Content

What is the Current Size of the Copper Scrap Market and Its Projected Growth?

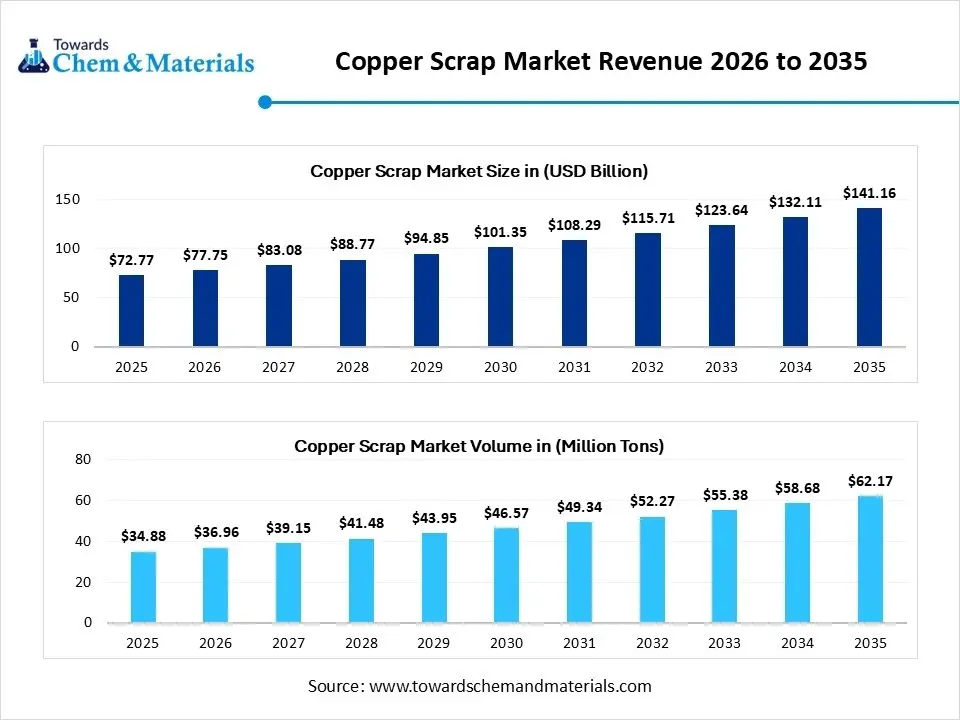

The global copper scrap market size was estimated at USD 72.77 billion in 2025 and is expected to increase from USD 77.75 billion in 2026 to USD 141.16 billion by 2035, growing at a CAGR of 6.85% from 2026 to 2035. Asia Pacific dominated the copper scrap market with the largest revenue share of 49% in 2025. In terms of volume, the market is projected to grow from 34.88 million tons in 2025 to 62.17 million tons by 2035. growing at a CAGR of 5.95% from 2026 to 2035. The market is driven by rapid urbanization, circular economy commitments, regulator pressure, advanced recycling practices and industrial expansion.

Market Highlights

- By region, Asia Pacific dominated the copper scrap market by holding a 49% share in 2025 and expected to sustain its position with the CAGR of 6.8% during the forecast period. due to its strong industrial infrastructure and recycling expansion.

- By region, Europe held the second largest share of 20% in 2025, and expects the notable growth in the market with 5.90% CAGR during the forecast period driven by stringent recycling regulations and circular economy practices.

- By scrap type, the old scrap segment held the largest 58% share in the market in 2025 due to growing recycling from end-of-life products and rapid urbanization.

- By scrap type, the new scrap segment expects the fastest growth in the market with a 6.7% CAGR during the forecast period due to an increase in demand for high-purity scrap and manufacturing expansion.

- By grade, the mixed copper scrap segment dominated the market with 28% share in 2025 due to demand for advanced sorting processes and volume availability.

- By grade, the bare bright copper segment expects the fastest growth in the market with 6.5% CAGR during the forecast period, driven by its high conductivity and ideal for electrical applications.

- By source industry, the electrical & electronics segment dominated with a held 34% share in the market in 2025 and expects the fastest growth in the market with 6.6% CAGR during the forecast period due to rapid electronics turnover and rising recycling to improve resource efficiency.

- By source industry, the construction segment held the second largest share of 26% in the 2025 segment due to rising demolition activities and infrastructure upgradation.

- By processing method, the mechanical processing segment dominated the market with 38% share in 2025, due to its cost-effectiveness for large-scale recycling and automation with high output.

- By processing method, the hydrometallurgical processing segment expects the fastest growth in the market with 7.1% CAGR during the forecast period, due to rising focus on sustainable processing and advances to improve recovery rates.

- By end-use, the copper smelters & refiners segment dominated the market with 36% share in 2025 due to high demand for refined copper, cost-efficiency and recycling.

- By end-use, the electrical manufacturing segment expects the fastest growth in the market with 6.6% CAGR during the forecast period, due to rapid electrification and renewable energy expansion.

Market Size and Volume Forecast

- Market Size (2025): USD 72.77 Billion | CAGR (2026–2035): 6.85%

- Market Projected Size (2035): USD 141.16 Billion

- Market Volume (2025): 34.88 Million Tons (MT) | Volume CAGR (2026–2035): 5.95%

- Market Projected Volume (2035): 62.17 Million Tons (MT)

- Market Pricing (2025):

- Average Manufacturing Price: USD 5,219/ton

- Average Selling Price: USD 7,850/ton

- Pricing CAGR (2025–2035): 4.25%

What is Copper Scrap?

Strong urbanization and infrastructure development in developing economies are the major factors driving market growth. The market is the global sector for the collection, processing, and selling of discarded copper materials, which can be recycled again into several products while maintaining their quality. Extensive economic trends affect industrial activity and overall investment, the hence impacting the demand for copper soon.The copper scrap is discarded copper material that is reclaimed for recycling. The copper shows the ability for infinite recycling without losing purity and its electric conductivity.

The copper scrap acts as a strategic resource essential for modern automotive, electronic, construction, and industrial manufacturing. The copper scrap market is the key backbone of the circular economy that is driven by rapid electrification and green energy infrastructure. The rising urbanization and industrialization are fueling the adoption of copper. The industry focuses on urban mining and advanced secondary smelting to reclaim conductible metals to lower the reliance on primary mining. Additionally, a stringent regulatory framework and rising eco-conscious consumers and climate-neutral goals are boosting the market adoption.

Copper Scrap Market Trends

- The Automotive Revolution: The automotive sector is shifting towards electric vehicles that accelerate the copper consumption drive in copper waste transformation to high-purity copper modern transportation.

- Government Initiatives and Strategic Alliance: The government supports and invests in advanced copper recycling technologies to increase recycling rates. The collaboration between recyclers, consumer brands, and waste management companies is allowing market expansion.

- Focus on Circular Economy Values: The global shift towards circular economy principles is reshaping the copper scrap market. This principle reinforces innovation in copper recovery and focuses on sustainability practices

Report Scope

| Report Attributes | Details |

| Market Size in 2026 | USD 77.75 Billion |

| Expected Size by 2034 | USD 141.16 Billion |

| Growth Rate from 2025 to 2034 | CAGR 6.85% |

| Base Year of Estimation | 2024 |

| Forecast Period | 2025 - 2034 |

| Dominant Region | Asia Pacific |

| Segment Covered | By Feed Material, By Grade, By Application, By End-use, By Region |

| Key Companies Profiled | Ames Copper Group, Aurubis AG, Glencore, KGHM METRACO S.A., Global Metals & Iron Inc., JAIN RESOURCE RECYCLING PVT LTD., Commercial Metals Group, Sims Limited,Kuusakoski Recycling, OmniSource, LLC., Pascha GmbH., Perniagaan Logam Panchavarnam Sdn Bhd,, S.I.C. Recycling, Inc. |

Key Technological Shifts and AI in the Copper Scrap Market

The convergence of artificial intelligence and advanced engineering is transforming the copper scrap market, turning the used copper into a high-performance material and optimizing it for the digital transformation. AI-driven data centres increase demand for specialized copper components in automotive, electronics and construction that handle high power and thermal requirements.

Manufacturers also uses AI in smart mining and autonomous refining to enhance yield and improve recycling, ensuring a reliable supply of high-purity copper from scrap. This integration supports the growth of sophisticated technological innovation and industry automation.

Trade Analysis of the Copper Scrap Market: Import and Export Statistics

- Vietnam exported 73,933 shipments of copper scrap.

- The United States exported 23,973 shipments of copper scrap.

- Mexico exported 9,646 shipments of copper scrap.

- From June 2024 to May 2025, the world exported 60,745 shipments of copper scrap.

Copper Scrap Market: Supply Chain Analysis

- Feedstock Procurement: The stage of urban mining, extraction and electrolytic refining to collect high-purity copper scrap from demolition sites and factory floors used for industrial-scale processing.

- Key Players: Commercial Metals Company, Scholz Recycling, and OmniSource.

- Mechanical Processing and Sorting: The technical stage of conversion of copper scrap by using shredders, granulators and magnetic separators to liberate copper from contamination. The optical sorters and density separators isolate pure copper from plastic, steel and aluminium.

- Key Players: Schnitzer Steel, Sims Metal, European Metal Recycling, Mitsui Mining and Smelting

- Smelting and Secondary Refining: The final stage of processed scrap is delivered to secondary smelters for purification using pyrometallurgical and hydrometallurgical. The refined anode and high-purity cathodes are sold back to the electrical and construction sector.

- Key Players: Aurubis AG, Mitsubishi Materials, Wieland Group, Jiangxi Copper and Intel

Regulatory Framework: Copper Scrap Market

| Region | Key Regulation | Strategic Focus |

| China | GB Standards | Reclassified high-grade copper scrap and regulation focus on quality control and strict purity thresholds to remove low-value and polluting imports. |

| European Union | Waste Shipment Regulation and Circular Economy Act | Restrict the export of copper scrap to non-OECD countries. The regulation for resource retention and urban mining for local secondary smelters. |

| United States | EPA RCRA and Section 301 Tariffs | Used high tariffs to manage the flow of scrap and trade protection to ensure recycling. |

| India | Hazardous Waste Rules and BWS Standards | Adopts mandatory registration for recyclers and stringent certification to prevent the dumping of contaminated copper. |

Segmental Insights

Scrap Type Insights

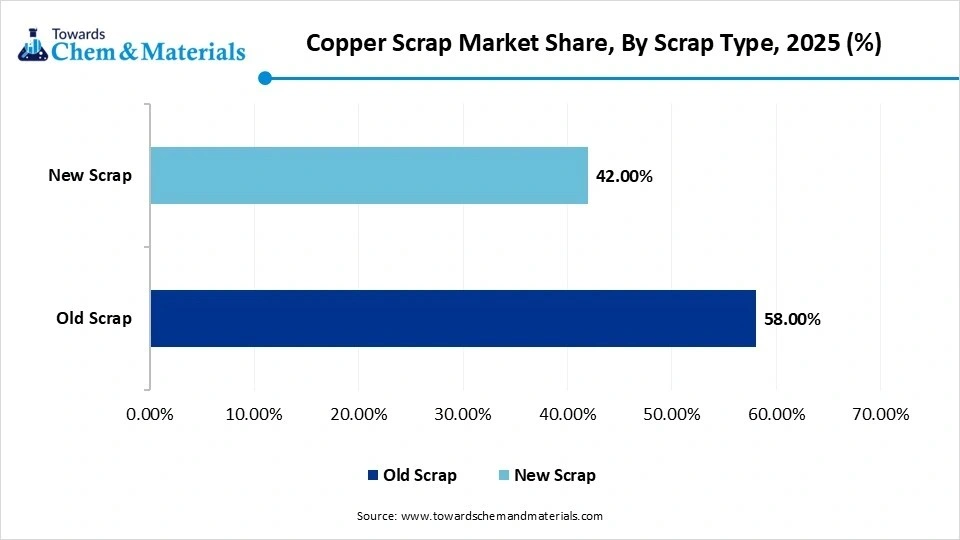

Old Scrap Segment Dominated the Copper Scrap Market with 58% of Market Share in 2025

Old scrap segment dominated the market with 58% share in 2025, representing recyclable resources utilized from weathered plumbing to industrial clippings. The segment growth is fueled by circular economy commitments and a shift towards electrification, where old scrap acts as secondary metal for primary mining for modern manufacturing.

")

New scrap segment is expected to be the fastest growing in the market with a 6.7% CAGR during the forecast period, serving as the highest-purity industrial byproduct created during product processing. The new scrap allows for instantaneous secondary smelting with low energy loss. Additionally, the segment maintains superior conductivity to meet circular economy goals for modern electrification.

Copper Scrap Market Share, By Scrap Type, 2025 (%)

| By Scrap Type | Revenue Share, 2025 (%) |

| Old Scrap | 58.00% |

| New Scrap | 42.00% |

- Old Scrap: Old scrap refers to copper scrap that has been previously used in products and is now being recycled after its useful life. This includes items like old electrical cables, plumbing pipes, and other discarded copper-containing products. It is a key source for recycled copper, contributing significantly to the overall scrap supply and helping reduce the need for newly mined copper.

- New Scrap: New scrap consists of copper waste generated during the manufacturing or production process, such as trimmings, shavings, and offcuts from the production of copper products. Unlike old scrap, new scrap is generated before the final product reaches consumers, making it easier to recycle and typically of higher quality due to its cleaner and more controlled nature.

Grade Insights

Mixed copper scrap segment dominated the market of 28% share in 2025.

Mixed copper scrap segment dominated the market of 28% share in 2025. It contains smudged plumbing, metallic remnants and oxidised wiring, which is useful in recycling alloys and industrial manufacturing. The segment is key for refining and the key backbone of the circular economy as an alternative to primary mining.

bare bright copper segment expects the fastest growth in the market with 6.5% CAGR during the forecast period, driven by the requirement of clean, unalloyed and uncoated wire for high-end electrical manufacturing. It is a high-purity grade that offers metallic lustre and superior conductivity crucial for secondary smelting. Additionally, the focus on the circular economy and recycling makes them ideal grade.

#1 copper segment held the third largest share of 24% in 2025, representing premium choices that involve clean, pure wires, tubing and bus bars. The segment essential feedstock for sustainable industrial manufacturing that offers high-efficiency, metallurgical purity and a carbon-neutral alternative for electrical infrastructure.

#2 copper segment held the fourth largest share of 22% in 2025, because it offers large-scale scrap grade that is key for metallic remnant, especially for secondary smelting. The segment supports cost-sensitive industries and reduces carbon content in industrial manufacturing as a sustainable alternative to primary mining and refined ore.

Copper Scrap Market Share, By Grade, 2025 (%)

| By Grade | Revenue Share, 2025 (%) |

| Bare Bright Copper | 26.00% |

| #1 Copper | 24.00% |

| #2 Copper | 22.00% |

| Mixed Copper Scrap | 28.00% |

- Bare Bright Copper: Bare bright copper is the highest grade of copper scrap, typically consisting of clean, uncoated copper wire that is free from insulation or other contaminants. It is highly sought after for recycling due to its purity, and it is primarily used in the production of high-quality copper products.

- #1 Copper: #1 copper scrap is also a high-quality grade, though it may contain minimal oxidation or surface tarnishing. This scrap is typically clean and free of contaminants, making it suitable for recycling into new copper products, including wiring and electrical components. It is a valuable resource for the copper industry due to its quality and ease of processing.

- #2 Copper: #2 copper scrap is of a lower grade compared to #1 copper and may contain more oxidation or dirt. It can include copper that is coated with insulation or has minor impurities, but it is still valuable for recycling. #2 copper is often used in less critical applications, such as industrial machinery or lower-grade wiring.

- Mixed Copper Scrap: Mixed copper scrap refers to a variety of copper scrap grades that are combined, often including #1 and #2 copper, along with other types of copper materials. This scrap is typically more difficult to process due to the variation in quality, but it is still used in recycling, especially for large-scale industrial applications where the purity requirements are not as stringent.

Source Industry Insights

Electrical & Electronics Segment Dominated the Copper Scrap Market with 34% of Market Share in 2025

The electrical & electronics segment dominated with a held 34% share in the market in 2025 and expects the fastest growth in the market with 6.6% CAGR during the forecast period, serving as a key source of obsolete wiring, circuit boards and telecommunication cables. The segment is a pillar of urban mining that contains high-purity materials by ensuring high electrical conductivity. The rising demand for copper in electronics production is pushing the industry towards a sustainable supply of recycled copper to meet green energy demand and significant investment in modern electrification projects.

Construction segment held the second largest share in the market of 26% in 2025, driven by demolition and urban upgradation. The #1 and #2 copper is key for reclaimed plumbing and roofing sheets by providing a sustainable alternative in building infrastructure. The rising demand for green building infrastructure to meet low-carbon goals and the circular economy is accelerating the market growth.

The automotive segment held the third largest share in the market of 16% in 2025 due to the transition towards electrification and green mobility. The surging demand for high-purity copper across the end-of-life recycling of vehicles is boosting market growth. By reclaiming these conductive components and wiring systems to meet decarbonization goals, reinforcing the segment towards green mobility.

Industrial appliances segment held the fourth largest share in the market of 14% in 2025, where copper is stream of heat exchangers, heavy-duty transportation and transformer windings. The industry focuses on the engineering of high-purity copper that offers superior thermal conductivity and electrical efficiency. The rapid urbanization driving waste production that fueling the reclamation of large-scale remnants from end-of life machinery and HVAC systems as a sustainable, low-carbon alternative.

Copper Scrap Market Share, By Source Industry, 2025 (%)

| By Source Industry | Revenue Share, 2025 (%) |

| Electrical & Electronics | 34.00% |

| Construction | 26.00% |

| Automotive | 16.00% |

| Industrial Machinery | 14.00% |

| Consumer Appliances | 10.00% |

- Electrical & Electronics: Copper scrap from the electrical and electronics industry is primarily derived from discarded wires, cables, transformers, and electrical components. This sector generates significant amounts of copper scrap due to the high copper content in electronic products, and it plays a vital role in supplying recycled copper for the production of new electrical components and systems.

- Construction: The construction industry is a major source of copper scrap, especially through the demolition of old buildings and infrastructure. Copper scrap from plumbing pipes, wiring, and roofing materials is collected and recycled. This helps meet the demand for copper in the construction of new buildings, especially for plumbing, electrical wiring, and HVAC systems.

- Automotive: The automotive industry contributes to copper scrap through the disposal of old vehicles, manufacturing offcuts, and the recycling of automotive parts. Copper is widely used in automotive components such as wiring, motors, and connectors. Scrap generated from these parts is a valuable source of copper for reuse in vehicle manufacturing and other industries.

- Industrial Machinery: Copper scrap from industrial machinery comes from the breakdown, replacement, or renovation of machinery and equipment. Components like motors, generators, and wiring are rich in copper and contribute to the supply of recyclable material. This scrap is typically processed for use in new machinery or industrial applications that require high-quality copper.

- Consumer Appliances: Copper scrap from consumer appliances comes from products such as refrigerators, air conditioners, washing machines, and other household electronics. These appliances often contain copper components like wiring and motors, which, once discarded, are processed and recycled for use in new products, helping reduce the demand for newly mined copper.

Processing Method Insights

Mechanical Processing Segment Dominated the Copper Scrap Market with 38% of Market Share in 2025

The mechanical processing segment dominated the market with 38% share in 2025. It is the cold-recovery stage that utilises granulators, shredders and magnetic separators. The mechanical processing employing optical sorting and density separation that offers high-putty copper form plastic, steel products by maintaining efficiency. It is cost-effective and an advanced liberation technique that ensures clean, smelter-ready feedstock for large-scale sorting infrastructure.

The hydrometallurgical processing segment is expected to be the fastest growing in the market with 7.1% CAGR during the forecast period, driven by the transition toward modern industrial manufacturing, where this process enables advanced chemical recovery by using acidic leaching and solvent extraction to dissolve metals. The hydrometallurgical process is an eco-friendly and low-temperature process for recovering copper from metal alloys and electronic scrap. Additionally, the rising focus on sustainable refining and improving the recovery rate is driving the adoption.

The pyrometallurgical processing segment held the second largest share in the market of 34% in 2025. It is a function as high-temperature recovery process that utilizing smelting and fire refining to purify and melt large volumes of copper scrap. The process efficiently separates impurities of slag, contaminated scrap and alloying elements. The well-established electrical infrastructure supports driving the segment implementation in bulk manufacturing by meeting the circular economy target.

Copper Scrap Market Share, By Processing Method, 2025 (%)

| By Processing Method | Revenue Share, 2025 (%) |

| Mechanical Processing | 38.00% |

| Pyrometallurgical Processing | 34.00% |

| Hydrometallurgical Processing | 28.00% |

- Mechanical Processing: Mechanical processing involves the physical separation and sorting of copper scrap through methods such as shredding, crushing, and sorting. This technique is used to remove impurities and prepare the copper for further refining or recycling. It is typically used for processing non-ferrous metals, including copper, to convert scrap into a more uniform and usable form for various applications.

- Pyrometallurgical Processing: Pyrometallurgical processing utilizes high temperatures to melt and separate copper from other materials in scrap. This method involves smelting, where the copper scrap is heated to very high temperatures in a furnace to remove contaminants and impurities. The resulting copper can then be refined into a pure form for manufacturing new products. Pyrometallurgy is commonly used for large-scale copper recycling.

- Hydrometallurgical Processing: Hydrometallurgical processing involves using aqueous solutions to extract copper from scrap. This method includes processes such as leaching, where copper is dissolved in a chemical solution, followed by purification and electro-winning to recover pure copper. This method is considered more environmentally friendly than pyrometallurgy, as it uses lower temperatures and reduces the risk of air pollution. It is often applied in the recycling of lower-grade copper scrap.

End-Use Insights

Copper Smelters & Refiners Segment Dominated the Copper Scrap Market with 36% of Market Share in 2025

Copper smelters & refiners segment dominated the market with 36% share in 2025, driven by shift towards electrification and demand for refined copper. The segment shows the transformation of secondary material into extra pure copper that utilizes pyrometallurgical smelting and electrorefining. The segment integrated the recycled copper feedstock for the production of high-conductivity cathode and refined anode, which makes copper scrap a catalyst for green energy infrastructure.

The electrical manufacturing segment is expected to be the fastest growing in the market with 6.6% CAGR during the forecast period, driven by rising consumption of reclaimed high-purity wire and bus bars. The segment depends on copper due to its conductivity, ductility, used for creating power cables, transformers, and circuit boards. The manufacturer uses secondary copper as a key substitute for a sustainable supply chain for global electrification.

Foundries segment held the third largest share in the market of 18% in 2025 due to its cost-effectiveness. The foundries focus on high-efficiency manufacturing of cast components and industrial alloys that utilizing mixed copper scrap to manufacture pumps, valves and automotive components. The segment shift toward a circular economy using a sustainable alloying process is important for heavy machinery infrastructure and casting applications.

Construction industry segment held the fourth largest share in the market of 14% in 2025, driven by massive consumer demand for reclaimed tubing, wiring and building sheets. The rising implementation of sustainable building practices and urban development is fueling the adoption of copper with superior corrosion resistance and thermal stability. The copper recyclability makes them ideal for building infrastructure by maintaining structural integrity and reducing energy use.

Copper Scrap Market Share, By End-Use, 2025 (%)

| By End-Use | Revenue Share, 2025 (%) |

| Copper Smelters & Refiners | 36.00% |

| Foundries | 18.00% |

| Electrical Manufacturing | 20.00% |

| Construction Industry | 14.00% |

| Automotive Industry | 12.00% |

- Copper Smelters & Refiners: Copper scrap is widely used in smelters and refiners for recycling and refining processes. This end-use sector is crucial for producing high-quality copper that meets industry standards, ensuring that raw material extraction is minimized.

- Foundries: Copper scrap serves as an essential raw material in foundries, where it is melted and cast into various products. These products are then used in diverse industries, including machinery, metal parts manufacturing, and industrial applications.

- Electrical Manufacturing: The electrical manufacturing sector heavily relies on copper scrap for the production of wiring, cables, and other electrical components. Copper’s excellent electrical conductivity makes it a prime material in this industry, especially in the production of transformers, motors, and generators.

- Construction Industry: Copper scrap finds its way into the construction industry, particularly in plumbing, roofing, and other building applications. Copper's corrosion resistance and longevity make it ideal for infrastructure projects, including electrical systems and piping.

- Automotive Industry: The automotive industry uses copper scrap in the manufacturing of various components, including electrical systems, motors, and wiring harnesses. Copper is essential for vehicle efficiency, contributing to lighter, more energy-efficient designs in modern automobiles.

Regional Insights

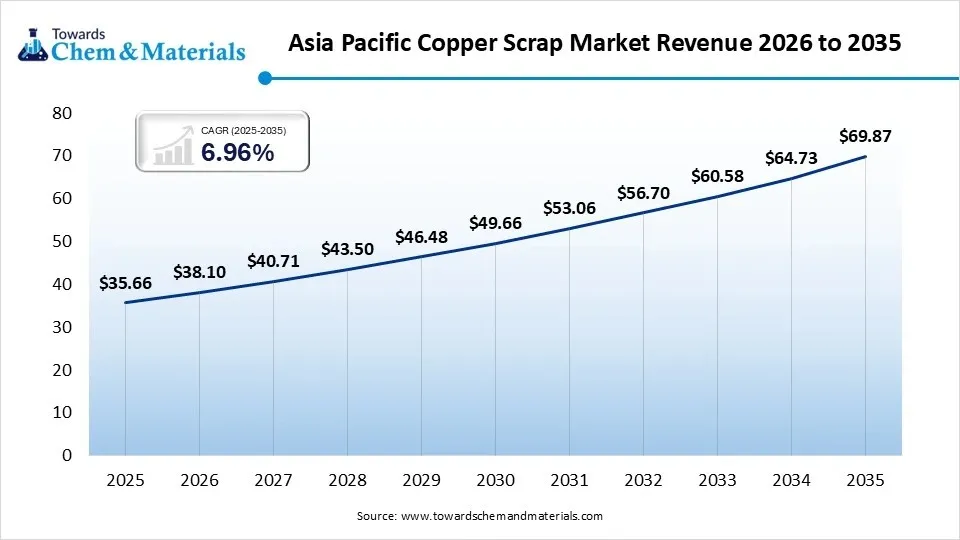

The Asia Pacific copper scrap market size was valued at USD 72.77 billion in 2025 and is expected to be worth around USD 141.16 billion by 2035, exhibiting at a compound annual growth rate (CAGR) of 6.85% over the forecast period from 2026 to 2035.The dominance of the region can be attributed to the increasing emphasis on sustainability, along with the ongoing adoption of innovative recycling technologies to enhance scrap quality. In addition, enhancements in the regional supply chain and growth in refining capacity also fuel the regional expansion.

China Copper Scrap Market Trends

In the Asia Pacific, China led the market owing to the substantial investment in green infrastructure and electric vehicles, along with the rapid industrialization and urbanization in the country., China's massive production and construction sector needs large volumes of the metal, driving market growth further.

The Middle East & Africa region is expected to grow at the fastest CAGR over the forecast period. The growth of the region can be credited to the expansion of renewable energy and the rising use of electric vehicles (EVs). Moreover, the shift towards wind and solar power requires significant amounts of copper for energy systems and related infrastructure, propelling demand for recycled copper. ")

Saudi Arabia Copper Scrap Market Trends

Saudi Arabia is witnessing the fastest growth during the forecast period due to the growth of data centers and the rise in demand for copper in renewable energy infrastructure. The implementation of smart infrastructure fuels demand for copper in advanced wiring and other components.

North America is expected to grow at a notable CAGR over the forecast period.

The growth of the region can be driven by growing emphasis on sustainable manufacturing, coupled with the robust industrial demand from the electric vehicle sector. Also, the region has a significant recycling network, such as shredding facilities, scrap yards, and processing plants.

Copper Scrap Market Share, By Regional, 2025 (%)

| Regional | Revenue Share, 2025 (%) |

| Asia-Pacific | 49.00% |

| Europe | 20.00% |

| North America | 16.00% |

| Latin America | 8.00% |

| Middle East & Africa | 7.00% |

U.S. Copper Scrap Market Trends

In North America, the U.S. dominated the market because of rapidly expanding construction and electronics industries along with the increasing focus on recycling and sustainability. The United States possesses a well-established and large recycling infrastructure, which offers a solid foundation for the market in the region.

Recent Developments

- In March 2026, One and One Green Technologies strategically enter into the Metro Manila electronic waste resource recovery market for the expansion into the e-scrap copper recycling. The strategic focus on strengthening the local supply of E-waste streams and metal recycling.(Source : www.nasdaq.com)

- In September 2025, Aurubis AG, known as the largest copper manufacturer, started manufacturing at a United States copper recycling plant in Richmond, Georgia, with an investment of about $800 million. The facility focuses on strengthening its recycled copper processing capacity and expansion of Aurubis global recycling presence, and reducing reliance on U.S. metal imports.(Source: money.usnews.com)

Top Companies in the Copper Scrap Market

- Ames Copper Group

- Aurubis AG

- Glencore

- KGHM METRACO S.A.

- Global Metals & Iron Inc.

- JAIN RESOURCE RECYCLING PVT LTD.

- Commercial Metals Group

- Sims Limited

- Kuusakoski Recycling

- OmniSource, LLC.

- Pascha GmbH.

- Perniagaan Logam Panchavarnam Sdn Bhd

- S.I.C. Recycling, Inc.

Segment Covered in the Report

By Scrap Type

- Old Scrap

- Post-consumer Scrap

- End-of-life Equipment

- New Scrap

- Industrial Scrap

- Manufacturing Offcuts

By Grade

- Bare Bright Copper

- #1 Copper

- #2 Copper

- Mixed Copper Scrap

By Source Industry

- Electrical & Electronics

- Wire & Cables

- Circuit Boards

- Construction

- Plumbing

- Roofing Material

- Automotive

- Wiring Harness

- Radiators

- Industrial Machinery

- Consumer Appliances

By Processing Method

- Mechanical Processing

- Shredding

- Sorting

- Pyrometallurgical Processing

- Smelting

- Refining

- Hydrometallurgical Processing

- Leaching

- Solvent Extraction

By End-Use

- Copper Smelters & Refiners

- Foundries

- Electrical Manufacturing

- Construction Industry

- Automotive Industry

By Regions

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Asia Pacific

- China

- India

- Japan

- South Korea

- Latin America

- Brazil

- Argentina

- Middle East & Africa

- Saudi Arabia

- South Africa

Tags

FAQ's

Select User License to Buy

Figures (4)