battery Solvent Market Share, By Battery Chemistry, 2025 (%)

| By Battery Chemistry | Revenue Share, 2025 (%) |

| NMC | 34.00% |

| LFP | 28.00% |

| LCO | 14.00% |

| NCA | 12.00% |

| LMO | 7.00% |

| Solid-State Lithium Batteries | 5.00% |

- NMC (Nickel Manganese Cobalt) holds the largest market share at 34.00%. Its popularity is driven by high energy density and long cycle life in electric vehicles and consumer electronics.

- LFP (Lithium Iron Phosphate) accounts for 28.00% of the market. Its increasing adoption is attributed to its safety, thermal stability, and cost-effectiveness in various applications.

- LCO (Lithium Cobalt Oxide) has a market share of 14.00%. This chemistry is widely used in portable electronics due to its high energy density.

- NCA (Nickel Cobalt Aluminum) represents 12.00% of the market. It is favored in electric vehicle applications for its high energy output and long-lasting performance.

- LMO (Lithium Manganese Oxide) holds 7.00% of the market. Known for its excellent thermal stability and safety, it is commonly used in power tools and medical devices.

- Solid-State Lithium Batteries comprise 5.00% of the market. This technology is gaining traction due to its potential for higher energy densities and improved safety.

Application Insights

The Electric Vehicles Segment Dominated The Market With 52% Share In 2025

The electric vehicles segment dominated the market with 52% share in 2025 and is expected to grow at the fastest CAGR of 16.8% over the forecast period. The dominance and growth of the segment can be linked to the rising demand for high-performance batteries coupled with the ongoing innovations in battery chemistry. The transition towards solid-state electrolyte components also impacts positive market growth.

The consumer electronics segment held the second-largest share of 21% in 2025. The growth of the segment is due to growing demand for laptops, smartphones, and wearables, which necessitate compact and high-performance batteries. Increasing focus on safety standards is also contributing to positive market expansion.

The energy storage systems segment held the third largest share of 17% in 2025. The growth of the segment is attributed to increasing demand for renewable energy storage systems (ESS) along with the rising battery energy safety and density. Growing demand for residential and off-grid storage improves overall energy independence.

The industrial applications segment held the fourth largest share of 10% in 2025. The growth of the segment can be credited to growing demand for high-performance solvents, like EMC and DMC, to enhance battery efficiency and ionic conductivity. Also, the ongoing transition towards renewable energy sources fuels segment growth further.

Lithium-Ion Battery Solvent Market Share, By Application, 2025 (%)

| By Application | Revenue Share, 2025 (%) |

| Electric Vehicles | 52.00% |

| Consumer Electronics | 21.00% |

| Energy Storage Systems | 17.00% |

| Industrial Applications | 10.00% |

- Electric Vehicles dominate the market with a share of 52.00%. The rapid growth of electric vehicle production is driving the high demand for lithium-ion batteries in this sector.

- Consumer Electronics account for 21.00% of the market. Lithium-ion batteries are essential in powering a wide range of portable devices such as smartphones, laptops, and tablets.

- Energy Storage Systems hold 17.00% of the market. The growing need for renewable energy storage solutions is fueling the demand for lithium-ion batteries in this application.

- Industrial Applications make up 10.00% of the market. Lithium-ion batteries are increasingly used in industrial equipment due to their efficiency and long cycle life.

End User Insights

The Battery Manufacturers Segment Dominated The Market With 38% Share In 2025

The battery manufacturers segment dominated the market with 38% share in 2025 and is expected to grow at the fastest CAGR of 15.9% over the forecast period. The dominance and growth of the segment can be credited to the ongoing technological innovations to enhance battery range and safety, along with the increasing emphasis on faster charging.

The automotive OEMs segment held the second-largest share of 27% in 2025. The dominance of the segment can be attributed to extensive investments in new battery production facilities by major cell and OEM manufacturers and stringent environmental policies in emerging nations.

The electronics manufacturers segment held the third largest share of 20% in 2025. The growth of the segment can be attributed to the ongoing adoption of innovative consumer electronics, rapid urbanisation, and the demand for higher energy density in various sectors.

The energy storage integrators segment held the fourth largest of 15% in 2025. The growth of the segment is due to ongoing enforcement of grid modernization initiatives and the growing demand for high-performance electrolyte solvents. Major market players are increasingly developing high-voltage solvents.

Lithium-Ion Battery Solvent Market Share, By End User, 2025 (%)

| By End User | Revenue Share, 2025 (%) |

| Battery Manufacturers | 38.00% |

| Automotive OEMs | 27.00% |

| Electronics Manufacturers | 20.00% |

| Energy Storage Integrators | 15.00% |

- Battery Manufacturers lead the market with a share of 38.00%. They play a crucial role in producing the lithium-ion batteries that power various industries and applications.

- Automotive OEMs (Original Equipment Manufacturers) account for 27.00% of the market. Their demand for high-performance batteries is driven by the expansion of electric vehicle production.

- Electronics Manufacturers hold 20.00% of the market. They are key drivers of the lithium-ion battery market, particularly for portable consumer electronics like smartphones and laptops.

- Energy Storage Integrators make up 15.00% of the market. Their focus on integrating lithium-ion batteries into large-scale energy storage systems contributes to their share in the market.

By Purity Level

The Lithium-Ion Battery Solvent Market is segmented into three key purity levels: Battery Grade, Industrial Grade, and Technical Grade. Among these, Battery Grade solvents hold the dominant position, driven by their high demand in the production of lithium-ion batteries used in electric vehicles, consumer electronics, and renewable energy storage. This segment benefits from stringent quality standards and high performance, making it the preferred choice for battery manufacturers.

On the other hand, the Industrial Grade segment is witnessing the fastest growth, as increasing industrial applications of lithium-ion batteries in sectors like automotive and power storage require solvents that offer a balance of cost and efficiency. Technical Grade solvents, while important, cater to niche applications with more specific performance needs. The growth in the Industrial Grade segment is particularly fueled by the rapid expansion of electric vehicle production and the adoption of advanced battery technologies, driving an increasing demand for solvents that support large-scale manufacturing processes.

Lithium-Ion Battery Solvent Market Share, By Purity Level, 2025 (%)

| By Purity Level | Revenue Share, 2025 (%) |

| Battery Grade | 68.00% |

| Industrial Grade | 20.00% |

| Technical Grade | 12.00% |

- Battery Grade dominates the market with a significant share of 68.00%. This high-purity solvent is essential for the production of reliable and efficient lithium-ion batteries.

- Industrial Grade accounts for 20.00% of the market. These solvents are used in various industrial applications but are not as high-purity as battery-grade solvents.

- Technical Grade holds 12.00% of the market. While commonly used in certain technical applications, it has a lower purity level compared to battery-grade solvents, making it suitable for less demanding uses.

Regional Insights

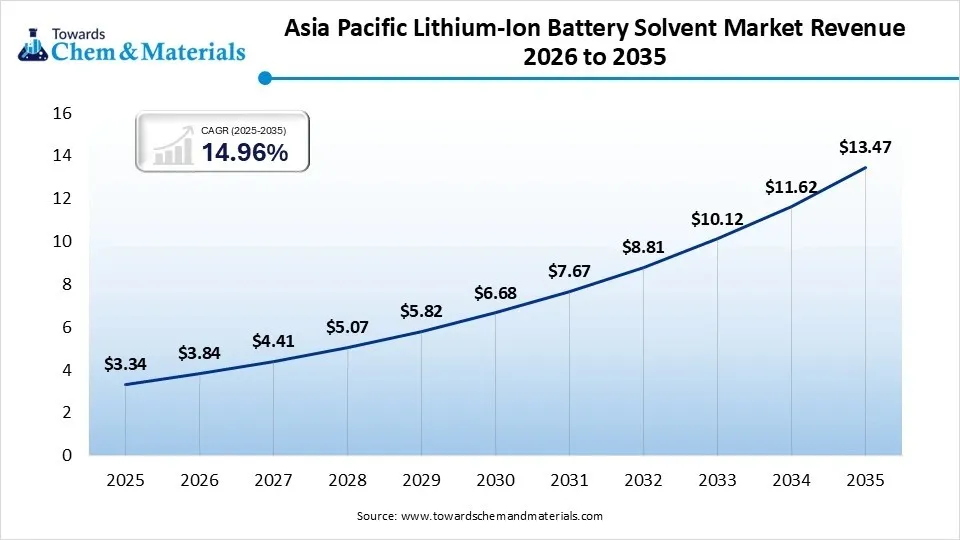

The Asia Pacific lithium-ion battery solvent market size was valued at USD 3.34 billion in 2025 and is expected to be worth around USD 13.47 billion by 2035, exhibiting at a compound annual growth rate (CAGR) of 14.96% over the forecast period from 2026 to 2035.Asia Pacific dominated the market with 54% share in 2025 and is expected to sustain its position in the market with 15.8% CAGR during the forecast period. The dominance and growth of the region can be attributed to the increasing consumer electronics sales and ongoing technological innovations in battery chemistry, along with effective regional policies. In addition, the ongoing deployment of energy storage systems to promote wind and solar power is propelling market expansion further.

China Lithium-Ion Battery Solvent Market Trends

In the Asia Pacific, China dominated the market owing to the growing demand for electrolyte components such as ethylene carbonate (EC) along with the robust integrated domestic supply chain. Also, ongoing enforcement of green energy initiatives and environmental regulations in the country supports the adoption of sustainable, safe, and high-performance battery materials.

Europe Lithium-Ion Battery Solvent Market Trends

Europe held the second largest share of 18% in 2025 is expected to experience notable growth in the market with 14.60% CAGR during the forecast period. The growth of the region can be credited to the rapid enforcement of stringent emission regulations, extensive EV adoption, and the growth of regional battery gigafactories. Furthermore, market players in the region are increasingly adopting Ethylene Carbonate (EC) for its ability to improve ionic productivity, leading to regional expansion soon.

")

Germany Lithium-Ion Battery Solvent Market Trends

The growth of the market in the country is due to its strong automotive production base and growing investments in battery cell manufacturing facilities. Moreover, favorable government regulations, subsidies, and tax credits optimise EV uptake, creating a preferred environment for the domestic lithium-ion supply chain.

Lithium-Ion Battery Solvent Market Share, By Regional, 2025 (%)

| Regional | Revenue Share, 2025 (%) |

| Asia-Pacific | 54.00% |

| Europe | 18.00% |

| North America | 16.00% |

| Latin America | 7.00% |

| Middle East & Africa | 5.00% |

- Asia-Pacific leads the Lithium-Ion Battery Solvent Market with a dominant 54.00% share, driven by the rapid growth in electric vehicle production, consumer electronics, and energy storage systems in key markets such as China, Japan, and South Korea.

- Europe holds a 18.00% share of the market, supported by strong demand for lithium-ion batteries in electric vehicles and renewable energy storage, as well as government initiatives promoting sustainable energy solutions.

- North America represents 16.00% of the market, driven by the growing electric vehicle industry and advancements in energy storage technology, particularly in the United States and Canada.

- Latin America accounts for 7.00% of the market share, with increasing investments in renewable energy and electric mobility, although the market is still in its early stages compared to other regions.

- Middle East & Africa contributes 5.00% of the market, with growth influenced by emerging energy storage and electric vehicle adoption trends, though the overall market remains relatively small.

Recent Developments

- In January 2026, Chinese chemical supplier Capchem Technology announced plans to invest USD 260 million in a new lithium-ion battery electrolyte solvent plant in Saudi Arabia. Additionally, the company will invest up to CNY 200 million (~USD 28.6 million) to expand production capacity at its existing electrolyte plant in Poland.(Source: www.yicaiglobal.com)

- In December 2025, Bristol-based battery tech firm Anaphite secured £1.4 million in Series A follow-on funding to advance its dry electrode coating technology. By removing the need for solvents and energy-intensive drying, this process aims to reduce EV battery production costs and carbon emissions.(Source: zagdaily.com)

Lithium-Ion Battery Solvent Market Companies

- UBE Corporation: UBE Corporation is a major player in the lithium-ion battery (LIB) solvent and electrolyte market, specializing in high-purity dimethyl carbonate (DMC) and ethyl methyl carbonate (EMC).

- OUCC: OUCC (Oriental Union Chemical Corporation), a prominent Taiwanese chemical manufacturer, is a key player in the global lithium-ion battery (LIB) solvent market. The company is actively involved in the production of high-purity carbonate solvents.

- Dongwha Electrolyte: Dongwha Electrolyte is a major South Korean manufacturer of high-performance lithium-ion battery electrolytes, established via the 2019 acquisition of Panax Etec. It is a key player in the global market, expanding its footprint through production facilities in various countries.

- Shenzhen Capchem Technology Co., Ltd. (“Capchem”)

- BASF SE

- Mitsubishi Chemical Corporation

- Zhangjiagang Guotai Huarong New Chemical Materials Co., Ltd.

- Huntsman International LLC

- Shandong Lixing Advanced Material Co., Ltd.

- Lotte Chemical

Segments Covered in the Report

By Solvent Type

- Carbonate Solvents

- Cyclic Carbonates

- Ethylene Carbonate (EC)

- Propylene Carbonate (PC)

- Linear Carbonates

-

- Dimethyl Carbonate (DMC)

- Diethyl Carbonate (DEC)

- Ethyl Methyl Carbonate (EMC)

-

- Cyclic Carbonates

- Non-Carbonate Solvents

- Esters

- Ethers

- Fluorinated Solvents

- Additive Solvents

- Film-Forming Additives

- Flame-Retardant Solvents

- High-Voltage Stabilizers

By Battery Chemistry

- Lithium Iron Phosphate (LFP)

- Lithium Cobalt Oxide (LCO)

- Lithium Nickel Cobalt Aluminum Oxide (NCA)

- Lithium Manganese Oxide (LMO)

- Solid-State Lithium Batteries

By Application

- Electric Vehicles (EVs)

- Passenger EVs

- Commercial EVs

- Two & Three Wheelers

- Consumer Electronics

- Smartphones

- Laptops & Tablets

- Wearables

- Energy Storage Systems (ESS)

- Grid Storage

- Residential Storage

- Commercial Storage

- Industrial Applications

- Power Tools

- Medical Devices

- Aerospace & Defense

By Purity Level

- Battery Grade

- Industrial Grade

- Technical Grade

By End User

- Battery Manufacturers

- Automotive OEMs

- Electronics Manufacturers

- Energy Storage Integrators

By Region

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Asia Pacific

- China

- India

- Japan

- South Korea

- Latin America

- Brazil

- Argentina

- Middle East & Africa

- Saudi Arabia

- South Africa

FAQ's

Select User License to Buy

Figures (4)