Content

What is the Semiconductor Fabrication Materials Market Size and Share?

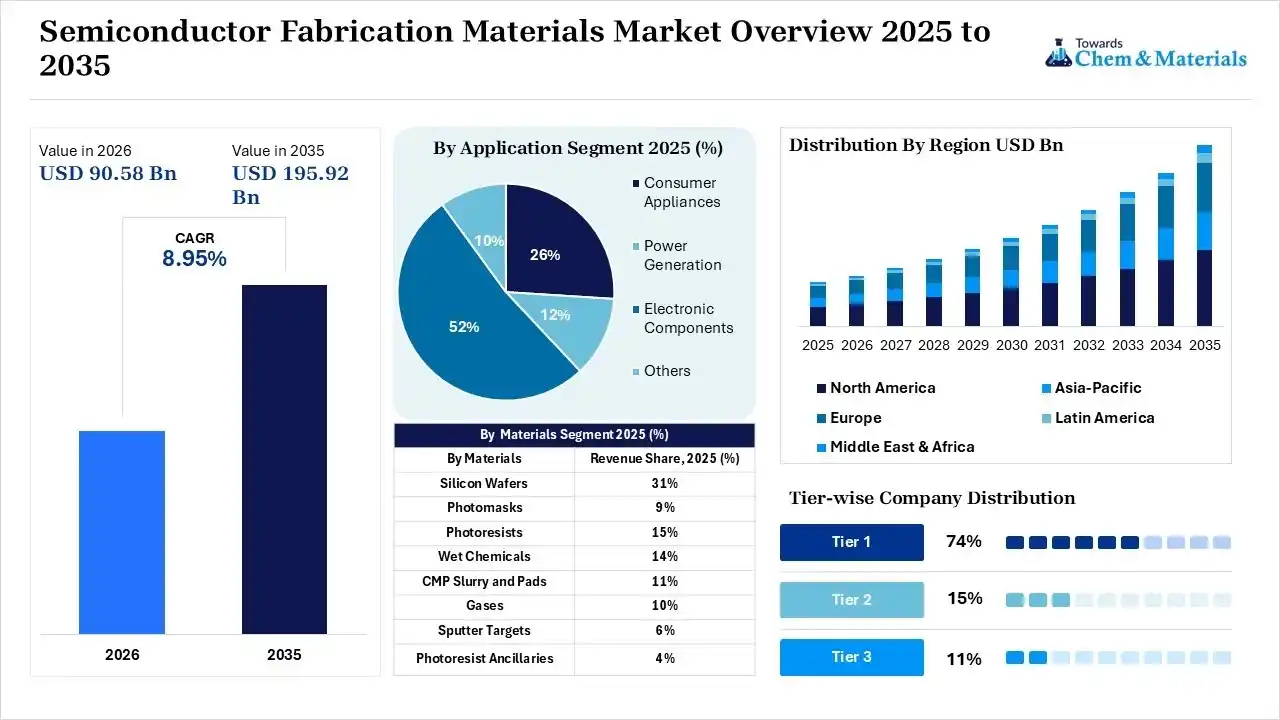

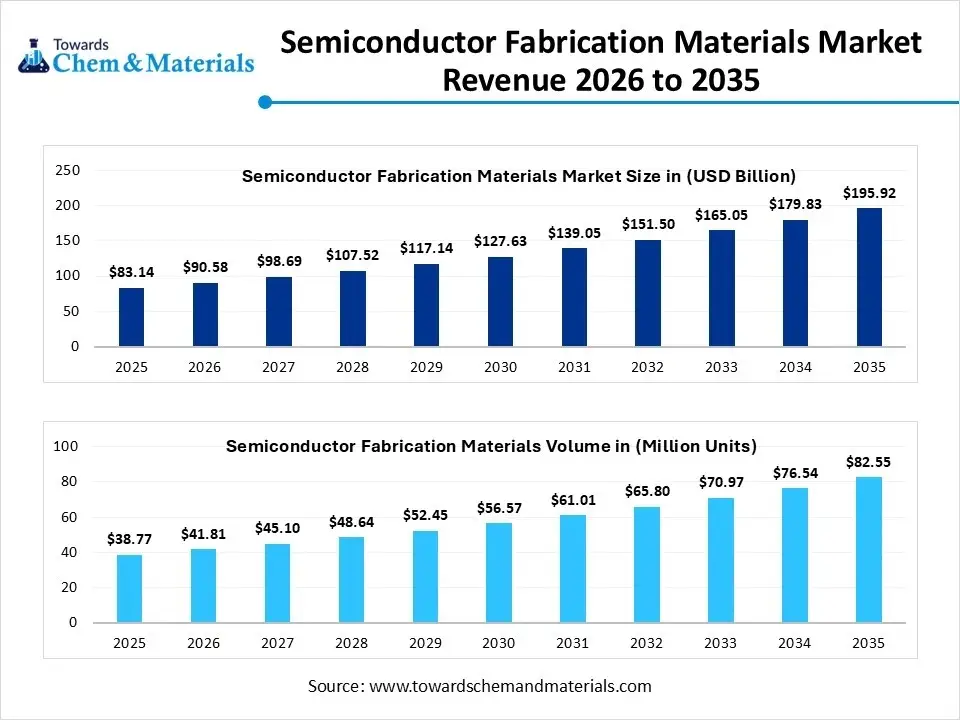

The global semiconductor fabrication materials market size was valued at USD 83.14 billion in 2025, is estimated to reach USD 90.58 billion in 2026, and is projected to reach USD 195.92 billion by 2035, exhibiting a compound annual growth rate (CAGR) of 8.95% over the forecast period from 2026 to 2035.Asia Pacific dominated the semiconductor fabrication materials market with the largest revenue share of xx% in 2025 and is expected to grow at the fastest CAGR of 8.04% during the forecast period. In terms of volume, the semiconductor fabrication materials market is projected to grow from xx million units in 2025 to xx million units by 2035. growing at a CAGR of xx% from 2026 to 2035.The technologies of artificial intelligence, IoT, and 5G are in the process of undergoing fast adoption, the demand for consumer electronics is growing, and the production of electric vehicles is on the rise, as well as rising investments in renewable energy systems, driving market growth. Demand is growing even faster in the global market for semiconductor process materials, purity materials for semiconductor manufacturing, specialty chemicals for miniaturization and advanced packaging technology, and advanced substrates.

Market Highlights

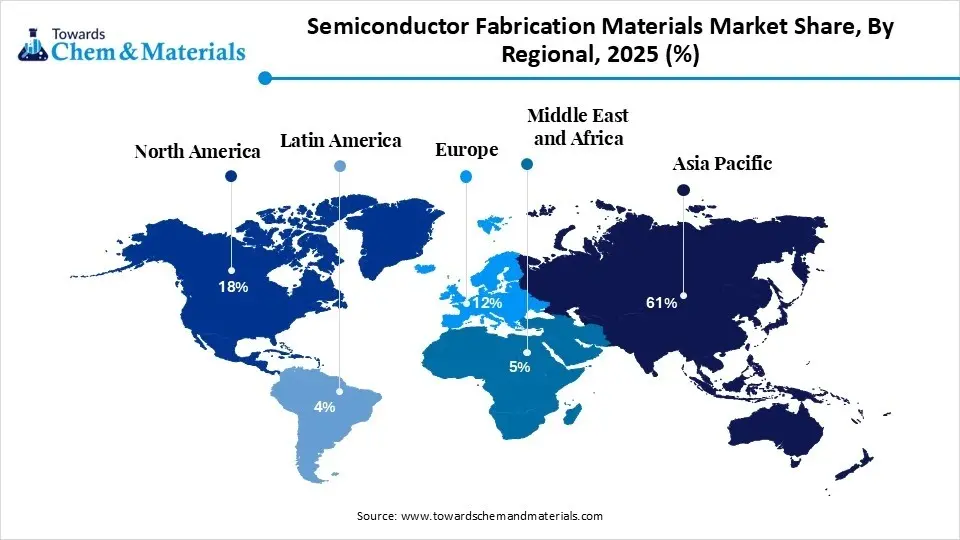

- By region, Asia Pacific dominated the market share 61% in 2025, due to well established and rapidly growing electronics manufacturing sector.

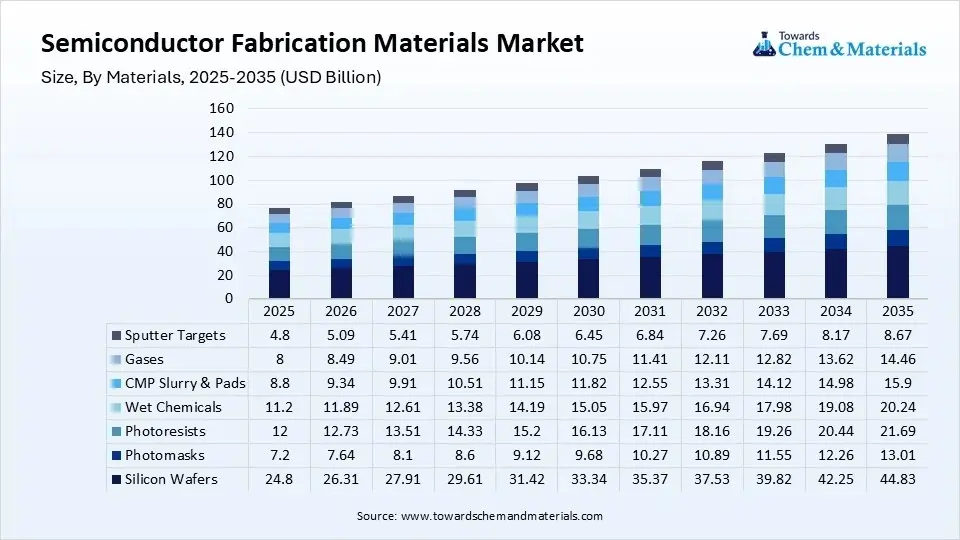

- By materials, silicon wafers segment held the dominating share of semiconductor fabrication materials market share 31% in 2025, due to their properties like crystal structure, electrical characteristics, and surface quality.

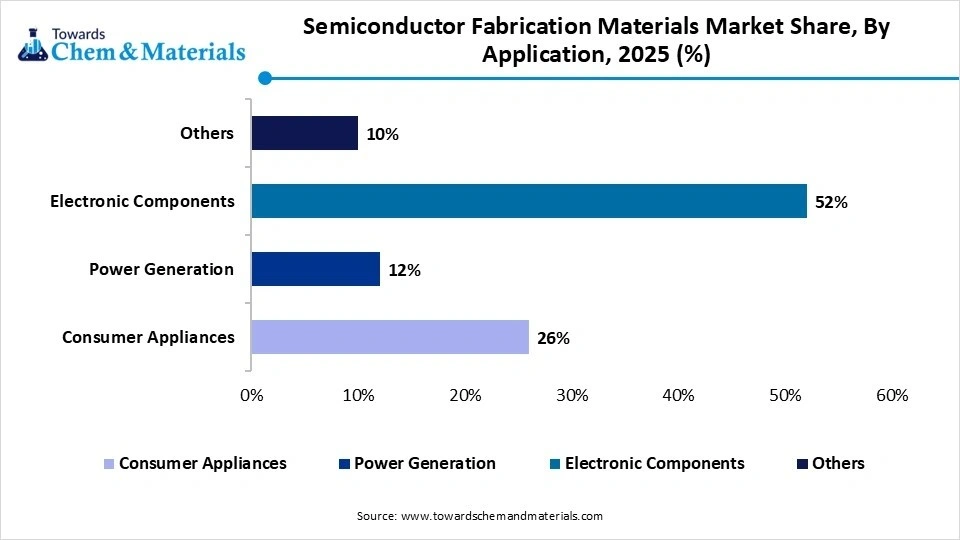

- By application, consumer application segment held the dominating share of semiconductor fabrication materials market share 26% in 2025, attributed to increasing demand of consumer electronics including smart phones and wearable.

The market for semiconductor fabrication materials is growing rapidly, driven by manufacturers' efforts to meet the demand for next-generation chip technologies, advanced packaging solutions, and high-performance computing applications. As the industry moves down to smaller process nodes and increasingly complex semiconductor architectures, demand for ultrapure chemicals, photoresists, specialty gases, and advanced wafer materials is growing. Investments in domestic fabrication and bolstering regional material ecosystems are being encouraged by initiatives like the U.S. CHIPS Act and the India Semiconductor Mission.

Moreover, the development of EUV resist materials, silicon carbide, gallium nitride, advanced slurries, and etchant materials is changing the semiconductor manufacturing landscape and enabling the advancement of device performance, efficiency, and scalability in today's advanced logic and memory devices.

- For instance, VFabTech opened its American doors in April 2026 to enable semiconductor companies to grow production capacity and solve the industry's bottlenecks due to the demand from AI and advanced manufacturing. It was introducing full-scale engineering solutions for fab development, process integration, planning for infrastructure, and training of the workforce, with the expansion of advanced semiconductor manufacturing ecosystems.(Source: cleanroomtechnology.com)

Rising Demand For Electronics Across Various Sectors Demands Semiconductors Fabrication Materials

Semiconductor fabrication materials are the substances which are used to create the tiny and complex component that make up electronic devices. Raw materials like silicon, germanium, and various metals are used in semiconductor fabrication materials. These materials plays major role in building integrated circuits, transistors, and other electronic components.

Silicon, GaN, and SiC are mainly used in power semiconductors for various applications including the switch mode power supplies and electric motor drives. It is also used in solar cells and other renewable energy technologies. Various technological advancements including use of 2D materials like Grapheme is overcoming the limitations of traditional silicon. Additionally, chiplet technology used to develop small, interconnected silicon component is rapidly growing, further accelerate the semiconductor fabrication materials market expansion.

Semiconductor Fabrication Materials Market Trends

-

Rising demand for advanced electronics : The growing popularity of smart phones, tablets, wearable’s, and other consumer goods increases demand of semiconductors fabrication materials. The automation of manufacturing, energy, and other industries requires high-performance chips to power complex systems and processes which contribute to semiconductor fabrication materials market growth.

-

Technological innovation in semiconductor manufacturing: Increased need for advanced packaging technologies like System-in-Package (SiP) drives the market. The industries are exploring new material like silicon carbide and gallium nitride due to their high performance ability. Various technological innovations like High-Purity Silicon Wafers are used in most semiconductors chips, advanced Photoresists used in lithography processes, further drives the market.

-

Technology like AI impact the semiconductor fabrication material: Ai tools can automate many steps such as layout generation, verification, and simulation. AI driven visual inspection system can detect the defect in wafers and chips with higher accuracy and speed, increases its demand. AI reduces downtime, improves efficiency, and minimizes waste, further driving the market.

-

Government Support: Government is increasingly offering the financial incentives in semiconductor manufacturing. This financial incentive attracts companies to establish or expand their facilities. Additionally government is increasingly investing in the research and development to develop innovation in semiconductor material and processes. This funding supports universities and private companies to work o various technologies, further drives the semiconductor fabrication materials market.

Market Report Scope

| Report Attributes | Details |

| Market Size in 2026 | USD 90.58 Billion/ 41.81 Million Units |

| Expected Size By 2035 | USD 195.92 Billion/ 82.55 Million Units |

| Growth Rate from 2025 to 2035 | CAGR 8.95% |

| Base Year of Estimation | 2025 |

| Forecast Period | 2025-2035 |

| Dominant Region | Asia Pacific |

| Segment Covered | By Material, By Application, By End User, By Region |

| Key Companies Profiled | BASF SE, Kanto Chemical Co., Inc., Air Liquide SA, Taiyo Nippon Sanso , Alent Plc, Praxair, Inc., Dow Chemical Company, Air Products and Chemicals Inc., JSR Corporation, LindeAG |

Market Opportunity

Increasing Use of Advanced Electronics

Increasing demand of smart phones, tablets and wearable’s increases need for advanced semiconductor fabrication materials. The transition to electric vehicles (EVs), autonomous driving, and connected car technologies is increasing the demand for semiconductors in the areas like battery management, navigation, and safety features. Various advancements in semiconductor materials and fabrication techniques enabled to create smaller and complex electronic components which increases processing speeds, energy efficiency, and high performance

Technological Advancement

Technological advancements in the artificial intelligence, the Internet of Things, 5G, and sustainable manufacturing are showing significant market opportunities for semiconductor fabrication materials. Rapid growth of AI and IoT applications needs specialized semiconductors for data processing and communication; demand the material like silicon and gallium nitride. Innovation in sustainable manufacturing reduces environmental impact of semiconductor production, which may drive the semiconductor fabrication materials market in future.

Market Challenges

Raw Material Shortages

Raw material shortage is a significant challenge to the semiconductors fabrication material market which impacts the supply chain and production. Shortage of raw materials can significantly slows down the production lines which delays the fulfilling order. Shortage of raw material reduces the production volume which limits the market of semiconductor fabrication materials.

High Cost of Raw Materials

High cost of raw materials increases the manufacturing cost which leads to the higher prices for the end product, limits the market. Challenges associated with the securing and transporting limited supplies can also contribute to the increased expenses. Additionally, the higher material cost can erode the profit margin which may limits the future market growth of semiconductor fabrication materials.

Supply Chain Analysis of the Semiconductor Fabrication Materials Market

Feedstock Procurement:

- This stage includes procurement of high-purity raw materials, including quartz, metallurgical-grade silicon, rare metals, and specialty minerals used in the manufacture of semiconductors. Manufacturers are increasingly prioritising the security of the supply chain, the purity of materials, and sustainable sourcing practices, in order to guarantee the availability of important fabrication inputs.

- Shin-Etsu Chemical: Leading provider of high-purity silicon wafers and semiconductor materials, providing high-quality material products to advanced chip manufacturers around the world.

- Other Key Player: SUMCO, Siltronic AG

Chemical synthesis and processing:

- Complex purification and synthesis processes are used to produce ultra-high purity chemicals, precursor gases, and semiconductor-grade materials from raw feedstocks. This is an essential process to obtain the high purity that is needed in the more advanced semiconductor manufacturing processes and to reduce production defects.

- Air Liquide: A leading supplier of electronic specialty gases, advanced materials for wafer fabrication, and high-purity process chemicals for the world's largest semiconductor manufacturers.

- Other Key Players: Linde plc, Merck KGaA

Compound Formulation and Blending:

- Photoresists, developers, etchants, CMP slurries, and other fabrication chemicals are made from purified materials mixed with specialized additives and processing agents. Accurate formulation provides superior process performance, uniformity, and compatibility with ever more demanding semiconductor manufacturing requirements.

- DuPont: A supplier of advanced photoresists, CMP materials, and semiconductor processing chemicals for next-generation logic and memory device manufacturing.

- Other Key Players: JSR Corporation, Tokyo Ohka Kogyo

Segmental Insights

Materials Insights

The silicon wafers segment held the dominating share of semiconductor fabrication materials market share 31% in 2025. Silicon wafers possess superior performance and characteristics as compared to the other semiconductor material contribute to growth of this segment. Silicon is readily available and also inexpensive to extract and purify. Silicon is ease to process which allows efficient and cost effective manufacturing of waffles. It is also modified though doping and other technique to create various types of semiconductor devices which make tem adoptable to wide range of applications. Cost effectiveness, versatility and superior performance further drive the market growth of this segment.")

The photomasks segment observed to grow at the fastest rate in the semiconductor fabrication materials market during the forecast period. Increasing demand of advanced semiconductor devices ad advancement in lithography processes contribute to the market growth of this segment. Various ongoing development s in lithography techniques including the use of extreme ultraviolet (EUV) lithography are important for improved photomasks technologies. Rising demand of LCD, smart phones, TV increases the need for photomasks used in their production, further drive the market.

Application Insights

The consumer application segment held the dominating share of semiconductor fabrication materials market share 26% in 2025, Increasing demand for electronic devices, advancement in technology and rise of emerging application like Artificial Intelligence (AI), Internet of Things, and 5G drives the growth of this segment. Increasing adoption of smart phones, smart home devices and other connected devices majorly demands semiconductor fabrication materials .Rising disposable income, allows consumer to purchase advanced electronic devices which is smaller and more efficient, further propel market.") The power generation segment observed to grow at the fastest rate in the semiconductor fabrication materials market during the forecast period. Increasing demand for power semiconductors in various applications including the electric vehicles, renewable energy systems and industrial automation drives the market of this segment. Rapidly expanding electric vehicle demands the semiconductors for function like battery management, motor control and charging. Additionally in the renewable energy sources like solar and wind power the power semiconductor plays very important role in the converting and managing the energy generated and distributed, further drives the market.

The power generation segment observed to grow at the fastest rate in the semiconductor fabrication materials market during the forecast period. Increasing demand for power semiconductors in various applications including the electric vehicles, renewable energy systems and industrial automation drives the market of this segment. Rapidly expanding electric vehicle demands the semiconductors for function like battery management, motor control and charging. Additionally in the renewable energy sources like solar and wind power the power semiconductor plays very important role in the converting and managing the energy generated and distributed, further drives the market.

End Use Insights

The telecommunication segment held the dominating share of semiconductor fabrication materials market in 2025. Rise of wireless communication technologies, increasing data usage, and adoption of 5G technology contributes to the telecommunication segment growth in the semiconductor fabrication materials. Growing data center require more semiconductors for processing and networking, boost the demand for the materials use in their fabrication. The increasing popularity of wireless technologies like Wi-Fi and mobile networks increase the need for semiconductors in communication devices, further drive the market.

The electrical and electronic materials segment expects significant growth in the market during the forecast period. Increasing demand for advanced electronics, rapid advancement in technology and growing importance of semiconductors in emerging application like 5G, IoT, and AI contribute to market growth of this segment. As technology advances, electronics devices require sophisticated chips, leads to increased use of semiconductor materials. Additionally, increasing adoption of digitally integrated circuits across these industries demands semiconductor fabrication material further drives the market.

Regional Insights

How did the Asia Pacific dominate the Semiconductor Fabrication Materials Market in 2025?

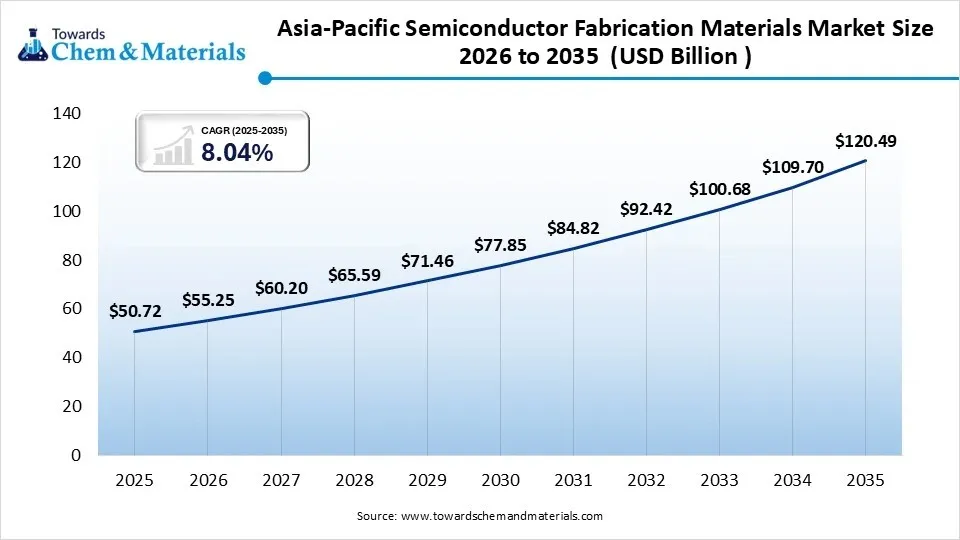

The Asia Pacific semiconductor fabrication materials market size was estimated at USD 50.72 billion in 2025 and is projected to reach USD 120.49 billion by 2035, growing at a CAGR of 8.04% from 2026 to 2035.Asia Pacific dominated the market with 61% share in 2025, as it had a large semiconductor fabrication capacity, a well-established semiconductor manufacturing ecosystem, and electronics production leadership. Demand for the region's fabrication materials remained strong due to a mix of major foundries, advanced packaging plants, and material suppliers, as well as government support for semiconductor self-sufficiency.

") China

China

- High-purity chemicals, wafers, and specialty materials were all needed with significant semiconductor manufacturing investments.

- Local production support policies for chips stimulated the development of local fabrication material ecosystems.

- Consumption of semiconductor process materials was strong due to the expansion of the electronics and artificial intelligence industries.

India

- Government semiconductor programs spurred investments in fabrication plants and material supply chains.

- The increased demand for advanced semiconductor fabrication material technologies throughout the country is a result of the growth of the electronics manufacturing sector.

- Foreign investment helped to build a domestic semiconductor industry and a corresponding material base.

North America held 18% market share in 2025 and is expected to grow at the fastest CAGR of 9.8% during the forecast period. The area enjoys broad investments in Local Semiconductor Manufacturing, advanced research, and high demand from the Artificial Intelligence, defense, automotive, and high-performance computing industries.

United States

- Domestic semiconductor manufacturing grew faster, and the demand for domestic fabrication materials expanded throughout the country, due to government incentives.

- The growth of the AI and high-performance computing industries boosted demand for AI chip materials.

- Advanced fabrication plants were built, leading to growth in material supply chains in the local area.

Canada

- The high quality of the research work stimulated innovation in new semiconductor materials and manufacturing technologies throughout the country.

- The surge in the semiconductor supply chain for North America contributed to the expansion of demand for specialty fabrication materials.

- The government's efforts in technology development provided substantially more support for expanding opportunities in the semiconductor ecosystem.

Europe held 12% market share in 2025. Strategic investments toward semiconductor sovereignty, the advancement of automotive electronics, and industrial automation technologies were among the factors that fueled Europe's semiconductor fabrication materials market. The research and innovation emphasis in the region and the increasing manufacturing prowess of semiconductors drove increased interest in high-quality fabrication materials and specialty chemicals.

Germany

- The advanced fabrication materials and specialty chemicals used in the automotive semiconductor market were driven by strong demand for semiconductors.

- Governments in the region made investments in their regional manufacturing capabilities nationwide while promoting semiconductor independence.

- High-performance semiconductor production materials gained strong demand with the extensive industrial automation activities.

France

- As more and more money was invested in the study of semiconductors, more sophisticated material technologies and uses were developed.

- Demand for specialized semiconductor fabrication materials was promoted by strong aerospace and electronics industries across the country.

- Innovation programmes backed by the government led to the growth of the semiconductor manufacturing and supply chain.

Latin America held 4% market share in 2025, owing to the growing electronics manufacturing, digital transformation initiatives, and growing investments in technology infrastructure for the region. As industrialisation efforts increased and regionalisation of semiconductor supply chains became more robust, there were opportunities for suppliers of fabrication materials in the region.

Brazil

- As electronics manufacturing grew, so did the requirement for semiconductor fabrication materials and processing chemicals.

- Advanced manufacturing and semiconductor-related industrial development was supported by increased technology investments.

- The growth of digital infrastructure projects led to the use of semiconductor technologies in various sectors.

Chile

- Advanced semiconductor materials and components demand continued to grow across the country, and technology modernization initiatives helped drive the demand.

- Increased industrial digitalization opened up opportunities for semiconductor-related manufacturing and the growth of the supply chain.

- Investment in innovation projects boosted the prospects of the growth of the advanced technology ecosystem.

The Middle East & Africa held 5% market share in 2025, as a result of rising investments in advanced manufacturing, technology diversification, and the development of digital infrastructure. Governments in the region are making strong efforts to facilitate and promote innovation-based industries, thereby fostering opportunities for semiconductor manufacturing and material supply chains.

") Saudi Arabia

Saudi Arabia

- The economic diversification programs facilitated the investments in advanced technology and semiconductor-related manufacturing capacities.

- The expansion of digital transformation projects led to the rise in demand for semiconductor-based systems in various sectors.

- The government's support for innovation enabled the development of advanced industrial and technology ecosystems across the country.

South Africa

- Growth in the technology sector brought opportunities for involvement in the semiconductor supply chain and material demand.

- Driven by increased investments in advanced manufacturing, the adoption of industrial technologies using semiconductors was promoted throughout the country.

- Development of high-value technology/electronics industries was facilitated through research and innovation efforts.

Recent Developments

- In June 2026, Applied Materials announced the Centris Spectral SiN ALD and Producer Selectra Mo Etch systems for semiconductor manufacturers to process materials for deeper and deeper narrow 3D structures needed for advanced logic and memory chips. The systems addressed the needs for higher processing accuracy for high aspect ratio structures and advanced manufacturing needs for nodes.

(Source: analyticsindiamag.com) - In March 2026, Hong Kong Science and Technology Parks Corporation and Oriental Materials Hong Kong Limited launched the HKSTP x Oriental Materials Semiconductor Equipment Manufacturing Base Project at Yuen Long InnoPark. The project created the first production base for researching, developing, and manufacturing the front-end equipment for semiconductor and integrated circuit production in Hong Kong.

(Source: hkstp.org) - In January 2026, Aegis Aerospace signed a contract with United Semiconductors to build the first advanced materials manufacturing facility to be used in space. The cooperation was based on advancing space-based manufacturing of semiconductors and on-going space-enabled semiconductor manufacturing in low Earth orbit for advanced semiconductor applications.

(Source: prnewswire.com)

Top Companies List in Semiconductor Fabrication Materials Market

- BASF SE

- Kanto Chemical Co., Inc.

- Air Liquide SA

- Taiyo Nippon Sanso

- Alent Plc

- Praxair, Inc.

- Dow Chemical Company

- Air Products and Chemicals Inc.

- JSR Corporation

- LindeAG

Segments Covered in the Report

By Materials

- Silicon Wafers

- 200 mm Wafers

- 300 mm Wafers

- SOI Wafers

- Photomasks

- Binary Masks

- Phase Shift Masks

- EUV Masks

- Photoresists

- ArF Immersion

- KrF

- EUV Photoresists

- i-Line

- Wet Chemicals

- Cleaning Chemicals

- Etchants

- Solvents

- CMP Slurry and Pads

- CMP Slurries

- Oxide Slurry

- Metal Slurry

- CMP Pads

- CMP Slurries

- Gases

- Electronic Specialty Gases

- Bulk Gases

- Deposition Gases

- Sputter Targets

- Aluminum Targets

- Copper Targets

- Titanium Targets

- Precious Metal Targets

- Photoresist Ancillaries

- Anti-Reflective Coatings

- Developers

- Edge Bead Removers

By Application

- Consumer Appliances

- Smart Home Devices

- Household Electronics

- Power Generation

- Solar Electronics

- Grid Control Systems

- Electronic Components

- IC Manufacturing

- Sensors

- Memory Devices

- Others

- Industrial Electronics

- Aerospace Electronics

By End Use

- Telecommunication

- 5G Infrastructure

- Data Centers

- Energy

- Renewable Energy Electronics

- Power Management Systems

- Electrical and Electronics

- Consumer Electronics

- Industrial Electronics

- Medical and Healthcare

- Diagnostic Devices

- Medical Imaging Systems

- Automotive

- EV Electronics

- ADAS Systems

- Others

- Defense

- Aerospace

By Region

- North America

- U.S.

- Canada

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Sweden

- Denmark

- Norway

- Asia Pacific

- China

- Japan

- India

- South Korea

- Thailand

- Latin America

- Brazil

- Mexico

- Argentina

- Middle East and Africa (MEA)

- South Africa

- UAE

- Saudi Arabia

- Kuwait

FAQ's

Select User License to Buy

Figures (7)