Content

What is the Metal Casting Market Size and Share?

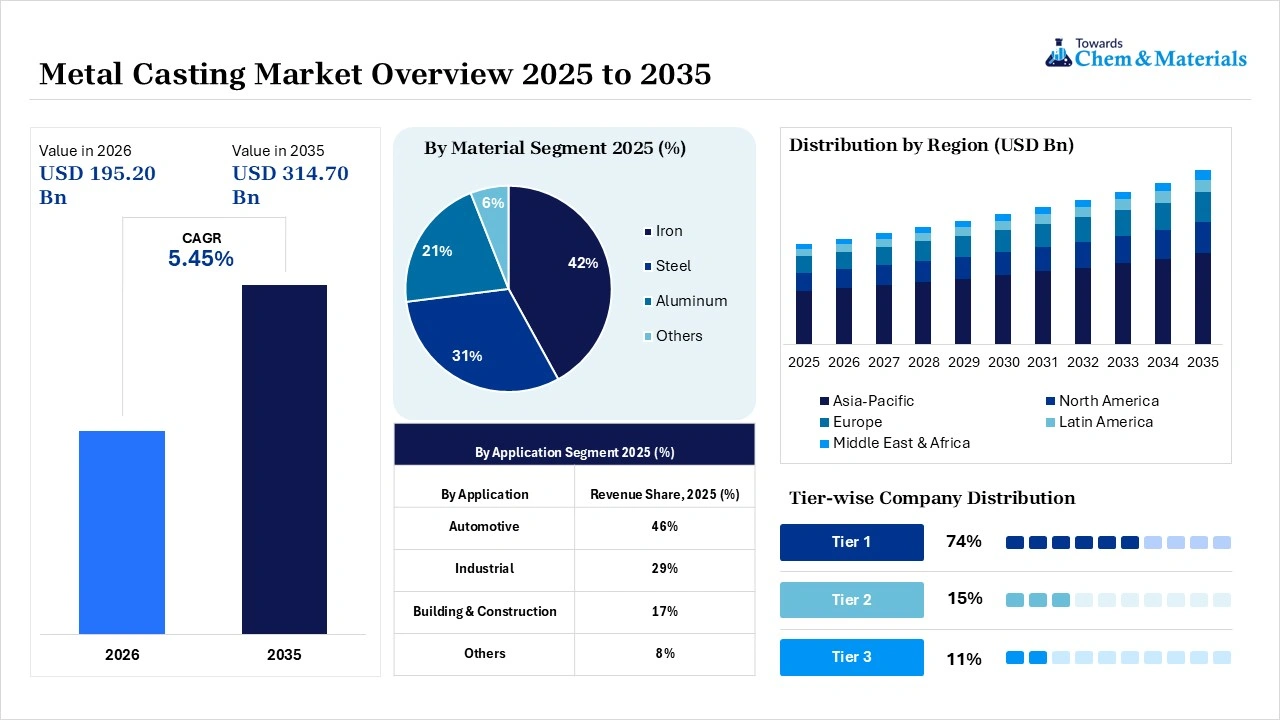

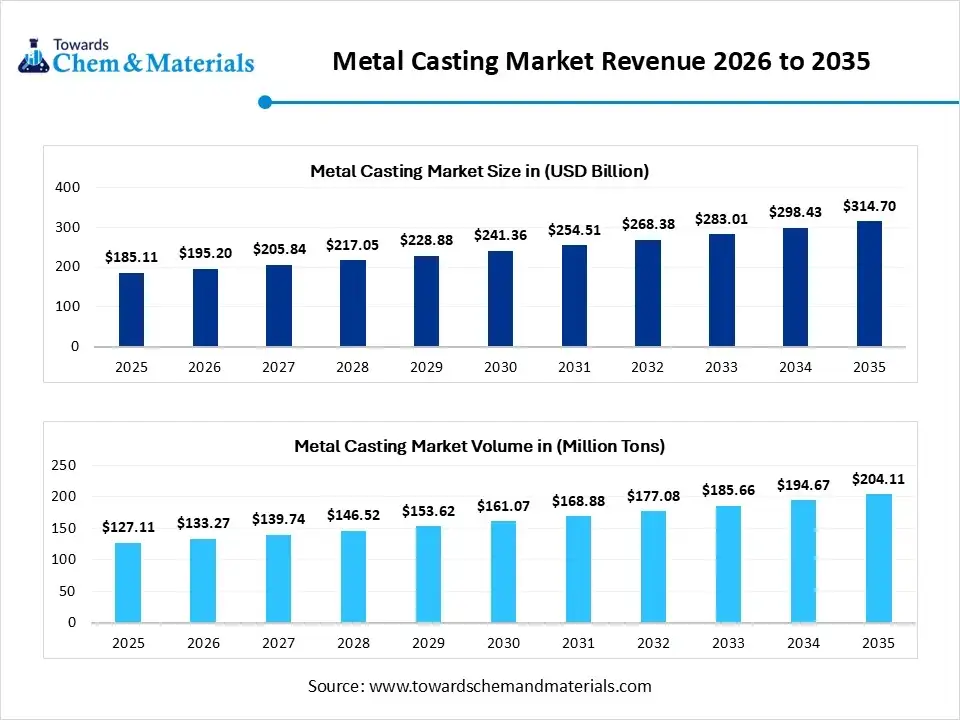

The global metal casting market size was valued at USD 185.11 billion in 2025, is estimated to reach USD 195.20 billion in 2026, and is projected to reach USD 314.70 billion by 2035, exhibiting a compound annual growth rate (CAGR) of 5.45% over the forecast period from 2026 to 2035. Asia Pacific dominated the metal casting market with the largest revenue share of 53% in 2025 and is expected to grow at the fastest CAGR of 5.55% during the forecast period. In terms of volume, the metal casting industry is projected to grow from 127.11 million tons in 2025 to 204.11 million tons by 2035. growing at a CAGR of 4.85% from 2026 to 2035. The growth of the market is driven by the cost-effectiveness and growing demand from industries, which drives the growth of the market.

The metal casting industry is crucial to modern manufacturing, enabling the mass production of complex, durable, and lightweight metal parts at lower costs than processes like forging or machining. It supports lightweighting initiatives and Electric Vehicle (EV) development through "giga casting,' which involves pouring entire structural sections of vehicles in one mold. Steel castings are essential for structural load-bearing parts and components used in power-generation turbines. Innovations such as ultra-large die casting, or giga-casting, let automakers produce large structural body sections in single casts, greatly reducing costs.

Metals like steel and ductile iron are widely used in construction due to their high strength, toughness, and wear resistance in load-bearing roles. Precision methods like investment casting create intricate geometries needed for medical devices, orthopedic implants, dental tools, and surgical instruments. Advances in technology, including 3D printing and automated molding lines, facilitate fast prototyping and the high-precision manufacturing of components.

Market Highlights

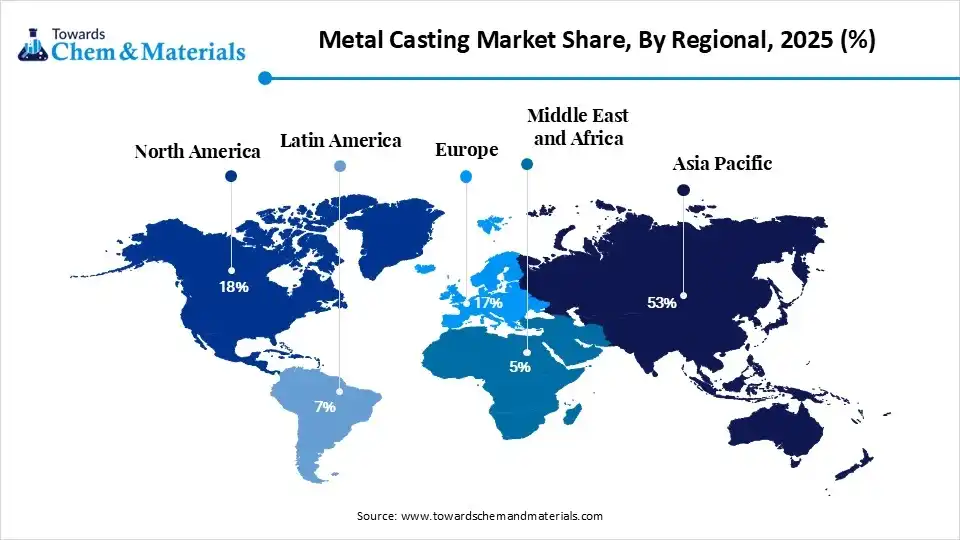

- By region, Asia Pacific dominated the market with a share of 53% in 2025. Large manufacturing base supports extensive casting production.

- By region, North America held 18% market share in 2025 and is expected to experience the fastest growth with a CAGR of 6.30% in the forecast period. Advanced manufacturing capabilities sustain market demand.

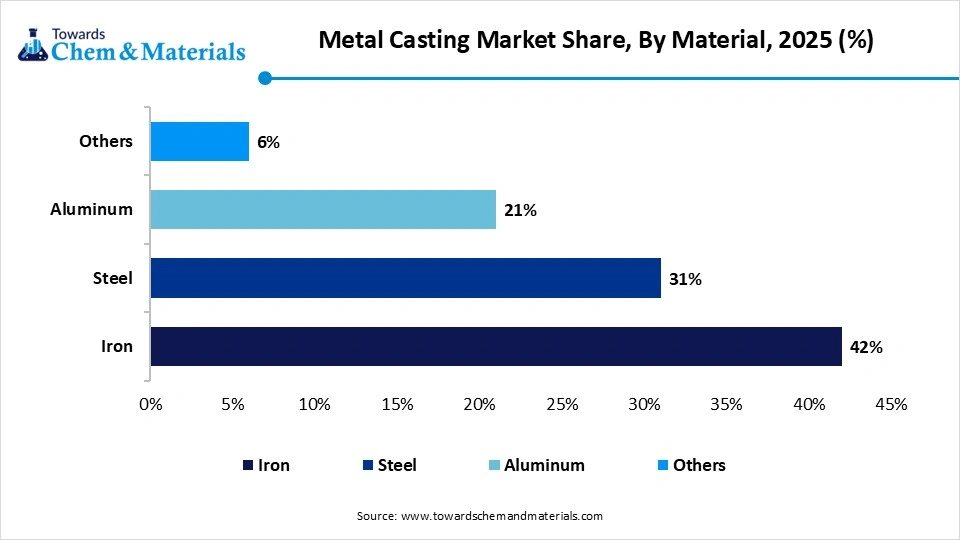

- By material, the iron segment dominated the market with 42% share in 2025. Heavy demand from the automotive and infrastructure sectors

- By material, the steel segment held 31% market share in 2025 and is expected to have the fastest growth with a CAGR of 5.8% in the forecast period. Rising demand for high-strength components drives adoption.

- By application, the automotive segment dominated the market with 46% share in 2025. Vehicle production continues to expand globally.

- By application, the industrial segment held 29% market share in 2025 and is expected to have the fastest growth with a CAGR of 5.6% in the forecast period. Industrial automation increases equipment production.

Market Trends

- Sustainability and Green Casting: Foundries are significantly increasing the use of recycled scrap to reduce their carbon footprint. Stricter environmental regulations, like those in the EU, are forcing the industry toward energy-efficient melting practices.

- Advanced Technologies: The industry is adopting digital imaging, X-ray flaw detection systems, and casting simulation software to drastically improve precision and reduce manufacturing defects.

- Lightweighting in Automotive: Driven by stricter emissions standards and the shift toward electric vehicles (EVs), automakers are replacing heavier parts with aluminum and magnesium to improve range and fuel efficiency.

Report Scope

| Report Attribute | Details |

| Market Size and Volume in 2026 | USD 195.20 Billion / 133.27 Million Tons |

| Revenue Forecast in 2035 | USD 314.70 Billion / 204.11 Million Tons |

| Growth Rate | CAGR 5.45% |

| Base Year of Estimation | 2025 |

| Forecast Period | 2025 - 2035 |

| High Impact Region | Asia Pacific |

| Segment Covered | By Material, By Application, By Region |

| Key Companies Profiled | Ryobi Limited, GF Casting Solutions (Georg Fischer), Nemak, Endurance Technologies Limited, Posco Holdings & Kobe Steel, Hitachi Metals, Rheinmetall AG, Dynacast International, Precision Castparts Corp. (PCC), Doosan Heavy Industries and Construction, Xinxing Ductile Iron Pipes, Amsted Rail, Aisin Group, Nucor Corporation, ArcelorMittal, Kobe Steel, Alcoa Corporation |

Key Technological Shifts in the Metal Casting Market Through Technological Advancements:

The metal casting market is rapidly evolving, driven by the shift to electric vehicles (EVs), the need for lightweight components, and Industry 4.0. Foundries are moving away from traditional processes to high-tech, precision-based manufacturing by adopting gigacasting, 3D printing, AI simulation software, and robotic automation. 3D printing is used to create sand cores, molds, and wax patterns quickly and affordably. Automakers are replacing multi-part assemblies with massive, single-piece structural castings like Tesla's Gigacasting to reduce weight, improve rigidity, and lower production costs.

Metal Casting Market Regulatory Landscape

| Country / Region | Regulatory Body | Key Regulations | Focus Areas | Notable Notes |

| United States | Occupational Safety and Health Administration (OSHA); Environmental Protection Agency (EPA); American Foundry Society (AFS) | Clean Air Act; OSHA Foundry Standards; Hazardous Waste Regulations | Worker safety, emissions control, and sustainable foundry operations | The U.S. regulates metal casting emissions, silica exposure, and waste management while promoting energy-efficient foundry technologies. |

| European Union | European Commission; European Chemicals Agency (ECHA) | REACH Regulation; Industrial Emissions Directive (IED); EU Green Deal | Emissions reduction, energy efficiency, circular manufacturing | Europe emphasizes low-emission foundries, recycled metals, and sustainable casting technologies. |

| China | Ministry of Industry and Information Technology (MIIT); Ministry of Ecology and Environment (MEE) | Foundry Industry Access Conditions; Environmental Protection Law | Energy-efficient foundries, industrial modernization | China is modernizing foundry operations and promoting green manufacturing in the metal casting industries. |

| India | Ministry of Steel; Central Pollution Control Board (CPCB) | Environmental Protection Act; National Manufacturing Policies | Industrial expansion, pollution control | India supports foundry modernization and sustainable manufacturing practices through industrial development initiatives. |

| Japan | Ministry of Economy, Trade and Industry (METI) | Industrial Safety and Health Law; Energy Conservation Act | Precision casting, energy-efficient production | Japan focuses on high-precision casting technologies for the automotive and electronics industries. |

Supply Chain Analysis of the Metal Casting Market:

- Metal Melting & Casting Processing:Metal casting involves melting ferrous and non-ferrous metals and pouring them into molds through processes such as sand casting, die casting, investment casting, and centrifugal casting to manufacture industrial components.

- Key players: Nemak, Ryobi Limited, Georg Fischer, Hitachi Metals

- Quality Testing and Certification:Metal castings must comply with standards for dimensional accuracy, tensile strength, heat resistance, metallurgical quality, and industrial safety requirements before commercial use.

- Key players: International Organization for Standardization, ASTM International, American Foundry Society, SAE International

- Distribution to Industrial Users:Metal castings are supplied to automotive manufacturers, aerospace companies, industrial machinery producers, construction equipment manufacturers, and energy sector applications.

- Key players: Nemak, Ryobi Limited, Georg Fischer.

Metal Casting Market Dynamics

| Drivers | Restrains | Opportunities |

| Automotive Lightweighting & EV Shift: | High Energy and Operational Costs: | Automated Foundries: |

| The transition toward Electric Vehicles and stricter emission standards requires vehicle weight reduction. This drives a massive shift toward high-strength, lightweight aluminum and magnesium castings for chassis, battery housings, and engine blocks. | Foundries are highly energy-intensive, requiring immense heat for metal melting and mold preparation. Rising electricity and fuel prices directly reduce profit margins. | The integration of robotics, AI, and automated pouring processes minimizes defects, lowers labor costs, and enables "smart" manufacturing practices. |

| Infrastructure & Urbanization: | Strict Environmental Regulations: | 3D Printing & Rapid Prototyping: |

| Rapid industrialization and heavy investments in smart cities, public transit, and commercial construction globally require massive volumes of structural cast iron and steel components | Stricter industrial emission standards require foundries to make heavy capital investments in filtration systems, waste recycling infrastructure, and pollution-control technologies. | Additive manufacturing 3D sand printing significantly reduces tooling times and allows for the production of highly complex casting geometries without traditional, costly molds. |

| Industrial Machinery Demand: | Skilled Labor Shortages: | Renewable Energy Infrastructure: |

| Expanding manufacturing sectors necessitate robust, durable cast metal components for heavy-duty equipment, mining, and agricultural machinery. | Foundries needs highly trained professionals for casting operations, and a deficit in this workforce limits production efficiency & capacity utilization. | The rapid expansion of wind, solar, and thermal power generation requires heavy steel and iron castings for turbines, valves, and pressure vessels. |

Segmental Insights

Material Insights

The iron segment dominated the market with 42% share in 2025. The growth is driven by massive demand for engine blocks, industrial machinery, and infrastructure components. The segment is evolving through the modernization of foundries, adopting technologies like 3D printing, AI-driven quality control, and automated sand molding. Iron casting manufacturers are successfully developing thinner, precision-engineered, lightweight components to meet strict fuel efficiency and performance standards.

") The steel segment held 31% market share in 2025 and is expected to have the fastest growth with a CAGR of 5.8% in the forecast period. This expansion is driven by surging demand for durable, high-strength metal components across automotive, heavy machinery, and renewable energy sectors. Rising investments in urbanization and railway networks are driving the need for steel components like girders, beams, and structural connectors.

The steel segment held 31% market share in 2025 and is expected to have the fastest growth with a CAGR of 5.8% in the forecast period. This expansion is driven by surging demand for durable, high-strength metal components across automotive, heavy machinery, and renewable energy sectors. Rising investments in urbanization and railway networks are driving the need for steel components like girders, beams, and structural connectors.

The aluminium segment held 21% market share in 2025, primarily driven by the transportation sector's push for lightweight vehicles. With stringent emission regulations and EV adoption, high-strength, lightweight aluminum alloys often processed via high-pressure die casting are replacing heavier metals to improve fuel efficiency. Smart cities and modernization trends are elevating the demand for durable, corrosion-resistant aluminum castings in infrastructure.

The others segment held 6% market share in 2025. The other segment includes copper-based alloys, magnesium alloys, zinc alloys, and nickel-based alloys. The growth in the copper-based alloys segment is primarily increased by the accelerating global transition toward electrification, with rising demand in renewable energy, electric vehicle (EV) production, & power transmission infrastructure. The magnesium alloys segment is experiencing significant growth in the metal casting market, primarily driven by the automotive and aerospace industries. The zinc alloys segment is growing rapidly, driven by the shift toward electric vehicles (EVs), the need for lightweight yet highly durable structural components, and advancements in high-pressure die casting. The nickel-based alloys segment is a major growth engine in the metal casting market.

Metal Casting Market Share, By Material, 2025 (%)

| By Material | Revenue Share, 2025 (%) |

| Iron | 42% |

| Steel | 31% |

| Aluminum | 21% |

| Others | 6% |

Application Insights

The automotive segment dominated the market with 46% share in 2025. This robust growth is heavily fueled by the shift toward electric vehicles (EVs) and the need for stricter vehicle weight reduction. The rise in EV adoption is driving high demand for specialized, complex castings. Manufacturers require cast aluminum and magnesium for battery enclosures, electric motor housings, and structural components.

The industrial segment held 29% market share in 2025 and is expected to have the fastest growth with a CAGR of 5.6% in the forecast period. This expansion is driven by surging demand for customized, heavy-duty industrial machinery components, valves, pumps, and specialized structural parts to support rapid infrastructure and manufacturing modernization. Global development projects are fueling continuous demand for heavy-duty machinery and structural cast elements.

The building & construction segment held 17% market share in 2025. The growth of the market is driven by rapid urbanization and expanding infrastructure development, which increases the demand. This growth is largely fueled by cast iron for structural strength and aluminum for lightweight fixtures. Government initiatives and investment for the development of hypo performance and modern housing infrastructure further fuel the growth of the market.

The others segment held 8% market share in 2025. The other segment includes aerospace components, marine components, railway components, and defense components. The aerospace components segment is a major growth driver in the metal casting market, driven by the demand for lightweight components that improve fuel efficiency and strict requirements for high-strength engine and structural parts. The global marine components segment in the market is witnessing robust growth, driven by an expansion in global maritime trade and naval modernization programs. The railway components segment is indeed experiencing a massive surge in the market, driven by global investments in high-speed rail, freight corridors, and urban transit.

Metal Casting Market Share, By Application, 2025 (%)

| By Application | Revenue Share, 2025 (%) |

| Automotive | 46% |

| Industrial | 29% |

| Building & Construction | 17% |

| Others | 8% |

Regional Analysis

How did Asia Pacific dominate the Metal Casting Market in 2025?

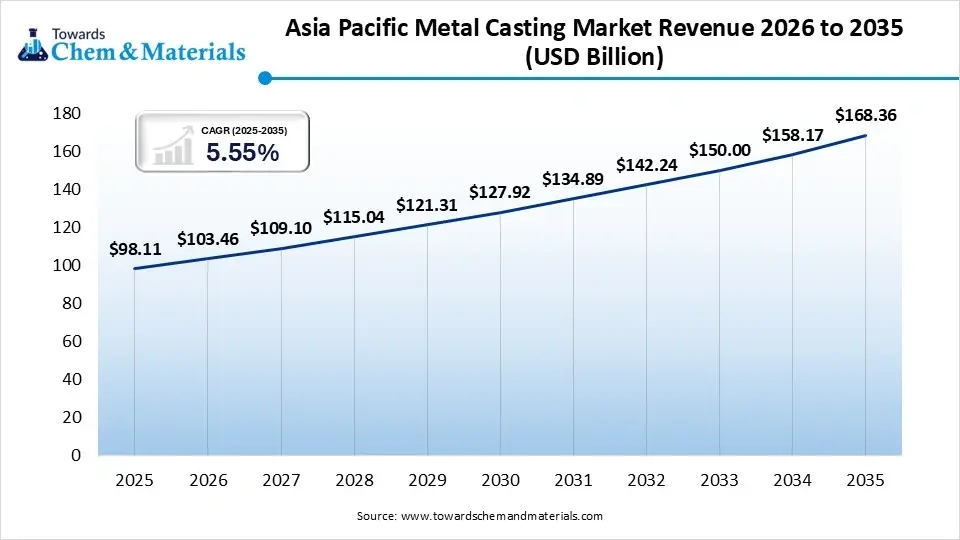

The Asia Pacific metal casting market size was estimated at USD 98.11 billion in 2025 and is projected to reach USD 168.36 billion by 2035, growing at a CAGR of 5.55% from 2026 to 2035.Asia Pacific dominated the market with a share of 53% in 2025, driven by its massive automotive manufacturing sector, rapid industrialization, and favorable government policies across major economic hubs like China, India, Japan, and South Korea. Countries like China and India served as the world's premier manufacturing bases. The region benefited significantly from the availability of cost-effective labor, abundant raw materials, and highly developed, large-scale production facilities.

India

India

- The metal casting market in India is projected to experience robust growth, driven by the automotive sector, expanding infrastructure projects, and the government's push for localized manufacturing.

- Backed by initiatives like the PM Gati Shakti plan and Smart Cities missions, there is high demand for heavy-duty iron and steel castings used in construction equipment, water distribution, and transportation systems.

- India is emerging as a global hub for metal casting. Government pushes for self-reliance has encouraged domestic production and export.

China

- The China metal casting market is experiencing steady expansion, driven primarily by domestic electric vehicle (EV) production, high-precision manufacturing, and infrastructure modernization.

- Domestic steel and metal consumption in China is shifting, with the manufacturing and industrial sectors now consuming a larger share of metal output than the historically dominant construction sector.

- The push for lighter, recyclable materials by both local OEMs and international automakers is a major catalyst that fuels the growth.

Japan

- Japan's metal casting market is experiencing growth driven by the automotive sector's shift toward lightweight electric and hybrid vehicles, advancements in industrial robotics, and robotics manufacturing.

- Japan’s advanced technological capabilities in robotics require precision-engineered components, pushing the sector to innovate in investment casting and die-casting processes.

- Initiatives like the "Monozukuri Innovation" program promote advanced manufacturing techniques, enhance production efficiency, and encourage sustainable practices within Japanese foundries.

North America Metal Casting Market Growth Factor

The North America metal casting market size was estimated at USD 33.32 billion in 2025 and is projected to reach USD 58.22 billion by 2035, growing at a CAGR of 5.74% from 2026 to 2035.North America held the market share of 18% in 2025 and is expected to have the fastest growth, growing with a CAGR of 6.30% in the forecast period. This expansion is primarily driven by strong demand from the automotive, aerospace, and defense sectors. Foundries are rapidly modernizing by integrating AI for quality control, robotics, and automation to offset traditionally high labor costs. Strict environmental regulations and the rising cost of energy are pushing foundries to adopt eco-friendly "green" casting methods and increase their reliance on recycled materials.

U.S.

- The U.S. metal casting market is driven heavily by automotive manufacturing, aerospace, and new infrastructure developments. The shift toward lightweighting in vehicles is boosting demand for non-ferrous materials like aluminum and magnesium.

- The EV boom continues to create massive new requirements for complex battery housings, motor parts, and chassis components.

- Increased federal spending and regional investments in renewable energy, water infrastructure, and national defense require localized, secure domestic supply chains.

Canada

- Canada's metal casting market sector is primarily fueled by lightweight aluminum casting for the automotive industry and rising investments in construction, aerospace, and clean-energy infrastructure.

- Substantial government and private investments in renewable energy and modern infrastructure are significantly boosting the demand for industrial and structural iron and steel castings.

Europe Metal Casting Market Growth Factor

The Europe metal casting market size was estimated at USD 31.47 billion in 2025 and is projected to reach USD 55.07 billion by 2035, growing at a CAGR of 5.15% from 2026 to 2035.Europe held the market share of 17% in 2025, growth is heavily driven by the automotive, aerospace, and industrial machinery sectors, which are increasingly prioritizing lightweight, custom-engineered components. European foundries are transitioning to energy-efficient electric and hydrogen furnaces to meet strict regional carbon-reduction targets and reduce environmental footprints. The shift toward electric vehicles requires lightweight aluminum and magnesium castings for battery housings and motor parts, while aerospace leaders like Airbus drive high-precision investment casting demand.

Germany

- Germany’s metal casting industry is largely driven by the automotive, aerospace, and heavy equipment sectors, shifting rapidly toward electric vehicles (EVs) and lightweight metal components.

- Germany's strong mechanical and electrical engineering base relies heavily on precision casting for specialized machine components.

- Foundries are modernizing by adopting automation, smart manufacturing, and increased use of recycled aluminum to comply with new environmental regulations.

Italy

Stricter EU COâ‚‚ emissions targets are pushing automakers across Italy to utilize lightweight cast components made from aluminum and magnesium. These are vital for EV battery housings, motor parts, and structural frames.

The HPDC process is the primary catalyst for market expansion. It allows for high-precision, thin-walled, lightweight components favored by aerospace and automotive manufacturers

France

- France has a massive footprint in aerospace, which heavily relies on specialized investment casting for highly complex engine components.

- Ongoing investments in public infrastructure and manufacturing modernization continue to generate stable demand for cast components.

Latin America Metal Casting Market Growth Factor

The Latin America metal casting market size was estimated at USD 12.96 billion in 2025 and is projected to reach USD 23.60 billion by 2035, growing at a CAGR of 6.18% from 2026 to 2035.Latin America held the market share of 6% in 2025 and is rapidly expanding due to accelerating infrastructure projects and strong automotive manufacturing. Ongoing investments in roadways, bridges, and urban infrastructure across Latin American countries are boosting the use of cast iron components for structural frameworks and drainage systems. Rising regional power generation needs and investments in rail networks are stimulating heavy engineering and casting operations.

") Brazil

Brazil

- Government incentives like the Mover program are pushing automakers to localize production and adopt high-pressure die casting (HPDC) for thin-wall aluminum parts used in electric and hybrid vehicles.

- Brazil's abundant local bauxite reserves and established scrap-recycling networks provide local foundries with cost-effective and low-carbon raw materials.

- Sustained investments in mining equipment driven by mining giant Vale in Minas Gerais and Pará, rail additions, and municipal water projects keep demand for ferrous castings high.

Argentina

- The Argentine metal casting market is expanding steadily, driven heavily by investments in the domestic automotive and manufacturing sectors.

- The automotive sector represents the largest revenue-generating application for metal casting in Argentina. The rising demand for engine blocks, chassis components, and transmission housings continues to fuel production.

Middle East and Africa Metal Casting Market Growth Factor

The Middle East and Africa metal casting market size was estimated at USD 9.26 billion in 2025 and is projected to reach USD 17.31 billion by 2035, growing at a CAGR of 6.46% from 2026 to 2035.The Middle East and Africa held the market share of 6% in 2025. Rapid industrialization, massive infrastructure investments, and a rebounding automotive sector are the primary drivers fueling this regional expansion. Mega-projects in the UAE and Saudi Arabia, such as urban development and industrial cities, are heavily boosting the demand for cast iron and structural steel components.

Metal Casting Market Share, By Regional, 2025 (%)

| Regional | Revenue Share, 2025 (%) |

| Asia-Pacific | 53% |

| North America | 18% |

| Europe | 17% |

| Latin America | 7% |

| Middle East & Africa | 5% |

Saudi Arabia

- In alignment with the Saudi Green Initiative, foundries are shifting toward eco-friendly casting technologies, advanced waste management, and energy-efficient melting processes.

- The scale-up of wind turbines, expansion of municipal water grids, and modernization of oil and gas processing infrastructure drive the demand for both ferrous and non-ferrous castings.

UAE

- Operation 300bn Launched to boost the UAE's industrial sector, this strategy has drawn over $1 billion in investments into the national metal casting industry, modernizing foundries and enhancing export capabilities.

- The UAE's strategy aims to double the industrial sector's GDP contribution, heavily incentivizing modernized foundry production and domestic casting capabilities.

Recent Developments

- In June 2025, Thyssenkrupp Steel commissioned a new continuous casting machine No. 4 (SGA 4) at its Duisburg, Germany, plant, marking a major investment in producing high-strength steel for electric vehicles and energy projects. The goal is to adapt the production processes at the Duisburg plant to make them more efficient and flexible, focusing on profitable premium products.(Source: gmk.center/en/news)

- In May 2026, at Metal China 2026, Clariant introduced the Ecosil™ LE III additive series, combining Geko™ P bentonite and high lustrous carbon to optimize foundry sand flowability and casting quality. The new, sustainable formulation reduces coal consumption and lowers BTEX emissions to support cleaner production standards. Read more about Clariant's latest innovations on their official website.(Source: www.clariant.com)

Top players in the Metal Casting Market & Their Offerings:

- Ryobi Limited: Japanese powerhouse specializing in precision aluminum die-casting for the automotive industry.

- GF Casting Solutions (Georg Fischer): Swiss manufacturer providing high-performance cast components for mobility and industrial sectors.

- Nemak: Global leader in lightweight aluminum components like engine blocks, EV parts, headquartered in Mexico.

- Endurance Technologies Limited: One of India's leading automotive component manufacturers, heavily focused on aluminum casting.

- Posco Holdings & Kobe Steel: Major Asian conglomerates heavily invested in advanced steel casting and alloy innovation.

Other Top Players Are

- Posco Holdings & Kobe Steel

- Hitachi Metals

- Rheinmetall AG

- Dynacast International

- Precision Castparts Corp. (PCC)

- Doosan Heavy Industries and Construction

- Xinxing Ductile Iron Pipes

- Amsted Rail

- Aisin Group

- Endurance Technologies

- Nucor Corporation

- ArcelorMittal

- Kobe Steel

- Alcoa Corporation

Segment Covered in the Report

By Material

- Iron

- Gray Iron Castings

- Ductile Iron Castings

- Malleable Iron Castings

- White Iron Castings

- Steel

- Carbon Steel Castings

- Alloy Steel Castings

- Stainless Steel Castings

- Aluminum

- Sand Cast Aluminum

- Die Cast Aluminum

- Permanent Mold Aluminum

- Others

- Copper-Based Alloys

- Magnesium Alloys

- Zinc Alloys

- Nickel-Based Alloys

By Application

- Automotive

- Engine Components

- Transmission Components

- Structural Components

- Wheels & Chassis Parts

- Industrial

- Machinery Components

- Pumps & Valves

- Mining Equipment

- Energy Equipment

- Building & Construction

- Structural Components

- Pipes & Fittings

- Architectural Castings

- Others

- Aerospace Components

- Marine Components

- Railway Components

- Defense Components

By Region

- North America

- U.S.

- Canada

- Mexico

- Europe

- UK

- Germany

- France

- Italy

- Spain

- Sweden

- Denmark

- Norway

- Asia Pacific

- Japan

- China

- India

- Australia

- South Korea

- Thailand

- Latin America

- Brazil

- Argentina

- The Middle East and Africa

- South Africa

- Saudi Arabia

- UAE

- Kuwait

FAQ's

Select User License to Buy

Figures (6)