Content

What is the Ductile Iron Pipes Market Size and Share?

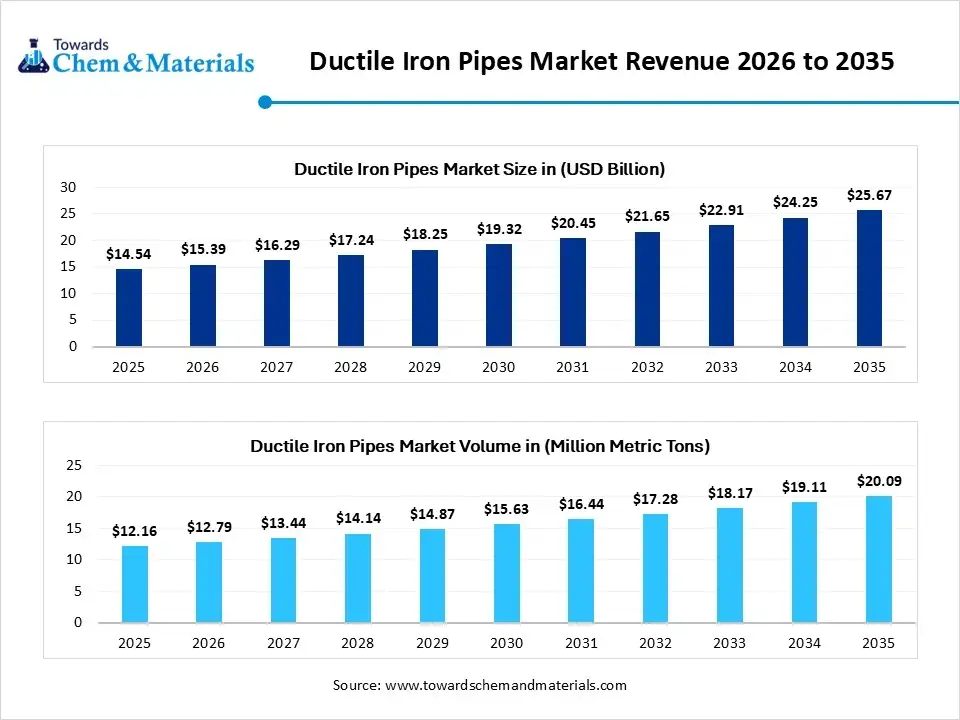

The ductile iron pipes market size was valued at USD 14.54 billion in 2025, is estimated to reach USD 15.39 billion in 2026, and is projected to reach USD 25.67 billion by 2035, exhibiting a compound annual growth rate (CAGR) of 5.85% over the forecast period from 2026 to 2035.Asia Pacific dominated the ductile iron pipes market with the largest revenue share of xx% in 2025 and is expected to grow at the fastest CAGR of 5.96% during the forecast period. In terms of volume, the ductile iron pipes market is projected to grow from 12.16 million metric tons in 2025 to 20.09 million tons by 2035 growing at a CAGR of 5.15% from 2026 to 2035. The growth of the market is attributed to the high investments in water infrastructure, the growing urbanization, the demand for durable pipeline solutions, and the growing wastewater management projects. New coatings, precision centrifugal casting, and trenchless installation technologies are also being developed for pipelines, helping to enhance pipeline performance and ensure long-term market growth.

Market Highlights

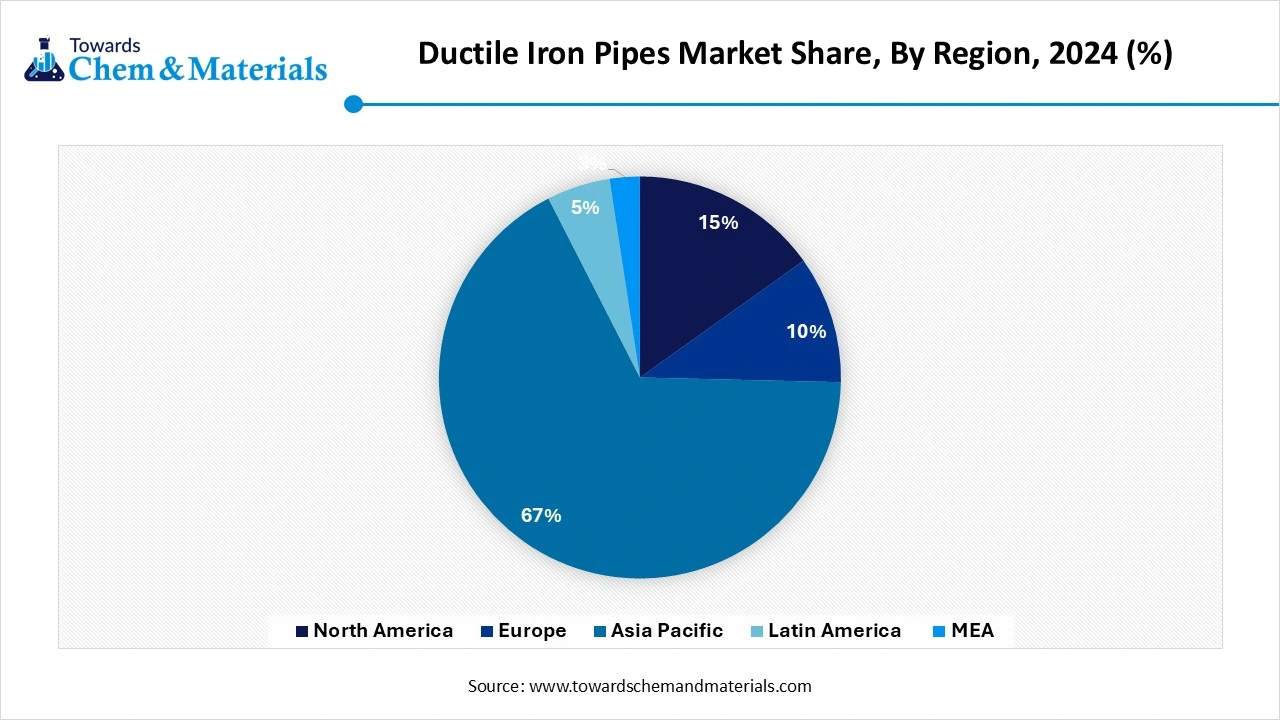

- By region, Asia Pacific dominated the ductile iron pipes market by holding 48% share in 2025, as large infrastructure spending supports new pipeline networks.

- By region, North America held 17% market share in 2025 and is expected to grow at the fastest with a CAGR of 6.8% during the forecast period, as water infrastructure rehabilitation remains a national priority.

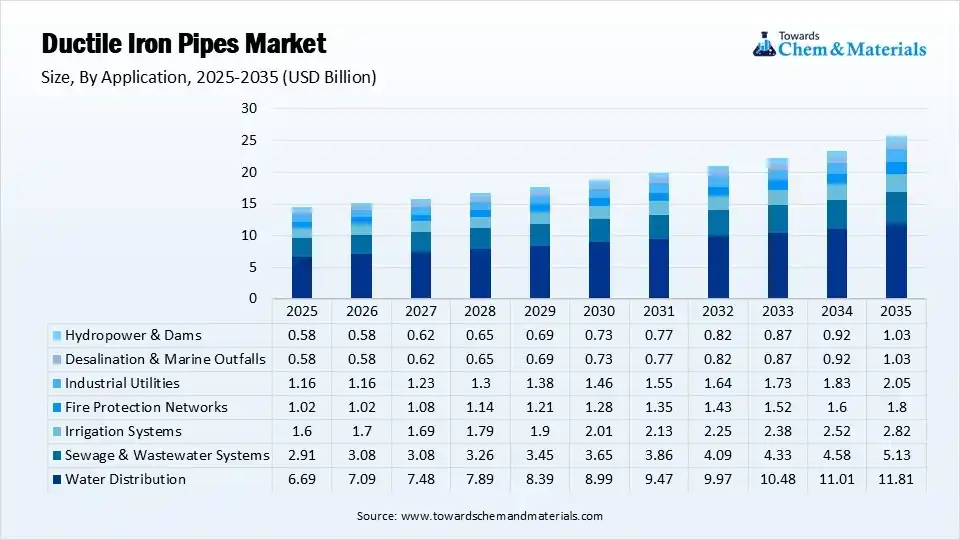

- By application, the water distribution segment dominated the market with the largest share of 46% in 2025, as utilities replace aging pipelines with durable ductile iron systems.

- By application, the desalination & marine outfalls segment held 4.0% market share in 2025 and is expected to grow at the fastest CAGR of 7.0% over the forecast period, driven by government investments stimulating deployment.

Ongoing Technological Innovations Expanding Market Growth

Ductile Iron Pipes are centrifugally cast-iron pipes manufactured using ductile cast iron, a type of iron known for its high strength, elasticity, and impact resistance. These pipes are extensively used in water and wastewater transportation systems due to their durability, corrosion resistance (often enhanced by linings/coatings), and long service life. Ductile iron offers better performance compared to traditional gray cast iron due to its nodular graphite inclusions. There is an increasing focus on eco-friendly water management practices; hence, these iron pipes are preferred for their long service life and durability, which makes them a crucial choice among manufacturers.

Market Overview

The market is growing due to rising investments in drinking water distribution, wastewater management, and the modernization of urban infrastructure in developed and emerging economies. Demand for pipeline systems that are high-strength, pressure-resistant, and government-supported is still growing, as is the use of water in industry.

The market is also expanding as a result of the availability of new opportunities for smart water grids, trenchless pipeline rehabilitation, and desalination infrastructure. Polyurethane, epoxy, ceramic, and cement mortar coatings, precision centrifugal casting technology, and joint technologies are being developed to further improve corrosion resistance, installation speed, and pipeline service life.

- For instance, Evonith Steel announced plans to expand its manufacturing capacity and diversify into ductile iron pipes. It is the company's intention to leverage the escalating demand from water infrastructure projects supported by the government by integrating its manufacturing, sustainable operations, logistics, and value-added steel production.(Source: tubepipeindia.com)

Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 17.66 Billion |

| Market Size by 2034 | USD 32.77 Billion |

| Growth rate from 2024 to 2025 | CAGR 7.11% |

| Base Year of Estimation | 2024 |

| Forecast Period | 2025 - 2034 |

| Dominant Region | Asia Pacific |

| Segment Covered | By Diameter, By Application, By Installation Technique, By Lining Type, By Coating Type, By End-Use Sector, By Pressure Rating, By Sales Channel, By Region |

| Key Profiled Companies | Saint-Gobain PAM (France), Jindal SAW Ltd. (India), Kubota Corporation (Japan), American Cast Iron Pipe Company (USA), U.S. Pipe (USA), Electrosteel Castings Ltd. (India), McWane Inc. (USA), Tata Metaliks (India), Benxi Beiying Iron and Steel (China), Xinxing Ductile Iron Pipes Co., Ltd. (China), AMSTED Industries (USA), Svobodny Sokol (Russia), Angang Group Yongtong Ductile Cast Iron Pipe Co., Ltd. (China), Duktus Rohrsysteme Wetzlar GmbH (Germany), Atlantic States Cast Iron Pipe Company (USA), Zhejiang Weifeng Pipe Industry Co., Ltd. (China), Shanxi Ductile Iron Pipes Co., Ltd. (China), Saint-Gobain PAM España (Spain), United Gulf Pipe Manufacturing Co. (Oman), Binhai New Area Tianjin Pipe Co. Ltd. (China) |

Market Opportunity

Stringent Government Standards

Regulatory bodies globally are mandating the use of nontoxic, safe, and anti-corrosion materials to ensure good water quality for public health. Their ability to bear high external loads and internal pressures enables them to comply with the strict performance standards fixed for industrial and municipal water systems. Furthermore, this regulatory environment propels the demand for long-lasting and long-lasting pipe materials in retrofitted water networks, creating future opportunities in the market.

- In January 2025, Rungta Steel announced its expansion into the manufacturing of Ductile Iron (DI) Pipes. The launches of Ductile Iron Pipes complement the firm's flagship product, TMT Bars, with Fly Ash Bricks and Wire Rods.(Source: www.ptinews.com)

Market Challenge

Competition from Substitute Materials

Substitutes such as HDPE, PVC, and steel are the major alternatives to the ductile iron pipes in the market. These materials offer crucial benefits such as lower installation costs and corrosion resistance, hindering market growth further. Moreover, poor port and road infrastructure can delay the supply of raw materials and hence the distribution of end products, affecting the market expansion negatively.

Supply Chain Analysis of the Ductile Iron Pipes Market

Feedstock Procurement:

- The materials used are sourced pig iron, scrap steel, metallurgical coke, limestone, and alloying materials to produce ductile iron pipe with excellent strength, durability, and corrosion resistance for water and industrial pipeline applications.

- Tata Metaliks Limited: Procures high-quality iron ore and Metallurgical Coking Coal, which are used to produce high quality Hot metal.

- Other key players: Jindal SAW, Electrosteel Castings, Rashmi Metaliks.

Chemical Synthesis and Processing

- High temperature furnaces are used to melt the raw materials and then convert them into spheroidal graphite iron with a higher mechanical strength and pressure bearing capacity by removing sulfur and adding magnesium during the smelting process.

- Electrosteel Castings Limited: Uses state-of-the-art cupola furnace and induction furnace technologies to melt and re-refine iron to ensure a higher quality metallurgy for high-quality ductile iron pipes.

- Other key players: Kubota Corporation, U.S. Pipe, and Xinxing Ductile Iron Pipes.

Compound Formulation and Blending:

- Ductile iron is melted and cast centrifugally, then annealed, machined, zinc-coated, bitumen finished, and cement mortar lined to produce high-quality pipelines for municipal, industrial, and wastewater systems.

- Jindal SAW Limited: Advanced centrifugal casting, annealing, and protection coating technology results in ultra-durable and corrosion-resistant ductile iron pipes.

- Other Key Players: Saint-Gobain PAM Canalisation, AMERICAN Cast Iron Pipe Company.

Segmental Insight

Application Insights

The water distribution segment holds a significant share of the ductile iron pipes market, supported by the growing global emphasis on providing safe and dependable drinking water. Governments and local authorities, particularly in developing economies, are investing heavily in expanding and upgrading water supply infrastructure to meet rising demand in urban and semi-urban areas. Ductile iron pipes are widely used in these projects because they offer excellent strength, a long operational lifespan, and the ability to withstand high internal pressure as well as external loads, making them a reliable choice for water transmission and distribution networks.

") The sewage & wastewater systems segment is expected to witness the fastest growth during the forecast period. Rapid urbanization and increasing wastewater generation are driving the need for modern sewer networks that can efficiently transport large volumes of wastewater while minimizing leaks and failures. Ductile iron pipes are well suited for these systems due to their high mechanical strength, corrosion resistance, and ability to perform under challenging ground conditions and varying pressure levels. Their long service life and low maintenance requirements make them an ideal solution for both gravity-fed and pressurized wastewater infrastructure, particularly in densely populated urban areas.

The sewage & wastewater systems segment is expected to witness the fastest growth during the forecast period. Rapid urbanization and increasing wastewater generation are driving the need for modern sewer networks that can efficiently transport large volumes of wastewater while minimizing leaks and failures. Ductile iron pipes are well suited for these systems due to their high mechanical strength, corrosion resistance, and ability to perform under challenging ground conditions and varying pressure levels. Their long service life and low maintenance requirements make them an ideal solution for both gravity-fed and pressurized wastewater infrastructure, particularly in densely populated urban areas.

Regional Insights

How did the Asia Pacific Dominate the ductile iron pipes market in 2025?

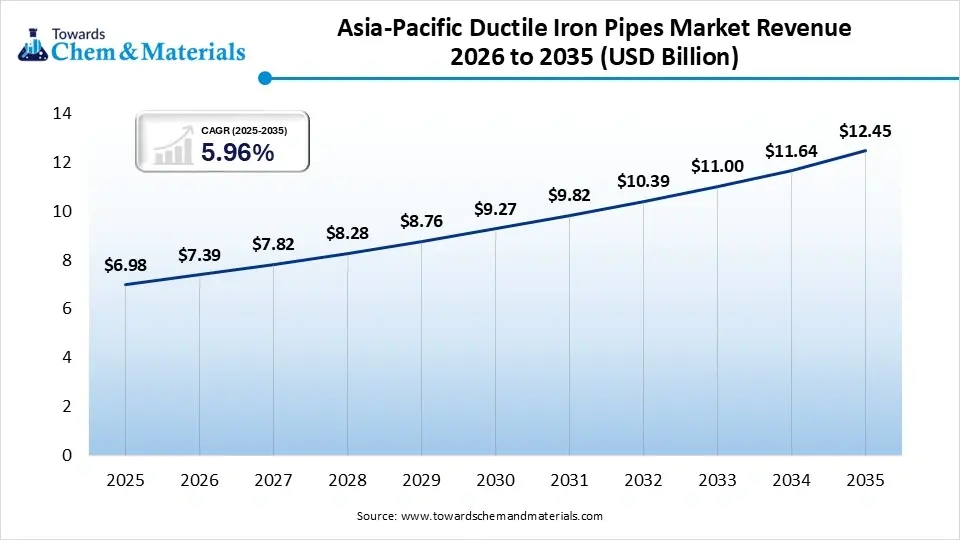

The Asia Pacific ductile iron pipes market size was estimated at USD 6.98 billion in 2025 and is projected to reach USD 12.45 billion by 2035, growing at a CAGR of 5.96% from 2026 to 2035.Asia Pacific dominated the market with the largest share of 48% in 2025, due to the presence of a rapidly developing urban population, growing water infrastructure and rising government investments in drinking water and sanitation projects. As more industries develop and irrigation continues to grow, pipelines continue to be installed throughout the region. Further, the increased use of durable water transmission systems further bolsters the long-term growth of the market.

") China

China

- Demand for ductile iron pipes is still high within municipal water distribution networks, continuing to be supported by the demand for large-scale urban infrastructure projects.

- As wastewater treatment and industrial development grows, the number of pipeline systems in use using corrosion-resistant materials expands across major provinces.

- A Smart City investment in infrastructure promotes the use of advanced ductile iron pipeline technologies that deliver enhanced operational capabilities.

India

- Ductile iron pipeline projects are being rapidly deployed in government water supply schemes in both rural and urban programs.

- Long-term demand for durable pipeline networks across the country is being met by rapid urbanization and growing wastewater treatment plants.

- The use of high-strength ductile iron pipe systems is growing as a result of more industrial, mining and irrigation activities.

North America held 17% market share in 2025 and is expected to grow at the fastest CAGR of 6.8% during the forecast period, because of aging water infrastructure, the rising investment in water infrastructure rehabilitation, and modernization of municipal pipeline networks. Utilities have a preference for the use of pipeline systems that will last a long time and have a minimal risk of corrosion affecting the water distribution system. Other attractive aspects of the region are technological developments that facilitate regional market expansion.

United States

- Replacing ageing municipal pipeline infrastructure remains a driver for replacing these pipes with durable ductile iron water transmission and distribution systems.

- The Federal government provides funding for infrastructure modernization of drinking water and wastewater pipeline systems in a number of states.

- More and more, utilities use coated pipes that are more corrosion resistant to ensure service reliability and to lower maintenance needs.

Canada

- Demand for high performance ductile iron pipelines in urban communities continues to be supported by municipal infrastructure upgrades.

- Durable pipelines for water transmission are adopted under harsh climatic conditions for long service life.

- Sustainable Water Management investments further reinforce the sustainability of long-term investments in corrosion resistant ductile iron products.

Europe held 20% market share in 2025, as it invests in improving water facilities, introducing environmental sustainability measures and upgrading the ageing pipeline network. Regulatory requirements promote the use of pipes that are durable and recyclable such as ductile iron pipes. Pipeline quality and quality of operations are still being enhanced by technological innovation.

Germany

- The demand for advanced ductile iron transmission and distribution pipeline systems has continued to grow in the water sector, which is undergoing modernization infrastructure programs.

- The wide range of high strength pressure pipe applications are supported by a strong industrial manufacturing sector.

- Long-life corrosion-resistant ductile iron technologies are promoted by sustainable infrastructure investments.

France

- Pipelines that are being replaced by durable ductile iron are continuing because of the upgrades to municipal water distribution systems.

- Environmental sustainability programs help promote use of the most recycled and durable pipeline materials.

- The expansion of wastewater treatment reinforces installations of corrosion resistant ductile iron pipe throughout the country.

Latin America held 6% market share in 2025, because growth in the sanitation program, water distribution program, and industrial development has increased the demand for ductile iron pipes. Water supply networks are maintained by government investment for market expansion. Pipeline demand for the mining and energy industries also drives demand in the region.

Brazil

- Demand for durable ductile iron transmission and distribution pipeline systems remains strong, as water infrastructure modernization projects continue.

- There is a growing demand for heavy duty pressure pipeline solutions in the expanded industrial and energy markets.

- Government sanitation efforts increase the replacement of old municipal water systems in big cities.

Chile

- High strength ductile iron, water transportation pipeline systems are still in demand for mining industry operations.

- Growing municipal water infrastructure drives growth in pressure pipe solutions that are resistant to corrosion.

- Reliable water distribution and wastewater management systems also benefit from increased investments through industrial development.

The Middle East & Africa held 9% market share in 2025, as more and more investments are made in water transmission projects, urban development, and desalination infrastructure. Increasing industrial development and water security projects enable pipeline installation. For long life of infrastructure, durable corrosion resistant pipe systems are still required.

Saudi Arabia

- Demand for ductile iron pipeline installations continues to remain high on large scale desalination and water transmission projects throughout the country.

- Government infrastructure diversification projects boost the implementation of modern water distribution networks in cities.

- Continued investments in sustainable water management enable long-term use of pipeline technologies that are resistant to corrosion.

South Africa

- Demand for ductile iron water transportation pipeline systems continues to grow due to mining and industrial activities.

- Rehabilitation projects for municipal water infrastructure enable the replacement of aging water pipe infrastructure in urban areas.

- The use of high-performance ductile iron pipe technologies is further increased through government investments in water security.

Recent Developments

- In January 2025, Rungta Steel started its business operations in manufacturing ductile iron pipes at its Jharkhand's Chaibasa facility, apart from the TMT bars and wire rods. The initiative is a response to the growth of demand for durable pipeline solutions in the water infrastructure and utility sector in India. (Source:economictimes.indiatimes.com)

Top Companies List

- Saint-Gobain PAM (France)

- Jindal SAW Ltd. (India)

- Kubota Corporation (Japan)

- American Cast Iron Pipe Company (USA)

- U.S. Pipe (USA)

- Electrosteel Castings Ltd. (India)

- McWane Inc. (USA)

- Tata Metaliks (India)

- Benxi Beiying Iron and Steel (China)

- Xinxing Ductile Iron Pipes Co., Ltd. (China)

- AMSTED Industries (USA)

- Svobodny Sokol (Russia)

- Angang Group Yongtong Ductile Cast Iron Pipe Co., Ltd. (China)

- Duktus Rohrsysteme Wetzlar GmbH (Germany)

- Atlantic States Cast Iron Pipe Company (USA)

- Zhejiang Weifeng Pipe Industry Co., Ltd. (China)

- Shanxi Ductile Iron Pipes Co., Ltd. (China)

- Saint-Gobain PAM España (Spain)

- United Gulf Pipe Manufacturing Co. (Oman)

- Binhai New Area Tianjin Pipe Co. Ltd. (China)

Segments Covered

By Application

- Water Distribution

- Sewage & Wastewater Systems

- Irrigation Systems

- Fire Protection Networks

- Industrial Utilities

- Desalination & Marine Outfalls

- Hydropower & Dams

By Region

- North America

- U.S.

- Canada

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Sweden

- Denmark

- Norway

- Asia Pacific

- China

- Japan

- India

- South Korea

- Thailand

- Latin America

- Brazil

- Mexico

- Argentina

- Middle East and Africa (MEA)

- South Africa

- UAE

- Saudi Arabia

- Kuwait

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

Select User License to Buy

Figures (5)