Content

What is the Offshore Oil and Gas Market Size and Share?

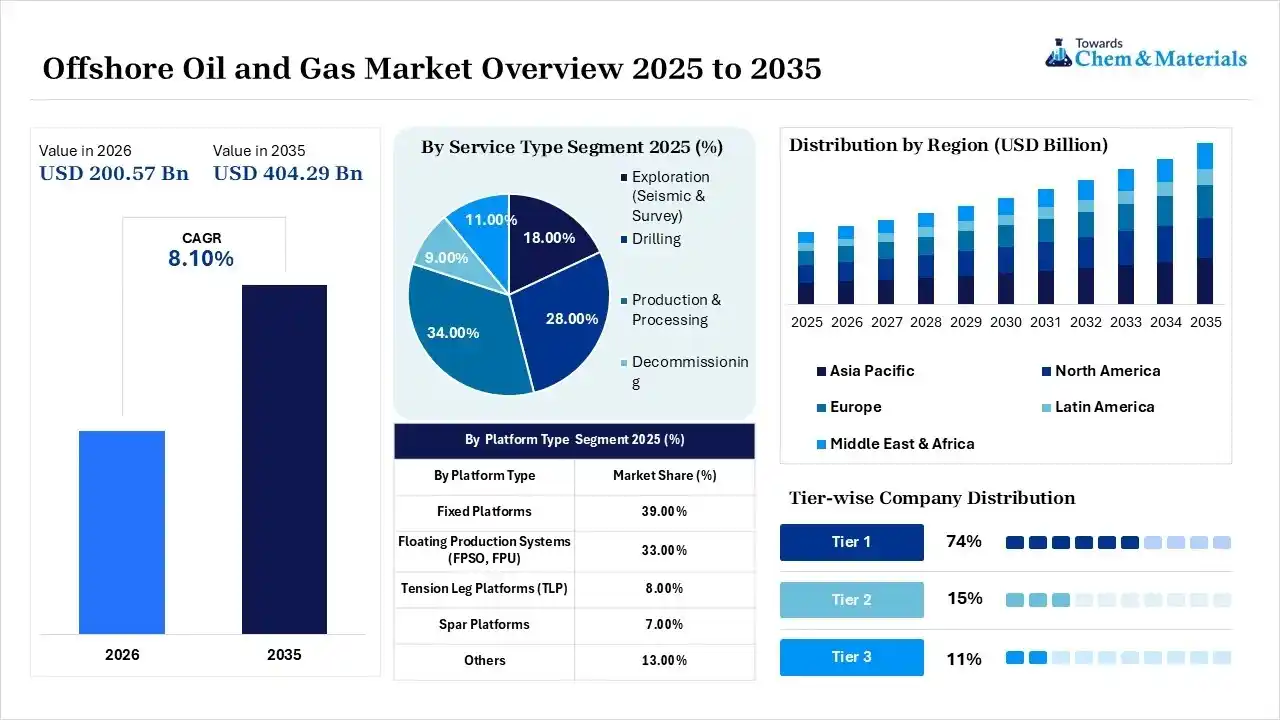

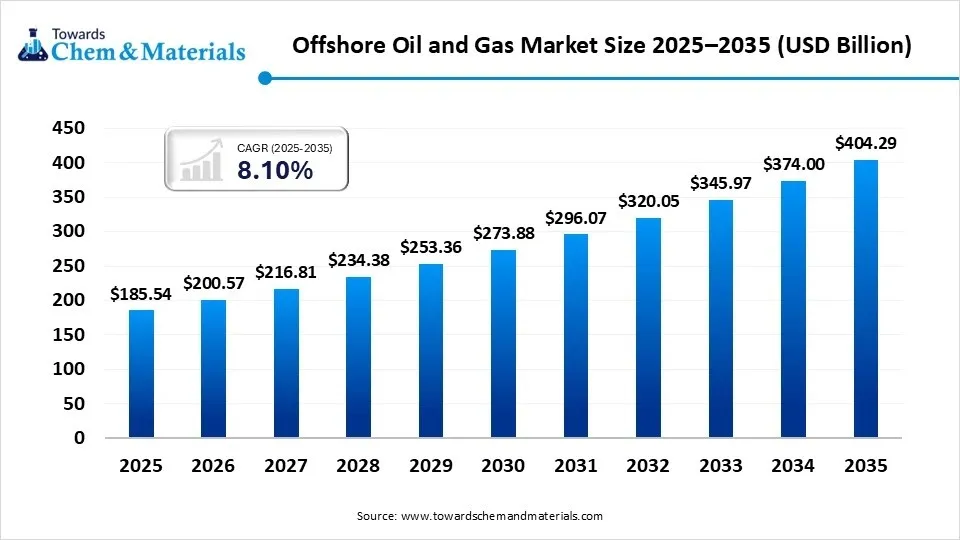

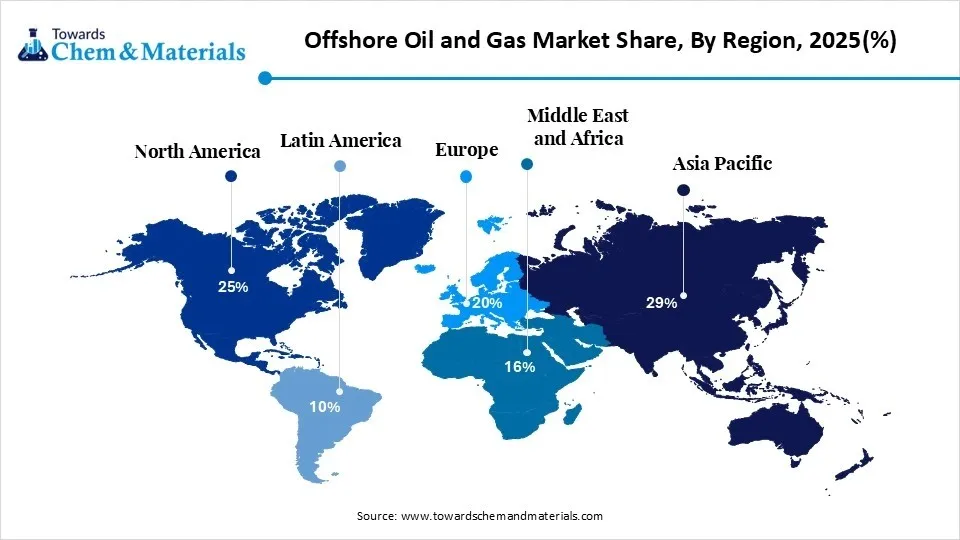

The global offshore oil and gas market size was valued at USD 185.5 billion in 2025, is estimated to reach USD 200.6 billion in 2026, and is projected to reach USD 404.3 billion by 2035, exhibiting a compound annual growth rate (CAGR) of 8.10% over the forecast period from 2026 to 2035. Asia Pacific dominated the offshore oil and gas market with the largest revenue share of 29.00% in 2025 and is expected to grow at the fastest CAGR of 8.28% during the forecast period.

The sector is experiencing exceptional growth as it is seeing increased deepwater and ultra-deepwater exploration in basins across regions. The shift towards subsea tiebacks and the use of hybrid battery systems on drilling rigs has also expanded deepwater activities. The strategic activities and planning for domestic expansion, like India, have initiated a comprehensive, two-year, 161,000-line-kilometer offshore seismic survey covering major sedimentary basins in the Bay of Bengal to enhance domestic energy production, which helps the market and is expected to grow in the coming years.

Market Highlights

- By region, Asia Pacific dominated the market with a share of 29.00% in 2025 and is expected to experience the fastest growth with a CAGR of 8.28% in the forecast period.

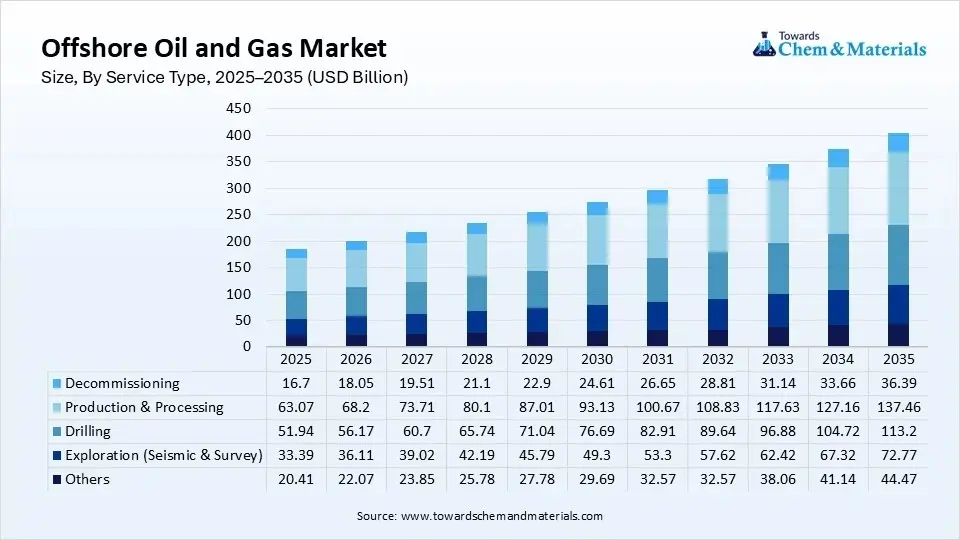

- By service type, the production and processing segment dominated the market with a 34% share in 2025 and is expected to grow at a CAGR of 4.70% over the forecast period.

- By service type, the decommissioning segment held 9% market share in 2025 and is expected to have the fastest growth with a CAGR of 7.40% in the forecast period.

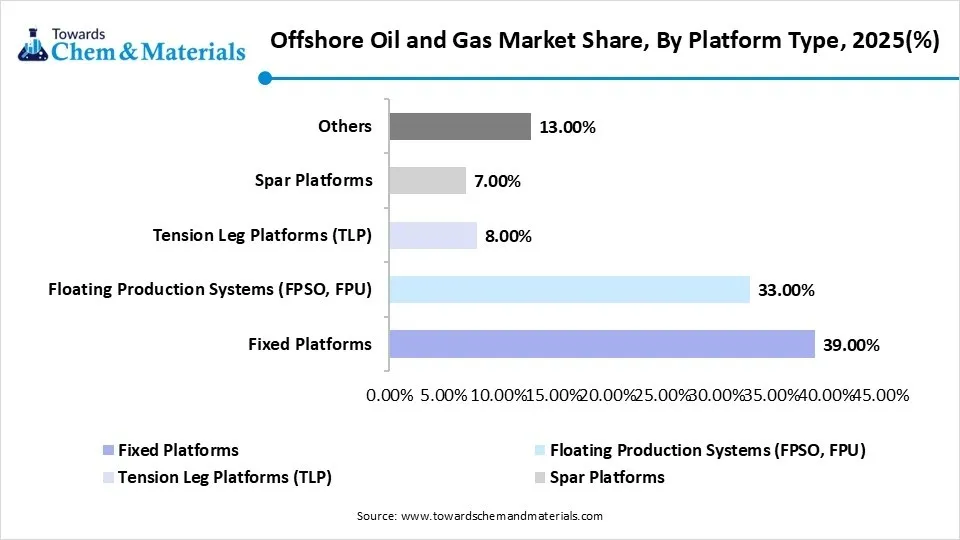

- By platform type, the fixed platforms segment dominated the market with a 39% share in 2025 and is expected to grow at a CAGR of 3.80% over the forecast period.

- By platform type, the floating production systems (FPSO, FPU) segment held 33% market share in 2025 and is expected to have the fastest growth with a CAGR of 6.60% in the forecast period.

- By water depth, the shallow water segment dominated the market with a 47% share in 2025 and is expected to grow at a CAGR of 3.50% over the forecast period.

- By water depth, the ultra-deepwater segment held 19% market share in 2025 and is expected to have the fastest growth with a CAGR of 6.80% in the forecast period.

- By hydrocarbon type, the crude oil segment dominated the market with a 68% share in 2025 and is expected to grow at a CAGR of 4.30% over the forecast period.

- By hydrocarbon type, the natural gas segment held 26% market share in 2025 and is expected to have the fastest growth with a CAGR of 5.60% in the forecast period.

")

Offshore Oil and Gas Market: Global Energy Supply and Security

Offshore oil and gas refer to the drilling, exploration, and extraction of petroleum and natural gas from beneath the ocean floor. The ocean holds immense reserves of hydrocarbons, which are a major component in the global energy supply. Offshore oil and gas are a vital energy source, supplying over a quarter of the world's crude oil and gas. It also serves as a major economic driver and advanced marine engineering technologies. The offshore oil and gas market is a critical pillar of global energy, supplying roughly 30% of the world's oil and natural gas. The technological advancement and innovation in the extraction and production to withstand the harsh, deepwater marine environment, and the development of cutting-edge technologies, which also include automated drilling systems and advanced seismic imaging technologies.

These advances enhance the safety and efficiency of offshore operations and foster broader technological progress across various industries. Moreover, the offshore oil and gas sector has gradually incorporated renewable energy solutions, like offshore wind farms, to cut its carbon emissions and align with the global pursuit of sustainable energy. As technological advancements persist, offshore oil and gas will continue to play a vital role in the worldwide energy landscape.

The environmental and energy transition considerations, like emission reduction, as companies are increasingly investing in lowering carbon footprints by using offshore wind power and innovative power from shore solutions, and decommissioning activities are experiencing a surge, which includes well plugging, recycling of materials, and site clearance due to aging platforms.

For instance, India launched Operation Samudra Manthan, an extensive offshore hydrocarbon exploration drive led by the Directorate General of Hydrocarbons (DGH) to scan previously untapped seabed territories across the east coast.

- This initiative uses 2D/3D seismic surveys and stratigraphic drilling to open nearly 1 million square kilometers of previously restricted "no-go" areas.(Source: www.shankariasparliament.com)

Global Investment Flow for Offshore Oil and Gas Market 2026

The Global offshore oil and gas investment in 2026 is experiencing rapid growth through strategic capital allocation, cost-effective and cost-competitive, and low-emission reserves, with major players like Shell and Chevron and government investments in the region supporting the massive growth in the market.

- Norway's state net cash flow from the petroleum sector is estimated to reach 686 billion NOK (over $74.43 billion) in 2026. This represents a solid increase from 2025, when the state's net cash flow stood at approximately 664 billion NOK (about $72.04 billion).(Source: www.offshore-energy.biz)

- Global energy capital investment is projected to reach approximately $3.4 trillion in 2026, marking a 5% increase over 2025 outlays, according to the International Energy Agency (IEA). This upward trajectory reflects a heightened global focus on energy security, self-reliance, and infrastructure modernization following consecutive macroeconomic energy shocks.(Source: www.industrialinfo.com)

- Vedanta Oil & Gas (formerly Cairn Oil & Gas) has reaffirmed its strategic target to scale domestic production to 500,000 barrels of oil equivalent per day (boed). The campaign focuses heavily on accelerated exploration and advanced enhanced oil recovery (EOR) technologies to tap into India's vast, underexplored hydrocarbon resources.(Source: megaproject.com)

Driven by an escalating domestic energy demand that is projected to lead global oil demand growth through 2030, India's Exploration & Production (E&P) sector presents a massive $100 billion investment opportunity by 2030. According to government data from Invest India, the country possesses significant hydrocarbon resources across its sedimentary basins, holding an estimated 651.8 million metric tons of recoverable crude oil and 1,138.6 billion cubic meters of recoverable natural gas.(Source: www.investindia.gov.in)

Market Growth Trends

- The deepwater exploration and ultra-deepwater dominance account for more than half of the offshore operations, with major regions being the main factor, such as Brazil, Guyana, Namibia, and the Krishna-Godavari basin in India. The use of drill ships and high-specification floating rigs as untapped reservoirs and lucrative opportunities is a growing trend in the market.

- With infrastructure optimization and acceleration of the project timeline, the operators are increasingly adopting the subsea tiebacks and hub-and-spoke model, which also significantly reduces capital expenditure as the existing infrastructure to connect with satellite fluid is a growing trend.

- The growing adoption of AI, growing digitalization and automation, and heavy investment in intelligent drilling analytics, autonomous subsea robotics, and digital twins, which help in maximizing production efficiency, is a growing trend in the offshore oil and gas market.

Report Scope

| Report Attributes | Details |

| Market Size in 2026 | USD 200.6 Billion/ 33.0 Billion Barrels Of Oil Equivalent |

| Expected Size in 2035 | USD 404.3 Billion/ 45.4 Billion Barrels Of Oil Equivalent |

| Growth Rate | CAGR of 8.10% |

| Base Year of Estimation | 2025 |

| Forecast Period | 2025-2035 |

| Dominant Region | Asia Pacific |

| Segment Covered | By Service Type, By Platform Type, By Water Depth, By Hydrocarbon Type, By Region |

| Key Companies Profiled | Saudi Aramco – Saudi Arabia, ExxonMobil – United States, Chevron – United States, Shell – United Kingdom/Netherlands, TotalEnergies – France, BP – United Kingdom, Petrobras – Brazil, Equinor – Norway, CNOOC – China, Eni – Italy, ConocoPhillips – United States, PetroChina / CNPC – China, Rosneft – Russia, Lukoil – Russia, Woodside Energy – Australia, Petronas – Malaysia, QatarEnergy – Qatar, ADNOC – United Arab Emirates, Equatorial Guinea's National Oil Company (GEPetrol) – Africa, ONGC (Oil and Natural Gas Corporation) – India |

The Offshore Oil And Gas Market: Integration of AI and Optimization

The integration of AI in the offshore oil and gas market is reshaping the market by integrating machine learning, which helps in reducing unplanned downtime and optimizing complex extraction processes in harsh marine environments. The integration of artificial intelligence is driving several critical technological shifts in the offshore sector, like closed-loop autonomous drilling and real-time optimization, and major players are significantly investing in advancements. The high-fidelity digital twins and predictive maintaining as it helps in equipment monitoring, downtime reduction, and industry performance. Subsurface and geoscience intelligence, which accelerated exploration and faster interpretation. Autonomous inspections and safety through robotics and computer vision, and environmental management through AI models. Agentic AI and intelligent operations that support autonomous decision-making and unified operations. These are the integral factors that are the key technological shifts which supports growth of the market.

Supply Chain Analysis of Offshore Oil and Gas Market:

Chemical Extraction and Processing

- The offshore oil and gas are extracted through separation, undergo treatment, and undergo water treatment. The four major phases of extraction include surveying, drilling, production/processing, and transportation. locating subsea deposits, drilling thousands of meters beneath the seabed, and using massive floating or fixed platforms to process the raw mixture.

- Saudi Aramco operates one of the world's largest and most capital-intensive offshore oil and gas networks, anchored by mega-fields like Safaniya, the world's largest offshore oil field. Manifa, Zuluf, and Marjan. The company drives billions in offshore engineering, procurement, and construction (EPC) contracts to continually expand production capacity.

- Key players: Saudi Aramco, ExxonMobil, TotalEnergies, Chevron, and Shell

Quality Testing and Certification

- The offshore oil and gas require quality testing like non-destructive testing, pressure and load testing, and QA/QC frameworks, focusing on equipment integrity, environmental safety, and personnel competence. These tests require certification from ISO standards, API standards, and an offshore medical certificate.

- Equinor (formerly Statoil) is a Norwegian multinational energy giant and a global leader in offshore oil and gas operations, recognized for pioneering deep-water drilling and low-carbon extraction techniques on the Norwegian Continental Shelf (NCS) and internationally.

- Key players: ASTM International, ASME, ATEX, and UL Solutions

Distribution to Industrial Users

- Offshore oil and gas are extracted in the upstream sector, and it is then further distributed to the downstream and midstream industries. Like crude oil is distributed to petroleum refineries, natural gas is delivered to power generation companies.

- Petrobras is a global leader in deepwater and ultra-deepwater offshore oil and gas exploration, best known for pioneering the extraction of hydrocarbons from massive sub-salt (pre-salt) basins off Brazil’s coast. The company heavily relies on massive Floating Production, Storage, and Offloading (FPSO) vessels to process and store crude at sea.

- Key players: BP, Petrobras, Equinor, CNOOC, and Eni

Offshore Oil and Gas Market Regulatory Landscape

| Country / Region | Regulatory Body | Key Regulations | Focus Areas | Notable Notes |

| United States | Bureau of Safety and Environmental Enforcement; Bureau of Ocean Energy Management | Outer Continental Shelf Lands Act; Offshore Safety Regulations | Offshore drilling safety, environmental protection | The U.S. regulates offshore exploration and production through stringent safety, environmental, and operational standards. |

| European Union | European Commission; European Union Offshore Oil and Gas Authorities Group | Offshore Safety Directive (2013/30/EU) | Operational safety, spill prevention | Europe emphasizes high safety standards and environmental risk management for offshore oil and gas activities. |

| Norway | Norwegian Offshore Directorate; Norwegian Environment Agency | Petroleum Act; Working Environment Act | Sustainable offshore production, resource management | Norway is a global leader in safe and efficient offshore oil and gas operations with strict environmental oversight. |

| Brazil | National Agency of Petroleum, Natural Gas and Biofuels; Brazilian Institute of Environment and Renewable Natural Resources | Petroleum Law; Environmental Licensing Regulations | Deepwater exploration, environmental compliance | Brazil supports offshore oil development with a strong focus on deepwater and pre-salt reserves. |

| United Kingdom | North Sea Transition Authority; Health and Safety Executive | Offshore Installations (Safety Case) Regulations | Offshore safety, energy transition | The UK promotes safe offshore operations while supporting carbon reduction and offshore energy transition initiatives. |

| Saudi Arabia | Ministry of Energy; Saudi Energy Efficiency Center | National Petroleum Regulations; Environmental Protection Standards | Offshore production, energy security | Saudi Arabia continues to invest in offshore oil and gas infrastructure to strengthen production capacity and long-term energy security. |

What are the Key Product Types of the Offshore Oil and Gas Product?

The offshore oil and gas are generally categorized by its physical infrastructure, operational equipment, and marketable hydrocarbon products, which are extracted products that generally range from specialized deep-sea drilling platforms and subsea machinery to refined petrochemicals.

Offshore Platforms & Production Structures

The primary product type of offshore engineering is structured to design the product to withstand harsh marine environments and water depth, like fixed platforms, which are built on steel or concrete legs that are anchored directly to the sea bed, which are ideal for shallow waters. Other platforms are floating production and storage and offloading units, tension leg platforms, SPAR platforms, and drill ships and semisubmersibles. These platforms and production structures are massive and deep-sea floorings and mobile floating units, which are dynamic.

Subsea & Specialized Equipment

These are the physical technologies that make up offshore systems and allow the safe extraction and processing of hydrocarbons. The widely used systems are subsea production systems, riser systems, and blowout preventers, which play a major role. The subsea production systems are underwater equipment like wellheads, manifolds mounted on the seafloor, and valves that help transport resources directly to the surface facilities. The riser systems are flexible pipes that transport the raw fluids to floating production platforms through the seabed.

Hydrocarbon Output Products

These are the final products which are marketable from upstream offshore drilling and separation processes, the final products include crude oil, natural gas, and condensates, and petroleum derivatives, which are then distributed to the end-user industry. The crude oil is the raw petroleum which is extracted, separated from water and gas before being sent to the offshore refineries. Natural gases are extracted alongside oil, which is compressed and used to generate power, or which is piped ashore. The last products, which are petroleum derivatives, are the downstream products like gasoline, jet fuel, diesel, and petrochemical feedstocks extracted from crude oil once it reaches refineries.

Market Dynamics

What are the Key Growth Drivers in the Offshore Oil and Gas Market?

The growth of the market is driven by the growing deepwater and ultra-deepwater exploration in these regions. The global demand for natural gas and LNG, particularly in regions like Australia, Brazil, and East Africa, is driving the global transition towards cleaner-burning fossil fuels and reducing reliance and power generation needs, propelling the growth of the market. The other major and key growth drivers are the shift to deepwater and ultra-deepwater reserves, rising technological innovation and digitalization through integration of AI and Machine learning, and government support and regulatory policies, which further propel the growth and expansion of the market.

What are the Key Growth Challenges in the Offshore Oil and Gas Market?

The key growth challenges that hinder the growth are the high capital costs and price volatility, as deepwater and ultra-deepwater reservoir developments require high construction investment, massive upfront engineering and procurement. The crude oil price is highly volatile, which requires high capital budgeting and long-term planning, which is highly unpredictable, needing financial management with the need to sustain long-term energy supplies. The other major restraints include supply chain bottlenecks, environmental regulation and SG pressure, workforce constraints and skill gaps, and regulatory uncertainty, which limit the growth of the market.

What are the Key Growth Opportunities in the Offshore Oil and Gas Market?

The market is experiencing rapid growth in the market through the development of deepwater and ultra-deepwater reserves, which is a key growth opportunity for the market. The industry is also seeing major investment in digitalization, artificial intelligence, emission-reduction tech, and unmanned platforms. Technologies like AI-assisted drilling, digital twins, and subsea robotics are significantly cutting non-productive operational time and increasing safety. Operators are leveraging technological innovations to reduce costs and improve recovery rates in increasingly complex environments, which is a major growth opportunity for the market.

Segmental Insights

Service Type Insights

The production and processing segment dominated the market with a 34% share in 2025 and is expected to grow at a CAGR of 4.70% over the forecast period, as it is experiencing growth as operators are shifting to deepwater fluids in regions, also due to massive investments. Deep water exploration, extended operational lifespan, decarbonization, and electrification are major factors in the growth of the market.")

The decommissioning segment held 9% market share in 2025 and is expected to grow at the fastest rate, with a CAGR of 7.40% over the forecast period, due to aging infrastructure and stricter government regulation, and a maturing asset base which drives growth. Cost-saving technologies, integrated contract models, stricter regulatory enforcement, and the well P and A dominance are also rapidly supporting the growth.

Offshore Oil and Gas Market Share, By Service Type, 2025(%)

| By Service Type | Market Share (%) |

| Exploration (Seismic & Survey) | 18.00% |

| Drilling | 28.00% |

| Production & Processing | 34.00% |

| Decommissioning | 9.00% |

| Others | 11.00% |

Platform Type Insights

The fixed platforms segment dominated the market with a 39% share in 2025 and is expected to grow at a CAGR of 3.80% over the forecast period, driven by strong shallow water operations, which need advanced and modernized assets to meet stricter environmental regulations. The integrated facilities, such as fixed structures such as steel jacket and concrete caisson platforms, have high bearing capacity. The rise of upcycled Mobile Offshore Production Units is also a major growth factor in the market.

")

The floating production systems (FPSO, FPU) segment held 33% market share in 2025 and is expected to grow at the fastest rate, with a CAGR of 6.60% over the forecast period, driven by a surge in deepwater and ultra-deepwater reserves where traditional fixed platforms are impractical. New FPS designs are incorporating advanced features to meet decarbonization goals, such as closed flare systems, deepwater intake suction hoses, and digital twin simulations is a fueling growth.

Offshore Oil and Gas Market Share, By Platform Type, 2025(%)

| By Platform Type | Market Share (%) |

| Fixed Platforms | 39.00% |

| Floating Production Systems (FPSO, FPU) | 33.00% |

| Tension Leg Platforms (TLP) | 8.00% |

| Spar Platforms | 7.00% |

| Others | 13.00% |

Water Depth Insights

The shallow water segment dominated the market with a 47% share in 2025 and is expected to grow at a CAGR of 3.50% over the forecast period by leveraging its dense, mature infrastructure and lower capital costs to drive field life extension and decommissioning. While deepwater operations command larger capital outlays, shallow-water depths up to 400 feet remain a highly viable sector for small-to-medium operators. Innovations in horizontal and vertical well integration have made the extraction of "ultra-shallow" natural gas commercially viable.

The ultra-deepwater segment held 19% market share in 2025 and is expected to have the fastest growth with a CAGR of 6.80% in the forecast period due to large untapped reserves in the U.S. Gulf of Mexico, Brazil's pre-salt, and Guyana. This expansion is driven by ultra-high-pressure (20k PSI) equipment, subsea automation, and a shift toward high-yield natural gas and oil extraction as onshore reserves decline supporting growth of the market.

Offshore Oil and Gas Market Share, By Water Depth, 2025(%)

| By Water Depth | Market Share (%) |

| Shallow Water | 47.00% |

| Deepwater | 34.00% |

| Ultra-Deepwater | 19.00% |

Hydrocarbon Type Insights

The crude oil segment dominated the market with a 68% share in 2025 and is expected to grow at a CAGR of 4.30% over the forecast period, driven by the growing deep-water and ultra-deep-water exploration in regions. The rising energy and refined product demand, advanced extraction technology, and regional deepwater focus are increasingly focused on fulfilling the global demand. The increased production capacities due to high investment in infrastructure development support growth.

The natural gas segment held 26% market share in 2025 and is expected to have the fastest growth with a CAGR of 5.60% in the forecast period, driven by high demand from various regions to fulfill the demand for clean and natural fuel and rapid expansion of export infrastructure with advanced extraction technologies, further propelling the growth and expansion of the market. Technological innovation and subsea tiebacks, record investments in global LNG trade, and expansion of floating LNG facilities further propel growth.

Offshore Oil and Gas Market Share, by Hydrocarbon Type , 2025(%)

| By Hydrocarbon Type | Market Share (%) |

| Crude Oil | 68.00% |

| Natural Gas | 26.00% |

| Others | 6.00% |

What are the key benefits of the oil and gas product?

The offshore oil and gas industry provides several significant benefits through access to vast and untapped resources that are present beneath the ocean bed. Offshore exploration opens great opportunities in deep water and ultra deep water fields, which hold large amounts of oil and gas reserves, playing a crucial and most important role in fulfilling the global need for energy and the supply of oil and gas in both domestic and international markets. This access makes it easy to enhance energy security for the countries, which reduces the dependency on imports, which is a crucial benefit of the offshore oil and gas products. The key benefit factor is the economic growth and job creation, which significantly help local and national economies.

Core Benefits & Applications Include:

- Transportation Fuels: Refined products (such as gasoline, diesel, and jet fuel) are easily transported and provide the high energy output needed to power global transit.

- Electricity Generation: Natural gas burns cleaner than coal, providing a reliable, responsive, and efficient energy source for power grids.

- Petrochemical Feedstocks: Oil and gas derivatives are essential raw materials for manufacturing. They are the base for plastics, synthetic rubber, detergents, cosmetics, and pharmaceuticals.

- Agricultural Support: Natural gas is the primary feedstock for producing synthetic ammonia, which is crucial for manufacturing the fertilizers needed to sustain global food production.

- Economic & Industrial Engine: The industry creates millions of jobs worldwide and drives affordability for consumers by keeping energy supplies stable.

Regional Analysis

How did Asia Pacific dominate the Offshore Oil and Gas Market in 2025?

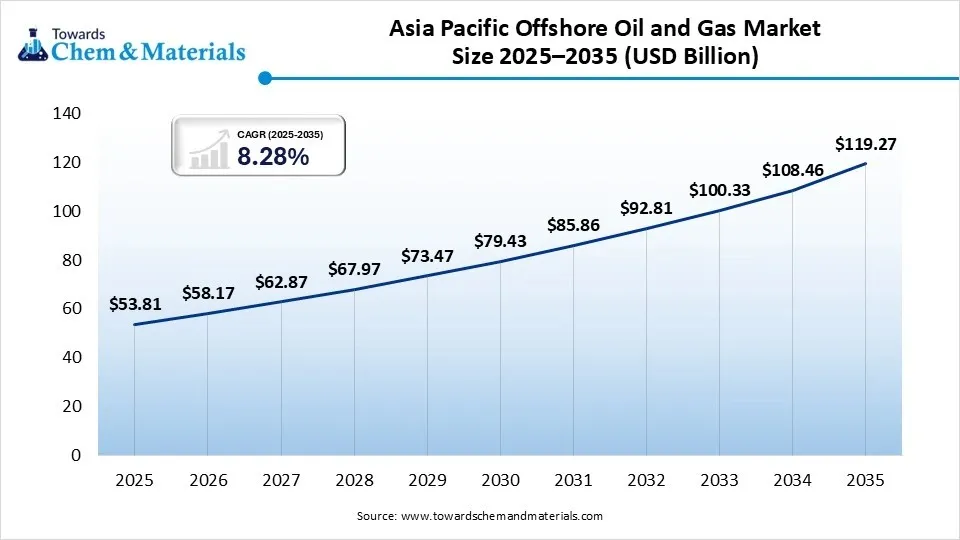

The Asia Pacific offshore oil and gas market size was estimated at USD 53.81 billion in 2025 and is projected to reach USD 119.27 billion by 2035, growing at a CAGR of 8.28% from 2026 to 2035. Asia Pacific dominated the market with a share of 29.00% in 2025 and is expected to have the fastest growth with a CAGR of 8.28% in the forecast period due to the growing demand for domestic energy production and aging onshore fields in the region supporting expansion. The Asia Pacific leadership, such as elevated national oil company budgets and the transition in the region towards the use of natural gas, is a major bridge that fuels the expansion of the market in the region. The regions' shift to gas is highly driven by the climate transitions and power needs; the supply of liquefied natural gas is highly dependent on deep-water gas projects, driving growth.

")

The India offshore oil and gas market is experiencing huge growth in the market, and domestic energy production and key collaborations between major players serve as the major factors in the growth of the market. Technological integration, like advanced reservoir management, deep-sea technologies to maximise efficiency ad digital surveillance supports the growth of the market. The country's low-carbon initiatives, like the integration of carbon capture and storage in offshore platforms to meet the decarbonization goals, support the growth and expansion of the market in the country.

- For instance, ONGC and BP have signed a Technical Services Contract (TSC) to expand their strategic partnership to optimize and boost hydrocarbon production across the Western Offshore Basin in the Arabian Sea. The agreement, originally established through a framework in May 2026 and finalized as a broader contract in June 2026, focuses on counteracting natural production declines in India's most critical offshore energy assets.

(Source: www.sarkaritel.com) - For Instance, India has initiated a comprehensive, two-year, 161,000-line-kilometer offshore seismic survey covering major sedimentary basins in the Bay of Bengal to enhance domestic energy production. Supervised by the Directorate General of Hydrocarbons, this project utilizes recently unblocked maritime zones to map high-potential areas in the Krishna Godavari, Mahanadi, and Andaman basins.(Source: www.gktoday.in)

The China's offshore oil and gas market is a major and critical factor, being a pillar of the nation's energy security, which is dominated by CNOOC. The government mandates for energy independence and domestic energy production, with the presence of offshore fields in the Bohai Gulf and the South China Sea, which account for a major part of China's domestic crude production, support the growth of the market. The technological advancements like advanced seismic inversion, subsea tiebacks, and AI-guided drilling for smart field development help in the extended lifespan of mature fields and support the growth and expansion of the market in the country.

Europe's Offshore Oil and Gas Market Growth Factor

The Europe offshore oil and gas market size was estimated at USD 37.1 billion in 2025 and is projected to reach USD 82.9 billion by 2035, growing at a CAGR of 8.37% from 2026 to 2035.Europe held the market share of 18% in 2025, driven by the expanding infrastructure investment in the region, providing cost-effective methods and helping in advancing and updating the offshore pipeline networks, which is a major and critical growth factor in the region's growth. The technological advancements, like innovation in deepwater extraction, corrosion resistance, and smart monitoring system which, help in unlocking preciously inaccessible deepwater sites, which propels the growth and expansion of the market.

The United Kingdom offshore oil and gas market is experiencing growth, driven by a surge in decommissioning services, as operators are adapting to save capital and repurpose existing infrastructure supporting growth. The government in the country also supports the offshore exploration and licensing of the North Sea, which reduces reliance on imports and also helps in sustaining domestic jobs. The policies for taxation, such as the Energy Profits Levy, which constrain new exploration drilling, encourage the industry to revitalize exploration and production, supporting growth of the market.

The Germany’s offshore oil and gas market is driven by energy security and a focus on a shift towards technological innovations, rapid expansion in offshore wind and LNG to diversify imports, and maintenance of infrastructure that fuels the growth of the market. The energy transition integration with increases in the dominance of fossil fuel and renewable intersections supports the growth of the market. The other major factors that drive growth are upgrading offshore infrastructure, energy security, geopolitical shifts, and declining conventional reserves.

North America Offshore Oil and Gas Market Growth Factor

The North America offshore oil and gas market size was estimated at USD 46.39 billion in 2025 and is projected to reach USD 103.09 billion by 2035, growing at a CAGR of 8.31% from 2026 to 2035. North America held the market share of 23% in 2025 through technological innovation by reducing extraction costs and rising global demand for liquefied natural gas exports, with exclusive investments in ultra-deepwater and deepwater exploration supporting the growth of the market. The region's rapid adoption of digitalization and automation, such as the adoption of digital drilling solutions, hybrid energy systems, and private networks, also helps in lowering the operational cost and significantly improves the operational safety, further supporting the growth and expansion of the market.

The United States offshore oil and gas market is experiencing growth driven by the advancement in deep-water exploration, increased export demand, and federal leasing, with rising investments fueling the growth of the market. The rising international demand and new coastal export terminals, which also help in encouraging the producers of upstream to integrate production in deepwater pipelines in the country, support the growth of the market. The region's adoption of AI, autonomous systems, and real-time drilling analytics also supports increased efficiency and supports the growth of the market.

The Canadian offshore oil and gas market is driven by robust international upstream investments, rising global energy demand, and favourable regulatory exploration incentives that support growth. The massive upstream capital investments in exploration and production support unlocking the new frontier basins like Flemish Pass and the Jeanne d’Arc Basin, supporting growth. The technological advancement like innovation in deepwater drilling technologies and favourable regulatory and licensing frameworks, support the growth.

Latin America Offshore Oil and Gas Market Growth Factor

The Latin America offshore oil and gas market size was estimated at USD 18.6 billion in 2025 and is projected to reach USD 42.5 billion by 2035, growing at a CAGR of 8.61% from 2026 to 2035.Latin America held a market share of 17% in 2025, driven by the highly competitive breakeven prices and rapid payback periods in deepwater and ultra-deepwater plays, supporting the growth of the market. The growing investments in hubs such as Brazil's pre-salt fields and Guyana's prolific Stabroek block and subsea tiebacks to existing floating production, storage, and offloading significantly increase upstream capital. The favorable economics and technological adoption further drive the growth and expansion of the market.

Brazil's offshore oil and gas market is experiencing robust growth, which is extensively driven by the pre-salt productivity in the Santos and Campos basins, which offer high yield and also break national production records, propelling growth. The technological innovation in fields like Búzios, Mero, and Tupi to maximize operational scalability with advanced extraction technologies, along with foreign investment and exports, supports the expansion of the market. The Brazilian government's implementation of the "New Gas Market" (Novo Mercado de Gás) framework fosters a competitive environment and encourages private infrastructure investment, which also supports the growth and expansion of the market in the region.

Argentina's offshore oil and gas market growth is extensively driven by the foreign direct investment incentives, favorable geological analogies, and the need to monetize surplus natural gas, which supports the growth of the market in the country. The promotional regime for large investments framework, which unlocks multi-billion-dollar projects like Argentina LNG and FLNG export terminals in the San Matías Gulf/Bahía Blanca, supports the growth. Deepwater exploration and expanding offshore capabilities by operators like Equinor, Shell, and YPF, and shallow water gas success, support the growth and expansion of the market.

- For instance, the Fénix Gas Pipeline is a 35-kilometer subsea natural gas project off Argentina's Tierra del Fuego coast, which began operations in September with a capacity of 3.65 bcm/y. Operated by TotalEnergies, the project connects the new Fénix field to the Véga Pléyade platform to supply roughly 8% of Argentina's daily gas needs, with ownership shared by Total Austral, Harbour Energy, and Pan American Energy.(Source: www.gem.wiki)

Middle East and Africa Offshore Oil and Gas Market Growth Factor

The Middle East and Africa offshore oil and gas market size was estimated at USD 17.40 billion in 2025 and is projected to reach USD 37.46 billion by 2035, growing at a CAGR of 7.97% from 2026 to 2035.The Middle East and Africa held the market share of 18% in 2025, driven by the massive upstream investments and capacity expansion by major producers in the region like ADNOC and Saudi Aramco, which also supports the growing export demand and accelerates exploration and production, driving growth. The leading national oil companies are aggressively hiking production limits. Rapid urbanization and population growth in the MENA region and Sub-Saharan Africa are directly driving up domestic power requirements.

")

For instance, ADNOC has selected its preferred contractors for the multi-billion-dollar expansion of the Upper Zakum offshore oilfield, which is the world's second-largest offshore oilfield. The landmark development project, valued at over $10 billion, is a critical component of the UAE’s broader strategic initiative to elevate its national oil production capacity to 5 million barrels per day by 2027.(Source: www.upstreamonline.com)

Saudi Arabia's offshore oil and gas market is driven by mega offshore project investments by major players like Saudi Aramco, to major offshore fields like Marjan, Zuluf, and Berri, driving demand for advanced offshore well services, high-performance drilling fluids, and drilling rigs, supporting the growth of the market. The technological advancements, strategic export flexibility, and focus on unconventional gas for power generation and for growing petrochemical sectors support the growth and expansion of the market in the country.

The primary growth factor for the UAE offshore oil and gas market is ADNOC's multibillion-dollar expansion plan aimed at increasing the nation's maximum sustainable production capacity to 5 million barrels per day (bpd). Major developments in offshore fields like Lower Zakum and the Hail and Ghasha sour-gas megaprojects require deepwater drilling, subsea completions, and extensive engineering contracts.

- For instance, ADNOC's Hail and Ghasha project has transitioned deeper into its execution phase, scaling up development on one of the Middle East's largest active sour gas megaprojects. Valued at roughly $17 billion, the project aims to produce 1.8 billion standard cubic feet per day of gas to support the UAE's domestic supply goals. (Source: epcintel.com)

Recent Developments

- The US Bureau of Ocean Energy Management (BOEM) has launched a public comment period to explore using the US Outer Continental Shelf (OCS) for commercial space activities, including rocket launches and vehicle re-entries. The initiative, announced by BOEM Acting Director Matt Giacona, marks a significant regulatory step toward repurposing or co-locating space launch infrastructure within traditional offshore energy basins.(Source:www.upstreamonline.com)

- ExxonMobil affiliate Esso Exploration and Production Nigeria and its partners are investing $1 billion in the Usan Infill Project within Oil Mining Lease (OML) 138 offshore Nigeria. The project is expected to add 40,000 barrels per day (bpd) of oil production. An announcement regarding the investment was made at the 25th NOG Energy Week Conference and Exhibition on 8 July 2026. (Source:www.offshore-technology.com)

Competitive Analysis

The offshore oil and gas sector is experiencing massive competition from key players like Saudi Aramco, ExxonMobil, Chevron, Shell, and TotalEnergies. Aiming to build massive projects with highly capital-intensive investments is a major factor. The growing import and export competition is a major factor in the growth.

- The state-run Syrian Petroleum Company (SPC) has launched an upstream gas development project in Homs province with Saudi energy services firm ADES to rebuild Syria's energy sector following the ouster of Bashar al-Assad. The project sites have been officially handed over to ADES to initiate operations under an implementation agreement finalized earlier this year.(Source: www.al-monitor.com)

- Eni and Libya's National Oil Corporation (NOC) have officially launched production from the Sabratha Compression Project to boost natural gas output from the offshore Bahr Essalam field. The project is operated through their local joint venture, Mellitah Oil & Gas, located roughly 100 kilometres off the Libyan coastline.(Source: decode39.com )

- Chevron has entered the Maltese energy sector to initiate upstream exploration operations for oil and natural gas across frontier offshore acreage positioned between Italy, Libya, and Tunisia. The project aims to establish domestic production in Malta, a nation that currently relies entirely on imported fossil fuels.(Source: egyptoil-gas.com)

Top players in the Offshore Oil and Gas Market & Their Offerings

| Company | Company Type/Position | Major Headquarters | Geographic Presence | Offshore Oil & Gas Offerings | Key Offering/Strength |

| SLB | Leading offshore oilfield services provider | Houston | North America, Europe, Middle East, Asia Pacific, Africa | Offshore drilling, well construction, production systems, digital oilfield solutions | Comprehensive offshore exploration and production technologies with strong digital capabilities |

| Halliburton company | Global provider of offshore energy services | Houston | North America, Europe, Middle East, Asia Pacific, Latin America | Offshore drilling services, well completion, cementing, reservoir evaluation, production optimization | Integrated offshore well lifecycle solutions and advanced drilling technologies |

| Baker Hughes company | Energy technology and oilfield services provider | Houston | North America, Europe, Middle East, Asia Pacific, Africa | Offshore drilling equipment, subsea production systems, turbomachinery, digital asset management | Broad offshore technology portfolio with a strong focus on operational efficiency |

| TechnipFMC plc | Offshore engineering and subsea systems provider | Newcastle | Europe, North America, South America, Asia Pacific, Middle East | Subsea production systems, flexible pipes, engineering, procurement, and construction (EPC) services | Leadership in integrated subsea technologies and offshore project execution |

| Saipem S.p.A. | Offshore engineering, drilling, and construction contractor | Milan | Europe, Middle East, Africa, Asia Pacific, Americas | Offshore drilling, platform construction, subsea engineering, installation, and maintenance services | Extensive experience in complex offshore engineering and deepwater infrastructure projects |

Market Top Key Players

- Saudi Aramco – Saudi Arabia

- ExxonMobil – United States

- Chevron – United States

- Shell – United Kingdom/Netherlands

- TotalEnergies – France

- BP – United Kingdom

- Petrobras – Brazil

- Equinor – Norway

- CNOOC – China

- Eni – Italy

- ConocoPhillips – United States

- PetroChina / CNPC – China

- Rosneft – Russia

- Lukoil – Russia

- Woodside Energy – Australia

- Petronas – Malaysia

- QatarEnergy – Qatar

- ADNOC – United Arab Emirates

- Equatorial Guinea's National Oil Company (GEPetrol) – Africa

- ONGC (Oil and Natural Gas Corporation) – India

Segments Covered:

By Service Type

- Exploration (Seismic & Survey)

- 2D Seismic Survey

- 3D Seismic Survey

- 4D Seismic Monitoring

- Geological & Geophysical Studies

- Drilling

- Exploration Drilling

- Development Drilling

- Directional Drilling

- Well Completion

- Production & Processing

- Production Operations

- Well Intervention

- Subsea Processing

- Flow Assurance

- Maintenance Services

- Decommissioning

- Well Plugging & Abandonment

- Platform Removal

- Pipeline Removal

- Site Remediation

- Others

- Inspection Services

- Digital Monitoring

- Logistics

- Support Vessels

By Platform Type

- Fixed Platforms

- Jacket Platforms

- Gravity-Based Structures

- Floating Production Systems (FPSO, FPU)

- FPSO

- FPU

- Tension Leg Platforms (TLP)

- Spar Platforms

- Others

- Jack-Up Rigs

- Semi-Submersibles

- Drillships

By Water Depth

- Shallow Water

- Up to 500 meters

- Deepwater

- 500–1,500 meters

- Ultra-Deepwater

- Above 1,500 meters

By Hydrocarbon Type

- Crude Oil

- Light Crude

- Medium Crude

- Heavy Crude

- Natural Gas

- Conventional Gas

- Associated Gas

- LNG Feed Gas

- Others

- Condensates

- Natural Gas Liquids

By Regions

- North America

- Europe

- Asia Pacific

- Middle East & Africa

- Latin America

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

FAQ's

Select User License to Buy

Figures (6)