Content

What is the Current Photoinitiator Market Size and Share?

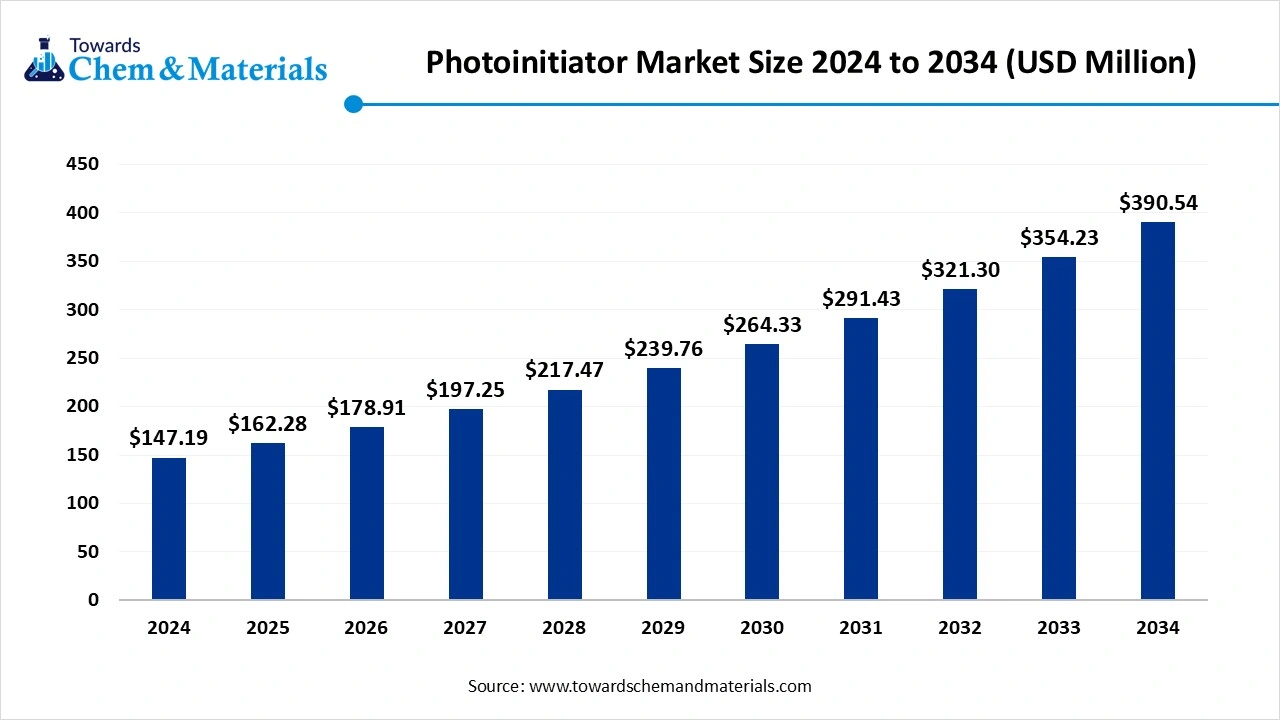

The global photoinitiator market size was USD 162.28 million in 2025 and is predicted to increase from USD 178.91 million in 2026 and is expected to be worth around USD 430.58 million by 2035, growing at a CAGR of 10.25% from 2026 to 2035. North America dominated the photoinitiator market with the largest revenue share of 36.11% in 2025. The increasing demand for UV curable materials from various industries like coatings, inks, and adhesives, and the shift towards the use of eco-friendly alternatives due to the shift towards sustainability and the use of low VOC-formulations, drives the growth of the market.")

Market Highlights

- The North America dominated the global photoinitiator market with the largest volume share of 36.11% in 2025.

- By type, the free radical segment dominated the market and accounted for the largest volume share of 75.45% in 2025.

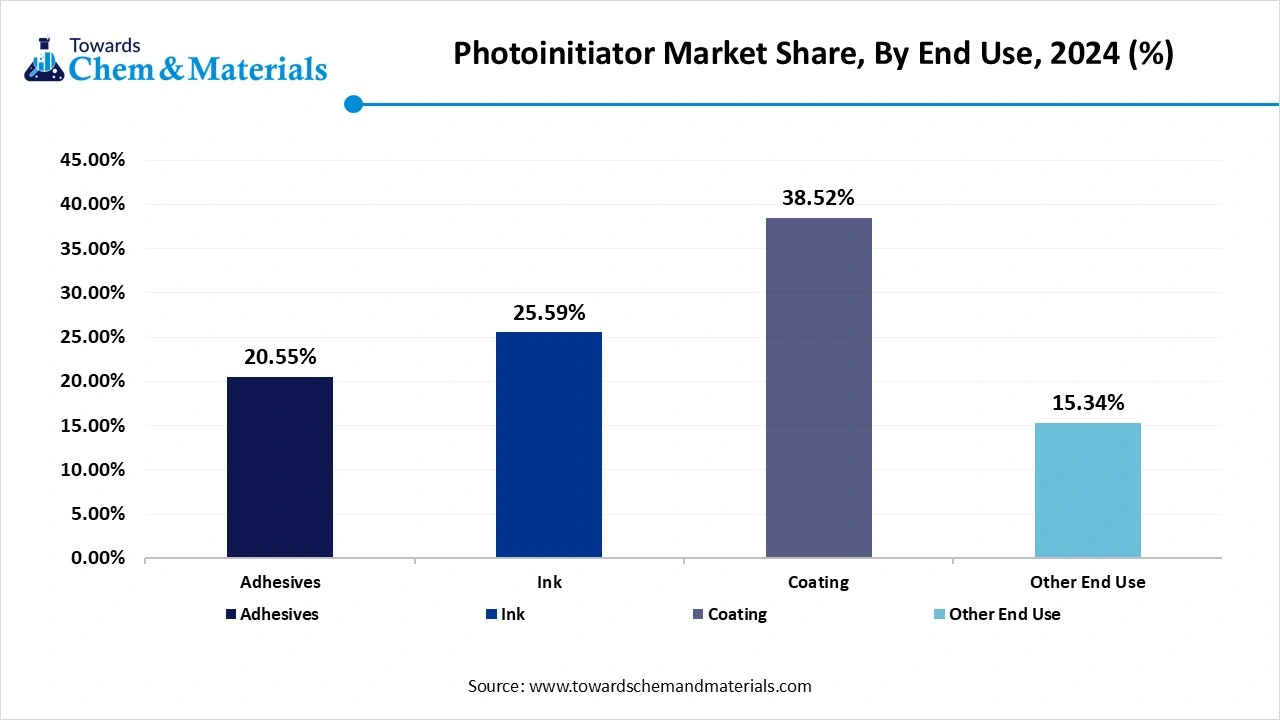

- By end use, the coatings segment led the market with the largest revenue volume share of 39.32% in 2025.

Market Overview

Rising Demand for Durable Materials: Photoinitiator Market to Expand

Photoinitiators are molecules that initiate chemical reactions when exposed to light. They're designed to absorb light at specific wavelengths, usually in the ultraviolet (UV) or visible spectrum. When they absorb light, the photoinitiator molecule transitions into an excited state. This excited state can then undergo various processes, such as breaking apart, abstracting a hydrogen atom, or transferring an electron, to generate reactive species like radicals, cations, or anions.

These reactive species then trigger further chemical reactions, such as polymerization, crosslinking, or degradation, depending on the system. In short, the photoinitiator absorbs photons (light energy) and becomes excited, leading to the formation of reactive species that trigger further reactions, often polymerization, the process of forming large molecules from smaller units. Photoinitiators play a crucial role in various technologies, including UV-curable inks, coatings, adhesives, and dental materials.

What Are the Key Growth Drivers Responsible for The Growth of The Photoinitiator Market?

The growth of the photoinitiator market is driven by the growing demand for UV curing materials like coatings, inks, and adhesives from various industries like electronics, automotives, and packaging industries drives the growth of the market. The growing use of eco-friendly and energy-efficient materials, which offer more sustainable alternatives to traditional solvent-based systems, has a lower environmental impact by reducing VOC emissions and energy consumption, fueling the growth of the market.

The driven demand for increasing production efficiency increases the demand for materials having faster curing times, like UV-cured coatings, inks, and adhesives boosts the growth of the market. Other drivers responsible for the growth of the market are technological advancements, growing industries, stringent environmental regulations, superior performance, and a wide range of applications high performance solutions in various industries, which boost the growth and expansion of the market.

Recent Trends in the Photoinitiator Market

- Increasing Demand from UV/EB Curing Technologies: Photoinitiators continue to gain traction due to rapid adoption of ultraviolet (UV) and electron beam (EB) curing systems across coatings, inks, adhesives, and 3D printing resins. These curing technologies offer near-instant polymerization, low energy requirements, and minimal volatile organic compound (VOC) emissions, driving formulators to select tailored photoinitiators that enable fast, deep, and uniform cure profiles for specific substrates.

- Shift Toward Low-Migration and Regulatory-Compliant Chemistries: Growing regulatory scrutiny, especially in packaging, toys, and medical devices, is pushing demand for low-migration, non-toxic photoinitiators that comply with food contact and biocompatibility standards. Manufacturers are increasingly using chemistries with reduced residual monomer levels and improved purity to meet EU, U.S. FDA, and Asian safety requirements, particularly in flexible packaging and pharmaceutical applications.

- Customization for Additive Manufacturing (3D Printing): Photoinitiators are becoming more specialized to support additive manufacturing resins with tailored cure rates, color stability, and mechanical performance. Demand is highest in dental and industrial 3D printing, where precise control of cure depth and layer adhesion affects part accuracy, surface finish, and functional performance. This trend is accelerating development of photoinitiators with sensitivity tuned to specific wavelengths (e.g., 405 nm, 385 nm) used in DLP and SLA systems.

- Development of Sustainable and Bio-Derived Photoinitiators: With sustainability mandates rising in packaging, automotive, and construction polymers, formulators and chemical manufacturers are investing in bio-based and greener photoinitiator chemistries that deliver comparable performance while reducing environmental footprint. This includes exploration of renewable feedstocks and photoinitiators with improved biodegradability and lower toxicity profiles.

- Enhanced Performance for High-Throughput Industrial Processes: End users are demanding photoinitiators capable of withstanding high-speed web coating, multi-layer print processes, and thick film applications without oxygen inhibition or incomplete cure. Newly developed photoinitiators demonstrate improved initiation efficiency, reduced odor, and compatibility with high-solid and low-migration resin systems to better support automotive coatings, industrial parts finishing, and floor coatings.

Report Scope

| Report Attributes | Details |

| Market Size in 2026 | USD 178.91 Million |

| Expected Size by 2035 | USD 430.58 Million |

| Growth Rate from 2026 to 2035 | CAGR 10.25% |

| Base Year of Estimation | 2025 |

| Forecast Period | 2026 - 2035 |

| Dominant Region | North America |

| Segment Covered | By Type, By End Use, By region |

| Key Companies Profiled | IGM Resins, Lambson Ltd (part of Aditya Birla Group), Arkema S.A., BASF SE, Tronly New Electronic Materials Co., Ltd., Tianjin Jiuri New Materials Co., Ltd., ADEKA Corporation, Evonik Industries AG, Rahul Photoinitiators Pvt. Ltd., Eutec Chemical Co., Ltd. |

Market Dynamics

Driver: Expanding Adoption of UV/EB Curing Technologies Across End-Use Industries

The global photoinitiator market is witnessing strong growth, primarily driven by the accelerating adoption of ultraviolet (UV) and electron beam (EB) curing technologies across coatings, inks, adhesives, and additive manufacturing applications. UV/EB curing offers rapid polymerization, lower energy consumption, and minimal VOC emissions compared to conventional thermal curing processes, increasing demand for efficient and application-specific photoinitiator chemistries.

Rising production of packaging materials, printed electronics, automotive coatings, and industrial finishes in major manufacturing hubs such as China, Germany, the U.S., and Japan has significantly increased consumption of photoinitiators. Their ability to enable fast curing, high surface quality, and strong adhesion makes photoinitiators essential in high-throughput industrial printing, protective coatings, and functional surface treatments. As industries continue to prioritize productivity, energy efficiency, and environmental compliance, photoinitiators are becoming a core enabler of modern radiation-curing technologies.

Restraint: Regulatory Pressure and Toxicity Concerns Associated With Certain Photoinitiator Chemistries

Despite strong demand, the photoinitiator market faces restraints related to regulatory scrutiny and health concerns associated with specific photoinitiator compounds. Certain conventional photoinitiators have been linked to migration risks, skin sensitization, and potential toxicity, particularly in food packaging, medical devices, and consumer-facing applications. Regulatory frameworks in regions such as the European Union and North America impose strict limits on residual photoinitiator content, migration behavior, and chemical safety compliance.

These regulatory constraints increase formulation complexity and compliance costs for manufacturers, especially in low-margin applications. In addition, restrictions on specific aromatic photoinitiators have forced reformulation efforts, extended qualification timelines, and additional testing requirements. Such factors can slow product adoption, particularly among small and mid-sized formulators with limited R&D resources.

Opportunity: Growth of Additive Manufacturing and Low-Migration, Application-Specific Photoinitiators

The photoinitiator market presents significant growth opportunities driven by rapid expansion of additive manufacturing and rising demand for low-migration, high-performance photoinitiator systems. Applications such as dental 3D printing, industrial prototyping, electronics, and medical devices require photoinitiators with precise wavelength sensitivity, controlled cure depth, and excellent mechanical performance. This is accelerating the development of customized photoinitiators optimized for specific resin systems and light sources.

In parallel, increasing demand for safer, low-migration photoinitiators in food packaging, pharmaceutical labeling, and medical applications is creating opportunities for advanced formulations with improved purity and regulatory compliance. The shift toward bio-based and sustainable chemistries further expands the innovation space, allowing manufacturers to differentiate through performance, safety, and environmental compatibility. These trends position photoinitiators as critical functional additives supporting next-generation manufacturing and materials technologies.

Value Chain Analysis

- Raw Material Procurement: This involves sourcing basic precursor chemicals, which are the building blocks for photoinitiators, and significantly impact production costs.

- Key Players: BASF SE and Evonik Industries AG.

- Research & Development (R&D): This is crucial for developing new, high-performance, and eco-friendly photoinitiators to meet evolving regulatory and performance demands.

- Key Players: IGM Resins, Arkema S.A., Tianjin Jiuri New Materials Co., Ltd., and RAHN AG.

- Manufacturing and Production: This involves the large-scale, and often complex, production of various photoinitiator types in manufacturing facilities.

- Key Players: IGM Resins, Zhejiang Yangfan Materials, Tianjin Jiuri New Materials Co., Ltd., and Changzhou Tronly New Electronic Materials Co., Ltd.

- Sales, Marketing, and Distribution: This involves a global supply chain network and strategic partnerships with distributors to reach various regional markets efficiently.

- Key Players: IGM Resins and Arkema.

Segmental Insights

Type Insights

Which Type Segment Dominated the Photoinitiator Market In 2024?

The free radical segment dominated the photo initiator market in 2024. The are molecules that, when exposed to light, like UV or visible it, break down into free radicals, which then perform polymerization reactions. These free radicals are reactive species that play a vital and crucial role in the curing process for various applications like coatings, 3D orienting, and adhesives, which increases the demand for the market due to increasing demand from the industries. They are in high demand due to their advantages, like speed, energy efficiency, reduced VOC, and precise control, which supports the growth of the market. A variety of applications UV curing, coating inks, adhesives, dental materials, and 3D printing, microelectronics in drug microencapsulation, and other medical applications, drive the growth of the market and support the expansion of the market.

The cationic segment is expected to experience significant growth in the photoinitiator market during the forecast period. The cationic photoinitiators are used in various applications like coatings, adhesives, and printing inks as they are used in UV-curing processes to harden and solidify materials fuels the growth of the market. They are used in applications such as food packaging, dental materials, medical devices, and electronic materials where there is a need, and with advantages like strong adhesion, high gloss, chemical resistance, oxygen inhibition resistance, oxygen inhibition resistance and low shrinkage post-cure reaction, versatility, and LED compatibility offering energy efficiency and environmental benefits boosts the growth of the market and also helps in expansion of the market.

End Use Insights

How Did the Coating Segment Dominate the Photoinitiator Market In 2024?

The coatings segment dominated the photoinitiator market in 2024. The growth of the market is driven by the growing applications of photoinitiator for a wide range of coatings, like general coatings, wood, metal, and plastics coatings, for specialty coatings like gel nails, which drives the growth of the market. They are crucial for UV curable coatings, which activate rapid and efficient hardening of the coating by the UV curing process. Their wide range of properties and advantages, like high mechanical properties, compatibility with chemicals, and solvent-free chemicals, which increases their demand for coating of various materials for protection and enhancing appearance, boosts the growth of the market, supporting the expansion.

")

The inks segment expects significant growth in the photoinitiator market during the forecast period. The growth of the market is driven by their properties of fast drying, UV curing, low energy consumption, compatibility with chemicals, and offering of resistance to abrasion ink formulations, which fuels the growth of the market. The growth of the market is also driven by the vital applications like labels, flexible packaging, food packaging, shrink sleeves, and many more. These applications further support the growth of the market and also support and boost its expansion of the market.

Regional Insights

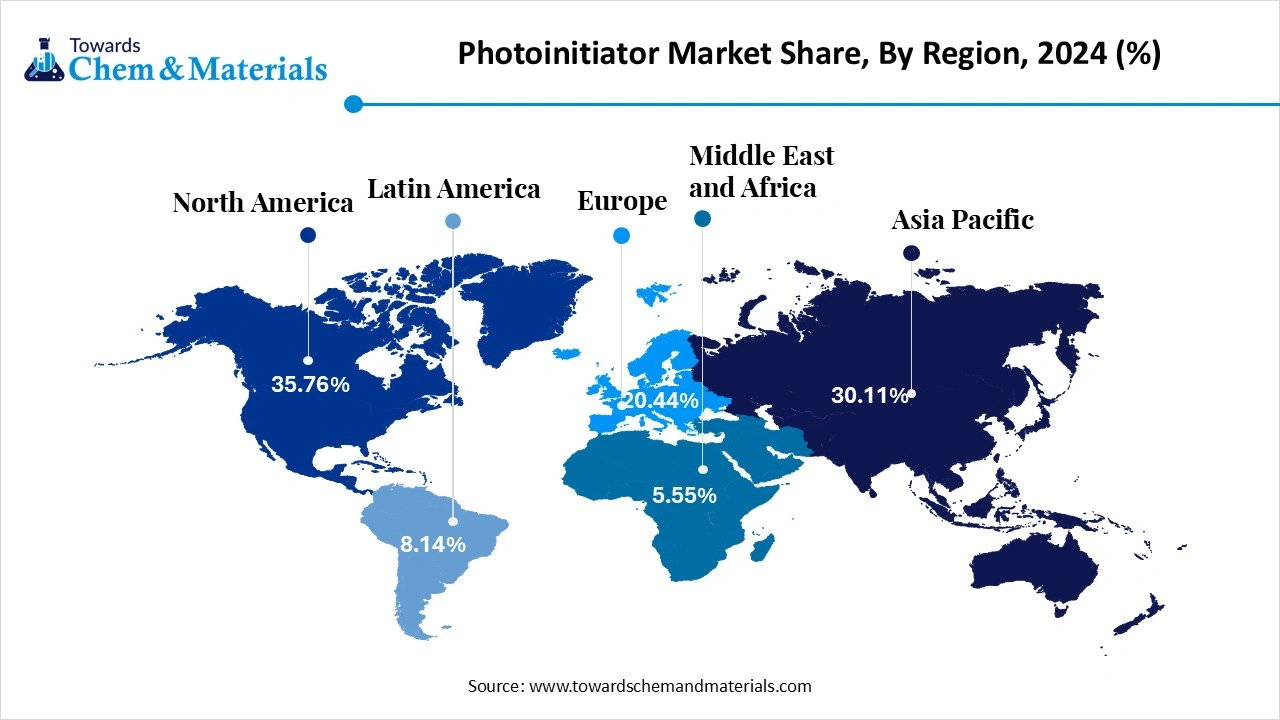

The North America photoinitiator market size was valued at USD 58.03 million in 2025 and is expected to be worth around USD 154.11 million by 2035, exhibiting at a compound annual growth rate (CAGR) of 10.26% over the forecast period from 2026 to 2035. North America dominated the photoinitiator market in 2024. The growth of the market is driven by the strong industrial sector in the region, like packaging, printing, and coating, which fuels the growth of the market in the region. The region is also advancing in technology, like the development of high-performance inks and coating materials, with innovation in 3D printing also boosting the growth of the market. The other industries, such as automotive, electronics, and healthcare, also demand coatings, inks, and adhesives, and demand for advanced materials for protection and appearance due to the growing automotive sector in the region, which fuels the growth of the market and also supports the growth.

")

The US String Regulatory Supports and Domestic Production Drive the Growth of the Market

The US has experienced a significant growth in the photoinitiator market, the growth is driven by the string regulatory supports and government regulations for promotion of low-VOC and eco-friendly materials for increasing adoption of UV-curing solutions due to rising environmental concerns and shift towards sustainability and environmentally friendly use of materials drives the growth of the market in the country. The growth is also driven by the strong and key manufacturers in the US, also ensures a reliable supply chain and easy access for photoinitiator to the industries, which boosts the growth of the American market and also supports the expansion of the market.

- The world shipped out 569 Photoinitiator shipments from September 2023 to October 2024 (TTM). These exports made by 114 world exporters to 121 buyers, with the growth rate of 3% over the previous one year.(Source: Volza.com)

- Globally China, Vietnam, and the United States are the top three exporters of Photoinitiator. China is the global leader in Photoinitiator exports with 882 shipments, followed closely by Vietnam with 207 shipments, and the United States in third place with 134 shipments.(Source: Volza.com)

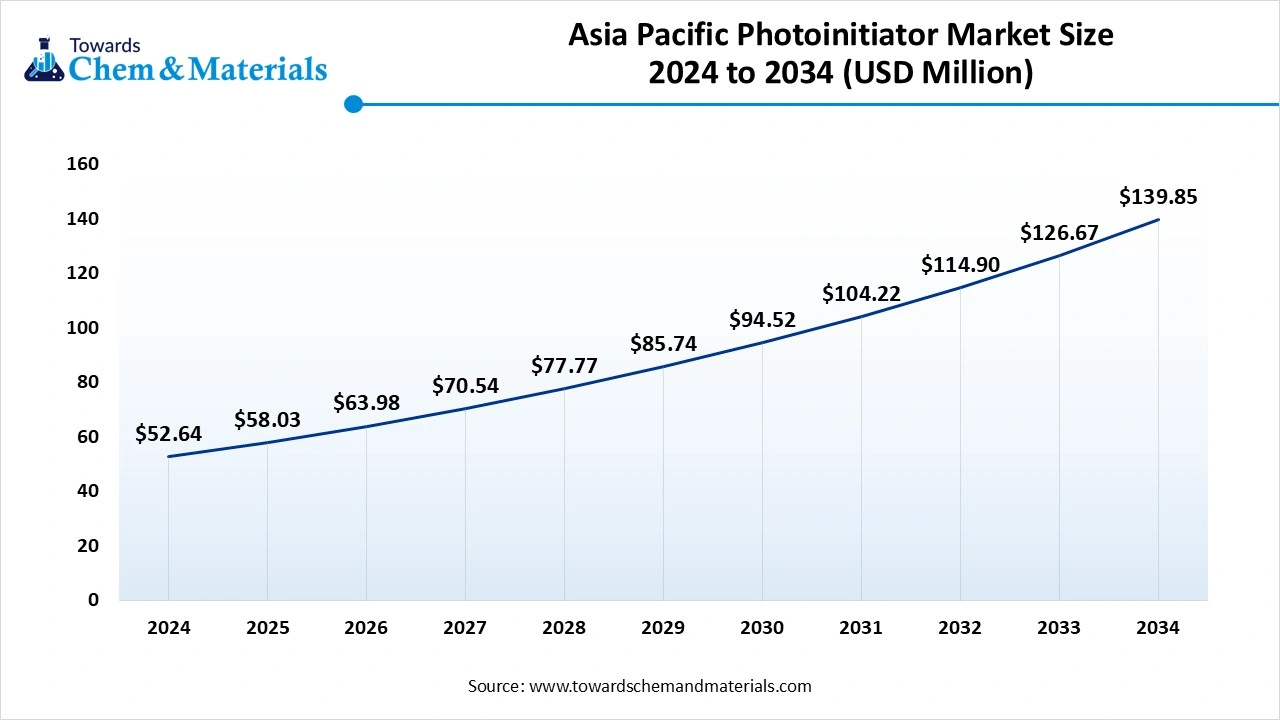

Asia Pacific Growth is Driven by the Rapid Industrial Manufacturing Sector

Asia Pacific is expected to experience significant growth in the photoinitiator market in the forecast period. The region is seen and experiencing steady growth in the market, the growth is driven by the rapid industrial expansion and expansion of manufacturing units, which increases the demand for products from industries like packaging, electronics, and automotive, fueling the growth of the market. The growth is driven by the rapid industrialization and urbanization, which creates strong demand for photoinitiator along with cost-effective manufacturing processes and solutions.

- Additionally, key players like ADEKA Corporation, Changzhou Tronly New Electronic Materials Co., Ltd., IGM Resins, Lambson, and Rahn AG. Plays a crucial role, which drives the growth and expansion of the market in the region.

")

China is a Leading Exporter Of Photoinitiator, Driving the Growth of the Market

China has seen steady growth, driven by the robust industrial sector, which increases the demand for UV curing process materials, and the driving adoption of advanced manufacturing technologies fuels the growth of the market in the country. Major players like Zhejiang Yangfan New Materials Co., Ltd, Tianjin Jiuri New Materials, and Changzhou Tronly New Electronic Materials Co., Ltd, in the country play a significant role in the growth and expansion of the market in the country.

- China shipped out 898 Photoinitiator shipments. These exports made by 111 world exporters to 132 buyers.(Source: Volza.com)

How will Europe Experience Notable Growth in the Photoinitiator Market?

Europe is expected to experience notable growth in the near future, primarily due to its stringent environmental regulations, strong focus on sustainability and innovation, and well-established manufacturing base. Countries such as Germany, France, and the UK have robust manufacturing sectors that are early adopters of advanced UV curing technologies. The presence of major global chemical companies, including BASF, Arkema, Evonik, and IGM Resins, along with research institutions in Europe, fosters continuous technological advancements.

Germany Photoinitiator Market Trends

Germany leads the European photoinitiator market, characterized by advanced manufacturing practices and a strong emphasis on environmental compliance. Prominent global chemical companies like BASF SE and Evonik Industries AG play a significant role in shaping the global market, leveraging their research and development capabilities to create new formulations. Germany's strong automotive, printing, and packaging industries are major consumers of photoinitiators used in UV and LED curing applications.

How will Latin America Surge in the Photoinitiator Market?

Latin America is a rapidly growing region in the global market, primarily due to the expansion of industrial activities, a push for environmentally friendly products, and the increasing adoption of advanced technologies such as UV and LED curing systems. Growing populations, increasing urbanization, and an expanding middle class in countries like Brazil and Mexico are driving the demand for consumer goods and high-quality packaging, creating a favorable environment for market expansion.

Brazil Photoinitiator Market Trends

Brazil is a key player in the global market, serving as an important hub for regional distribution. While it depends on imports for some advanced raw materials, local manufacturers are increasingly adopting innovative technologies and collaborating with international firms. There is a rising preference for sustainable products in Brazil, alongside the development of regulatory frameworks that emphasize environmental safety, promoting innovation in eco-friendly formulations.

Emergence of the Middle East and Africa in the Photoinitiator Market

The Middle East and Africa are crucial contributors to the global market, driven by rapid industrialization, economic diversification initiatives, and growing demand for eco-friendly UV-cured solutions across various end-use industries such as packaging, automotive, and electronics. Countries in the MEA, particularly the GCC nations like Saudi Arabia and the UAE, are heavily investing in industrial development and infrastructure projects, enhancing the demand for coatings, inks, and adhesives that utilize photoinitiators.

Saudi Arabia Photoinitiator Market Trends

Saudi Arabia is emerging as a growing market within the region, with robust demand for advanced photoinitiators compatible with UV and LED curing technologies. These solutions offer faster curing cycles and lower energy consumption, aligning with global sustainability goals. The market is further advancing through strategic collaborations between local entities and international technology providers, facilitating knowledge transfer and the adoption of cutting-edge chemical technologies.

Recent Developments

- In October 2025, researchers from the City University of Hong Kong demonstrated alternative uses of Pt(IV) prodrugs as photoinitiators, enabling facile fabrication of multifunctional macromolecular materials such as antibacterial and conductive hydrogels for motion sensing. Efficient protein crosslinking further suggests that Pt(IV) coordination complexes have the potential to be employed as photocrosslinkers for gelatin hydrogelation and as reagents for protein photoreactive labeling.(Source: www.nature.com)

- In March 2025, researchers from the Institute of Applied Synthetic Chemistry conducted a study to synthesize several MAPO photoinitiators, which primarily exhibit modifications on the phosphorous atom. Based on the absorption behavior and reactivities in photo-DSC measurements, the scientists investigated derivatives with alkyl and phenyl substituents on the phosphorus in more detail.(Source: onlinelibrary.wiley.com)

Top Companies List

- IGM Resins

- Lambson Ltd (part of Aditya Birla Group)

- Arkema S.A.

- BASF SE

- Tronly New Electronic Materials Co., Ltd.

- Tianjin Jiuri New Materials Co., Ltd.

- ADEKA Corporation

- Evonik Industries AG

- Rahul Photoinitiators Pvt. Ltd.

- Eutec Chemical Co., Ltd.

Segments Covered

By Type

- Free Radical

- Cationic

By End Use

- Adhesives

- Ink

- Coating

- Other End Use

By Region

- North America

- U.S.

- Canada

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Sweden

- Denmark

- Norway

- Asia Pacific

- China

- Japan

- India

- South Korea

- Thailand

- Latin America

- Brazil

- Mexico

- Argentina

- Middle East and Africa (MEA)

- South Africa

- UAE

- Saudi Arabia

- Kuwait

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

FAQ's

Select User License to Buy

Figures (5)