Content

What is the Current Carbon Steel Market Size and Share?

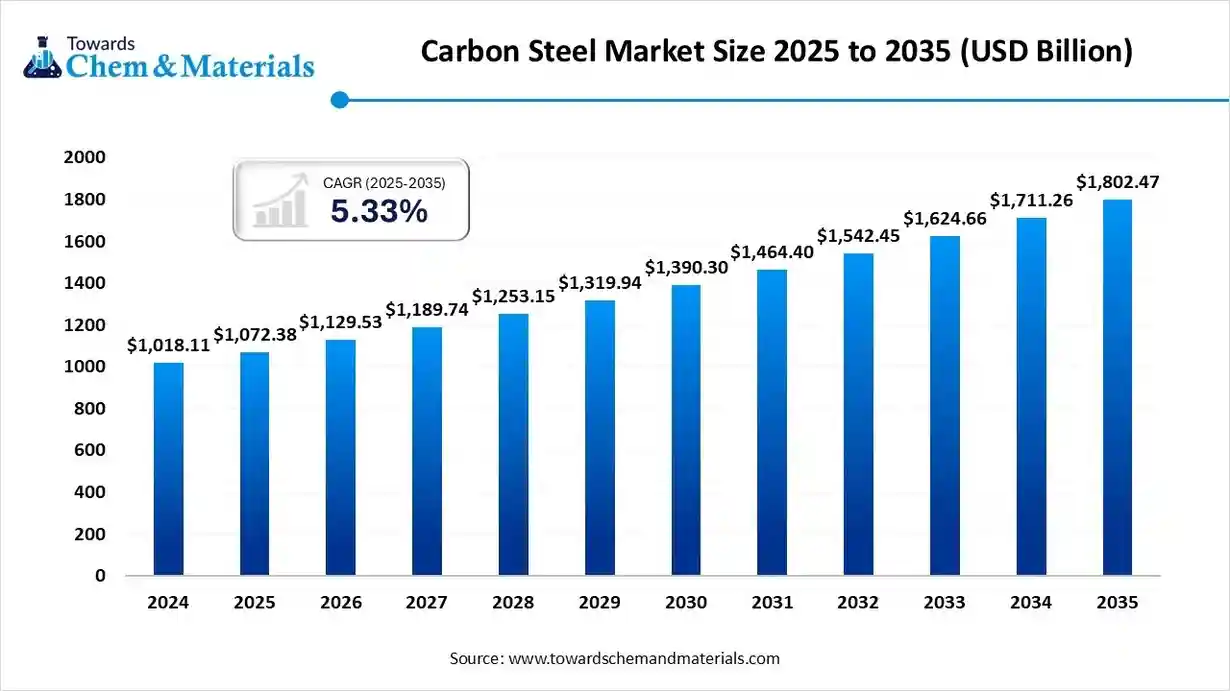

The carbon steel market size was valued at USD 1,146.3 billion in 2025, is estimated to reach USD 1201.92 billion in 2026, and is projected to reach USD 1840.73 billion by 2035, exhibiting a compound annual growth rate (CAGR) of 4.85% over the forecast period from 2026 to 2035.Asia Pacific dominated the carbon steel market with the largest revenue share of 61% in 2025 and is expected to grow at the fastest CAGR of 4.93% during the forecast period. In terms of volume, the carbon steel market is projected to grow from 1955.40 million metric tons in 2025 to 2880.58 million metric tons by 2035. growing at a CAGR of 3.95% from 2026 to 2035.The turn toward low-carbon construction and sustainable manufacturing practices is the major pillar of the industry, while manufacturers are likely to revolutionize the industry through their ongoing research and development activities. Furthermore, artificial intelligence and robotics are expected to lower manufacturing costs and human errors at the same time, which supports industry modules during the anticipated period.

")

Market Highlights

- By region, Asia Pacific dominated the market with a share of 61% in 2025 and is expected to grow at a CAGR of 5.20% over the forecast period.

- By region, North America held 13% market share in 2025 and is expected to be the fastest-growing region in the market, with a CAGR of 5.50% in the forecast period.

- By type, the low carbon steel segment dominated the market with 56% share in 2025 and is expected to grow at a CAGR of 5% over the forecast period.

- By type, the high carbon steel segment held a 16% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 5.50% in the forecast period.

- By application, the construction segment dominated the market with 43% share in 2025 and is expected to grow at the CAGR of 4.70% over the forecast period.

- By application, the others segment held a 15% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 5.30% in the forecast period.

Enabling Modern Industrial Expansion

Stronger, reliable, and affordable industrial materials have created greater attention in global industry infrastructure. Manufacturers and consumers are looking for suitable materials for their wide range of applications nowadays, where carbon steel has created its own presence in major industries such as automotive, construction, pipelines, and energy projects, as per recent observations. Furthermore, the regional governments across the globe are seen under the greater implementation of sustainability standards.

- For instance, in March 2026, TATA Steel successfully established and started a scrap-based electric arc furnace, which was primarily designed to minimize carbon pollution and achieve CO2 emissions, as per the published report. (Source: www.tatasteel.com)

Carbon steel is a type of steel formed using carbon, iron, and other elements like silicon, phosphorus, manganese, & sulfur. In carbon steel, iron is the primary component, the content of a carbon content from 0.05% to 2.1%, and other elements present in small amounts. Carbon steel consists of excellent strength, greater hardness, weldability, and greater ductility. The various types of carbon steel include low-carbon steel, medium-carbon steel, and high-carbon steel. The rapid development of various infrastructure projects like transportation networks, buildings, bridges, and highways increases demand for carbon steel.

The global carbon steel industry is changing in response to new environmental goals and customer expectations. Manufacturers are working to improve production efficiency by using modern equipment, better process control, and higher recycling rates. Instead of focusing only on increasing output, companies are also improving product quality, reducing energy consumption, and making operations more sustainable. Many steel producers are modernizing their manufacturing plants to improve competitiveness and respond to changing market conditions.

The Growing Energy Sector Propels Carbon Steel Market Growth

The growing expansion of the energy sector increases demand for carbon steel for extraction processes and energy infrastructure. The growing energy sector, including renewable energy and oil & gas, increases demand for carbon steel for various applications. The growth in the oil & gas industry increases demand for carbon steel industry increases demand for carbon steel for platforms, pipelines, and drilling equipment.

The increasing offshore and onshore extraction of oil & gas increases demand for carbon steel. The expansion of solar and wind energy is driving demand for carbon steel for transmission towers, wind turbines, and solar panel structures. The focus on the development of efficient power plants increases demand for a wide range of steel components. The demand for the development of energy infrastructures like pipelines is fueling the adoption of carbon steel. The growing energy sector is a key driver for the growth of the carbon steel market.

Global Investment Flow for the Carbon Steel Market 2026

Steel manufacturers are investing heavily in upgrading existing production plants instead of relying only on building completely new facilities. Modern equipment improves manufacturing efficiency, reduces production delays, lowers maintenance costs, and helps companies produce higher-quality carbon steel.

Environmental improvement has become an important investment priority for the carbon steel industry. Companies are increasing spending on energy-saving technologies, recycling systems, cleaner production methods, and emission reduction projects.

- For Instance, in July 2026, JSW Steel announced the start of construction for its Rayalaseema integrated steel plant in Andhra Pradesh with a planned investment of around ₹16,350 crore.(Source:www.jswsteel.in)

Many carbon steel manufacturers are expanding production capacity and strengthening supply chains to meet growing demand from infrastructure, automotive, renewable energy, and industrial sectors.

Carbon Steel Market Trends

- The greater need for high-quality carbon steel has created profitable pathways for manufacturers in recent years. Also, the major manufacturers are actively developing materials that have durability, strength, and consistent performance as per the recent survey.

- A shift towards environmentally friendly and sustainable manufacturing practices is actively providing benefits to the industry in the current period. Also, several governments are actively promoting sustainability practices while providing attractive benefits to manufacturers such as tax reductions and subsidies.

- The emergence of the digital transformation in the production plant is likely to create profitable avenues for the manufacturers during the forecast period. Also, the manufacturers are seeking real-time monitoring and artificial intelligence to smoothly run manufacturing plants and establishments.

Digital Innovation Powers Sustainable Steel Growth

The industry is quickly moving toward the combination of intelligent manufacturing with cleaner production systems. Steel manufacturers are replacing traditional production methods with automated operations, digital monitoring, artificial intelligence, advanced process control, and energy-efficient equipment. These technologies improve production accuracy, reduce raw material waste, lower energy consumption, and support better product consistency.

Report Scope

| Report Attributes | Details |

| Market Size in 2026 | USD 1,201.9 Biilion/ 2,032.6 Million Metric Tons |

| Market Size by 2035 | USD 1,840.7 Billion/ 2,880.6 Million Metric Tons |

| Growth Rate from 2026 to 2035 | CAGR 4.85% |

| Base Year of Estimation | 2025 |

| Forecast Period | 2026 - 2035 |

| Dominant Region | Asia Pacific |

| Segment Covered | By Type, By Application, By Region |

| Key Profiled Companies | Nippon Steel Corporation, POSCO, HBIS Group, JFE Steel Corporation, Tata Steel Limited, United States Steel Corporation, JSW Steel Limited, ThyssenKrupp AG |

Supply Chain Analysis of the Carbon Steel Market

Production & Processing

- Making carbon steel is like baking a high-strength metal recipe by cooking iron and coal together.

Mills melt raw iron ore inside roaring, white-hot towers, then blast the liquid metal with intense shots of pure oxygen to strip out unwanted chemical impurities. - They mix in precise pinches of carbon to build up strength before rolling the glowing metal slabs into heavy building beams.

- China Baowu Steel Group: China Baowu Steel Group stands as the undisputed titan of the global metal sector, churning out more raw tonnage than any other company.

- Key players: ArcelorMittal, Ansteel Group, Nippon Steel Corporation, Shagang Group, and POSCO Holdings

Quality Testing and Certification

- Testing carbon steel means stretching, crushing, and bending structural samples inside high-pressure labs to prove the metal won't snap under heavy loads.

- Technicians shoot beams with magnetic currents and X-rays to hunt for microscopic internal cracks. Earning an official safety stamp certifies the alloy is completely tough enough to hold up skyscrapers and bridges.

- Key agencies: SGS, Bureau Veritas, Intertek, ASTM International, and ISO (International Organization for Standardization)

Distribution to Industrial Users

- Moving bulk carbon steel requires heavy-duty flatbed trucks, dedicated cargo trains, and massive shipping vessels to carry the extreme weight. Distributors manage sprawling metal yards where they cut massive coils and slabs down to custom sizes for immediate delivery.

- This structured logistics pipeline ensures factories receive raw building blocks exactly when production lines demand them.

- Reliance Steel & Aluminum Co.: Reliance Steel & Aluminum Co. is the largest metals service center operator in North America, acting as a critical bridge between mills and customers.

- Key players: Kloeckner Metals, Thyssenkrupp Materials Services, Ryerson, and Marubeni-Itochu Steel

Carbon Steel Market Dynamics

Driver

The Infrastructure Boom

The continuous growth of infrastructure and industrial projects across the world is a strong foundation for the industry in the current period. Also, governments are investing in highways, bridges, railways, airports, factories, power plants, and residential buildings, all of which require large quantities of carbon steel because of its strength, durability, and affordable cost. Manufacturing industries are also expanding production facilities, increasing demand for machinery and equipment made from carbon steel. As urban populations continue to grow and developing countries improve public infrastructure, carbon steel consumption is expected to remain strong, making construction and industrial development the primary growth engine for the global market.

Restraint

Frequent Price Fluctuations of Raw Materials

The frequent change in raw material and energy prices is expected to hinder industry growth during the forecast period. Moreover, the cost of iron ore, coking coal, scrap steel, electricity, and transportation often changes due to global economic conditions and supply chain disruptions. These fluctuations increase manufacturing costs and reduce profit margins for steel producers. Companies sometimes struggle to maintain stable product prices because production expenses change rapidly. Furthermore, the uncertain costs also affect long-term investment planning, making it more difficult for manufacturers to expand production while remaining competitive in domestic and international markets.

Opportunity

More Clean Manufacturing

The increasing demand for cleaner and more sustainable steel production is expected to create lucrative opportunities in the coming years. Also, many governments and industries are encouraging manufacturers to reduce emissions and improve energy efficiency. This creates opportunities for companies investing in recycled steel, energy-saving equipment, digital manufacturing, and modern production technologies. Customers are also giving greater importance to environmentally responsible suppliers when selecting construction materials and industrial products. As sustainability becomes a long-term business priority across many industries, manufacturers that successfully improve environmental performance can strengthen their market position and attract new business opportunities worldwide.

Carbon Steel Market Regulatory Landscape: Regulations

| Country Region | Regulatory Body | Key Regulations | Focus Areas |

| United States | Occupational Safety and Health Administration (OSHA) | OSHA General Industry Standards [29 CFR Section 1910.1025]: Sets strict legal boundaries for air quality in mills. | Workplace Heavy Metal Protection: Mandating advanced ventilation hoods and continuous air filtering inside foundries to protect workers from inhaling fine metallic slag and iron dust. |

| Europe | European Chemicals Agency (ECHA) | EU Carbon Border Adjustment Mechanism (CBAM) [Regulation (EU) 2023/956 Annex I]: Imposes a landmark environmental tariff on heavy imports. | Decarbonising International Trade: Equalizing the market by taxing cheap, high-pollution foreign steel to protect domestic European mills that are spending capital to cut emissions |

| China | Ministry of Industry and Information Technology (MIIT) | Action Plan for Carbon Peaking in Industrial Sectors [MIIT Decree No. 2022-88] Section 3: Sets a hard legislative deadline for the entire heavy metal market. | Phasing Out Inefficient Mills: Aggressively shutting down older, highly polluting coal foundries and merging production into highly automated, energy-efficient coastal steel complexes. |

Regional Insights

How Asia Pacific Dominated the Carbon Steel Market in 2025?

The Asia Pacific carbon steel market size was estimated at USD 699.3 billion in 2025 and is projected to reach USD 1,132.0 billion by 2035, growing at a CAGR of 4.93% from 2026 to 2035.Asia Pacific dominated the market with a share of 61% in 2025 and is expected to grow at a CAGR of 5.20% over the forecast period, due to the region having the world's largest construction industry, manufacturing sector, and infrastructure investment. Rapid urbanization, expanding industrial production, and strong government support continue increasing steel demand. Large-scale transportation projects, residential construction, renewable energy development, and industrial expansion create continuous demand for carbon steel. The region also benefits from large domestic steel production capacity, improving supply chain efficiency and reducing dependence on imports.

China

The country is continuing to strengthen its steel industry by improving production efficiency while focusing on higher-value steel products instead of only increasing production volume. Also, they are investing in cleaner manufacturing technologies, intelligent steel plants, and energy-efficient production systems. Infrastructure development, renewable energy projects, electric vehicle manufacturing, and industrial modernization continue supporting domestic steel demand. Also, the steel companies are expanding exports while improving environmental performance through technology upgrades.

Japan

Japan is focusing on producing advanced, high-quality carbon steel for automotive manufacturing, industrial machinery, shipbuilding, and engineering applications. Steel companies are investing in automation, digital manufacturing, and low-emission production technologies to improve competitiveness. Furthermore, the manufacturers continue developing stronger steel products with improved performance while reducing production costs through modern equipment. The country is also increasing collaboration between steel producers and automotive manufacturers to support future mobility technologies.

Carbon Steel Market Evaluation in North America

The Norht America carbon steel market size was estimated at USD 149.02 billion in 2025 and is projected to reach USD 248.50 billion by 2035, growing at a CAGR of 5.25% from 2026 to 2035.North America held 13% market share in 2025 and is expected to be the fastest-growing region in the market, with a CAGR of 5.50% in the forecast period, owing to governments and private industries increasing investment in infrastructure modernization, manufacturing expansion, clean energy projects, and industrial reshoring. Companies are also investing in advanced steel production technologies and improving domestic manufacturing capacity. Growing demand from automotive, renewable energy, heavy equipment, and construction industries is expected to support long-term market expansion.

United States

The country is actively expanding its carbon steel industry through investments in infrastructure modernization, manufacturing growth, energy projects, and industrial reshoring. Steel producers are upgrading production facilities with automation, digital monitoring, and advanced processing technologies to improve productivity. Demand remains strong from construction, automotive, defense, machinery, and renewable energy sectors. Government support for domestic manufacturing is encouraging additional investment in steel production and supply chains. Also, companies are also increasing the use of recycled steel and energy-efficient production methods to improve sustainability.

Canada

Steel demand is heavily increasing in Canada because of railway expansion, industrial equipment production, and renewable energy developments. Moreover, manufacturers are improving operational efficiency through plant modernization and better production technologies. The country also benefits from close trade relationships with the United States, supporting regional steel demand and supply chain stability. Growing investment in industrial development and infrastructure renewal is creating additional opportunities for steel producers while encouraging long-term market expansion across several industrial sectors.

Europe Carbon Steel Industry Conditions

The Europe carbon steel market size was estimated at USD 160.48 billion in 2025 and is projected to reach USD 266.91 billion by 2035, growing at a CAGR of 5.22% from 2026 to 2035.Europe held a 14% market share in 2025 and is expected to grow at a CAGR of 3.80% over the forecast period, owing to manufacturers investing in cleaner production technologies while maintaining high-quality steel manufacturing. Governments are supporting industrial modernization, energy-efficient production, and sustainable infrastructure projects. Demand from automotive, engineering, renewable energy, and transportation industries continues increasing. Steel producers are improving operational efficiency through automation and digital manufacturing while reducing environmental impact. These developments continue supporting steady regional growth.

Germany

The country’s strong automotive, engineering, industrial equipment, and machinery sectors are leading the industry sales. Also, steel manufacturers are modernizing production plants with automation, digital manufacturing systems, and energy-efficient technologies to improve productivity. Demand for carbon steel remains stable as industries continue investing in industrial equipment, transportation infrastructure, and manufacturing expansion. German companies are also focusing on producing higher-value steel products for advanced engineering applications.

Italy

The country is continuously supporting carbon steel demand through its machinery, engineering, industrial equipment, and construction industries. Steel manufacturers are improving production efficiency while expanding exports of specialized steel products to international markets. Infrastructure renovation projects, commercial construction, and industrial modernization continue creating stable domestic demand for carbon steel. Companies in Italy are investing in advanced manufacturing technologies to improve product quality and reduce operating costs. Strong engineering expertise and export-oriented manufacturing continue supporting the country's steel industry.

Carbon Steel Market Survey in Latin America

The Latin America carbon steel market size was estimated at USD 57.32 billion in 2025 and is projected to reach USD 101.24 billion by 2035, growing at a CAGR of 5.85% from 2026 to 2035.Latin America held a 6% market share in 2025 and is expected to grow at a CAGR of 4.60% over the forecast period, driven by improving industrial activity and rising investments in construction, packaging, and consumer goods manufacturing. Urban development projects and increasing demand for affordable housing are supporting greater use of paints, coatings, and construction chemicals. Furthermore, manufacturers are adopting water-based polymer technologies to improve product quality and comply with evolving environmental standards.

Brazil

The country is actively strengthening its carbon steel market through infrastructure development, mining activities, transportation projects, agriculture, and industrial manufacturing. Steel demand continues increasing because of logistics expansion, warehouse construction, renewable energy projects, and heavy equipment manufacturing. Steel producers are improving operational efficiency while expanding export opportunities to international markets. The country's large natural resource base also supports domestic steel production. Ongoing industrial investment and government infrastructure programs continue creating stable demand for carbon steel products across multiple sectors.

Argentina

The industry is expanding in Argentina as investments increase in infrastructure improvement, industrial recovery, agriculture, transportation, and energy development. Demand is supported by construction projects, machinery production, and agricultural equipment manufacturing. Local industries continue modernizing production facilities to improve competitiveness and operational efficiency. Infrastructure renovation and industrial investment are creating additional opportunities for carbon steel suppliers. The country is also encouraging manufacturing growth to strengthen domestic production capacity.

Middle East and Africa Carbon Steel Sector Observation

The Middle East and Africa carbon steel market size was estimated at USD 80.24 billion in 2025 and is projected to reach USD 138.05 billion by 2035, growing at a CAGR of 5.58% from 2026 to 2035.The Middle East and Africa held a 6% market share in 2025 and is expected to grow at a CAGR of 4% over the forecast period, driven by large infrastructure projects, industrial diversification, energy investments, and urban development. Governments are investing in transportation, commercial buildings, manufacturing, and renewable energy facilities. Industrial expansion and economic diversification programs continue increasing regional steel consumption. Local production capacity is also improving, reducing dependence on imports while supporting future market growth.

Saudi Arabia

The country's long-term economic diversification strategy is increasing investment in industries that require large volumes of structural steel. Also, the domestic steel manufacturers are expanding production capacity to meet growing local demand while reducing dependence on imports. Industrial development, logistics expansion, and urban construction continue creating stable business opportunities for carbon steel producers. These investments are expected to support long-term market growth across the Middle East.

South Africa

The country is increasingly expanding its industry through increasing demand from construction, mining, packaging, and industrial manufacturing sectors. Also, infrastructure maintenance, commercial development, and residential construction projects continue supporting the consumption of paints, coatings, and adhesive products. Furthermore, manufacturers are adopting improved production technologies to deliver better-quality and environmentally friendly polymer solutions.")

Segmental Insights

Type Insights

The low carbon steel segment dominated the market with 56% share in 2025 and is expected to grow at the CAGR of 5% over the forecast period, as it offers an excellent balance between strength, affordability, flexibility, and ease of manufacturing. It is widely used in construction, automotive parts, machinery, pipelines, appliances, and general engineering because it is easy to weld, shape, and process. Manufacturers also prefer low carbon steel because production costs remain lower compared to other steel grades. The material performs well in large-volume applications where cost efficiency is important.

The high carbon steel segment held a 16% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 5.50% in the forecast period, owing to industries increasingly requiring materials with greater hardness, wear resistance, and long service life. It is becoming more important for manufacturing cutting tools, industrial equipment, mining machinery, springs, railway components, and heavy engineering products. As industrial automation, mining activities, and advanced manufacturing continue expanding, demand for durable high-performance steel is expected to increase. Manufacturers are also improving production technology to enhance the quality of high-carbon steel.

Carbon Steel Market Share,By Type, 2025(%)

| By Type | Market Share (%) |

| Low Carbon Steel | 56.00% |

| Medium Carbon Steel | 28.00% |

| High Carbon Steel | 16.00% |

Application Insights

The construction segment dominated the market with 43% share in 2025 and is expected to grow at the CAGR of 4.70% over the forecast period, owing to carbon steel being an essential material for buildings, bridges, highways, airports, industrial facilities, commercial complexes, and residential housing. The material provides excellent structural strength while remaining cost-effective for large projects. Growing urbanization, population growth, and government investment in public infrastructure continue increasing demand for construction steel. Carbon steel is also widely used in reinforcement bars, structural beams, roofing systems, and foundation components.

The others segment held a 15% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 5.30% in the forecast period, owing to carbon steel finding increasing use across renewable energy, industrial machinery, agricultural equipment, railway systems, defense, and specialized manufacturing applications. As industries modernize production facilities and expand infrastructure, demand for customized carbon steel products is increasing. Renewable energy projects, logistics equipment, and industrial automation are also creating new opportunities outside traditional construction and automotive markets. This wider range of applications is expected to increase carbon steel consumption across several industries.

Carbon Steel Market Share,By Application, 2025(%)

| By Application | Market Share (%) |

| Construction | 43.00% |

| Automotive | 24.00% |

| Ship Building | 18.00% |

| Others | 15.00% |

Recent Developments

- In July 2026, JSW Steel established its latest carbon steel project in India. Also, the company has made a greater investment to establish its project, and the investment cost is around INR 163.50 billion as per the published report. Furthermore, this project is expected to improve regional logistics operations as per the company's claim.(Source: www.steelradar.com)

Competitive Analysis

The industry is highly competitive, akin to companies investing in cleaner production technologies, plant modernization, automation, digital manufacturing, and capacity expansion. Also, competition is based on product quality, manufacturing efficiency, sustainability, production cost, and global supply capability. Leading steel manufacturers are also strengthening their positions through strategic partnerships, acquisitions, research activities, and expansion into high-growth markets.

ArcelorMittal is continuing investments in low-carbon steel production and recently highlighted progress in its sustainability program, including reduced carbon emissions and advanced decarbonization projects.

- Nippon Steel is expanding advanced steel technologies, strengthening sustainability initiatives, and continuing investments following its global business expansion activities with the mid- and longer-term industry strategies. (Source:cdn.arcelormittal.com)

Top Vendors in the Carbon Steel Market & Their Offerings

| Company | Company Type/Position | Major Headquarters | Geographic Presence | Offerings | Key Strength |

| China Baowu Steel Group | State-Owned Megacorporation / Global Production Leader | Shanghai, China | Overwhelming dominance across Asia with a massive distribution network supplying steel worldwide. | Hot-rolled and cold-rolled carbon steel coils, heavy structural building plates, automotive steel sheets, and specialized wire rods. | Massive global R&D ecosystem and unparalleled manufacturing scale for architectural coatings and high-performance industrial barriers. |

| ArcelorMittal | Multinational Industrial Giant / Premier Western Steelmaker | Luxembourg City, Luxembourg | Extensive industrial footprint with major mining and manufacturing hubs spanning Europe, the Americas, Africa, and Asia. | High-strength structural carbon steel beams, pipeline steel, tin-plated packaging steel, and tailored blanks for car chassis. | Industry-leading expertise in high-performance eco-friendly coatings designed to comfortably pass hyper-strict global VOC and environmental regulations. |

| Nucor Corporation | Sustainable Mini-Mill Pioneer / North American Market Leader | North Carolina, USA | Heavily concentrated across North America with strategic international trade offices and subsidiary lines. | Structural steel angles and channels, carbon steel bars, metal building systems, steel joists, and recycled-content sheets. | Vertical raw-material integration (controlling its own acetyl chain inputs), which protects margins from raw material price volatility. |

Other Key Players

- Nippon Steel Corporation

- POSCO

- HBIS Group

- JFE Steel Corporation

- Tata Steel Limited

- United States Steel Corporation

- JSW Steel Limited

- ThyssenKrupp AG

Segments Covered

By Type

- Low Carbon Steel

- Hot Rolled Low Carbon Steel

- Cold Rolled Low Carbon Steel

- Galvanized Low Carbon Steel

- Medium Carbon Steel

- Forged Medium Carbon Steel

- Heat-Treated Medium Carbon Steel

- High Carbon Steel

- Tool Grade High Carbon Steel

- Spring Steel

- Wire Rod Grade

By Application

- Ship Building

- Hull Structures

- Deck Components

- Offshore Platforms

- Construction

- Structural Steel

- Reinforcement Bars

- Bridges

- Industrial Buildings

- Automotive

- Chassis

- Body Panels

- Powertrain Components

- Suspension Systems

- Others

- Railways

- Machinery

- Energy

- Consumer Goods

By Region

- North America

- U.S.

- Canada

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Sweden

- Denmark

- Norway

- Asia Pacific

- China

- Japan

- India

- South Korea

- Thailand

- Latin America

- Brazil

- Mexico

- Argentina

- Middle East & Africa

- South Africa

- UAE

- Saudi Arabia

- Kuwait

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

Tags

Select User License to Buy

Figures (2)