Content

What is the Current Asia Pacific Aquaculture Market Size and Share?

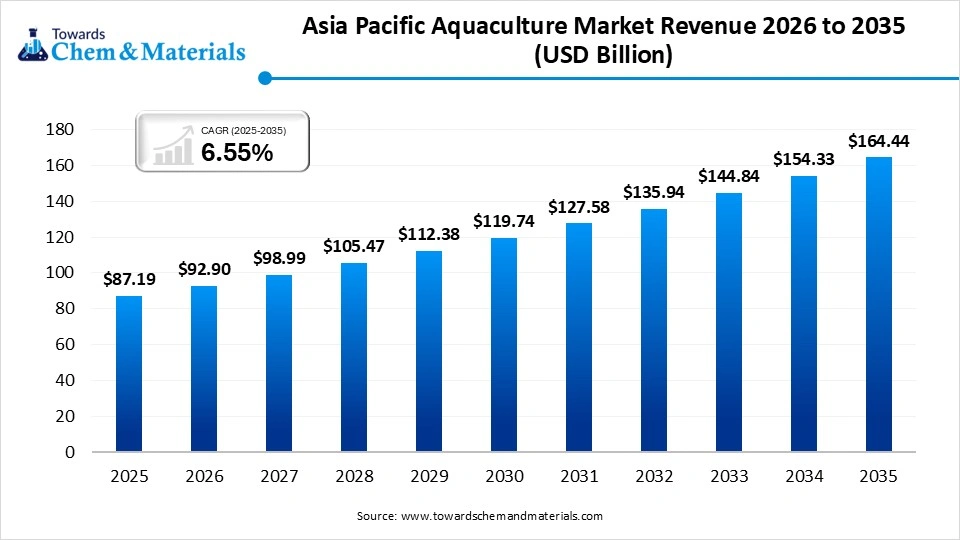

The Asia Pacific aquaculture market size was estimated at USD 87.19 billion in 2025 is estimated to reach USD 92.90 billion in 2026, and is expected to be worth around USD 164.44 billion by 2035, growing at a CAGR of 6.55% from 2026 to 2035.The growth of the market is driven by skyrocketing domestic seafood demand, rapid regional population growth, and the depletion of wild fish stocks. The Asia Pacific aquaculture sector is the leading global hub for fish and seafood farming, producing over 90% of the world's aquaculture. It plays a crucial role in regional food security, economic development, and job creation, while easing pressure on wild fish populations. Key countries like China, India, Vietnam, and Indonesia dominate, with China accounting for more than half of all global aquaculture production.

The sector encompasses a wide range of finfish, shellfish, and aquatic plants (such as algae), with freshwater farms generating the largest revenue. Seafood is integral to the diets, economies, and cultural traditions of Asia Pacific communities. It supports millions of livelihoods through activities like hatcheries, aquafeed manufacturing, harvesting, and processing. Fish are highly efficient in converting feed into body mass, making them a sustainable protein source.

To address environmental and climate challenges, the region is rapidly adopting innovations like recirculating aquaculture systems (RAS) and integrated systems such as aquaponics.Governments actively support the industry with financial subsidies and modernization efforts aimed at improving farm productivity, water efficiency, and long-term resilience. Beyond local markets, aquaculture is a significant contributor to international trade, providing vital foreign exchange for developing economies.

Market Highlights

- By country, China dominated the market with a share of 46% in 2025. The growth is driven by the growing government initiatives and support.

- By country, India held 19% market share in 2025 and is expects the fastest growth in the market with the CAGR of 6.90% in the forecast period. the growth is propelled by the presence of strong export revenue.

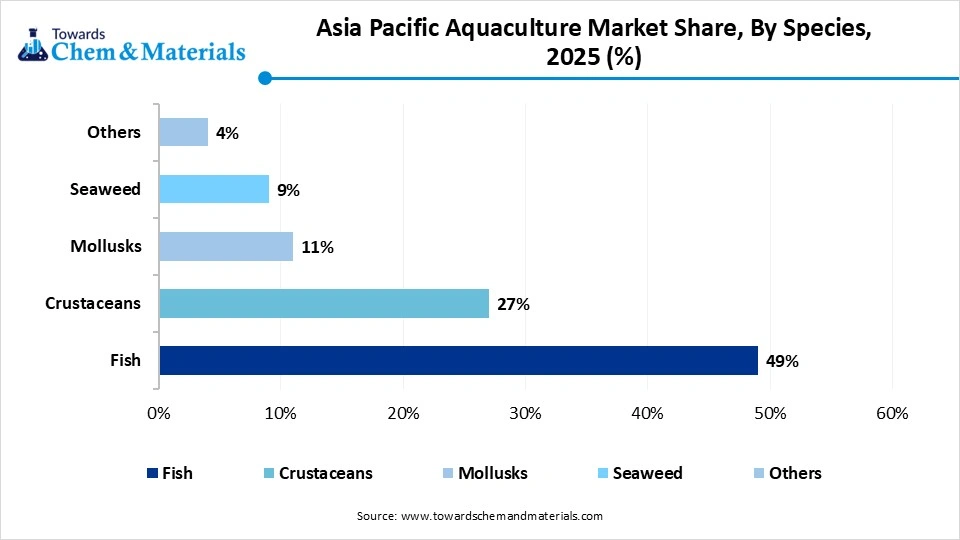

- By species, the fish segment dominated the market with 49% share in 2025. Rising seafood consumption across the Asia Pacific drives fish farming expansion.

- By species, the crustaceans segment held 27% market share in 2025 and is expected to have the fastest growth with a CAGR of 7.42% in the forecast period. Strong export demand for shrimp and prawns accelerates the crustacean.

- By culture environment, the freshwater segment dominated the market with 58% share in 2025. Freshwater aquaculture remains dominant due to extensive carp and tilapia farming across the Asia Pacific.

- By culture environment, the marine water segment held 28% market share in 2025 and is expected to have the fastest growth with a CAGR of 7.28% in the forecast period. Offshore and coastal aquaculture investments increase marine seafood production capabilities.

- By farming technology, the traditional aquaculture segment dominated the market with 24% share in 2025. Small-scale farmers continue relying on conventional aquaculture methods due to lower capital requirements.

- By farming technology, the recirculating aquaculture systems (RAS) segment held 9% market share in 2025 and is expected to have the fastest growth with a CAGR of 9.31% in the forecast period. RAS technology enables controlled environment farming with minimal water consumption.

- By production type, the inland aquaculture segment dominated the market with 57% share in 2025. Extensive freshwater fish farming activities drive inland aquaculture dominance across Asia-Pacific.

- By production type, the offshore aquaculture segment held 14% market share in 2025 and is expected to have the fastest growth with a CAGR of 8.41% in the forecast period. Offshore farming reduces coastal congestion and supports large-scale marine seafood production.

- By feed type, the compound feed segment dominated the market with 61% share in 2025. Commercial aquaculture farms increasingly rely on nutritionally balanced compound feed to maximize productivity.

- By feed type, the live feed segment held 17% market share in 2025 and is expected to have the fastest growth with a CAGR of 7.89% in the forecast period. Hatcheries increasingly utilize live feed to improve larval survival and growth performance.

- By application, the food consumption segment dominated the market with 71% share in 2025. Rising seafood consumption across urban populations strongly drives aquaculture production growth.

- By application, the nutraceutical segment held 8% market share in 2025 and is expected to have the fastest growth with a CAGR of 8.02% in the forecast period. Omega-3 supplements and marine-based health products fuel nutraceutical application demand.

- By distribution channel, the direct sales segment dominated the market with 28% share in 2025. Producers increasingly sell directly to wholesalers and processors to improve profit margins.

- By distribution channel, the online retail segment held 11% market share in 2025 and is expected to have the fastest growth with a CAGR of 9.26% in the forecast period. E-commerce platforms accelerate seafood sales through home delivery and digital ordering services.

- By end user, the commercial aquaculture farms segment dominated the market with 52% share in 2025. Large-scale commercial farms continue expanding production capacity to meet regional seafood demand.

- By end user, the export-oriented producers segment held 13% market share in 2025 and is expected to have the fastest growth with a CAGR of 8.11% in the forecast period. Strong international demand for shrimp, fish, and shellfish accelerates export-focused aquaculture investments.

Recent Growth Trends:

- Technology & Innovation: The shift toward advanced farming techniques is rapidly changing the landscape. Recirculating Aquaculture Systems (RAS) and offshore cage farming are gaining widespread adoption to maximize yields in land-scarce, urbanized areas like Singapore.

- Sustainable Practices & Policy: Governments and agencies across the region are prioritizing sustainable, resilient aquaculture systems. This includes promoting disease-resistant species, innovative feed formulations, and improved cold chain logistics to reduce spoilage.

- Government Subsidies and Initiatives: National governments across the region are implementing aggressive modernization programs and financial subsidies to boost domestic production and ensure food security.

Key Technological Shifts in the Asia Pacific Aquaculture Market:

The Asia Pacific aquaculture market is rapidly shifting toward sustainability and data-driven management. Key technological transformations include AI-driven precision farming, advanced bio-controlled systems, "Aquavoltaics", and modernized, small-holder adaptations. The region is addressing environmental bottlenecks by recycling aquaculture waste. Innovations include turning nutrient-rich pond sludge into circular construction materials and developing low-emission, solar-powered electric propulsion for small fishing boats.

Report Scope

| Report Attributes | Details |

| Market Size and Volume in 2026 | USD 92.90 Billion |

| Projected Market Size and Volume in 2035 | USD 164.44 Billion |

| CAGR (2026 - 2035) | 6.55% |

| Forecast Period | 2026 - 2035 |

| Base Year | 2025 |

| Market Segmentation | By Species, By Culture Environment, By Farming Technology, By Production Type, By Feed Type, By Application, By Distribution Channel, By End User, By Country |

| Top Key Players | Charoen Pokphand Foods PCL., Tassal Group Limited, Blue Ridge Aquaculture, Selonda Aquaculture S.A., AKVA Group, Pentair plc, Nireus SA, Ltd. (Greece), Thai Union Group PCL (Thailand), MOWI ASA (Norway), Cermaq Group AS (Norway), SalMar ASA (Norway), Norway Royal Salmon ASA (Norway), Maruha Nichiro Corporation (Japan), Kyokuyo Co., Ltd. (Japan), Stoly Sea Farm SA (Spain), Cooke Aquaculture Inc. (Canada). |

Supply Chain Analysis of the Asia Pacific Aquaculture Market:

- Aquaculture Production & Farming Operations:Aquaculture in the Asia Pacific involves the cultivation of fish, crustaceans, mollusks, and aquatic plants through freshwater, marine, and brackish water farming systems using advanced feeding, breeding, and water management technologies.

- Key players: Mitsubishi Corporation, Cooke Aquaculture, Thai Union Group, Charoen Pokphand Foods.

- Quality Testing and Certification: Aquaculture products must comply with food safety standards, sustainability regulations, water quality requirements, and traceability certifications to ensure safe seafood production and environmental protection.

- Key players: Food and Agriculture Organization, Aquaculture Stewardship Council, International Organization for Standardization, Network of Aquaculture Centres in Asia-Pacific.

- Distribution to Industrial Users:Aquaculture products are supplied to seafood processing companies, food service providers, retail chains, export markets, pharmaceutical applications, and animal feed industries across the Asia Pacific region.

- Key players: Thai Union Group, Charoen Pokphand Foods, Cooke Aquaculture.

Asia Pacific Aquaculture Regulatory Landscape: Regulations

| Country / Region | Regulatory Body | Key Regulations | Focus Areas | Notable Notes |

| China | Ministry of Agriculture and Rural Affairs (MARA); State Oceanic Administration | Fisheries Law of China; Aquaculture Environmental Regulations | Sustainable aquaculture, disease control, and water quality | China is the world’s largest aquaculture producer and is increasingly focusing on sustainable and technology-driven aquaculture practices. |

| India | Department of Fisheries; Coastal Aquaculture Authority (CAA) | Coastal Aquaculture Authority Act; National Fisheries Policy | Shrimp farming regulation, biosecurity, export compliance | India promotes aquaculture expansion through subsidies and infrastructure development while regulating coastal shrimp farming activities. |

| Vietnam | Ministry of Agriculture and Rural Development (MARD) | Fisheries Law 2017; Aquaculture Development Strategy | Seafood exports, traceability, and sustainable farming | Vietnam emphasizes export-oriented aquaculture and compliance with international sustainability standards. |

| Indonesia | Ministry of Marine Affairs and Fisheries (MMAF) | Fisheries and Aquaculture Regulations; Sustainable Fisheries Policies | Marine aquaculture, sustainability, export growth | Indonesia supports aquaculture modernization and sustainable seafood production to strengthen exports. |

| Thailand | Department of Fisheries | Aquatic Animal Disease Control Act; Fisheries Ordinance | Disease management, seafood safety | Thailand focuses on high-quality shrimp and seafood exports with strict disease prevention standards. |

| Australia | Department of Agriculture, Fisheries and Forestry (DAFF); Fisheries Research and Development Corporation (FRDC) | Environment Protection and Biodiversity Conservation Act; Aquaculture Licensing Frameworks | Environmental sustainability, biosecurity | Australia regulates aquaculture through strict environmental and marine ecosystem protection measures. |

Market Dynamics

Drivers

What are the Key Growth Drivers of the Asia Pacific Aquaculture Market?

The Asia Pacific aquaculture market is driven by high regional seafood consumption, overfishing of wild stocks, and rapid technological advancements. Key drivers include state-sponsored modernization, optimal climatic conditions, and rising disposable incomes. A massive, expanding population with rising disposable incomes has led to an increased per capita intake of seafood, which is viewed as a healthy protein alternative.

The integration of precision aquaculture AI-driven monitoring, IoT sensors, and automated feeding systems increases operational efficiency, optimizes water quality, and reduces disease. Regional governments provide substantial financial subsidies, modernization programs, and export incentives. Notable examples include India's Pradhan Mantri Matsya Sampada Yojana (PMMSY), which boosts farmer profitability and feed quality.

Restrains

What are the Key Growth Restraints of the Asia Pacific Aquaculture Market?

The primary growth restraints for the Asia Pacific aquaculture market include high operational costs, stringent environmental regulations, infrastructure gaps, and vulnerability to diseases. These challenges particularly impact small and mid-scale producers as the industry undergoes a major shift from traditional farming to heavily regulated, tech-driven systems. Governments in dominant producing countries like China are implementing aggressive crackdowns on illegal or environmentally degrading operations. Producers face heavy compliance burdens regarding water usage, antibiotic/chemical use, and waste management to meet certifications. Balancing strict environmental mandates with economic profitability remains a core hurdle.

Opportunities

What are the Key Growth Opportunities of the Asia Pacific Aquaculture Market?

The Asia Pacific aquaculture market is the dominant global powerhouse, producing over 90% of the world's farmed aquatic foods. Key growth opportunities are driven by the rising demand for high-protein seafood, overfishing of wild stocks, and the rapid adoption of "smart" farming technologies in major production hubs like China, India, and Indonesia. Adopting the Internet of Things (IoT) and artificial intelligence for real-time water quality monitoring, automated feeding, and automated aeration systems. This maximizes yield while minimizing resource waste, especially in tech-forward countries like India and China.

Segmental Insights

Species Insights

The fish segment dominated the market with 49% share in 2025, Driven by rising disposable incomes, declining wild fish stocks, and dietary shifts, this rapid expansion highlights a booming demand for accessible, protein-rich seafood.Operations are modernizing with AI-enabled farming, automated filleting, and eco-friendly extruded feed pellets to meet sustainability standards and reduce production waste.

")

The crustaceans segment held 27% market share in 2025 and is expected to have the fastest growth with a CAGR of 7.42% in the forecast period, premium pricing, high export demand from international markets, and shifting dietary habits favoring high-protein luxury seafood. Producers are transitioning from traditional to semi-intensive and intensive farming models. This involves heavily upgrading farm designs, water processing ponds, and nursing technologies to achieve higher yields.

Asia Pacific Aquaculture Market Share, By Species, 2025 (%)

| By Species | Revenue Share, 2025 (%) |

| Fish | 49% |

| Crustaceans | 27% |

| Mollusks | 11% |

| Seaweed | 9% |

| Others | 4% |

Culture Environment Insights

The freshwater segment dominated the market with 58% share in 2025, fueled by lower operational costs, simple infrastructure, and an abundance of inland waterways. Rapid regional growth is propelled by strong local demand for affordable species like carp, tilapia, and catfish, alongside smallholder integration with rice farming. Localized government policies, such as subsidies, public-private partnerships, and tax incentives, are modernizing traditional fish farms and supporting the expansion of the freshwater segment.

Asia Pacific Aquaculture Market Share, By Culture Environment, 2025 (%)

| By Culture Environment | Revenue Share, 2025 (%) |

| Freshwater | 58% |

| Marine Water | 28% |

| Brackish Water | 14% |

The marine water segment held 28% market share in 2025 and is expected to have the fastest growth with a CAGR of 7.28% in the forecast period, driven by the commercial shift toward high-value species like salmon, shrimp, and oysters, and expanding offshore farming operations. Marine species consistently command higher market prices compared to freshwater fish, making them incredibly attractive for large-scale commercial aquaculture investments.

Farming Technology Insights

The traditional aquaculture segment dominated the market with 24% share in 2025. It is growing significantly due to rapid urbanization, increasing per capita seafood consumption, and supportive local government initiatives that ensure accessible, protein-rich diets. Population growth and changing dietary habits are drastically boosting seafood consumption. Traditional aquaculture provides a crucial, steady source of affordable animal protein for regional populations.

Asia Pacific Aquaculture Market Share, By Farming Technology, 2025 (%)

| By Farming Technology | Revenue Share, 2025 (%) |

| Traditional Aquaculture | 24% |

| Intensive Aquaculture | 21% |

| Semi-Intensive Aquaculture | 17% |

| Biofloc Technology | 10% |

| Recirculating Aquaculture Systems (RAS) | 9% |

| Integrated Multi-Trophic Aquaculture (IMTA) | 8% |

| Smart Aquaculture | 11% |

The recirculating aquaculture systems (RAS) segment held 9% market share in 2025 and is expected to have the fastest growth with a CAGR of 9.31% in the forecast period, fueled by rising seafood consumption, environmental degradation of coastal waters, and shrinking freshwater supplies. This closed-loop technology allows high-density, land-based farming by recycling up to 99% of water.

Production Type Insights

The inland aquaculture segment dominated the market with 57% share in 2025, due to lower operational costs, favorable tropical/subtropical climates, abundant natural freshwater resources, and strong government subsidies promoting sustainable, protein-rich food production. Rising disposable incomes and dense populations in emerging APAC markets have accelerated seafood consumption.

Asia Pacific Aquaculture Market Share, By Production Type, 2025 (%)

| By Production Type | Revenue Share, 2025 (%) |

| Inland Aquaculture | 57% |

| Coastal Aquaculture | 29% |

| Offshore Aquaculture | 14% |

The offshore aquaculture segment held 14% market share in 2025 and is expected to have the fastest growth with a CAGR of 8.41% in the forecast period, propelled by escalating seafood demand, diminishing coastal space, and the need to mitigate environmental pressure on nearshore ecosystems. Moving farms offshore provides better water quality, stronger ocean currents, and stable temperatures. This creates optimal conditions that reduce disease outbreaks and parasite infestations.

Feed Type Insights

The compound feed segment dominated the market with 61% share in 2025, driven by the massive structural shift away from traditional, unformulated farm-made mixtures toward highly controlled, nutrient-dense commercial formulations. Governments across the APAC region are aggressively pushing for self-sufficient, sustainable aquaculture systems.

Asia Pacific Aquaculture Market Share, By Feed Type, 2025 (%)

| By Feed Type | Revenue Share, 2025 (%) |

| Compound Feed | 61% |

| Farm-Made Feed | 22% |

| Live Feed | 17% |

The live feed segment held 17% market share in 2025 and is expected to have the fastest growth with a CAGR of 7.89% in the forecast period, driven by a surge in commercial hatchery operations. Live feeds such as rotifers, Artemia, and copepods are critical during the early larval and juvenile stages of high-value fish and shrimp, as they provide essential nutrients and mimic natural predatory foraging.

Application Insights

The food consumption segment dominated the market with 71% share in 2025, expanding middle-class populations, rising disposable incomes, and a cultural shift toward premium, protein-rich seafood. Overfishing wild stocks, aggressive government investments, and rapid cold-chain advancements have solidified aquaculture as the primary source of affordable, sustainable protein across the region.

Asia Pacific Aquaculture Market Share, By Application, 2025 (%)

| By Application | Revenue Share, 2025 (%) |

| Food Consumption | 71% |

| Pharmaceutical | 6% |

| Nutraceutical | 8% |

| Cosmetics | 5% |

| Animal Feed | 7% |

| Industrial Applications | 3% |

The nutraceutical segment held 8% market share in 2025 and is expected to have the fastest growth with a CAGR of 8.02% in the forecast period, driven by a shift toward preventive health, a demand for residue-free farming, and a booming middle class. Aquafeed producers are increasingly replacing antibiotics and artificial additives with health-promoting bioactives to boost immunity, disease resistance, and market value in farmed aquatic species.

Distribution Channel Insights

The direct sales segment dominated the market with 28% share in 2025, due to the rapid expansion of digital e-commerce, rising consumer demand for traceable and sustainable seafood, and the need for agile distribution channels. The proliferation of digital engagement platforms and mobile shopping apps enables aquaculture farmers to sell directly to consumers, bypassing traditional wholesalers and reducing supply chain costs.

Asia Pacific Aquaculture Market Share, By Distribution Channel, 2025 (%)

| By Distribution Channel | Revenue Share, 2025 (%) |

| Direct Sales | 28% |

| Supermarkets & Hypermarkets | 24% |

| Specialty Seafood Stores | 13% |

| Online Retail | 11% |

| Foodservice | 24% |

The online retail segment held 11% market share in 2025 and is expected to have the fastest growth with a CAGR of 9.26% in the forecast period, driven by massive e-commerce adoption and improved cold-chain logistics. Consumers can now purchase fresh, processed, and live seafood directly via online platforms. This digital shift ensures product traceability, convenience, and faster direct-to-consumer delivery across the region.

End User Insights

The commercial aquaculture farms segment dominated the market with 52% share in 2025, driven by the need to meet surging seafood demand, declining wild fish stocks, and lucrative export opportunities. These farms are scaling up through modernization, technological integration, and high-value species cultivation. Regional governments are providing financial incentives, subsidies, and favorable policies to modernize traditional ponds into large-scale commercial operations, boosting overall food security.

Asia Pacific Aquaculture Market Share, By End User, 2025 (%)

| By End User | Revenue Share, 2025 (%) |

| Commercial Aquaculture Farms | 52% |

| Household Consumption | 14% |

| Food Processing Companies | 18% |

| Export-Oriented Producers | 13% |

| Research Institutions | 3% |

The export-oriented producers segment held 13% market share in 2025 and is expected to have the fastest growth with a CAGR of 8.11% in the forecast period, driven by premium pricing for species like frozen shrimp and pangasius. Producers are transitioning from traditional farming to technology-driven models to meet rigorous international food safety and sustainability standards, capturing high global demand and generating strong foreign exchange revenues.

Country Level Analysis

China Asia Pacific Aquaculture Market Growth Factor

The China AI in chemicals market size was estimated at USD 40.11 billion in 2025 and is projected to reach USD 76.46 billion by 2035, growing at a CAGR of 8.40% from 2026 to 2035. China dominated the market with a share of 46% in 2025, driving regional growth through rapid urbanization, rising per capita seafood consumption, and strong government initiatives promoting sustainable, technology-driven farming. A massive population with deep-rooted culinary traditions creates consistent, high demand for both domestic consumption and the export market. The continuous migration of rural populations to cities has stimulated heavy demand for convenience, processed, and ready-to-cook seafood products.

The China AI in chemicals market size was estimated at USD 40.11 billion in 2025 and is projected to reach USD 76.46 billion by 2035, growing at a CAGR of 8.40% from 2026 to 2035. China dominated the market with a share of 46% in 2025, driving regional growth through rapid urbanization, rising per capita seafood consumption, and strong government initiatives promoting sustainable, technology-driven farming. A massive population with deep-rooted culinary traditions creates consistent, high demand for both domestic consumption and the export market. The continuous migration of rural populations to cities has stimulated heavy demand for convenience, processed, and ready-to-cook seafood products.

Asia Pacific Aquaculture Market Share, By countries, 2025(%)

| By countries | Revenue Share, 2025 (%) |

| China | 46% |

| India | 19% |

| Japan | 11% |

| South Korea | 8% |

| Australia | 7% |

| Rest of Asia Pacific | 9% |

India Asia Pacific Aquaculture Market Growth Factor

India held 19% market share in 2025 and is expected to grow fastest in the market with the CAGR of 6.90% in the forecast period, driven by the rising domestic protein demand, strong export revenues, and targeted government modernization schemes. Initiatives like the Pradhan Mantri Matsya Sampada Yojana (PMMSY) pump financial investments into modernizing infrastructure, enhancing cold chain logistics, and boosting domestic fish production. Rapid urbanization and changing dietary habits across the Asia Pacific region are driving massive consumption of nutrient-rich seafood and white meats.

Recent Development

- In April 2026, WorldFish officially announced the launch of WorldFish Ventures (WFV), a wholly owned commercial subsidiary designed to scale aquaculture and fisheries innovations through market-based strategies. The platform aims to mobilize private investment and expand the deployment of aquatic food technologies, particularly in underserved markets across Asia and Africa.(Source: www.globalseafood.org)

Top players in the Asia Pacific Aquaculture Market & Their Offerings:

- Charoen Pokphand Foods PCL: CPF is a major producer of aquaculture feed and shrimp farming solutions in Southeast Asia, focusing on integrated aquaculture production systems.

- Tassal Group Limited: Tassal specializes in salmon aquaculture and prawn farming, supporting sustainable seafood production in Australia and neighboring markets.

- Blue Ridge Aquaculture: Blue Ridge Aquaculture develops recirculating aquaculture systems (RAS) and advanced fish farming technologies serving the Asia Pacific demand.

- Selonda Aquaculture S.A.: Selonda supplies aquaculture products and expertise for marine fish farming and sustainable seafood production.

- AKVA Group: AKVA Group provides aquaculture equipment, digital monitoring systems, cages, and feed technologies to fish farming operations across the Asia Pacific.

- Pentair plc: Pentair supplies water filtration, recirculation, and aquaculture infrastructure systems supporting modern fish farming operations.

Other Top Players Are

- Nireus SA, Ltd. (Greece)

- Thai Union Group PCL (Thailand)

- MOWI ASA (Norway)

- Cermaq Group AS (Norway)

- SalMar ASA (Norway)

- Norway Royal Salmon ASA (Norway)

- Maruha Nichiro Corporation (Japan)

- Kyokuyo Co., Ltd. (Japan)

- Stoly Sea Farm SA (Spain)

- Cooke Aquaculture Inc. (Canada)

Segments Covered:

By Species

- Fish

- Carp

- Tilapia

- Salmon

- Catfish

- Seabass

- Tuna

- Milkfish

- Others

- Crustaceans

- Shrimp

- Prawns

- Crabs

- Lobsters

- Mollusks

- Oysters

- Mussels

- Clams

- Scallops

- Seaweed

- Red Seaweed

- Brown Seaweed

- Green Seaweed

- Others

- Sea Cucumbers

- Ornamental Aquatic Species

By Culture Environment

- Freshwater

- Ponds

- Tanks

- Recirculating Aquaculture Systems (RAS)

- Marine Water

- Offshore Aquaculture

- Coastal Aquaculture

- Brackish Water

- Estuarine Farming

- Mangrove-based Farming

By Farming Technology

- Traditional Aquaculture

- Intensive Aquaculture

- Semi-Intensive Aquaculture

- Biofloc Technology

- Recirculating Aquaculture Systems (RAS)

- Integrated Multi-Trophic Aquaculture (IMTA)

- Smart Aquaculture

- IoT Monitoring

- AI-based Feeding Systems

- Automated Water Quality Management

By Production Type

- Inland Aquaculture

- Coastal Aquaculture

- Offshore Aquaculture

By Feed Type

- Compound Feed

- Pellets

- Extruded Feed

- Powder Feed

- Farm-Made Feed

- Live Feed

- Artemia

- Rotifers

- Algae Feed

By Application

- Food Consumption

- Pharmaceutical

- Nutraceutical

- Cosmetics

- Animal Feed

- Industrial Applications

By Distribution Channel

- Direct Sales

- Supermarkets & Hypermarkets

- Specialty Seafood Stores

- Online Retail

- Foodservice

- Hotels

- Restaurants

- Catering Services

By End User

- Commercial Aquaculture Farms

- Household Consumption

- Food Processing Companies

- Export-Oriented Producers

- Research Institutions

By Country

- China

- Taiwan

- India

- Japan

- Australia and New Zealand

- ASEAN Countries (Singapore, Malaysia)

- South Korea

- Rest of APAC

FAQ's

Select User License to Buy

Figures (3)