Content

What is the Current Aroma Chemicals Market Size and Share?

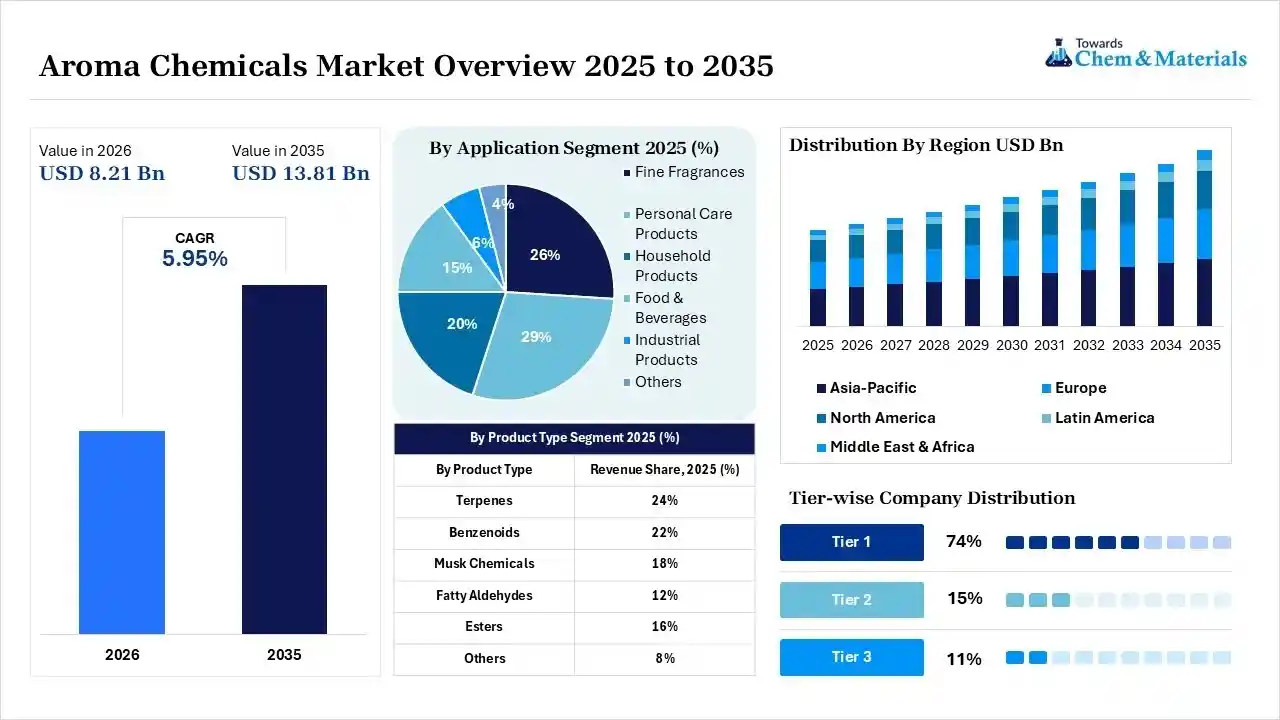

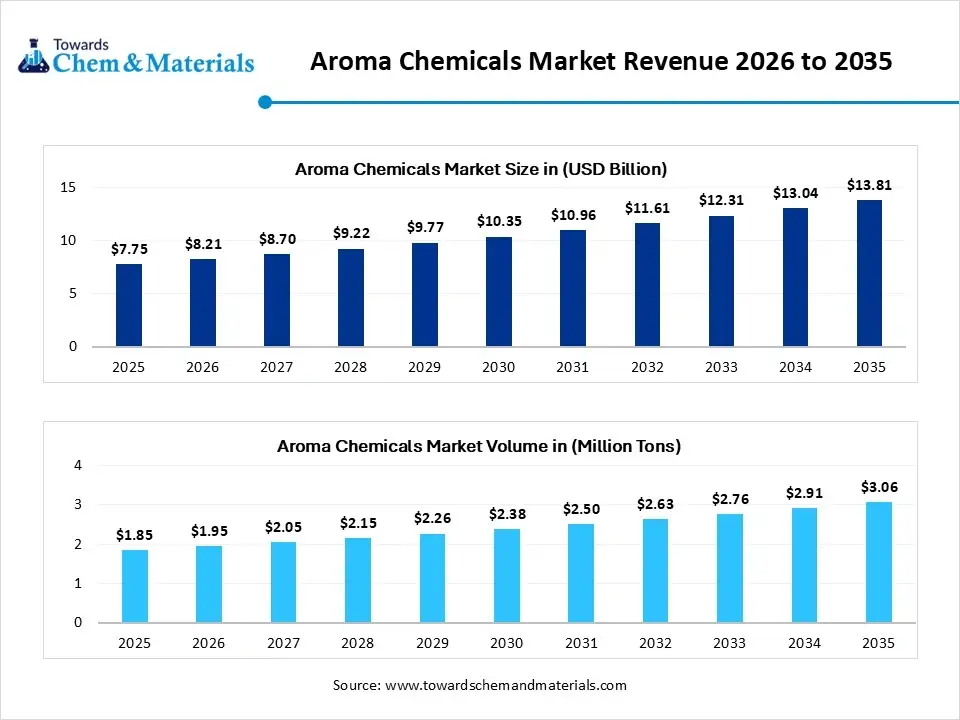

The global aroma chemicals market size was valued at USD 7.75 billion in 2025, is estimated to reach USD 8.21 billion in 2026, and is projected to reach USD 13.81 billion by 2035, exhibiting a compound annual growth rate (CAGR) of 5.95% over the forecast period from 2026 to 2035.Asia Pacific dominated the aroma chemicals market with the largest revenue share of 39.0% in 2025 and is expected to grow at the fastest CAGR of 6.08% during the forecast period. In terms of volume, the aroma chemicals market is projected to grow from 1.85 million tons in 2025 to 3.06 million tons by 2035. growing at a CAGR of 5.15% from 2026 to 2035. Increasing sales of ready-to-eat and packaged foods across the globe is the key factor driving market growth. Also, a surge in consumer need for premium sensory experiences coupled with the changing personal care habits and advancements in production technologies can fuel market growth further.

Market Highlights

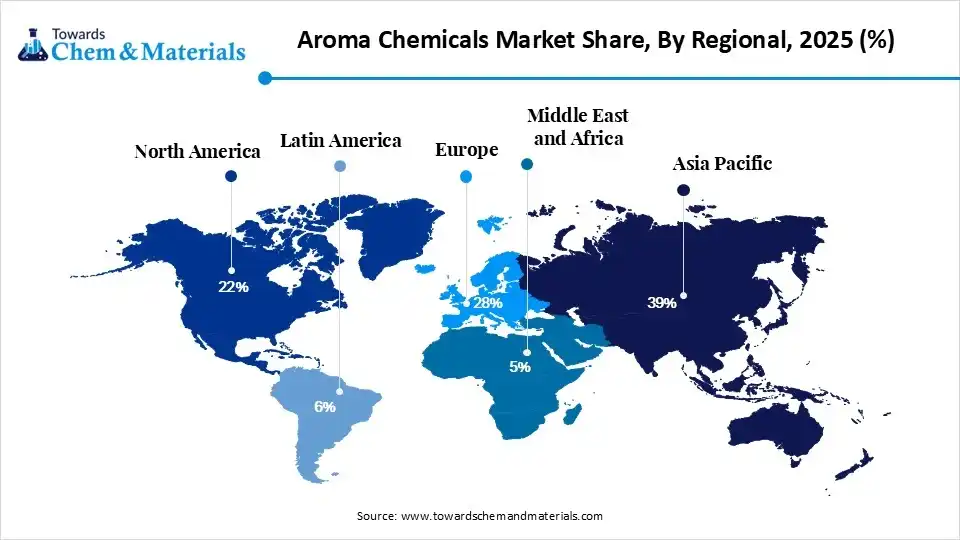

- By region, Asia Pacific dominated the market with the largest share of 39.0% in 2025. The dominance of the region can be attributed to the increasing demand for personal care products, fine fragrances, and processed foods.

- By region, Europe held a market share of 28% in 2025 and was expected to grow at the fastest CAGR of 7.10% over the forecast period. The growth of the region can be credited to the increasing consumer demand for clean-label cosmetics.

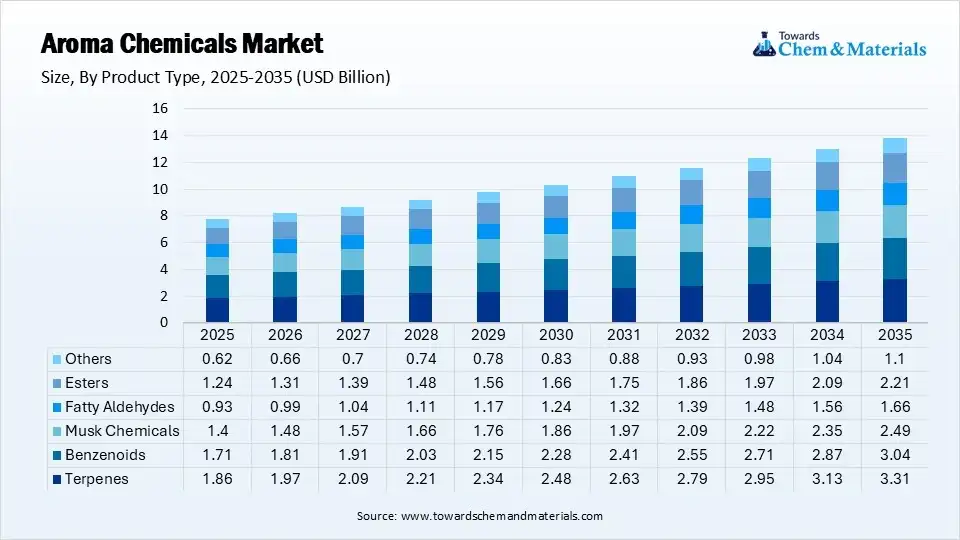

- By product type, the terpenes segment dominated the market with the largest share of 24% in 2025. Terpenes are naturally occurring organic compounds produced by plants. They are generally sought after for their fresh scents in fine fragrances.

- By product type, the musk chemicals segment held a market share of 18.00% in 2025 and is expected to grow at the fastest CAGR of 6.8% over the forecast period. This segment emphasizes compounds that offer long-lasting and distinct scent profiles.

- By source, the synthetic segment dominated the market with the largest share of 71% in 2025. Manufacturers are increasingly preferring synthetic sources as they cost less, give a consistent quality, and scale easily for mass production in food, cosmetics, and household items.

- By source, the natural segment held a market share of 29.0% in 2025 and is expected to grow at the fastest CAGR of 7.30% over the forecast period. Natural chemicals are gentler and more sensitive on skin and offer much calmer effects.

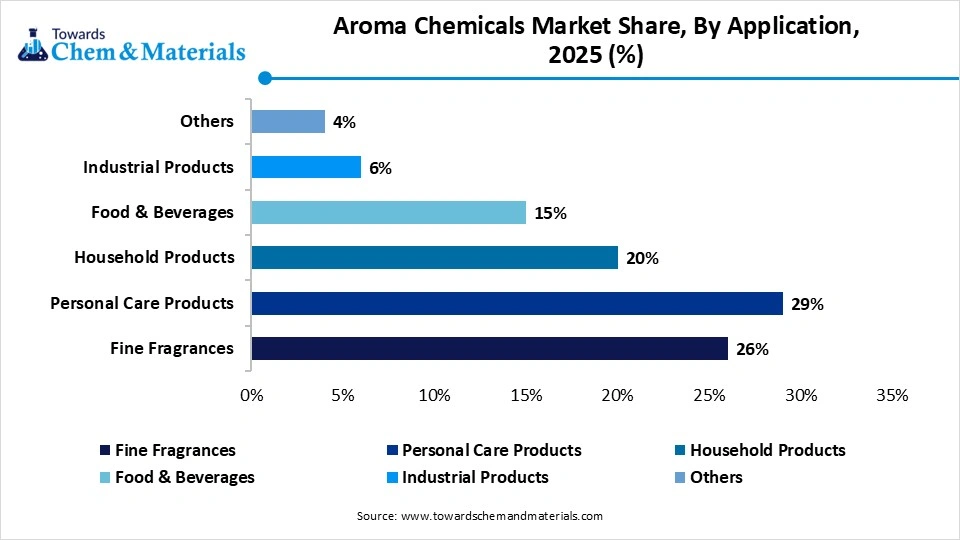

- By application, the personal care products segment dominated the market with the largest share of 29% in 2025. Aroma chemicals offer the core scents and therapeutic benefits in different personal care products.

- By application, the food & beverages segment held a market share of 15.0% in 2025 and is expected to grow at the fastest CAGR of 6.90% during the projected period. Synthetic aroma chemicals give high formulation stability and taste consistency.

- By end use, the consumer goods manufacturers segment dominated the market with the largest share of 35% in 2025. The end-use segment determines production capacity, innovation pathways, and resource acquisition across the broader chemical category.

- By end use, the food & beverage manufacturers segment held a market share of 19.0% in 2025 and was expected to grow at the fastest CAGR of 6.70% during the forecast period. F&B producers use these compounds to improve flavors and replace expensive natural extracts.

Quick Stats at a Glance

- Market in Size 2025: USD 7.75 Billion | CAGR (2026–2035): 5.95%

- Market Estimated Size in 2026: USD 8.21 Billion

- Market Projected Size by 2035: USD 13.81 Billion

- Asia Pacific: largest Regional Market Revenue Share of 39% in 2025 | USD 3.02 Billion

- Europe: Fastest-growing Regional Market Revenue Share of 28% in 2025 | USD 2.17 Billion

- By country: The China held the largest Market share of 49% in 2025

- Market Volume in 2025: 1.85 Million Tons| Volume CAGR (2026–2035): 5.15%

- Market Estimated Volume in 2026: 1.95 Million Tons

- Market Projected Volume by 2035: 3.06 Million Tons

- Market Pricing (2025):

- Average Manufacturing Price: USD 5,470/Ton

- Average Selling Price: USD 6,680/Ton

- Pricing CAGR (2026–2035): 2.35%

The aroma chemical industry belongs to compounds that provide the fragrances and flavours to various industries. The aroma chemicals have different types, like nature-identical, natural, and synthetic. Furthermore, the aroma chemicals are generally single compounds which is blended and offer long-lasting fragrances as per the recent industry observation.

The surge in demand for fragrances in many applications, such as industrial and home care uses, is presenting crucial opportunities in the market. Allergen assessment and stability testing are necessary factors in ensuring the overall safety and quality of these chemicals. Consumer emphasis on sustainable and natural ingredients has facilitated the environmental impact reduction.

- For instance, Hindustan Unilever Limited (HUL) inaugurated the Unilever Fragrance Hub (UFH) in Mumbai to accelerate fragrance development. The new global innovation facility will enhance India's role in the company's research and development network. This investment is part of Unilever’s broader €100 million program to expand digital-first fragrance creation.(Source: hdfcsky.com)

Quality control and maintaining safety standards are crucial to keep consumer trust and ensure the effectiveness of aroma chemicals.

Global Investment Flow for Aroma Chemicals 2026

Major market players are transitioning their focus more towards bio-based compounds and increasing manufacturing to fulfill consumer demand for clean label and sustainable personal care products.

- During 2025, the United States exported essential oils valued at $787 million, ranking this commodity 304th out of 1,232 total exported products from the nation. The primary international destinations for these exports included China ($71.4M), Mexico ($55.7M), Ireland ($55.2M), Canada ($54.9M), and Japan ($53.9M).(Source: oec.world)

The increasing preference towards sustainable and natural products is impelling the market towards fermentation and biotechnology. These methods create natural and synthetic aroma chemicals more affordably while reducing their environmental footprint.

Market Trends

- Increasing demand for personal care products and cosmetics is the latest trend in the market shaping positive market growth. Fragrances and other perfumes need aroma chemicals to create long-lasting and unique fragrance-boosting appeal for different consumers.

- In recent years, aroma chemicals are increasingly used in major quantities within the food and beverage industry as flavoring agents. Hence, consumer preference towards aromatic sensory experiences makes aroma chemicals a crucial part of food manufacturers' advancements.

- Growing demand for natural and plant-based fragrances is the future trend in the market driving expansion. As consumers are increasingly becoming health conscious and environmentally aware, the need for aroma compounds extracted from essential oils, botanicals, and fermentation processes is growing across various industries.

Report Scope

| Report Attributes | Details |

| Market Size in 2026 | USD 8.21 Billion/ 1.95 Million Tons |

| Expected Size by 2035 | USD 13.81 Billion/ 3.06 Million Tons |

| Growth Rate from 2025 to 2035 | CAGR 5.95% |

| Base Year of Estimation | 2025 |

| Forecast Period | 2025 - 2035 |

| Leading Region | Asia Pacific |

| Segment Covered | By Product Type, By Source, By Application, By End User, By Regions |

| Key Companies Profiled | Kao Corporation, LANXESS, MANE, PFW Aroma Chemicals (Kelkar Group), Robertet, S H Kelkar and Company, Symrise AG, Takasago International Corporation |

AI-Powered Predictive Formulations in the Aroma Chemicals Market

AI-powered predictive formulations are revolutionizing the market by transforming complex molecular data into commercial fragrance compositions. By using ML, the sector can now map the whole molecular structures directly to sensory traits, boosting time to market and regulatory compliance. Furthermore, these systems can also map chemical volatility against sensory inputs.

Supply Chain Analysis of the Aroma Chemicals Market

- Production & Processing:It includes the methods used to create and refine the scent and flavor compounds used in everyday products. It converts raw materials into high-quality, stable ingredients that perfume makers and food producers use to scent or flavor their goods. Common processing techniques are solvent extraction, steam distillation, and fractional distillation.

- BASF SE (Germany): A global leader in large-scale petrochemical synthesis and aroma intermediates. BASF focuses heavily on carbon reduction, recently launching eco-forward ingredients like L-Menthol FCC and investing in massive new citral plants in China.

- Other Key Players: Solvay, Takasago International Corporation

- Quality Testing and Certification :It ensures that fragrance ingredients should meet global purity, safety, and ethical standards. Strict laws need companies to test all scents. This proves the chemicals are safe to use on human skin. This stage serves as the major barrier preventing adulterated, toxic, or inconsistent products from reaching consumers.

- Givaudan: The global leader, heavily invested in bio-fabricated transparency and strict allergen-mapping software to align with EU 2026 mandates.

- Other Key Players: Privi Specialty Chemicals, Solvay

- Distribution to Industrial Users :It includes how scent and flavor molecules move from factories to the makers of finished goods such as soaps, perfumes, and foods. Major players use direct sales or distributors to supply these vital ingredients to major brands. High-volume buyers need cost-effective and highly stable synthetic compounds that can bear harsh chemical bases.

- Symrise (Germany): A major supplier of both synthetic and natural aroma chemicals and cosmetic ingredients.

- Other Key Players: Takasago, Privi Specialty Chemicals.

Aroma Chemicals Market’s Regulatory Landscape: Global Regulations

| Country/Region | Key Regulations |

| European Union | Allergen expansion: Expanded declarable fragrance allergens from 26 to over 80 substances (54 individual chemicals, 28 natural extracts). |

| United States | MoCRA (Modernization of Cosmetics Regulation Act): Enforces stronger rules on ingredient safety and reporting. Brands must register their products and report any health problems caused by scented items. |

| India | Follows BIS (Bureau of Indian Standards) rules. India's large production hubs align with global environmental regulations to export fine fragrances and soaps to Europe and the US. |

Market Dynamics

Driver

Sustainability Trends in Manufacturing

Sustainability is increasingly becoming the major factor driving the growth of the market. As consumers and market players are heavily focusing on using sustainable practices. The demand for natural aroma chemicals is growing. In addition, manufacturers are increasingly adopting environmentally responsible production methods and securing raw materials from ethical sources. Hence, the market is poised for a significant increase in the development of sustainable alternatives.

Restraint

Raw Material Price Volatility

Natural ingredients such as vanilla or patchouli rely heavily on farming. Hence, weather, pests, and climate change make their supply uncertain and prices highly unstable, which is the major factor hindering market growth. Moreover, the heavy concentration of essential chemical intermediates and botanical feedstocks within specific global trade corridors makes supply networks vulnerable. Increased geopolitical friction and the enforcement of protective import tariffs substantially inflate the final landed costs of these crucial materials.

Opportunity

Technological Advancements in Aroma Production

Technological innovations are playing a key role in shaping positive market trajectory over the forecast period, creating lucrative opportunities in the market soon. Advancements in manufacturing techniques, including biotechnology and advanced extraction methods, are improving the overall quality and efficiency of aroma chemical production. Furthermore, these advancements enable the synthesis of novel aroma compounds, which were previously unattainable. This broadens market potential and creates market demand soon.

Segmental Insights

Product Type Insights

The terpenes segment dominated the market with the largest share of 24% in 2025. Terpenes are naturally occurring organic compounds produced by plants. They are generally sought after for their fresh scents in fine fragrances, cosmetics, and household care. Companies are using terpenes to make soaps, perfumes, and cleaning products. In addition, companies are increasingly utilizing microbial fermentation as an alternative to traditional botanical extraction from trees or fruits. This bio-based process leverages engineered yeast or bacterial strains to metabolize simple sugars, synthesizing high-value terpene compounds such as limonene and santalene.

The musk chemicals segment held a market share of 18.00% in 2025 and is expected to grow at the fastest CAGR of 6.8% over the forecast period. This segment emphasizes compounds that offer long-lasting and distinct scent profiles. They act as necessary base notes and fixatives in the fragrance industry. These materials are extracted directly from plant or animal sources. Due to strict ethical and conservation restrictions on animal-derived musks, the natural musk relies primarily on botanical extracts. Hence, these ingredients have a premium price and are exclusively reserved for luxury fine fragrances.

The musk chemicals segment held a market share of 18.00% in 2025 and is expected to grow at the fastest CAGR of 6.8% over the forecast period. This segment emphasizes compounds that offer long-lasting and distinct scent profiles. They act as necessary base notes and fixatives in the fragrance industry. These materials are extracted directly from plant or animal sources. Due to strict ethical and conservation restrictions on animal-derived musks, the natural musk relies primarily on botanical extracts. Hence, these ingredients have a premium price and are exclusively reserved for luxury fine fragrances.

Aroma Chemicals Market Share, By Product Type, 2025 (%)

| By Product Type | Revenue Share, 2025 (%) |

| Terpenes | 24% |

| Benzenoids | 22% |

| Musk Chemicals | 18% |

| Fatty Aldehydes | 12% |

| Esters | 16% |

| Others | 8% |

Source Insights

The synthetic segment dominated the market with the largest share of 71% in 2025. Manufacturers are increasingly preferring synthetic sources as they cost less, give a consistent quality, and scale easily for mass production in food, cosmetics, and household items. Synthetic aroma chemicals are generally used in cost-sensitive, high-volume products. This includes household cleaners, laundry detergents, and everyday cosmetics. Major market players, including BASF SE and Symrise, are utilizing fermentation technologies to develop bio-identical synthetic alternatives that align with the growing consumer demand for clean-label products.

The natural segment held a market share of 29.0% in 2025 and is expected to grow at the fastest CAGR of 7.30% over the forecast period. Natural chemicals are gentler and more sensitive on skin and offer much calmer effects. Market players use bacteria, yeast, and enzymatic processes to breed complex molecules organically. In the extraction process, molecules are directly extracted from various botanical components, including flowers, bark, leaves, seeds, roots, and citrus peels.

Aroma Chemicals Market Share, By Source, 2025 (%)

| By Source | Revenue Share, 2025 (%) |

| Synthetic | 71% |

| Natural | 29% |

Application Insights

The personal care products segment dominated the market with the largest share of 29% in 2025. Aroma chemicals offer the core scents and therapeutic benefits in different personal care products. The industry is increasingly shifting towards sustainable sourcing and green chemistry. The Asia-Pacific region serves as a primary global hub for the manufacturing of personal care chemicals, with a particularly high concentration of production facilities situated in India. Synthetic musk’s and stable benzenoids are the favored elements in this segment. These molecules resist degradation when exposed to the harsh chemical bases and active surfactants found in soaps.

")

The food & beverages segment held a market share of 15.0% in 2025 and is expected to grow at the fastest CAGR of 6.90% during the projected period. Synthetic aroma chemicals give high formulation stability and taste consistency. They are heavily used in mass-market convenience foods, low-cost confectionery, and carbonated soft drinks. Also, synthetic vanillin, ethyl vanillin, maltol, and ethyl maltol constitute primary chemical additives used in the food and beverage industry to simulate sweet, creamy, and baked flavor characteristics, leading to segment growth further.

Aroma Chemicals Market Share, By Application, 2025 (%)

| By Application | Revenue Share, 2025 (%) |

| Fine Fragrances | 26% |

| Personal Care Products | 29% |

| Household Products | 20% |

| Food & Beverages | 15% |

| Industrial Products | 6% |

| Others | 4% |

End User Insights

The consumer goods manufacturers segment dominated the market with the largest share of 35% in 2025. The end-use segment determines production capacity, innovation pathways, and resource acquisition across the broader chemical category. Moreover, this product category incorporates synthetic fragrances into hair and personal care items. Segment expansion relies on functional wellness components, as consumers expect these scents to deliver therapeutic benefits like stress reduction. Shifting consumer priorities have prompted manufacturers to implement green biotechnology, impacting positive market growth soon.

The food & beverage manufacturers segment held a market share of 19.0% in 2025 and was expected to grow at the fastest CAGR of 6.70% during the forecast period. F&B producers use these compounds to improve flavors, replace expensive natural extracts, and keep sensory appeal in processed foods. Furthermore, food and beverage aroma chemicals are subject to strict regulations by global agencies, including the US FDA and European authorities. This increases market penetration for large chemical suppliers such as DSM-Firmenich, Givaudan, and Symrise.

Aroma Chemicals Market Share, By End User, 2025 (%)

| By End User | Revenue Share, 2025 (%) |

| Consumer Goods Manufacturers | 35% |

| Food & Beverage Manufacturers | 19% |

| Fragrance & Perfume Manufacturers | 28% |

| Industrial Manufacturers | 12% |

| Others | 6% |

Regional Analysis

How did Asia Pacific Dominated the Aroma Chemicals Market in 2025?

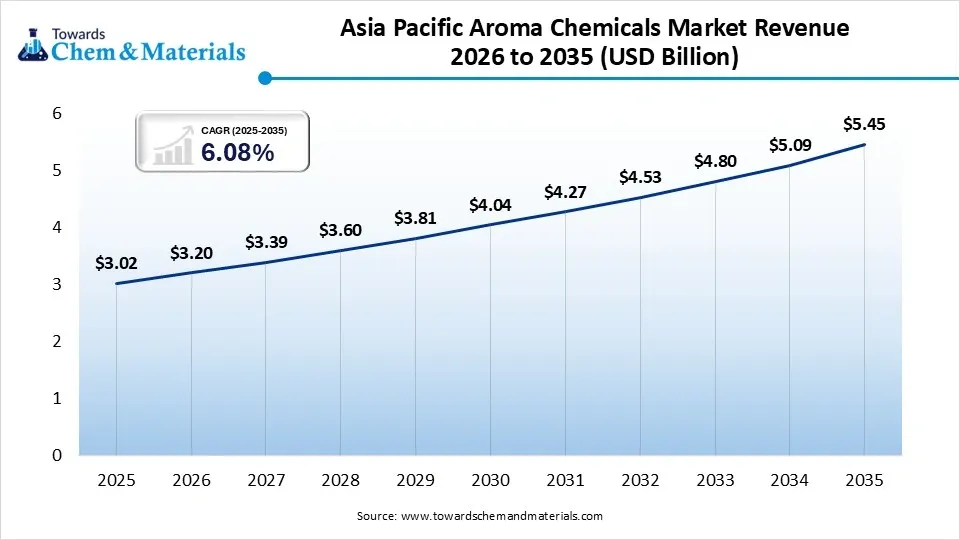

The Asia Pacific aroma chemicals market size was estimated at USD 3.02 billion in 2025 and is projected to reach USD 5.45 billion by 2035, growing at a CAGR of 6.08% from 2026 to 2035.Asia Pacific dominated the market with the largest share of 39.0% in 2025. The dominance of the region can be attributed to the increasing demand for personal care products, fine fragrances, and processed foods in highly populated countries such as China, India, and Indonesia. In addition, leading manufacturers are using advanced scientific methods to produce high-quality, cost-effective fragrances. By employing biotechnological techniques, such as microbial fermentation, companies synthesize identical scent molecules in laboratory environments.

China

China

- China has leading chemical manufacturing hubs. Efficient production scales lower the costs of chemical making.

- A rapidly expanding middle-class population has higher purchasing power, accelerating consumer spending on scented goods.

India

- India’s expanding middle class and growing urbanization drive the massive consumption of cosmetics, soaps, and fine fragrances.

- The shift to premium household items such as fabric softeners and concentrated detergents increases the need for long-lasting scent boosters.

The Europe aroma chemicals market size was estimated at USD 2.17 billion in 2025 and is projected to reach USD 3.94 billion by 2035, growing at a CAGR of 6.15% from 2026 to 2035.Europe held a market share of 28% in 2025 and was expected to grow at the fastest CAGR of 7.10% over the forecast period. The growth of the region can be credited to the increasing consumer demand for clean-label cosmetics, perfumes, and natural home care products along with the high preference for niche and luxury perfumes. The leading corporations are investing highly in R&D to develop sustainable extraction methodologies & biodegradable product alternatives.

Germany

- The need for household cleaners and detergents is growing; hence, consumers want pleasant scents to make their cleaning products feel premium.

- Major German companies invest heavily in nature-friendly technology. They use biotechnology to produce sustainable, natural-identical scents.

France

- France is the global epicenter for fine fragrances. An increase in demand for premium and niche perfumes drives constant innovation in aroma compounds.

- Consumers want natural and bio-based aromas. This transition the market toward natural extracts and safe, nature-identical synthetic chemicals.

The North America aroma chemicals market size was estimated at USD 1.71 billion in 2025 and is projected to reach USD 3.11 billion by 2035, growing at a CAGR of 6.16% from 2026 to 2035.North America held a market share of 22.00% in 2025. The growth of the region can be linked to the escalating demand for premium fine fragrances and a post-pandemic rise in the consumption of household hygiene products, along with a significant consumer transition toward clean-label and natural, bio-based ingredients. Also, major market players are synthetic chemistry and biotech investments to create sustainable, greener, and more sustainable fragrance molecules.

United States

- Companies now use biotechnology (like fermentation) to extract or build natural scents from plant sugars, leading to market growth soon.

- The demand for niche, high-quality perfumes and "clean" cosmetic products fuels the need for premium and specialized aroma ingredients.

Canada

- An increasing Canadian standard of living and high consumer purchasing power drive continuous demand for luxury and daily-use personal care products.

- The surge in use of flavorings in functional foods, beverages, and organic products requires a steady supply of food-grade aroma chemicals.

The Latin aroma chemicals market size was estimated at USD 0.47 billion in 2025 and is projected to reach USD 0.90 billion by 2035, growing at a CAGR of 6.71% from 2026 to 2035.Latin America held a market share of 6.00% in 2025. The growth of the region can be driven by an increasing middle-class population, ongoing urbanization, and robust cultural demand for premium personal care products and processed foods. There is an increasing consumer demand for convenience foods, snacks, and flavoured beverages. Hence, aroma chemicals have become essential for enhancing the flavor profiles and olfactory appeal of these packaged goods.

Brazil

- Brazil is one of the world's largest markets for beauty, perfumes, and deodorants. The increasing demand for fine fragrances and daily cosmetics heavily boosts aroma chemical consumption.

- Brazil's rich biodiversity offers an excellent foundation for locally sourced, natural ingredients. Hence, leading flavor and fragrance companies are investing in local production and research.

Argentina

- Rising consumer interest in sophisticated, long-lasting scent profiles and niche fine fragrances.

- Argentina’s large food processing sector relies heavily on aroma chemicals for a competitive edge, accelerating the market growth.

")

The Middle East & Africa aroma chemicals market size was estimated at USD 0.39 billion in 2025 and is projected to reach USD 0.76 billion by 2035, growing at a CAGR of 6.90% from 2026 to 2035.The Middle East & Africa held a market share of 5.00% in 2025. The growth of the region can be attributed to the increasing consumer preference for luxury fine fragrances, the ongoing expansion of the personal care sector, and a strategic industry moving toward sustainable, natural ingredients. In addition, aroma chemicals are used to flavor food and beverages. This demand is driven by the growth of the food processing industry in Africa and the Middle East.

Saudi Arabia

- The strong demand for fine fragrances and attars remains a primary driver for high-end aroma chemical consumption.

- Increasing purchasing power and evolving personal grooming habits among the country's young, digitally connected population are propelling the usage of everyday personal care products.

UAE

- The UAE has a deep cultural and commercial appreciation for high-end oud, fine perfumes, and exotic scents. This drives massive local consumption of aroma chemicals.

- Rapid growth in local cosmetic, toiletry, and household cleaning sectors offers a steady demand for everyday scent compounds.

Competitive Analysis

The market is highly consolidated and competitive, dominated by five major players: BASF SE, Givaudan, Symrise, DSM-Firmenich, and IFF. These industry leaders use vertically integrated supply chains and biotechnology to fuel innovation while fulfilling strict regulations.

- The BASF Aroma Ingredients business unit has officially commissioned three new world-scale production facilities. This global expansion includes newly constructed plants for menthol and linalool in Ludwigshafen, Germany.

- Givaudan has formally announced the strategic expansion of its operations in Turkey, representing a significant milestone in the corporation’s ongoing regional development.(Source: basf.com),(Source: givaudan.com)

Competitive Landscape

| Company Name | Headquarters | Country | What They Do | Key Strengths & Recent Moves |

| BASF SE | Ludwigshafen | Germany | Produces massive quantities of synthetic aroma molecules (like citral, menthol, and linalool) from petrochemical feedstocks. | Backward-integrated chemical giant expanding capacity with a mega-citral plant in China. |

| Givaudan | Savièr | Switzerland | Creates advanced flavor and fragrance delivery systems, proprietary synthetic molecules, and biotechnology-driven ingredients. | World's largest F&F company collaborated with Privi Speciality Chemicals in the "Prigiv" joint venture. |

| DSM-Firmenich | Kaiseraugst & Geneva / Netherlands | Switzerland / Netherlands | Develops sustainable, bio-based aroma ingredients, nutrition solutions, and eco-friendly fragrance molecules. | Generated through a massive merger; global leader in biotechnology & renewable ingredient production. |

Recent Developments

- In June 2026, Villain, a prominent men’s fragrance and grooming brand within the BRND. The ME portfolio has officially launched in the United States, with distribution established through Amazon. This entry represents a pivotal milestone in the brand's international expansion strategy, aligning with BRND. ME's ongoing initiatives to scale its digital-first consumer brands across global markets.(Source: www.indianretailer.com)

- In September 2025, Natara, a leading independent global manufacturer of flavor and fragrance ingredients, has announced a strategic distribution partnership with Ashapura, an Azelis company, effective October 1, 2025. Under this agreement, Ashapura will manage the distribution of Natara’s premium natural extracts, oils, and specialty aroma chemicals to customers across India.(Source: indianchemicalnews.com)

Other Key Players

- Kao Corporation

- LANXESS

- MANE

- PFW Aroma Chemicals (Kelkar Group)

- Robertet

- S H Kelkar and Company

- Symrise AG

- Takasago International Corporation

Segments Covered in the Report:

By Product Type

- Terpenes

- Limonene

- Pinene

- Myrcene

- Terpineol

- Benzenoids

- Benzyl Alcohol

- Benzaldehyde

- Phenyl Ethyl Alcohol

- Vanillin

- Musk Chemicals

- Polycyclic Musks

- Macrocyclic Musks

- Alicyclic Musks

- Fatty Aldehydes

- Hexanal

- Nonanal

- Decanal

- Esters

- Acetate Esters

- Butyrate Esters

- Salicylate Esters

- Others

- Ketones

- Lactones

- Sulfur Compounds

- Specialty Aroma Molecules

By Source

- Synthetic

- Petrochemical-Based Aroma Chemicals

- Bio-Based Synthetic Aroma Chemicals

- Natural

- Plant-Derived Extracts

- Essential Oil Derivatives

- Fermentation-Derived Ingredients

By Application

- Fine Fragrances

- Luxury Perfumes

- Mass-Market Perfumes

- Personal Care Products

- Skin Care

- Hair Care

- Cosmetics

- Household Products

- Detergents

- Fabric Softeners

- Air Fresheners

- Food & Beverages

- Flavor Enhancers

- Beverage Formulations

- Confectionery Applications

- Industrial Products

- Industrial Cleaners

- Specialty Chemical Formulations

- Others

- Pharmaceuticals

- Aromatherapy Products

By End User

- Consumer Goods Manufacturers

- Personal Care Manufacturers

- Household Product Manufacturers

- Food & Beverage Manufacturers

- Beverage Producers

- Processed Food Producers

- Fragrance & Perfume Manufacturers

- Luxury Fragrance Producers

- Mass Fragrance Producers

- Industrial Manufacturers

- Specialty Chemical Producers

- Cleaning Product Manufacturers

- Others

- Pharmaceutical Companies

- Wellness Product Manufacturers

By Region

North America:

- U.S.

- Canada

- Mexico

- Rest of North America

- South America:

- Brazil

- Argentina

- Rest of South America

Europe:

- Western Europe

- Germany

- Italy

- France

- Netherlands

- Spain

- Portugal

- Belgium

- Ireland

- UK

- Iceland

- Switzerland

- Poland

- Rest of Western Europe

- Eastern Europe

- Austria

- Russia & Belarus

- Türkiye

- Albania

- Rest of Eastern Europe

Asia Pacific:

- China

- Taiwan

- India

- Japan

- Australia and New Zealand,

- ASEAN Countries (Singapore, Malaysia)

- South Korea

- Rest of APAC

MEA:

- GCC Countries

- Saudi Arabia

- United Arab Emirates (UAE)

- Qatar

- Kuwait

- Oman

- Bahrain

- South Africa

- Egypt

- Rest of MEA

Tags

FAQ's

Select User License to Buy

Figures (7)