Content

What is the Bio-Rational Fungicides Market Size and Share?

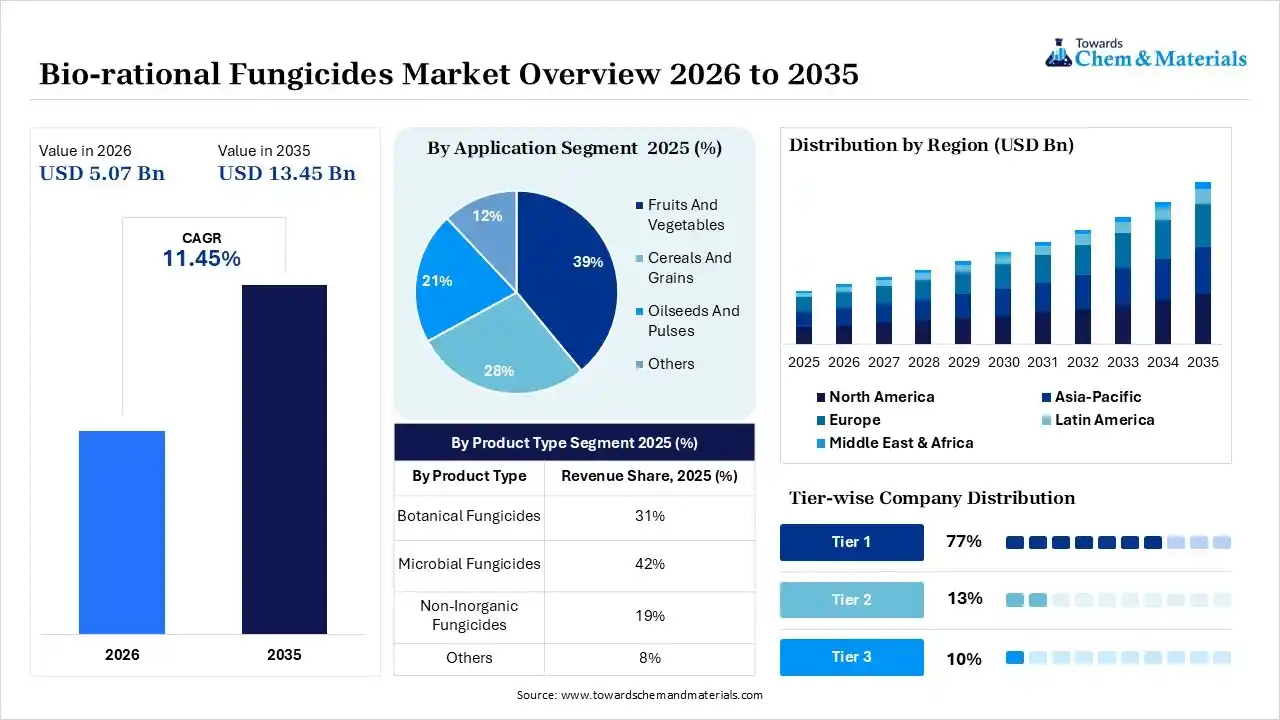

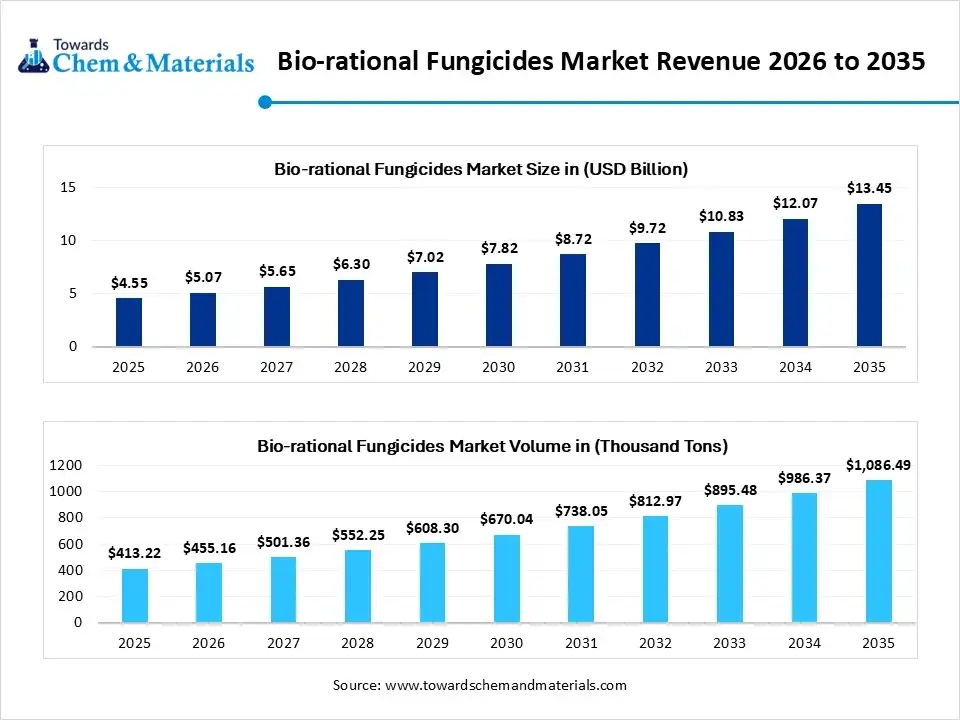

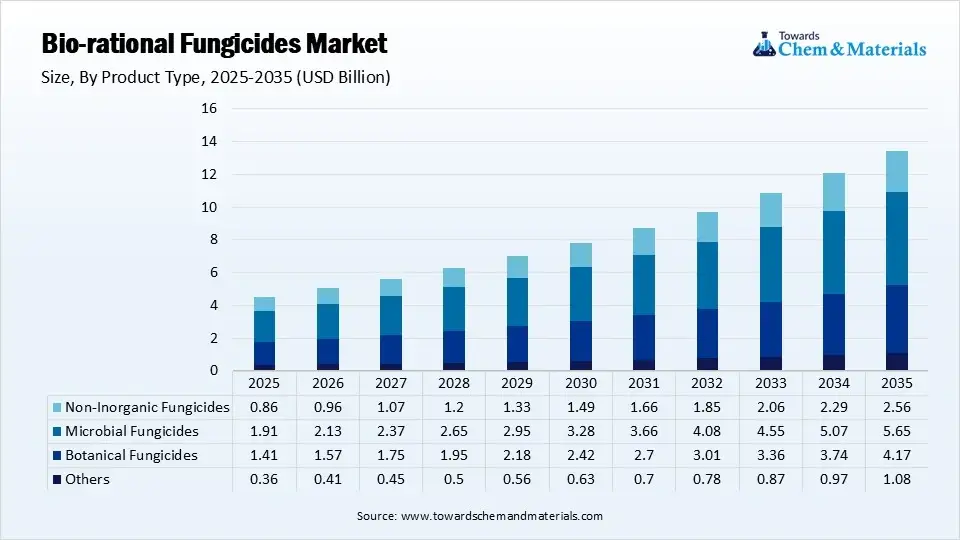

The global bio-rational fungicides market size was valued at USD 4.55 billion in 2025, is estimated to reach USD 5.07 billion in 2026, and is projected to reach USD 13.45 billion by 2035, exhibiting a compound annual growth rate (CAGR) of 11.45% over the forecast period from 2026 to 2035.North America dominated the bio-rational fungicides market with the largest revenue share of 31% in 2025 and is expected to grow at the fastest CAGR of 11.64% during the forecast period. In terms of volume, the bio-rational fungicides market is projected to grow from 413.22 thousand tons in 2025 to 1,086.49 thousand tons by 2035. growing at a CAGR of 10.15% from 2026 to 2035.The bio-rational fungicides are reshaping crop protection by combining biological actives, residue-conscious disease control and compatibility with integrated pest management, giving farmers a more sustainable way to protect yield and crop quality. The market is witnessing rapid growth as fungal diseases rise in crops, pushing farmers to adopt sustainable, eco-friendly agricultural practices that balance effective crop protection with environmental responsibility.

Market Highlights

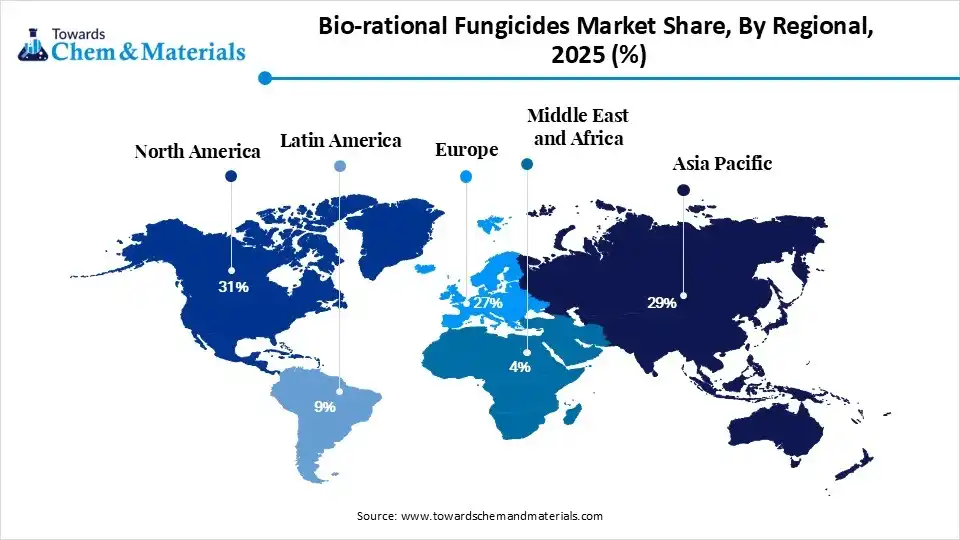

- By region, North America dominated the bio-rational fungicides market share 31% in 2025 due to a rising consumer adoption of organic and non-GMO products.

- By product type, the botanical fungicides segment dominated the bio-rational fungicides market share 31% in 2025 due to the rising demand for sustainable farming.

- By product type, the microbial fungicides segment is expected to grow at a significant rate in the market during the forecast period due to its versatility and cost-effectiveness.

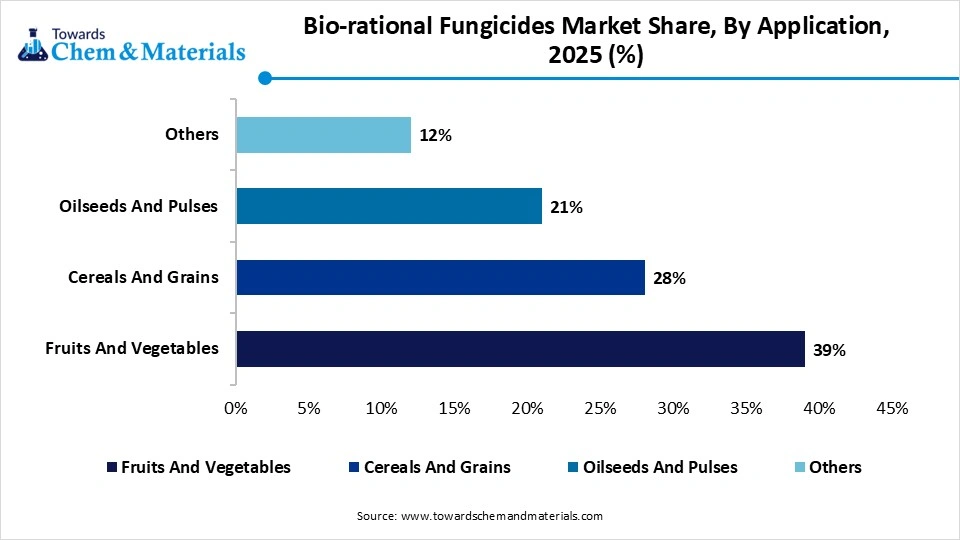

- By application, the fruits and vegetables segment dominated the market share 39% in 2025 due to rising fungal diseases.

- By mode of action, the contact segment dominated the bio-rational fungicides market with the largest share 58% in 2025 due to the growing demand for the protective barrier in crop yields.

- By formulation, the liquid segment held the dominating share in the bio-rational fungicides market share 63% in 2025 due to the ease of application.

- By end use, the agriculture segment dominated the market in share 61% 2025 due to the rising demand for food.

The bio-rational fungicides market is witnessing strong growth as agriculture gradually shifts toward effective, residue-conscious and better aligned with sustainable farming goals crop protection solutions. Bio-rational fungicides are derived from microbial strains, natural fermentation processes, plant-based extracts or mineral-based inputs. These fungicides are increasingly used to manage fungal and bacterial diseases and reduce dependence on conventional synthetic chemistries. Farmers are adopting bio-rational fungicides as they fit well within integrated pest management and organic farming systems to maintain crop quality, meet stricter residue requirements and protect soil and ecosystem health.

The rising disease burden across high-value crops such as fruits, vegetables, grapes and specialty crops, where pathogens like powdery mildew, botrytis, fusarium, rusts and leaf spots are significantly affecting yield and marketability, is creating a major growth opportunity for the market. Bio-rational fungicides are emerging as a stronger role as farmers are seeking products that can offer preventive disease control, low resistance risk and compatibility with broader sustainability programs. The market is witnessing innovations in modes of action, favorable environmental profiles, support for plant health and flexibility in both conventional and organic production systems.

- For instance, in March 2025, Certis Biologicals announced the first EU authorization of NemaClean®, reflecting how biological crop protection portfolios are expanding through new regulatory approvals and commercialization efforts. (Source: https://www.certisbio.com/)

The Power of Bio-Rational Fungicides in Sustainable Farming

Biorational fungicides are a kind of pest control product that includes biologicals, botanicals, and minerals. They are non-toxic and contain the best alternative to synthetic chemicals. These fungicides are sustainable, and they are considered as organic agriculture. Bio-rational fungicides reduce the use of synthetic fungicides and lower environmental impacts.

They target specific pathogens and lower the risk of resistance development. They enhance the growth of plants by triggering microbial activity in the soil and improving nutrient intake for healthier crop yields and plants. Diseases that control using bio-rational fungicides are alternaria, black spot, blight, fire blight, fusarium, powdery mildew, Septoria, xanthomonas, rusts, root rots, and many more.

Some minerals like iron and copper phosphate worked as fungicides. The growing demand for organic food and strong government support for the adoption of bio-rational fungicides drive the market growth. Factors like growing awareness about the harmful effects of chemical pesticides, innovations in the formulation of fungicides, and adoption of sustainable agricultural activities are responsible for bio-rational fungicides market growth.

Organic agriculture shaping bio-rational fungicides market

The growing adoption of organic agriculture increases the demand for organic farming practices. Organic farming is searching for the best alternatives to synthetic fungicides. The growing consumer demand for organic food products is driving demand for organic farming practices. These fungicides are originated from natural sources and follow principles of organic agriculture.

The growing environmental problems increase the adoption of organic farming. The rising disposable incomes of consumers allow them to pay for premium organic products that encourage farmers to adopt organic farming practices. Organic farming helps farmers to improve soil health, enhance biodiversity, and reduce environmental impact.

- For instance, In March 2024, India had 1,764,677.15 hectares of land for organic farming, and 3,627,115.82 hectares of land was going to convert into organic farming. The lower toxicity of fungicides in plants increases, and several benefits of fungicides in farming is key drivers for the growth of the market.

Bio-Rational Fungicides Market Trends

- Growing government support: Globally, governments are executing various policies, rules, and regulations that encourage the adoption of bio-rational fungicides that support market growth.

- Rising environmental concerns: The growing awareness about harmful effects of chemical pesticides on the environment that increases demand for environment friendly products.

- Rising demand for effective disease control: The bio-rational fungicides do not cause any harmful effects, and they help to control various diseases in plants.

Report Scope

| Report Attributes | Details |

| Market Size in 2026 | USD 5.07 Billion/ 455.16 Thousand Tons |

| Expected size in 2035 | USD 13.45 Billion/ 1,086.49 Thousand Tons |

| Growth Rate | 11.45% |

| Base Year in Estimation | 2025 |

| Forecast Period | 2025-2035 |

| Dominant Region | North America |

| Segment Covered | By Product Type, By Application, By Mode of Action, By End Use, By Region |

| Key Companies Profiled | BASF SE,Bayer AG,Marrone Bio Innovations, Inc.,Syngenta AG,Koppert Biological Systems,Certis Biologicals,Bioworks, Inc.,The Stockton Group,Andermatt Biocontrol AG,Valent BioSciences Corporation,Gowan Company,FMC Corporation,Nufarm Limited,Sumitomo Chemical Co., Ltd,Seipasa S.A.,Lallemand Inc.,Agrinos AS, Novozymes A/S,UPL,Koppert Biological Systems,Pro Farm Group Inc,Biobest Group,BIONEMA,Vestaron Corporation |

Bio-Rational Fungicides Market Opportunity

Technological Advancement Creating Opportunities for Bio-Rational Fungicides

Technological advancement in the bio-rational fungicides market creates a strong chance for market growth. Innovating new formulations like nano-encapsulation and novel formulations to control fungal diseases and enhance performance. The growing integration with other technologies, such as RNA interface to protect crop yields, integrated pest management to improve disease management, and precision agriculture practices to optimize agricultural activities, helps in the market growth.

The growing environmental concerns give preference to sustainable farming, which increases the demand for advancement in fungicide formulation. The growing focus on developing more efficient & effective sustainable products increases the demand for technological advancement. Technological advancement in formulations and delivery systems is creating a strong opportunity for market growth.

Bio-Rational Fungicides Market Challenge

Limited Effectiveness Hampers the Bio-Rational Fungicides Market

With the several benefits of bio-rational fungicides, the limited effectiveness of fungicides restricts the growth of the market. These are effective against different fungal infections, but not in case of specific pathogens. They require more frequent applications, and higher concentrations increase the cost for farmers.

They do not provide the same efficacy as synthetic pesticides. These fungicides are vulnerable to environmental factors like temperature fluctuations, UV radiation, and pH, which impact their effectiveness. They are less effective against a broader spectrum of fungal diseases that hampers the growth of the bio-rational fungicides market.

Supply Chain Analysis

- Raw Material Sourcing and Procurement: This stage covers the sourcing of the raw materials used to formulate bio-rational fungicides. It includes microbial strains such as Bacillus and Trichoderma, botanical extracts, mineral-based compounds, fermentation media and stabilizing ingredients. It involves biological input suppliers, microbial strain libraries, fermentation feedstock providers and natural raw material suppliers.

- Key Companies: BASF, Bayer, UPL, Syngenta, Certis Biologicals

- Chemical Synthesis and Processing: the selected biological active is produced at a scale and transformed into a stable commercial fungicide product. This includes fermentation, microbial propagation, extraction, concentration, blending, drying, liquid or wettable powder formulation and batch production. These processes take place in biological manufacturing plants, fermentation facilities, formulation units and quality-controlled production sites.

- Key Companies: Certis Biologicals, UPL, BASF, Bayer, Syngenta

- Quality Testing and Certification: This includes verification of fungicides to meet the required standards for efficacy, microbial purity, shelf life, formulation stability and safe agricultural use. It includes microbial count analysis, contamination screening, batch consistency checks, stability studies, residue-related validation and certification for organic suitability.

- Key Companies: BASF, Bayer, Syngenta, UPL, Certis Biologicals

- Packaging and Labeling: the formulated fungicide is packaged into commercial formats and prepared for sale with the required product-use information. It includes filling, sealing, pack sizing, storage labeling, dosage instructions, crop-use recommendations, safety guidance and compatibility instructions.

- Key Companies: BASF, Bayer, UPL, Certis Biologicals, Syngenta

- Distribution: the formulated, packaged and labelled fungicides are distributed to growers and supported through agronomic advice. It includes distribution through agri-input dealers, cooperatives, direct sales channels, crop advisors and field demonstration programs.

- Key Companies: BASF, Certis Biologicals, Syngenta, Bayer, UPL

Regional Analysis

What are the Advancements in the Bio-rational Fungicides Market in North America?

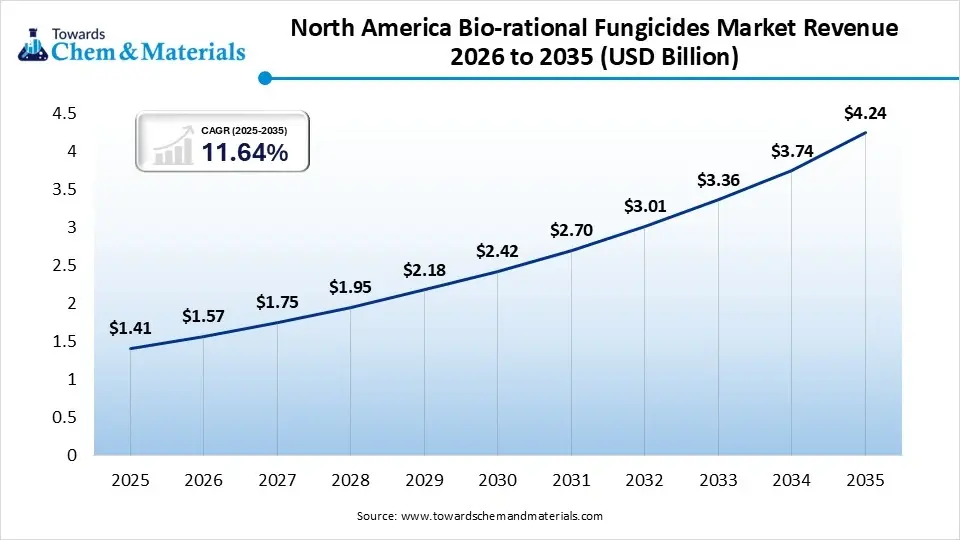

The North America bio-rational fungicides market size was estimated at USD 1.41 billion in 2025 and is projected to reach USD 4.24 billion by 2035, growing at a CAGR of 11.64% from 2026 to 2035.North America dominated the market with the largest share of 31% in 2025. The dominance of the region can be attributed to strong biological crop protection adoption, which supports growth. Regulatory approvals encourage market expansion. Sustainable farming drives demand. Farmers are increasingly seeking tools that can complement conventional fungicides and extend resistance management programs. The region has a strong pace of product registrations and commercial launches. The region has a well-developed network of agronomic advisors, retail distributors, seed-treatment providers and crop input companies.

United States

- The U.S. offers a favorable environment for adoption because farmers are increasingly under pressure to manage fungicide resistance, soil health and yield protection.

- The country is involved in producing high-value crops, which require high disease protection, increasing the adoption of the market.

- The rising adoption of organic farming and precision farming in the country supports market growth.

Canada

- The country is witnessing the rising commercial availability of biological and botanical fungicides for Canadian farmers.

- Major crop protection companies are expanding biological platforms in the country rather than treating them as side applications.

- One of the major market trends includes the broadening of biological fungicide use beyond greenhouse or specialty crops into mainstream field-crop programs.

How is the Asia Pacific Bio-rational Fungicides Market Growing?

Asia Pacific held a market share of 29% in 2025 and was expected to grow at the fastest CAGR of 13.2% over the forecast period. The growth of the region can be credited to expanding agricultural production, which drives demand, rising awareness of biological solutions supports adoption, and government sustainability initiatives encourage growth. The region is witnessing evolving specialty crops and export-oriented agriculture, which creates a favorable environment for bio-rational fungicides. The regional market is being shaped by a mix of climate-driven disease pressure, rising resistance concerns and a gradual shift toward more sustainable disease-control strategies.

Japan

- The country reflects high-value crop systems, strong product-quality expectations and a growing need for advanced resistance-management solutions.

- The country has a significant focus on tea, fruits, vegetables, rice and horticulture crops, which are highly sensitive to fungal disease, driving demand for the market.

- Companies in the country are investing in new chemistry, resistance management tools and sustainability-oriented disease control solutions.

China

- The country has a growing emphasis on innovation-led fungicide launches for high-value and high-risk crops, especially where disease resistance has become a challenge.

- The rising role of biological and bio-based crop protection within broader sustainability programs is creating new opportunities for the market.

- China’s fungicide market is becoming more resistance-management focused.

How is the Europe Bio-rational Fungicides Market Expanding?

Europe held a market share of 27% in 2025. The Europe bio-rational fungicides market is steadily growing. The growth of the region can be credited to strict pesticide regulations that support bio-rational products. Organic farming expansion increases the adoption of the market. Sustainability initiatives strengthen market demand. The region is witnessing an increasing shift toward a more balanced crop protection approach, combining disease control with residue management, resistance control and sustainability goals. The region is heavily investing in commercial crops, boosting market adoption. The region has a strong manufacturing and innovation base for biological crop protection.

France

- France reflects high-value crop exposure, strong sustainability pressure and active biological product development.

- The country has a large agricultural base spanning vineyards, fruits, vegetables, cereals and oilseeds, which demand flexible disease management tools.

- The country benefits from the presence of companies and partnerships focused on biological crop protection innovation.

Germany

- The country is investing heavily in localized biological crop protection manufacturing.

- Germany is seeing broader crop-level access to biological fungicides, particularly in specialty crops.

- Resistance management is becoming a stronger driver for bio-rational fungicide adoption.

What are the Key Trends in the Bio-rational Fungicides Market in Latin America?

Latin America held a market share of 9% in 2025. The growth of the region can be credited to export-oriented agriculture, which increases bio-rational fungicide use. Disease management needs for the high-value crops support the adoption of the market. Sustainable farming expands market opportunities. The region combines intense fungal pressure, large export-oriented horticulture and rising interest in resistance and residue management. Across the region, farmers are dealing with humid growing conditions, long crop cycles and disease-heavy environments, boosting adoption of bio-rational fungicides. Companies in the region are focusing on the production of biological and lower-residue fungicides.

") Brazil

Brazil

- Brazil has a large agricultural scale, year-round disease pressure and rapid adoption of biological inputs across crop protection.

- The region is investing in organic production and residue management. The farmers are seeking solutions that can help maintain export quality, reduce resistance pressure and fit more sustainably into intensive horticulture systems.

- The market is driven by crop diversity, export orientation and growing comfort with biological crop protection technologies.

Chile

- The stronger commercialization of botanical fungicides through local distribution alliances is driving the market.

- The country is becoming a launchpad for locally adapted biological crop-protection solutions.

- The rising use of bio-rational products in fruit-export systems where postharvest quality matters as much as disease suppression is accelerating market adoption.

How is the Middle East and Africa Region Growing in the Bio-rational Fungicides Market?

The Middle East and Africa held a market share of 4% in 2025. The growth of the region can be credited to agricultural modernization programs, which increase product penetration. Protected cultivation boosts demand for the market. Food security initiatives support the adoption of the market. The region is witnessing steady growth in the market. The farmers across the region are seeking disease management tools that balance productivity, crop quality and sustainability. The region is a mix of high-value horticulture, protected cultivation, export-focused fruit and vegetable production and staple crop farming, accelerating market growth. The region is represented as a secondary market for standard fungicides, where biological disease control solutions can be commercialized for greenhouse and specialty crop systems.

Bio-rational Fungicides Market Share, By Regional, 2025 (%)

| Regional | Revenue Share, 2025 (%) |

| North America | 31% |

| Europe | 27% |

| Asia-Pacific | 29% |

| Latin America | 9% |

| Middle East & Africa | 4% |

South Africa

- South Africa has a commercial-scale horticulture, export-oriented fruit production and a relatively advanced crop protection distribution system.

- The country has strong distribution channels, farmer awareness and regulatory pathways for biological crop protection.

- Companies are expanding their biological portfolios across disease management.

Saudi Arabia

- The country is witnessing an institutional push toward biological pest control and IPM.

- Bio-rational crop protection in the country is being driven from the top down through sustainability and food-security programs.

- The country expresses a broader interest in biotechnology-based agricultural inputs.

Segmental Insights

By Product Type

The botanical fungicides segment dominated the bio-rational fungicides market share 31% in 2025. The easy availability and natural origin support sustainable and environment-friendly farming, which drives the market growth. These fungicides are originated from plants like neem or pyrethrum. The rising demand for eco-friendly and sustainable products promotes the growth of the market.

") The rising applications in crop protection, organic farming, and increased fungal diseases in crop yields demand bio-rational fungicides. Furthermore, the biodegradable nature of many botanical fungicides and lower risks to human health and other organisms drive the growth of the market.

The rising applications in crop protection, organic farming, and increased fungal diseases in crop yields demand bio-rational fungicides. Furthermore, the biodegradable nature of many botanical fungicides and lower risks to human health and other organisms drive the growth of the market.

The microbial fungicides segment expects the significant growth in the market during the forecast period. The wide applications in various plant pathogens and the growing adoption of sustainable agricultural practices drive the market growth. These fungicides, like bacillus subtilis, trichoderma species, and many more, originate from bacteria, fungi, and viruses. The ability of some microbial fungicides to stimulate growth and enhance nutrient uptake increases the demand for microbial fungicides. The cost-effectiveness and versatility in a wide range of plant diseases drive the market growth.

Bio-rational Fungicides Market Share,By Product Type, 2025 (%)

| By Product Type | Revenue Share, 2025 (%) |

| Botanical Fungicides | 31% |

| Microbial Fungicides | 42% |

| Non-Inorganic Fungicides | 19% |

| Others | 8% |

By Application

The fruits and vegetables segment held the dominating share of the bio-rational fungicides market share 39% in 2025. The growing fungal diseases in fruits and vegetables and rising consumer adoption of organic and environment-friendly options drive the market growth. The rising adoption of sustainable farming options due to the adverse effect of chemicals promotes market growth.

These fungicides are used in storage to protect fruits and vegetables from fungal rots. The rising need to minimize the presence of synthetic chemicals and meet regulatory requirements drives the market growth.

") The cereals and grains segment expects the fastest growth in the market during the forecast period. The rising food demand globally and high chances of fungal diseases in these crops drive the growth of the market. Crops like wheat, barley, oat, rice, and millet are highly prone to diseases that increase the demand for bio-rational fungicides.

The cereals and grains segment expects the fastest growth in the market during the forecast period. The rising food demand globally and high chances of fungal diseases in these crops drive the growth of the market. Crops like wheat, barley, oat, rice, and millet are highly prone to diseases that increase the demand for bio-rational fungicides.

Fungal pathogens like rusts, smuts, and blights can cause damage to cereal crop yields. Bio-rational fungicides are used in the storage of grains due to spoilage and production of mycotoxins. The growing food security demand and rising adoption of sustainable agricultural practices in cereals and grain crops drive the market growth.

Bio-rational Fungicides Market Share,By Application, 2025 (%)

| By Application | Revenue Share, 2025 (%) |

| Fruits And Vegetables | 39% |

| Cereals And Grains | 28% |

| Oilseeds And Pulses | 21% |

| Others | 12% |

By Mode Of Action

The contact segment dominated the market with the largest share share 58% in 2025. The direct killing or hindering the growth of fungi on crop yields or plant surfaces drives the market growth. Easy applications like foliar sprays and farmers quickly and efficiently treat affected plants increases demand for contact fungicides.

The ability of these fungicides to provide faster response in integrated pest management drives the market growth. The rising demand for protective barriers on plant surfaces to protect from fungal infection supports the market growth. The rising demand for versatile tools for crop protection and cost-effectiveness propels the market growth.

The systematic segment is expected to grow at the significant rate in the market during the forecast period. The growing awareness regarding the fungicides and protection against accelerate the growth of the market.

These fungicides are absorbed into crop yields and distributed into tissues. The long-term protection and property of controlling fungal diseases that are present inside the plant promote market growth. These fungicides require less frequent application and are effective against soilborne pathogens that infect plants from roots, fueling market growth.

Bio-rational Fungicides Market Share,By Mode Of Action, 2025 (%)

| By Mode Of Action | Revenue Share, 2025 (%) |

| Contact | 58% |

| Systematic | 42% |

By Formulation

The liquid segment held the dominating share of the bio-rational fungicides market share 63% in 2025. The ease of application, such as being easily mixed with water and other chemicals and growing large-scale farming, drives the market growth. The versatility of use, like sprayers and irrigation systems, and its effectiveness in crop yield protection further drive the market growth.

The wide applications in seeds, fruits, vegetables, tubers, and ornamental plants and its availability in various formulations like wettable powders, flowables, and concentrates contribute to the overall growth of the market.

The dry segment expects the significant growth in the market during the forecast period. The dry fungicides have a long shelf life and are easy to store & transport, which drives the market growth. They are available in powder or granular form and are applied using conventional equipment. They are applied to soil to preserve the crown and root of plants.

They are ready to use and can be directly applied to crops and are easily mixed with water. Furthermore, the lower transportation cost and less packaging overall all these factors drives the market growth.

Bio-rational Fungicides Market Share,By Formulation, 2025 (%)

| By Formulation | Revenue Share, 2025 (%) |

| Liquid | 63% |

| Dry | 37% |

By End Use

The agriculture segment dominated the bio-rational fungicides market share 61% in 2025. The rapid growth in global population increases the demand for food, which increases the production of crop yield, which helps in market growth. The rising awareness about health problems caused by synthetic chemicals and growing environmental concerns increases the demand for bio-rational fungicides.

The rising adoption of sustainable farming practices and the growing demand for organic food drive the market growth. Crops like cereals and grains are prone to fungal diseases, and strong government support promotes market growth. The lower environmental impact and lower toxicity levels because they are originated from natural sources further drive the market growth.

The horticulture segment expects the significant growth during the forecast period. The rising demand for controlling fungal diseases in greenhouse or outdoor settings drives the market growth. The rising consumer demand for organic and residue-free products increases the adoption of natural alternatives like bio-rational fungicides.

They are used to control root & crown diseases, prevent fungal diseases, and are effective against soil-borne diseases. The rising consumer demand for horticulture products like vegetables, fruits, medicinal plants, flowers, nuts, spices, and ornamental plants drives the growth of the market.

Bio-rational Fungicides Market Share,By End Use, 2025 (%)

| By End Use | Revenue Share, 2025 (%) |

| Agriculture | 61% |

| Horiculture | 21% |

| Turf and Ornamentals | 12% |

| Others | 6% |

Bio-Rational Fungicides Market Recent Developments

Syngenta

- Launch: In August 2024, Syngenta introduced Miravis Duo and Reflect Top two fungicides for rice in the Indian market. Miravis Duo is made for use in groundnut, grape, tomato, and chili, and it is powered by ADEPIDYN technology. Reflect Top is made for rice, and it contains double-binding technology and supports Indian farmers in providing healthier and productive rice crops. It protects against powdery mildew, antharacnose, and leaf spots.

FMC Corporation

- Launch: In June 2024, FMC India introduced fungicides for fruits and vegetables named Velzo and Cosuit. These fungicides are manufactured using superior formulations and it control fungi diseases of fruits and vegetables. The company develops new tools to improve productivity in agriculture.

BASF SE

- Launch: In August 2024, BASF launched a fungicide management spray timer tool. This tool provides alerts to users on a timely basis by understanding the existing disease situation, disease prediction modelling, and advanced growth stage. The tool suggests the best time for the application of fungicides. The spray timer tool helps farmers to control disease and improve investment in fungicide.

Recent Developments

- In February 2025, Syngenta made one of the biggest moves in the biologicals space by acquiring Novartis' natural compounds and genetic strains repository and opening a new biologicals production facility in Orangeburg, South Carolina. (Source: https://www.syngenta.com/)

- In December 2025, UPL announced a California label expansion for Lepigen® bioinsecticide, adding nine new specialty crops, including rice, strawberries, tree nuts and apples. This is a remarkable development for the bio-rational fungicides market. (Source: https://news.agropages.com/)

Bio-Rational Fungicides Market Top Companies List

- BASF SE

- Bayer AG

- Marrone Bio Innovations, Inc.

- Syngenta AG

- Koppert Biological Systems

- Certis Biologicals

- Bioworks, Inc.

- The Stockton Group

- Andermatt Biocontrol AG

- Valent BioSciences Corporation

- Gowan Company

- FMC Corporation

- Nufarm Limited

- Sumitomo Chemical Co., Ltd

- Seipasa S.A.

- Lallemand Inc.

- Agrinos AS

- Novozymes A/S

- UPL

- Koppert Biological Systems

- Pro Farm Group Inc

- Biobest Group

- BIONEMA

- Vestaron Corporation

Segments Covered in the Report

By Product Type

- Botanical Fungicides

- Neem-Based Fungicides

- Essential Oil-Based Fungicides

- Plant Extract-Based Fungicides

- Microbial Fungicides

- Bacillus-Based

- Trichoderma-Based

- Pseudomonas-Based

- Other Microbial Strains

- Non-Inorganic Fungicides

- Mineral-Based Fungicides

- Sulfur-Based Fungicides

- Copper-Based Bio-rational Fungicides

- Others

- Biochemical Fungicides

- Fermentation-Derived Products

By Application

- Fruits And Vegetables

- Fruits

- Vegetables

- Greenhouse Crops

- Cereals And Grains

- Wheat

- Rice

- Corn

- Barley

- Oilseeds And Pulses

- Soybean

- Canola

- Pulses

- Others

- Plantation Crops

- Turf Crops

- Industrial Crops

By Mode Of Action

- Contact

- Protective Fungicides

- Surface Acting Fungicides

- Systematic

- Xylem Mobile

- Translaminar

By Formulation

- Liquid

- Suspension Concentrates

- Emulsifiable Concentrates

- Liquid Bioformulations

- Dry

- Wettable Powders

- Granules

- Water Dispersible Powders

By End Use

- Agriculture

- Field Crops

- Commercial Crops

- Horiculture

- Floriculture

- Nursery Crops

- Protected Cultivation

- Turf and Ornamentals

- Turf Management

- Landscape Ornamentals

- Others

- Forestry

- Public Green Spaces

By Regional

- North America

- Asia Pacific

- Europe

- Middle East & Africa

- Latin America

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

FAQ's

Select User License to Buy

Figures (7)