Content

What is the Hydrazine Hydrate Market Size and Share?

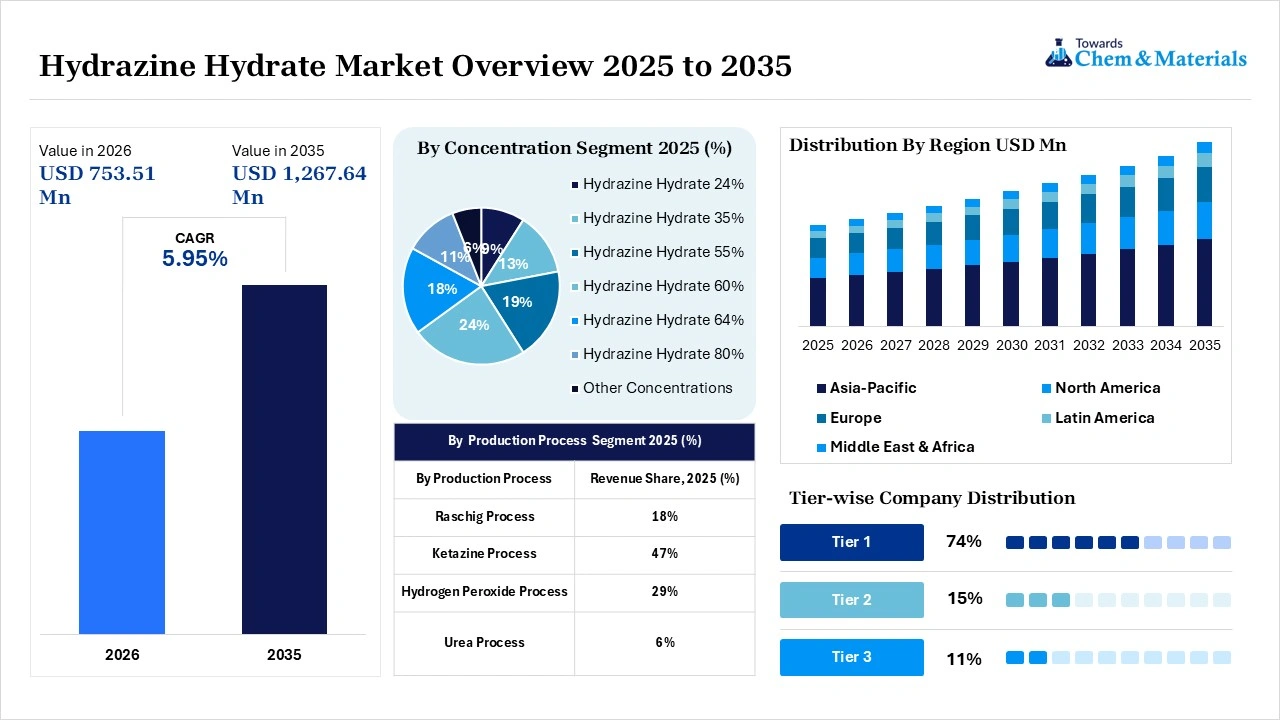

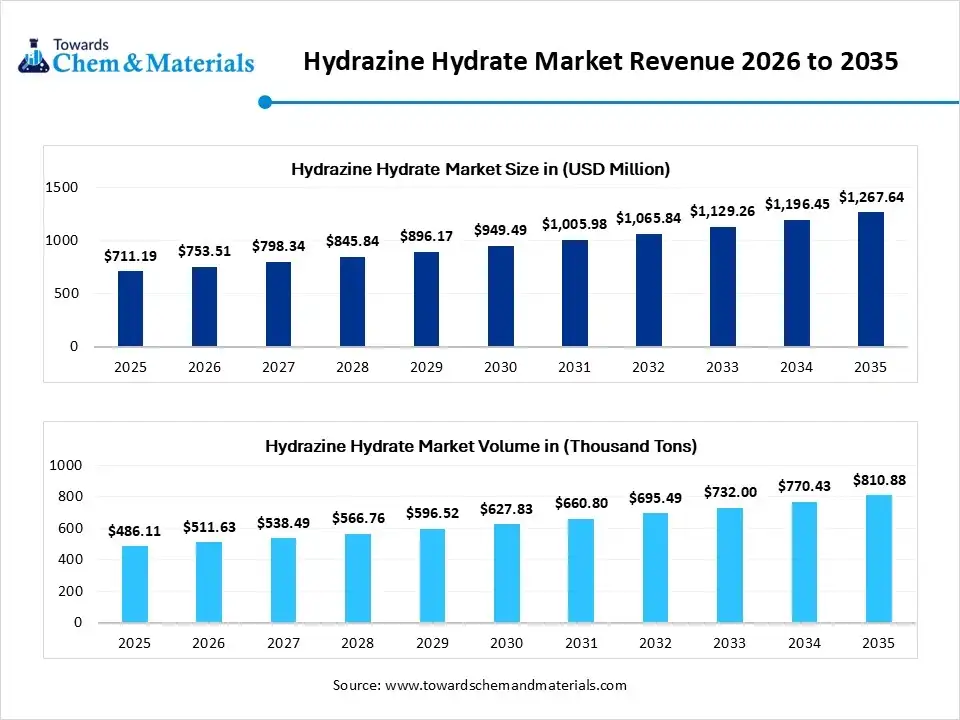

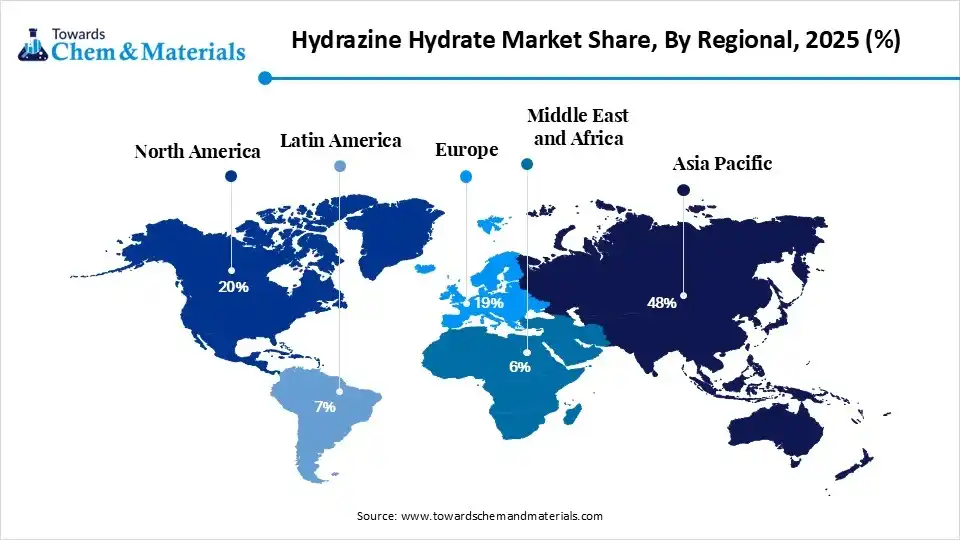

The hydrazine hydrate market size was valued at USD 711.19 million in 2025, is estimated to reach USD 753.51 million in 2026, and is projected to reach USD 1,267.64 million by 2035, exhibiting a compound annual growth rate (CAGR) of 5.95% over the forecast period from 2026 to 2035.Asia Pacific dominated the hydrazine hydrate market with the largest revenue share of 48% in 2025 and is expected to grow at the fastest CAGR of 6.06% during the forecast period. In terms of volume, the hydrazine hydrate market is projected to grow from 486.11 thousand tons in 2025 to 810.88 thousand tons by 2035. growing at a CAGR of 5.25% from 2026 to 2035. With the heavy shift from traditional chemicals to the advanced intermediates, the world has been providing greater attention to the hydrazine hydrate industry. Also, the need for specialty and personalized chemical emergence is likely to create profitable pathways for the industry in the upcoming advanced industrialization.

Market Highlights

- By region, Asia Pacific dominated the market with a share of 48% in 2025, due to the region having become the world's largest center for chemical manufacturing, industrial production, and specialty material processing.

- By region, North America is held the 20% market share in 2025 and is expected to be the fastest-growing region in the market, with a CAGR of 6.40% in the forecast period, owing to the region's investment in advanced manufacturing, aerospace innovation, defense modernization, and specialty chemical production.

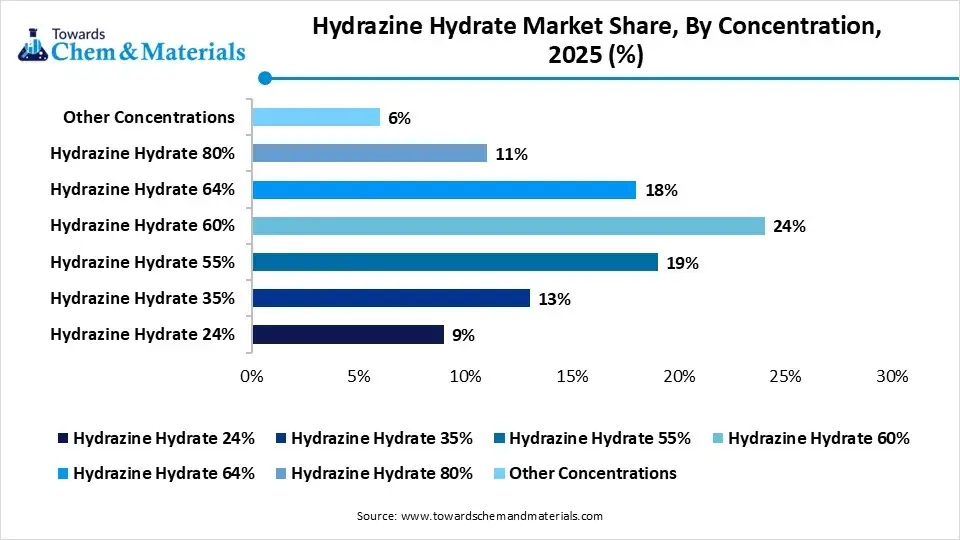

- By concentration, the hydrazine hydrate 60% segment dominated the market with 24% share in 2025, akin to it having become the industry's working concentration.

- By concentration, the hydrazine hydrate 80% segment held the 11% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 6.8% in the forecast period, owing to industries being increasingly focused on chemical efficiency rather than volume consumption.

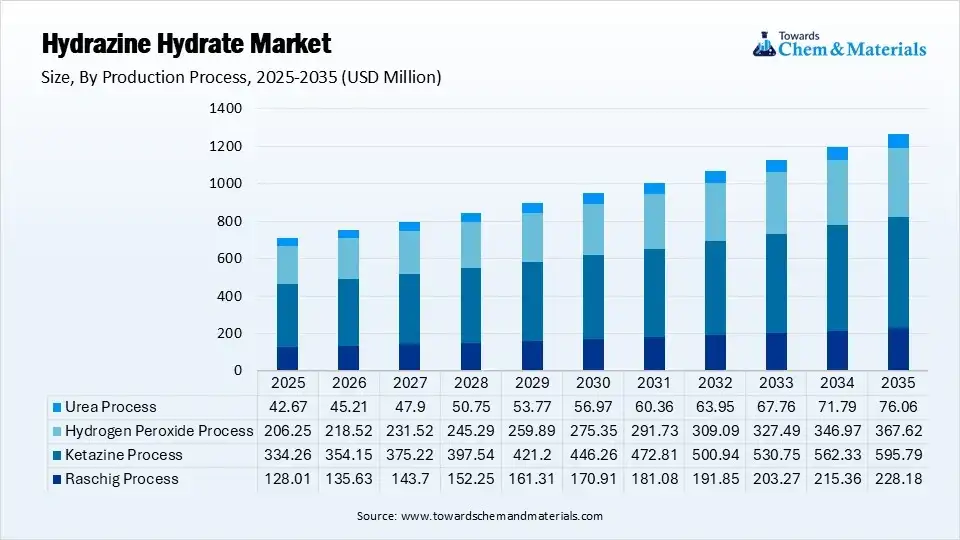

- By production process, the ketazine process segment dominated the market with 47% share in 2025, akin to it helped producers achieve something highly valued in the chemical industry with predictable production.

- By production process, the hydrogen peroxide process segment held the 29% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 7.1% in the forecast period, owing to chemical companies are increasingly measuring production success through environmental efficiency.

- By application, the polymerization & blowing agents segment dominated the market with 34% share in 2025, akin to it is directly connected to the global lightweight materials economy.

- By application, the aerospace & defense segment held the 4% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 7.8% in the forecast period, owing to hydrazine-based systems that remain difficult to replace in several mission-critical applications.

- By end-use industry, the chemical industry segment dominated the market with 46% share in 2025, akin to hydrazine hydrate, which functions as a chemical building block rather than a final product.

- By end-use industry, the aerospace & defence industry segment held the 5% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 7.9% in the forecast period, owing to the sector prioritizing performance reliability over material cost.

- By grade, the industrial grade segment dominated the market with 68% share in 2025, akin to most hydrazine hydrate consumption occurring in applications where functional performance is more important than ultra-high purity.

- By grade, the high-purity grade segment held the 14% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 7.4% in the forecast period, owing to manufacturing industries entering an era where contamination control is becoming a competitive advantage

- By distribution channel, the direct sales segment dominated the market with 61% share in 2025, akin to hydrazine hydrate, purchasing decisions are often based on trust, compliance, and technical support rather than price alone.

- By distribution channel, the online chemical platforms segment held the 7% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 7.3% in the forecast period, owing to the chemical industry gradually adopting digital procurement strategies like those already used in manufacturing and retail sectors.

Quick Stats at a Glance

- Market Estimated Size (2025): USD 711.19 Million | CAGR (2026–2035): 5.95%

- Market Projected Size (2035): USD 1,267.64 Million

- Asia Pacific: Revenue Share of 48% in 2025|USD 341.37 Million

- Market Estimated Volume (2025): 486.11 Thousand Tons | Volume CAGR (2026–2035): 5.25%

- Market Projected Volume (2035): 810.88 Thousand Tons

- Market Pricing (2025):

- Average Manufacturing Price (2025): USD 1,330/Ton

- Average Selling Price (2025): USD 1,860/Ton

- Pricing CAGR (2026–2035): 2.45%

Quality Focused Industries Increase Consumption

The global push for the improvement of the product quality, efficiency, and environmental performance has been observed from the major industries where water treatment has emerged as a large application area for the hydrazine hydrate industry. Furthermore, the need for innovative chemical productions across major regions such as Europe, North America, and the Asia Pacific has created significant industry opportunities for the hydrazine hydrate market, as per the recent survey. Globe has been demanding hydrazine-based specialty formulas and intermediates in recent years.

- For instance, in March 2026, LANXESS introduced the innovative hydrazine-based oxygen scavenger for the water systems of industry. Also, the newly launched brand called LEVOXIN®, as per the published report.(Source: lanxess.com)

In recent years, manufacturers have increasingly invested in production optimization, safety improvements, and emission-control technologies to comply with stricter environmental regulations. The market is also witnessing a gradual shift toward higher-purity hydrazine hydrate grades for pharmaceutical, electronics, and specialty chemical applications.

Moreover, rising investments in renewable energy infrastructure, industrial steam generation systems, and advanced manufacturing facilities are creating additional opportunities for hydrazine hydrate suppliers.

Global Investment Flow for Hydrazine Hydrate 2026

- Chemical manufacturers are investing in production capacity expansion to meet growing demand from water treatment, agrochemical, and specialty chemical industries in the current period.

- Companies are shifting toward automated production lines and environmental compliance technologies to improve operational efficiency and regulatory performance.

- Investment is increasingly flowing into regional manufacturing hubs across Asia-Pacific and the Middle East to strengthen local supply chains, reduce import dependence, and support expanding industrial activities as per recent regional survey.

Recent Market Trends

- The heavy shift for the higher purity hydrazine hydrate grades has resulted in high yield outcomes for the industrial players in recent years. Furthermore, specialty chemical producers and pharmaceutical manufacturers have been observed to be in greater need.

- The emergence of smart manufacturing technologies has attracted increased capital and investment in manufacturing. The hydrazine hydrate producers are actively using smarter monitoring systems and automated control platforms nowadays.

- The growing concerns of industrial water sustainability are likely to act as a high-margin opportunity during the forecast period. Also, hydrazine hydrate has been seen in reducing equipment corrosion, improving energy efficiency, while extending boiler life, as per the industry experts.

Report Scope

| Report Attributes | Details |

| Market Size and Volume in 2026 | USD 753.51 Million / 511.63 Thousand Tons |

| Revenue Forecast in 2035 | USD 1,267.64 Million / 810.88 Thousand Tons |

| Growth Rate | CAGR 5.95% |

| Base Year of Estimation | 2025 |

| Forecast Period | 2025 - 2035 |

| High Impact Region | Asia Pacific |

| Segment Covered | By Concentration, By Production Process, By Application, By End-Use Industry, By Grade, By Distribution Channel |

| Key Companies Profiled | Arkema S.A., LANXESS AG, Lonza Group AG, Otsuka Chemical Co., Ltd., Yibin Tianyuan Group Co., Ltd., Chongqing Chuandong Chemical (Group) Co., Ltd., Hunan Zhongchuang Chemical Co., Ltd., Weifang Yaxing Chemical Co., Ltd., Nippon Carbide Industries Co., Inc., Gujarat Alkalies and Chemicals Limited (GACL) |

Digital Innovation Enhances Production Efficiency

The industry is observing a transition from conventional production systems to digitally managed, low-emission manufacturing processes. Also, in recent years, producers have begun implementing advanced process control systems, automated safety monitoring, energy-efficient reactors, and real-time quality tracking technologies. These innovations help improve production consistency while reducing waste generation and operational costs.

Supply Chain Analysis of Hydrazine Hydrate Market

- Production & Processing:Manufacturers create hydrazine hydrate by oxidizing ammonia or urea with sodium hypochlorite or hydrogen peroxide through multi-step chemical reactions. The resulting mixture undergoes complex heat-regulated distillation to concentrate the liquid.

- This highly reactive fluid is strictly processed using enclosed, automated equipment to prevent hazardous toxic exposure.

- Key players: Arkema S.A., LANXESS AG, and Lonza Group AG

- Quality Testing and Certification:Quality testing of hydrazine hydrate relies on precise chemical titrations to verify purity percentages and track strict impurity thresholds. Because this chemical is highly volatile and hazardous, batches require official Certificates of Analysis (CoA).

Compliance standards ensure airtight containment, stable shelf life, and flawless quality for critical propellant and water-treatment applications.- Key players: Arkema S.A., LANXESS AG, and Lonza Group AG

- Distribution to Industrial Users:Distributing hydrazine hydrate requires specialized transport infrastructure like stainless steel tankers and nitrogen-blanketed drums to prevent hazardous air contact.

- Chemical suppliers ship these bulk orders directly to industrial complexes using strict tracking protocols. Heavy manufacturers then consume the chemical for corrosion control in power plants, pharmaceuticals, and agricultural manufacturing.

- Key players: Arkema S.A., LANXESS AG, Lonza Group AG, and Otsuka Chemical Co., Ltd

Hydrazine Hydrate Market Dynamics

Driver

Advanced Chemical Intermediates Create Value

The growing need for high-performance chemical intermediates across multiple industries has increased return on investment for manufacturers. In the current period, manufacturers are focusing on producing advanced polymers, specialty chemicals, pharmaceutical ingredients, and industrial treatment solutions that require reliable chemical building blocks. Hydrazine hydrate plays a crucial role in these value chains because it supports the production of several downstream products with high commercial value.

Restraint

Stricter Regulations Increase Operational Burdens

The rising complexity of chemical compliance requirements is expected to hinder the industry's growth during the projected time. In recent years, industries have faced stricter regulations related to hazardous material management, workplace safety, transportation procedures, and environmental reporting. These requirements increase operational costs throughout the supply chain, from production facilities to end users.

Opportunity

Advanced Industries Fuel Chemical Demand

The emergence of advanced technology industries that require specialized chemical materials is expected to support stronger cash flows for manufacturing enterprises in the coming years. In the current period, sectors such as aerospace, semiconductor manufacturing, energy storage, advanced composites, and precision engineering are expanding rapidly across global markets. These industries increasingly demand high-purity chemical inputs capable of supporting sophisticated production processes.

Segmental Insights

Concentration Insights

The hydrazine hydrate 60% segment dominated the market with 24% share in 2025, akin to it has become the industry's working concentration. Many factories purchase hydrazine hydrate not for maximum strength but for operational flexibility. In the current period, 60% concentration allows easier dilution, safer storage, lower insurance costs, and simpler transportation compared with highly concentrated grades.

") The hydrazine hydrate 80% segment held the 11% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 6.8% in the forecast period, owing to industries being increasingly focused on chemical efficiency rather than volume consumption. Higher concentrations reduce transportation frequency, storage requirements, packaging materials, and logistics expenses. Furthermore, advanced industries such as aerospace, specialty chemicals, and high-performance materials prefer concentrated feedstocks to improve process precision.

The hydrazine hydrate 80% segment held the 11% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 6.8% in the forecast period, owing to industries being increasingly focused on chemical efficiency rather than volume consumption. Higher concentrations reduce transportation frequency, storage requirements, packaging materials, and logistics expenses. Furthermore, advanced industries such as aerospace, specialty chemicals, and high-performance materials prefer concentrated feedstocks to improve process precision.

Hydrazine Hydrate Market Share,By Concentration, 2025 (%)

| By Concentration | Revenue Share, 2025 (%) |

| Hydrazine Hydrate 24% | 9% |

| Hydrazine Hydrate 35% | 13% |

| Hydrazine Hydrate 55% | 19% |

| Hydrazine Hydrate 60% | 24% |

| Hydrazine Hydrate 64% | 18% |

| Hydrazine Hydrate 80% | 11% |

| Other Concentrations | 6% |

Production Process Insights

The ketazine process segment dominated the market with 47% share in 2025, akin to it helped producers achieve something highly valued in the chemical industry with the predictable production. In the current period, manufacturers prefer production routes that offer stable yields, established operating procedures, and decades of industrial experience. The ketazine process benefits from extensive technical knowledge accumulated over many years.

") The hydrogen peroxide process segment held the 29% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 7.1% in the forecast period, owing to chemical companies increasingly measuring production success through environmental efficiency. Unlike older manufacturing routes, this process aligns more closely with future sustainability targets and cleaner production objectives. Furthermore, investors and industrial customers are placing greater emphasis on carbon reduction and responsible manufacturing practices.

The hydrogen peroxide process segment held the 29% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 7.1% in the forecast period, owing to chemical companies increasingly measuring production success through environmental efficiency. Unlike older manufacturing routes, this process aligns more closely with future sustainability targets and cleaner production objectives. Furthermore, investors and industrial customers are placing greater emphasis on carbon reduction and responsible manufacturing practices.

Hydrazine Hydrate Market Share, By Production Process, 2025 (%)

| By Production Process | Revenue Share, 2025 (%) |

| Raschig Process | 18% |

| Ketazine Process | 47% |

| Hydrogen Peroxide Process | 29% |

| Urea Process | 6% |

Application Insights

The polymerization & blowing agents segment dominated the market with 34% share in 2025, akin to it is directly connected to the global lightweight materials economy. In the current period, manufacturers are under pressure to reduce product weight without sacrificing strength, particularly in packaging, construction panels, consumer goods, and transportation components. Hydrazine hydrate serves as a critical feedstock for blowing agent production that creates microscopic air structures inside materials, reducing material consumption while maintaining performance.

The aerospace & defense segment held the 4% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 7.8% in the forecast period, owing to hydrazine-based systems remain difficult to replace in several mission-critical applications. In recent years, governments have shifted their focus from traditional defence spending toward satellite networks, space security programs, unmanned systems, and advanced propulsion technologies. These programs require highly specialized chemicals capable of delivering reliable performance under extreme conditions.

Hydrazine Hydrate Market Share,By Application, 2025 (%)

| By Application | Revenue Share, 2025 (%) |

| Polymerization & Blowing Agents | 34% |

| Water Treatment | 21% |

| Agrochemicals | 16% |

| Pharmaceuticals | 8% |

| Chemical Intermediates | 12% |

| Aerospace & Defense | 4% |

| Metal Treatment | 3% |

| Others | 2% |

End-Use Industry Insights

The chemical industry segment dominated the market with 46% share in 2025, akin to hydrazine hydrate, which functions as a chemical building block rather than a final product. In the current period, chemical manufacturers use it to create numerous downstream compounds that eventually enter pharmaceuticals, agricultural products, industrial additives, polymers, and specialty formulations.

The aerospace & defence industry segment held the 5% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 7.9% in the forecast period, owing to the sector prioritizing performance reliability over material cost. Unlike many industries that focus mainly on reducing expenses, aerospace applications require materials and chemicals that perform consistently under highly demanding operational conditions. Furthermore, growing investments in satellite deployment, strategic communication systems, deep-space missions, and defence modernization programs are increasing the need for specialized chemical inputs.

Hydrazine Hydrate Market Share,By End-Use Industry, 2025 (%)

| By End-Use Industry | Revenue Share, 2025 (%) |

| Chemical Industry | 46% |

| Water Treatment Industry | 20% |

| Agriculture Industry | 13% |

| Pharmaceutical Industry | 8% |

| Aerospace & Defense Industry | 5% |

| Electronics Industry | 4% |

| Others | 4% |

Grade Insights

The industrial grade segment dominated the market with 68% share in 2025, akin to most hydrazine hydrate consumption occurring in applications where functional performance is more important than ultra-high purity. In the current period, industries such as water treatment, polymer manufacturing, and chemical processing require large volumes of material at competitive costs. Industrial-grade products provide the necessary effectiveness without the additional purification expenses associated with premium grades.

The high-purity grade segment held the 14% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 7.4% in the forecast period, owing to manufacturing industries entering an era where contamination control is becoming a competitive advantage. In recent years, sectors such as aerospace, electronics, advanced materials, and pharmaceuticals have adopted stricter quality requirements. Even small impurities are likely to affect product performance, production yields, and regulatory compliance.

Hydrazine Hydrate Market Share,By Grade, 2025 (%)

| By Grade | Revenue Share, 2025 (%) |

| Industrial Grade | 68% |

| Pharmaceutical Grade | 11% |

| Electronic Grade | 7% |

| High-Purity Grade | 14% |

Distribution Channel Insights

The direct sales segment dominated the market with 61% share in 2025, akin to hydrazine hydrate, purchasing decisions are often based on trust, compliance, and technical support rather than price alone. In the current period, industrial buyers prefer working directly with manufacturers to ensure product consistency, regulatory documentation, and supply security. Furthermore, hydrazine hydrate requires specialized transportation, storage, and handling procedures, making close supplier relationships especially important.

The online chemical platforms segment held the 7% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 7.3% in the forecast period, owing to the chemical industry gradually adopting digital procurement strategies like those already used in manufacturing and retail sectors. In recent years, buyers have started prioritizing real-time inventory visibility, faster supplier comparisons, digital compliance documentation, and automated purchasing systems. Furthermore, younger procurement professionals are increasingly comfortable making sourcing decisions through digital platforms.

Hydrazine Hydrate Market Share,By Distribution Channel, 2025 (%)

| By Distribution Channel | Revenue Share, 2025 (%) |

| Direct Sales | 61% |

| Distributors & Traders | 32% |

| Online Chemical Platforms | 7% |

Regional Analysis

How will Asia Pacific Dominate the Hydrazine Hydrate Market in 2025?

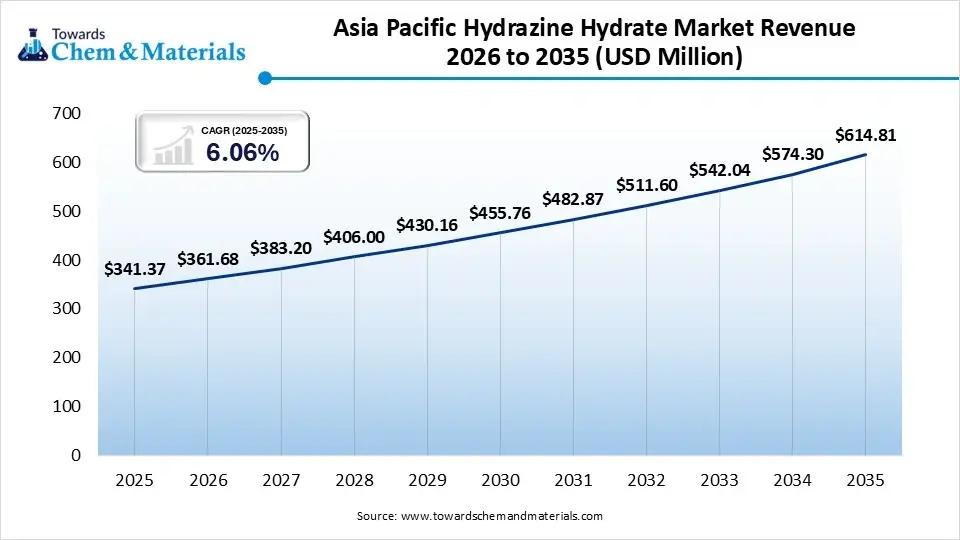

The Asia Pacific hydrazine hydrate market size was estimated at USD 341.37 million in 2025 and is projected to reach USD 614.81 million by 2035, growing at a CAGR of 6.06% from 2026 to 2035.Asia Pacific dominated the market with a share of 48% in 2025, due to the region having become the world's largest center for chemical manufacturing, industrial production, and specialty material processing. In the current period, countries across the region are expanding domestic chemical supply chains to support industries such as polymers, pharmaceuticals, electronics, and advanced materials. Additionally, lower production costs, strong industrial infrastructure, and rising demand from downstream industries continue to drives hydrazine hydrate consumption.

China

- Producers in China have moved beyond bulk chemical production and are increasingly focusing on specialty chemicals, advanced polymers, and performance materials.

- Also, the manufacturers are modernizing production facilities to improve efficiency and environmental performance.

Japan

- Industries in Japan are concentrating on advanced electronics, specialty chemicals, aerospace technologies, and high-quality industrial products, while manufacturers prioritize product purity and consistency.

- As the country strengthens research-intensive industries and next-generation manufacturing technologies, demand for high-quality hydrazine hydrate products continues to expand steadily.

Hydrazine Hydrate Market Evaluation in North America

North America hydrazine hydrate market size was estimated at USD 142.24 million in 2025 and is projected to reach USD 259.87 million by 2035, growing at a CAGR of 6.21% from 2026 to 2035.North America is notably growing with 20% market share in 2025 and is expected to be the fastest-growing region in the market, with a CAGR of 6.40% in the forecast period, owing to the region's investment in advanced manufacturing, aerospace innovation, defense modernization, and specialty chemical production. In recent years, governments and private companies have increased investments in strategic industrial sectors that require high-performance chemical materials.

United States

- The major investments are being directed toward domestic manufacturing capacity, advanced technology industries, and strategic industrial projects in the United States. Furthermore, increased activity in satellite development, space exploration programs, and defense, as per the observation.

- Also, the United States benefits from strong demand across multiple high-value sectors.

Canada

- The industries in Canada have focused on improving operational efficiency and extending equipment performance through advanced chemical solutions.

- Canada's strong mining, energy, and industrial processing sectors create steady demand for water treatment and industrial chemicals.

Europe Hydrazine Hydrate Industry Conditions

The Europe hydrazine hydrate market size was estimated at USD 135.13 million in 2025 and is projected to reach USD 247.19 million by 2035, growing at a CAGR of 6.23% from 2026 to 2035.Europe held the 19% market share in 2025, owing to industries that are increasingly investing in sustainable chemical manufacturing, advanced materials, and specialty production technologies. In the current period, companies are focusing on improving resource efficiency while maintaining high product quality standards. Furthermore, European manufacturers are developing advanced chemical formulations for aerospace, automotive, healthcare, and industrial applications.

Germany

- German companies are highly investing in precision chemicals, advanced materials, & industrial automation technologies, while the country's automotive transformation and industrial modernization initiatives are driving the demand for innovative chemical solutions.

- Germany's strength comes from large-scale industrial integration and technological expertise, as per the observation.

Italy

- Manufacturers in Italy are focusing on improving product quality, manufacturing flexibility, and export competitiveness while demand from specialty coatings, industrial materials, and niche chemical applications is creating new opportunities for chemical suppliers.

- Italy benefits from diversified medium-sized manufacturers serving multiple industrial sectors.

Hydrazine Hydrate Market Survey in Latin America

The Latin America hydrazine hydrate market size was estimated at USD 49.78 million in 2025 and is projected to reach USD 95.07 million by 2035, growing at a CAGR of 6.68% from 2026 to 2035.Latin America held the 7% market share in 2025 due to governments and industries increasing investments in domestic manufacturing, industrial processing, and chemical value chains. In recent years, companies have focused on reducing dependence on imported industrial products while strengthening regional production capabilities. Furthermore, expanding agricultural, mining, and industrial sectors are generating greater demand for specialty chemicals and water treatment solutions.

Brazil

- The country's growth is driven by industrial expansion, agricultural chemical production, and manufacturing development, while the companies are investing in local processing capabilities to support growing domestic demand for industrial materials and specialty chemicals.

- Brazil's large industrial base creates opportunities across water treatment, chemical processing, and polymer manufacturing sectors.

Argentina

- The growth of Argentina is gradually improving as industrial activity and manufacturing investment recover, while businesses have focused on improving productivity, reducing import dependence, and strengthening domestic production capabilities.

- Also, the industrial operators are seeking efficient chemical solutions that support cost optimization and equipment performance.

Middle East and Africa Hydrazine Hydrate Sector Observation

The Middle East and Africa hydrazine hydrate market size was estimated at USD 42.67 million in 2025 and is projected to reach USD 82.40 million by 2035, growing at a CAGR of 6.80% from 2026 to 2035.The Middle East and Africa held the 6% market share in 2025, akin to countries are actively diversifying their economies beyond traditional resource sectors. In the current period, governments are investing in chemical manufacturing, industrial processing, advanced materials, and downstream value-added industries. Furthermore, industrial infrastructure development and growing domestic production capabilities are creating new demand for specialty chemicals.

") Saudi Arabia

Saudi Arabia

- The significant investments have been directed toward creating value-added industries that utilize locally available resources in the country, while the chemical production, industrial processing, and manufacturing diversification initiatives are creating new opportunities for specialty chemical suppliers.

- Saudi Arabia is focused on building large-scale industrial production capacity.

UAE

- The UAE’s growing role as a regional trade, logistics, and advanced manufacturing hub, while the country is attracting investment in specialty chemicals, industrial services, and technology-driven manufacturing activities.

- Also, the strong connectivity with international markets allows companies to participate in global chemical supply chains more efficiently in the UAE nowadays.

Competitive Analysis

The leading companies are competing through product specialization, process efficiency, and supply chain control rather than simply increasing manufacturing capacity. Also, the growing number of customers is looking for reliable suppliers that are able to provide stable quality, regulatory compliance, and application-specific solutions.

- The Gujarat Alkalies and Chemicals Limited (GACL) has focused on strengthening domestic hydrazine hydrate manufacturing capabilities through indigenous technology development. This strategy supports local supply chain security and reduces dependence on imported production technologies.

- Otsuka Chemical Co., Ltd. is focusing on developing high-value hydrazine derivatives used in advanced industrial applications. Rather than competing mainly in bulk chemical volumes, the company is strengthening its presence in specialty chemical segments where product performance and technical expertise are more important than production scale.(Source: gacl.com, www.otsukac.co.jp, www.otsukac.co.jp)

Recent Development

- In May 2026, the GACL established an advanced high-purity hydrogen peroxide plant in India. Moreover, these greater establishments of the plant are specifically formed for the purpose of semiconductor and solar applications as per the company's claim.(Source: thehindubusinessline.com)

Top Vendors in the Hydrazine Hydrate Market & Their Offerings

- Arkema S.A.: This French chemical pioneer is famous for developing sustainable, specialized materials. They produce hydrazine hydrate to support global industries like agriculture and water treatment.

- LANXESS AG: Based in Germany, this major player focuses entirely on high-tech plastics and specialty chemical ingredients. They are highly respected for making reliable chemical intermediates, including hydrazine hydrate, used to prevent rust in industrial boilers. They emphasize strict safety, helping global clients safely handle complex, highly reactive materials.

- Lonza Group AG: This Swiss company is a globally trusted supplier for the healthcare and pharmaceutical industries. While they are world leaders in biotechnology and medicine manufacturing, their specialized chemical division provides high-purity ingredients. They deliver premium chemical solutions tailored for strict applications that require maximum consistency and safety compliance.

Other Key Players

- Otsuka Chemical Co., Ltd.

- Yibin Tianyuan Group Co., Ltd.

- Chongqing Chuandong Chemical (Group) Co., Ltd.

- Hunan Zhongchuang Chemical Co., Ltd.

- Weifang Yaxing Chemical Co., Ltd.

- Nippon Carbide Industries Co., Inc.

- Gujarat Alkalies and Chemicals Limited (GACL).

Segments Covered in the Report

By Concentration Level

- Hydrazine Hydrate 24%

- Hydrazine Hydrate 35%

- Hydrazine Hydrate 55%

- Hydrazine Hydrate 60%

- Hydrazine Hydrate 64%

- Hydrazine Hydrate 80%

- Other Concentrations

By Production Process

- Raschig Process

- Ketazine Process

- Hydrogen Peroxide Process

- Urea Process

By Application

- Polymerization & Blowing Agents

- Azodicarbonamide Production

- Chemical Foaming Agents

- Water Treatment

- Boiler Water Treatment

- Oxygen Scavenging

- Agrochemicals

- Herbicides

- Plant Growth Regulators

- Pesticide Intermediates

- Pharmaceuticals

- API Intermediates

- Drug Synthesis

- Chemical Intermediates

- Specialty Chemicals

- Organic Synthesis

- Aerospace & Defense

- Propellants

- Satellite Thrusters

- Metal Treatment

- Corrosion Inhibitors

- Surface Treatment

- Others

By End-Use Industry

- Chemical Industry

- Water Treatment Industry

- Agriculture Industry

- Pharmaceutical Industry

- Aerospace & Defense Industry

- Electronics Industry

- Others

By Grade

- Industrial Grade

- Pharmaceutical Grade

- Electronic Grade

- High-Purity Grade

By Distribution Channel

- Direct Sales

- Distributors & Traders

- Online Chemical Platforms

By Region

- North America

- U.S.

- Canada

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Sweden

- Denmark

- Norway

- Asia Pacific

- China

- Japan

- India

- South Korea

- Thailand

- Latin America

- Brazil

- Mexico

- Argentina

- Middle East & Africa

- South Africa

- UAE

- Saudi Arabia

- Kuwait

FAQ's

Select User License to Buy

Figures (7)