Content

What is Hazardous Chemicals Logistics Market Size and Share?

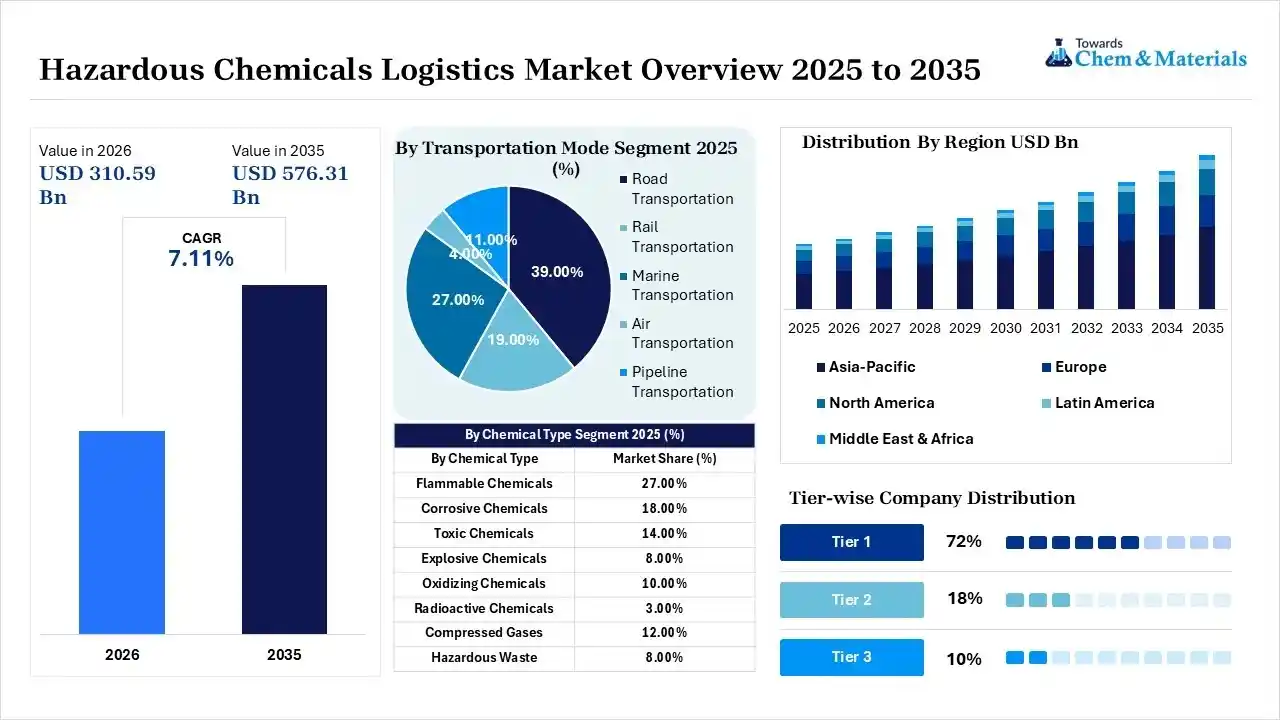

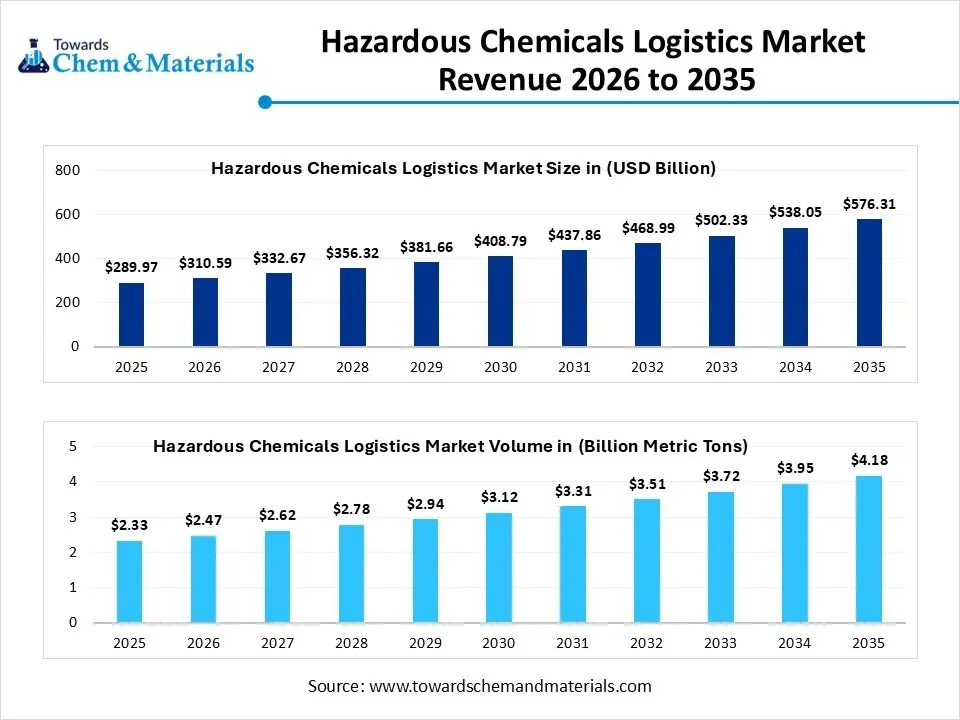

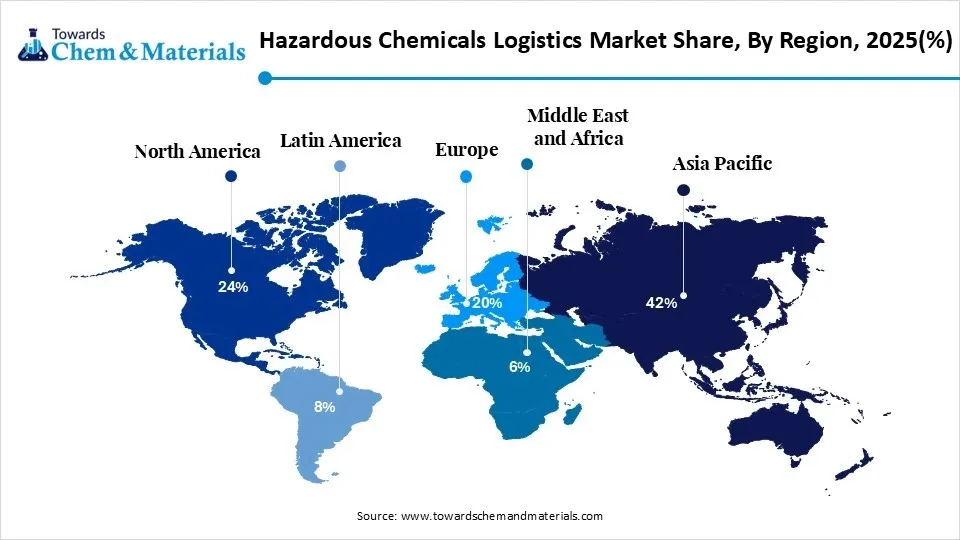

The global hazardous chemicals logistics market size was valued at USD 289.97 billion in 2025, is estimated to reach USD 310.59 billion in 2026, and is projected to reach USD 576.31 billion by 2035, exhibiting a compound annual growth rate (CAGR) of 7.11% over the forecast period from 2026 to 2035. Asia Pacific dominated the hazardous chemicals logistics market with the largest revenue share of 42.00% in 2025 and is expected to grow at the fastest CAGR of 7.24% during the forecast period.

The convergence of accelerating global production and stringent regulatory frameworks is the key factor leading to market growth. Also, Governments are straitly regulating how hazardous materials are moved, which impels companies to must follow complex rules to avoid large fines, optimising consumer growth.

Market Highlights

- By region, Asia Pacific dominated the market with largest share of 42.00% in 2025 and expected to grow at fastest CAGR of 7.48% over the forecast period.

- By region, North America held a market share of 24% in 2025 and was expected to grow at a CAGR of 5.94% over the forecast period.

- By transportation mode, the road transportation segment dominated the market with the largest share of 39.00% in 2025 and is expected to grow at a CAGR of 6.58% over the forecast period.

- By transportation mode, the marine transportation segment held a market share of 27.00% in 2025 and is expected to grow at the fastest CAGR of 7.12% over the forecast period.

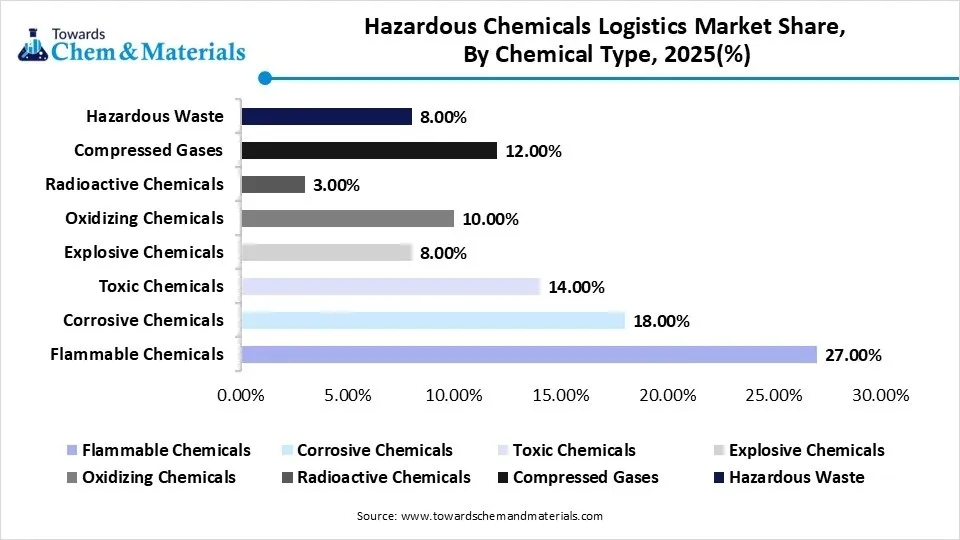

- By chemical type, the flammable chemicals segment dominated the market with the largest share of 27.00% in 2025 and is expected to grow at a CAGR of 6.83% over the forecast period.

- By chemical type, the compressed gases segment held the market share of 12.00% in 2025 and is expected to grow at the fastest CAGR of 7.18% over the forecast period.

- By service type, the transportation segment dominated the market with the largest share of 46.00% in 2025 and is expected to grow at a CAGR of 6.44% over the forecast period.

- By service type, packaging & labelling held a market share of 11.00% in 2025 and is expected to grow at the fastest CAGR of 7.22% over the forecast period.

- By hazard class, the Class 3 (flammable liquids) segment dominated the market with largest share of 31.00% in 2025 and expected to grow at CAGR of 6.76% over the forecast period.

- By hazard class, the class 2 (gases) segment held the market share of 16.00% in 2025 and expected to grow at fastest CAGR of 7.20% over the projected period.

Increasing Focus on Environmental Sustainability

According to Towards Chemicals and Materials Analytics and Consulting, the global hazardous chemicals logistics market volume was valued at 2.33 billion metric tons in 2025 and is expected to surpass around 4.18 billion metric tons by 2035, accelerating a compound annual growth rate (CAGR) of 6.03% over the forecast period from 2026 to 2035.

There is a crucial trend towards environmental sustainability market, presenting lucrative opportunities. Major companies are actively opted to reduce their ecological impact by adopting greener practices. This involves the use of sustainable packaging materials and the exploration of other transportation methods.

- In May 2026, In Rabat, stakeholders launched a national project aimed at removing hazardous chemicals from the construction supply chain in Morocco. This initiative by the United Nations Industrial Development Organization (UNIDO) and the Moroccan Agency for Energy Efficiency (AMEE) advances the country's transition toward sustainable, energy-efficient building models with financial support from the Global Environment Facility (GEF).(Source: en.yabiladi.com)

- Major stakeholders are emphasizing minimizing the carbon footprint associated with the transportation of hazardous goods; this transition may optimize the adoption of greener technologies and other fuels, which can reshape logistics strategies in the near future.

Global Investment Flow for Hazardous Chemicals Logistics 2025

Global investment in the market is transitioning towards safety, technology, and the advent of new markets. The major emphasis on investments is on smart warehouses, real-time tracking, and compliance, fuelled by a surge in global trade. Firms are building PESO-compliant and temperature-controlled warehouse fleets.

- In 2025, the United States exported $29.8M of benzene, making it the 2,557th most exported product in the United States. The main destinations of the United States' benzene exports were Canada ($28.2M), Mexico ($1.46M), Germany ($93.1k), Australia ($14.8k), and Switzerland ($13.1k).(Source: oec.world)

- For instance, in 2026, industry data of China indicates that recent domestic benzene capacity has expanded by approximately 2.26 million metric tons, primarily driven by ethylene cracking units operated by major enterprises such as Tangshan Dimu and North China Huajin.(Source: www.sunsirs.com)

Chemical manufacturers rapidly favor "one-stop" third-party logistics contracts to offload regulatory risks. This leads to strategic investment toward consolidated, large-scale providers capable of solely funding hazmat-graded fleets and safety certifications.

Market Trends

- The surge in global chemical production is the latest trend in the market shaping positive market growth. As demand for specialty, industrial, and pharmaceutical chemicals is heavily rising, market players are manufacturing larger volumes across a range of regions and sectors.

- In recent years, there has been an increase in emphasis on compliance, safety, and hazardous material handling. Market players are heavily partnering with logistics providers capable of offering safe, certified, and compliant handling solutions. This need for high-quality safety practices such as ADR-certified fleets is rising continuously.

- Innovations in cold chain technologies and digital tracking are the future trends in the market driving market growth. Digital tracking systems such as RFID tags and GPS-enabled sensors offer real-time visibility of chemical shipments over the supply chain operations.

Report Scope

| Report Attributes | Details |

| Market Size in 2026 | USD 310.59 Billion/ 2.47 Billion Metric Tons |

| Expected Size in 2035 | USD 576.31 Billion/ 4.18 Billion Metric Tons |

| Growth Rate | CAGR of 7.11% |

| Base Year of Estimation | 2025 |

| Forecast Period | 2025-2035 |

| Dominant Region | Asia Pacific |

| Segment Covered | By Transportation Mode, By Chemical Type, By Service Type, By Hazard Class, By Region |

| Key Companies Profiled | FedEx Custom Critical (United States), UPS Supply Chain Solutions (United States), HOYER Group (Germany), Bertschi AG (Switzerland), Royal Den Hartogh Logistics (Netherlands), Stolt-Nielsen Limited (United Kingdom / Norway), MOL Chemical Tankers (Singapore / Japan), Suttons Group (United Kingdom), Quantix (United States) |

AI-Powered Predictive Formulations in the Hazardous Chemicals Logistics Market

AI-powered predictive formulations utilize machine learning to produce safer, smarter chemical mixtures. In hazardous logistics, these tools forecast how different chemicals would react to temperature, movement, and time. Furthermore, sensors on trucks and tanks are used to predict when a part will break before it happens. This further stops dangerous leaks.

Supply Chain Analysis of the Hazardous Chemicals Logistics Market

Production & Processing

- It includes managing and altering chemical cargo while it moves through the supply chain.

Instead of just providers blending, moving chemicals, repackaging, heating, filtering, or labelling dangerous goods and route, they are converting basic materials into ready-to-use products while following safety rules. - DHL Supply Chain: A massive global provider that handles temperature-controlled storage, blending, and repackaging for hazardous pharmaceutical and industrial chemicals.

- Other Key Players: A&R Logistics, BDP International

Quality Testing and Certification

- It involves the strongest audits, safety checks, and validations needed to move and store dangerous goods. It also ensures all packing equipment and training meet global safety laws to stop leaks, fires, or explosions.

Also, it ensures containers (like drums, tanks, and ISO containers) pass United Nations (UN) standards for dangerous goods. - SGS Group: A global leader that provides dangerous goods testing, cargo inspections, and logistics compliance services.

- Other Key Players: Intertek, DEKRA

Distribution to Industrial Users

- It involves the secure transportation of bulk or specialized hazardous chemicals from manufacturing facilities to industrial plants, agricultural sectors, and processing units. Transport vehicles must be custom retrofitted with advanced safety mechanisms designed for hazardous material containment.

- DHL Supply Chain: A global leader that manages massive B2B supply chains. They focus on safe handling, digital tracking, and reducing carbon footprints.

- Other Key Players: Bertschi Group, Den Hartogh

Hazardous Chemicals Logistics Market’s Regulatory Landscape: Global Regulations

| Country / Region | Regulatory Body | Key Regulations & Standards | Focus Areas |

| Global | United Nations (UN) | UN RTDG (Model Regulations) | Harmonized classification, labeling, and packaging standards globally. |

| Europe (EU) | ECHA / National Authorities | REACH, CLP, ADR | Chemical safety registration, hazard communication, and road transport safety. |

| United States | EPA, OSHA, DOT | TSCA, HazCom, 49 CFR | Chemical tracking, workplace worker safety, and multi-modal transport security. |

What are the types of Hazardous Chemicals?

Physical Hazards

These chemicals present immediate dangers due to their explosive, reactive, and unstable properties.

- Flammables: Liquids, gases, or solids that ignite easily and burn rapidly when exposed to a spark or heat source (e.g., gasoline, acetone, propane).

- Explosives: Substances that can trigger a sudden, violent chemical reaction releasing energy, heat, and gas (e.g., ammunition, fireworks).

- Oxidizers: Chemicals that release oxygen, which can cause or severely intensify a fire even without an external air supply (e.g., hydrogen peroxide, nitrates).

- Gases Under Pressure: Compressed, liquefied, or dissolved gases stored in cylinders that can be exposed violently or cause cryogenic freeze burns (e.g., liquid nitrogen).

- Pyrophorics & Self-Heating Substances: Highly unstable compounds that catch fire spontaneously upon making contact with air or after prolonged storage.

Health Hazards

These substances cause long-term or short-term illness or damage to the human body via inhalation, contact, or ingestion.

- Acute Toxins: Highly dangerous poisons that cause severe illness, target organ failure, or death from a single small exposure (e.g., cyanide, arsenic).

- Irritants & Sensitizers: Compounds causing temporary redness, inflammation, or severe allergic respiratory reactions like occupation-induced asthma (e.g., bleach, industrial disinfectants).

- Skin & Eye Corrosives: Chemicals that cause immediate, permanent, or irreversible chemical burns to flesh and ocular tissue (e.g., sulfuric acid and caustic soda).

- Asphyxiants: Vapors or gases that actively displace oxygen in the air or bloodstream, which results in suffocation (e.g., carbon monoxide).

Environmental Hazards

- Ozone Layer Depleters: Volatile chemicals capable of escaping into the upper atmosphere and breaking down the earth's protective ozone shield (e.g., legacy chlorofluorocarbons).

- Aquatic Toxins: Materials that poison marine life, fish, and underwater ecosystems either through immediate contact or long-term systemic runoff (e.g., heavy metal waste, pesticides).

Hazardous Chemicals Logistics Market Dynamics

Driver

Growing Adoption of Digital Supply Chain Technologies

The surge in adoption of digital supply chain technologies is the major factor driving the growth of the market. Digital transformation boosts across the chemical sector as companies are adopting IoT sensors, AI-based route optimization, and automation. In addition, advanced analytics enable logistics providers to predict demand fluctuations, facilitate container usage, and enhance overall fleet scheduling. Digital platforms minimize administrative burdens and give faster order fulfilment.

Restraints

Complex Global Regulations

Shipping hazardous goods across international borders needs adherence to vastly different laws, such as REACH in Europe, DOT regulations in the US, and national mandates such as PESO in India, which is the major factor hindering market growth. Moreover, logistics companies must heavily invest in safety certifications, constant regulatory audits, and specific legal labelling protocols. Also, the high market value of chemical raw materials makes them prone to theft, where expensive agents are stolen and replaced with low-quality substitutes.

Opportunity

Advancements in Logistics Technology

Hazardous chemical logistics is witnessing an evolution because of innovations like digitization, real-time tracking, automation, and IoT, creating notable opportunities in the market soon. The above solutions help to optimize real-time cargo tracking, save costs, improve operational efficiency, and improve overall safety levels for transporting hazardous materials. Furthermore, AI and predictive analytics also draw improvement of inventory control and routing.

Segmental Insights

Transportation Mode Insight

The road transportation segment dominated the market with the largest share of 39.00% in 2025 and is expected to grow at a CAGR of 6.58% over the forecast period. The dominance of the segment can be attributed to the growing pharmaceutical and industrial demand for various chemicals along with the stringent safety regulations. In addition, it also offers door-to-door delivery, flexible routing, and last-mile connectivity to remote agricultural and industrial sites that lack rail or port access.

")

The marine transportation segment held a market share of 27.00% in 2025 and is expected to grow at the fastest CAGR of 7.12% over the forecast period. The growth of the segment can be credited to the surge in global trade of industrial chemicals and crude oil along with stringent safety rules. Major companies hire expert shipping providers rather than doing it themselves, which helps them avoid heavy fines for rule violations.

Hazardous Chemicals Logistics Market Share, By Transportation Mode, 2025(%)

| By Transportation Mode | Market Share (%) |

| Road Transportation | 39.00% |

| Rail Transportation | 19.00% |

| Marine Transportation | 27.00% |

| Air Transportation | 4.00% |

| Pipeline Transportation | 11.00% |

Chemical Type Insight

The flammable chemicals segment dominated the market with the largest share of 27.00% in 2025 and is expected to grow at a CAGR of 6.83% over the forecast period. The dominance of the segment can be linked to the expanding specialty chemical industry and increasing demand for temperature-controlled complex transport. Government needs compliant, specialized storage and transport for flammable goods. This pushed companies to outsource to logistics experts.")

- In July 2026, Offgrid Energy Labs launched its premier ZincGel® pilot manufacturing facility in Hook, Hampshire. This site includes a 10-MWh demonstration line, which makes the transition of India-developed energy storage technology to international markets. This global expansion aligns with India's energy goals. India aims for 500 GW of non-fossil fuel capacity by 2030, which drives a major need for storage infrastructure. (Source: www.manufacturingtodayindia.com)

The compressed gases segment held the market share of 12.00% in 2025 and is expected to grow at the fastest CAGR of 7.18% over the forecast period. The growth of the segment can be driven by an increase of high-grade industrial gases in electronics and cryogenic transport coupled with the healthcare and electronics needs. Also, the ongoing growth of clinical healthcare, biohazardous materials, and medical devices depends largely on consistent medical gas supply chains.

Hazardous Chemicals Logistics Market Share, By Chemical Type, 2025(%)

| By Chemical Type | Market Share (%) |

| Flammable Chemicals | 27.00% |

| Corrosive Chemicals | 18.00% |

| Toxic Chemicals | 14.00% |

| Explosive Chemicals | 8.00% |

| Oxidizing Chemicals | 10.00% |

| Radioactive Chemicals | 3.00% |

| Compressed Gases | 12.00% |

| Hazardous Waste | 8.00% |

Service Type Insight

The transportation segment dominated the market with the largest share of 46.00% in 2025 and is expected to grow at a CAGR of 6.44% over the forecast period. The dominance of the segment is owing to the increasing industrial chemical output, multi-modal infrastructure upgrades, and stringent safety mandates. The surge in manufacturing of specialty chemicals, petrochemicals, and agrochemicals directly increases the volume of hazardous materials requiring reliable and safe transit.

The packaging & labelling held a market share of 11.00% in 2025 and is expected to grow at the fastest CAGR of 7.22% over the forecast period. The growth of the segment is due to the growing use of smart technology, a surge in global trade, and stringent safety rules. The growth of cutting-edge agrochemicals, polymers, and clinical biologics fuels a demand for specialized containers that prevent environmental degradation.

Hazardous Chemicals Logistics Market Share, By Service Type, 2025(%)

| By Service Type | Market Share (%) |

| Transportation | 46.00% |

| Warehousing & Storage | 18.00% |

| Packaging & Labeling | 11.00% |

| Freight Forwarding | 9.00% |

| Customs Clearance | 5.00% |

| Inventory Management | 6.00% |

| Value-added Logistics Services | 5.00% |

Hazard Class Insight

The Class 3 (flammable liquids) segment dominated the market with the largest share of 31.00% in 2025 and is expected to grow at a CAGR of 6.76% over the forecast period. The dominance of the segment can be attributed to the increasing global petrochemical production and rising demand for high-tech, specialized transport. Furthermore, more products such as fuels, paints, alcohols, and cosmetics are manufactured and shipped on a daily basis, leading to segment growth soon.

The class 2 (gases) segment held the market share of 16.00% in 2025 and is expected to grow at the fastest CAGR of 7.20% over the projected period. The growth of the segment can be credited to the surge in petrochemical manufacturing, stringent international safety laws, and the growing demand for global energy. Companies pay a premium for automated warehousing and certified drivers shifting cargo from roads to safer rail or pipeline networks.

Hazardous Chemicals Logistics Market Share, By Hazard Class, 2025 (%)

| By Hazard Class | Market Share (%) |

| Class 2 (Gases) | 16.00% |

| Class 3 (Flammable Liquids) | 31.00% |

| Class 4 (Flammable Solids) | 9.00% |

| Class 5 (Oxidizing Substances & Organic Peroxides) | 11.00% |

| Class 6 (Toxic & Infectious Substances) | 12.00% |

| Class 8 (Corrosive Substances) | 15.00% |

| Class 9 (Miscellaneous Dangerous Goods) | 6.00% |

What are the benefits of Hazardous Chemicals?

Hazardous chemicals are fundamental components of modern society, fueling innovations in agriculture, technology, medicine, and manufacturing. While these substances pose some risks to health and safety, their specific, toxic, reactive, and flammable properties make them uniquely qualified to perform critical functions that safer alternatives cannot achieve.

Advanced pharmaceutical manufacturing requires the use of hazardous chemical agents and solvents to produce vital medications like antibiotics, heart drugs, and chemotherapies. Lithium, cobalt, and other acids and bases are crucial components in manufacturing high-capacity batteries for electric vehicles and renewable energy grids. In addition, flammable liquids and combustible gases, such as petroleum derivatives and natural gas, act as essential energy sources for global transportation and power generation.

Regional Analysis

How did the Asia Pacific dominate the Hazardous Chemicals Logistics Market in 2025?

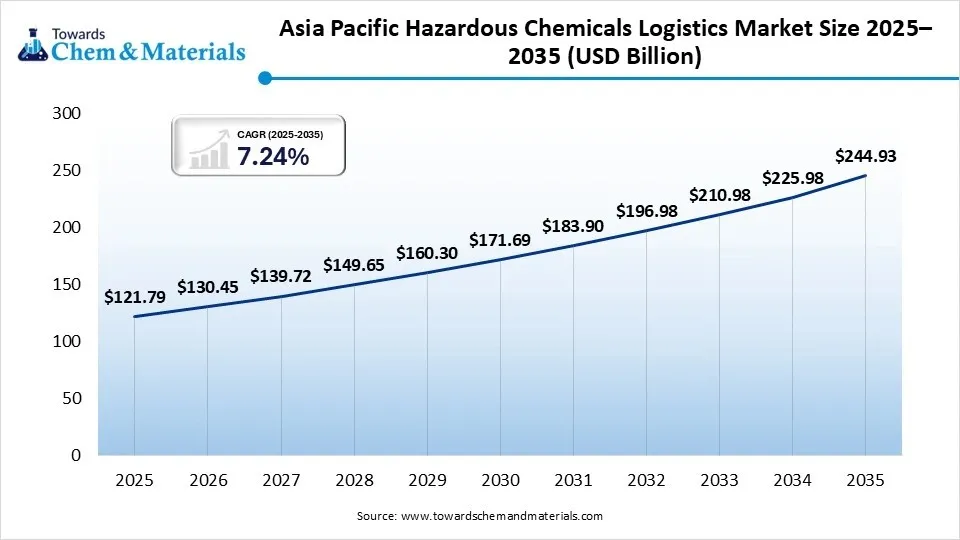

The Asia Pacific hazardous chemicals logistics market size was estimated at USD 121.79 billion in 2025 and is projected to reach USD 244.93 billion by 2035, growing at a CAGR of 7.24% from 2026 to 2035. Asia Pacific dominated the hazardous chemicals logistics market with the largest share of 42.00% in 2025 and is expected to grow at the fastest CAGR of 7.48% over the forecast period. The dominance of the region can be attributed to the extensive production output, stringent safety laws, and superior transport networks in emerging economies such as China, India, and Japan. In addition, governments are spending plenty of money to build better railways, ports, and special warehouses, leading to market growth soon.

")

The China heavily regulates hazardous cargo. Chemicals cannot move without licensed carriers, route controls, and strict cargo tracking. The country is the world's top chemical manufacturer. Extensive demand for agrochemicals, petrochemicals, and battery materials needs large-scale and constant movement. Logistics companies now provide extra safety services such as temperature control, mixing, and 24-hour monitoring to meet new compliance rules.

The Indian market in the country highly depends on expanding domestic manufacturing, strict safety rules, and superior transport networks. Modern logistics facilities employ automated fire suppression and real-time tracking to safely oversee dangerous substances. Which needs significant financial investment, these facility enhancements are crucial to meet global regulatory safety standards.

North America Hazardous Chemicals Logistics Market Analysis

The North America hazardous chemicals logistics market size was estimated at USD 69.59 billion in 2025 and is projected to reach USD 141.20 billion by 2035, growing at a CAGR of 7.33% from 2026 to 2035. North America held a market share of 24% in 2025 and was expected to grow at a CAGR of 5.94% over the forecast period. The growth of the region can be credited to the rapid technological modernization initiatives, strong mix of industrial scaling, and ongoing investments in chemical manufacturing hubs. To lower incident rates, high-tech operators are increasingly adopting advanced technologies, including AI-driven predictive analytics, algorithmic routing, and IoT sensor platforms. These strategic implementations enable logistics firms to mitigate the financial pressures of increasing cross-border compliance costs and rising insurance premiums.

")

The United States surge in manufacturing in extensive chemical clusters and stringent regulatory frameworks are the major factors driving country growth. Businesses are rapidly deploying the Internet of Things (IoT), blockchain technology, real-time tracking systems, and automated warehouse robotics to reduce human error. These integrated solutions also ensure strict compliance with precise temperature control standards.

Canada is enforcing stringent rules to safeguard the environment and workers; hence, companies are hiring expert logistics teams to stay compliant. Strict regulatory enforcement of the Transportation of Dangerous Goods (TDG) Act and municipal fire codes compels manufacturers to transition from internal logistics models to specialized third-party logistics (3PL) providers.

Europe Hazardous Chemicals Logistics Market Analysis

The Europe hazardous chemicals logistics market size was estimated at USD 57.99 billion in 2025 and is projected to reach USD 118.14 billion by 2035, growing at a CAGR of 7.38% from 2026 to 2035. Europe held a market share of 20.00% in 2025 and was expected to grow at a CAGR of 5.76% over the forecast period. The growth of the region can be linked to the innovative tracking technologies, stringent safety mandates, and structural shifts in regional manufacturing. Moreover, the Carbon Border Adjustment Mechanism incentivizes domestic production and enforces rigorous regulatory standards for materials entering European markets, leading to further regional growth.

The Germany market in the country is driven by growing pharmaceutical demands and a growing need to move fragile vaccines and toxic battery salts. The European Union's REACH [Registration, Evaluation, Authorization, and Restriction of Chemicals] regulations obligate enterprises to implement rigorous material tracking and logistics protocols. This needs the deployment of highly qualified personnel and secure, specialized containment facilities to ensure full legal compliance.

France is implementing a strategic initiative to reduce its reliance on road freight. By redirecting chemical loads to railways and inland waterways, the nation seeks to minimize road congestion, reduce the risk of accidents, and achieve its long-term ecological goals. Major industrial hubs near ports such as Marseille and Dunkirk fuel high demand soon. The market emphasizes multi-modal and safe monitoring.

Latin America Hazardous Chemicals Logistics Market Analysis

The Latin America hazardous chemicals logistics market size was estimated at USD 23.20 billion in 2025 and is projected to reach USD 48.99 billion by 2035, growing at a CAGR of 7.76% from 2026 to 2035. Latin America dominated the market with the largest share of 7.00% in 2025 and is expected to grow at a CAGR of 6.41% over the forecast period. The growth of the region can be driven by major manufacturing complexes in leading economies that are actively producing volatile compounds such as toluene, xylene, and methanol. Also, operators are transitioning towards integrated rail, maritime, and road hazardous material networks to reduce overall downstream logistical operational costs while keeping safety integrity.

Brazil depends on a massive farming sector. This drives high demand for moving hazardous agricultural chemicals like urea and ammonia to rural hubs. The consistent, large-scale production of benzene, toluene, xylene, and methanol drives the bulk transport of these materials to downstream automotive, plastics, and construction facilities.

Argentina’s large-scale farming economy needs a continuous, bulk supply of agrochemicals and fertilizers. These products must be transported reliably across vast distances to remote grain-producing provinces. Additionally, local governments need businesses to use certified equipment to prevent spills. This compliance increases the demand for professional logistics providers.

Middle East & Africa Hazardous Chemicals Logistics Market Analysis

The Middle East & Africa hazardous chemicals logistics market size was estimated at USD 17.40 billion in 2025 and is projected to reach USD 37.46 billion by 2035, growing at a CAGR of 7.97% from 2026 to 2035. The Middle East & Africa held the market share of 7.00% in 2025 and is expected to grow at a CAGR of 6.68% during the projected period. The growth of the region can be attributed to the growing regional infrastructure investments and surge in petrochemical outputs. Furthermore, governments in the region are implementing strict regulations for hazardous materials. This impels market players to hire expert logistics providers rather than using basic transport.

Saudi Arabia is the largest chemical producer in the MENA region. State-backed investments are building massive downstream plants to turn raw oil into valuable plastics and chemicals. This needs millions of tons of hazardous materials to move daily. The government is transitioning its economy away from the export of raw crude oil to focus on the domestic production of high-value commodities, such as fertilizers, advanced construction materials, and pharmaceuticals.

Under state plans like the UAE Centennial 2031, the region's output of specialty chemicals, plastics, and fertilizers is growing. This expansion needs new and improved chemical storage and handling. Refineries are increasingly emphasizing higher-margin value-added chemicals, transitioning logistic demand from basic bulk to specialized handling. Non-hydrocarbon sectors such as pharmaceuticals and agricultural chemicals are scaling fast under the UAE's economic roadmap.

Competitive Analysis

The market is a highly consolidated, high-moat sector having considerable value. It features intense competition driven by stringent safety compliance, advanced digital tracking, and multi-modal asset ownership. The competitive landscape comprises two primary segments: large multinational third-party logistics (3PL) corporations with extensive global forwarding capabilities and asset-heavy specialists managing dedicated fleets of ISO tank containers and temperature-controlled equipment.

The HOYER Group is expanding its hazardous chemicals logistics by advancing digital tracking, global fleet capabilities, and emergency preparedness. HOYER focuses on reducing risks during chemical transport through strict regulatory compliance and IoT-enabled monitoring.

- Bertschi AG is successfully navigating complex and highly volatile chemical logistics by reinforcing its core competencies in resilient door-to-door transport, intermodal shipping networks, and sustainable supply chain solutions.(Source: www.hoyer-group.com)

Recent Developments

- In March 2026, the International Air Transport Association (IATA) introduced DG Digital, an integrated feature of DG AutoCheck. This digital solution streamlines the creation and validation of shippers' declarations for over 3,800 regulated commodities, including lithium batteries and chemicals. This transition from paper to digital documents enhances operational safety and significantly reduces shipment rejections.(Source: www.iata.org)

- In April 2026, the Abu Dhabi Hazardous Materials Management Centre partnered with the Abu Dhabi Quality and Conformity Council to launch 11 new safety guidelines. These rules align with global best practices. They streamline hazardous goods operations across the emirate. This strengthens environmental protection, unifies regulatory standards, and optimizes compliance.(Source: www.mediaoffice.abudhabi)

Strategic Profiles of Key Players Shaping the Hazardous Chemicals Logistics Market

| Company | Company Type / Position | Headquarters | Geographic Presence | Offerings | Key Offering / Strength |

| DHL Supply Chain | Global logistics leader. | Bonn, Germany. | Over 220 countries and territories | Air, ocean, and road freight; warehousing; end-to-end supply chain management. | Strict adherence to global safety standards (like ISO and SQAS) and a vast, specialized infrastructure for temperature-controlled chemical transport. |

| BDP International (PSA BDP) | Specialized chemical logistics provider. | Philadelphia, Pennsylvania, USA. | Strong presence in North America, Europe, and Asia-Pacific. | Ocean and air freight forwarding, customs brokerage, regulatory compliance management. | Advanced risk-management software and deep expertise in complex global chemical regulatory frameworks. |

| Brenntag SE | Global market leader in chemical and ingredients distribution. | Essen, Germany. | Global footprint operating across roughly 70 countries. | Bulk and less-than-truckload chemical distribution, custom blending, storage, and value-added logistics. | Seamless blending of value-added chemical processing services with secure, highly regulated global distribution networks. |

Other Key Players

- FedEx Custom Critical (United States)

- UPS Supply Chain Solutions (United States)

- HOYER Group (Germany)

- Bertschi AG (Switzerland)

- Royal Den Hartogh Logistics (Netherlands)

- Stolt-Nielsen Limited (United Kingdom / Norway)

- MOL Chemical Tankers (Singapore / Japan)

- Suttons Group (United Kingdom)

- Quantix (United States)

Segments Covered in the Report

By Transportation Mode

- Road Transportation

- Tank Trucks

- Dry Van Trucks

- Container Trucks

- Specialized Hazardous Material Vehicles

- Rail Transportation

- Tank Railcars

- Covered Railcars

- Intermodal Rail Transport

- Marine Transportation

- Chemical Tankers

- ISO Tank Containers

- Bulk Chemical Carriers

- Barge Transport

- Air Transportation

- Dedicated Cargo Aircraft

- Commercial Air Cargo

- Pipeline Transportation

- Liquid Chemical Pipelines

- Gas Pipelines

By Chemical Type

- Flammable Chemicals

- Corrosive Chemicals

- Toxic Chemicals

- Explosive Chemicals

- Oxidizing Chemicals

- Radioactive Chemicals

- Compressed Gases

- Hazardous Waste

By Service Type

- Transportation

- Domestic Transportation

- International Transportation

- Warehousing & Storage

- Temperature-Controlled Warehousing

- Hazardous Material Warehousing

- Packaging & Labeling

- Freight Forwarding

- Customs Clearance

- Inventory Management

- Value-added Logistics Services

By Hazard Class

- Class 2 (Gases)

- Class 3 (Flammable Liquids)

- Class 4 (Flammable Solids)

- Class 5 (Oxidizing Substances & Organic Peroxides)

- Class 6 (Toxic & Infectious Substances)

- Class 8 (Corrosive Substances)

- Class 9 (Miscellaneous Dangerous Goods)

By Regions

- North America

- Europe

- Asia Pacific

- Middle East & Africa

- Latin America

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

FAQ's

Select User License to Buy

Figures (6)