Content

What is the Vapor Barrier Market Size and Share?

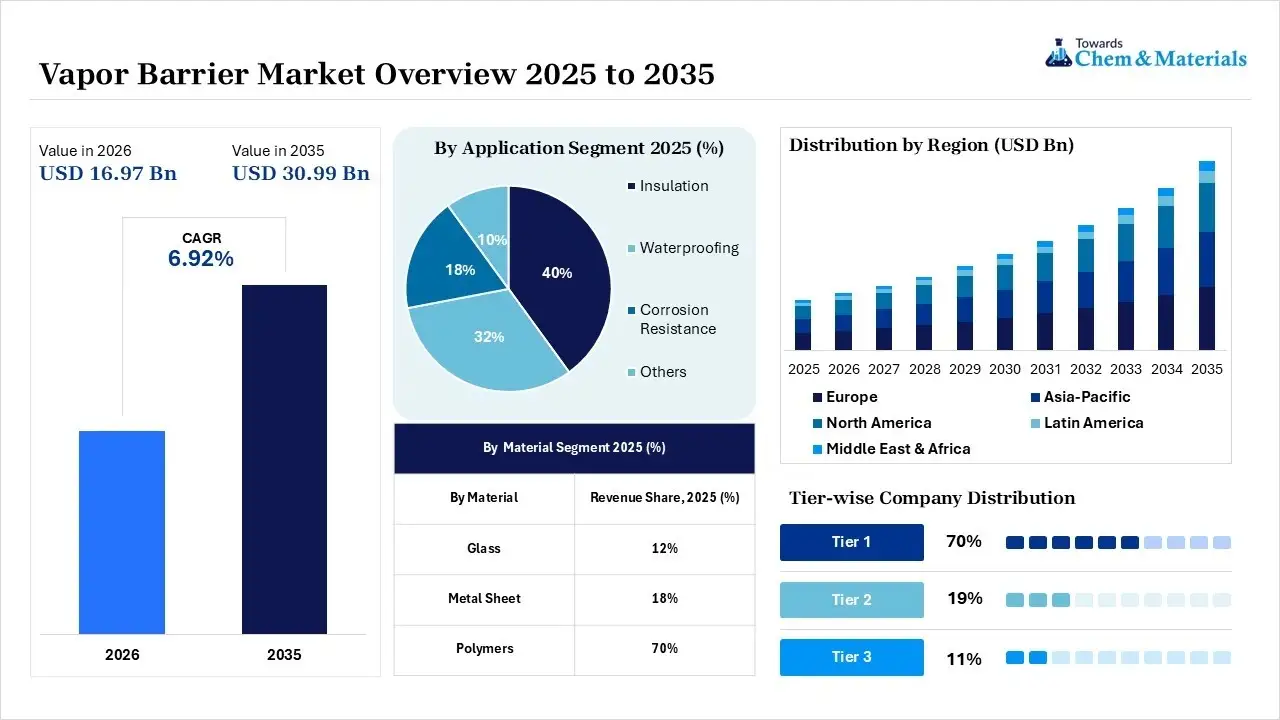

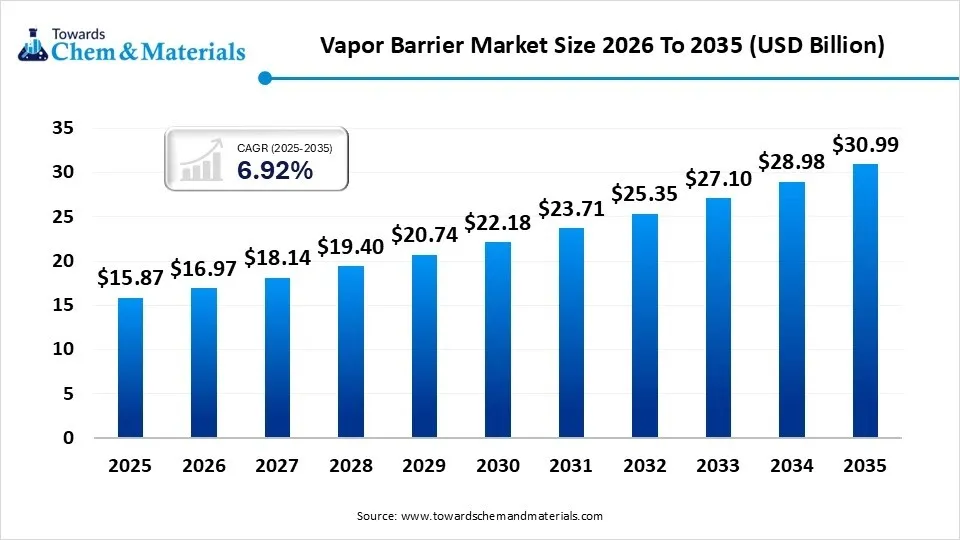

The global vapor barrier market size was valued at USD 15.87 billion in 2025, is estimated to reach USD 16.97 billion in 2026, and is projected to reach USD 30.99 billion by 2035, exhibiting a compound annual growth rate (CAGR) of 6.92% over the forecast period from 2026 to 2035.Asia Pacific dominated the vapor barrier market with the largest revenue share of 40% in 2025 and is expected to grow at the fastest CAGR of 7.05% during the forecast period. As the percentage of sustainable construction grows, the building codes are tighter, and attention is being paid to buildings becoming more energy-efficient, the number of retrofit projects has been increasing, as has awareness of indoor air quality and mold prevention. Advanced solutions for vapor barrier use are further gaining traction in emerging economies due to the speed of urbanisation and infrastructure development.

Market Highlights

- By region, Asia Pacific dominated the vapor barrier market share 40% in 2025. The market is driven by strict building regulations, high construction standards, and widespread adoption of energy-efficient and moisture-resistant building practices.

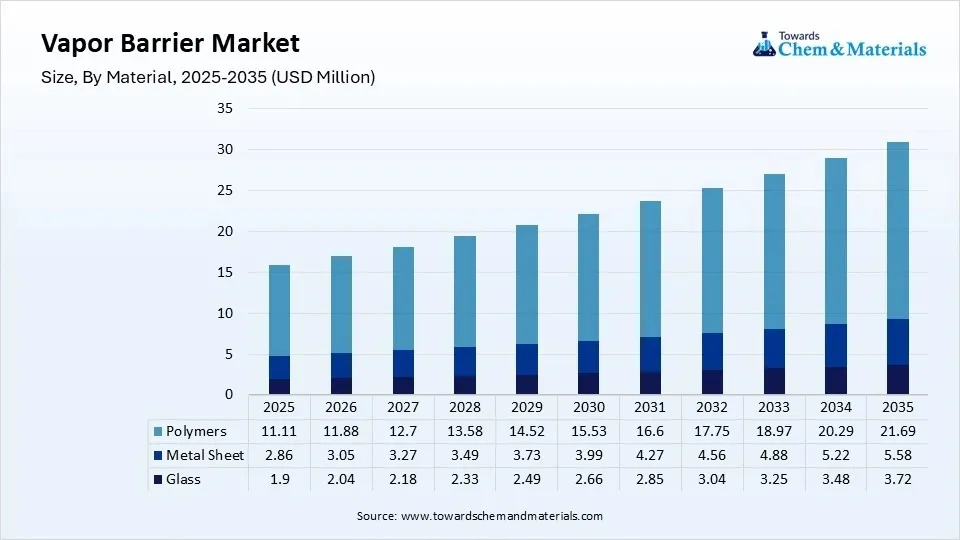

- By material, the polymer segment dominated the market share 70% in 2025. versatility, durability, and cost-effectiveness, increases the demand for the market.

- By application, the insulation segment dominated the market share 40% in 2025. is a major application area for vapor barriers, as controlling moisture is essential to maintaining the effectiveness of thermal insulation.

")

As builders and developers become more interested in energy efficiency, moisture control, and sustainable building practices, the vapor barrier market continues to grow steadily. Advanced vapor control solutions are being used to improve insulation performance and eliminate moisture damage to structures, all in response to strict building codes and green building standards.

There are also fresh growth prospects in the growing retrofit market, increasing construction industry, and the demand for specialized facilities like data centres, cold storage centres, and pharmaceutical manufacturing plants. The industry is undergoing significant changes due to technological innovations such as smart vapor retarders and bio-based membrane solutions, enhancing building performance and sustainability.

- In September 2025, CelluForce introduced CelluShield™, a bio-based barrier coating from renewable cellulose that provides superior oxygen and moisture barrier properties, and is ideal for flexible packaging applications that can be recycled, and circular economy goals.

(Source: www.businesswire.com)

Vapor Barrier Market Trends

- The increasing demand for eco-friendly materials: The growing adoption of sustainable products and growing concerns regarding energy efficiency increase demand for eco-friendly vapor barriers. The eco-friendly vapor barriers are made up of biodegradable & recycled materials. They help in lowering environmental impact and promote sustainable building practices. Manufacturers are focusing on the production of eco-friendly vapor barriers and innovating new materials.

- Growing construction industry in various countries: The growth in the construction industry, like industrial, commercial, residential, and infrastructural projects, increases demand for vapor barrier. Vapor barrier improves energy efficiency, prevents moisture from entering building, protects the structural integrity of the construction, and improves the indoor environment of buildings. Vapor barriers are widely used in various construction applications like roof assemblies, under-slab, and walls.

- Technological advancements: Technological advancements in vapor barriers, like the development of innovative materials, the development of new technologies, the addition of barrier pigments, and improving barrier performance through double coating, help in the growth of the market. The growing advancements like smart vapor barriers, the use of nanotechnology, and aerobic vapor migration barriers, enhance its performance and application in various fields.

Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 15.66 Billion |

| Expected Size By 2034 | USD 25.22 Billion |

| Growth Rate from 2025 to 2034 | CAGR 5.44% |

| Base Year of Estimation | 2024 |

| Forecast Period | 2025-2034 |

| High Impact Region | Asia Pacific |

| Segment Covered | By Material, By Application, By Installation, By End Use , By Region |

| Key Companies Profiled | Glenroy Inc., Celplast Metallized Product Ltd., Polifilm Group, ProAmpac Holdings, Optimum Plastics, Inc., 3M Company, Amcor Limited, SAES Getters S.p.A., Kalliomuovi Oy, GLT Products, UFP Industries, Inc., W.R. Meadows, Inc., BMI Icopal, Carlisle Companies Inc. |

Supply Chain Analysis of the Vapor Barrier Market

Feedstock Procurement

- It includes the procurement of raw materials like polyethylene, polypropylene, asphalt compounds, specialty resins, and performance additives for the production of a vapor barrier. Availability of high-quality polymers is critical for ensuring durability, water resistance, flexibility, and long-term performance in residential, commercial, and industrial building applications.

- Dow Inc.: the world's largest provider of polyethylene resins and specialty polymer materials for high-performance vapor barrier membranes and construction films.

- Other Key Players: ExxonMobil Chemical, LyondellBasell Industries

Chemical Synthesis and Processing

- At this stage, the raw polymers and resins are converted to moisture-resistant materials by the aforementioned polymerization, refining, extrusion, and coating processes. Vapor barriers are durable, resist UV degradation, and provide permeability control with advanced processing technologies that allow them to be effective under various environmental and climatic conditions.

- Berry Global: Advanced film extrusion and polymer processing technology to produce high-performance membranes for use in vapor barrier applications for construction and infrastructure.

- Other Key Players: Saint-Gobain, Carlisle Companies

Compound Formulation and Blending

- It encompasses processing polymers with stabilizers, antioxidants, UV inhibitors, fillers, and specialty additives to tailor a specific vapor barrier formulation. Accurate formulation leads to better water resistance, puncture resistance, thermal stability, and insulation system, and contemporary building envelope performance.

- BASF SE: Supplies specialty additives and performance-enhancing materials, which enhance the strength, flexibility and environmental resistance of the vapor barrier.

- Other Key Players: Sika AG, 3M

Vapor Barrier Market Opportunity

Rapid Expansion of the Construction Industry in Emerging Economies

One of the major opportunities contributing to the growth of the vapor barrier market is the growing and rapid expansion of the construction industry in the emerging economies, where they are experiencing accelerated urbanization and infrastructural development, leading to increased demand for moisture control solutions in residential, commercial, and industrial buildings. The initiatives, such as the smart city mission and substantial investment in infrastructure development, further boost the demand and growth of the market. The regions with humid conditions require and demand efficient moisture management to prevent structural damage and health hazards, which increases demand

Vapor Barrier Market Challenge

Lack Of Awareness and Inconsistent Installation Practices

The vapor barrier market has a key challenge that hinders the growth of the market in the developing region, especially the lack of awareness and inconsistent installation practices. Many builders and contractors overlook the importance of or have poor installation techniques, which leads to reduced effectiveness. Additionally, the selection of inappropriate barrier materials for specific climate conditions results in poor results, and limited availability of skilled labor and lack of training also result in poor performance, which results in less growth and is a challenge to overcome.

Vapor Barrier Market Segmental Insights

Material Insights

The polymer segment dominated the vapor barrier market share 70% in 2025. The polymer segment holds a significant share in the market due to its versatility, durability, and cost-effectiveness, which increases the demand for the market. Polymers such as polyethylene, polypropylene, and polyvinyl chloride (PVC) are widely used since they offer excellent moisture resistance and can be easily manufactured into sheets or films. These materials are lightweight, flexible, and suitable for various applications in construction, especially in insulation and under-slab installations, making them a preferred choice for builders and contractors, which increases the demand for the market.

")

The metal sheet segment expects significant growth in the vapor barrier market during the forecast period. The metal sheet segment in the market is valued for its high strength, durability, and superior resistance to vapor transmission. Typically made from materials like aluminum or galvanized steel, these sheets are used in industrial and commercial buildings where long-term protection and fire resistance are critical. Although heavier and more expensive than polymer options, metal sheets are ideal for harsh environments and are often chosen for roofing and specialized wall applications requiring robust moisture control, which increases the demand and helps in the growth of the market.

Application Insights

The insulation segment dominated the vapor barrier market share 40% in 2025. The insulation segment is a major application area for vapor barriers, as controlling moisture is essential to maintaining the effectiveness of thermal insulation. Vapor barriers are typically installed on the warm side of insulation in walls, roofs, and floors to prevent condensation that can degrade insulating materials and lead to mold growth.

This application improves energy efficiency, indoor comfort, and building longevity, making it a critical component in both residential and commercial construction. The waterproofing segment expects significant growth in the vapor barrier market during the forecast period. In the waterproofing segment, vapor barriers play a vital role in protecting structures from moisture intrusion, especially in basements, foundations, and roofing systems.

These barriers act as a seal to prevent water vapor from penetrating building envelopes, which can lead to structural damage, corrosion, and mold formation. Used alongside other waterproofing materials, vapor barriers enhance the overall moisture management system, ensuring building integrity and longevity in both new construction and renovation projects.

Installation Insights

The membranes segment dominated the vapor barrier market in 2024. The membranes segment is a widely used installation type in the market due to its flexibility, ease of application, and reliable performance. These barriers are typically made from polyethylene, bituminous materials, or synthetic polymers and are applied as sheets or rolls.

Membrane vapor barriers are ideal for roofing, walls, and under-slab installations, offering consistent coverage and resistance to moisture penetration. Their adaptability to various surfaces makes them a preferred choice in modern construction practices. The cementitious segment expects significant growth in the vapor barrier market during the forecast period. The cementitious segment includes vapor barriers made from cement-based coatings that are applied to concrete surfaces to block moisture penetration.

These barriers are especially suited for basements, foundations, and water-retaining structures due to their strong adhesion, durability, and compatibility with masonry substrates. Cementitious vapor barriers are easy to apply and offer excellent resistance to hydrostatic pressure, making them a popular choice for both new constructions and repair projects in high-moisture environments.

End Use Insights

The construction segment dominated the vapor barrier market in 2025. The construction sector represents the largest end-use for vapor barriers, encompassing residential, commercial, and industrial building projects. Demand is driven by stringent building codes, growing emphasis on energy efficiency, and moisture control in new construction and renovation. Vapor barriers in walls, roofs, floors, and foundations prevent condensation, protect components, and extend building lifespan. Retrofit projects further boost adoption as older buildings are upgraded for improved thermal performance and indoor air quality.

The automotive segment expects significant growth in the vapor barrier market during the forecast period. In the automotive segment, vapor barriers are used to protect the interior part of the vehicle and components from moisture, particularly in doors, roofs, and electric battery compartments for EVs, which drives the growth. Polymer-based films and adhesives are applied to prevent the vehicle from corrosion, mold, and electrical failures. Precision in thickness and compatibility with paints and trim is critical. Growing electric vehicle adoption increases the demand for advanced moisture management to ensure safety, reliability, and extended component life, which drives the growth of the market.

Regional Insights

How did the Asia Pacific dominate the Vapor Barrier Market in 2025?

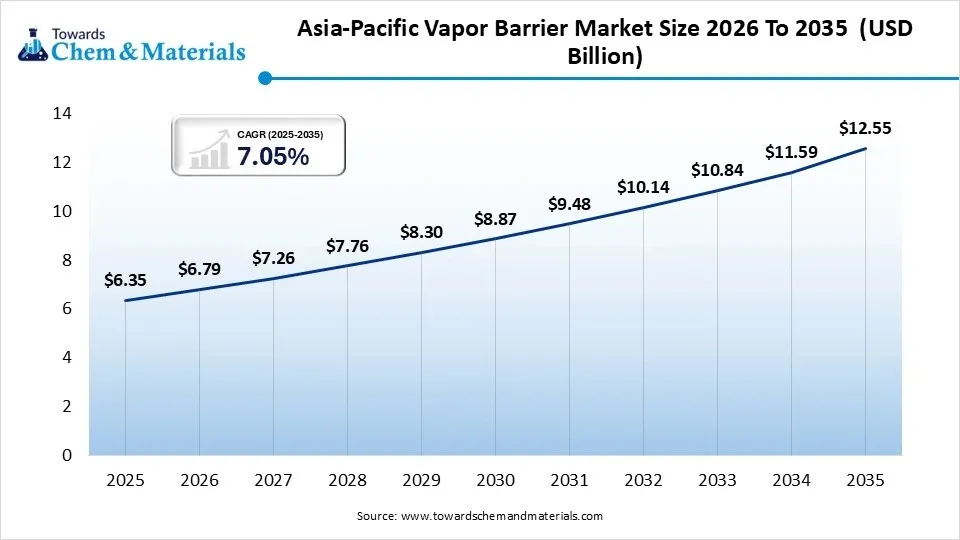

The Asia Pacific vapor barrier market size was estimated at USD 6.35 billion in 2025 and is projected to reach USD 12.55 billion by 2035, growing at a CAGR of 7.05% from 2026 to 2035.Asia Pacific dominated the market with 40% share in 2025, as the region saw a significant volume of both residential and commercial construction activity, especially in high-humidity regions where moisture control is important for the durability of buildings. Demand for vapor barrier membranes increased further throughout the region with the growing use of an energy-efficient building envelope, increased investment in cold storage buildings, and the rapid development of urban infrastructure.

") China

China

- The demand for vapor barriers that prevent condensation and moisture damage to structures due to large-scale residential construction rose.

- Advances in moisture-control membranes promoted by green building initiatives were brought about for energy-efficient building envelope systems.

- The growth of cold-chain logistics infrastructure facilitated the use of high-performance vapor barrier technologies across the country.

India

- High rate of urbanization to increase the vapor barrier demand in residential, commercial, and industrial construction projects.

- Incentives for growing green building certifications led to increased use of moisture-control and energy-saving building materials.

- The development of warehouses and cold storage helped to fuel durable vapor barrier membrane solutions.

North America held 25% market share in 2025 and is expected to grow at the fastest CAGR of 6.2% during the forecast period, as strict building energy codes, broad building retrofit projects, and the building focus on indoor air quality continued. The market grew across the region due to the rise of the use of encapsulated crawl spaces, high-tech insulation systems, and moisture-management techniques in homes and commercial structures.

United States

- For building retrofit projects, vapor barriers to enhance the insulation efficiency and energy performance were required.

- The trend of crawlspace encapsulation spurred the growth of the thick polyethylene vapor barrier membrane system.

- Growth in data center building drove the growth of moisture control equipment for the protection of critical infrastructure assets.

Canada

- The colder climate conditions made the use of vapor barriers for condensation control and optimization of insulation essential.

- The implementation of the net-zero building initiative promoted the use of cutting-edge vapor-retarding membrane technologies across the country.

- Demand for moisture-resistant and energy-efficient building envelope solutions increased as a result of residential renovation activities.

Europe held 22% market share in 2025. Energy-efficiency requirements, the need to renovate old buildings, and a high sustainable construction adoption rate were the reasons behind the growth of the market for the vapor barriers. As builders sought to balance moisture control with building envelope performance, smart vapor retarders and breathable membrane technologies met greater demand.

Germany

- Advanced vapor barriers gained popularity for use in high-performance energy-efficient renovation projects.

- The passive house construction criteria promoted the successful implementation of high performing moisture control membrane systems across the country.

- The increasing use of smart vapor retarders enhanced building envelope efficiency and long-term durability.

France

- Nationwide, green building regulations led to the adoption of vapor barriers for low-energy buildings.

- Increased interest in IAQ led to the installation of improved moisture-management building materials.

- Increased renovation programs led to greater use of breathable and adaptive vapor membrane solutions.

Latin America held 7% market share in 2025, as residential construction expanded, awareness of moisture issues leading to structural damage increased, and the number of commercial construction projects rose. In areas with high humidity levels, demand for moisture control systems was especially high, as moisture control is crucial to maintaining building integrity and comfort for occupants.

Brazil

- With the tropical climates, the need for vapor barriers to keep moisture from entering and mold from forming grew.

- Adoption of advanced building envelope protection systems was increased by growing commercial construction.

- Increased awareness of building durability led to investments in moisture control membrane technologies.

Chile

- As the industrial and commercial building industry continued to grow, the need for effective vapor barrier solutions grew as well.

- Advanced systems using insulation supporting membranes were adopted because of the increased awareness of energy-efficient buildings.

- Moisture protection construction materials were in demand due to infrastructure modernization projects.

The Middle East & Africa held 6% market share in 2025, due to rising investments in commercial infrastructure, massive urban development, and the use of modern building technologies, which supported the growth of this market. The demand for vapor barriers was encouraged because they were needed to guard against moisture penetration of insulation and to improve energy efficiency in extreme weather.

Saudi Arabia

- Advanced vapor barriers for high-performance building envelopes were required to meet the growing demand from mega building projects.

- The promotion of energy efficiency in buildings led to the widespread use of moisture-control membranes in commercial buildings across the country.

- Increased capacity of cold-storage and logistics facilities increased the use of industrial vapor barrier systems.

South Africa

- The demand for moisture-resistant building materials rose dramatically with the increase in the construction of houses and office buildings.

- Improved knowledge of mold prevention contributed to the adoption of the new vapor barrier membrane technologies.

- With the infrastructure development projects, there were incentives for using energy-efficient building envelope protection systems.

Recent Developments

- In June 2026, Siegwerk introduced CIRKIT OXYBAR, an innovative white printing ink that is equipped with oxygen barrier properties. The solution was able to integrate the functions of printing and barrier in one layer, and lowered the complexity of packaging, material consumption, and processing steps, which would facilitate more sustainable packaging designs.

(Source: packagingeurope.com) - In April 2026, Lecta launched a new EraCup paper cup at Interpack together with its range of paper-based barrier solutions. The range encompassed rigid and flexible solutions for packaging and labelling of food and beverages, aiming to improve product protection, processability, technical performance, and packaging circularity. (Source: packaginginsights.com)

Vapor Barrier Market Top Companies List

- Glenroy Inc.

- Celplast Metallized Product Ltd.

- Polifilm Group

- ProAmpac Holdings

- Optimum Plastics, Inc.

- 3M Company

- Amcor Limited

- SAES Getters S.p.A.

- Kalliomuovi Oy

- GLT Products

- UFP Industries, Inc.

- W.R. Meadows, Inc.

- BMI Icopal

- Carlisle Companies Inc.

Segments Covered in the Report

By Material

- Glass

- Metal Sheet

- Aluminum Sheet

- Steel Sheet

- Stainless Steel Sheet

- Polymers

- Polyethylene

- LDPE

- HDPE

- Cross-linked PE

- Polypropylene

- Woven PP

- Non-woven PP

- Polyvinyl Chloride

- Flexible PVC

- Rigid PVC

- Others

- Polyamide

- EVOH

- PET

- Polyethylene

By Application

- Insulation

- Thermal Insulation

- Acoustic Insulation

- Waterproofing

- Roofing Waterproofing

- Foundation Waterproofing

- Wall Waterproofing

- Corrosion Resistance

- Industrial Equipment

- Pipelines

- Storage Tanks

- Others

- Moisture Control

- Air Barrier Systems

By Installation

- Membranes

- Sheet Membranes

- Self-Adhesive Membranes

- Fluid-Applied Membranes

- Coatings

- Acrylic Coatings

- Polyurethane Coatings

- Epoxy Coatings

- Cementitious Waterproofing

- Flexible Cementitious

- Rigid Cementitious

- Stacking and Filling

- Landfill Barriers

- Structural Filling Applications

By End-Use

- Construction

- Residential Buildings

- Commercial Buildings

- Industrial Buildings

- Infrastructure

- Packaging

- Food Packaging

- Pharmaceutical Packaging

- Industrial Packaging

- Automotive

- Interior Components

- Underbody Protection

- EV Battery Protection

- Others

- Agriculture

- Marine

- Aerospace

By Region

- North America

- U.S.

- Canada

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Sweden

- Denmark

- Norway

- Asia Pacific

- China

- Japan

- India

- South Korea

- Thailand

- Latin America

- Brazil

- Mexico

- Argentina

- Middle East and Africa (MEA)

- South Africa

- UAE

- Saudi Arabia

- Kuwait

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

FAQ's

Select User License to Buy

Figures (5)