Content

What is the Current Biorefinery Market Size and Share?

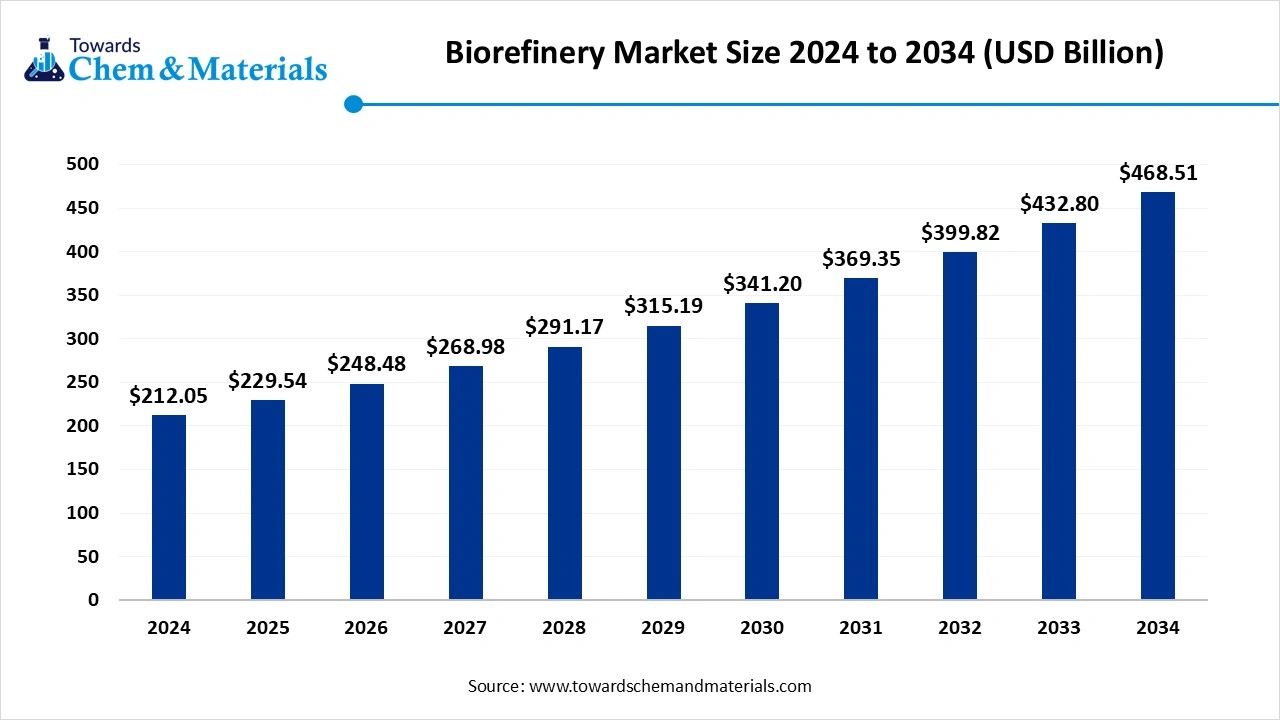

The global biorefinery market size was estimated at USD 229.70 billion in 2025 and is expected to increase from USD 248.65 billion in 2026 to USD 507.50 billion by 2035, growing at a CAGR of 8.25% from 2026 to 2035. Asia Pacific dominated the biorefinery market with the largest revenue share of 43% in 2025. Growing environmental awareness is the key factor driving market growth. Also, supportive government policies coupled with the increasing demand for renewable energy can fuel market growth further.

Key Takeaways

- Asia-Pacific dominated the global biorefinery industry with the largest revenue share of 43% in 2025.

- By feedstock type, the lignocellulosic biomass segment led the market with the largest revenue share of 42% in 2025.

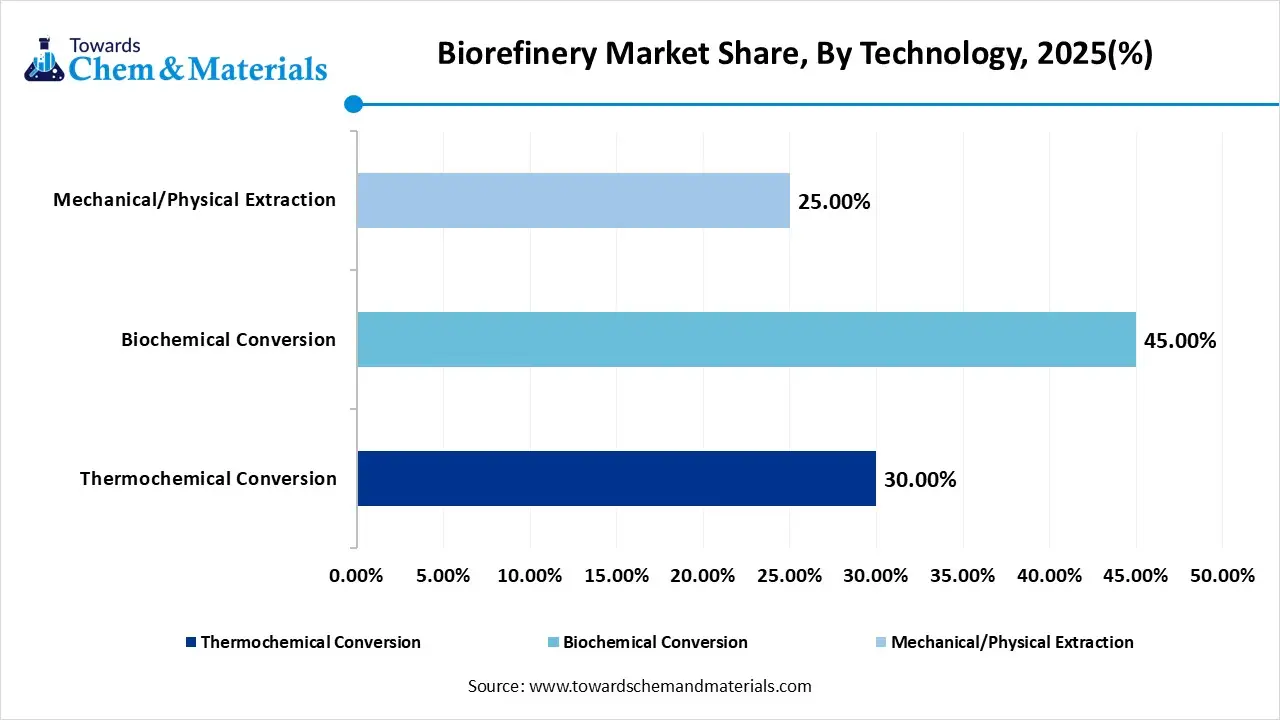

- By technology, the biochemical conversion segment dominated the market with a revenue share of 45% in 2025.

- By product type, the Biofuels segment led the market with the largest revenue share of 35% in 2025.

- By end use industry, the transportation segment dominated the market with a revenue share of 47% in 2025.

- By refinery type, the second-generation biorefineries segment led the market with the largest revenue share of 46% in 2025.

Advancements in Biorefining Technologies are Expanding Market Growth

A biorefinery is a type of unit that integrate biomass conversion processes and equipment to produce fuels, heat, power, chemicals, and materials from biomass. Like petroleum refineries, biorefineries convert biomass into a spectrum of marketable products and energy. The biorefinery market includes the technologies, processes, and value chains that enable this transformation from raw biomass into value-added products. Technological innovations in areas such as microbial optimization and enzyme engineering are improving the cost-effectiveness and efficiency of biorefining processes.

What Are the Key Trends Influencing the Biorefinery Market?

- Growing environmental awareness has boosted efforts to curb water, air, and soil pollution, which is the latest trend in the market nowadays. Many countries have grown awareness of their carbon footprints and have announced targets to minimize their carbon emissions soon. This factor boosted the investments in biorefineries.

- Advances in microbial optimization, enzyme engineering, and other advanced technologies are improving the cost-effectiveness and efficiency of biorefinery processes, impacting positive market growth soon. Also, Biorefineries are outgrowing their product portfolio to include biochemicals, biofuels, and bioplastics, tailored to different industries.

- Easy availability of biomass is the key market trend shaping a good market trajectory. Biomass, like animals, organic materials from plants and microorganisms, is accessible and abundant in nature. Biorefineries use this resource to produce biochemicals, biofuels, and biomaterials. This minimizes dependence on fossil fuels by supporting sustainable energy production.

Report Scope

| Report Attribute | Details |

| Market Size in 2026 | USD 248.65 Billion |

| Expected Size by 2035 | USD 507.50 Billion |

| Growth Rate from 2025 to 2034 | CAGR 8.25% |

| Base Year of Estimation | 2025 |

| Forecast Period | 2025 - 2035 |

| Dominant Region | Asia Pacific |

| Segment Covered | By Feedstock Type, By Technology Pathway, By Product Type, By End-use Industry, By Refinery Type, By Region |

| Key Companies Profiled | Neste Corporation, Abengoa Bioenergy, Clariant AG, POET LLC, TotalEnergies SE, ADM (Archer Daniels Midland Company), UPM-Kymmene Corporation, Renewable Energy Group (Chevron), Gevo Inc., BASF SE, Borregaard ASA, Beta Renewables (Biochemtex), Enerkem Inc., Valero Energy Corporation, Algenol Biotech LLC, Dong Energy (Ørsted), GranBio, St1 Nordic Oy, LanzaTech, Cargill Incorporated |

Market Opportunity

Investment in Green Energy

Private companies, governments, and research institutions are heavily investing in sustainable products and green energy technologies, creating lucrative opportunities in the market. Biorefineries align with these investments by reducing waste, supporting circular economies, and promoting the shift to cleaner energy sources. Furthermore, biorefineries provide a way to use renewable biomass to create chemicals, biofuels, and other products, tackling climate change problems.

Market Challenges

High Initial Capital Investment

Establishing a biorefinery needs a substantial initial investment in equipment, infrastructure, and technology, which is the major factor hampering market growth in the long run. Moreover, producing high-quality and consistent products from biomass can be challenging, necessitating strong quality and process assurance measures, hindering market expansion further.

Emerging Initiatives for the Biorefinery

| Region/Country | Initiative Name | Focus Area |

| India | National Bioenergy Programme (NBP) | Supports waste-to-energy projects, providing Central Financial Assistance for biomass pellet/briquette manufacturing and biogas plants. |

| U.S | Renewable Fuel Standard (RFS) & IRA | Continues to drive investment in cellulosic ethanol and biogas via tax credits. |

| EU | Renewable Energy Directive (RED III) | Driving demand for advanced biofuels and biomass-based products. |

| Australia | ARENA Biofuel Feasibility Studies | Allocates funds for projects targeting SAF production from sugarcane waste. |

Value Chain Analysis

Feedstock Sourcing and Logistics

- This involves securing a consistent, cost-effective supply of biomass, including agricultural residues, forestry residues, wood chips, and organic waste.

- Key Players: ADM, Cargill, Raízen, Neste, and Enviva.

Pretreatment and Biomass Conversion

- This converts complex, raw lignocellulosic biomass into intermediate building blocks through chemical, mechanical, and biological processes like steam explosion and enzymatic hydrolysis.

- Key Players: Novozymes A/S, Clariant, DuPont, and Dyadic International.

Manufacturing and Bioprocessing

- This involves the conversion of intermediate building blocks into finished products through fermentation, anaerobic digestion, and thermochemical conversion.

- Key Players: Neste, TotalEnergies, Valero Energy Corporation, Gevo, Raízen, POET, and Green Plains Inc.

Logistics and Distribution

- This involves specialized logistics are required to transport liquid biofuels, biocrude, and solid bioproducts from processing plants to final distributors.

- Key Players: DHL Group, Neste, and Valero Energy Corporation.

Commercialization and End-Use Markets

- In this, the final products are distributed to industries such as automotive, packaging, aviation, and chemicals.

- Key Players: Neste, Chevron, and TotalEnergies.

Segmental Insight

By Technology Insights

How did the Biochemical Conversion Segment Dominate the Biorefinery Market?

The biochemical conversion segment dominated the market with a revenue share of 45% in 2025. This dominance is mainly stems from its lower energy requirements, high product selectivity, and compatibility with existing infrastructure. This segment's efficient processes, including fermentation and enzymatic hydrolysis, convert sugars, starches, and increasingly lignocellulosic biomass into high-value bioethanol and sustainable chemicals. Biochemical pathways are highly selective, producing specific, high-value biochemicals, organic acids, and bioplastics. By operating at low temperatures and pressures, these processes significantly reduce energy costs.

")

The thermochemical conversion segment is expected to experience the fastest growth during the forecast period. This growth is attributed to its high efficiency in converting diverse, non-food biomass feedstocks into sustainable fuels and chemicals. Processes such as gasification, pyrolysis, and hydrothermal liquefaction are capable of handling lignocellulosic biomass, agricultural waste, and wet algal biomass, thereby reducing reliance on food crops. These are generally faster and better suited for large-scale industrial production, and the urgent demand in aviation and transportation is accelerating investments.

Biorefinery Market Share, By Technology , 2025(%)

| By Technology | Revenue Share, 2025 (%) |

| Thermochemical Conversion | 30.00% |

| Biochemical Conversion | 45.00% |

| Mechanical/Physical Extraction | 25.00% |

- Thermochemical Conversion technology holds a revenue share of 30.00% in the Biorefinery Market in 2025, contributing a significant portion of the total market.

- Biochemical Conversion technology is the dominant technology in the Biorefinery Market, commanding a 45.00% share of the revenue in 2025.

- Mechanical/Physical Extraction technology captures 25.00% of the market share in 2025, highlighting its importance in the biorefinery industry.

By Feedstock Type Insight

Which Feedstock Type Segment Dominated the Biorefinery Market in 2025?

The lignocellulosic biomass segment held a 42.00% market share in 2025. The dominance of the segment can be attributed to the innovations in pretreatment technologies for smooth biomass conversion, along with the supportive government regulations. In addition, the segment uses materials such as forestry waste and agricultural residues to produce biochemicals, biofuels, and biomaterials.

The aquatic biomass segment is expected to grow at the fastest CAGR over the forecast period. The growth of the segment can be credited to the innovations in photobioreactor technology and increasing utilisation of algae-based biofuels. Research and development efforts focused on promoting growing, harvesting, and extraction processes are important for minimizing the overall cost of algae-based products.

Biorefinery Market Share, By Feedstock Type , 2025(%)

| Feedstock Type | Revenue Share, 2025 (%) |

| Lignocellulosic Biomass | 42.00% |

| Sugar & Starch Crops | 7.00% |

| Oil Crops | 15.00% |

| Organic Waste | 11.00% |

| Aquatic Biomass | 20.00% |

| Microalgae | 5.00% |

- Lignocellulosic Biomass holds the largest revenue share of 42.00% in the Biorefinery Market in 2025, making it the primary feedstock type.

- Sugar & Starch Crops contribute 7.00% of the revenue share in the Biorefinery Market in 2025, representing a smaller yet significant portion.

- Oil Crops account for 15.00% of the market share in 2025, showcasing their relevance in biorefinery feedstocks.

- Organic Waste represents 11.00% of the Biorefinery Market's revenue share in 2025, emphasizing its role as a sustainable feedstock option.

- Aquatic Biomass has a revenue share of 20.00% in the Biorefinery Market in 2025, making it a noteworthy contributor to the industry.

- Microalgae, though smaller, contribute 5.00% of the revenue share in the Biorefinery Market in 2025, highlighting its emerging potential.

Product Type Insight

Product Type Insights

What made the Biofuels Segment Lead the Biorefinery Market?

The biofuels segment led the market with the largest revenue share of 35% in 2025., with the bioethanol sub-segment holding a significant market share. This dominance results from mandatory ethanol blending programs, the maturity of first-generation technology, and the availability of high-volume, cost-effective feedstocks. The transition to second-generation bioethanol, derived from lignocellulosic biomass, enhances sustainability and diversifies feedstock options. Bioethanol is primarily used as an additive to gasoline, improving octane levels and reducing carbon emissions. Stringent environmental regulations and blending mandates ensure consistent demand in the transportation sector, as the largest consumer of biofuels.

The biochemicals segment is anticipated to grow the fastest, particularly the specialty chemicals sub-segment. This growth is driven by the increasing demand for sustainable, high-value materials. The segment is shifting focus from low-value fuels to high-performance bio-based platform chemicals, polymers, and specialty ingredients for personal care products. There is a growing emphasis on sustainability in industries such as packaging, pharmaceuticals, cosmetics, and automotive. Strict regulations on volatile organic compounds and a reduction in petrochemical dependency are driving the adoption of bio-based surfactants, lubricants, and polymers with higher profit margins.

Biorefinery Market Share, By Product Type , 2025(%)

| By Product Type | Revenue Share, 2025 (%) |

| Biofuels | 35.00% |

| Biochemicals | 21.00% |

| Solvents | 15.00% |

| Bioelectricity | 11.00% |

| Solvents | 8.00% |

| Natural Fibers | 6.00% |

| District Heating | 4.00% |

- Biofuels dominate the Biorefinery Market with a revenue share of 35.00% in 2025, marking them as the leading product type.

- Biochemicals account for 21.00% of the market share in 2025, establishing their significant role in the biorefinery industry.

- Solvents make up 15.00% of the revenue share in 2025, indicating their important position within the biorefinery product portfolio.

- Bioelectricity contributes 11.00% of the market share in 2025, underlining its relevance as a renewable energy source.

- Solvents, with an additional share of 8.00% in 2025, highlight their dual significance in different biorefinery applications.

- Natural Fibers represent 6.00% of the market share in 2025, reflecting their role in the sustainable production sector.

- District Heating makes up 4.00% of the revenue share in 2025, showcasing its utility in biorefinery-based energy systems.

End-Use Industry Insight

Why Did the Transportation Segment Dominated the Biorefinery Market in 2025?

The transportation segment dominated the market with a 47% market share in 2025 The dominance of the segment can be attributed to the rising awareness of climate change, innovations in biorefinery technologies, and the stringent environmental regulations. Also, consumers are increasingly opting for sustainable products such as eco-friendly transportation options, further boosting the demand for this segment in the market.

The packaging segment is expected to grow at the fastest CAGR over the study period. The growth of the segment is due to advancements in biorefining technologies, which have made it more cost-effective and efficient to produce bio-based plastics and other materials for packaging use. The integration of biorefineries with other sectors like the paper and pulp industry is also impacting overall segment growth positively in the near future.

Biorefinery Market Share, By End-use Industry, 2025(%)

| By End-use Industry | Revenue Share, 2025 (%) |

| Transportation (Road, Aviation, Marine) | 47.00% |

| Chemical Industry | 20.00% |

| Power Generation | 10.00% |

| Agriculture | 7.00% |

| Packaging | 5.00% |

| Textiles | 4.00% |

| Pharmaceuticals & Personal Care | 3.00% |

| Construction & Building Materials | 4.00% |

- The Transportation sector, covering Road, Aviation, and Marine, leads the Biorefinery Market with a substantial revenue share of 47.00% in 2025.

- The Chemical Industry holds a significant 20.00% of the market share in 2025, demonstrating its vital role in biorefinery applications.

- Power Generation accounts for 10.00% of the revenue share in 2025, highlighting the importance of biorefinery products in energy production.

- The Agriculture sector contributes 7.00% to the Biorefinery Market in 2025, emphasizing the growing integration of sustainable practices in agriculture.

- Packaging represents 5.00% of the market share in 2025, underlining its role in utilizing biorefinery-derived materials for eco-friendly packaging solutions.

- The Textiles industry holds 4.00% of the revenue share in 2025, demonstrating the use of biorefinery products in sustainable fabric production.

- Pharmaceuticals & Personal Care account for 3.00% of the market share in 2025, reflecting the use of biorefinery products in the healthcare and beauty sectors.

- The Construction & Building Materials industry contributes 4.00% to the Biorefinery Market in 2025, highlighting the adoption of sustainable bioproducts in construction.

Refinery Type Insight

Which Refinery Type Segment Dominated the Biorefinery Market in 2025?

The second-generation biorefineries segment held a 46% market share in 2025. The dominance of the segment can be linked to its ability to produce valuable biochemicals, along with the rising environmental concerns. Second-generation biorefineries use lignocellulosic biomass as a feedstock, which is more convenient and sustainable than food-based feedstocks used in first-generation biorefineries.

The third-generation biorefineries segment is expected to grow at the fastest CAGR over the projected period. The growth of the segment can be credited to the growing global demand for renewable energy sources, coupled with the advancements in technology. Moreover, third-generation biorefineries use microalgae, which can grow in different environments and fix CO2, making them a reliable feedstock for biofuel production.

Biorefinery Market Share, By Refinery Type, 2025(%)

| By Refinery Type | Revenue Share, 2025 (%) |

| First-Generation Biorefineries (food-based) | 22.00% |

| Second-Generation Biorefineries (non-food biomass) | 46.00% |

| Third-Generation Biorefineries (algae and aquatic sources) | 15.00% |

| Integrated Biorefineries (multi-feedstock, multi-product) | 17.00% |

- Second-Generation Biorefineries, which use non-food biomass, hold the largest revenue share of 46.00% in the Biorefinery Market in 2025.

- First-Generation Biorefineries, based on food sources, contribute 22.00% of the market share in 2025, reflecting their continued relevance in the industry.

- Third-Generation Biorefineries, utilizing algae and aquatic sources, account for 15.00% of the revenue share in 2025, highlighting their emerging potential.

- Integrated Biorefineries, which employ multi-feedstock and multi-product processes, capture 17.00% of the market share in 2025, showcasing their versatility and efficiency.

Regional Insights

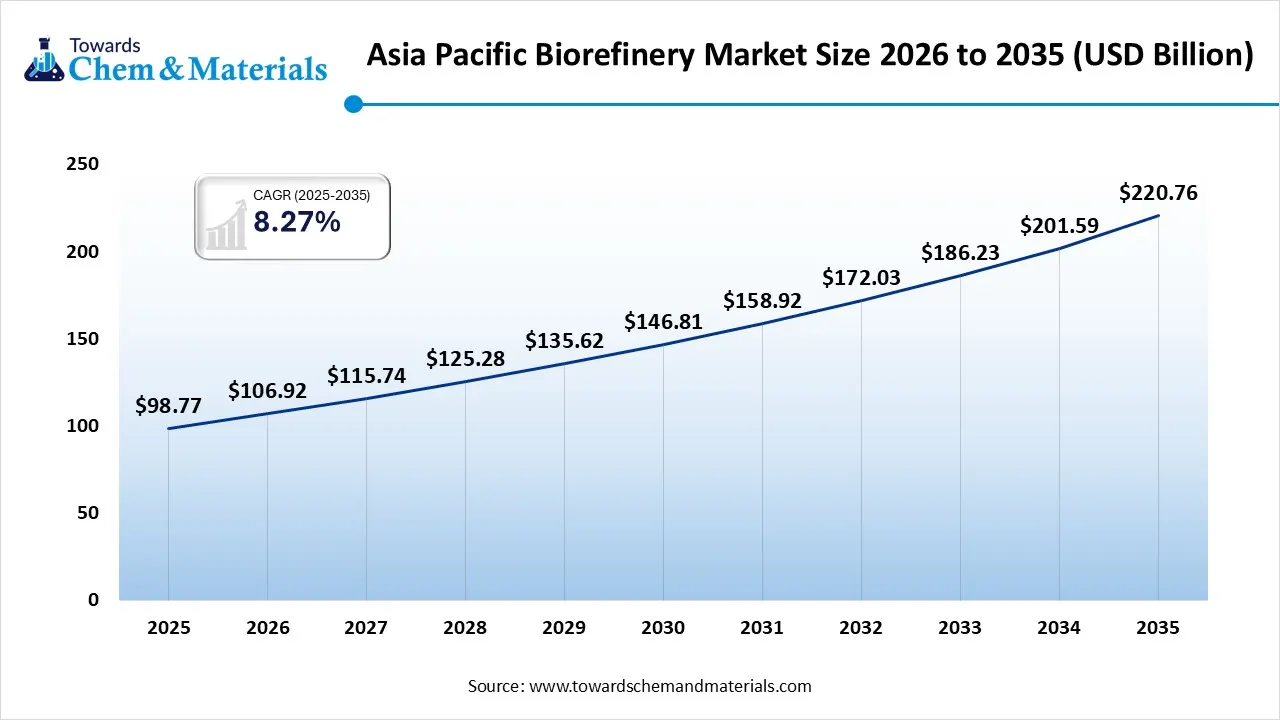

The Asia Pacific biorefinery market size was valued at USD 98.77 billion in 2025 and is expected to be worth around USD 220.76 billion by 2035, exhibiting at a compound annual growth rate (CAGR) of 8.27% over the forecast period from 2026 to 2035. Asia-Pacific dominated the global biorefinery industry with the largest revenue share of 43% in 2025.

The growth of the region can be credited to the rapid urbanization, rising population, and industrialization in emerging economies such as China and India. Furthermore, biofuel production is rising in China, India, and Thailand due to several major factors. These nations also possess large arable land and favourable climates for cultivating feedstock crops such as corn, sugarcane, and palm oil, which are crucial for biofuel production. In the Asia Pacific, China dominated the market by holding the largest market share, due to ongoing technological advancements, increasing awareness of environmental sustainability, and the country's commitment to carbon neutrality. China also has a huge agricultural sector and generates substantial amounts of agricultural residues, offering handy feedstock for biorefineries

How will North America be considered a notable Region in the Biorefinery Market?

North America is experiencing significant growth in the global market, primarily driven by strong government support, abundant feedstocks, and a rapid transition to advanced biofuels. The U.S. Renewable Fuel Standard mandates and tax incentives, particularly those promoting Sustainable Aviation Fuel (SAF), play crucial roles in this development. The region has a consistent and large-scale supply of agricultural waste, forestry residue, corn, and soybeans, which facilitates the scaling of first-generation ethanol and the adoption of second-generation feedstocks.

The U.S. Biorefinery Market Trends

The U.S. is pivotal in this region, focusing on large-scale bioethanol and biodiesel production while making substantial investments in research and development for second-generation and third-generation biorefineries. The Renewable Fuel Standard and EPA mandates for biodiesel and SAF are key drivers of this growth. The U.S. biofuels market is projected to expand significantly, propelled by efforts toward decarbonization and the increasing adoption of SAF in aviation.

Biorefinery Market in Germany

In Europe, Germany led the market owing to the increasing consumer awareness regarding carbon footprints and the desire for sustainable alternatives across many sectors such as pharmaceuticals, packaging, and transportation. Also, Germany has a robust agricultural sector that offers a readily available supply of biomass residues, which can be utilised as feedstock for biorefineries.

Emergence of Latin America in the Biorefinery Market

Latin America is an emerging region within the global market, owing to its unmatched agricultural resources, robust government mandates, and a pioneering role in biofuel production. The region is actively transitioning from first-generation biofuels to second-generation biofuels, utilizing sugarcane bagasse and residues to promote a circular economy. It possesses a vast and diverse natural resource base, with over 50% of land classified as having agricultural potential, providing an ideal supply of feedstocks such as sugarcane, soybeans, and palm oil.

Brazil Biorefinery Market Trends

Brazil plays a distinctive role in this region as a major exporter of biofuels, significantly contributing to its trade balance and green energy goals. By leveraging its extensive agricultural sector, Brazil produces, consumes, and exports biofuels with a strong focus on sugarcane ethanol. Additionally, Brazil is rapidly advancing the development of second-generation ethanol from bagasse and straw, with plans to scale up production to meet future demand.

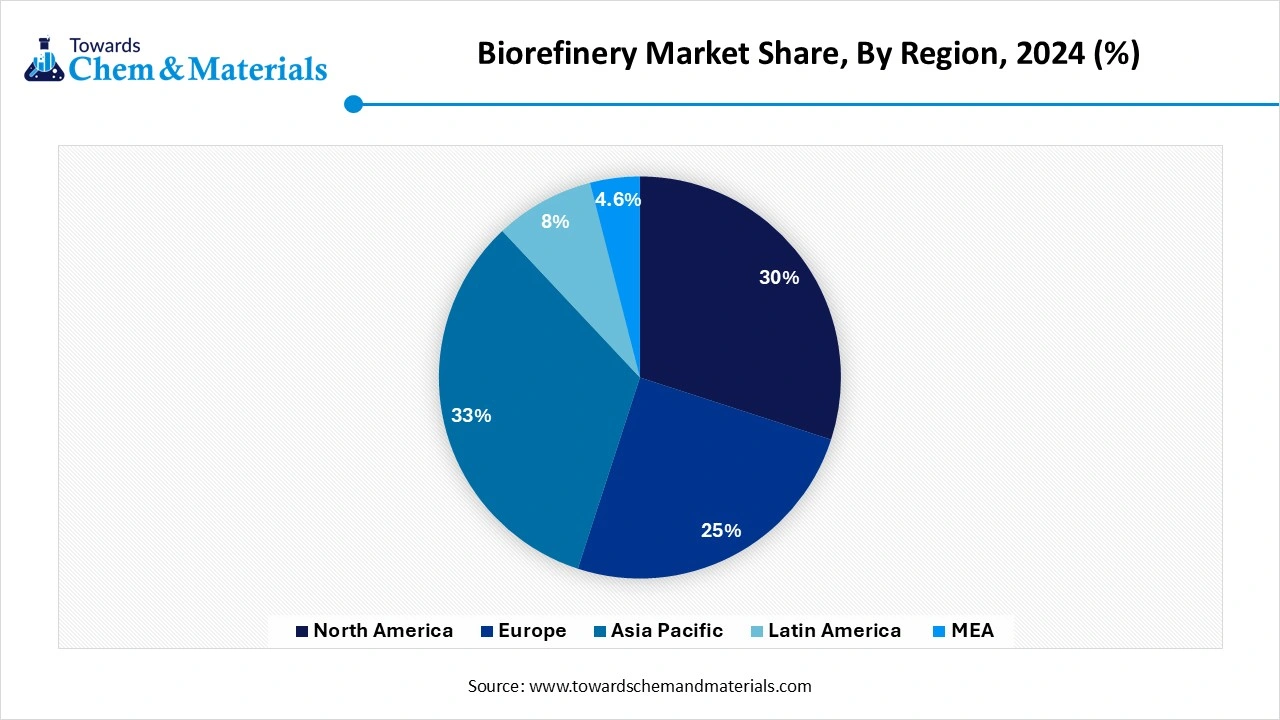

Biorefinery Market Share, By Region, 2025(%)

| By Region | Revenue Share, 2025 (%) |

| North America | 30.00% |

| Europe | 15.00% |

| Asia Pacific | 43.00% |

| Latin America | 7.00% |

| Middle East & Africa | 5.00% |

How will the Middle East and Africa Biorefinery Market?

The Middle East and Africa is a key contributor in the global market, driven by the need to decarbonize, manage waste, and utilize agricultural residues. The region boasts extensive agricultural resources and high-potential non-food biomass sources, including agricultural residue, date palm waste, animal manure, and municipal solid waste. Major producers like Saudi Arabia and the UAE are investing in biorefineries to diversify their economies and energy mixes and reduce reliance on oil and gas revenues.

The UAE Biorefinery Market Trends

The UAE stands out as a mature market within this region, characterized by its economic power and strategic location. It is investing in and developing the biorefinery sector, particularly in sustainable fuels. The UAE is pioneering the conversion of waste, including used cooking oil and food waste, into biodiesel and SAF, aiming to reduce greenhouse gas emissions and position itself as a key player in the supply of low-carbon marine fuels.

Recent Developments

- In January 2026, Haffner Energy launched its new C-iC modular industrial units line to address the financing and deployment challenges facing medium-scale, decentralized biofuel projects. This approach also makes mid-sized projects financeable and enables their realization without reliance on subsidies, offering a value proposition that is currently unmatched for medium-sized projects.(Source: www.haffner-energy.com)

- In December 2025, UPM began producing industrial sugars at its Leuna biorefinery in Germany, marking the first commercial output from Europe's largest biochemicals investment. This milestone demonstrates UPM's commitment to bio-based material innovations and reinforces its position as a leader in sustainable materials, as remarked by Massimo Reynaudo, President and CEO of UPM.(Source: www.indianchemicalnews.com)

Top Companies List

- Neste Corporation

- Abengoa Bioenergy

- Clariant AG

- POET LLC

- TotalEnergies SE

- ADM (Archer Daniels Midland Company)

- UPM-Kymmene Corporation

- Renewable Energy Group (Chevron)

- Gevo Inc.

- BASF SE

- Borregaard ASA

- Beta Renewables (Biochemtex)

- Enerkem Inc.

- Valero Energy Corporation

- Algenol Biotech LLC

- Dong Energy (Ørsted)

- GranBio

- St1 Nordic Oy

- LanzaTech

- Cargill Incorporated

Segments Covered

By Feedstock Type

- Lignocellulosic Biomass

- Wood

- Straw

- Corn stover

- Bagasse

- Sugar & Starch Crops

- Sugarcane

- Corn

- Wheat

- Oil Crops

- Soybean

- Rapeseed

- Palm

- Algae

- Organic Waste

- MSW

- Industrial Waste

- Food Waste

- Aquatic Biomass

- Seaweed

- Microalgae

By Technology Pathway

- Thermochemical Conversion

- Pyrolysis

- Gasification

- Hydrothermal Liquefaction

- Biochemical Conversion

- Fermentation

- Anaerobic Digestion

- Enzymatic Hydrolysis

- Mechanical/Physical Extraction

- Pressing

- Drying

- Milling

By Product Type

- Biofuels

- Bioethanol

- Biodiesel

- Biogas

- Sustainable Aviation Fuel (SAF)

- Bio-oil

- Biochemicals

- Platform Chemicals

- Succinic Acid

- Lactic Acid

- Others (Furfural, etc.)

- Specialty Chemicals

- Surfactants

- Solvents

- Biopolymers

- Biomaterials

- Bioplastics

- Bio-composites

- Natural Fibers

- Cellulosic Fibers

- Lignin‑Based Fibers

- Plant/Vegetal Fibers

- Agricultural Residue Fibers

- Power & Heat

- Biomass Power

- Bio‑Steam

- Bio‑Thermal

- Combined Heat & Power

- Bioelectricity

- Biogas‑to‑Electricity

- Biomass Steam Turbines

- Gasification‑based Electricity

- Waste‑to‑Energy Electricity

- District Heating

- Biomass District Heating

- Bio‑CHP District Heating

- Thermal Networks

By End-use Industry

- Transportation (Road, Aviation, Marine)

- Chemical Industry

- Power Generation

- Agriculture

- Packaging

- Textiles

- Pharmaceuticals & Personal Care

- Construction & Building Materials

By Refinery Type

- First-Generation Biorefineries (food-based)

- Second-Generation Biorefineries (non-food biomass)

- Third-Generation Biorefineries (algae and aquatic sources)

- Integrated Biorefineries (multi-feedstock, multi-product)

By Region

- North America

- U.S.

- Canada

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Sweden

- Denmark

- Norway

- Asia Pacific

- China

- Japan

- India

- South Korea

- Thailand

- Latin America

- Brazil

- Mexico

- Argentina

- Middle East and Africa (MEA)

- South Africa

- UAE

- Saudi Arabia

- Kuwait

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

FAQ's

Select User License to Buy

Figures (5)