Content

What is the Current Elastic Adhesives Market Size and Share?

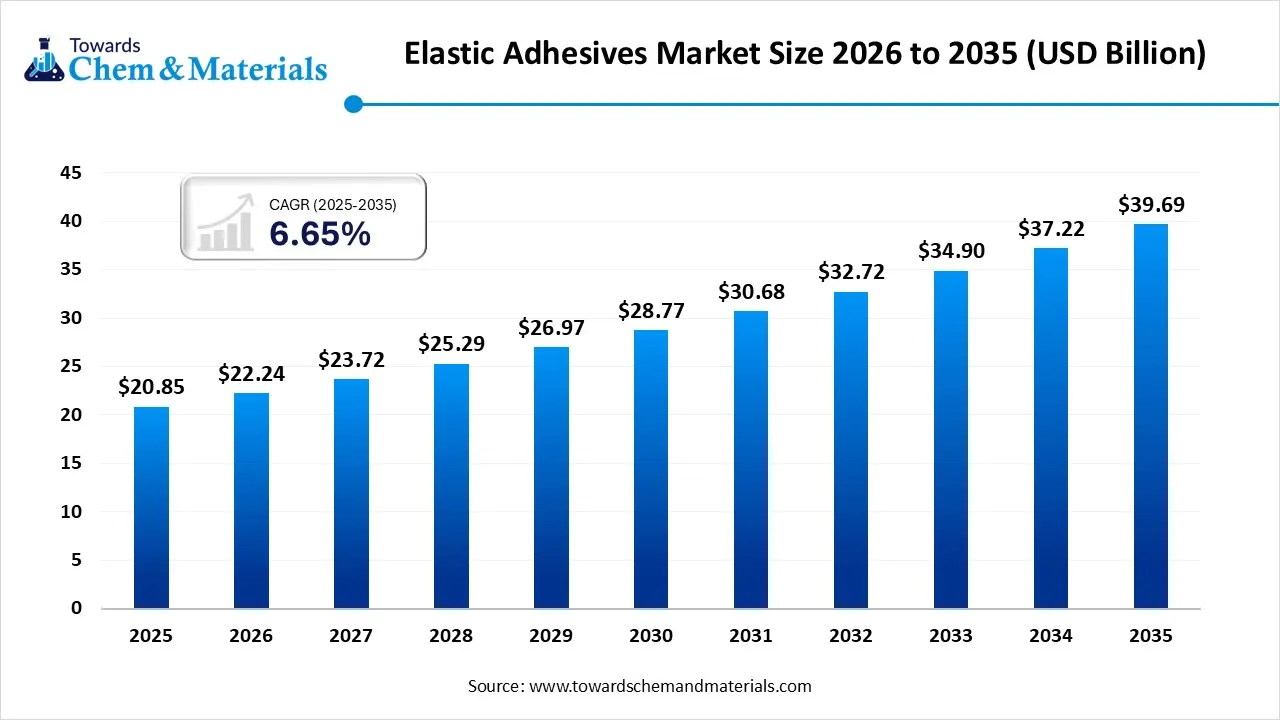

The global elastic adhesives market size was estimated at USD 20.85 billion in 2025 and is expected to increase from USD 22.24 billion in 2026 to USD 39.69 billion by 2035, growing at a CAGR of 6.65% from 2026 to 2035. Asia Pacific dominated the elastic adhesives market with the largest revenue share of 48.00% in 2025. The increased demand for stronger and more flexible bonding solutions has fueled the industry's growth in recent years. The special type of glue that can bend, stretch, and move without breaking is called the elastic adhesive. Moreover, by playing a major role in the reduction of noise and vibration, the elastic adhesives are likely to gain significant industry attention from the versatile sector, such as building and construction, automotive, and other major sectors in the coming years.

Market Highlights

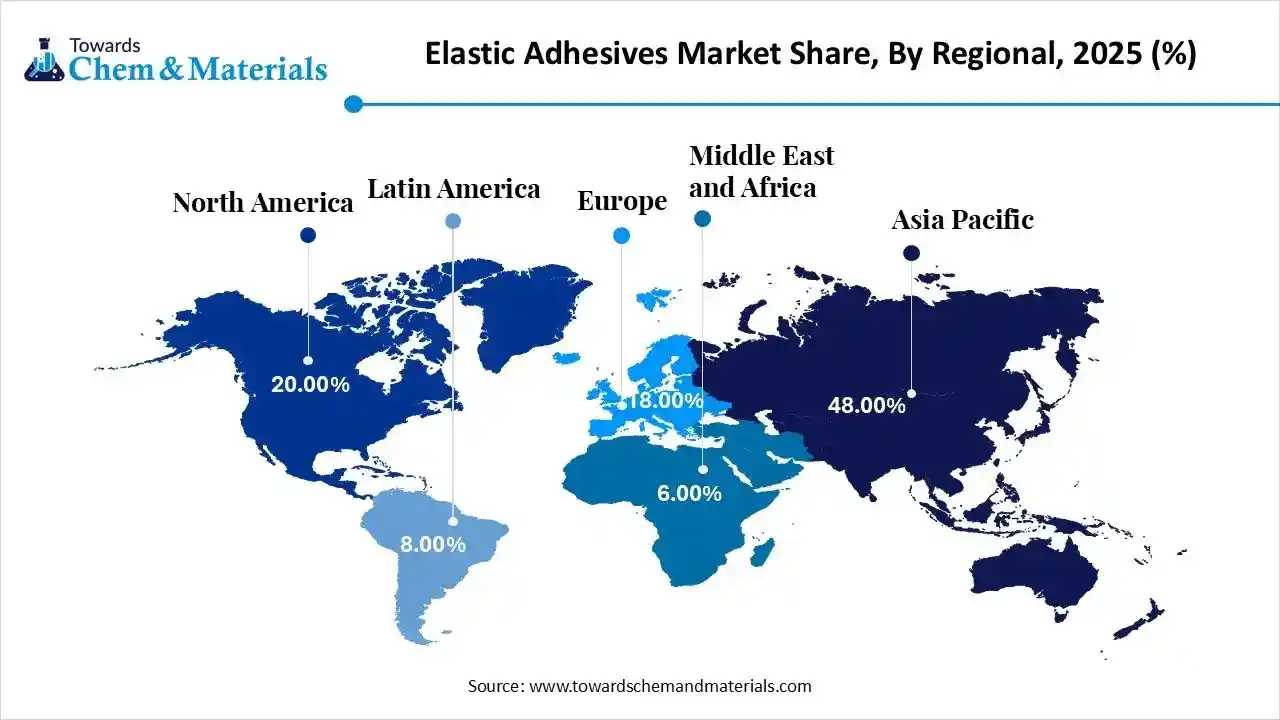

- The Asia Pacific dominated the elastic adhesives market with the largest revenue share of 48.00% in 2025, due to the heavy urbanization and faster industrial growth.

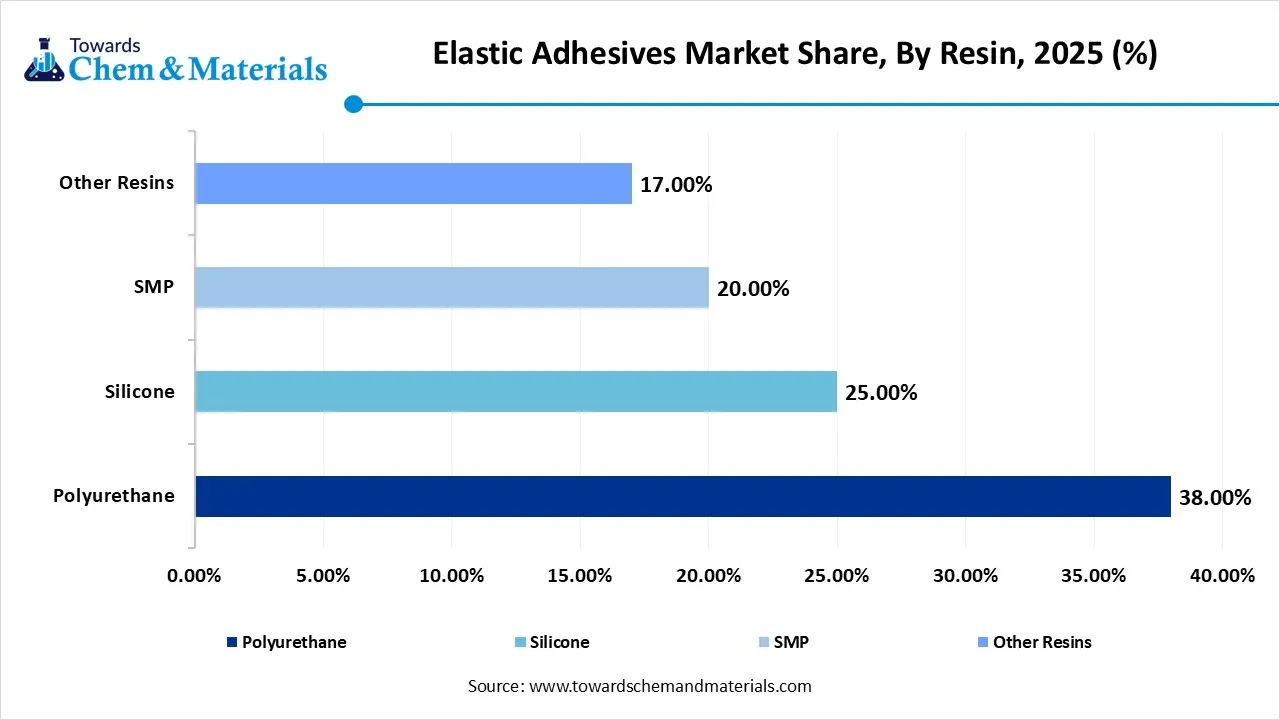

- By resins, the polyurethane segment dominated the market and accounted for the largest revenue share of 38.00% in 2025, owing to factors like durability, flexibility, and strength.

- By resins, the SMP segment is expected to grow at the fastest CAGR of 6.95% from 2026 to 2035 in terms of share. They do not release harmful chemicals, so they meet strict environmental rules.

- By end-use, the building and construction segment led the market with the largest revenue share of 44.00% in 2025, owing to these adhesives allowing buildings to handle movement caused by temperature changes and vibrations.

- By end-use, the automotive and transportation segment anticipated to grow at the fastest CAGR of 6.9% from 2026 to 2035 in terms of share, due to vehicles becoming lighter and more advanced.

Advanced Bonding Powers Next Growth Wave

The industry is actively shifting from traditional solvent-based adhesives to advanced smart adhesives, which may translate into favorable financial prospects for the producers in the coming years. Moreover, the new elastic adhesives can cure faster, work at low temperatures, and provide stronger bonding. Some adhesives now have moisture-curing or UV-curing technology, which saves time and energy. Hybrid polymers like silane-modified polymers are also becoming popular because they combine strength and flexibility.

Trade Analysis of the Elastic Adhesives Market:

Import, Export, Consumption, and Production Statistics

- The world has observed the heavy export of the retail adhesives in recent years through 6,538 exporters and 9,318 buyers with 33,397 global shipments between July 2024 and June 2025.

- China has emerged as the leading exporter of retail adhesives with 21,731 shipments, while South Africa (8,739 shipments) and the European Union (8,220 shipments) are actively following China nowadays.

Also, the leading importer of retail adhesives includes Ukraine with 21,264 shipments, Mexico (10,239), and Botswana (9,451), as per the recently published report.

Market Trends:

- The heavy shift towards the lightweight and flexible designs has supported stronger cash flows for the manufacturing enterprises in the current period. Also, the elastic adhesives have been seen in joining these smaller design materials without damaging them.

- The trend towards construction and infrastructure has attracted increased capital and investment in manufacturing in recent years. Also, by preventing leaks and cracks, the developer has used these elastic adhesives in panels, flooring, windows, and sealings as per the recent reports.

- The emergence of the low-emission and eco-friendly products is seen as a high-margin opportunity for manufacturers during the forecast period. Furthermore, the major developers or companies are actively investing in research and development activities in the current period.

Report Scope

| Report Attribute | Details |

| Market Size in 2026 | USD 22.24 Billion |

| Revenue Forecast in 2035 | USD 39.69 Billion |

| Growth Rate | CAGR 6.65% |

| Forecast Period | 2026 - 2035 |

| Base Year | 2025 |

| Dominant Region | Asia Pacific |

| Segment Covered | By Resin, By End Use, By Region |

| Key companies profiled | BASF SE, Henkel AG & Co. KGaA, H.B. Fuller Company, 3M, Dow, DuPont, Inc., Arkema, The Sherwin-Williams Company, Huntsman International LLC, PPG Industries, Sika AG, Wacker Chemie AG |

Value Chain Analysis of the Elastic Adhesives Market:

Distribution to Industrial Users

- The elastic adhesives market is dominated by Henkel, Sika, 3M, and Arkema (Bostik), which distribute products through direct OEM sales and extensive industrial networks. Leading industrial users include the construction and automotive sectors, where polyurethane and silicone adhesives are essential for structural bonding, weather sealing, and vibration damping.

Chemical Synthesis and Processing

- Chemical synthesis of elastic adhesives involves creating long-chain polymers like polyurethanes, silicones, or silane-modified polymers through polymerization and cross-linking.

- Processing includes compounding these resins with fillers, plasticizers, and catalysts to enhance flexibility and strength. The final mixture is degassed and packaged into cartridges or drums for industrial use, ensuring durability under mechanical stress.

Regulatory Compliance and Safety Monitoring

- Regulatory compliance for elastic adhesives involves adhering to REACH and RoHS standards to limit hazardous substances. Safety monitoring focuses on VOC emissions and skin/respiratory exposure.

- Manufacturers provide Safety Data Sheets (SDS) to ensure industrial users follow strict handling, ventilation, and waste disposal protocols mandated by agencies like OSHA or ECHA.

Elastic Adhesives Market Regulatory Landscape: Global Regulations

| Country Region | Regulatory Body | Key Regulations | Focus Areas |

| United States | Environmental Protection Agency (EPA) | TSCA Section 6: Grants EPA authority to restrict chemicals posing "unreasonable risk". | Elimination of toxic solvents, management of PFAS, "forever chemicals." |

| European Union | ECHA | REACH (EC 1907/2006): Governs the registration and restriction of chemical substances. Annex XVII includes upcoming 2026 restrictions on PFAS in cosmetics and reporting for synthetic polymer microparticles (microplastics) in industrial uses. | Transitioning to VOC-free formulations, enforcing the Ecodesign for Sustainable Products Regulation (ESPR), and mandatory updates to Safety Data Sheets (SDS) by Q2 2026 |

| China | National Standardization Administration (SAC) |

Hazardous Chemicals Safety Law: Effective May 1, 2026, this new law elevates chemical safety management from administrative regulation to national law. | Tightening limits on hazardous substances in consumer products, standardising food-contact adhesives, and implementing electronic labels (e-labels) for chemical compliance |

Segmental Insights

Resins Insights

How did the Polyurethane Segment Dominate the Elastic Adhesives Market in 2025?

The polyurethane segment dominated the market share 38.00% in 2025, due to factors like durability, flexibility, and strength. Moreover, by working efficiently in harsh environments and handling heat, moisture, and movement, the polyurethane has gained major industry attention in recent years. Also, several developers have been seen using polyurethane resins for flooring, panels, and institutions in the current period.

")

The SMP segment is expected to grow with a rapid CAGR, owing to they are eco-friendly and safer than traditional adhesives. They do not release harmful chemicals, so they meet strict environmental rules. They also combine the best features of silicone and polyurethane flexibility, strength, and weather resistance. SMP works well without primers, which saves time and labor. Also, SMP is becoming popular in green building certifications like LEED, where low emissions are required.

Elastic Adhesives Market Share, By Resin, 2025 (%)

| By Resin | Revenue Share, 2025 (%) |

| Polyurethane | 38.00% |

| Silicone | 25.00% |

| SMP | 20.00% |

| Other Resins | 17.00% |

End Use Insights

How did Building and Construction Dominate the Elastic Adhesives Market in 2025?

The building and construction segment dominated the market share 44.00% in 2025, due to these adhesives allowing buildings to handle movement caused by temperature changes and vibrations. Also, they are used in windows, facades, flooring, and roofing. Growth in urbanization and infrastructure projects has increased demand. Moreover, modern buildings need energy efficiency, and elastic adhesives help improve insulation and reduce energy loss.

The automotive and transportation segment is expected to grow, owing to vehicles becoming lighter and more advanced. Elastic adhesives help replace welding and screws, reducing weight and improving fuel efficiency. They are also important in electric vehicles (EVs), where they provide vibration resistance and battery protection. Adhesives improve safety by distributing stress across surfaces.

Elastic Adhesives Market Share, By End Use , 2025 (%)

| By End Use | Revenue Share, 2025 (%) |

| Building & Construction | 44.00% |

| Industrial | 25.00% |

| Automotive & Transportation | 18.00% |

| Other End Use | 13.00% |

Regional Insights

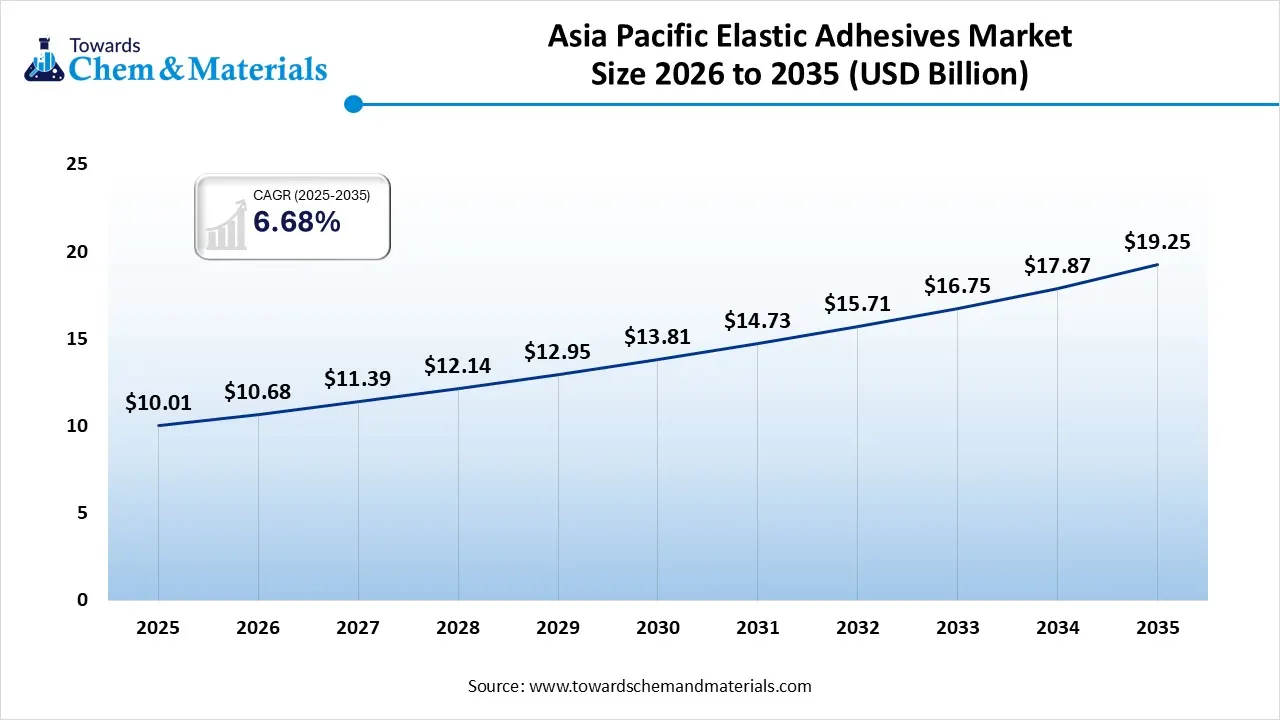

The Asia Pacific elastic adhesives market size was valued at USD 10.01 billion in 2025 and is expected to be worth around USD 19.25 billion by 2035, exhibiting at a compound annual growth rate (CAGR) of 6.68% over the forecast period from 2026 to 2035.

")

Asia Pacific dominated the elastic adhesives market share 48.00% in 2025, due to the heavy urbanization and faster industrial growth. Moreover, the regional countries such as China, India, and Japan have been seen under the heavy investment in modern constructions, which is actively leading to robust revenue growth across the sector in the current period. Also, the local manufacturing companies or producers are offering cost-effective adhesive solutions as per the recent regional survey.

China’s Industrial Growth Powers Adhesives

China maintained its dominance in the market, owing to its massive manufacturing and construction in the current period. Also, the country produces a huge number of buildings, vehicles, and electronic products, all of which use adhesives. Government policies support infrastructure development, increasing demand. Moreover, China's focus on green materials is pushing companies to develop low-emission adhesives like SMP. Local companies are rapidly innovating and offering cheaper alternatives, increasing competition.

Elastic Adhesives Market Evaluation in North America

The North America elastic adhesives market segment accounted for the major revenue share of 20.00% in 2025. North America is expected to capture a major share of the elastic adhesives market with a rapid CAGR, owing to a strong demand for high-performance and sustainable adhesives. The region focuses on advanced technologies, especially in automotive, aerospace, and construction. Strict environmental rules push companies to adopt eco-friendly products like SMP. Also, the rise of smart manufacturing and automation, where adhesives are used in robotic assembly lines in the region.

Green Buildings Propel Adhesive Innovation in the United States

The United States is expected to emerge as a prominent country for the elastic adhesives market in the coming years, due to its advanced industries and innovation. It has strong demand from the automotive, aerospace, and construction sectors. The country is a leader in electric vehicles and green buildings, which require advanced adhesives. Also, the use of adhesives in modular construction, where building parts are made off-site and assembled quickly. This increases efficiency and reduces waste.

Elastic Adhesives Market Share, By Regional, 2025 (%)

| Regional | Revenue Share, 2025 (%) |

| North America | 20.00% |

| Europe | 18.00% |

| Asia Pacific | 48.00% |

| Latin America | 8.00% |

| Middle East & Africa | 6.00% |

Europe Elastic Adhesives Market Examination

The Europe elastic adhesives market segment accounted for the major revenue share of 18.00% in 2025, Europe is notably growing in industry, owing to strict environmental regulations and sustainability goals. Companies are shifting toward low-VOC and eco-friendly adhesives. The region has strong automotive and construction industries, which support demand. Moreover, Europe's push for a circular economy, where materials are recyclable. Adhesives are being designed to allow easy disassembly of products in the region.

Innovation Powering Germany’s Adhesives Industry

Germany is expected to gain a significant industry share owing country's demands high-quality adhesives for precision applications. German companies focus on innovation and sustainability, driving new product development. Moreover, the use of adhesives in lightweight vehicle design improves efficiency and reduces emissions in the country nowadays.

Recent Developments

- In January 2026, Henkel introduced their latest production of adhesives called Loctite MS 9650. Also, the newly launched adhesives are dedicated to automotive applications, and they will work better in terms of durability, flexibility, and sustainability as per the company's claim.(Source: www.indianchemicalnews.com)

- In November 2025, Molibon unveiled the innovative product line of industrial adhesive and its high performance. Also, the names of adhesives are MA-5137, MA-5235, MA-5539, ME-7352, and PU-7456, which have different capabilities as per the company's claim.(Source: www.molibon.com)

Top Vendors in the Elastic Adhesives Market & Their Offerings:

- BASF SE: Based in Germany, BASF is a leading chemical supplier providing raw materials like polyurethanes and acrylics for adhesive formulations. Their focus is on sustainability and high-performance resins used in automotive and construction. They emphasize circular economy solutions, developing bio-based monomers to reduce carbon footprints in industrial bonding applications.

- Henkel AG & Co. KGaA: A global market leader headquartered in Germany, Henkel operates through its Adhesive Technologies business unit. Known for iconic brands like Loctite, Teroson, and Technomelt, they provide advanced elastic bonding solutions for the electronics, automotive, and aerospace industries. Their strategy prioritizes digitalized manufacturing and high-impact structural adhesives for lightweight vehicle designs.

- H.B. Fuller Company: This American multinational, H.B. Fuller, specializes in industrial adhesives across diverse sectors, including packaging, hygiene, and renewable energy. They are major players in reactive hot melt and elastic adhesives for the woodworking and textile markets. Their recent innovations focus on high-speed automated assembly and sustainable packaging solutions to meet global environmental standards.

- 3M: The US-based 3M Company is a powerhouse of R&D, famous for its VHB tapes and high-strength liquid elastic adhesives. They serve the electronics and healthcare sectors with precision bonding materials. 3M's current initiatives include developing PFAS-free alternatives and advanced structural adhesives that replace mechanical fasteners in harsh industrial environments.

- Dow

- DuPont, Inc.

- Arkema

- The Sherwin-Williams Company

- Huntsman International LLC

- PPG Industries

- Sika AG

- Wacker Chemie AG

Segments Covered in the Report

By Resin

- Polyurethane

- Silicone

- SMP

- Other Resins

By End Use

- Building & Construction

- Industrial

- Automotive & Transportation

- Other End Use

By Region

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Asia Pacific

- China

- India

- Japan

- South Korea

- Latin America

- Brazil

- Argentina

- Middle East & Africa

- Saudi Arabia

- South Africa

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

Tags

FAQ's

Select User License to Buy

Figures (4)