Content

Construction Adhesives Market Size and Forecast 2026 – 2035

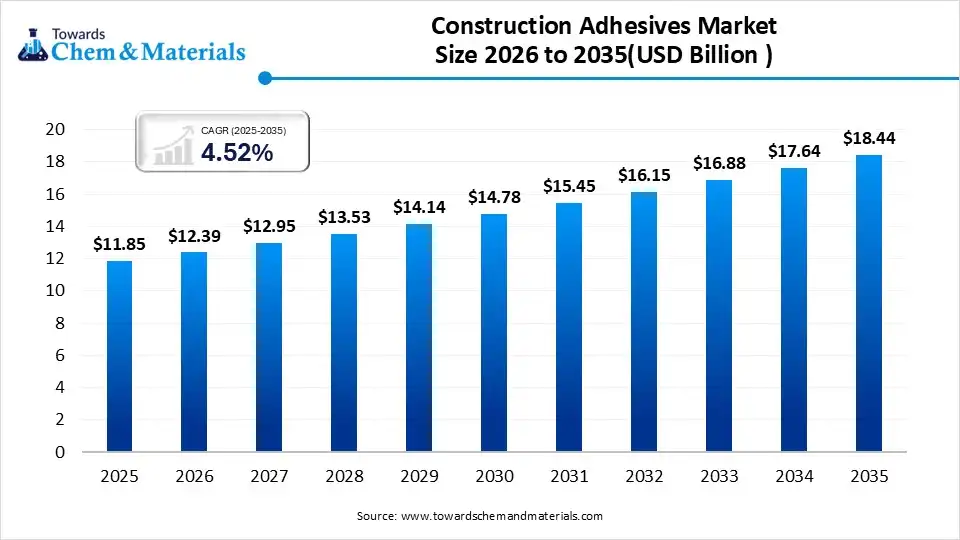

The global construction adhesives size was estimated at USD 11.85 billion in 2025 and is expected to increase from USD 12.39 billion in 2026 to USD 18.44 billion by 2035, growing at a CAGR of 4.52% from 2026 to 2035. Asia Pacific dominated the construction adhesives with the largest revenue share of 41.00% in 2025.The heavy shift towards the modern and time-saving infrastructure building has fueled the industry's growth in recent years.")

Market Highlights

- Asia Pacific dominated the market shaer 41.00% in 2025, due to its continuous construction across many sectors at the same time.

- By region, North America is anticipated to capture a greater portion of the market with a significant CAGR in the future due to many buildings now require upgrading rather than completely new construction.

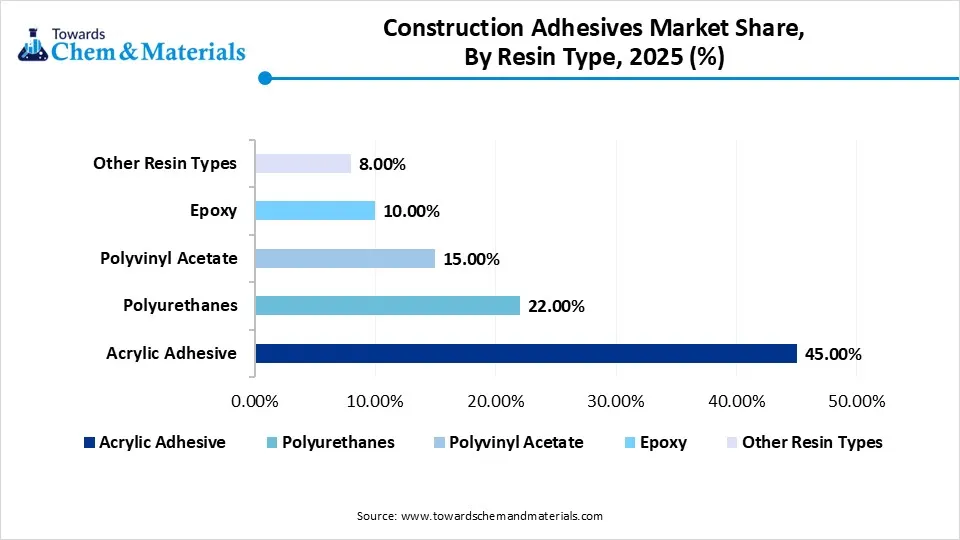

- By resin type, the acrylic adhesive segment dominated the market share 45.00% in 2025, owing to it offers a strong balance between bonding strength, flexibility, and easy use.

- By resin type, the polyvinyl acetate adhesives segment is expected to grow during the forecast period, due to its easy-to-use, affordable, and works especially well in interior applications.

- By technology, the water-based adhesives segment dominated the market share 46.00% in 2025, owing to its simplicity to handle and its wide acceptance in daily construction work.

- By technology, the reactive and others segment is expected to grow during the forecast period, due to they give stronger long-term bonding in demanding applications.

- By application, the commercial segment dominated the market share 36.00% in 2025, owing to offices, malls, hotels, hospitals, and retail spaces that use large amounts of adhesive during interior and finishing work.

- By application, the industrial segment is expected to grow during the forecast period, due to its factories, warehouses, production units, and technical buildings that use adhesive in many important installation areas.

Power Glue for Every Construction Need

Construction adhesive is a strong bonding material used to join building materials such as wood, metal, concrete, tiles, plastic, and wall panels. Also, it works like a powerful glue made for construction work, where strength and long holding power are important. Builders use it when nails or screws alone are not enough or when smooth finishing is needed.

Market Trends:

- The increasing need for products that save time has translated into valuable financial prospects for adhesives producers in recent years. Earlier, more mechanical fixing methods were used, which needed drilling, alignment, and extra labor. Now, many contractors prefer adhesive because it joins materials quickly and reduces visible fixing marks.

- Surface appearance now matters more than before in many buildings, which is seen as a high-margin opportunity for manufacturers. In recent years, strength was often the first priority, but now people also want cleaner walls, smooth panel joints, and neat visible finishing.

- The trend toward mixing different materials is likely to elevate earning potential for producers in the coming years. The modern construction now mixes many different materials in one project. A single building may use metal, wood, glass, foam boards, plastic panels, and engineered boards together.

Report Scope

| Report Attribute | Details |

| Market Size in 2026 | USD 12.39 Billion |

| Revenue Forecast in 2035 | USD 18.44 Billion |

| Growth Rate | CAGR 4.52% |

| Forecast Period | 2026 - 2035 |

| Base Year | 2025 |

| Dominant Region | Asia Pacific |

| Segment Covered | By Resin Type, By Technology, By Application, By Region |

| Key companies profiled | H.B. Fuller, 3M Company, Sika AG, The Dow Chemical Company, Bostik SA (An Arkema Company), Henkel AG & Co. KGaA, Dap Products, Franklin International, Illinois Tool Works Incorporated, Avery Dennison Corporation |

Smarter Adhesives for Every Environment

The products are now designed for stronger performance under different weather and surface conditions, which is projected to support stronger cash flows for manufacturing enterprises during the forecast period. In recent times, many adhesives have worked well only in limited environments. Now builders want one adhesive that works in heat, moisture, indoor spaces, and outdoor use. Manufacturers are improving formula balance, so adhesives spread easily, cure faster, and hold better over time. Also, adhesive is moving from simple bonding toward smarter bonding that adapts to real building conditions.

Trade Analysis of the Construction Adhesives Market:

Import, Export, Consumption, and Production Statistics

- The construction adhesives emerged as one of the leading exporting products with 10,841 shipments globally via 2,390 buyers and 2,066 exporters between July 2024 and June 2025, as per the published report.

- China has seen a heavy export of construction adhesives with 17,946 shipments, while Vietnam (7,324 shipments) and Japan (3,696 shipments) are following.

- Vietnam has been observed in sophisticated import of construction adhesives with 23,568 shipments, while Russia (7,465 shipments) and Kazakhstan (2,093 shipments).

Supply Chain Analysis of the Construction Adhesives Market:

Distribution to Industrial Users

- Distribution to industrial users of construction adhesives typically occurs through direct sales from manufacturers like Henkel or 3M for large-scale projects, or via specialized industrial distributors like Fastenal and Grainger.

- These channels provide high-volume supply, technical support, and bulk dispensing solutions for infrastructure and manufacturing facilities.

Chemical Synthesis and Processing

- Chemical synthesis involves polymerizing raw materials like resins, hardeners, and solvents to create bonding agents. Processing utilizes high-shear mixers to blend these polymers with fillers and stabilizers, ensuring uniform viscosity and strength. Controlled heating and cooling cycles then stabilize the chemical structure before the adhesive is packaged for industrial use.

Regulatory Compliance and Safety Monitoring

- Regulatory compliance for construction adhesives involves adhering to REACH, RoHS, and VOC emission standards to ensure environmental and worker safety. Safety monitoring utilizes Material Safety Data Sheets (MSDS) and rigorous batch testing to track chemical exposure and fire hazards, maintaining high-performance reliability across diverse industrial applications.

Construction Adhesives Market Regulatory Landscape: Global Regulations

| Country Region | Regulatory Body | Key Regulations | Focus Areas |

| United States | Environmental Protection Agency (EPA) | 40 CFR Part 59: National VOC emission standards for consumer and commercial products | Reduction of ground-level ozone (smog), indoor air quality (LEED certification), and chemical labeling under the Federal Hazardous Substances Act (FHSA). |

| European Union | European Chemicals Agency (ECHA). | REACH (EC 1907/2006): Controls the registration, evaluation, and restriction of chemicals to protect human health and the environment | chemical transparency, circular economy (recyclability), and protecting indoor environments from toxic substances and radiation |

| China | Ministry of Ecology and Environment (MEE). |

GB 33372-2020: Limits of volatile organic compounds content in adhesives (mandatory national standard). |

Environmental impact reduction, mandatory safety labeling (Orange Label 2), and digital compliance tools like QR codes for product information. |

Segmental Insights

Resin Type Insights

How did the Acrylic Adhesive Segment Dominate the Construction Adhesives Market in 2025?

The acrylic adhesive segment dominated the market share 45.00% in 2025, due to its offering a strong balance between bonding strength, flexibility, and easy use. Builders prefer acrylic because it works well on many common surfaces, such as concrete, wood, tiles, and wall materials. Also, it handles small surface movement without breaking easily, which is useful in buildings where materials expand or contract slightly. Acrylic products also give good durability in indoor and outdoor applications.")

The polyvinyl acetate adhesives segment is expected to grow with a rapid CAGR, owing to its easy-to-use, affordable, and works especially well in interior applications. It is widely useful for wood panels, decorative laminates, furniture fittings, and light building materials. As more construction focuses on interiors, modular fittings, and fast finishing, this adhesive becomes attractive because workers already understand how to apply it easily. Also, it supports quick and clean indoor bonding without complicated handling. Future growth may come strongly from interior construction and light assembly work, where cost control and easy application matter more than heavy structural strength.

Construction Adhesives Market Share, By Resin Type , 2025 (%)

| By Resin Type | Revenue Share, 2025 (%) |

| Acrylic Adhesive | 45.00% |

| Polyurethanes | 22.00% |

| Polyvinyl Acetate | 15.00% |

| Epoxy | 10.00% |

| Other Resin Types | 8.00% |

- The acrylic adhesive segments' share of 45.00% in 2025 dominates due to their strong versatility, excellent bonding properties, and cost-effectiveness in a wide range of applications.

- The polyurethanes segments share 22.00% in 2025. Gaining momentum with increasing demand in automotive and construction applications for their durability and flexibility.

- The polyvinyl acetate segments share 15.00% in 2025, gaining momentum due to their high usage in packaging and paper products, driven by consumer demand for eco-friendly solutions.

- The epoxy segments share 10.00% in 2025, not dominating but growing due to its high performance in specialized applications like electronics and heavy-duty bonding.

- The other resin type segments share 8.00% in 2025, not dominating, representing a smaller share due to limited use in niche sectors compared to dominant resin types.

Technology Insights

How did the Water-Based Adhesives Segment Dominate the Construction Adhesives Market in 2025?

The water-based adhesives segment dominated the market share 46.00% in 2025, due to its simplicity to handle and its wide acceptance in daily construction work. It spreads easily, cleans more easily during application, and is commonly used in indoor projects where controlled application matters. Moreover, many workers already know how to use water-based products, so training needs are lower. It also fits many common materials used in walls, panels, flooring, and decorative work. As the builders trust it because it feels practical and familiar.

The reactive and others segment is expected to grow with a rapid CAGR, owing to they give stronger long-term bonding in demanding applications. Also, these adhesives react chemically after application and create a very strong attachment between difficult surfaces. They are useful where builders need stronger resistance against heat, stress, vibration, or heavy industrial use. Also, when projects become more demanding, stronger chemistry becomes more important. Future construction increasingly uses advanced materials and technical designs, so reactive systems are expected to grow.

Construction Adhesives Market Share, By Technology , 2025 (%)

| By Technology | Revenue Share, 2025 (%) |

| Water-based | 46.00% |

| Solvent-based | 28.00% |

| Reactive & Others | 26.00% |

- The water-based segments share 46.00% in 2025, dominating due to their eco-friendliness, low toxicity, and regulatory preferences, making them the top choice for industries prioritizing sustainability.

- The Solvent-based segments share 28.00% in 2025. Not dominating but still significant due to its fast-drying properties and effectiveness in heavy-duty applications, though losing favor in environmentally conscious sectors.

- The Reactive & Others segments share 26.00% in 2025, gaining momentum due to the increasing demand for high-performance adhesives in specialized applications like construction and automotive.

Application Insights

How did the Commercial Segment Dominate the Construction Adhesives Market in 2025?

The commercial segment dominated the market share 36.00% in 2025, due to offices, malls, hotels, hospitals, and retail spaces using large amounts of adhesive during interior and finishing work. These buildings often need panels, flooring, ceiling systems, decorative materials, and partitions installed quickly and neatly. Adhesive helps reduce visible fixing marks and improves appearance. Also, commercial projects often follow strict timelines, so faster bonding methods are preferred. Moreover, the adhesives became important because commercial construction needs both speed and clean finishing.

The industrial segment is expected to grow with a rapid CAGR, owing to its factories, warehouses, production units, and technical buildings that use adhesive in many important installation areas. Adhesives are used for fixing insulated panels, industrial flooring, wall sheets, machine-area coverings, and protective surface materials where strong bonding is required. Also, the industrial buildings often face vibration, load, and repeated mechanical movement, so traditional fixing alone is sometimes not enough, which leads to the need for stronger adhesion.

Construction Adhesives Market Share, By Application , 2025 (%)

| By Application | Revenue Share, 2025 (%) |

| Residential | 40.00% |

| Commercial | 36.00% |

| Industrial | 24.00% |

- The residential segments share 40% in 2025, dominated due to strong demand driven by home construction, renovations, and DIY projects, with growing investments in residential development.

- The commercial segments share 36.00% in 2025, not dominating but maintaining a strong presence due to the growth of commercial construction and infrastructure projects, including office buildings and retail spaces.

- The industrial segments share 24.00% in 2025, not dominating but gaining momentum due to increasing industrial applications in manufacturing, automotive, and heavy-duty industries, focusing on high-strength adhesives.

Regional Insights

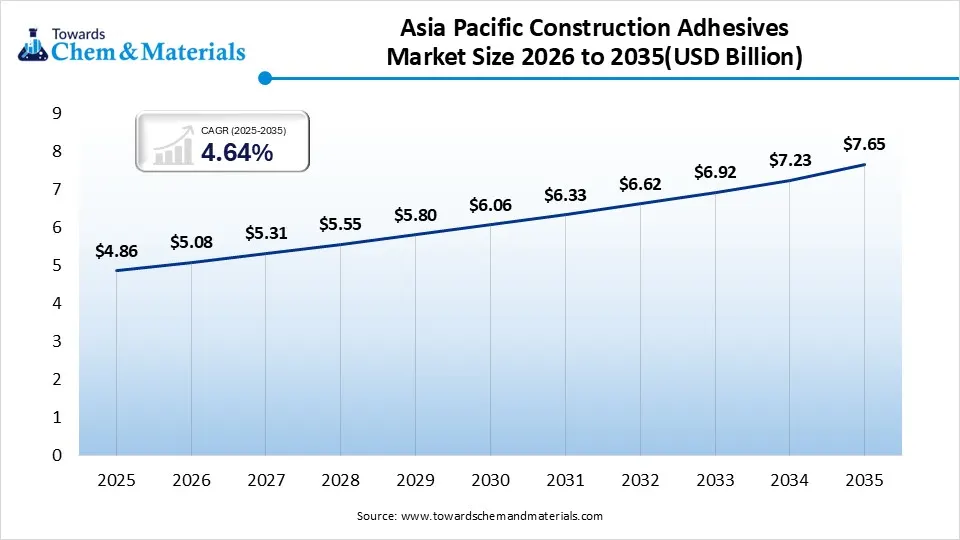

The Asia Pacific construction adhesives market size was valued at USD 4.86 billion in 2025 and is expected to be worth around USD 7.65 billion by 2035, exhibiting at a compound annual growth rate (CAGR) of 4.64% over the forecast period from 2026 to 2035.")

Asia Pacific dominated the construction adhesives market in 2025, due to its continuous construction across many sectors at the same time. Residential towers, office buildings, transport projects, shopping spaces, and industrial parks all create strong adhesive demand. Also, many buildings in this region now use lightweight panels, modular interiors, and pre-finished materials, where adhesive becomes very useful. As modern construction methods are increasing faster here than before. Since many countries in this region are expanding cities and infrastructure together, adhesive demand remains strong across daily building activity, which keeps the region ahead in the global market.

China Leads with Fast-Built Adhesive Demand

China maintained its dominance in the market, owing to large-scale building projects often moving quickly and using many factory-made materials that need adhesive during final installation. Moreover, the wall boards, insulation layers, decorative sheets, flooring systems, and ceiling structures all create strong demand. Also, the many commercial buildings and public facilities require clean finishing, where adhesive gives better visual results than visible fixing methods. Furthermore, China uses adhesive heavily because many modern projects depend on fast assembly.

Construction Adhesives Market Share, By Regional, 2025 (%)

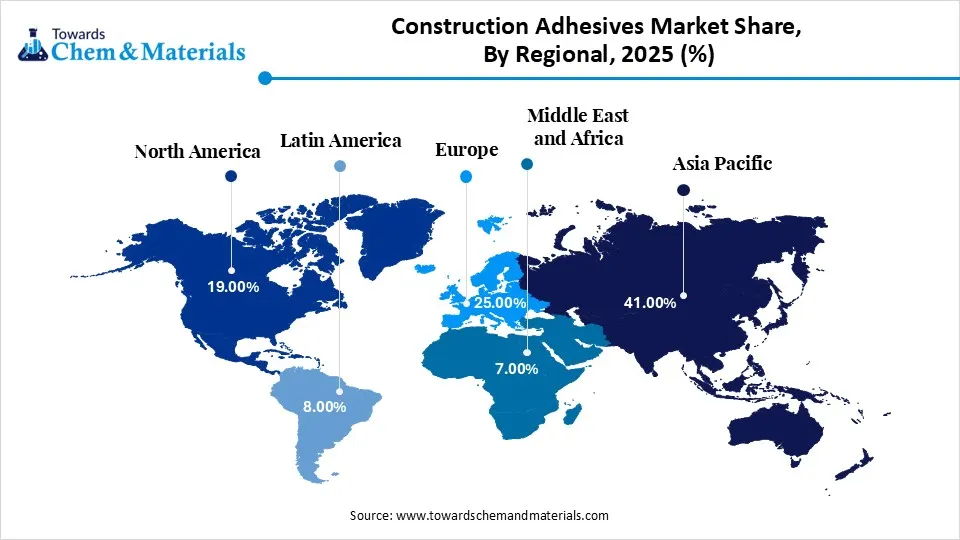

| Regional | Revenue Share, 2025 (%) |

| North America | 19.00% |

| Europe | 25.00% |

| Asia Pacific | 41.00% |

| Latin America | 8.00% |

| Middle East & Africa | 7.00% |

- The Asia Pacific shares 41.00% in 2025, dominating due to rapid urbanization, growing construction activities, and increasing demand for affordable housing in developing economies.

- The North America shares 19.00% in 2025, not dominating but holding a significant share due to advanced infrastructure and strong demand in construction and automotive industries.

- The Europe shares 25.00% in 2025, gaining momentum with high demand for eco-friendly and innovative construction materials, supported by strong regulations and sustainable practices.

- The Latin America shares 8.00% in 2025. Not dominating, with limited share due to slower infrastructure development and lower demand in the construction sector compared to other regions.

- The Middle East & Africa 7.00% in 2025 Not dominating, with a smaller market share, driven by niche demand in construction projects and challenges in infrastructure development.

Construction Adhesives Market Evaluation in North America

North America construction adhesives market segment accounted for the major revenue share of 19.00% in 2025. North America is expected to capture a major share of the construction adhesives market with a rapid CAGR, owing to many buildings now require upgrading rather than completely new construction. Moreover, the old offices, commercial spaces, hospitals, warehouses, and public buildings are being improved with modern materials, which increases adhesive demand. Adhesives become important when surfaces must be renewed without damaging existing structures. Also, the builders increasingly prefer faster installation methods to reduce labor time.

Modern Building Fuels United States Adhesive Adoption

The United States is expected to emerge as a prominent country for the construction adhesives market in the coming years, due to many projects now using engineered boards, insulation panels, acoustic materials, and layered flooring systems that depend on adhesive during installation. Moreover, the builders often choose adhesive because it supports cleaner work and helps reduce visible fixing marks in finished spaces. Also, the industrial and logistics buildings are expanding, and these projects use strong bonding solutions in flooring and panel installation. Moreover, the adhesive demand stays strong because modern building methods increasingly depend on surface bonding instead of only mechanical fixing.")

Europe Construction Adhesives Market Examination

Europe is growing in industry, owing to many building projects now focusing on interior modernization and energy-saving construction methods. Also, adhesives are used more when insulation materials, wall systems, and modern interior surfaces are installed carefully. Also, many buildings are upgraded instead of replaced, which creates steady demand for bonding materials during renovation. Also, the adhesives become important because modern improvement work often needs clean attachment methods that do not damage older structures.

Precision Bonding Drives Germany’s Construction Growth

Germany is expected to gain a significant industry share owing to many construction projects there that use precision installation where exact surface quality matters. Moreover, the adhesive is preferred when flooring, insulation boards, technical panels, and interior systems must stay aligned for long periods. Also, the country's industrial construction uses many bonded materials where stable performance matters more than quick fixing alone. Also, the German projects often choose materials carefully, and adhesive becomes important because it supports both strength and a neat finish.

Recent Developments

- In November 2025, Bostik introduced the latest production of construction sealant and adhesive. Also, these newly launched adhesives are specifically designed for the multi surface and are named OB1Multi-Surface Construction Sealant and Adhesive as per the published report.(Source: www.specialchem.com )

- In July 2025, Polyglass unveiled the eco-friendly adhesive solutions, which are specifically designed for the roofing of cold-applied systems. Moreover, the newly launched adhesives are known as PG 350 LV and PG SFA, as per the company's claim.(Source: www.azobuild.com)

Top Vendors in the Construction Adhesives Market & Their Offerings:

- H.B. Fuller: Founded in 1887 and headquartered in Minnesota, H.B. Fuller is a leading global provider of specialty adhesives, sealants, and chemical products. It serves diverse markets including electronics, hygiene, medical, transportation, and construction. The company focuses on innovation and sustainable solutions to improve products and manufacturing processes worldwide.

- 3M Company: Originally the Minnesota Mining and Manufacturing Company (founded 1902), 3M is a massive American multinational conglomerate. It produces over 60,000 products, including Scotch tape, Post-it notes, and N95 respirators. Operating in industry, safety, healthcare, and consumer goods, 3M is globally renowned for its immense patent portfolio and R&D-driven culture.

- Sika AG: Headquartered in Baar, Switzerland, Sika is a specialty chemicals giant established in 1910. It leads the market in systems for bonding, sealing, damping, reinforcing, and protecting in the building and automotive sectors. Sika is famous for its pioneering tunnel waterproofing solutions and has a massive global manufacturing presence across 100+ countries.

- The Dow Chemical Company: Founded in 1897 in Michigan, Dow is one of the world's largest chemical producers. It specializes in plastics, chemicals, and performance materials for packaging, infrastructure, and consumer care. After a high-profile merger and subsequent 2019 split from DuPont, Dow now focuses on high-value materials science and innovation in global industrial markets.

- Bostik SA (An Arkema Company)

- Henkel AG & Co. KGaA

- Dap Products

- Franklin International

- Illinois Tool Works Incorporated

- Avery Dennison Corporation

Segments Covered in the Report

By Resin Type

- Acrylic Adhesive

- Polyurethanes

- Polyvinyl Acetate

- Epoxy

- Other Resin Types

By Technology

- Water-based

- Solvent-based

- Reactive & Others

By Application

- Residential

- Ceramic Tiles

- Countertop Lamination

- Carpet Laying

- Floor Coverings

- Gypsum Boards

- Other Residential Applications

- Commercial

- Ceramic Tiles

- Countertop Lamination

- Carpet Laying

- Floor Coverings

- Gypsum Boards

- Other Commercial Applications

- Industrial

- Ceramic Tiles

- Countertop Lamination

- Carpet Laying

- Floor Coverings

- Gypsum Boards

- Other Industrial Applications

By Region

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Asia Pacific

- China

- India

- Japan

- South Korea

- Latin America

- Brazil

- Argentina

- Middle East & Africa

- Saudi Arabia

- South Africa

FAQ's

Select User License to Buy

Figures (4)