Content

What is the Current Fracking Chemicals And Fluids Market Size and Share?

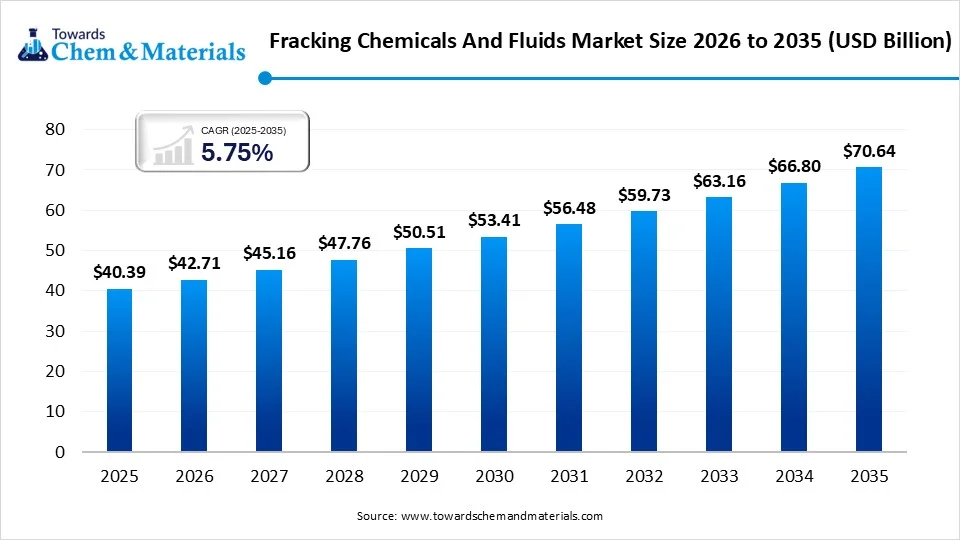

The global fracking chemicals and fluids market size was estimated at USD 40.39 billion in 2025 and is expected to increase from USD 42.71 billion in 2026 to USD 70.64 billion by 2035, growing at a CAGR of 5.75% from 2026 to 2035. North America dominated the fracking chemicals and fluids market with the largest revenue share of 59.00% in 2025.The growth of the market is driven by the rising energy demand and increased unconventional oil and gas extraction, which fuels the growth. The fracking chemicals and fluids market is highly significant as a key enabler for unlocking unconventional oil and gas resources. These fluids increase extraction efficiency by maintaining well pressure, enhancing viscosity, and reducing friction. Driven by rising global energy demand and advancements in horizontal drilling, this market directly boosts productivity in shale formations while shifting towards more environmentally sustainable, or green chemical formulations.

Market Highlights

- By region, North America dominated the fracking chemicals and fluids market with the largest revenue share of 59.00% in 2025. The growth is driven by advanced technological adoption.

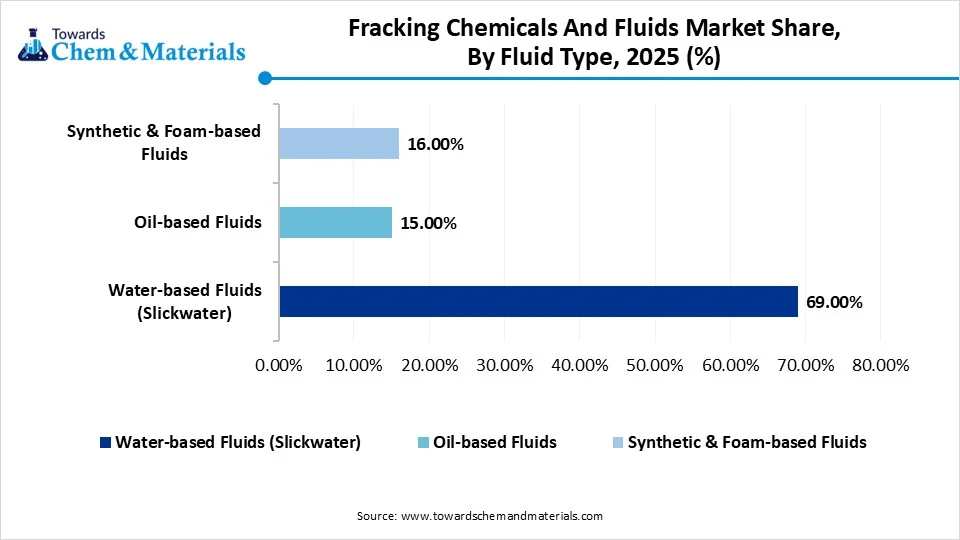

- By fluid type, the water-based fluids segment dominated the market with a share of approximately 69% in 2025, The growth is driven by cost-effective & widely used.

- By fluid type, the oil-based fluids segment is projected to grow at the fastest CAGR between 2026 and 2035. The growth is driven by the growing use in complex formations.

- By additive function, the friction reducers segment dominated the market with a share of approximately 32% in 2025. The growth is driven by the essential need for high-rate slickwater.

- By additive function, the surfactants segment is projected to grow at the fastest CAGR between 2026 and 2035. The growth is driven by demand for enhanced oil recovery.

- By well type, the horizontal wells segment dominated the market with a share of approximately 85% in 2025. The growth is driven by the industry standard for shale.

- By well type, the vertical wells segment is projected to grow at the fastest CAGR between 2026 and 2035. The growth is driven by niche growth in lower-cost projects.

- By application, the shale gas segment dominated the market with a share of approximately 48% in 2025. The growth is driven by mature infrastructure/high volume.

- By application, the tight oil segment is projected to grow at the fastest CAGR between 2026 and 2035. The growth is driven by a surge in liquid-rich shale plays.

Key Technological Shifts in the Fracking Chemicals and Fluids Market:

Key technological shifts in the fracking chemicals and fluids market are driven by sustainability, digitalization, and efficiency, specifically targeting reduced water usage and improved environmental compliance. Other major factors include the rise of "green" biodegradable chemicals, advanced nanomaterials for enhanced, stable fracturing fluids, and waterless technologies like CO-based fluids. Digitalization, AI, and IoT are transforming monitoring and optimizing chemical applications.

Trade Analysis of Fracking Chemicals and Fluids Market: Import & Export Statistics

- Based on Global Export Data, the worldwide export of Drilling Chemicals amounted to 91 shipments, handled by 28 verified exporters and 43 buyers,

Similarly, the global export of Drilling Fluids reached 47 shipments through 4 verified exporters and 5 buyers. - Additionally, between July 2024 and June 2025 (TTM), the world exported 208 Drilling Fluids shipments via 60 verified exporters and 44 buyers.

- Saudi Arabia, Ecuador, and the United States are the leading importers of Drilling Fluids, while the United States (894 shipments), Italy (250 shipments), and China (54 shipments) are the top exporters worldwide.

Top-performing Global Drilling Fluids Exporters by volume:

- OILFIELD INTERNATIONAL EQUIPMENT SUPPLIES PTE: 209 shipments (27%)

- OEC LIQUID LOGISTICS SOLUTIONS: 170 shipments (22%)

- OMEGA GLOBAL LOGISTICS: 146 shipments (19%)

Market Trends:

- Shift to Eco-Friendly Chemicals: Growing environmental regulations are pushing the industry toward green, biodegradable, and less toxic chemical additives.

- Water-Based Fluids Dominance: Water-based systems are experiencing high demand due to their efficiency and lower environmental impact compared to oil-based alternatives.

- Technological Advancements: The industry is focusing on advanced fluid engineering, including high-performance friction reducers, biocides, and cross-linkers to optimize production in deep, high-temperature wells.

Report Scope

| Report Attribute | Details |

| Market Size in 2026 | USD 42.71 Billion |

| Revenue Forecast in 2035 | USD 70.64 Billion |

| Growth Rate | CAGR 5.75% |

| Forecast Period | 2026 - 2035 |

| Base Year | 2025 |

| Dominant Region | North America |

| Segment Covered | By Fluid Type, By Additive Function, By Well Type, By Application, By Regions |

| Key companies profiled | Halliburton Company, SLB (Schlumberger Limited), Baker Hughes Company, BASF SE, The Dow Chemical Company, ChampionX (formerly Nalco Champion), Chevron Phillips Chemical Company, Solvay S.A., Clariant AG, Albemarle Corporation, Ashland Inc., Innospec Inc., Kemira Oyj, Calfrac Well Services Ltd., Group |

Fracking Chemicals and Fluids Market Value Chain Analysis

Fluid Formulation & Processing

- Fracking chemicals and fluids are developed through the blending of water, proppants, and specialty additives such as friction reducers, biocides, scale inhibitors, surfactants, and gelling agents to optimize hydraulic fracturing performance and reservoir productivity.

- Key players: Halliburton, Schlumberger, Baker Hughes, Dow

Quality Testing and Certification

- Fracking fluids require certifications ensuring operational effectiveness, environmental protection, and worker safety. Key certifications include ISO quality standards, API specifications, chemical disclosure compliance, and regional environmental regulations.

- Key players: ISO (International Organization for Standardization), API (American Petroleum Institute), ECHA (REACH), EPA

Distribution to Industrial Users

- Fracking chemicals and fluids are supplied to shale gas and tight oil operators, hydraulic fracturing service providers, and exploration and production companies.

- Key players: Halliburton, Schlumberger, Baker Hughes.

Fracking Chemicals and Fluids Regulatory Landscape: Global Regulations

| Country / Region | Regulatory Body | Key Regulations / Policies | Focus Areas |

| United States | EPA (Environmental Protection Agency) OSHA (Occupational Safety & Health Administration) State Environmental Agencies (e.g., Pennsylvania DEP, Colorado EMCMC) |

Chemical disclosure rules (e.g., EPA’s Hydraulic Fracturing Chemical Disclosure requirements) Clean Water Act – wastewater discharge & surface water protection Hazard Communication/OSHA standards State disclosure mandates (FracFocus registry, Pennsylvania PPC plans, Colorado full disclosure) |

Public reporting of injected fracturing chemicals Worker safety and hazard labeling Regulatory oversight of wastewater and spill prevention |

| European Union | European Chemicals Agency (ECHA) European Commission National Governments |

REACH (Registration, Evaluation, Authorization & Restriction of Chemicals) CLP (Classification, Labelling & Packaging) Water/waste protection laws National bans/moratoriums (e.g., France) |

Chemical safety assessment & restrictions Hazard labelling & public transparency Large-scale fracking bans or moratoria |

| China | Ministry of Ecology and Environment (MEE) National/Regional Environmental Bureaus |

Environmental Protection Law Pollution discharge standards Chemical registration/notification systems (e.g., for additives) |

Environmental compliance, wastewater disposal oversight Regulation of chemical content and discharge |

Segmental Insights

Fluid Type Insights

How Did Water Based Fluids Segment Dominate The Fracking Chemicals And Fluids Market In 2025?

The water-based fluids segment dominated the market with a share of approximately 69% in 2025, driven by their cost-effectiveness, environmental compliance, and superior ability to transport proppants. These fluids are preferred due to being more environmentally friendly, readily available, and cheaper compared to alternative oil-based or synthetic-based fluids. They are highly effective for transporting proppants and are widely used in shale gas and oil resources.

The oil-based fluids segment is projected to grow at the fastest CAGR between 2026 and 2035 in the market, driven by their superior ability to carry proppants, enhance well productivity in challenging formations, and increased use in unconventional, deepwater, and high-temperature reservoirs. Continued R&D to improve the efficiency and environmental performance of oil-based formulations further fuels the growth.

Fracking Chemicals And Fluids Market Share, By Fluid Type , 2025 (%)

| By Fluid Type | Revenue Share, 2025 (%) |

| Water-based Fluids (Slickwater) | 69.00% |

| Oil-based Fluids | 15.00% |

| Synthetic & Foam-based Fluids | 16.00% |

Additive Function Insights

Which Additive Function Segment Dominates the Fracking Chemicals and Fluids Market In 2025?

The friction reducers segment dominated the market with a share of approximately 32% in 2025, due to their essential role in high-rate slick-water pumping. These chemicals, particularly in high-concentration liquid form, are vital for reducing drag in long horizontal wells. Friction reducers are key in reducing resistive forces during pumping, enhancing energy efficiency, and supporting the shift toward water-based, environmentally conscious fracking.

The surfactants segment is projected to grow at the fastest CAGR between 2026 and 2035 in the market, driven by increasing demand for enhanced oil recovery (EOR) and unconventional shale gas extraction, leading to high growth projections. Surfactants, including anionic, cationic, and amphoteric types, are crucial for reducing liquid surface tension and improving stimulation efficiency, with a strong focus on biodegradable, environmentally friendly formulations.

Fracking Chemicals And Fluids Market Share, By Additive Function , 2025 (%)

| By Additive Function | Revenue Share, 2025 (%) |

| Friction Reducers | 32.00% |

| Gelling Agents | 25.00% |

| Surfactants & Biocides | 15.00% |

| Crosslinkers & Breakers | 10.00% |

| Others (Scale/Corrosion Inhibitors) | 18.00% |

Well Type Insights

How did Horizontal Wells Segment Dominate the Fracking Chemicals and Fluids Market in 2025?

The horizontal wells segment dominated the market with a share of approximately 85% in 2025, driven by higher production rates and increased shale gas/oil extraction. This segment thrives due to the need for specialized fluids to enhance hydrocarbon recovery in extended lateral sections. Horizontal wells provide significantly higher production rates compared to vertical wells, necessitating larger volumes of specialized chemicals.

The vertical wells segment is projected to grow at the fastest CAGR between 2026 and 2035 in the market, driven by its established technology and lower initial investment costs compared to horizontal drilling. Additionally, vertical wells are experiencing renewed demand due to ongoing exploration and the need for enhanced recovery techniques in specific applications.

Fracking Chemicals And Fluids Market Share, By Well Type , 2025 (%)

| By Well Type | Revenue Share, 2025 (%) |

| Horizontal Wells | 85.00% |

| Vertical Wells | 15.00% |

Application Insights

Which Application Segment Dominates the Fracking Chemicals And Fluids Market In 2025?

The shale gas segment dominated the market with a share of approximately 48% in 2025, driven by rising global energy demand and increased, efficient extraction of unconventional, trapped, and deeper resources, particularly through advancements in horizontal drilling. This segment thrives on increased shale exploration and the need for specialized, effective chemical additives in complex, horizontal well environments.

The tight oil segment is projected to grow at the fastest CAGR between 2026 and 2035 in the market, driven by expansion in unconventional oil and gas drilling. Other key growth factors are the dominance of water-based fluids and horizontal well types, while rising demand for tighter oil and gas reserves drives further sector expansion.

Fracking Chemicals And Fluids Market Share, By Application , 2025 (%)

| By Application | Revenue Share, 2025 (%) |

| Shale Gas Extraction | 48.00% |

| Tight Oil Extraction | 32.00% |

| Others (Coal Bed Methane/Geothermal) | 20.00% |

Regional Insights

The North America fracking chemicals and fluids market size was valued at USD 23.83 billion in 2025 and is expected to be worth around USD 42.03 billion by 2035, exhibiting at a compound annual growth rate (CAGR) of 5.84% over the forecast period from 2026 to 2035. North America dominated the market with a share of approximately 59.00% in 2025, driven by intense shale gas/tight oil exploration, particularly in the Permian Basin. The dominance was fueled by high demand for advanced, eco-friendly fluids, significant infrastructure, and major industry players. Innovation in high-performance, eco-friendly, and biodegradable chemicals, along with water-based fluids, increases growth in the region.

U.S. Fracking Chemicals and Fluids Market Growth Trends

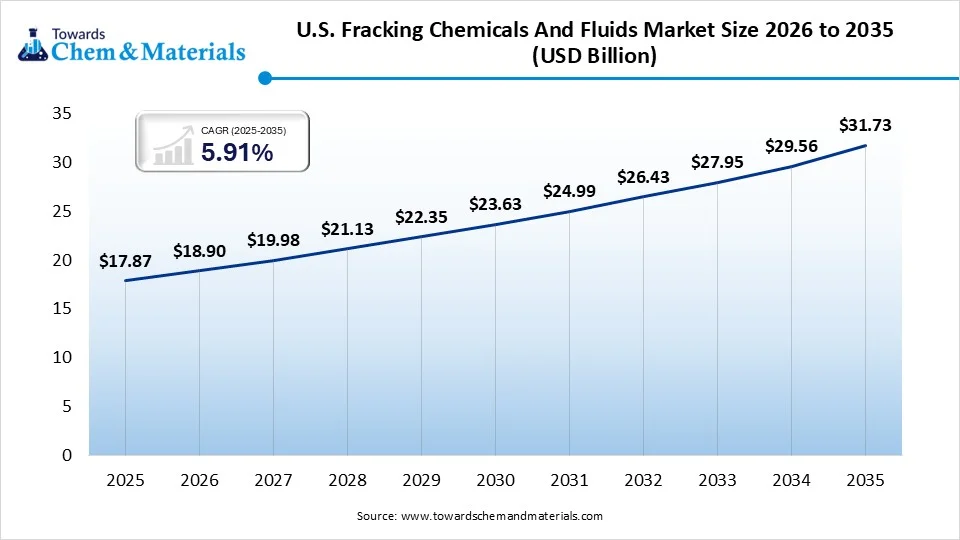

The U.S. fracking chemicals and fluids market size was valued at USD 17.87 billion in 2025 and is expected to be worth around USD 31.73 billion by 2035, exhibiting at a compound annual growth rate (CAGR) of 5.91% over the forecast period from 2026 to 2035. The U.S. fracking chemicals and fluids market is experiencing robust growth, driven by increasing shale exploration. The market is transitioning toward environmentally friendly, biodegradable additives, high-performance friction reducers, and waterless, or water-efficient, technologies. A strong shift is occurring toward non-toxic, biodegradable, and sustainable fracturing fluids to meet stringent environmental regulations and reduce groundwater contamination risks.

Asia Pacific Fracking Chemicals and Fluids Market Growth Factors

Asia Pacific is expected to have fastest growth in the market in the forecast period between 2026 and 2035, driven by rising unconventional energy demand and rapid industrialization. The market is experiencing growth due to the adoption of advanced horizontal drilling, the increasing need for eco-friendly, high-performance fluid additives, and investments in energy security. Increased focus on sustainability is driving the development of eco-friendly, biodegradable, and water-efficient fracking fluids.

Fracking Chemicals And Fluids Market Share, By Regional, 2025 (%)

| Regional | Revenue Share, 2025 (%) |

| North America | 59.00% |

| Europe | 15.00% |

| Asia Pacific | 12.00% |

| Latin America | 7.00% |

| Middle East & Africa | 7.00% |

China Fracking Chemicals and Fluids Market Growth Trends

The Chinese fracking chemicals and fluids market is projected to grow at a strong rate, driven by aggressive domestic shale gas expansion, deep-well drilling, and efforts to reduce energy import dependence. Other key growth factors include increasing use of eco-friendly water-based fluids and high-performance friction reducers. Increased adoption of horizontal drilling and advanced, environmentally friendly fracturing fluids, such as slickwater, is boosting efficiency and reducing environmental impact.

Recent Developments

- In July 2025, ADNOC Drilling was awarded an $800 million contract to provide hydraulic fracturing services for the Ghasha mega-project and other offshore developments. This deal supports ADNOC's goal of reaching a production capacity of 5 million barrels per day by 2027 and achieving gas self-sufficiency for the UAE.(Source: www.rigzone.com)

- In April 2025, the Colorado Energy and Carbon Management Commission finalized regulations mandating oil and gas drillers recycle fracking water under the Water Conservation in Oil and Gas Operations Act. The rules establish phased-in recycling targets for permits issued after January 1, 2026, starting at 2–4% in 2026 and increasing to 35% by 2038.(Source: coloradosun.com)

Top players in the Fracking Chemicals and Fluids Market & Their Offerings:

- Halliburton Company: Halliburton is one of the largest suppliers of fracking chemicals and fluid systems, offering comprehensive hydraulic fracturing fluid formulations including biocides, gelling agents, friction reducers, surfactants, and corrosion inhibitors designed to enhance hydrocarbon recovery and protect well infrastructure. Its CleanStim® bio-based fluids emphasize environmental performance and regulatory compliance capabilities.

- SLB (Schlumberger Limited): SLB (formerly Schlumberger) is a market leader providing integrated hydraulic fracturing chemicals and fluids, tailored to geological conditions with technology-driven solutions. Its portfolio includes advanced fluid systems, specialty additives, and digital optimization services that improve fracturing efficiency and reduce water usage.

- Baker Hughes Company: Baker Hughes delivers next-generation fracking fluid additives and fluid management technologies, including polymers, gelling agents, and friction reducers aimed at improving operational efficiency and reservoir stimulation. Its solutions are designed to balance performance with environmental compliance and cost-effectiveness.

- BASF SE: BASF leverages its advanced chemical manufacturing capability to supply high-performance fracking additives such as surfactants, biocides, gelling agents, and viscosity modifiers that optimize fluid performance in shale gas and tight oil operations. It emphasizes sustainable and effective formulations.

- The Dow Chemical Company: Dow provides specialty polymers, surfactants, friction reducers, and other chemical technologies for fracking fluids that improve proppant transport, reduce operational friction, and enhance hydrocarbon flowback.

- ChampionX (formerly Nalco Champion)

- Chevron Phillips Chemical Company

- Solvay S.A.

- Clariant AG

- Albemarle Corporation

- Ashland Inc.

- Innospec Inc.

- Kemira Oyj

- Calfrac Well Services Ltd.

- SNF Group

Segments Covered:

By Fluid Type

- Water-based Fluids (Slickwater)

- Oil-based Fluids

- Synthetic & Foam-based Fluids

By Additive Function

- Friction Reducers

- Gelling Agents

- Surfactants & Biocides

- Crosslinkers & Breakers

- Others (Scale/Corrosion Inhibitors)

By Well Type

- Horizontal Wells

- Vertical Wells

By Application

- Shale Gas Extraction

- Tight Oil Extraction

- Others (Coal Bed Methane/Geothermal)

By Regions

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Asia Pacific

- China

- India

- Japan

- South Korea

- Latin America

- Brazil

- Argentina

- Middle East & Africa

- Saudi Arabia

- South Africa

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

FAQ's

Select User License to Buy

Figures (4)