Content

What is the Current Asia Pacific Crop Protection Chemicals Market Size and Share?

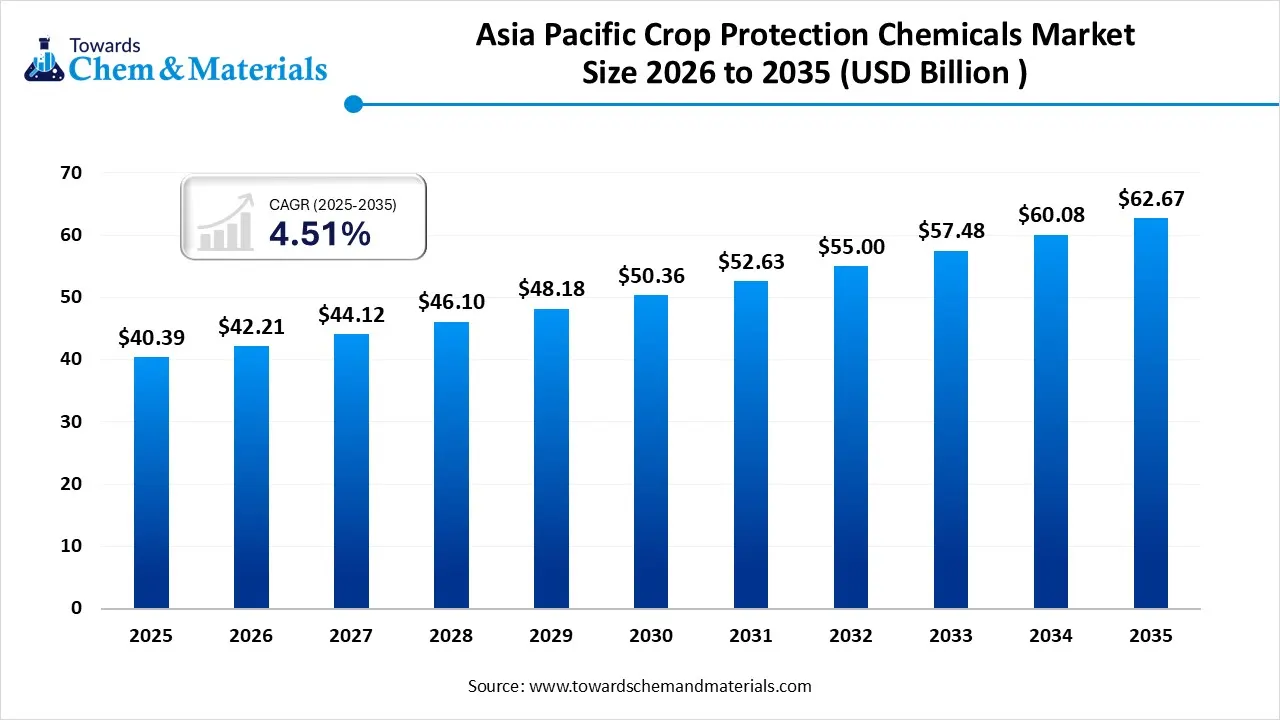

The Asia Pacific crop protection chemicals market size was estimated at USD 40.39 billion in 2025 and is expected to increase from USD 42.21 billion in 2026 to USD 62.67 billion by 2035, growing at a CAGR of 4.51% from 2026 to 2035.The growth of the market is driven by the growing demand for high-quality produce and government initiatives promoting modern farming to boost yields. the Asia-Pacific crop protection chemicals market is significant for ensuring food security for over 60% of the world's population, driving economic stability, and addressing major pest/disease pressures through increased demand for pesticides, especially fungicides and herbicides, while also shifting towards sustainable, precision farming methods with innovative, targeted solutions.

Market Highlights

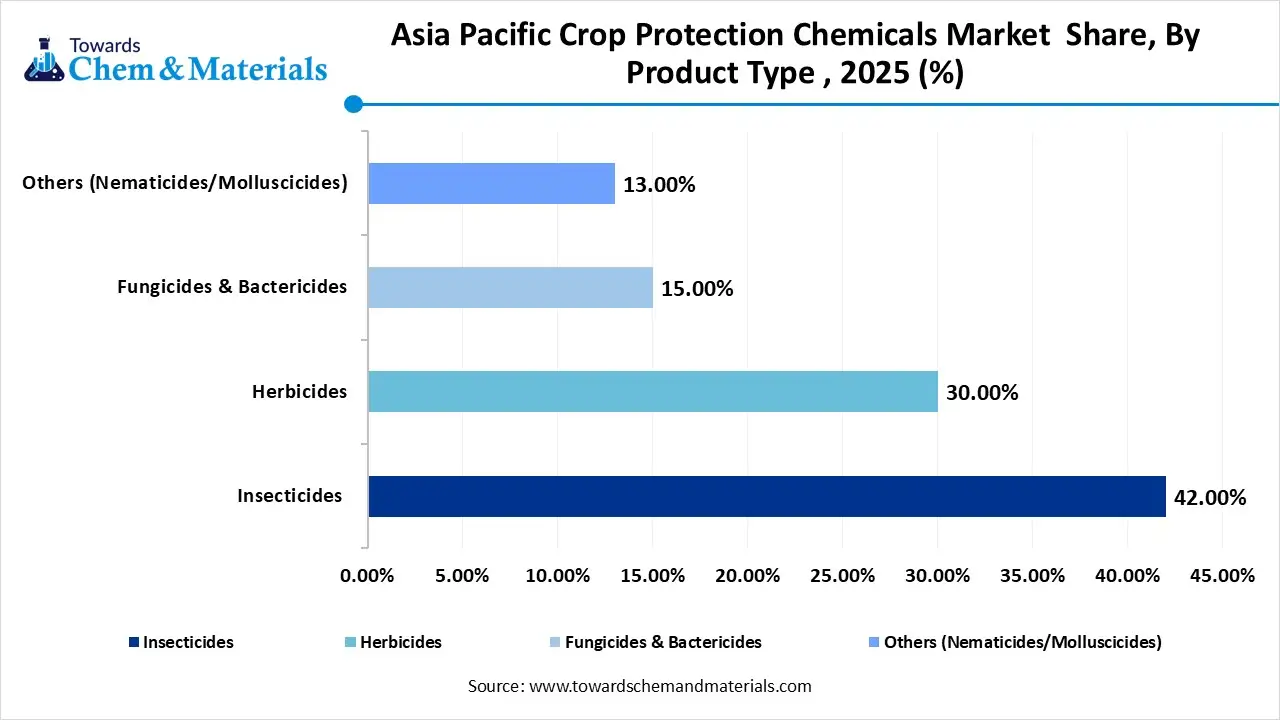

- By product type, the insecticides segment dominated the market and accounted for the largest revenue share of 42.00% in 2025.The segment benefits from intensive cultivation of rice, vegetables, and fruits, particularly in China and Southeast Asia.

- By source, the synthetic chemicals segment led the market with the largest revenue share of 85.00% in 2025, Large-scale farming systems rely heavily on synthetic insecticides and herbicides to ensure consistent yields.

- By form, the liquid formulations segment dominated the market and accounted for the largest revenue share of 65.00% in 2025, These formulations are widely used in foliar applications for insecticides and fungicides.

- By crop type, the cereals & grains led the market with the largest revenue share of 52.00% in 2025, High pest and weed pressure in staple crops necessitates regular chemical usage.

- By mode of application, the foliar spray segment dominated the market and accounted for the largest revenue share of 58.00% in 2025, This method allows quick absorption and targeted action, making it suitable for insecticides and fungicides.

Trade Analysis Of the Asia-Pacific Crop Protection Chemicals Market: Import & Export Statistics

- According to Volza's Global Export data, the World exported 40 shipments of Agro Chemicals to India from Feb 2024 to Jan 2025 (TTM). These exports were made by 8 Exporters to 2 India Buyers.

Most of the agrochemicals exports from the World go to India, the United States, and Chile. - Globally, the top three exporters of Agro Chemicals are Switzerland, India, and the United Kingdom. Switzerland leads the world in Agro Chemicals exports with 266 shipments, followed by India with 157 shipments, and the United Kingdom taking the third spot with 155 shipments.(Source: Volza)

- According to Volza's China Export data, China exported 971 shipments of Crop Protection. These exports were made by 115 Chinese exporters to 163 Buyers.

- Most of the Crop Protection exports from China go to Russia, Nigeria, and Uzbekistan.

- Globally, the top three exporters of Crop Protection are the United States, China, and Russia. The United States leads the world in Crop Protection exports with 1,075 shipments, followed by China with 950 shipments, and Russia taking the third spot with 135 shipments. (Source: Volza)

Market Recent Trends:

- Product Dominance: Insecticides and herbicides are the largest segments, crucial for controlling widespread pest/weed issues in rice, soybeans, and vegetables.

- Rise of Biopesticides: Growing environmental awareness and government support foster the development and adoption of biological alternatives.

- Precision Agriculture: Integration with GPS-guided systems boosts demand for high-efficacy, compatible formulations.

- Focus on Sustainability: Development of targeted, eco-friendly solutions addresses environmental safety concerns and pesticide residues.

Report Scope

| Report Attribute | Details |

| Market Size in 2026 | USD 42.21 Billion |

| Revenue Forecast in 2035 | USD 62.67 Billion |

| Growth Rate | CAGR 4.51% |

| Forecast Period | 2026 - 2035 |

| Base Year | 2025 |

| Segment Covered | By Product Type, By Source, By Form, By Crop Type, By Mode of Application, By Regions |

| Key companies profiled | Syngenta Group, BASF SE, Bayer AG, Corteva Agriscience, UPL Limited, FMC Corporation, Sumitomo Chemical Co., Ltd., ADAMA Ltd., Nufarm Limited, Kumiai Chemical Industry Co., Ltd., Nippon Soda Co., Ltd., Sino-Agri Leading Biosciences, Jiangsu Yangnong Chemical Group, PI Industries, Shandong Weifang Rainbow Chemical |

Market Value Chain Analysis

Chemical Formulation and Processing

- In the Asia Pacific region, crop protection chemicals are produced through active ingredient synthesis, fermentation for bio-based products, formulation blending, emulsification or granulation, and packaging to supply herbicides, insecticides, fungicides, and bio-pesticides tailored to regional crop patterns and climatic conditions.

- Key players Syngenta Group, Bayer AG, UPL Limited, Sumitomo Chemical Co., Ltd

Quality Testing and Certification

- Crop protection chemicals in the Asia Pacific require certifications ensuring efficacy, environmental safety, and compliance with country-specific agricultural regulations. Key certifications include ISO quality standards, FAO/WHO pesticide specifications, national regulatory approvals, residue testing, and GLP compliance.

- Key players: ISO (International Organization for Standardization), FAO, WHO, national agricultural authorities, TÜV SÜD.

Distribution to Industrial Users

- Crop protection chemicals are distributed across the Asia Pacific region to agricultural producers, commercial farms, agrochemical distributors, cooperatives, and government-supported farming programs serving staple and high-value crops.

Key players: UPL Limited, Syngenta Group, FMC Corporation.

Key Technological Shifts In The Asia-Pacific Crop Protection Chemicals Market:

The Asia-Pacific crop protection market is shifting from broad-spectrum chemicals to precision, digital, and biological solutions, driven by AI, drones, nanotechnology, and biotechnology for targeted application, reduced environmental impact, and better pest resistance management, while also seeing demand for novel active ingredients to combat resistant weeds and pests.

Asia-Pacific Crop Protection Chemicals Regulatory Landscape: Global Regulations

| Country / Region | Regulatory Body | Key Regulations / Policies | Focus Areas |

| China | Ministry of Ecology and Environment (MEE) China Pesticide Administration (under Ministry of Agriculture & Rural Affairs) |

Pesticide Administration Regulation Environmental protection laws (air/water/soil) Rotterdam Convention (implementation) |

Active ingredient & formulation registration Residue limits (MRLs) Environmental safety assessments |

| India | Central Insecticides Board & Registration Committee (CIB&RC) Ministry of Agriculture & Farmers Welfare |

Insecticides Act, 1968 Insecticide Rules, 1971 Pesticide residue labeling and MRL mandates |

Product registration & labeling Efficacy, toxicity & residue data Inspectorate enforcement |

| Japan | Ministry of Agriculture, Forestry and Fisheries (MAFF) Ministry of the Environment (MOE) |

Agricultural Chemicals Regulation National pesticide residue and safety frameworks |

Registration with local data requirements Environmental monitoring & residue control |

Segmental Insights

Product Type Insight

Which Product Type Segment Dominated The Asia-Pacific Crop Protection Chemicals Market In 2025?

The insecticides segment dominated the Asia-Pacific crop protection chemicals market with a share of 42% in 2025. Insecticides hold a significant share in the Asia Pacific crop protection chemicals market due to high pest pressure across tropical and subtropical agricultural regions. Rising adoption of integrated pest management and demand for higher crop yields continue to support sustained insecticide consumption.

The herbicides segment is projected to grow at the fastest CAGR between 2026 and 2035 in the Asia-Pacific crop protection chemicals market. Herbicides are witnessing steady growth driven by labor shortages, rising farm wages, and increased mechanization across the Asia Pacific agriculture. Expansion of commercial farming, growing focus on weed resistance management, and adoption of selective and post-emergence herbicides further strengthen market demand.

Asia Pacific Crop Protection Chemicals Market Share, By Product Type , 2025 (%)

| By Product Type | Revenue Share, 2025 (%) |

| Insecticides | 42.00% |

| Herbicides | 30.00% |

| Fungicides & Bactericides | 15.00% |

| Others (Nematicides/Molluscicides) | 13.00% |

Source Insight

How Did the Synthetic Chemicals Segment Dominated The Asia-Pacific Crop Protection Chemicals Market In 2025?

The synthetic chemicals segment dominated the Asia-Pacific crop protection chemicals market with a share of 85% in 2025. Synthetic crop protection chemicals dominate the Asia Pacific market owing to their cost-effectiveness, immediate efficacy, and wide availability. Despite increasing regulatory scrutiny, continued demand from high-intensity agriculture and food security concerns sustains the dominance of this segment.

The biologicals/biopesticides segment is projected to grow at the fastest CAGR between 2026 and 2035 in the Asia-Pacific crop protection chemicals market. Biologicals and biopesticides are gaining traction due to rising environmental awareness, regulatory support, and demand for residue-free produce. Advancements in microbial formulations and improved shelf stability are accelerating adoption across developing Asia Pacific markets.

Asia Pacific Crop Protection Chemicals Market Share, By source , 2025 (%)

| By source | Revenue Share, 2025 (%) |

| Synthetic Chemicals | 85.00% |

| Biologicals | 9.00% |

| Biopesticides | 6.00% |

Form Insight

Which Form Segment Dominated The Asia-Pacific Crop Protection Chemicals Market In 2025?

The liquid formulations segment dominated the Asia-Pacific crop protection chemicals market with a share of 65% in 2025. Liquid formulations account for a major share of the market due to ease of application, uniform coverage, and compatibility with modern spraying equipment. Their fast absorption and convenience make them highly preferred among commercial farmers across the Asia Pacific region.

The solid/dry formulations segment is projected to grow at the fastest CAGR between 2026 and 2035 in the Asia-Pacific crop protection chemicals market. Solid and dry formulations are favored for their longer shelf life, cost efficiency, and ease of transportation and storage. Small and medium farmers across developing economies prefer dry formulations due to reduced handling risks and lower packaging and logistics costs.

Asia Pacific Crop Protection Chemicals Market Share, By Form , 2025 (%)

| By Form | Revenue Share, 2025 (%) |

| Liquid Formulations | 65.00% |

| Solid/Dry Formulations | 35.00% |

Crop Type Insight

How Did the Cereals And Grains Segment Dominated The Asia-Pacific Crop Protection Chemicals Market In 2025?

The cereals & grains segment dominated the Asia-Pacific crop protection chemicals market with a share of 52% in 2025. Cereals and grains represent the largest crop segment for crop protection chemicals in the Asia Pacific, driven by extensive cultivation of rice, wheat, and maize. Government food security programs and an increasing population further reinforce strong demand from this segment.

The fruits & vegetables segment is projected to grow at the fastest CAGR between 2026 and 2035 in the Asia-Pacific crop protection chemicals market. The fruits and vegetables segment is expanding rapidly due to rising consumer demand for high-quality produce and export standards. Growing adoption of specialty chemicals and biopesticides is particularly notable in horticulture-focused economies.

Asia Pacific Crop Protection Chemicals Market Share, By Crop Type , 2025 (%)

| By Crop Type | Revenue Share, 2025 (%) |

| Cereals & Grains | 52.00% |

| Fruits & Vegetables | 22.00% |

| Oilseeds & Pulses | 14.00% |

| Commercial/Turf & Ornamentals | 12.00% |

Mode of Application Insight

Which Mode Of Application Segment Dominated The Asia-Pacific Crop Protection Chemicals Market In 2025?

The foliar spray segment dominated the Asia-Pacific crop protection chemicals market with a share of 58% in 2025. Foliar spray is the most widely used mode of application due to its effectiveness in controlling above-ground pests and diseases. Advances in spraying technology and precision agriculture are further improving application efficiency across the region.

The seed treatment segment is projected to grow at the fastest CAGR between 2026 and 2035 in the Asia-Pacific crop protection chemicals market. Seed treatment is gaining importance as a preventive approach to protect crops during early growth stages. Increasing awareness of sustainable farming practices and cost efficiency is driving the adoption of seed treatment solutions in the Asia Pacific agriculture.

Asia Pacific Crop Protection Chemicals Market Share, By Mode of Application , 2025 (%)

| By Mode of Application | Revenue Share, 2025 (%) |

| Foliar Spray | 58.00% |

| Seed Treatment | 18.00% |

| Soil Treatment | 14.00% |

| Others (Chemigation/Fumigation) | 10.00% |

Recent Developments

- In November 2025, BASF commissioned a new high-performance dispersant production line in Nanjing, China. This launch is noted as a significant advancement in localizing chemical technology within the Asia-Pacific region.(Source: www.basf.com)

- In May 2025, BASF introduced innovations to its crop protection portfolio in the Asia-Pacific region, 2025- 2026, focusing on rice production to improve yields and combat pest resistance.(Source: chemindigest.com)

- In June 2025, Covestro launched the first localized production of its Desmopan® Rx medical-grade thermoplastic polyurethane (TPU) in the Asia-Pacific region at its Changhua site in Taiwan. This expansion aims to reduce lead times for regional medical device manufacturers and enhance supply chain resilience.(Source: www.indianch44.emicalnews.com)

Top players in the Asia-Pacific Crop Protection Chemicals Market & Their Offerings:

- Syngenta Group: Syngenta is a major global supplier of crop protection products with a strong regional presence across the Asia Pacific. Its portfolio includes herbicides, fungicides, insecticides, and emerging biological solutions tailored for high-yield farming and sustainable pest control.

- BASF SE:BASF offers a wide range of crop protection chemicals, including weed control, disease management, and insect management products. Its solutions focus on performance, low environmental impact, and integration with regional agronomic practices.

- Bayer AG:Bayer provides specialized crop protection chemistries like herbicides and fungicides designed to improve crop resistance and soil health. The company emphasizes innovation and alignment with integrated pest management practices.

- Corteva Agriscience:Corteva delivers a broad portfolio of crop protection products, including herbicides, insecticides, and fungicides. Its offerings support cereals, oilseeds, and horticultural crops, backed by digital agronomy services to enhance farmer decision-making.

- UPL Limited:UPL is a key regional player with diverse offerings spanning herbicides, insecticides, fungicides, and biologicals. It focuses on cost-effective and locally adapted formulations to serve smallholder and commercial farmers.

- FMC Corporation

- Sumitomo Chemical Co., Ltd.

- ADAMA Ltd.

- Nufarm Limited

- Kumiai Chemical Industry Co., Ltd.

- Nippon Soda Co., Ltd.

- Sino-Agri Leading Biosciences

- Jiangsu Yangnong Chemical Group

- PI Industries

- Shandong Weifang Rainbow Chemical

Segments Covered:

By Product Type

- Insecticides

- Herbicides

- Fungicides & Bactericides

- Others (Nematicides/Molluscicides)

By Source

- Synthetic Chemicals

- Biologicals

- Biopesticides

By Form

- Liquid Formulations

- Solid/Dry Formulations

By Crop Type

- Cereals & Grains

- Rice

- Wheat

- Corn

- Fruits & Vegetables

- Oilseeds & Pulses

- Commercial/Turf & Ornamentals

By Mode of Application

- Foliar Spray

- Seed Treatment

- Soil Treatment

- Others (Chemigation/Fumigation)

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

FAQ's

Select User License to Buy

Figures (2)