Content

What is Bio-Based Textiles Market Size and Share?

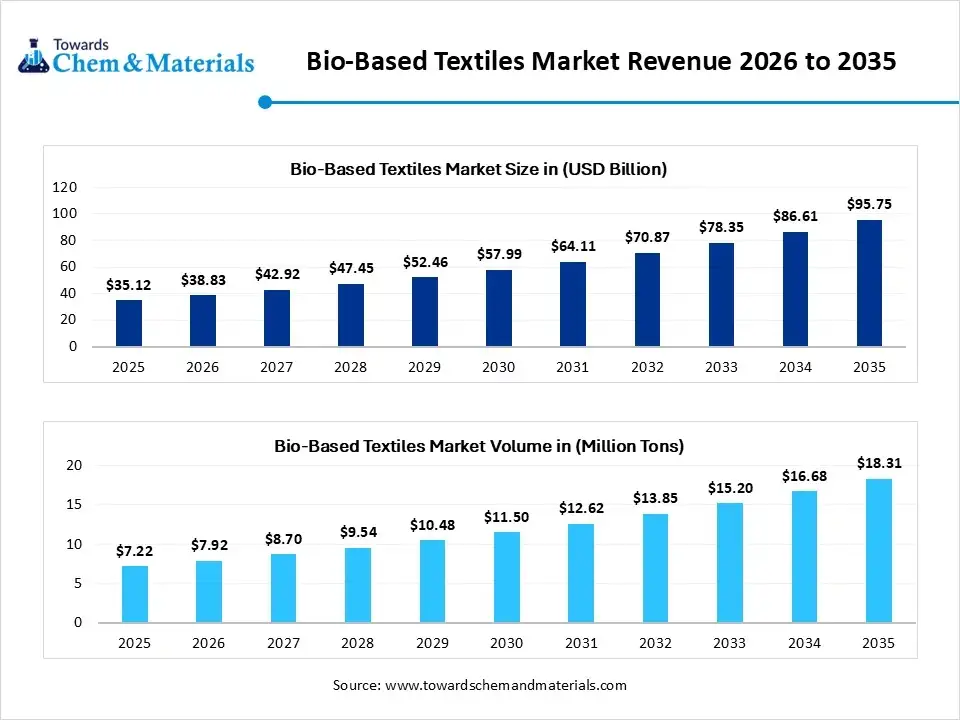

The global bio-based textiles market size was valued at USD 35.12 billion in 2025, is estimated to reach USD 38.83 billion in 2026, and is projected to reach USD 95.75 billion by 2035, exhibiting a compound annual growth rate (CAGR) of 10.55% over the forecast period from 2026 to 2035.Asia Pacific dominated the bio-based textiles market with the largest revenue share of 41% in 2025 and is expected to grow at the fastest CAGR of 10.68% during the forecast period. In terms of volume, the bio-based textiles market is projected to grow from 7.22 million tons in 2025 to 18.31 million tons by 2035. growing at a CAGR of 9.75% from 2026 to 2035.This growth relies on a shift away from traditional petroleum-based fabrics like polyester. The primary drivers accelerating this transition include consumer demand, stricter government rules, and new material technologies. Major players like BASF SE, Ralph Lauren, PVH Corp, and Reformation joined Materiom; these partnerships aim to solve problems and supply, according to the report.

Market Highlights

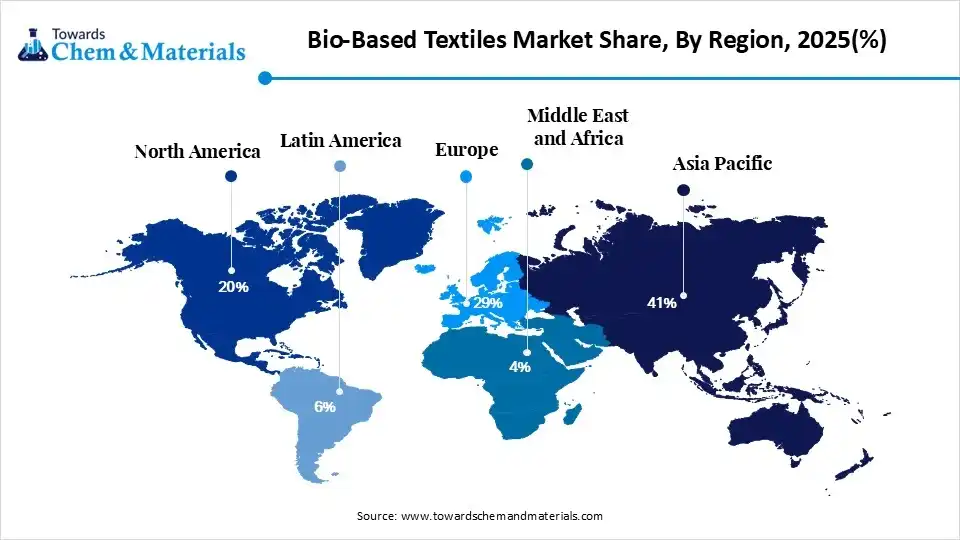

- By region, Asia Pacific dominated the market with a share of 41% in 2025. Large textile manufacturing capacity and abundant biomass resources support production.

- By region, North America held 20% market share in 2025 and is expected to experience the fastest growth with a CAGR of 13.1% in the forecast period. Corporate ESG commitments and consumer demand increase adoption.

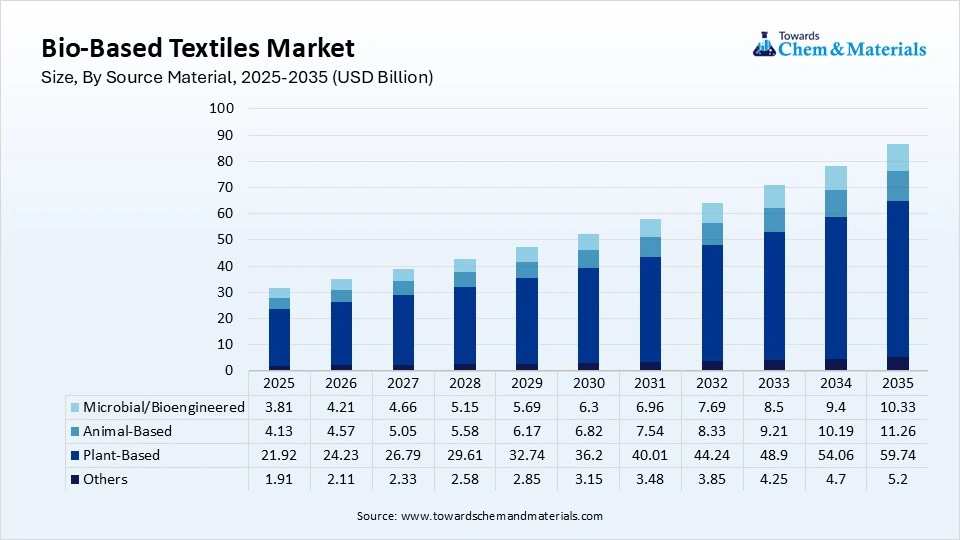

- By source material, the plant-based segment dominated the market with a 69% share in 2025. Driven by sustainable fashion regulations and expanding renewable fiber production.

- By source material, the microbial/bioengineered segment held 12% market share in 2025 and is expected to have the fastest growth with a CAGR of 18.50% in the forecast period. Biotechnology innovations accelerate the commercialization of next-generation fibers.

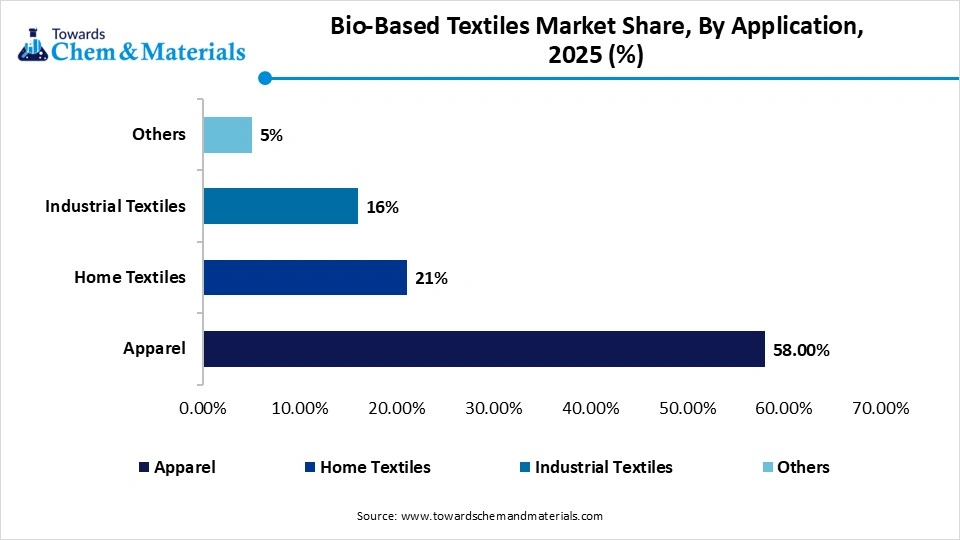

- By application, the apparel segment dominated the market with a 58% share in 2025. Fashion brands rapidly adopt sustainable fibers to reduce environmental footprints.

- By application, the home textiles segment held 21% market share in 2025 and is expected to have the fastest growth with a CAGR of 13.60% in the forecast period. Green building trends and sustainable home furnishings expand consumption.

Market Overview

Bio-Based Textiles Market: Replacement of Petroleum-Derived Fabrics

The bio-based textiles market is important because it replaces petroleum-derived fabrics like polyester with materials from renewable sources such as plants, fungi, and agricultural waste. This transition reduces carbon emissions, lowers plastic pollution, and promotes a more sustainable fashion and manufacturing industry. Since most clothing is made from oil, using natural materials instead not only conserves oil but also decreases pollution. Producing bio-based fibers generally results in fewer greenhouse gases compared to synthetic fibers. Some raw materials like algae or fungal mycelium absorb carbon dioxide as they grow.

Additionally, many bio-based fabrics utilize food waste, such as pineapple leaves or banana stems, helping reduce waste and providing farmers with extra income. Unlike cotton, which requires extensive water and land, bio-based crops like hemp or flax need significantly less water and no harmful chemicals. Many of these fabrics are biodegradable, meaning they decompose naturally like food, unlike plastic fabrics that persist in landfills for centuries. By using agricultural by-products, such as pineapple leaves or banana stems, these materials promote upcycling waste instead of using fresh water.

- For instance, the Stretching Circularity Project, initiated by Fashion for Good, this project validates bio-based and recycled elastane alternatives to remove technical recycling barriers in stretch clothing. (Source:www.fashionforgood.com)

Market Trends:

- The versatile product launch has driven industry growth in recent years. Several major brands are increasingly seen in launching wide product lines to gain industry attention in the current period.

- The increased demand for eco-friendly and recyclability-labeled clothing is contributing to the industry's growth in recent years. Moreover, this trend is encouraging manufacturers to adopt clean manufacturing processes in the coming years.

Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 54.21 Billion |

| Market Size by 2034 | USD 113.43 Billion |

| Growth rate from 2024 to 2025 | CAGR 8.55% |

| Base Year of Estimation | 2024 |

| Forecast Period | 2025 - 2034 |

| Dominant Region | Europe |

| Segment Covered | By Fiber Type, By Source of Raw Material, By Application, By End-User, By Distribution Channel, By Processing Method, By Region |

| Key Profiled Companies | Lenzing AG, DuPont Biomaterials, NatureWorks LLC, Teijin Limited, Grasim Industries Ltd (Aditya Birla Group), BASF SE, Evonik Industries, Eastman Chemical Company, Covation Biomaterials, Toray Industries Inc., Ananas Anam (Piñatex), Orange Fiber, Bolt Threads, MycoWorks, Spiber Inc., Natural Fiber Welding (NFW), Circular System, Pangaia, Ecoalf, Greenfibres |

Eco-Friendly Fabrics Carve a Niche in Non-Apparel Markets

The expansion into the non-apparel segment, like automotive interiors, medical fabrics, and upholstery, is expected to create lucrative opportunities for the manufacturers in the coming years. Moreover, with the increased need for comfort and sustainability, biobased textiles can gain major market share in sectors like healthcare, transport, and construction for the wide applications in the coming years, as per the industry expectations.

Maintaining the Green Standards Increases Operational Cost for Producers

The high price of production is expected to hinder the industry's growth in the coming years, as biobased textiles production can be expensive compared to synthetic materials, akin to factors such as the outsourcing of raw materials, the maintenance of sustainability, and several others. However, the manufacturer can take advantage of the technological advancements, such as the implementation of automation in their manufacturing plant, and other benefits.

Supply Chain Analysis of Bio-Based Textiles Market

Chemical Synthesis and Processing

- Bio-based textiles replace oil-based synthetics with renewable resources like plants, agricultural waste, and microbes. Production extracts natural polymers (like cellulose) or ferments biomass into basic building blocks called monomers. These are then spun into soft, biodegradable fabrics for everyday clothing.

- The Lenzing Group is an Austrian company that manufactures wood-based, biodegradable cellulose fibers used in the textile and nonwovens industries. Headquartered in Lenzing, Austria, they are an industry leader in sustainability, transforming renewable wood pulp into eco-friendly fibers like TENCEL, LENZING ECOVERO, and VEOCEL.

- Key players: Lenzing, NatureWorkd, Spinnova, Eastman

Quality Testing and Certification

- Bio-based textile testing checks if fabrics are truly made from natural, renewable plants rather than fossil fuels. Labs use radiocarbon tests to measure this content. Organizations then provide official seals. These labels prove to buyers that the products are eco-friendly.

- Spinnova develops biobased textile fibers manufactured without harmful dissolving chemicals and supports compliance with international sustainability and textile quality standards.

- Key Authorities and standards: International Organization for Standardization, OLO-TEX, Global Organic Textile Standard, Forest Stewardship Council.

Distribution to Industrial Users

- Industrial users distribute these fabrics for auto parts, medical supplies, and protective clothing. High-demand variants include polylactic acid (PLA), rayon, and regenerated cellulose. Distributors bridge the gap between raw material suppliers and commercial factories.

- NatureWorkd supplies PLA biopolymer materials used to produce bio-based textile fibers for apparel, hygiene products, and nonwoven fabrics, helping manufacturers reduce reliance on fossil-based synthetic fibers while supporting sustainability goals.

- Key players: Architectural Plastics Inc. and Arkay Plastics Inc.

Regional Insights

How did Asia Pacific dominate the Bio-Based Textiles Market in 2025?

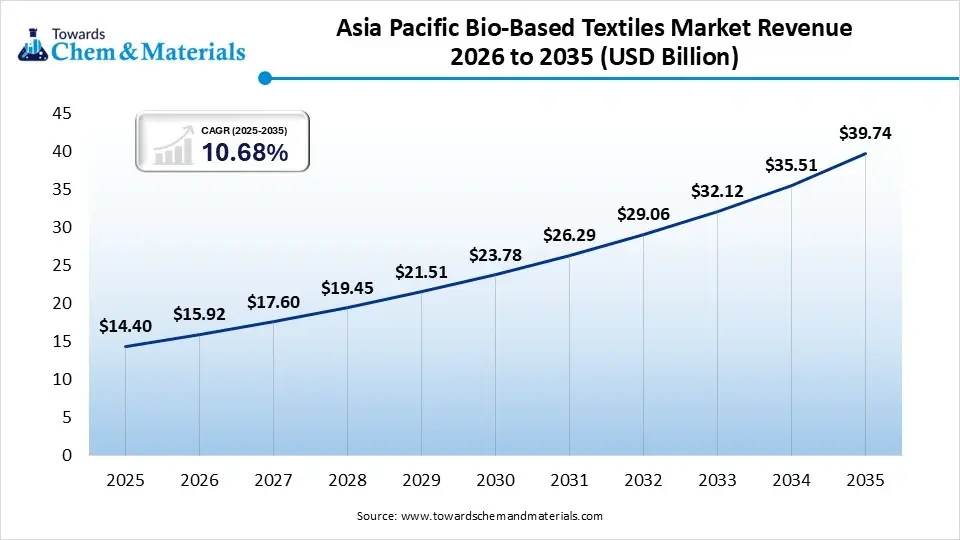

The Asia Pacific bio-based textiles market size was estimated at USD 14.40 billion in 2025 and is projected to reach USD 39.74 billion by 2035, growing at a CAGR of 10.68% from 2026 to 2035.Asia Pacific dominated the market with the largest share of 41% in 2025. The region secured this leadership through its massive manufacturing infrastructure, abundant plant-based raw materials, and strong government support for sustainable production. Countries like China and India operate the world's largest spinning, weaving, and finishing facilities. This established, vertically integrated supply chain enables highly efficient, low-cost production of plant-based fibers like organic cotton and bamboo.

") China

China

- Strict environmental policies and carbon-reduction goals are forcing domestic manufacturers to adopt sustainable production methods.

- Chinese companies are investing heavily in advanced, closed-loop technologies (like Lyocell) to produce high-quality biodegradable fabrics.

India

- Strict laws in places like Europe push brands to look for biodegradable and renewable materials. India makes 74% of the world's organic clothing, putting the country in a strong position.

- The Indian government helps through programs like PM MITRA and A-TUFS. These plans boost green technology and improve global competitiveness.

North America Bio-Based Textiles Market Growth Factor

North America held a market share of 20% in 2025 and is expected to grow at the fastest CAGR of 13.1% over the forecast period, expanding rapidly due to consumer demand for sustainable fashion, stricter environmental regulations, and investments in bio-materials. This shift helps reduce the industry's reliance on fossil-fuel-based synthetics. Strict bans in states like California and New York restrict toxic chemicals (like certain water-repellent finishes), pushing companies to adopt renewable or bio-based solutions. Major brands in the region are committing to reducing their carbon footprints to fight climate change. These factors drive the growth of the market in the region.

United States

- State and federal laws mandate strict supplier audits and ban toxic chemicals in textiles. For example, states like California and New York restrict the use of petroleum-based, water-repellent coatings. These bans force brands to switch to bio-based alternatives.

- Major U.S. companies commit to long-term sustainability targets. They replace standard polyester with bio-based or recycled polyester to shrink their carbon footprints. Brands partner with fiber innovators to secure a green supply chain.

Canada

- The Canadian government enforces strict rules on plastic pollution and single-use items. This forces companies to find natural, biodegradable textiles.

- Canadians are highly aware of the environmental damage caused by "fast fashion". Many shoppers actively choose organic cotton, hemp, or bio-synthetics, and are willing to pay more for sustainable clothing.

Europe Bio-Based Textiles Market Growth Factor

Europe held a market share of 29% in 2025, driven by strict government regulations, high consumer demand for eco-friendly fashion, and a push to reduce reliance on fossil fuels. The European Union (EU) leads global revenue shares in this sector due to aggressive sustainability programs. Policies like the EU Green Deal and the Circular Economy Action Plan force manufacturers to minimize environmental waste. European shoppers increasingly demand transparency in clothing production. They actively choose garments made from renewable materials over synthetic, fossil-based alternatives.

Germany

- The EU circular economy action plan and Germany's sustainable plans and laws for a clear and more competitive Europe, for reducing pressure on natural resources, which fuels the growth.

- Major German brands adopt bio-based textiles to meet corporate social responsibility targets. They want to comply with extended producer responsibility regulations, supporting growth.

France

- People in France care a lot about the planet. Young shoppers and eco-conscious buyers want clothes made from plants or lab-grown materials. These materials include organic cotton, hemp, and lab-grown mushroom leather.

- The European Union requires companies to be more sustainable. France has rules that cut down on waste and support circular fashion. A circular economy means clothes are made, worn, and then recycled or reused rather than thrown away.

- French companies are transforming natural resources into eco-friendly fabrics, which are backed by strict laws, and boosting sustainable fashion is a growing trend in the country.

Latin America Bio-Based Textiles Market Growth Factor

Latin America held a market share of 6% in 2025, driven by growing consumer demand for eco-friendly and natural materials in the manufacturing of sustainable clothing, aligning with rising environmental concerns and driving market growth. The presence of abundant natural resources like cotton, wool, and alpaca, and agricultural innovation further increases the demand. Key hubs like Colombia and Brazil are expanding their textile mills to meet increasing consumer demand, driving further growth and expansion of the regional market.

Brazil

- In Brazil, the innovation in the textile market by companies like Muush, which grows mushroom roots on Brazilian farm waste, creating flexible leather-like fabric that is mycelium leather, is expanding the use of bio-based textiles, fueling growth in the market.

- Brazil is a top global exporter of cotton, along with the largest producer of silk, heavily relying on a circular farming economy. This drives the growth of the market in the country.

Argentina

- Some local brands source plant-based yarns in partnership with indigenous communities. For example, Coruja makes 100% plant-based yarn co-produced with the Qom community in Chaco.

- Emerging biotech organizations like Fiberly operating in Argentina and France are pioneering ways to turn leftover cotton waste into wearable, sustainable cellulose fibers.

- Argentina has hundreds of native cactus species. Scientists and local designers are finding ways to harvest cactus waste and turn it into vegan leather alternatives that are similar to those produced by DESSERTO Cactus Leather Alternative Recycled Line Navy Blue.

Middle East & Africa Bio-Based Textiles Market Growth Factor

The Middle East & Africa held a market share of 4% in 2025, due to rising environmental awareness, shifting consumer preferences toward sustainable fashion, and government economic diversification initiatives. This shift helps reduce the carbon footprint of traditional clothing. Many manufacturers export their textiles to Europe. Since the European Union has strict rules on carbon emissions, MEA producers must make bio-based or recycled textiles to keep those customers. Countries in the Middle East, like the United Arab Emirates, are building textile trade hubs. African nations like Ethiopia and Kenya are growing as manufacturing centers. Governments offer tax breaks and build eco-friendly industrial parks to attract business.

Saudi Arabia

Saudi Arabia

- Government support like Vision 2030, which prioritizes reducing carbon footprints. The government regulates and promotes eco-friendly textile alternatives over petroleum-based synthetics.

- Major Saudi companies like SABIC are developing bio-based chemical solutions. These innovations cut water use in the textile dyeing process by 30%.

UAE

- The UAE has a massive, brand-conscious luxury fashion market. Consumers are increasingly willing to pay a premium for certified, cruelty-free, and earth-friendly fabrics.

- The UAE’s booming hotel industry prioritizes green practices. Eco-conscious hotels adopt bio-based textiles such as organic cotton or biodegradable bedding and towels to reduce their carbon footprint.

Segmental Insights

Source Material Insights

The plant-based segment accounted for the largest share of the bio-based textiles market in 2024, capturing 63.9% of total revenue. Its strong market position is supported by the long-standing use of natural fibers such as cotton, flax (linen), hemp, and bamboo, along with well-established farming and supply networks. These materials are widely valued for being biodegradable, renewable, and having a lower environmental footprint than conventional synthetic fibers. Their softness, breathability, durability, and versatility have made them a preferred choice for clothing, home furnishings, and other textile products. Continuous improvements in farming methods, fiber processing, and manufacturing technologies have also enhanced the quality, consistency, and availability of plant-based textiles, helping the segment maintain its market leadership.

") The microbial and bioengineered textiles segment is projected to register the fastest growth over the forecast period. These advanced textiles are created using microorganisms such as bacteria, yeast, and algae to produce innovative fibers, including bacterial cellulose and bioengineered protein-based materials like spider silk. Compared to traditional fiber production, these methods require significantly less water, land, and chemical inputs, making them a more sustainable alternative. In addition to being biodegradable, bioengineered textiles can be developed with customized characteristics such as enhanced strength, flexibility, durability, and moisture management. As sustainability becomes a key priority for both consumers and fashion companies, the demand for these next-generation materials continues to increase. Their compatibility with circular economy principles and ongoing technological advancements are expected to accelerate their adoption across the textile industry.

The microbial and bioengineered textiles segment is projected to register the fastest growth over the forecast period. These advanced textiles are created using microorganisms such as bacteria, yeast, and algae to produce innovative fibers, including bacterial cellulose and bioengineered protein-based materials like spider silk. Compared to traditional fiber production, these methods require significantly less water, land, and chemical inputs, making them a more sustainable alternative. In addition to being biodegradable, bioengineered textiles can be developed with customized characteristics such as enhanced strength, flexibility, durability, and moisture management. As sustainability becomes a key priority for both consumers and fashion companies, the demand for these next-generation materials continues to increase. Their compatibility with circular economy principles and ongoing technological advancements are expected to accelerate their adoption across the textile industry.

Application Insights

The apparel segment dominated the market in 2024, accounting for 51.2% of total revenue. The growth of this segment is being driven by increasing consumer interest in sustainable fashion and the rising popularity of environmentally responsible clothing. Fashion brands across premium and mass-market categories are incorporating bio-based materials such as organic cotton, hemp, and bamboo into their product lines to meet growing environmental and ethical expectations. Consumers are becoming more conscious of the environmental impact of their purchasing decisions, encouraging brands to expand their use of renewable and biodegradable textile materials. The segment also benefits from mature global manufacturing networks and effective marketing efforts that emphasize the sustainability advantages of bio-based apparel.

The home textiles segment is expected to witness the fastest growth during the forecast period. Demand for eco-friendly household products, including bed sheets, curtains, towels, carpets, and upholstery fabrics, is increasing as consumers look for more sustainable options for their homes. Furniture manufacturers, interior designers, and home décor brands are increasingly adopting bio-based fabrics to meet green building standards and satisfy consumer demand for safer, non-toxic, and biodegradable materials. Rising awareness of indoor air quality, health, and environmental sustainability is further encouraging the use of textiles made from renewable resources. Continued product innovation, improving affordability, and wider availability through retail channels are expected to support the rapid expansion of this segment in the coming years

The home textiles segment is expected to witness the fastest growth during the forecast period. Demand for eco-friendly household products, including bed sheets, curtains, towels, carpets, and upholstery fabrics, is increasing as consumers look for more sustainable options for their homes. Furniture manufacturers, interior designers, and home décor brands are increasingly adopting bio-based fabrics to meet green building standards and satisfy consumer demand for safer, non-toxic, and biodegradable materials. Rising awareness of indoor air quality, health, and environmental sustainability is further encouraging the use of textiles made from renewable resources. Continued product innovation, improving affordability, and wider availability through retail channels are expected to support the rapid expansion of this segment in the coming years

Recent Developments

- In March 2026, Bioforcetech, a Bay Area-based developer, announced the launch of a collaboration for the development of advanced high-performance and sustainable textile materials and garment options with RDD and Virus Inks. (Source: textileworld.com)

- In January 2026, Denmark-based Octarine Bio launched precision fermented pigments for food, textiles, and personal care and secured 5.8 million USD in funding. This will help Octarine Bio to accelerate the industrial-scale validation and commercial rollout, which is used across multiple industries. (Source: greenqueen.com)

- In May 2026, Fashion brands PANGAIA has launched biobased performance fabric that reduces reliance on petroleum-derived materials. The collection centers on (gaia) BioStretch; the material consists of 72% bio-based nylon and 28% elastane. (Source: worldbiomarketinsights.com)

- In August 2025, ANTA, in partnership with Donghu University, launched AEROVENT ZERO, a high-performance PFAS-free waterproof breathable material, which aims at the development and reshaping of the competitive landscape of technical textiles.(Source: thewire.in)

- In August 2025, Octarine Bio collaborated with textile leaders Impetus Group, Acatel Acabamentos Têxteis S.A., and Positive Materials to launch sustainable bio-based dyes, marking a significant step towards sustainable textile production. This collaboration aims to fast-track the industrial validation and deployment of PurePalette.(Source: synbiobeta.com)

Top Companies list

- Lenzing AG

- DuPont Biomaterials

- NatureWorks LLC

- Teijin Limited

- Grasim Industries Ltd (Aditya Birla Group)

- BASF SE

- Evonik Industries

- Eastman Chemical Company

- Covation Biomaterials

- Toray Industries Inc.

- Ananas Anam (Piñatex)

- Orange Fiber

- Bolt Threads

- MycoWorks

- Spiber Inc.

- Natural Fiber Welding (NFW)

- Circular Systems

- Pangaia

- Ecoalf

- Greenfibres

Segment covered

By Source Material

- Plant-Based

- Organic Cotton

- Hemp

- Flax (Linen)

- Bamboo

- Wood Pulp (Lyocell/Modal/Viscose)

- Corn-Based PLA Fibers

- Banana Fiber

- Pineapple Leaf Fiber

- Others

- Animal-Based

- Organic Wool

- Silk

- Alpaca Fiber

- Camel Hair

- Others

- Microbial/Bioengineered

- Bacterial Cellulose

- Bioengineered Spider Silk

- Mycelium Fibers

- Fermentation-Based Protein Fibers

- Others

- Seaweed Fibers

- Recycled Bio-Based Blends

- Agricultural Waste Fibers

By Application

- Apparel

- Casual Wear

- Sportswear

- Luxury Fashion

- Workwear

- Children's Wear

- Home Textiles

- Bedding

- Curtains

- Upholstery

- Towels

- Carpets & Rugs

- Industrial Textiles

- Automotive

- Medical Textiles

- Geotextiles

- Agriculture Textiles

- Filtration

- Protective Clothing

- Others

- Packaging Textiles

- Footwear Components

- Lifestyle Products

By Region

- North America

- U.S.

- Mexico

- Canada

- Europe

- Germany

- UK

- France

- Italy

- Asia Pacific

- China

- India

- Japan

- South Korea

- Central & South America

- Brazil

- Argentina

- Middle East & Africa

- Saudi Arabia

- UAE

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

FAQ's

Select User License to Buy

Figures (6)