Content

Metal Recycling Market Size, Share and Trends Report 2035

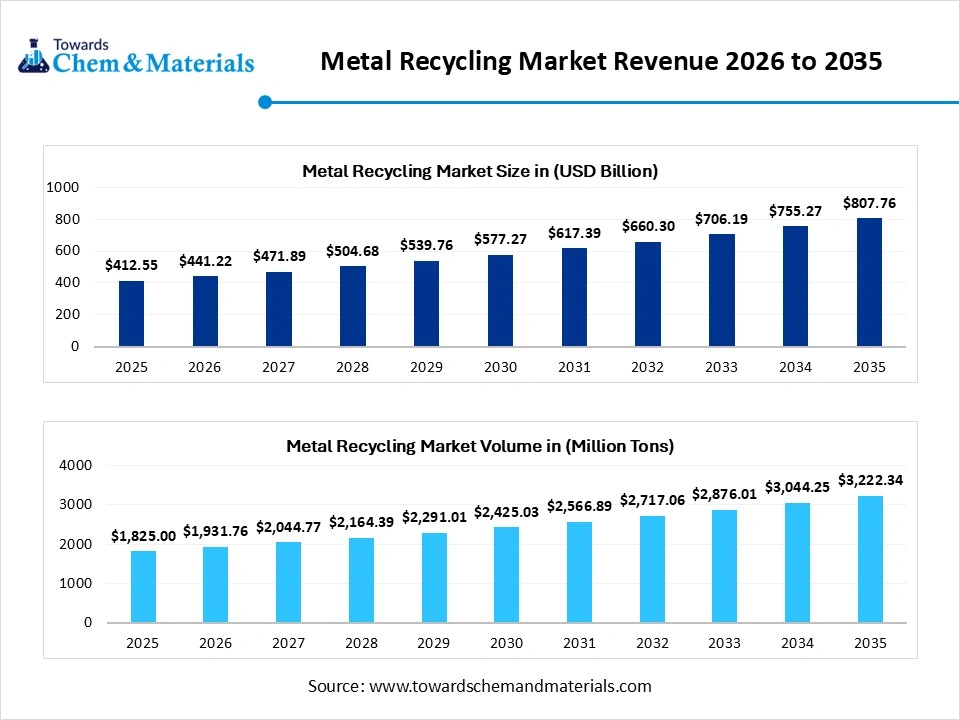

The global metal recycling market was valued at USD 412.55 billion in 2025, is estimated to reach USD 441.22 billion in 2026, and is projected to reach USD 807.76 billion by 2035, growing at a CAGR of 6.95% from 2026 to 2035. In terms of volume, the metal recycling market is projected to grow from 1825 million tons in 2025 to 3222.34 million tons by 2035. growing at a CAGR of 5.85% from 2026 to 2035.

Key Takeaways

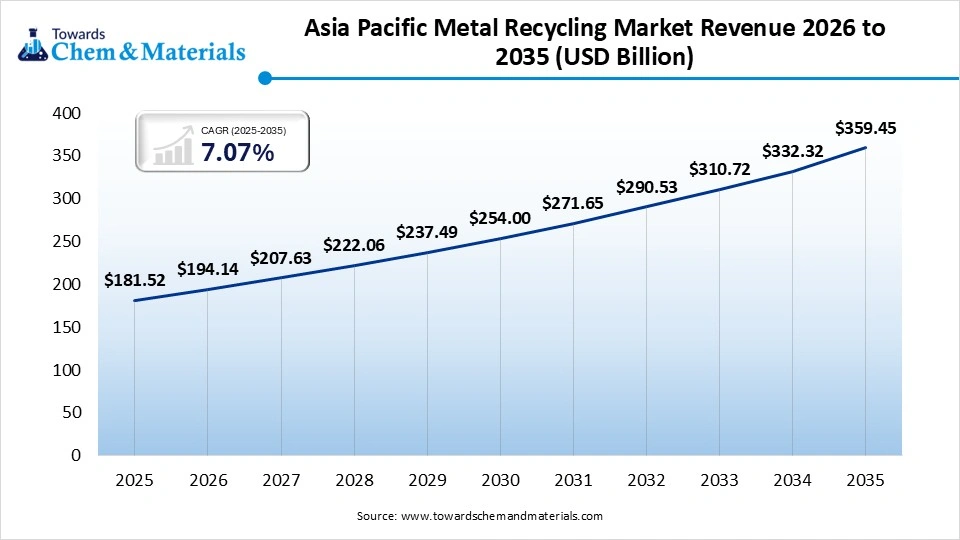

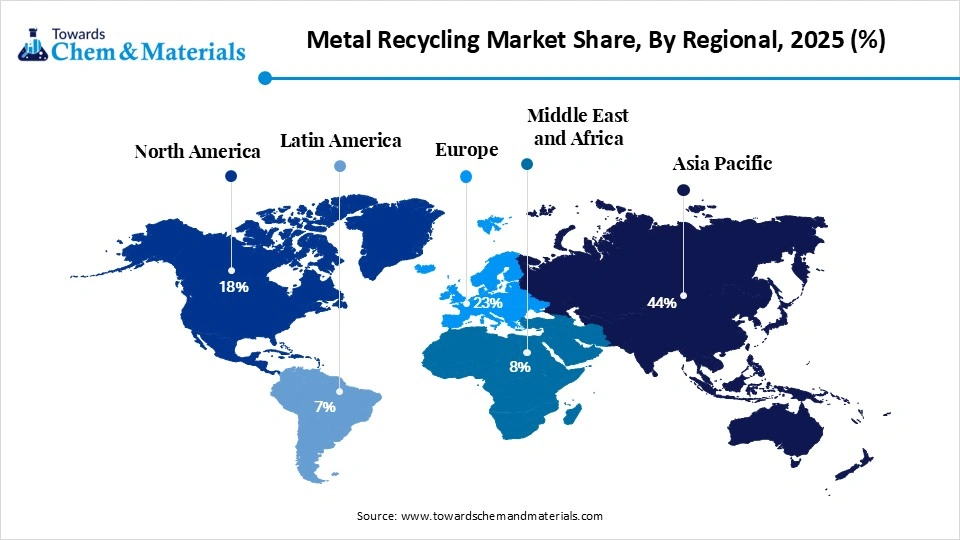

- By region, Asia Pacific dominated the market with the largest share of 44% in 2025 and is expected to grow at the fastest CAGR of 7.4% over the forecast period.

- By region, Europe held the market share of 23% in 2025.

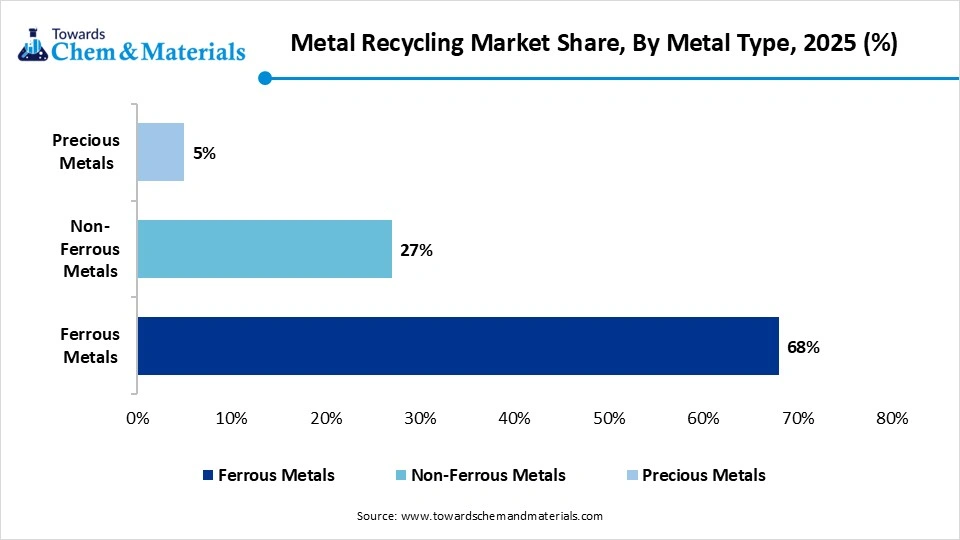

- By metal type, the ferrous metals segment dominated the market with the largest share of 68% in 2025.

- By metal type, the non-ferrous metals segment is expected to grow at the fastest CAGR of 7.8% over the forecast period.

- By scrap source, the old scrap (post-consumer) segment dominated the market with the largest share of 61% in 2025.

- By scrap source, the new scrap (pre-consumer) segment is expected to grow at the fastest CAGR of 7.4% during the forecast period.

- By processing method, the mechanical processing segment dominated the market with the largest share of 52% in 2025.

- By processing method, the hydrometallurgical processing segment is expected to grow at the fastest CAGR of 8.1% over the forecast period.

- By application, the building & construction segment dominated the market with the largest share of 34% in 2025.

- By application, the electrical & electronics segment is expected to grow at the fastest CAGR of 7.9% during the study period.

- By distribution channel, the direct sales (B2B) segment dominated the market with the largest share of 49% in 2025.

- By distribution channel, the online trading platforms segment is expected to grow at the fastest CAGR of 8.4% during the study period.

Market Size and Volume Forecast

- Market Estimated Size (2026): USD 441.22 Billion | CAGR (2026–2035): 6.95%

- Market Projected Size (2035): USD 807.76 Billion

- Market Volume (2025): 1,825 Million Tons (MT) | Volume CAGR (2026–2035): 5.85%

- Market Projected Volume (2035): 3,222.34 Million Tons (MT)

- Market Pricing (2025):

- Average Manufacturing Price: USD 425/Ton

- Average Selling Price: USD 615/Ton

- Pricing CAGR (2025–2035): 2.11%

What is Metal Recycling Market?

The market encompasses the industrial process of gathering, sorting, shredding, and melting obsolete metal products to create essential raw materials for new production. The market supplies these materials to high-demand sectors such as Automotive (car bodies, engines), Building & Construction (beams, rebar), and Electronics (e-waste recovery).

Metal Recycling Market Trends

- Increasing focus on sustainable manufacturing and circular economy principles is the latest trend in the market, shaping positive market growth. The shift is mainly driven by the demand to minimize carbon footprints and the depletion of virgin metal reserves. This approach conserves valuable resources by reducing environmental impact.

- The growing global demand for metals, along with the increased focus on resource conservation and sustainability, is one of the major factors driving market growth. Major players are recognizing the ecological and economic benefits of using recycled metals over virgin materials.

- There is an increasing emphasis on recovering high-value metals such as gold, copper, and silver from electronic waste (e-waste), which is another major trend in the market. Steelmakers are transitioning from conventional blast furnaces to Electric Arc Furnaces (EAFs), which use recycled scrap as a main feedstock to cut emissions.

Report Scope

| Report Attribute | Details |

| Market Size and Volume in 2026 | USD 441.22 Billion / 1931.76 Million Metric Tons |

| Expected Size and Volume by 2035 | USD 807.76 Billion / 3222.34 Million Metric Tons |

| Growth Rate from 2026 to 2035 | CAGR 6.95% |

| Forecast Period | 2026 - 2035 |

| Dominant Region | Asia-Pacific |

| Segment Covered | By Metal Type, By Scrap Source, By Processing Method, By Application, By End-Use Industry, By Distribution Channel and By Regions |

| Key companies profiled | GFG Alliance, Norsk Hydro ASA, Kimmel Scrap Iron & Metal Co., Inc., Schnitzer Steel Industries, Inc., Novelis, Tata Steel, Sims Metal, Utah Metal Works |

How Cutting-Edge Technologies Are Revolutionizing the Metal Recycling Market?

Advanced technologies are transforming the market by shifting it from labour-intensive manual sorting to high-precision, automated, and data-driven operations. Furthermore, sensors and equipment offer real-time data on material flows and machine performance, facilitating predictive maintenance that minimizes overall unplanned downtime, leading to market growth soon.

Metal Recycling Market Supply Chain Analysis

Feedstock Procurement

It involves sourcing, purchasing, and collecting waste metal, both post-industrial and post-consumer scrap, to be processed, refined, and reused as raw material in new metal production.

- Major Players: Gravita India Ltd, Pondy Oxides & Chemicals Ltd (POCL)

Chemical Synthesis and Processing

It refers to the use of chemical reactions and metallurgical methods to recover, purify, and refine high-grade metals from complex waste streams.

- Major Players: Dowa Holdings, Tanaka

Packaging and Labelling

It refers to the design, material selection, and informational labeling of metal containers to ensure they are easily separable, identifiable, and fully recyclable at the end of their life cycle.

- Major Players: Crown Holdings, Inc., Ardagh Group S.A

Regulatory Compliance and Safety Monitoring

It involves adhering to strict environmental, occupational, and legal standards to control emissions, manage hazardous waste, and protect workers, fueled by growing ESG principles.

- Major Players: Sims Metal Management, Commercial Metals Company (CMC)

Metal Recycling Market's Regulatory Landscape: Global Regulations

| Country/Region | Key Regulations |

| European Union (EU) | From May 21, 2026, new rules strictly govern the export of metal waste. Documentation must be digital and highly transparent, aiming to prevent the export of "dirty" or hazardous scrap to countries with lower environmental standards. |

| China | 2026 Export Licenses: Beginning January 1, 2026, China reintroduced export licenses for roughly 300 steel products, including pig iron and steel scrap, to stabilize domestic supply and manage trade frictions. |

| India | Solid Waste Management (SWM) Rules 2026: Taking full effect on April 1, 2026, these rules mandate four-stream segregation at the source, specifically separating "dry waste" (including metals) for transport to Material Recovery Facilities (MRFs). |

Market Dynamics

Driver

Government Initiatives for Sustainable Practices

The governments in various regions are encouraging sustainable practices, which have had a significant impact on the metal recycling business. The investments in this metal recycling infrastructure can make the recycling process more cost-effective, smooth, and efficient. This initiative further aims to maximize resource utilization, driving market growth soon.

Restraint

High Operational Costs

High operational costs in metal recycling, such as processing and transportation, reduce profitability, which is the major factor hindering market growth. Moreover, strict environmental regulations, like the EU's Waste Framework Directive, increase overall compliance costs.

Opportunity

Technological Innovations in Recycling Processes

Ongoing technological advancements in recycling technologies are improving the metal recovery and efficiency, creating lucrative opportunities in the market. These innovations optimise the extraction of metals from complex waste streams, hence growing the yield of recycled materials.

Segmental Insights

Metal Type Insights

The Ferrous Segment Dominated the Market with 68% of Market Share in 2025

The ferrous metals segment dominated the market with the largest share of 68% in 2025. The dominance of the segment can be attributed to its high-volume usage in the construction and infrastructure sector, along with the presence of established collection systems. Steel recycling reduces energy consumption significantly.

The non-ferrous metals segment held the market share of 27% in 2025 and is expected to grow at the fastest CAGR of 7.8% over the forecast period. The growth of the segment can be credited to the increasing demand for lightweight materials and the surge in electronics usage. Also, higher-value metal enhances profitability.

The precious metals segment held the market share of 5% in 2025. The growth of the segment can be linked to the rising e-waste volumes and increasing electronics recycling. High market value further incentivizes the recycling process.

Scrap Source Insights

The Old Scrap (Post-Consumer) Segment Dominated the Market with 61% of Market Share in 2025

The old scrap (post-consumer) segment dominated the market with the largest share of 61% in 2025. The dominance of the segment can be driven by a surge in the number oof end of end-of-life vehicles and ongoing infrastructure demolition projects, which generate large scrap volumes. Strong recycling regulations fuel recovery rates.

Metal Recycling Market Share, By Scrap Source, 2025 (%)

| By Scrap Source | Revenue Share, 2025 (%) |

| Old Scrap (Post-consumer) | 61% |

| New Scrap (Pre-consumer) | 39% |

The new scrap (pre-consumer) segment held the market share of 39% in 2025 and is expected to grow at the fastest CAGR of 7.4% during the forecast period. The growth of the segment is owing to the increasing industrial output and enhancements in industrial efficiency. A rise in industrial output will soon increase scrap generation.

Processing Method Insights

The Mechanical Processing Segment Dominated the Market with 52% of Market Share in 2025

The mechanical processing segment dominated the market with the largest share of 52% in 2025. The dominance of the segment is due to the growing adoption of advanced sorting technologies and their extensive use across recycling facilities. Cost-effective methods support large-scale operations.

Metal Recycling Market Share, By Processing Method, 2025 (%)

| By Processing Method | Revenue Share, 2025 (%) |

| Mechanical Processing | 52% |

| Pyrometallurgical Processing | 30% |

| Hydrometallurgical Processing | 18% |

The hydrometallurgical processing segment held the market share of 18% in 2025 and is expected to grow at the fastest CAGR of 8.1% over the forecast period. The growth of the segment can be credited to the growing demand for sustainable methods and their lower emissions as compared to the thermal process. It is efficient for extracting metals from complex waste systems.

The pyrometallurgical processing segment held the market share of 30% in 2025. The growth of the segment can be attributed to the ongoing technological innovations in processing, along with its suitability for bulk metal recycling. High-temperature process recovers metal effectively.

Application Insights

The Building & Construction Segment Dominated the Metal Recycling Market with 34% of Market Share in 2025

The building & construction segment dominated the market with the largest share of 34% in 2025. The dominance of the segment can be credited to the construction of large-scale projects, which increases metal demand, coupled with the enforcement of government regulations. Sustainable construction practices further support recycling.

Metal Recycling Market Share, By Application, 2025 (%)

| By Application | Revenue Share, 2025 (%) |

| Building & Construction | 34% |

| Automotive | 22% |

| Packaging | 14% |

| Electrical & Electronics | 16% |

| Industrial Machinery | 12% |

The electrical & electronics segment held the market share of 16% in 2025 and is expected to grow at the fastest CAGR of 7.9% during the study period. The growth of the segment can be driven by a surge in e-waste volumes, increasing recycling volumes, and technological innovations enhancing extraction. Valuable metal recovery propels profitability.

The automotive segment held the market share of 22% in 2025. The growth of the segment is owing to increasing demand for lightweight materials and growing vehicle production globally. End-of-life vehicle recycling boosts supply shortly.

Distribution Channel Insights

The Direct Sales (B2B) Segment Dominated the Market with 49% of Market Share in 2025

The direct sales (B2B) segment dominated the market with the largest share of 49% in 2025. The dominance of the segment can be attributed to strong industrial demand for metal recycling and long-term contracts between recyclers and manufacturers. Bulk transaction enhances margins.

Metal Recycling Market Share, By Distribution Channel, 2025 (%)

| By Distribution Channel | Revenue Share, 2025 (%) |

| Direct Sales (B2B) | 49% |

| Scrap Dealers | 34% |

| Online Trading Platforms | 17% |

The online trading platforms segment held the market share of 17% in 2025 and is expected to grow at the fastest CAGR of 8.4% during the study period. The growth of the segment can be credited to the increasing digitalization, and its ease of transactions attracts small and large buyers. Digital platform enhances profitability.

The scrap dealers segment held the market share of 34% in 2025. The growth of the segment can be driven by a wide collection network to ensure a steady scrap supply along with efficient aggregation systems. The informal sector plays a crucial role in the developing market.

Regional Insights

How did Asia Pacific Dominate the Metal Recycling Market in 2025?

Asia Pacific dominated the market with the largest share of 44% in 2025 and is expected to grow at the fastest CAGR of 7.4 % over the forecast period. The dominance and growth of the region can be attributed to the ongoing urbanisation, rapid industrialization, and strict environmental regulations in emerging nations. In addition, extensive growth of cities creates substantial construction waste while necessitating large amounts of recycled steel, copper, and aluminium.

")

China Metal Recycling Market Trends

In the Asia Pacific, China dominated the market owing to the stringent government policies supporting a circular economy to minimize emissions. Also, the expanding electric vehicle (EV) and renewable energy sectors are fuelling the demand for recycled non-ferrous metals such as nickel, copper, and lithium.

Europe held the market share of 23% in 2025. The growth of the region can be credited to the stringent decarbonization targets and robust EU circular economy policies. Furthermore, major players such as EMR, Aurubis, and TSR Recycling have established a wide infrastructure, improving the market's overall efficiency and capacity.

Germany Metal Recycling Market Trends

The growth of the market in the country is due to a surge in electronic waste recycling and a rise in demand for recycled materials in the construction and automotive sectors. Moreover, major automotive, manufacturing, and construction sectors in Germany generate consistent and massive demand for high-grade recycled metals, especially steel, iron, and aluminium.

Recent Development

- In January 2026, the European Aluminium Foil Association (EAFA) and Flexible Packaging Europe (FPE) established a new alliance to boost recycling for small aluminium items like coffee capsules, dairy lids, and snack wrappers. The initiative aims to improve collection and sorting infrastructure across Europe to meet new environmental regulations.

Top Metal Recycling Market Company

- European Metal Recycling: European Metal Recycling (EMR) is a premier global player in the European metal recycling sector, operating alongside companies like Aurubis and TSR to manage vast ferrous and non-ferrous scrap networks.

- CMC: Commercial Metals Company (CMC) is a major player in the global metal recycling market, operating as a vertically integrated manufacturer and recycler of steel and metal products.

Metal Recycling Market Companies

- GFG Alliance

- Norsk Hydro ASA

- Kimmel Scrap Iron & Metal Co., Inc.

- Schnitzer Steel Industries, Inc.

- Novelis

- Tata Steel

- Sims Metal

- Utah Metal Works

Metal Recycling Market Segments Covered in the Report

By Metal Type

- Ferrous Metals

- Steel

- Iron

- Non-Ferrous Metals

- Aluminum

- Copper

- Lead

- Zinc

- Nickel

- Precious Metals

- Gold

- Silver

- Platinum Group Metals (PGMs)

By Scrap Source

- Old Scrap (Post-consumer)

- End-of-Life Vehicles (ELV)

- Construction & Demolition Scrap

- Consumer Appliances

- New Scrap (Pre-consumer)

- Industrial Scrap

- Manufacturing Waste

By Processing Method

- Mechanical Processing

- Shredding

- Sorting & Separation

- Pyrometallurgical Processing

- Smelting

- Refining

- Hydrometallurgical Processing

- Leaching

- Electro-winning

By Application

- Construction

- Structural Steel

- Reinforcement Bars

- Automotive

- Vehicle Manufacturing

- Auto Components

- Packaging

- Metal Cans

- Foils

- Electrical & Electronics

- Wiring

- Circuit Boards

- Industrial Machinery

- Equipment Manufacturing

- Heavy Machinery

By End-Use Industry

- Building & Construction

- Automotive

- Electrical & Electronics

- Packaging

- Industrial Manufacturing

- Others

- Aerospace

- Shipbuilding

By Distribution Channel

- Direct Sales (B2B)

- Scrap Dealers

- Online Trading Platforms

By Region

- North America:

- U.S.

- Canada

- Mexico

- Rest of North America

- Latin America:

- Brazil

- Argentina

- Rest of Latin America

- Europe:

- Western Europe

- Germany

- Italy

- France

- Netherlands

- Spain

- Portugal

- Belgium

- Ireland

- UK

- Iceland

- Switzerland

- Poland

- Rest of Western Europe

- Eastern Europe

- Austria

- Russia & Belarus

- Türkiye

- Albania

- Rest of Eastern Europe

- Asia Pacific:

- China

- Taiwan

- India

- Japan

- Australia and New Zealand,

- ASEAN Countries (Singapore, Malaysia)

- South Korea

- Rest of APAC

- MEA:

- GCC Countries

- Saudi Arabia

- United Arab Emirates (UAE)

- Qatar

- Kuwait

- Oman

- Bahrain

- South Africa

- Egypt

- Rest of MEA

- GCC Countries

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

FAQ's

Select User License to Buy

Figures (4)