Content

What is the Forestry Lubricants Market Size and Share?

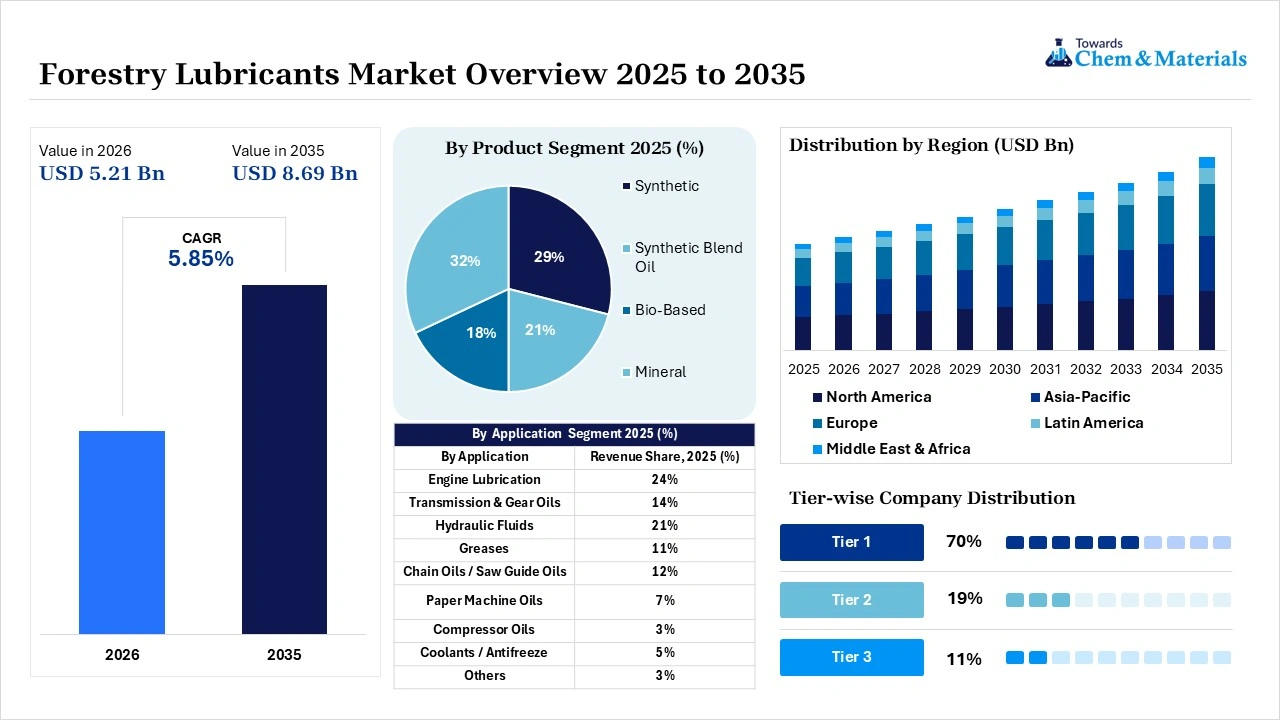

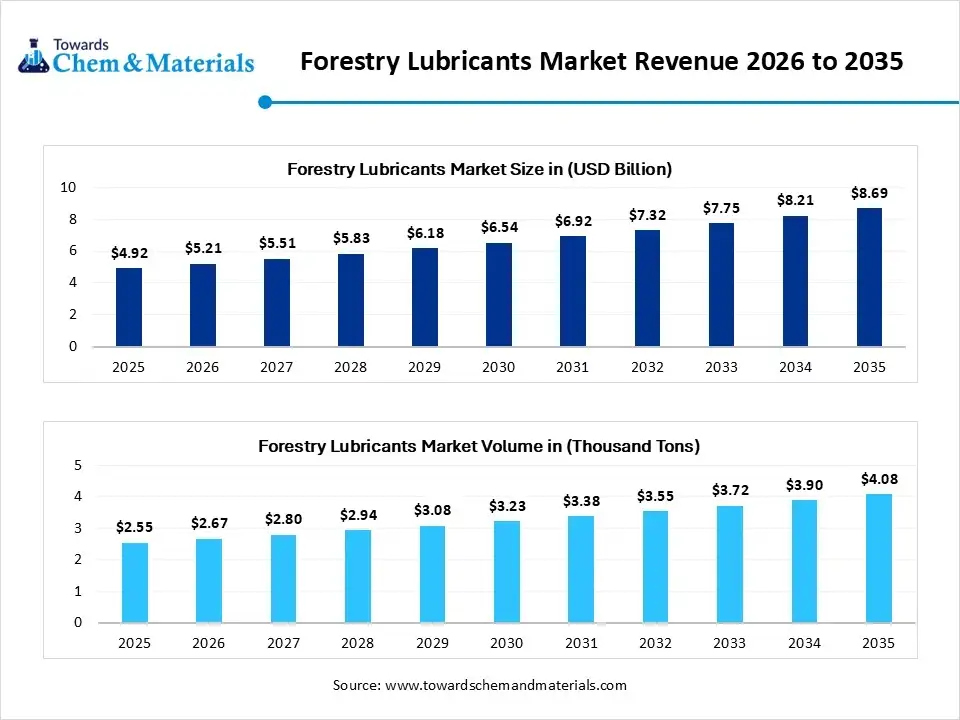

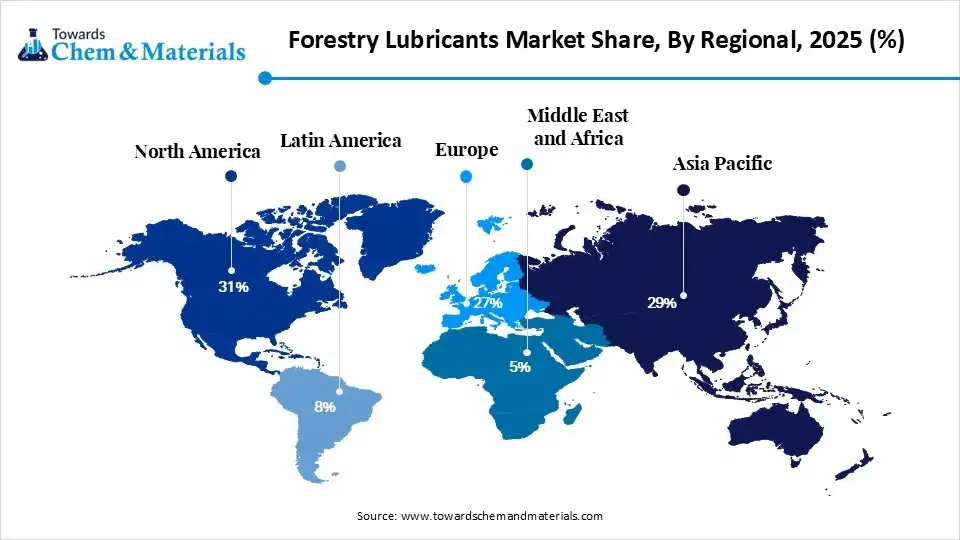

The forestry lubricants market size was valued at USD 4.92 billion in 2025, is estimated to reach USD 5.21 billion in 2026, and is projected to reach USD 8.69 billion by 2035, exhibiting a compound annual growth rate (CAGR) of 5.85% over the forecast period from 2026 to 2035.North America dominated the forestry lubricants market with the largest revenue share of 31% in 2025 and is expected to grow at the fastest CAGR of 6.00% during the forecast period. In terms of volume, the forestry lubricants market is projected to grow from 2.55 million tons in 2025 to 4.08 million tons by 2035. growing at a CAGR of 4.82% from 2026 to 2035.

The growth is propelled by rising mechanization of logging, stringent environmental regulations favoring biodegradable fluids, and OEM requirements for high-performance synthetics that minimize equipment downtime. Stricter mandates, government investments, due to the high cost of heavy machinery through major players like Shell, Chevron, and ExxonMobil, are driving growth, according to the latest reports.

The growth is propelled by rising mechanization of logging, stringent environmental regulations favoring biodegradable fluids, and OEM requirements for high-performance synthetics that minimize equipment downtime. Stricter mandates, government investments, due to the high cost of heavy machinery through major players like Shell, Chevron, and ExxonMobil, are driving growth, according to the latest reports.

Market Highlights

- By region, North America dominated the market with a share of 31% in 2025. Large commercial forestry operations support lubricant demand.

- By region, Asia Pacific held 29% market share in 2025 and is expected to experience the fastest growth with a CAGR of 6.80% in the forecast period. Expanding forestry activities increases equipment utilization.

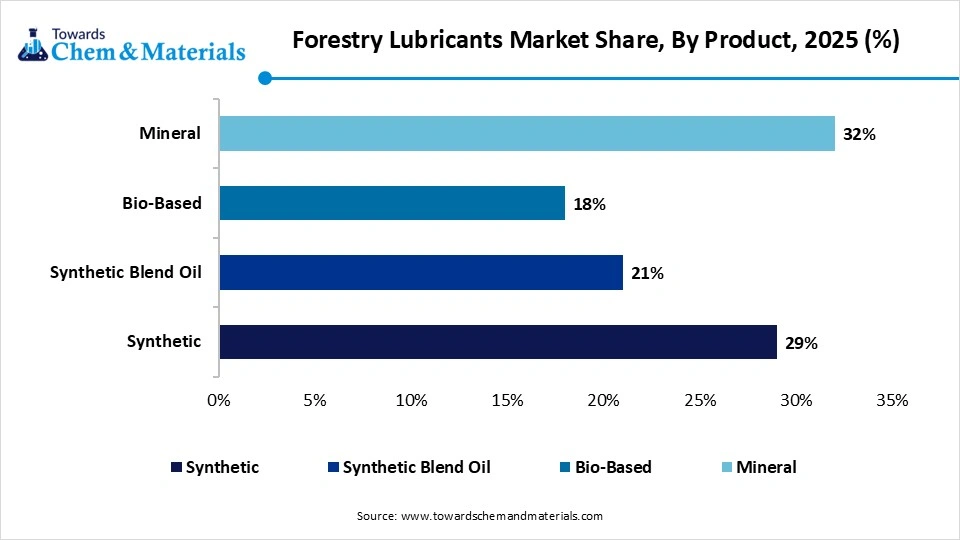

- By product, the mineral segment dominated the market with 32% share in 2025. Remains cost-effective for large-scale forestry operations.

- By product, the bio-based segment held 18% market share in 2025 and is expected to have the fastest growth with a CAGR of 7.8% in the forecast period. Environmental regulations promote biodegradable lubricants.

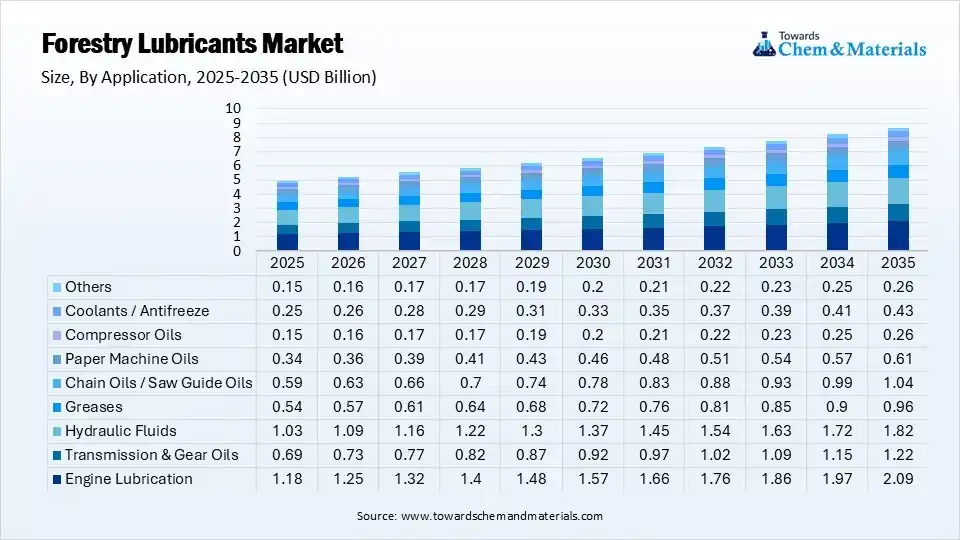

- By application, the engine lubrication segment dominated the market with 24% share in 2025. Heavy-duty forestry engines require continuous lubrication.

- By application, the hydraulic fluids segment held 21% market share in 2025 and is expected to have the fastest growth with a CAGR of 6.50% in the forecast period. Hydraulic systems dominate forestry equipment functions.

- By end use, the logging/harvesting companies segment dominated the market with 22% share in 2025. Harvesting equipment operates under severe conditions.

- By end use, the forest contractors/operators segment held 7% market share in 2025 and is expected to have the fastest growth with a CAGR of 6.7% in the forecast period. Outsourced forestry services continue expanding.

Quick Stats at a Glance

- Market Estimated Size (2025): USD 711.19 Million | CAGR (2026–2035): 5.95%

- Market Projected Size (2035): USD 1,267.64 Million

- Asia Pacific: Revenue Share of 48% in 2025|USD 341.37 Million

- Market Estimated Volume (2025): 486.11 Thousand Tons | Volume CAGR (2026–2035): 5.25%

- Market Projected Volume (2035): 810.88 Thousand Tons

- Market Pricing (2025):

- Average Manufacturing Price (2025): USD 1,330/Ton

- Average Selling Price (2025): USD 1,860/Ton

- Pricing CAGR (2026–2035): 2.45%

Market Overview

Forestry Lubricants Market Growth Aligning with Environmental Conditions

The forestry lubricants market plays a crucial role in supporting heavy machinery used in logging, sawmilling, and paper manufacturing. These specialized fluids reduce friction, prevent wear under harsh environmental conditions, decrease maintenance expenses, and are designed to be biodegradable to protect waterways. Growing global demand for timber and increased automation in equipment drive companies like Shell, ExxonMobil, and TotalEnergies to develop advanced synthetic and nanotech lubricants.

- For instance, STIHL develops specialty lubricants for chainsaws and forestry harvesting equipment. These lubricants reduce chain wear, improve cutting efficiency, and support equipment durability in harsh forest environments.(Source: stihlusa.com)

The industry is increasingly adopting Environmentally Acceptable Lubricants (EALs), with a shift toward bio-based oils to avoid soil and water pollution during sensitive logging activities. In Europe and North America, strict environmental regulations are accelerating the transition to biodegradable lubricants. Heavy-duty equipment such as harvesters, skidders, and chainsaws requires high-quality lubricants to maximize lifespan and performance while safeguarding against dust, moisture, and temperature variations.

- For instance, FUCHS Group supplies biodegradable hydraulic lubricants for forestry machinery. The products minimize environmental contamination risks in sensitive forest and agricultural areas.(Source: www.fuchs.com)

Global Investment Flow for Forestry Lubricants 2026

Global investments in the forestry lubricants market are increasingly directed toward biodegradable and bio-based lubricants due to stricter environmental regulations and sustainable forestry practices.

- For instance, Market leaders Indian Oil Corporation Ltd (Servo Lubricants) and Hindustan Petroleum Corporation Limited (HP Lubricants) are expanding high-performance industrial and equipment oils to match the rapid modernization of logging machinery in regional mills

Europe is attracting significant investment in environmentally acceptable lubricants, supported by strong ESG policies and regulations limiting petroleum-based lubricant usage in forest operations.

Major lubricant manufacturers like ExxonMobil, Shell, TotalEnergies, and Chevron are investing in R&D for advanced additive technologies, extended-drain synthetic oils, and vegetable-oil-based lubricants to improve efficiency and sustainability.

Strategic partnerships between forestry equipment manufacturers and lubricant producers are increasing globally to develop customized lubrication solutions for harvesters, chainsaws, skidders, and biomass processing equipment.

Forestry Lubricants Market Trends

- Eco-friendly Bio-lubricants:Stricter environmental regulations near waterways are pushing a massive transition toward biodegradable, bio-based base oils and ashless additives to prevent soil and water contamination.

- Mechanization of Logging:Expanded use of heavy-duty, automated machinery such as harvesters, skidders, and forwarders requires specialized oils and greases to withstand extreme pressures and hostile conditions.

- Equipment Longevity: Operators are prioritizing premium, OEM-recommended branded lubricants. Using the correct products prevents unscheduled downtime and expensive part replacements for costly machinery.

Report Scope

| Report Attributes | Details |

| Market Size and Volume in 2026 | USD 5.21 Billion / 2.67 Million Tons |

| Revenue Forecast in 2035 | USD 8.69 Billion / 4.08 Million Tons |

| Growth Rate | CAGR 5.85% |

| Base Year of Estimation | 2025 |

| Forecast Period | 2025 - 2035 |

| High Impact Region | North America |

| Segment Covered | By Product, By Application, By End Use, By Regions |

| Key Companies Profiled | Shell Plc, Kluber Lubrication, Exxon Mobil Corporation, TotalEnergies, Chevron Corporation, Frontier Performance Lubricants INC., Cortec Corporation, Repsol, Thermal-Lube Inc., Neste, Penine Lubricants, Morris Lubricants, CONDAT Group, Exol Lubricants Limited, Petro Canada Lubricants Inc., Matrix Specialty Lubricants |

Technological Shifts with Integration of AI in the Forestry Lubricants Market

The forestry lubricants market is shifting rapidly toward bio-based/biodegradable formulations and IoT-enabled smart lubrication systems to comply with strict environmental regulations and maximize machinery uptime in harsh operating conditions. Artificial Intelligence (AI) and IoT integration in the market are driving a major shift from reactive maintenance to automated, predictive, and sustainable lubrication ecosystems. This technological transformation optimizes lubricant dosing, minimizes machine downtime, and extends equipment lifespan in harsh environments.

Forestry Lubricants Regulatory Landscape

| Country / Region | Regulatory Body | Key Regulations | Focus Areas | Notable Notes |

| United States | Environmental Protection Agency (Epa); United States Department Of Agriculture (Usda) | Vessel General Permit (VGP); Environmental Protection Regulations | Biodegradable Lubricants, Environmental Safety | The U.S. Promotes Environmentally Acceptable Lubricants For Forestry And Off-Road Equipment Operating In Sensitive Ecosystems. |

| European Union | European Chemicals Agency (ECHA); European Commission | Reach Regulation; EU Ecolabel Criteria | Bio-Based Lubricants, Emissions Reduction | Europe Strongly Supports Biodegradable Forestry Lubricants To Minimize Environmental Contamination In Forestry Operations. |

| Canada | Natural Resources Canada (NRCAN); Environment And Climate Change Canada | Canadian Environmental Protection Act | Sustainable Forestry Operations, Eco-Friendly Lubricants | Canada Encourages Sustainable Lubricant Usage In Logging And Forestry Machinery. |

| Sweden | Swedish Environmental Protection Agency | Swedish Forestry And Environmental Regulations | Biodegradable Hydraulic Oils, Sustainable Forestry | Sweden Is A Leading Adopter Of Bio-Based Lubricants In Forestry Applications Due To Strong Sustainability Initiatives. |

| Finland | Ministry Of The Environment; Finnish Forest Centre | Environmental Protection Regulations | Renewable Lubricants, Forest Sustainability | Finland Promotes Low-Toxicity And Biodegradable Lubricants In Forestry Equipment. |

| Japan | Ministry Of Economy, Trade, and Industry (METI) | Industrial Safety And Environmental Standards | High-Performance Industrial Lubricants | Japan Focuses On Advanced Lubricant Formulations For Forestry And Heavy-Duty Machinery Applications. |

Supply Chain Analysis of Forestry Lubricants Market

- Lubricant Production & Blending:Forestry lubricants are produced through the blending of base oils, performance additives, and biodegradable components to provide lubrication, wear protection, and thermal stability for forestry machinery and equipment operating in harsh environments.

- Production relies on precise dosing, heating, and computerized automation to meet the stringent demands of modern logging machinery. Made via chemical reactions like polyol esters. Preferred for high-load, extreme-temperature harvesting and skidding equipment.

- Key players: Shell, ExxonMobil, Fuchs Petrolub, TotalEnergies

- Quality Testing and Certification:Forestry lubricants must comply with standards for biodegradability, viscosity, oxidation stability, wear resistance, and environmental safety for use in forestry operations.

- Quality testing and certification of forestry lubricants, such as biodegradable chain oils and hydraulic fluids, verify performance, environmental safety, and regulatory compliance. Rigorous protocols ensure equipment protection under harsh conditions while preventing soil and water contamination.

- Key players: American Petroleum Institute, International Organization for Standardization, ASTM International, European Ecolabel

- Distribution to Industrial Users:Forestry lubricants are supplied to logging companies, forestry equipment manufacturers, agricultural machinery operators, construction industries, and heavy equipment maintenance providers.

- Distribution of forestry lubricants to industrial users relies on specialized B2B supply chains moving lost-in-use products like chainsaw oils and bio-hydraulic fluids from global manufacturers like Exxon Mobil Corporation and TotalEnergies to sawmills, paperboard mills, and logging OEMs.

- Key players: Shell, ExxonMobil, Fuchs Petrolub.

Forestry Lubricants Market Dynamics

| Drivers | Restrains | Opportunities |

| Environmental Regulations & Eco-Friendly Formulations:The growing adoption of biobased and environmentally friendly products due to growing environmental regulations fuels the growth of the market. | Raw Material Price Volatility:The cost of weakening base oils and core chemical additives shifts continuously, straining the profit margins of manufacturers like Exxon Mobil Corporation and TotalEnergies. | Bio-Based & Biodegradable Formulations:Stricter environmental regulations and proximity to waterways are driving demand for readily biodegradable lubricants, bio-based base oils, and low-toxicity formulations. |

| Mechanization & High-Tech Forestry Machinery:Modern automated harvesters, forwarders, and high-torque skidders operate under intense thermal and mechanical stress, requiring high-performance synthetic fluids that can handle heavy loads. | High Compliance and R&D Costs:Developing, testing, and rolling out eco-friendly alternatives demands long-term R&D investments, which strains resources and delays product launches. | Smart Lubrication & IoT Integration:The integration of IoT, sensors, and telematics into heavy machinery allows for real-time monitoring and predictive diagnostics. |

| Total Cost of Ownership (TCO) & Efficiency:Equipment owners are prioritizing premium lubricants to prevent wear-related breakdowns and cut back on costly maintenance downtime in remote logging locations. | Intense Competition and Pricing Pressure:Because buyers have multiple equivalent options, brand switching is common and forces suppliers to compete aggressively on price, restricting revenue growth. | High-Performance Chain and Saw Guide Oils:Mechanized logging, harvesters, and forwarders require specialized heavy-duty oils and greases designed for extreme pressure and high-moisture conditions. The chain oils and saw guide oils continue to command a major portion of product-specific revenue. |

Segmental Insights

Product Insights

The mineral segment dominated the market with 32% share in 2025, due to its cost-effectiveness, easy availability, and reliable performance in heavy-duty off-road machinery like harvesters, skidders, and chainsaws. It remains the most widely used base oil grade, particularly in developing economies. The rapid rise of mechanization in forestry activities, including extensive use of harvesters and skidders, demands high-volume, dependable lubrication to prevent excess wear under strenuous loads in hostile, outdoor conditions.

")

The bio-based segment held 18% market share in 2025 and is expected to have the fastest growth with a CAGR of 7.8% in the forecast period, because forestry machinery frequently operates in ecologically sensitive areas where petroleum spills directly contaminate soil and waterways. Stricter global environmental mandates make biodegradable lubricants a necessity, while technological advances in chemical formulations have successfully overcome historical limits regarding their thermal and oxidative stability.

Forestry Lubricants Market Share,By Product, 2025 (%)

| By Product | Revenue Share, 2025 (%) |

| Synthetic | 29% |

| Synthetic Blend Oil | 21% |

| Bio-Based | 18% |

| Mineral | 32% |

Application Insights

The engine lubrication segment dominated the market with 24% share in 2025. It is driven by the severe operating conditions of heavy machinery and the rising demand for timber, which necessitates high-performance lubricants to extend engine life and prevent costly breakdowns. There is a strong market push toward synthetic and bio-based engine oils. These advanced products provide longer drain intervals, resist thermal breakdown, and comply with strict environmental regulations in regions like North America and Europe.

")

The hydraulic fluids segment held 21% market share in 2025 and is expected to have the fastest growth with a CAGR of 6.50% in the forecast period, due to heavy mechanization, strict environmental regulations on logging near water bodies, and the superior power density required by modern harvesters and forwarders. Advanced synthetic and bio-based fluids now match or exceed traditional mineral oils in oxidation resistance, cold flow, and seal compatibility.

Forestry Lubricants Market Share,By Application, 2025 (%)

| By Application | Revenue Share, 2025 (%) |

| Engine Lubrication | 24% |

| Transmission & Gear Oils | 14% |

| Hydraulic Fluids | 21% |

| Greases | 11% |

| Chain Oils / Saw Guide Oils | 12% |

| Paper Machine Oils | 7% |

| Compressor Oils | 3% |

| Coolants / Antifreeze | 5% |

| Others | 3% |

End Use Insights

The logging/harvesting companies segment dominated the market with 22% share in 2025. This expansion is primarily driven by an industry-wide transition toward highly mechanized, cut-to-length logging systems and an increased reliance on heavy equipment like harvesters, skidders, and felling machinery. Logging firms face stringent regulatory pressures from environmental agencies to use biodegradable or environmentally acceptable lubricants (EALs) to avoid soil and water contamination during on-site processing.

The forest contractors/operators segment held 7% market share in 2025 and is expected to have the fastest growth with a CAGR of 6.7% in the forecast period, aggressively shifting from manual labor to advanced, heavy-duty mechanized equipment like harvesters, skidders, and chainsaws to meet soaring global timber demands. To protect these high-investment assets against severe operating conditions and minimize costly downtime, contractors increasingly rely on specialized, high-performance lubricants.

Forestry Lubricants Market Share,By End Use, 2025 (%)

| By End Use | Revenue Share, 2025 (%) |

| OEMs | 11% |

| Sawmills | 14% |

| Paper & Paperboard Mills | 16% |

| Wood Products Manufacturing Units | 9% |

| Logging / Harvesting Companies | 22% |

| Biomass Pellet Mills | 5% |

| Pulp Mills | 8% |

| Forest Contractors / Operators | 7% |

| Timber Transport Services | 5% |

| Others | 3% |

Regional Analysis

How did North America dominate the Forestry Lubricants Market in 2025?

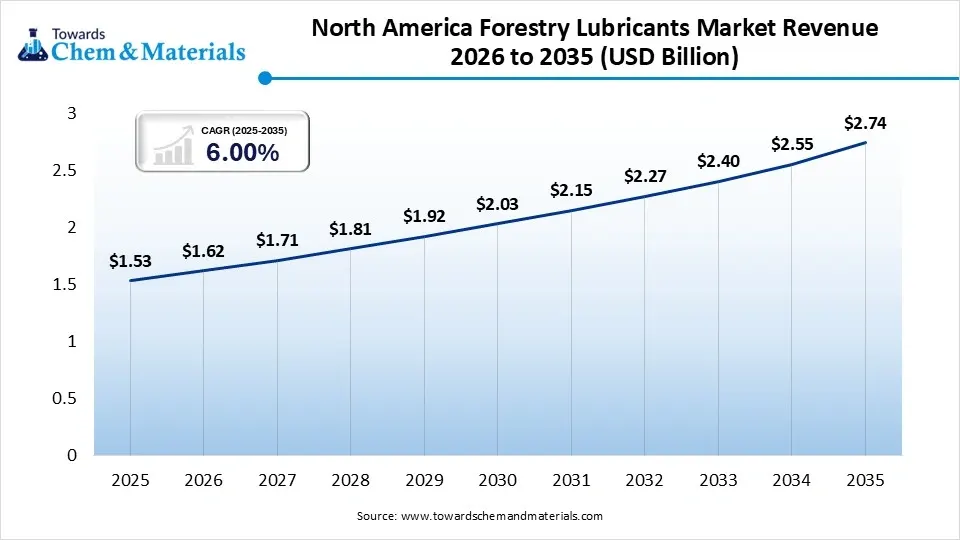

The North America forestry lubricants market size was estimated at USD 1.53 billion in 2025 and is projected to reach USD 2.74 billion by 2035, growing at a CAGR of 6.00% from 2026 to 2035.North America dominated the market with a share of 31% in 2025, by capturing the largest revenue share, driven by highly mechanized logging activities, advanced sawmill infrastructure, and stringent environmental policies mandating biodegradable lubricants. Widespread use of heavy-duty harvesters, cranes, tractors, and load carriers across the United States and Canada necessitates premium lubricants to maintain tool output and extend machinery lifespan.

U.S.

U.S.

- The U.S. forestry lubricants market is primarily driven by the increasing mechanization of forestry operations, stringent environmental regulations favoring bio-based lubricants, and the need to extend equipment lifespan under extreme operational conditions.

- Rising R&D investments focus heavily on bio-based lubricants to prevent soil and water contamination, particularly in timber-rich regions like Oregon and Washington.

Canada

- The expansion of Canada's broader timber, paper, and pulp industries requires continuous maintenance of high-performance machinery. Proper lubrication prevents costly downtime in remote logging operations.

- Heavy forestry equipment represents a massive capital investment. Advanced synthetic lubricants that provide superior wear protection under extreme cold and heavy loads are highly favored to maximize uptime and protect financial returns.

Asia Pacific Forestry Lubricants Market Growth Factor

The Asia Pacific forestry lubricants market size was estimated at USD 1.43 billion in 2025 and is projected to reach USD 2.57 billion by 2035, growing at a CAGR of 6.09% from 2026 to 2035.Asia Pacific held 29% market share in 2025 and is expected to experience the fastest growth with a CAGR of 6.80% in the forecast period, driven by rapid mechanization, rising demand for sustainable bio-based lubricants, and surging production of paper, paperboard, and wood products in economic powerhouses like China, India, and Japan. Intensifying efforts to reduce environmental impacts are driving a massive shift toward eco-friendly, bio-based, and synthetic lubricants in environmentally sensitive forestry operations.

India

- The Indian forestry lubricants market is expanding due to rising mechanization, demand for equipment reliability, and strict environmental regulations. Operators are utilizing advanced synthetics and bio-based fluids to cut maintenance costs and prevent ecological damage near forest waterways.

- Steady consumption from adjacent sectors such as wood furniture manufacturing, paper milling, and construction sustains a baseline demand for specialized industrial oils.

China

- China's forestry lubricants market growth is primarily driven by accelerated mechanization in logging, robust domestic paper and pulp processing demands, and government sustainability mandates favoring eco-friendly, bio-based formulations.

- Rising domestic consumption of paper, packaging, and wood products across China directly necessitates continuous, reliable processing capacity, driving lubricant consumption in industrial machinery

Japan

- Japan's forestry lubricants market is primarily propelled by the rising mechanization of logging operations, equipment efficiency optimization, and strict sustainability mandates.

- The push toward eco-friendly bio-lubricants directly aligns with corporate net-zero targets and national waste-oil recycling regulations overseen by Japan's Ministry of Economy, Trade, and Industry.

Europe Forestry Lubricants Market Growth Factor

The Europe forestry lubricants market size was estimated at USD 1.33 billion in 2025 and is projected to reach USD 2.39 billion by 2035, growing at a CAGR of 6.04% from 2026 to 2035.Europe held the market share of 27% in 2025. This expansion is heavily driven by stringent environmental regulations, increased mechanization of heavy forestry equipment, and a strategic shift toward bio-based lubricants to meet sustainability targets. Europe's aggressive European Green Deal policies strictly regulate the use and disposal of mineral-based lubricating oils. This acts as a primary catalyst for forestry machinery to switch to biodegradable and bio-based lubricants to prevent soil and water contamination.

Germany

- Germany's forestry lubricants market is driven by a shift toward bio-based lubricants to meet strict EU environmental mandates, rising agricultural and forestry machinery sales, and the need to optimize heavy-duty engine life under severe operating conditions.

- With the overall German lubricants market expanding alongside machinery evolution, operators prioritize advanced synthetic and bio-lubricants to extend drain intervals and protect costly equipment investments.

Italy

- Growing investments in precision forestry and advanced agricultural/forestry harvesting equipment require specialized high-viscosity lubricants for smooth operations.

- Steady output from the Italian construction, paper, pulp, and wooden furniture manufacturing sectors continually drives timber harvesting needs.

France

- France's forestry lubricants market is driven by strict environmental regulations and a shift toward bio-based, biodegradable fluids. This transition prevents soil and water contamination in ecologically sensitive areas, while high-performance synthetics extend machinery lifespan under harsh operating conditions.

- Forestry machinery represents a massive capital investment. Operators rely on specialized forestry lubricants to protect engines and hydraulics against extreme dust, humidity, and temperature swings.

Latin America Forestry Lubricants Market Growth Factor

The Latin America forestry lubricants market size was estimated at USD 0.39 billion in 2025 and is projected to reach USD 0.74 billion by 2035, growing at a CAGR of 6.61% from 2026 to 2035.Latin America held the market share of 8% in 2025, driven by rising equipment mechanization, robust pulp and paper exports, and stringent environmental regulations. Operators increasingly utilize high-performance fluids to prevent wear, extend machinery life, and prevent soil contamination in ecologically sensitive logging areas. The shift from manual logging to heavy-duty harvesters, forwarders, and skidders across major forestry hubs, primarily Brazil, Chile, and Argentina, necessitates specialized lubricants to withstand extreme operating stress.

") Brazil

Brazil

- The Brazilian forestry lubricants market is propelled by rising mechanization in timber harvesting and strict environmental regulations. High-performance synthetic and biodegradable fluids are increasingly required to protect heavy machinery operating in harsh tropical climates and sensitive ecosystems.

- Strict mandates from IBAMA (Brazilian Institute of Environment and Renewable Natural Resources) drive the adoption of bio-based and biodegradable lubricants to prevent soil and water contamination near logging sites.

Argentina

- The Argentine forestry equipment market is growing, which directly increases the deployment of skidders, harvesters, & processors requiring specialized high-performance lubricants.

- Broader economic stabilization in Argentina and steady industrial activity from the Argentine Lubricants Market underpin overall lubricant consumption across paper, pulp, and agricultural harvesting operations.

Middle East and Africa Forestry Lubricants Market Growth Factor

The Middle East and Africa forestry lubricants market size was estimated at USD 0.25 billion in 2025 and is projected to reach USD 0.48 billion by 2035, growing at a CAGR of 6.74% from 2026 to 2035.The Middle East and Africa held the market share of 5% in 2025, driven by economic diversification, infrastructure investments, and the high cost of forestry machinery. Growth is propelled by the need for equipment reliability, technological advances in synthetic formulations, and rising demand for sustainable practices. Economic diversification programs like Saudi Vision 2030 and UAE green economy initiatives are actively fostering rural and forest-access infrastructure, opening deployment opportunities for heavy forestry and agricultural equipment.

Saudi Arabia

- Massive investments exceeding $100 billion in regional developments (such as NEOM) heavily boost the demand for heavy-duty industrial and agricultural machinery lubricants.

- Rising environmental regulations and sustainability initiatives are accelerating the adoption of biodegradable, bio-based lucintel lubricants, which offer higher flash points and lower friction coefficients

UAE

- Driven by Abu Dhabi National Oil Co. and broader sustainability goals, there is a major shift toward non-toxic, eco-friendly lubricants that reduce environmental impact and lower lifecycle maintenance costs.

- Local blending initiatives like the ADNOC In-Country Value (ICV) program are channeling industrial procurement toward local suppliers, while broader market intelligence reports project steady valuation increases across specialty lubricants.

Competitive Analysis

The forestry lubricants market is highly competitive, with global lubricant manufacturers focusing on high-performance products for heavy forestry machinery and logging equipment.

- Companies like Shell plc, BP plc, and TotalEnergies SE are increasingly investing in biodegradable and environmentally friendly lubricants to comply with strict forestry and environmental regulations.

- Product innovation remains a major strategy, especially in synthetic lubricants that improve equipment life, reduce wear, and perform efficiently in extreme outdoor conditions.

- Strong partnerships with forestry equipment manufacturers help lubricant suppliers strengthen brand positioning and expand their aftermarket sales channels.

- Leading companies are prioritizing co-branded fluid partnerships with OEMs and leveraging ashless additives to meet environmental biodegradability mandates near waterways.

Top players in the Forestry Lubricants Market & Their Offerings

- Shell Plc: Major supplier of eco-friendly, biodegradable, and high-performance lubricants for the forestry and logging sector.

- Kluber Lubrication: Focuses on specialty lubricants that withstand high pressures, moisture, and dust in biomass pellet mills and sawmills.

- Exxon Mobil Corporation: Provides synthetic gear, chain, and hydraulic lubricants (such as the Mobil SHC series) for extreme-temperature forestry operations.

- TotalEnergies: Manufactures specialized biodegradable oils and greases tailored for harvesters and skidders.

Chevron Corporation: Offers heavy-duty lubricants and hydraulic oils engineered for forestry equipment.

Other Top Players Are

- Frontier Performance Lubricants INC.

- Cortec Corporation

- Repsol

- Thermal-Lube Inc.

- Neste

- Penine Lubricants

- Morris Lubricants

- CONDAT Group

- Exol Lubricants Limited

- Petro Canada Lubricants Inc

- Matrix Specialty Lubricants

- FUCHS

- Chevron Corporation

- Zeller Gmelin

- Rymax Lubricants

- Phillips 66 Company

- MOL Group

Segments Covered in the report

By Product

- Synthetic

- Polyalphaolefin (PAO)-Based

- Ester-Based

- PAG-Based

- Synthetic Blend Oil

- Semi-Synthetic Engine Oils

- Semi-Synthetic Hydraulic Oils

- Bio-Based

- Vegetable Oil-Based

- Biodegradable Ester-Based

- Mineral

- Group I Mineral Oils

- Group II Mineral Oils

- Group III Mineral Oils

By Application

- Engine Lubrication

- Harvesters

- Forwarders

- Skidders

- Transmission & Gear Oils

- Forestry Gearboxes

- Heavy-Duty Transmissions

- Hydraulic Fluids

- Hydraulic Forestry Equipment

- Mobile Forestry Machinery

- Greases

- Bearing Greases

- Multipurpose Greases

- Chain Oils / Saw Guide Oils

- Chainsaw Oils

- Guide Bar Oils

- Paper Machine Oils

- Wet-End Lubrication

- Dry-End Lubrication

- Compressor Oils

- Rotary Compressors

- Reciprocating Compressors

- Coolants / Antifreeze

- Engine Cooling Systems

- Heavy Equipment Cooling Systems

- Others

- Specialty Forestry Fluids

- Corrosion Protection Fluids

By End Use

- OEMs

- Forestry Equipment Manufacturers

- Component Manufacturers

- Sawmills

- Softwood Processing

- Hardwood Processing

- Paper & Paperboard Mills

- Packaging Paper Mills

- Specialty Paper Mills

- Wood Products Manufacturing Units

- Engineered Wood Products

- Furniture Components

- Logging / Harvesting Companies

- Commercial Logging

- Timber Harvesting Operations

- Biomass Pellet Mills

- Industrial Pellet Production

- Residential Pellet Production

- Pulp Mills

- Chemical Pulp Mills

- Mechanical Pulp Mills

- Forest Contractors / Operators

- Equipment Service Providers

- Forestry Management Contractors

- Timber Transport Services

- Trucking Fleets

- Rail Timber Logistics

- Others

- Government Forestry Operations

- Research & Training Facilities

By Regional

- North America

- U.S.

- Canada

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Sweden

- Denmark

- Norway

- Asia Pacific

- China

- Japan

- India

- South Korea

- Thailand

- Latin America

- Brazil

- Mexico

- Argentina

- Middle East and Africa (MEA)

- South Africa

- UAE

- Saudi Arabia

- Kuwait

FAQ's

Select User License to Buy

Figures (7)