Content

U.S. Agrochemicals Market Size, Share and Trends 2026 to 2035

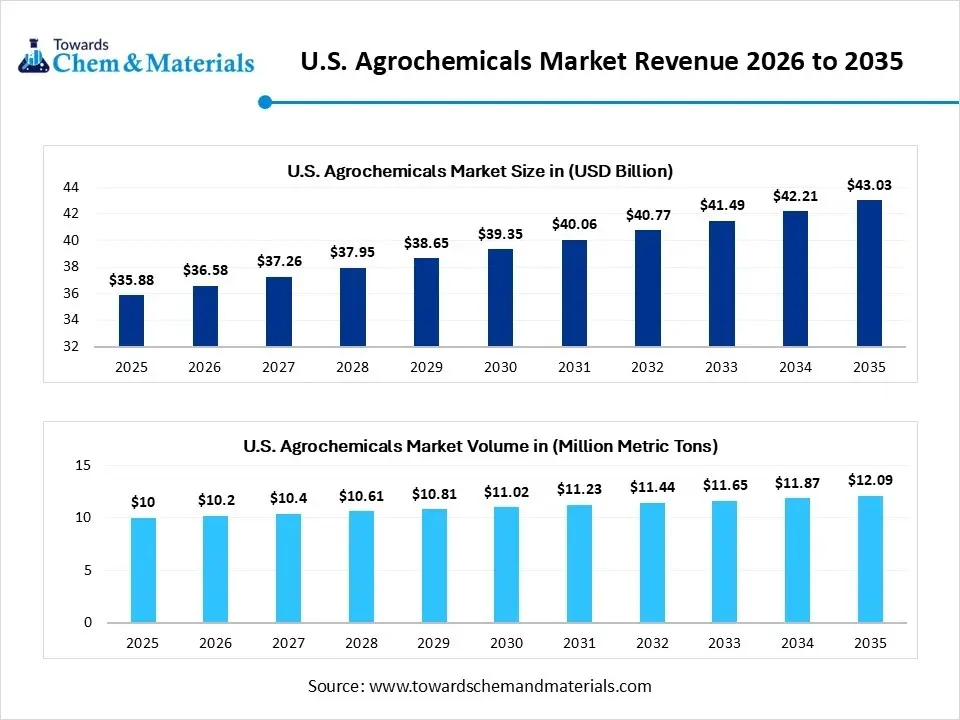

The U.S. agrochemicals market size was estimated at USD 35.88 billion in 2025 and is expected to be worth around USD 43.03 billion by 2035, growing at a CAGR of 1.95% from 2026 to 2035. In terms of volume, the U.S. agrochemicals market is projected to grow from 10 million metric tons in 2025 to 12.09 million metric tons by 2035. growing at a CAGR of 1.95% from 2026 to 2035.Growing demand for specialized and cost-effective products is the key factor driving market growth. Also, the expansion of the food and beverage industry, coupled with the ongoing technological advancements like precision farming, can fuel market growth further.

Key Takeaways

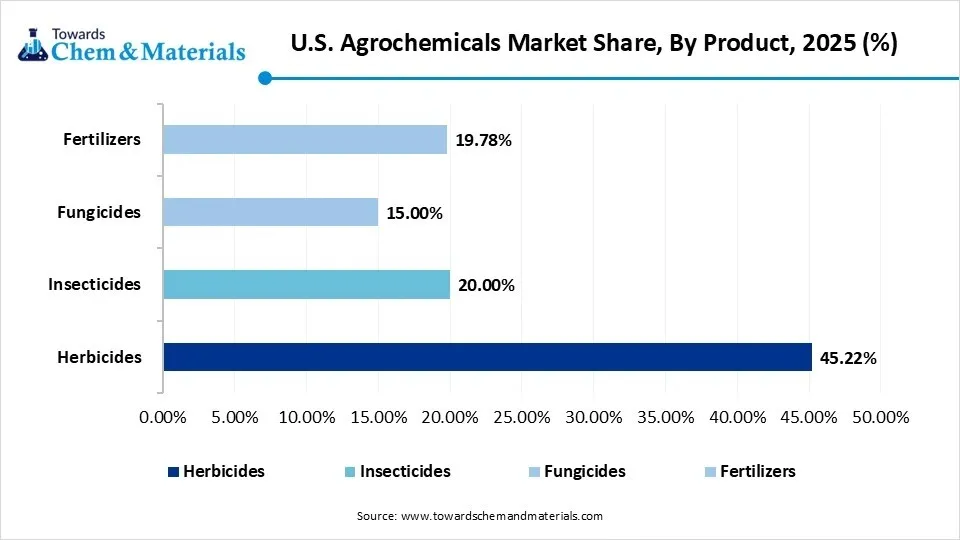

- By product, the herbicides segment dominated the market with a 45.22% share in 2025.

- By product, the insecticides segment held a 20.00% market share and is expected to grow at the fastest CAGR of 7.54% over the forecast period.

- By crop type, the cereals & grains segment held a 41.00% market share in 2025.

- By crop type, the fruits & vegetables segment held a 24.00% market share and is expected to grow at the fastest CAGR of 8.21% over the forecast period.

- By formulation, the liquid formulations segment dominated the market by holding 50.10% market share in 2025.

- By formulation, the dry formulations segment held a 32% market share and is expected to grow at the fastest CAGR of 8.0% during the forecast period.

- By application, the crop protection segment held a 56.00% market share in 2025.

- By application, the soil treatment & fertility segment held a 31% market share and is expected to grow at the fastest CAGR of 8.0% during the projected period.

- By end user, the commercial farmers segment dominated the market by holding a 51.30% share in 2025.

- By end user, the government/research institutes segment held a 25.04% market share and is expected to grow at the fastest CAGR of 7.51% during the study period.

Market Size and Volume Forecast

- Market Estimated Size (2025): USD 35.88 Billion | CAGR (2026–2035): 1.95%

- Market Projected Size (2035): USD 43.03 Billion

- Market Volume (2025): 10 Million Metric Tons | Volume CAGR (2026–2035): 1.95%

- Market Projected Volume (2035): 12.09 Million Metric Tons

- Market Pricing for 2025:

- Average Manufacturing Price: USD 3,588/MT

- Average Selling Price: USD 3,588/MT

- Pricing CAGR (2025–2035): 1.95%

What are Agrochemicals?

Rising research and development into bio-based pesticides with other biopesicides is the major factor driving market growth. The U.S. agrochemicals market comprises chemical products used in agriculture to protect crops, enhance growth, and increase yield. This includes pesticides, herbicides, fungicides, fertilizers, and plant growth regulators that improve crop productivity and protect against pests, diseases, and environmental stressors.

U.S. Agrochemicals Market Outlook:

- Industry Growth Overview: Between 2025-2034, the market is anticipated to witness substantial growth due to the government subsidies, programs, and initiatives that support modern and smooth farming practices, promoting the adoption of agrochemicals. Also, the adoption of various technologies such as precision farming, Artificial Intelligence, and digital farming tools helps increase efficiency and optimise chemical use.

- Sustainability Trends: The major sustainability trends in the market include a surge in demand for biostimulants and bio-pesticides, along with the adoption of precision agriculture boosted by digital technologies. Sustainability efforts also involve a greater emphasis on products and practices that support soil health.

- Global Expansion: Major players such as Syngenta, Bayer, and Corteva are expanding their presence through strategies such as mergers, acquisitions, and collaborations in areas such as precision agriculture and biologics. These players are also investing heavily in research and development to build new products and technologies.

Report Scope

| Report Attributes | Details |

| Market Size in 2026 | USD 36.58 Billion / Million Metric Tons |

| Expected Size by 2035 | USD 43.03 Billion / 12.09 Million Metric Tons |

| Growth Rate from 2025 to 2035 | CAGR 1.95% |

| Base Year of Estimation | 2025 |

| Forecast Period | 2025 - 2035 |

| Segment Covered | By Product, By Crop Type, By Formulation, By Application, By End User |

| Key Companies Profiled | Corteva Agriscience, Syngenta AG, FMC Corporation, ADAMA Agricultural Solutions, Nutrien Ltd., UPL Limited, Valent U.S.A. LLC, Sumitomo Chemical Co., Ltd., Dow AgroSciences, Cheminova A/S, Nufarm Limited, Sipcam Agro USA, Arysta LifeScience |

Key Technological Shifts in the U.S. Agrochemicals Market:

The key technological shifts are revolutionizing how crops are protected and cultivated. The market is moving towards more precise and sustainable methods by combining digital farming tools, using advanced material science, and harnessing the power of biological products. These advancements are further boosted by a need for stringent environmental regulations and higher agricultural productivity.

Trade Analysis of U.S. Agrochemicals Market: Import & Export Statistics:

- In 2024, the United States exported $4.83B of Pesticides, being the 75th most exported product in the United States.(Source: oec.world)

- In 2024, the main destinations of the United States' pesticide exports were: Canada ($1.57B), Brazil ($1.11B), Mexico ($532M), India ($158M), and France ($153M).(Source: oec.world)

- In 2024, U.S. agricultural exports to the European Union reached a record high of $12.8 billion, marking a 1% increase over 2023. This growth was primarily driven by strong sales of tree nuts and a record performance in distilled spirits.(Source: www.ers.usda.gov)

- In 2024, Mexico was the top U.S. agricultural export market with top products including corn, soybeans, dairy, pork, and poultry. Canada was the second-largest market, with exports valued at $28.4 billion in 2024.(Source: www.ers.usda.gov)

Value Chain Analysis of the U.S. Agrochemicals Market:

- Feedstock Procurement : It refers to the process of sourcing and acquiring the raw materials required to produce fertilizers, pesticides, and other agricultural chemicals.

- Chemical Synthesis and Processing : It includes the whole production value chain, from manufacturing the fundamental chemical building blocks to creating the final products that farmers utilize in the fields.

- Packaging and Labelling : This stage includes the important processes and materials used to contain, protect, and identify products such as fertilizers, pesticides, and herbicides.

- Regulatory Compliance and Safety Monitoring : It includes the stringent guidelines, laws, and processes that control the entire lifecycle of an agrochemical product, from development to disposal.

U.S. Agrochemicals Market 's Regulatory Landscape: Global Regulations

| Country/Region | Key Regulations/Investments |

| California | The state's Department of Pesticide Regulation (DPR) conducts a thorough, independent data review, and applicants must submit data beyond what is required by the EPA. |

| New York | Under the "Birds and Bees Protection Act," New York is phasing out certain neonicotinoid pesticides for use on outdoor ornamental plants and turf. |

| Illinois | Illinois Department of Agriculture (IDOA): The primary authority for enforcing state regulations concerning pesticides and fertilizers used for agricultural production. |

Segmental Insights

Product Insights

How Much Share Did the herbicides Segment Held in 2025?

The herbicides segment dominated the market with a 50.95% share in 2025. The dominance of the segment can be attributed to the increasing use of herbicide-resistant crops and the extensive prevalence of weeds. In addition, advancements such as precision spraying technology help to minimize herbicide usage while keeping effectiveness.

")

Companies are rapidly developing smart, customized, and sustainable solutions to enhance crop productivity.

The insecticides segment held a 25% market share and is expected to grow at the fastest CAGR of 7.5%over the forecast period. The growth of the segment can be credited to the growing demand for crop protection to boost yields, along with the cultivation of crops such as fruits and vegetables. High investment in R&D is leading to the creation of advanced and more sustainable insecticide formulations.

U.S. Agrochemicals Market Share,By Product,2025(%)

| By Product | Revenue Share, 2025 (%) |

| Herbicides | 45.22% |

| Insecticides | 20.00% |

| Fungicides | 15.00% |

| Fertilizers | 19.78% |

- Herbicides: Leading the market with 45.22% of the share, herbicides are the most widely used agrochemicals, essential for controlling unwanted weeds and grasses that compete with crops for nutrients, water, and sunlight.

- Insecticides: Representing 20% of the market, insecticides are vital for protecting crops from insect pests, helping to preserve plant health and ensure better yields by preventing damage caused by harmful insects.

- Fungicides: Accounting for 15% of the market, fungicides are used to prevent and control fungal diseases in crops, playing a key role in maintaining crop health and quality, especially in humid or wet growing conditions.

- Fertilizers: Contributing 19.78% to the market, fertilizers are used to provide essential nutrients to crops, improving soil fertility and promoting robust plant growth to maximize yields.

Crop Type Insights

Which Crop Type Segment Dominated the U.S. Agrochemicals Market in 2025?

The cereals & grains segment held a 41% market share in 2025. The dominance of the segment can be credited to the growing need for food due to population growth and ongoing government support to produce grain to ensure food security. Furthermore, cereals and grains are rapidly being used for non-food purposes such as animal feed and biofuel, further fuelling demand for their large-scale production.

The fruits & vegetables segment held a 25% market share and is expected to grow at the fastest CAGR of 8.0% over the forecast period. The growth of the segment can be driven by growing consumer demand for healthy and fresh produce, which leads to the need for higher-quality yields. Moreover, advanced farming technologies are propelling productivity and efficiency in fruit and vegetable cultivation, leading to further positive segment growth.

U.S. Agrochemicals Market Share,By Crop Type,2025(%)

| By Crop Type | Revenue Share, 2025 (%) |

| Cereals & Grains | 41.00% |

| Fruits & Vegetables | 24.00% |

| Oilseeds & Pulses | 21.00% |

| Others (Cotton, Horticulture) | 14.00% |

- Cereals & Grains: Holding the largest share of 41%, cereals and grains are the dominant crop type in the U.S. agrochemicals market, with farmers using agrochemicals to protect crops like wheat, corn, and rice from pests and diseases while promoting higher yields.

- Fruits & Vegetables: Representing 24% of the market, fruits and vegetables are a significant application for agrochemicals, where fertilizers, pesticides, and growth regulators help enhance crop quality, yield, and resistance to environmental stresses.

- Oilseeds & Pulses: Accounting for 21% of the market, oilseeds and pulses, such as soybeans, sunflower, and lentils, use agrochemicals to improve productivity, protect against pests, and ensure high-quality harvests.

- Others (Cotton, Horticulture): Contributing 14% to the market, the "Others" category includes crops like cotton and horticultural products, where agrochemicals play a crucial role in pest control, growth regulation, and boosting crop yields.

Formulation Insights

Which Formulation Type Segment Dominated the U.S. Agrochemicals Market in 2025?

The liquid formulations segment dominated the market by holding a 50.10% market share in 2025. The dominance of the segment is owed to the growing demand for easy-to-apply products coupled with the advancements in precision farming. Also, these formulations generally have better penetration into plant tissues with better bioavailability, which leads to more effective results.

The dry formulations segment held a 30% market share and is expected to grow at the fastest CAGR of 8.0 % during the forecast period. The growth of the segment is due to the growing adoption of IPM systems, which depend on strategic and targeted applications. Dry formulations such as granules have a low drift hazard, which reduces exposures to non-target areas and organisms. This makes them convenient for various applications.

U.S. Agrochemicals Market Share, By Formulation,2025(%)

| By Formulation | Revenue Share, 2025 (%) |

| Liquid Formulations | 50.10% |

| Dry Formulations | 30.00% |

| Granular Formulations | 19.90% |

- Liquid Formulations: Dominating the market with 50.10% of the share, liquid formulations are the most commonly used type of agrochemicals, favored for their ease of application and rapid absorption by crops.

- Dry Formulations: Representing 30% of the market, dry formulations, including powders and dusts, are typically used for more targeted applications, offering effective control over pests and diseases while being more stable for storage.

- Granular Formulations: Accounting for 19.90% of the market, granular formulations are often used for controlled-release applications, providing long-lasting effects and reducing the need for frequent reapplication in soil treatment and fertilization.

Application Insights

How Much Share Did the Crop Protection Segment Held in 2025?

The crop protection segment held a 56% market share in 2025. The dominance of the segment can be attributed to the surge in pest and disease pressure exacerbated by climate change and increasing adoption of precision agriculture methods. The use of technologies such as sensors, drones, and Artificial Intelligence enables the more effective and targeted application of agrochemicals, which minimizes overall chemical use while enhancing crop protection.

The soil treatment & fertility segment held a 30% market share and is expected to grow at the fastest CAGR of 8.0% during the projected period. The growth of the segment can be credited to the growing demand for increased agricultural productivity and technological innovations in precision agriculture. Increasing consumer awareness regarding organic and sustainably produced food is fuelling the adoption of bio-based soil treatments soon.

U.S. Agrochemicals Market Share,By Application,2025(%)

| By Application | Revenue Share, 2025 (%) |

| Crop Protection | 56.00% |

| Soil Treatment & Fertility | 30.00% |

| Plant Growth Regulation | 14.00% |

- Crop Protection: Leading the market with 56% of the share, crop protection is the largest application of agrochemicals, including pesticides, herbicides, and fungicides, used to safeguard crops from pests, diseases, and weeds.

- Soil Treatment & Fertility: Representing 30% of the market, soil treatment and fertility agrochemicals are used to improve soil health and fertility, promoting better crop growth through the use of fertilizers and soil conditioners.

- Plant Growth Regulation: Accounting for 14% of the market, plant growth regulators are used to influence the growth of plants, improving crop yield, quality, and the overall efficiency of farming operations.

End User Insights

Which End User Segment Dominated the U.S. Agrochemicals Market in 2025?

The commercial farmers segment dominated the market by holding a 51.30% share in 2025. The dominance of the segment can be linked to the growing demand for higher crop yields because of shrinking arable land and population growth. Furthermore, partnerships among companies are boosting advancements in creating more efficient and sustainable agrochemical formulations.

The government/research institutes segment, which held a large market share, is expected to grow at the fastest CAGR of 7.5% during the study period. The growth of the segment can be driven by the ongoing shift toward bio-based products, along with the rise in concerns regarding environmental pollution and climate change. Moreover, research is more focused on biopesticides, which are obtained from natural materials, to fulfil the need for eco-friendly solutions.

U.S. Agrochemicals Market Share,By End User,2025(%)

| By End User | Revenue Share, 2025 (%) |

| Commercial Farmers | 51.30% |

| Government/Research Institutes | 22.00% |

| Smallholder Farmers | 17.00% |

| Agrochemical Distributors | 9.70% |

- Commercial Farmers: Leading the market with 51.30% of the share, commercial farmers are the largest consumers of agrochemicals, using them to enhance crop yields, protect plants from pests, and improve overall agricultural productivity.

- Government/Research Institutes: Representing 22% of the market, government bodies and research institutes play a key role in the development, regulation, and application of agrochemicals, focusing on agricultural research and sustainable farming practices.

- Smallholder Farmers: Accounting for 17% of the market, smallholder farmers use agrochemicals to improve the efficiency and productivity of their farms, often with a focus on improving crop quality and increasing food security.

- Agrochemical Distributors: Contributing 9.70% to the market, agrochemical distributors are responsible for the wholesale distribution of agrochemicals, ensuring their availability to farmers across various regions.

Country Insights

Midwest U.S. Agrochemicals Market Trends

The Midwest region dominated the market with a 40% share in 2025. The dominance of the region can be attributed to the rapid adoption of technologies such as GPS, data analytics, and AI, which enable more targeted and precise application of agrochemicals. In addition, this region is crucial for the production and trade of grains and oilseeds, impacting positive market growth.

South U.S. Agrochemicals Market Trends

The South region held 25% market share and is expected to grow at 8.0% CAGR during the forecast period. The growth of the region can be credited to the increasing emphasis on sustainable and biological products, coupled with the surge in research and development in the southern states. Furthermore, Government initiatives and regulations are facilitating the development of more sustainable and safer agrochemicals.

Recent Development

- In February 2025, Landus and TalusAg, an agriculture technology company, announced that they had started production of green ammonia in North America. The companies are actively deploying additional systems with an expansion planned across the United States.(Source: fuelcellsworks.com)

Top Vendors in the U.S. Agrochemicals Market & Their Offerings:

- Bayer CropScience: Bayer CropScience is a major player in the U.S. agrochemical market, offering a wide range of products and digital solutions that include traditional chemical-based solutions like herbicides, fungicides, and insecticides.

- BASF SE: BASF SE is a major player in the U.S. agrochemicals market, offering a broad portfolio of solutions including herbicides, fungicides, insecticides, seeds, seed treatments, and biological products.

- Corteva Agriscience: Supplies crop protection chemicals and seeds, enhancing productivity with advanced R&D and sustainable practices.

- Syngenta AG: Provides herbicides, fungicides, and insecticides while offering digital tools and seed innovations for efficient U.S. farming.

Other Players

- Corteva Agriscience

- Syngenta AG

- FMC Corporation

- ADAMA Agricultural Solutions

- Nutrien Ltd.

- UPL Limited

- Valent U.S.A. LLC

- Sumitomo Chemical Co., Ltd.

- Dow AgroSciences

- Cheminova A/S

- Nufarm Limited

- Sipcam Agro USA

- Arysta LifeScience

Segment Covered

By Product

- Herbicides

-

- Glyphosate-Based

- Atrazine-Based

-

- Insecticides

-

- Organophosphates

- Neonicotinoids

-

- Fungicides

-

- Triazoles

- Strobilurins

-

- Fertilizers

-

- Nitrogen-Based

- Phosphate-Based

- Potash-Based

-

By Crop Type

- Cereals & Grains

- Fruits & Vegetables

- Oilseeds & Pulses

- Others (Cotton, Horticulture)

By Formulation

- Liquid Formulations

- Dry Formulations

- Granular Formulations

By Application

- Crop Protection

- Soil Treatment & Fertility

- Plant Growth Regulation

By End User

- Commercial Farmers

- Government/Research Institutes

- Smallholder Farmers

- Agrochemical Distributors

Tags

FAQ's

Select User License to Buy

Figures (2)