Content

Surface Treatment Chemicals Market Growth, Demand and Production Forecast

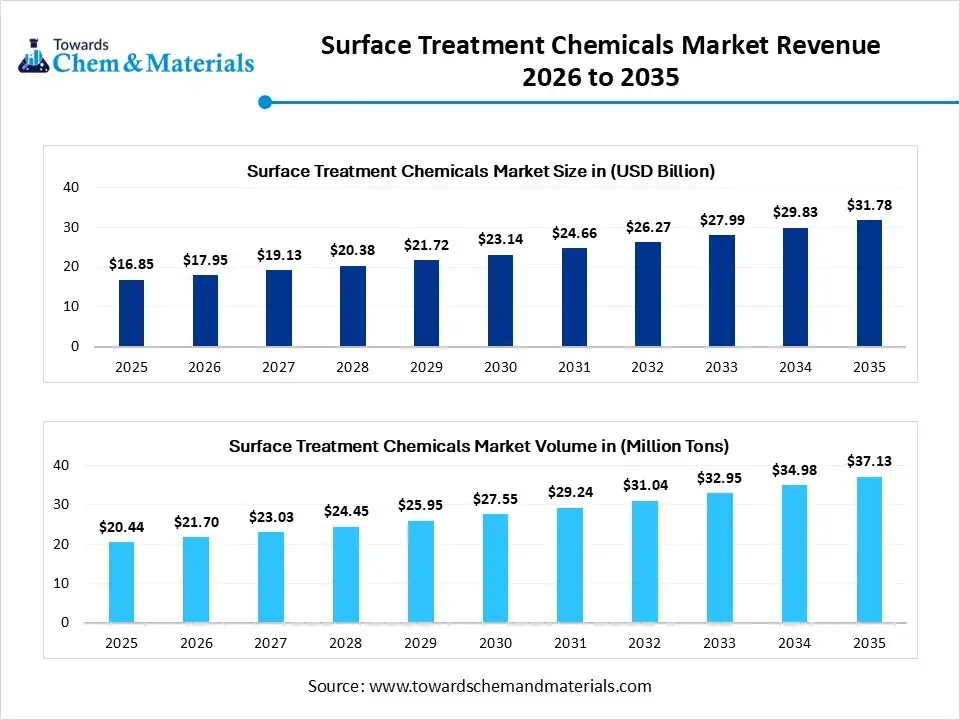

The surface treatment chemicals market size was valued at USD 16.85 billion in 2025 and is expected to reach USD 17.95 billion in 2026, further projected to grow to USD 31.78 billion by 2035, registering a CAGR of 6.55% during 2026–2035. In volume terms, the market is anticipated to expand from 20.44 million tons in 2025 to 37.13 million tons by 2035 at a CAGR of 6.15%. the surface treatment chemicals are defined by their environmental compatibility and longevity, which drive interfacial engineering and substrate protection. The manufacturers' focus on the circular economy is accelerating the shift towards chromium-free and bio-based formulations, boosting innovation in green chemistry. As the rising demand in precision industries, such as renewable energy, advanced adhesives, and semiconductors, requires improved surface energy, molecular bonding, and corrosion inhibition, the adoption of surface treatment chemicals is enabled. Additionally, the integration of smart coatings and nanofabrication ensures their demand in modern and automated industrial infrastructure.

Key Takeaways

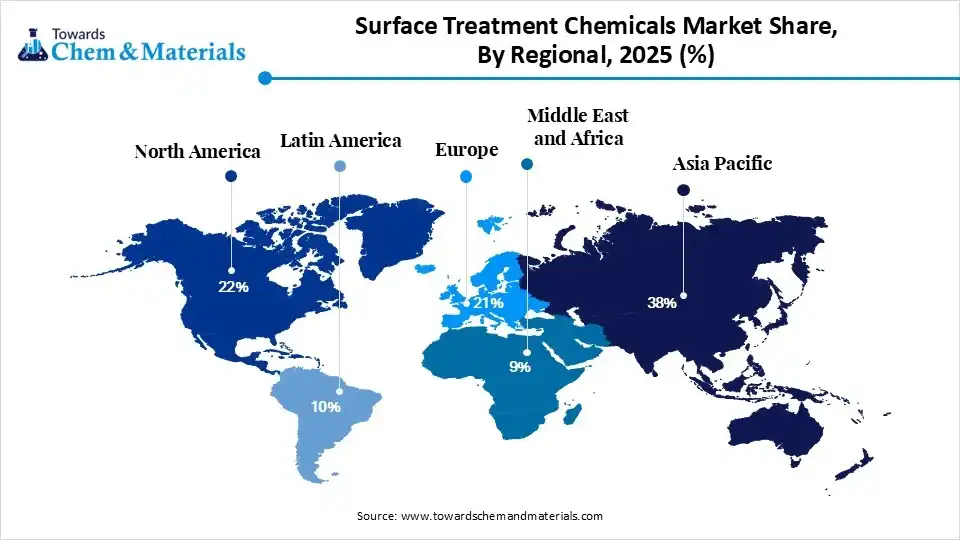

- By region, Asia Pacific dominated the surface treatment chemicals market by holding 38% share in 2025 and is expected to grow at the fastest with a CAGR of 6.80% during the forecast period.

- By region, North America held the 22% market share in 2025 and expects notable growth in the market with 5.20% CAGR during the forecast period.

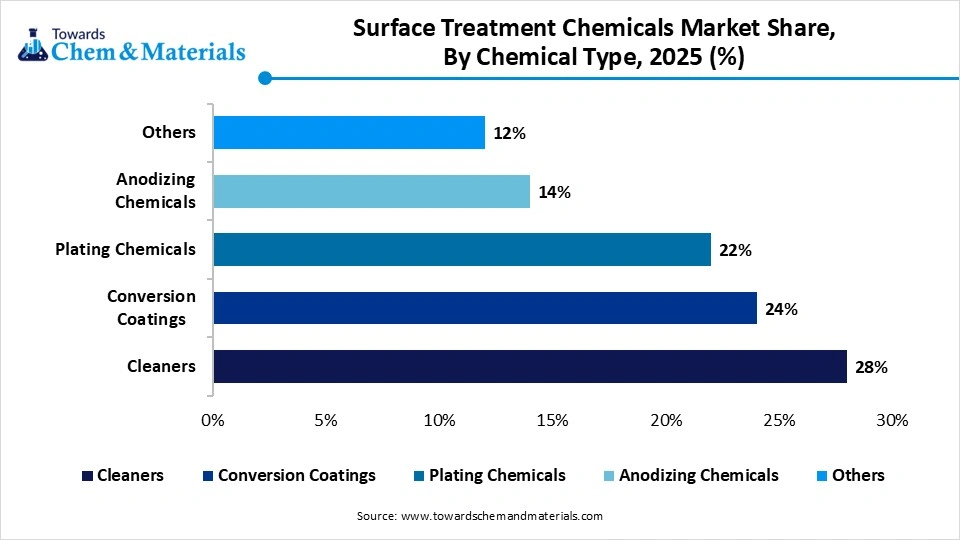

- By chemical type, the cleaners segment dominated the market with the largest share of 28% in 2025

- By chemical type, the plating chemicals segment held 22% market share in 2025 and is expected to grow at the fastest CAGR of 6.40% over the forecast period.

- By substrate, the metals segment dominated the market with the largest share of 72% in 2025

- By substrate, the plastics segment held 13% market share in 2025 and is expected to grow at the fastest CAGR of 6.20% over the forecast period.

- By application, the automotive segment dominated the market with the largest share of 29% in 2025

- By application, the electronics segment held 21% market share in 2025 and is expected to grow at the fastest CAGR of 6.50% over the forecast period.

- By process, the coating segment dominated the market with 27% share in 2025 and is expected to grow at the fastest CAGR of 6.20% over the forecast period.

At a glance

- Market Estimated Size (2025): USD 16.85 Billion | CAGR (2026–2035): 6.55%

- Market Projected Size (2035): USD 16.85 Billion

- Market Volume (2025): 20.44 Million Tons | Volume CAGR (2026–2035): 6.15%

- Market Projected Volume (2035): 37.13 Million Tons

- Market Pricing (2025):

- Average Manufacturing Price: USD 1.66 per kg

- Average Selling Price: USD 3.45 per kg

- Pricing CAGR (2025–2035): 2.19%

Surface Treatment Chemicals Market Trends

- Government Initiatives and Strategic Partnership: The government supports and invests in advanced surface technologies to increase operational efficiency through strategic collaboration that allows market expansion.

- Stringent Environmental Protocols: The main driver that shapes this trend is driven by enforcing stringent regulations regarding treatment and waste minimization, to reduce environmental impact, conserve resources, and promote green chemistry.

Key Technological Shifts and AI in the Surface Treatment Chemicals Market

The technological and digital integration is transforming the surface treatment chemicals market. In manufacturing, the smart sensor and automated dosing systems enable real-time, precise monitoring and lower chemical waste by managing operational efficiency.

The adoption of Industry 4.0 in surface treatment chemicals production offers process repeatability and coating uniformity. Additionally, machine leaning boost the discovery of eco-friendly alternatives and improve operational durability of treated surfaces.

Supply Chain Analysis of the Surface Treatment Chemicals Market

Feedstock Procurement: The key stage of sourcing alkalis, acids, specialty resins, and surfactants. Suppliers offer manganese, zinc, and phosphate utilized for conversion coatings and industrial infrastructure.

- Key Players: Dow, Inc., Solvay S.A., BASF SE, and Huntsman Corporation

Chemicals Manufacturing and Formulation: The stage of conversion of raw material into electroplating solution, passivation treatments, and pickling agents. The stage focuses on innovation to develop water-based technology and chrome-free solutions.

- Key Players: Henkel AG & Co. KGaA, The Sherwin-Williams Company, Chemetall, PPG Industries, and Quaker Houghton

End-use Integration and Distribution: The final stage includes integration of surface treatment chemicals to original equipment manufacturers, such as aerospace components, surface finishing shops, automotive assembly, and consumer electronics.

- Key Players: Tesla, Caterpillar, Boeing, Samsung, and General Motors

Regulatory Framework: Surface Treatment Chemicals Market

| Region | Key Regulations | Regulatory Focus |

| Global | Stockholm Convention, ISO Standards | A strict environmental management system and a ban on organic pollutants. |

| European Union | REACH, RoHS, IPPC Directive | Mandatory phase-out of hexavalent chromium and stringent limits on cobalt and boron in plating and VOC emissions. |

| North America | EPA TSCA, PFAS Reporting and OSHA Standards | Eliminating hazardous surfactants and pushing manufacturers towards low-VOC compliance for solvent-based cleaners. |

| Asia Pacific | China GB Standards, ICMSR Rules, Blue Sky Action, and E-Waste Rules | Standardization of heavy metal limits in metal finishing and standards for export safety |

Surface Treatment Chemicals Market Dynamics

Driver

Substantial Investment in Industrial Infrastructure

The rising demand for lightweighting and long-term corrosion inhibitors is driving substantial investment in emerging economies. Additionally, the rising urban population is a key catalyst for the rapid expansion of the aerospace and automotive industries.

Restraints

Stringent Environmental Regulation and Feedstock Volatility

The strict environmental compliance focusing on hexavalent chromium, while volatile costs of raw chemical materials and superior energy needs for processing restrain the market growth.

Opportunity

Integration of Digital and Nano-Technology

The manufacturers focus on integration of nano-fabrication and AI-driven modeling to enhance durability and eco-friendly coatings through the multi-metal processing for streamlining complex assembly and production lines.

Segmental Insights

Chemical Type Insights

The Cleaners Segment Dominated the Surface Treatment Chemicals Market with 28% of Market Share in 2025

The cleaners segment dominated the market with the largest share of 28% in 2025, driven by its pretreatment ability that offers surface purity and operational sustainability. These formulations focus on multi-metal compatibility and low-temperature efficiency, that driving the innovation in aqueous-based and biodegradable systems. By integrating surfactant technology, cleaners maximized adhesion and corrosion resistance, that make them key for industrial cleaning.

The plating chemicals segment held the 22% market share in 2025 and is expected to grow at the fastest CAGR of 6.40% over the forecast period. It acts as a high-purity electrochemical solution that replaces hazardous precursors with chromium-trioxide-free alternatives. The research preferred advancement in next-generation electrolytes to enhance atomic-level accuracy in semiconductor and modern electrification sectors. Plating chemicals, like electroplating and electroless plating, offer higher solderability, thermal resilience, and electromagnetic protection by maintaining void-free deposition for precision engineering.

The conversion coatings segment held the 24% market share in 2025, driven by its ability to improve the structural integrity of aluminium and galvanized steel and its ability to create self-healing thin films. The conversion coating, like phosphate, chromates, and non-chromate, represents surface transformers essential for lightweighting and protection in topcoats, energy, an automotive industry. As the industry shifts towards zirconium-based and chrome-free alternative align with room-temperature processing, driving the growth.

The anodizing chemicals segment held 14% market share in 2025, due to its electrochemical passivation that thickens native oxide layers into a ceramic matrix. As innovation shifts towards eco-friendly sealing agents and low-voltage electrolyte that, anodizing chemical offers optimal hexagonal porosity, abrasion resistance, and UV stability. Additionally, this segment is essential for high-performance transport and satellite infrastructure.

Substrate Insights

The Metals Segment Dominated the Surface Treatment Chemicals Market with 72% of Market Share in 2025

The metals segment dominated the market with the largest share of 72% in 2025. It is a surface interface and electrochemical stabilizer for industrial chemical applications. With the rising demand for atomic-level non-ferrous alloys to moderate oxidation and intergranular corrosion, metals enable long-term adhesion and mechanical resilience in renewable energy and transport infrastructure. Advancement of multi-substrate compatibility enables uniform reactivity across titanium, magnesium, and cold-rolled steel for high-performance engineering.

The plastics segment held the 13% market share in 2025 and is expected to grow at the fastest CAGR of 6.20% over the forecast period. The expansion is driven fueled by a shift towards non-etching adhesion promoters and bio-based surfactants through advanced interfacial modification and molecular functionalization. Plastics offer high-tenacity adhesion and thermal resilience for automotive, aerospace, and high-frequency electronics applications.

The glass segment held the 8% market share in 2025, due to the requirement for surface energy advancement to enhance interfacial adhesion across non-porous, inorganic substrates. This substrate utilizes organofunctional silane to establish covalent linkages for smart-device glass and solar energy systems. The rising focus on fluorinated chemistries and nano-scale modification of glass offers liquid-repellent, optical clarity, and structural performance.

Application Insights

The Automotive Segment Dominated the Surface Treatment Chemicals Market with 29% of Market Share in 2025

The automotive segment dominated the market with the largest share of 29% in 2025, serving as a high-volume driver for advanced surface functionalization to multi-material lightweighting and battery-system protection. Surface treatment chemicals offer galvanic shielding, corrosion resistance, and molecular precision across hybrid assemblies and high-adhesion e-coats. Additionally automotive sector focuses on zirconium-driven pretreatments and the adoption of thin-film conversion drives its high-speed automation for the longevity of next-generation vehicles.

The electronics segment held the 21% market share in 2025 and is expected to grow at the fastest CAGR of 6.50% over the forecast period. The growth is driven by its high-frequency reliability and micron-scale functionalization. The shift toward halogen-free and cyanide-free electrolytes to promote green electronics infrastructure is boosting the demand for surface treatment chemicals. It is used in electroless plating, semiconductor packaging, dense interconnects, and the advancement of high-performance computing and AI hardware.

The industrial machinery segment held the 16% market share in 2025, due to industrial demand for heavy-duty phosphating and tribological performance, where surface treatment chemicals offer high wear resistance and frictional control. In infrastructure equipment, its ensure extended service life and mechanical resilience by integrating non-ceramic reinforcement and self-lubricating surface treatments.

The construction segment held 14% market share in 2025 due to the shift towards sustainability and rapid urbanization to meet green-building compliance and demanding environmental standards. Surface treatment chemicals improve durability and corrosion resistance utilizes in the waterproofing sealants, adhesion promoters, and conversion coatings that make its key material for concrete and structural steel.

Process Insights

The Coating Segment Dominated The Market With 27% Share In 2025

The coating segment dominated the market with 27% share in 2025 and is expected to grow at the fastest CAGR of 6.20% over the forecast period. It is a functional layer that enhances corrosion shield and surface hardness that converts substrate finishing. The coating industry is shifting towards thin-film and solvent-free technologies to boost material longevity and adhesion for secondary layers to meet next-generation eco-friendly coating standards.

The cleaning segment held the 26% market share in 2025, known for its optimal removal of impurity and surface activation efficiency, that boosting growth of multi-metal cleaners and low-temperature formulation. Cleaning acts as a pre-treatment process that utilizes specialized chemical cleaners to prepare the substrate for plating and coating with performance reliability.

The pretreatment segment held the 24% market share in 2025, driven by its structural integrity and barrier protection that represent surface modification for final finishes. Using conditioning agents and chemical etching pretreatment optimizes surface energy and mechanical bonding. The move towards sludge-free chemicals and integration of de-smutting to avoid coating delamination and maintain manufacturing workflows.

The finishing segment held the 23% market share in 2025. It is a visual enhancement and a protective stage that offers a final glossy and textured finish. This process utilizes surface refinements by offering superior weatherability and chemical resistance. The rising adoption of smart additives and ultra-thin coatings manufacturer achieving longevity and self-l=cleaning that accelerating the growth.

Regional Insights

How Did the Asia Pacific Dominated the Surface Treatment Chemicals Market in 2025?

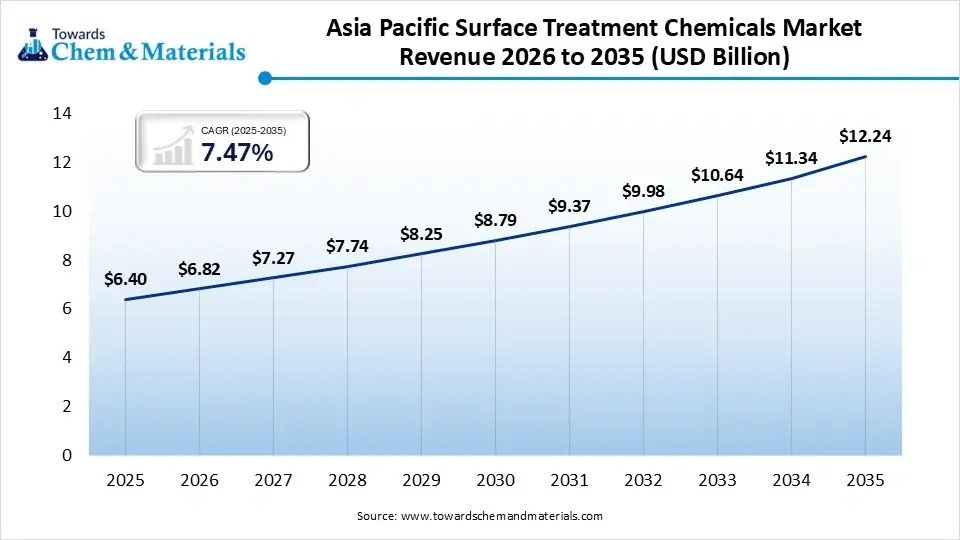

The Asia Pacific surface treatment chemicals market size was estimated at USD 6.40 billion in 2025 and is projected to reach USD 12.24 billion by 2035, growing at a CAGR of 7.47% from 2026 to 2035 The region is a key hub for industrial manufacturing and domestic capacity expansion of surface treatment chemicals. Asia Pacific leads in consumer electronics, hybrid material assembly, and heavy machinery production lines. Additionally, the region shifts towards green and sustainable formulation to meet modern regulatory compliance and cost-competitiveness.

")

China Surface Treatment Chemicals Market Growth Trends

China's market growth is driven by its regional shift towards electric vehicle manufacturing and heavy machinery expansion. Chinas stringent environmental mandates and export compliance enable the adoption of bio-based and nano-ceramic technologies. China's focus on carbon neutrality is driving domestic growth.

North America held the 22% market share in 2025 and is expected to experience notable growth in the market with a CAGR of 5.20% during the forecast period, serving as technological driven region. North America's rapid shift towards renewable chemistries and advanced material science to meet strict environmental compliance is boosting the domestic expansion. Additionally, the region focuses on high-performance surface modification for industrial safety and clean-air compliance.

U.S. Surface Treatment Chemicals Market Growth Trends

The United States is witnessing significant growth in the market that focuses on advancement in the application of innovation. The U.S. shift towards electrification and chromium-free formulation to meet PFAS-compliance and industrial safety. The regional major players investing in sustainability and technological advancement are accelerating the regional dominance in the market.

Recent Developments

- In March 2026, CHEMEON Surface Technology and SurTec formed a strategic partnership to accelerate the expansion of surface technology. The alliance focuses on strengthening high-performance and sustainable surface treatment solutions.

- In August 2025, Henkel announced launched od new additives for optimizing the anodizing of aluminium with Henkel Bonderite M-AD 2000A. The launched shorter anodizing process time and treats aluminium surface with sustainability and efficiency.

Top Companies in the Surface Treatment Chemicals Market

- Henkel Balti OÜ

- Nippon Paint Holdings Co., Ltd.

- Chemetall GmbH

- MKS | Atotech

- Element Solutions Inc

- The Sherwin-Williams Company

- Solvay

- Lamberti S.p.A

- Hainan Zhongxin Chemical Co., Ltd

- Axalta Coating Systems

Surface Treatment Chemicals Market Segment Covered in the Report

By Chemical Type

- Cleaners

- Alkaline Cleaners

- Acidic Cleaners

- Solvent-based Cleaners

- Conversion Coatings

- Phosphate Coatings

- Zinc Phosphate

- Iron Phosphate

- Chromate Coatings

- Non-Chromate Coatings

- Phosphate Coatings

- Plating Chemicals

- Electroplating Chemicals

- Nickel Plating

- Copper Plating

- Zinc Plating

- Electroless Plating

- Electroplating Chemicals

- Anodizing Chemicals

- Others

By Substrate

- Metals

- Steel

- Aluminum

- Copper

- Zinc

- Plastics

- Glass

- Others

By Application

- Automotive

- Body Coatings

- Engine Components

- Aerospace

- Electronics

- Printed Circuit Boards

- Semiconductor Components

- Industrial Machinery

- Construction

- Others

By Process

- Cleaning

- Pretreatment

- Coating

- Finishing

By Regions

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Asia Pacific

- China

- India

- Japan

- South Korea

- Latin America

- Brazil

- Argentina

- Middle East & Africa

- Saudi Arabia

- South Africa

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

FAQ's

Select User License to Buy

Figures (4)