Content

What is the Quetiapine Intermediate Chemicals Market Size and Share?

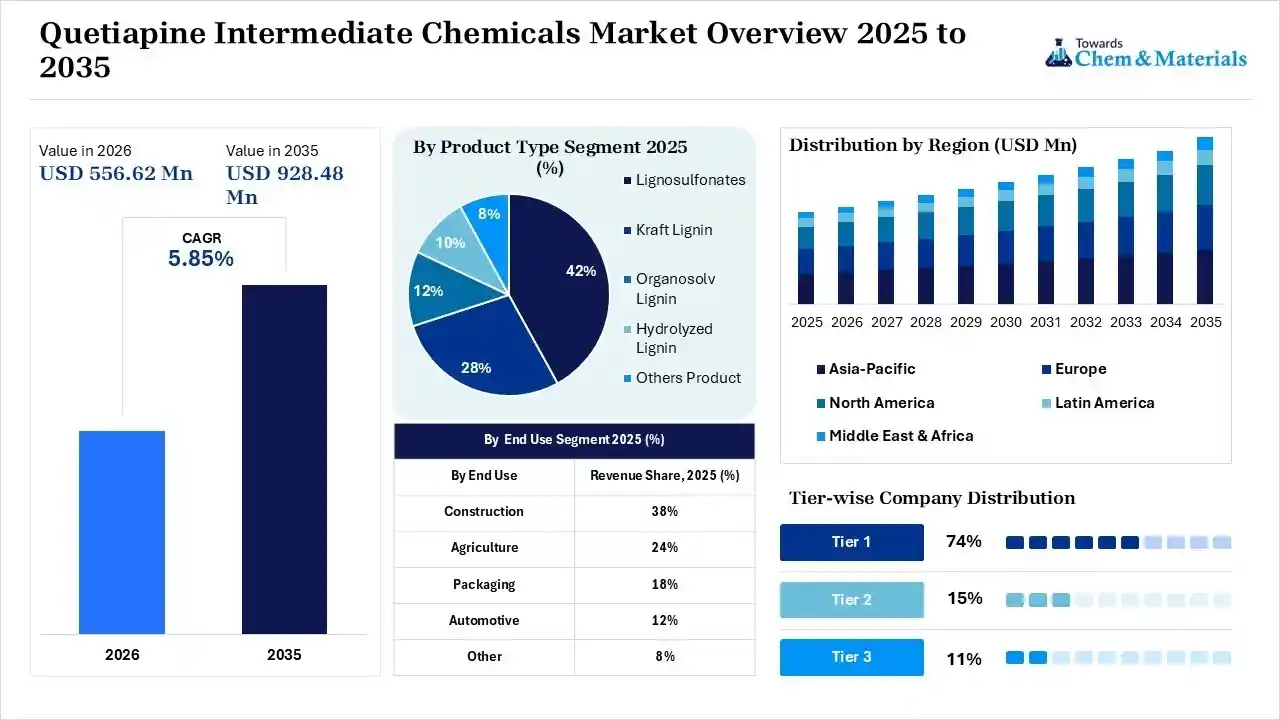

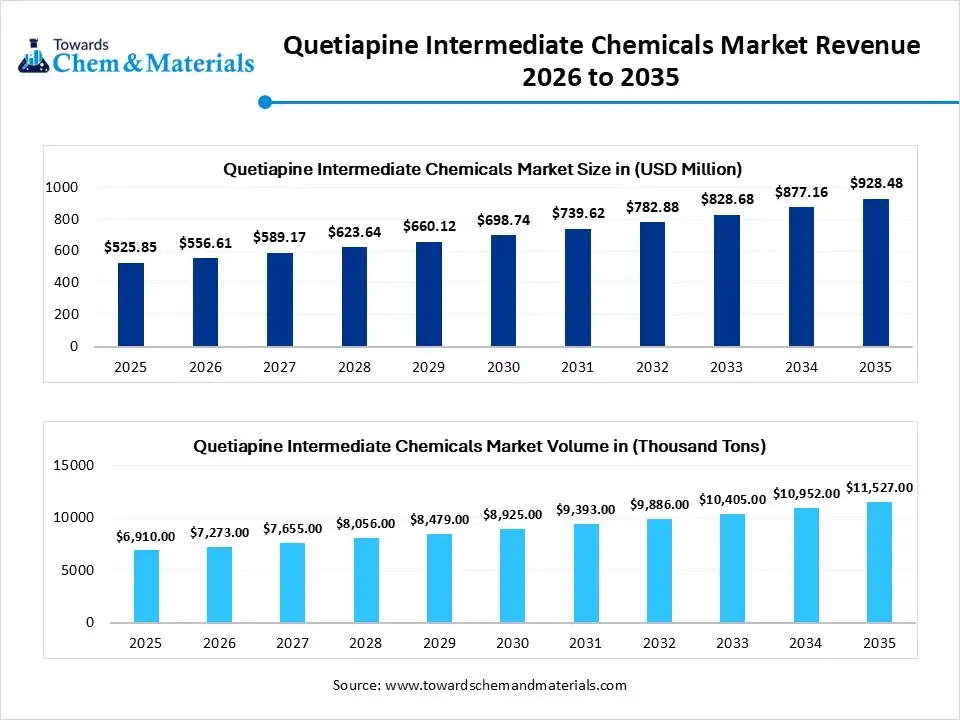

The global quetiapine intermediate chemicals market size was valued at USD 525.85 million in 2025, is estimated to reach USD 556.61 million in 2026, and is projected to reach USD 928.48 million by 2035, exhibiting a compound annual growth rate (CAGR) of 5.85% over the forecast period from 2026 to 2035.Asia Pacific dominated the quetiapine intermediate chemicals market with the largest revenue share of 33.0% in 2025 and is expected to grow at the fastest CAGR of 6.01% during the forecast period. In terms of volume, the quetiapine intermediate chemicals market is projected to grow from 6,910 thousand tons in 2025 to 11,527 thousand tons by 2035. growing at a CAGR of 5.25% from 2026 to 2035.Increasing mental health awareness and patient expectations are the key factors driving market growth. Also, rapid transitions towards cost-effective generic manufacturing coupled with the ongoing advancements in chemical syntheses can fuel market growth further. Moreover, emerging nations are witnessing enhanced healthcare access, leading to market growth soon.

Market Highlights

- By region, Asia Pacific dominated the market with the largest share of 33.0% in 2025 and is expected to grow at the fastest CAGR of 7.10% over the forecast period. The growth of the region can be attributed to the growth of generic drug manufacturing and rising mental health awareness in emerging economies.

- By region, Europe held a market share of 27.0% in 2025. The growth of the region can be credited to the increasing mental health diagnoses, robust regional R&D, and ongoing drug manufacturing.

- By product, the 1-[2-(2-hydroxyethoxy) ethyl] piperazine segment dominated the market with the largest share of 46% in 2025. It is a crucial piperazine-sidechain intermediate mainly used in the synthesis of quetiapine, an active pharmaceutical ingredient (API) and an extensively prescribed antipsychotic.

- By product, the dibenzo[b,f][1,4]thiazepin 11 (10 H)-one segment held a market share of 38.00% in 2025 and is expected to grow at the fastest CAGR of 6.2% over the forecast period. It acts as the basic core scaffold required to synthesize quetiapine. It is the main and most vital precursor used by pharmaceutical companies.

- By end use, the pharmaceuticals segment dominated the market with the largest share of 91.0% in 2025 and is expected to grow at the fastest CAGR of 5.90% during the projected period. This segment is characterized by ongoing continuous synthesis of active pharmaceutical ingredients (APIs) for branded and generic psychiatric drugs.

Rise in Generic Manufacturing Supports Market Growth

The increase in generic production is heavily fueling demand for major intermediates such as dibenzo[1,4] thiazepine-11(10H)-one, which is crucial for the synthesis of quetiapine. High grade and consistent quality of these intermediates are vital as they directly impact the safety and efficacy of the final pharmaceutical product, presenting key opportunities in the market.

Market players are heavily investing in process optimization and capacity growth to ensure a convenient supply of these intermediates. This includes enhancements in yield optimization, reaction efficiency, and impurity control.

This is crucial for fulfilling regulatory standards and maintaining competitiveness in the market.

Global Investment Flow for Quetiapine Intermediate Chemicals 2026

The emerging nations are using their strong active pharmaceutical ingredient (API) infrastructure to dominate the export flow, while major market players are increasingly expanding their manufacturing capacities.

Solstice Advanced Materials, a global leader in high-performance specialty materials, has announced a planned investment of over $220 million to establish a new manufacturing facility in Colonial Heights, Virginia. This strategic project is projected to generate 100 full-time employment opportunities within the region by 2029.(Source: indianchemicalnews)

Quetiapine Intermediate Chemicals Market Trends

- The growing burden of psychiatric disorders across the globe is the latest trend in the market shaping positive market growth. Quetiapine's broad label, efficacy, and favorable safety profile as compared to older antipsychotics make it a key pharmacological option for psychiatrists managing comorbid and complex presentations.

- In recent years, major market players such as Mylan, Sun Pharmaceutical, Teva Pharmaceutical Industries, Lupin, Aurobindo Pharma, and Zydus Cadila have established robust production and distribution footprints across semi-regulated and regulated markets, allowing competing pricing strategies that make quetiapine more accessible psychiatric medications across the globe.

- Growing emphasis on sustained formulations is the future trend in the market driving market growth. This surge in consumer demand for long-acting treatments has surged the need for high-purity and specialized chemical intermediates catered to specifically for extended-release matrices.

Report Scope

| Report Attributes | Details |

| Market Size and Volume in 2026 | USD 556.61 Million / 7,273 Thousand Tons |

| Market Size and Volume by 2035 | USD 928.48 Million / 11,527 Thousand Tons |

| Growth Rate from 2025 to 2035 | CAGR 5.85% |

| Base Year from Estimation | 2025 |

| Forecast Period | 2025 - 2035 |

| High Impact Region | Asia Pacific |

| Segment Covered | By Product, By End Use, By Regions |

| Key Companies Profiled | Merck KGaA, Aarti Pharmalabs, Luye Pharma Group, Ami Organics Ltd, IOL Chemicals & Pharmaceuticals Ltd, AR Lifesciences, ALLCHEM LIFESCIENCE PVT. LTD., Aether Industries, Shreeneel Chemicals, AstraZeneca |

AI-Powered Predictive Formulations in the Quetiapine Intermediate Chemicals Market

AI-powered predictive formulation is transforming the market by boosting API synthesis, facilitating excipient compatibility for modified-release (MR) tablets, and extensively reducing formulation timelines for complex platforms such as self-nanoemulsifying drug delivery systems (S-SNEDDS). Furthermore, AI models, like tree ensemble regression, process features such as packaging materials, API content percentage, and storage conditions to predict shelf life and drug stability.

Supply Chain Analysis of the Quetiapine Intermediate Chemicals Market

Production & Processing

- It involves the production and processing of key starting Materials needed to synthesize quetiapine, an extensively prescribed atypical antipsychotic. Manufacturing these chemical precursors needs innovative processing methodologies to fulfill stringent pharmaceutical standards. Manufacturing often begins with chemical reactions like condensation, reductive amidation, and chlorination.

AstraZeneca PLC: The original innovator behind Seroquel, it maintains deep ties across the vertical chemical pipeline.

- Other Key Players are Ami Organics Limited, Aarti Pharmalabs Limited

Quality Testing and Certification

- It includes strict, rigorous analytical and regulatory processes needed to verify that chemical compounds should fulfill stringent pharmaceutical purity and safety standards before they are used to synthesize finished quetiapine. Market players rely heavily on certified standards, such as Supelco Quetiapine-Related Compounds, to calibrate instruments and validate their assays.

- Teva Pharmaceuticals: A global generic giant that sources and heavily audits third-party intermediate suppliers for pharmacopeial alignment.

- Other Key Players are Cipla, Lupin, Hetero Drugs, and Cambrex.

Distribution to Industrial Users

- It includes the supply chain channel where solvents, raw materials, and tricyclic building blocks are sold directly from chemical manufacturers and specialized distributors to pharmaceutical companies. These market players then create and formulate the active pharmaceutical ingredient (API), quetiapine, utilized to treat schizophrenia and bipolar disorder. Chemical and pharma-grade distributors act as intermediaries, decreasing the gap between bulk chemical plants & drug manufacturers.

- AR Lifesciences: A trusted manufacturer specializing in core tricyclic intermediates and side-chain components for quetiapine fumarate.

- Other Key Players are Aarti Pharmalabs Limited, AR Lifesciences.

Quetiapine Intermediate Chemicals Market’s Regulatory Landscape: Global Regulations

| Country/Region | Key Regulations |

| United States | The U.S. Food and Drug Administration (FDA) oversees the supply chain through mandatory Drug Master Files (DMFs). Manufacturers of quetiapine intermediates must submit a Type IV DMF (for excipients, colorants, flavors, or materials used in their preparation) or be clearly cited in the API manufacturer's Type II DMF. |

| European Union | EU-GMP & ASMF: The European Medicines Agency (EMA) enforces equivalent standards to the FDA. Intermediate chemical criteria are reviewed through the Active Substance Master File (ASMF) procedure during marketing authorization. |

| India | CDSCO & State FDA Control: The Central Drugs Standard Control Organisation (CDSCO) regulates manufacturing licences through Schedule M of the Drugs and Cosmetics Act, which outlines domestic GMP parameters. |

| China | NMPA Mandates: The National Medical Products Administration (NMPA) requires the joint review of APIs, excipients, and intermediate packaging materials alongside the final drug formulation. |

Market Dynamics

Driver

Growing Off-Label Prescribing Therapy Adoption

The increasing utilization of the compound in off-label indications, most commonly generalized anxiety disorder, insomnia, and post-traumatic stress disorder, is the major factor driving market growth. In addition, as awareness of treatment-resistant major depressive disorder as a distinct clinical entity grows, the adjunctive utilization of extended-release quetiapine, formally approved as an add-on therapy to antidepressants, expands rapidly across the globe. The growing empirical foundation for these applications, along with heightened clinician comfort with quetiapine's pharmacological mechanisms, optimizes more widespread therapeutic utilization.

Restraint

Supply Chain Fragility

Major market players are increasingly moving away from single-country, low-cost sourcing models (primarily based in India and China) toward regional, resilient supply chains, which can be the major factor hindering the growth of the market. Moreover, unexpected manufacturing bottlenecks at key formulation facilities have created regional shortages across the EU, severely disrupting established procurement agreements for raw intermediates.

Opportunity

Integration of Digital Health

The ongoing growth of telehealth services and digital mental health platforms has changed how these medicines, such as quetiapine, are prescribed and dispensed, creating lucrative opportunities in the market. Furthermore, the expansion of telehealth has successfully mitigated obstacles to psychiatric care by overcoming geographical constraints, reducing stigma-related hurdles, and expanding access for patients unable to attend traditional face-to-face consultations. The blockchain technology in the healthcare market is increasingly integrating decentralized ledger solutions to track pharmaceutical assets. This technology ensures end-to-end traceability of generic quetiapine throughout multi-tier distribution networks in emerging markets, which guarantees product authenticity and reliability.

Segmental Insights

Product Insights

The 1-[2-(2-hydroxyethoxy) ethyl] piperazine segment dominated the market with the largest share of 46% in 2025. It is a crucial piperazine-sidechain intermediate mainly used in the synthesis of Quetiapine Active Pharmaceutical Ingredient (API), an extensively prescribed antipsychotic. It acts as a crucial structural component deciding the drug's core pharmacological activity. In addition, this compound acts as a fundamental reagent in the synthesis of quetiapine fumarate, an atypical antipsychotic used globally for the management of schizophrenia, bipolar disorder, and major depressive disorder. It is generally sold in high-purity grades (98% to 100% assay) to ensure strict compliance with international pharmaceutical impurity benchmarks.

") The dibenzo[b,f][1,4]thiazepin 11 (10 H)-one segment held a market share of 38.00% in 2025 and is expected to grow at the fastest CAGR of 6.2% over the forecast period. It acts as the basic core scaffold needed to synthesize quetiapine. It is the main and most vital precursor used by pharmaceutical companies to formulate quetiapine medication prescribed for schizophrenia and bipolar disorder. Also, it is synthesized via multi-step processes from baseline precursors like 1-chloro-2-nitrobenzene; this compound serves as a versatile agent for the growth of novel therapeutic agents. Due to its specialized role in directly streamlining the synthesis process, this segment consistently yields superior results compared to other intermediates, including 2-aminodiphenyl sulphide.

The dibenzo[b,f][1,4]thiazepin 11 (10 H)-one segment held a market share of 38.00% in 2025 and is expected to grow at the fastest CAGR of 6.2% over the forecast period. It acts as the basic core scaffold needed to synthesize quetiapine. It is the main and most vital precursor used by pharmaceutical companies to formulate quetiapine medication prescribed for schizophrenia and bipolar disorder. Also, it is synthesized via multi-step processes from baseline precursors like 1-chloro-2-nitrobenzene; this compound serves as a versatile agent for the growth of novel therapeutic agents. Due to its specialized role in directly streamlining the synthesis process, this segment consistently yields superior results compared to other intermediates, including 2-aminodiphenyl sulphide.

Quetiapine Intermediate Chemicals Market Share, By Product Type, 2025 (%)

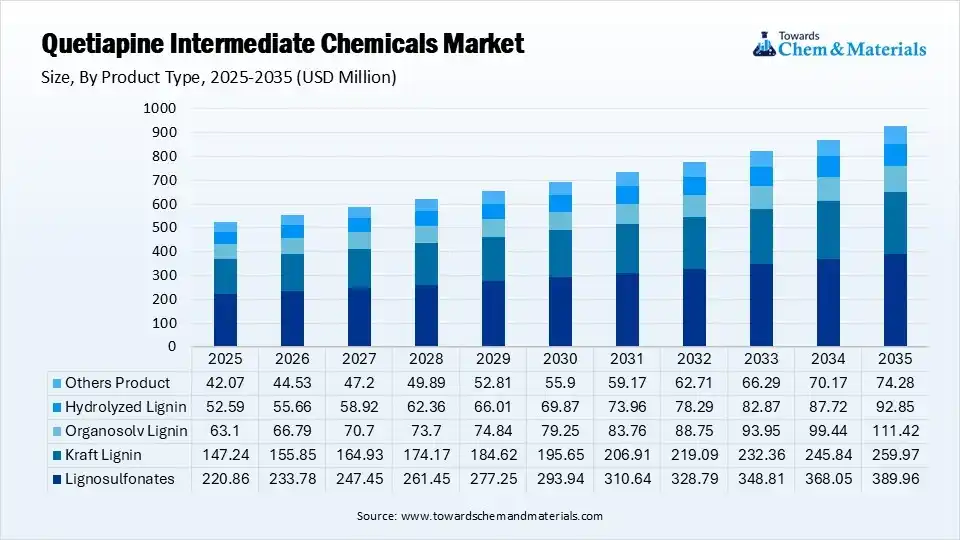

| By Product Type | Revenue Share, 2025 (%) |

| Lignosulfonates | 42% |

| Kraft Lignin | 28% |

| Organosolv Lignin | 12% |

| Hydrolyzed Lignin | 10% |

| Others Product | 8% |

End Use Insights

The pharmaceuticals segment dominated the market with the largest share of 91.0% in 2025 and is expected to grow at the fastest CAGR of 5.90% during the projected period. This segment is characterized by ongoing continuous synthesis of active pharmaceutical ingredients (APIs) for branded and generic psychiatric drugs. Furthermore, pharmaceutical companies and Contract Development and Manufacturing Organizations (CDMOs) use specific intermediates, including piperazine derivatives and tricyclic building blocks, as Key Starting Materials (KSMs) in the synthesis of quetiapine fumarate. The Asia-Pacific region serves as the primary hub for pharmaceutical manufacturing and intermediate synthesis, with China and India positioning themselves as the major global producers and exporters to international pharmaceutical developers.

")

The other end use segment held a market share of 9.00% in 2025. The segment includes end-use facilities such as contract research and manufacturing services (CRAMS) organizations and off-label therapeutic research. Furthermore, a significant number of chemical synthesis facilities, such as those manufacturing dibenzo[b,f][1,4]thiazepin-11(10H)-one intermediates, outsource their operations to specialized third-party industries. These contract manufacturing organizations (CMOs) deliver custom synthesis services essential for pipeline drug development, leading to segment growth soon.

Quetiapine Intermediate Chemicals Market Share, By End Use, 2025 (%)

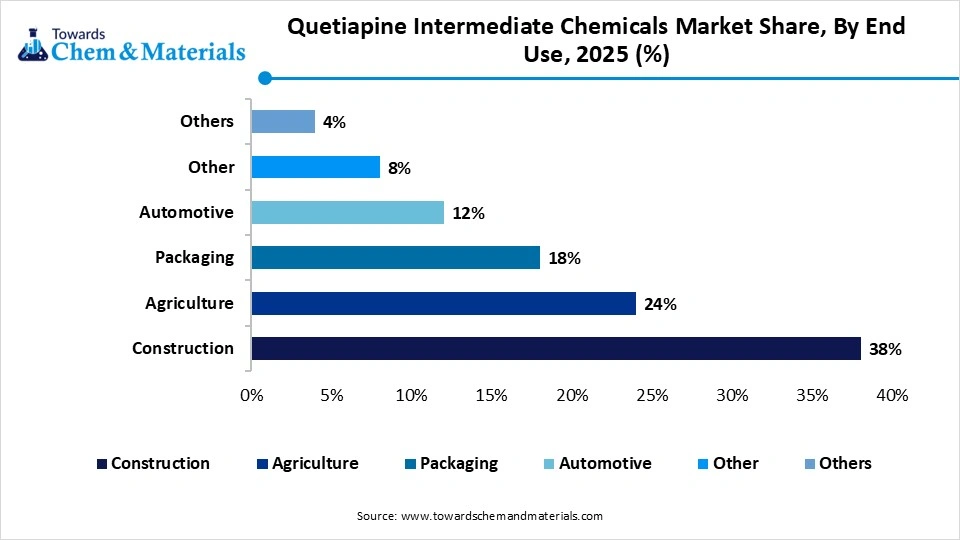

| By End Use | Revenue Share, 2025 (%) |

| Construction | 38% |

| Agriculture | 24% |

| Packaging | 18% |

| Automotive | 12% |

| Other | 8% |

Regional Analysis

How did Asia Pacific Dominate the Quetiapine Intermediate Chemicals Market in 2025?

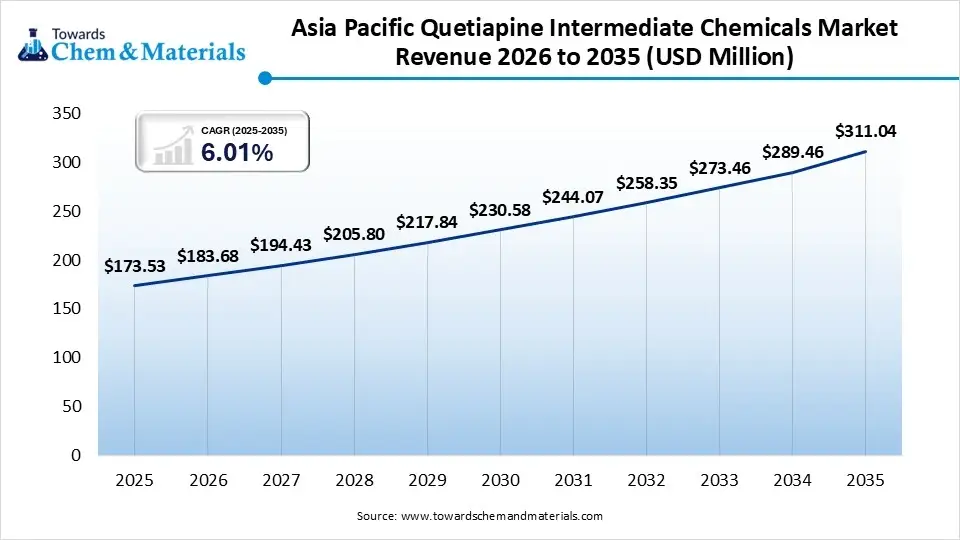

The Asia Pacific quetiapine intermediate chemicals market size was estimated at USD 173.53 million in 2025 and is projected to reach USD 311.04 million by 2035, growing at a CAGR of 6.01% from 2026 to 2035.Asia Pacific dominated the market with the largest share of 33.0% in 2025 and is expected to grow at the fastest CAGR of 7.10% over the forecast period. The growth of the region can be attributed to the growth of generic drug manufacturing and rising mental health awareness in emerging economies. In addition, his growth is propelled by improving healthcare infrastructure across developing economies, with nations like India and China at the forefront of this regional market expansion.

China

China

- Substantial government investment in public health awareness campaigns and healthcare facilities has expanded access to mental health medications across the country.

- China is also a global hub for chemical synthesis and API (active pharmaceutical ingredient) production.

India

- A surge in global diagnoses of schizophrenia, depression, and bipolar disorder needs scaled production of quetiapine formulations.

- Indian government schemes promoting "Make in India" and self-reliance aim to reduce dependence on raw material imports, facilitating domestic fine chemical production.

The Europe quetiapine intermediate chemicals market size was estimated at USD 141.98 million in 2025 and is projected to reach USD 255.33 million by 2035, growing at a CAGR of 6.04% from 2026 to 2035.Europe held a market share of 27.0% in 2025. The growth of the region can be credited to the increasing mental health diagnoses, robust regional R&D, and ongoing drug manufacturing. Furthermore, the consistent global prevalence of schizophrenia, bipolar disorder, and major depressive disorder sustains a continuous demand for quetiapine, which in turn drives the ongoing need for key starting materials (KSMs) and intermediate synthesis.

Germany

- Germany possesses highly established national mental health policies that focus on early diagnosis and continuous treatment, significantly boosting drug uptake.

- The country's robust domestic drug manufacturing hubs and commitment to integrating mental health care into primary services ensure steady production and consumption of key starting materials.

France

- An increasing incidence of neurological and psychiatric disorders, primarily schizophrenia and bipolar disorder, drives a steady, baseline demand for quetiapine.

- France's national healthcare strategies and proactive mental health policies encourage early diagnosis and continuous community-based treatment, leading to market growth soon in the country.

The North America quetiapine intermediate chemicals market size was estimated at USD 126.20 million in 2025 and is projected to reach USD 227.48 million by 2035, growing at a CAGR of 6.07% from 2026 to 2035.North America held a market share of 24.00% in 2025. The growth of the region can be linked to the fact that it is primarily driven by the increasing prevalence of mental health disorders, a mature pharmaceutical sector, and rising healthcare expenditures. Also, this growth is significantly propelled by the increasing demand for generic psychiatric medications and the region's strong strategic emphasis on cost-efficient, high-volume manufacturing.

") United States

United States

- A notable surge in diagnoses for psychiatric conditions, such as schizophrenia, bipolar

disorder, and major depressive disorder, is the major factor driving market growth in the country. - The extensive expiration of branded medication patents (Seroquel) has led to a massive spike in generic active pharmaceutical ingredient (API) manufacturing.

Canada

- Canadian pharmaceutical companies and API manufacturers are increasingly relying on outsourcing to achieve cost-effectiveness and process optimization, impacting positive market growth soon.

- Ongoing healthcare initiatives and a surge in societal acceptance have led to higher treatment rates and prolonged medication adherence across the board.

The Latin America quetiapine intermediate chemicals market size was estimated at USD 47.33 million in 2025 and is projected to reach USD 88.21 million by 2035, growing at a CAGR of 6.42% from 2026 to 2035.Latin America held a market share of 8.00% in 2025. The growth of the region can be linked to the escalating awareness of mental health, the expansion of regional pharmaceutical manufacturing, and the broadening of healthcare insurance coverage. Furthermore, the increasing adoption of generic antipsychotic medications and the growth of localized contract manufacturing boost industry development soon.

Brazil

- The integration of mental healthcare into Brazil's Unified Health System (SUS) has widened the accessibility and distribution of antipsychotic therapies, driving API demand soon.

- The expiration of patents on branded antipsychotics has opened the market for more cost-effective generic alternatives.

Argentina

- A growing diagnosis of conditions like schizophrenia, bipolar disorder, and major depressive disorder directly drives the need for active pharmaceutical ingredients (APIs) for antipsychotics.

- The trend of contract manufacturing organizations (CMOs) outsourcing chemical synthesis to decrease costs and increase therapeutic yield boosts supply chain momentum.

The Middle East & Africa quetiapine intermediate chemicals market size was estimated at USD 36.81 million in 2025 and is projected to reach USD 69.64 million by 2035, growing at a CAGR of 6.58% from 2026 to 2035.The Middle East & Africa held a market share of 8.00% in 2025. The growth of the region can be attributed to the heightened awareness of mental health, augmented investments in regional healthcare, and the expanded domestic manufacturing of generic psychiatric medications. Furthermore, substantial improvements in regional diagnostic rates and a shift in social attitudes toward mental health are pushing the regional healthcare network shortly.

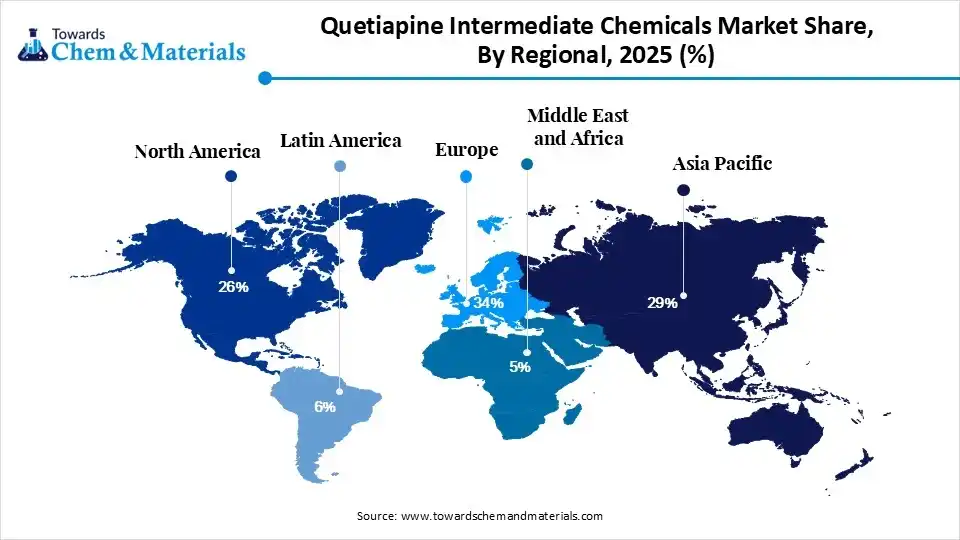

Quetiapine Intermediate Chemicals Market Share, By Regional, 2025 (%)

| Regional | Revenue Share, 2025 (%) |

| North America | 26% |

| Europe | 34% |

| Asia-Pacific | 29% |

| Latin America | 6% |

| Middle East & Africa | 5% |

Saudi Arabia

- Saudi Arabia’s localized pharmaceutical manufacturing is expanding, supported by government healthcare initiatives focusing on reducing reliance on imported medication.

- A notable surge in diagnoses for conditions like schizophrenia, bipolar disorder, and unipolar depression is driving up the regional consumption of antipsychotic drugs.

UAE

- The UAE government's heavy investment in advanced healthcare facilities and specialized psychiatric centers grows the accessibility and adoption of modern antipsychotic medications.

- The expiration of key quetiapine patents has boosted the production of affordable generic formulations, increasing the volume requirement for its base raw materials.

Competitive Analysis

The market mainly consists of chemical precursors like dibenzo[b, f][1,4]thiazepin-11(10H)-one, piperazine derivatives, and key starting materials (KSMs) used to synthesize the atypical antipsychotic Quetiapine. Pharmaceutical companies are increasingly developing new cost-effective generic delivery systems, facilitating better market penetration.

Aarti Pharmalabs is a key manufacturer of vital intermediates required for quetiapine APIs, specifically producing the foundational starting chemicals 1-(2-(2-hydroxyethoxy)). Ethyl Piperazine and Dibenzo-(1,4)-Thazepine-11-(10H)-One.

Top Vendors in the Quetiapine Intermediate Chemicals Market & Their Offerings:

- Merck KGaA: It serves as a premier, high-purity provider of analytical standards, impurities, and research materials for pharmaceutical quality control and method development. Merck supports the global pharmaceutical supply chain by providing highly regulated, traceable chemical reference standards.

- Aarti Pharmalabs: Aarti Pharmalabs Limited is a leading Indian manufacturer that develops and supplies Quetiapine Fumarate, APIs, and related pharmaceutical intermediates for central nervous system (CNS) agents. Backed by CDMO/CMO services, the company supports global drug manufacturing.

- Luye Pharma Group: Luye Pharma Group is a major international pharmaceutical company that dominates the Quetiapine value chain primarily through its ownership, marketing, and distribution of Seroquel and Seroquel XR (Quetiapine Fumarate), rather than operating as a basic manufacturer of intermediate chemicals.

- Ami Organics Ltd.: Ami Organics Ltd. is a research-driven manufacturer of advanced pharmaceutical intermediates and specialty chemicals. In the Quetiapine intermediate chemicals market, they act as a major global manufacturer of the key starting materials used to produce this vital antipsychotic API.

Other Key Players

- IOL Chemicals & Pharmaceuticals Ltd

- AR Lifesciences

- ALLCHEM LIFESCIENCE PVT. LTD.

- Aether Industries

- Shreeneel Chemicals

- AstraZeneca

Segments Covered in the Report

By Product

- 1-[2-(2-Hydroxyethoxy) ethyl] Piperazine

- Pharmaceutical Grade

- GMP-Compliant Grade

- High-Purity Grade

- Commercial Grade

- Dibenzo[b,f][1,4]thiazepin 11 (10 H)-one

- Pharmaceutical Grade

- API Synthesis Grade

- High-Purity Intermediate Grade

- Research Grade

- Other Products

- Specialty Quetiapine Intermediates

- Custom Synthesis Intermediates

- Process Development Intermediates

By End Use

- Pharmaceuticals

- Generic Drug Manufacturing

- Branded Drug Manufacturing

- Contract Manufacturing Organizations (CMOs)

- Other End Use

- Research & Development

- Academic Research

- Process Validation Activities

By Region

- North America

- U.S.

- Canada

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Sweden

- Denmark

- Norway

- Asia Pacific

- China

- Japan

- India

- South Korea

- Thailand

- Latin America

- Brazil

- Mexico

- Argentina

- Middle East & Africa

- South Africa

- UAE

- Saudi Arabia

- Kuwait

Select User License to Buy

Figures (6)