Content

What is the Current AdBlue Oil Market Size and Share?

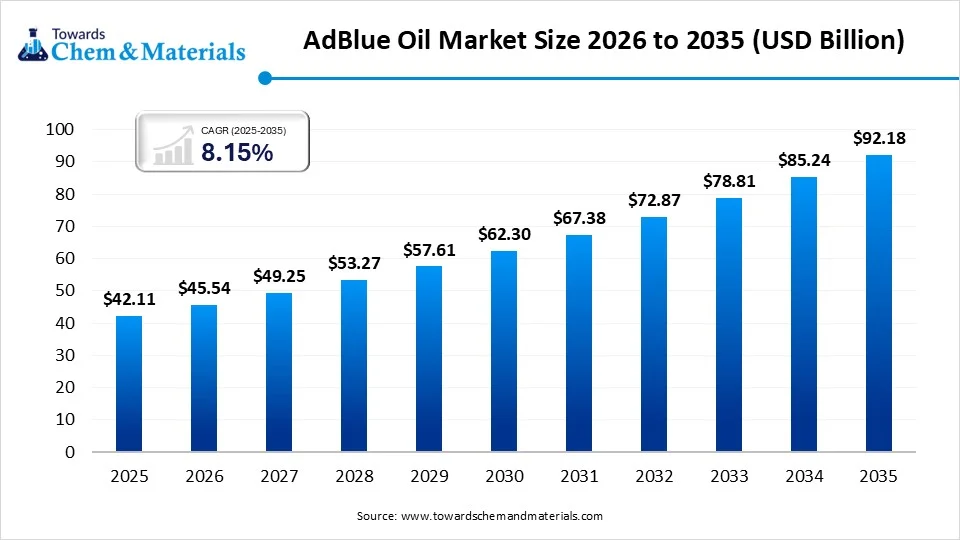

The global AdBlue oil market size was estimated at USD 42.11 billion in 2025 and is expected to increase from USD 45.54 billion in 2026 to USD 92.18 billion liters by 2035, growing at a CAGR of 40% from 2026 to 2035. Asia Pacific dominated the AdBlue oil market with the largest revenue share of 38.50% in 2025. The implementation of sustainability initiatives by global governments is fueling market growth in the current period.

Market Highlights

- The Asia Pacific dominated the adBlue oil market with the largest revenue share of over 38.50% in 2025

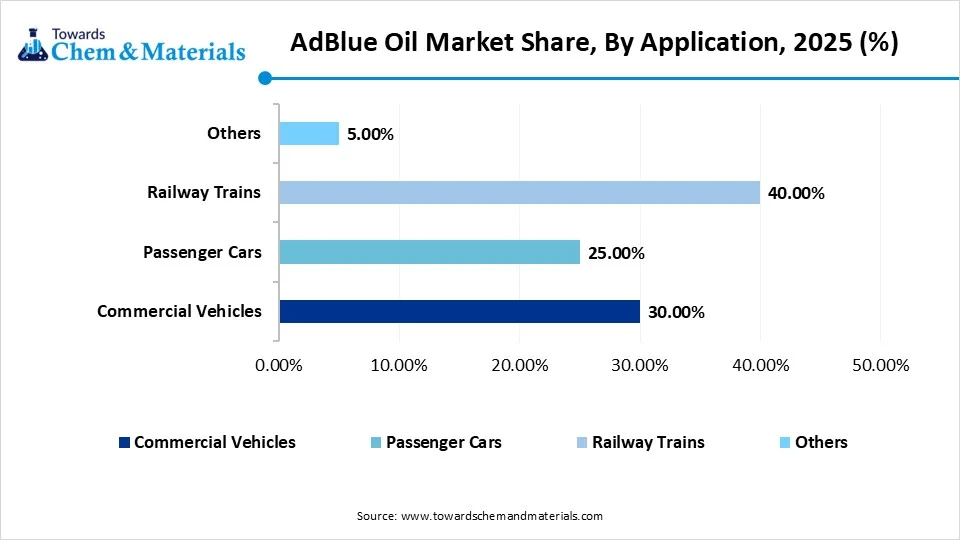

- By application, the commercial vehicles segment dominated the market with the largest revenue share of 47.85% in 2025, akin to the rising need for emission control in high-power diesel engines.

- By application, the passenger vehicles are anticipated to register the fastest CAGR of 6.89% over the forecast period, owing to governments globally enforcing stricter emission regulations for heavy-duty transport.

Trade Analysis

- According to Global Export Data, 50 Adblue shipments were exported from the world between Jun 2025 and May 2025 (TTM) through 30 verified exporters and 27buyers.

- The United States, Namibia, and the Philippines are the top Adblue importers, while China with 89 shipments, Germany with 50 shipments, and South Africa with 22 shipments, rank as the largest global Adblue exporters.

AdBlue Surge : Regulation, Innovation, and Global Demand Drive Market

The AdBlue oil market is undergoing a rapid phase of growth akin to the increasing regulatory push for reduced vehicular emissions across global markets. As governments implemented stricter environmental regulations, the demand for selective catalytic reduction (SCR) technology and, by extension, AdBlue, has witnessed consistent growth in recent years. This urea-based diesel exhaust fluid plays a critical role in lowering nitrogen oxide emissions, specifically in heavy-duty vehicles and off-road machinery. Also, the market is gaining momentum across transportation, agriculture, and construction sectors, where diesel engine usage remains high.

Manufacturers are rapidly increasing their production capacities and distribution networks to meet rising regional demands, particularly in regions such as Europe, North America, and Asia-Pacific. Furthermore, digital tracking and quality monitoring technologies are increasingly being integrated into the supply chain, ensuring efficiency and product integrity. With emission standards becoming stronger, AdBlue has become central to achieving sustainable mobility goals, making it a key focus area for automotive and fuel supply chains.

The increasing application of emission control regulations, particularly those aimed at curbing nitrogen oxide emissions from diesel engines, is driving the AdBlue oil market in the current period. As international standards such as Euro 6 and others take effect, vehicle manufacturers are increasingly adopting SCR technology, which requires a consistent supply of AdBlue in recent years. This regulation-driven transformation is encouraging operators and fuel distributors to invest in AdBlue infrastructure and storage facilities, contributing to industry growth in the current period. Also, the commercial vehicle sector, from logistics to public transportation, is accelerating the adoption of emission-reducing systems to comply with sustainability mandates. Furthermore, the regulatory landscape is not only increasing demand but also compelling innovation in fluid formulation, packaging, and delivery systems in recent years.

Recent Market Trends

- The expansion of dispensing infrastructure at fuel stations and logistics is driving the growth of the AdBlue oil market in the current period. With commercial operations growing increasingly, specifically in urban logistics and long trucking, the need for on-site and easily accessible AdBlue refilling stations has become critical in recent years. Moreover, fuel retailers and service providers are now integrating AdBlue pumps alongside diesel dispensers, sorting out operational logistics for transport companies.

- Strategic collaborations between AdBlue manufacturers and automotive OEMs are spearheading the industry's potential. As emission regulations become stronger globally, vehicle manufacturers are prioritizing partnerships with reliable AdBlue suppliers to ensure fluid compatibility, consistent quality, and seamless integration with SCR systems. This trend is changing product quality standards and boosting brand differentiation for both suppliers and automotive brands.

- The introduction of digital monitoring and smart dispensing systems is contributing to the industry's growth in the current period. Also, fleet operators and industrial users are seen adopting telemetry-based solutions to track AdBlue levels, consumption patterns, and refill needs in real time. These innovations are enhancing operational planning, reducing wastage, and ensuring uninterrupted compliance with emission regulations in the current period. Moreover, smart dispensers, equipped with IoT sensors and cloud connectivity, which allows for remote diagnostics, temperature control, and inventory alerts.

- Sustainability is an emerging trend in the AdBlue market, driving interest in bio-based and environmentally low-impact urea alternatives. Moreover, traditional AdBlue is derived from synthetic urea, which involves a carbon-intensive production process. Moreover, manufacturers are exploring formulations using urea produced from renewable storage or lower-emission chemical processes in the current period.

Report Scope

| Report Attribute | Details |

| Market Size in 2026 | USD 45.54 Billion |

| Expected Size by 2035 | USD 92.18 Billion |

| Growth Rate from 2025 to 2034 | 8.15% |

| Base Year of Estimation | 2025 |

| Forecast Period | 2025 - 2035 |

| Dominant Region | Asia Pacific |

| Segment Covered | By Type, By Application, By Region |

| Key Companies Profiled | BASF SE, Bosch Limited, Brenntag S.p.A., CF Industries Holdings, Inc., CrossChem Limited, Graco Inc., Komatsu, Mitsui Chemical, Inc., Nandan Petrochem Ltd., Nissan Chemical Company, S.C. OMV PETROM S.A., Shell plc, STOCKMEIER Group, TotalEnergies, Yara |

Market Opportunity

Next Gen Dispensing and Fleet Growth Fuel AdBlue Opportunities

The rapid growth of commercial and logistics fleets across global markets is expected to create lucrative opportunities for AdBlue oil market during the forecast period. As emission regulations become stronger, specifically in developing countries, fleet operators are under pressure to adopt SCR (Selective Catalytic Reduction) technologies that depend upon AdBlue. This shift can open significant growth doors for manufacturers to increase production capacities, establish supply partnerships, and enhance distribution networks in the future, as per the observation.

The increasing integration of IoT-enabled dispensing and monitoring systems is anticipated to create lucrative opportunities for manufacturers in the coming years. As the market increases, industries are moving toward digital tracking of AdBlue usage to improve operational efficiency, reduce wastage, and meet regulatory compliance. Also, the ability to offer real-time tracking, automated refill alerts, and remote diagnostics creates differentiation, allowing manufacturers to gain major attention in the coming years.

Market Challenge

Strong Sensitivity Creates Challenges for AdBlue Reliability

The material’s sensitivity to temperature and contamination affects its shelf-life and performance is likely Unlike traditional fuels or fluids, AdBlue requires strict storage conditions to maintain urea concentration and prevent degradation. Moreover, variations in temperature or exposure to sunlight can lead to crystallization or ammonia loss, reducing its effectiveness in SCR systems, which can create growth barriers for the AdBlue oil market in the coming years.

Trade Analysis

- According to Global Export Data, 50 Adblue shipments were exported from the world between Jun 2024 and May 2025 (TTM) through 30 verified exporters and 27buyers.

- The United States, Namibia, and the Philippines are the top Adblue importers, while China with 89 shipments, Germany with 50 shipments, and South Africa with 22 shipments, rank as the largest global Adblue exporters.

Segmental Insights

Application Insights

The railway trains segment dominated the market with the largest share in 2025, akin to the rising need for emission control in high-power diesel engines. Rail operators are seen adopting selective catalytic reduction (SCR) systems to meet stringent NOx emission standards while maintaining fuel efficiency. As long-distance trains and passenger trains depend heavily on diesel locomotion, consistent AdBlue usage becomes integral. Moreover, regulatory frameworks in Europe and Asia have accelerated compliance-driven demand, making railways a key application area.

")

The commercial vehicle segment is expected to experience notable market growth in the future, owing to governments globally enforcing stricter emission regulations for heavy-duty transport. Fleets across logistics, construction, and municipal services increasingly integrate SCR technologies to align with evolving environmental standards in the current period. Moreover, the growing dependence on diesel-based movement, specifically in developing markets, fuels consistent AdBlue demand. Furthermore, fleet operators prioritize efficiency and regulatory compliance, leading to higher consumption patterns. With infrastructure expansion and e-commerce growth boosting road vehicle volumes, which is expected to drive the growth of the market during the upcoming years.

AdBlue Oil Market Share, By Application, 2025 (%)

| By Application | Revenue Share, 2025 (%) |

| Commercial Vehicles | 30.00% |

| Passenger Cars | 25.00% |

| Railway Trains | 40.00% |

| Others | 5.00% |

Regional Insights

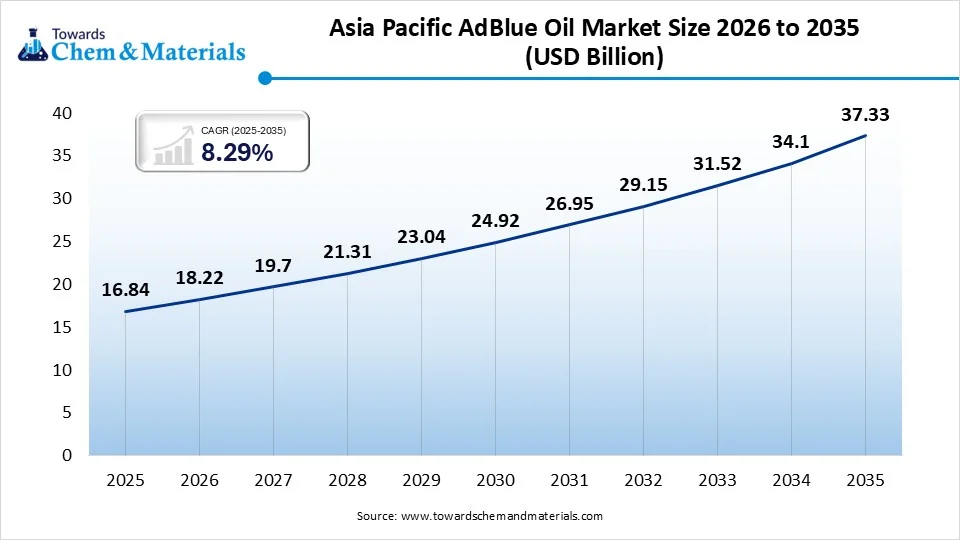

The Asia-Pacific adBlue oil market size is valued at 18.22 billion in 2026 and is expected to be worth around 37.33 billion by 2035, growing at a compound annual growth rate (CAGR) of 8.29% over the forecast period 2025 to 2035.

Asia Pacific Accelerates: Emerging Economies Drive AdBlue Demand, Asia Pacific is expected to grow at a significant pace in the coming period, akin to rising vehicle production, expanding transportation networks, and accelerating environmental regulations in countries such as China and India in the current period. Also, governments are actively pushing for cleaner diesel technologies, promoting SCR system adoption in the commercial sector, which has severely contributed to the demand for AdBlue oil in recent years. The growing industrialization and surge in diesel-powered vehicles in emerging economies contribute to increased AdBlue consumption. Furthermore, as domestic manufacturing capacities rise, regional suppliers are increasing production to meet demand.

")

Green Mandates and Market Stability: Europe’s AdBlue Advantage, Europe expects notable growth in the market in future, akin to early adoption of sustainability policies and a mature regulatory framework. The region’s focus on decarbonization and strict Euro emission standards has long driven SCR implementation in both commercial and passenger vehicles in the region. However, supply chain challenges such as high energy costs and regional production disruptions have occasionally impacted availability and pricing in Europe. Despite this, the strong policy backing and consumer attention on green mobility have sustained consistent demand in recent years. Europe’s adoption of alternative fuels and electrification introduces uncertainty, but AdBlue remains important for existing diesel fleets in the current period.

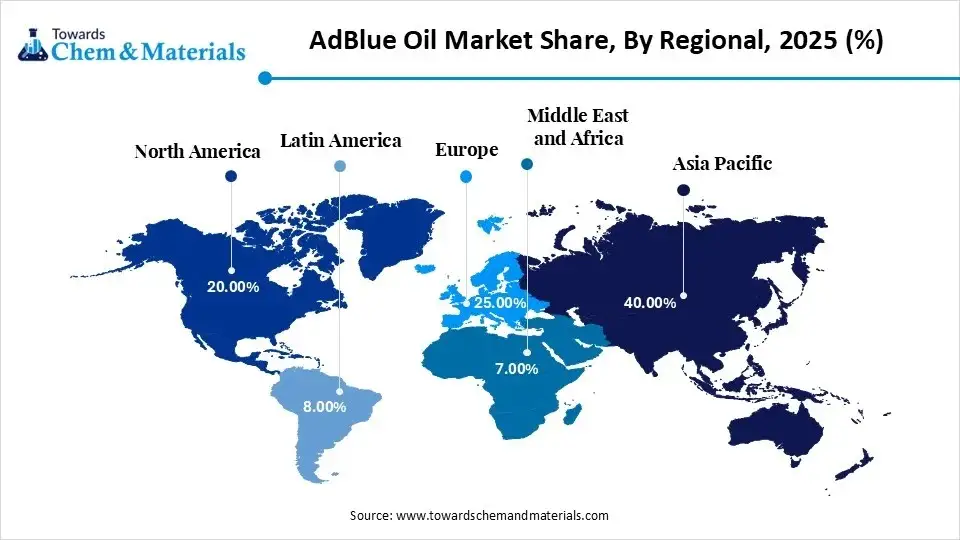

North America Leads With Regulation-Driven AdBlue Adoption, North America dominated the AdBlue oil market share 20.00% in 2025, akin to stringent emission regulations, particularly in countries such United States, where EPA standards have driven widespread adoption of selective catalytic reduction (SCR) systems in the current period. The well-established commercial transportation network, along with high diesel vehicle penetration, supports consistent AdBlue demand, which is the primary driver in the country nowadays. Also, the region gained advantage from a robust distribution infrastructure and early regulatory enforcement, pushing fleet operators and vehicle manufacturers to follow emission control technologies in the current period. These factors, combined with growing

U.S. AdBlue Oil Market Growth Trends

The U.S. AdBlue market is experiencing robust growth, largely driven by strict EPA emission regulations for heavy-duty diesel vehicles. The other key growth factors include widespread Adoption of Selective Catalytic Reduction (SCR) technology, rising demand in the construction/transportation sectors, and the integration of IoT for real-time AdBlue level monitoring, driving market growth. Major players include Yara International ASA, TotalEnergies, and BASF, with US-DEF focusing on retail market growth.

India AdBlue Oil Market Growth Trends

The India AdBlue (Diesel Exhaust Fluid) market is experiencing rapid growth, driven by the strict enforcement of BS-VI emission standards, which mandate Selective Catalytic Reduction (SCR) technology in diesel vehicles. The market is expanding due to increasing heavy-d00uty vehicle sales, rapid urbanization, and rising environmental awareness, supporting the growth of the market. Expansion in logistics, infrastructure development, and the construction sector is boosting the number of diesel trucks, cranes, and heavy machinery, which are major users of AdBlue.

AdBlue Oil Market Share, By Regional, 2025 (%)

| Regional | Revenue Share, 2025 (%) |

| North America | 20.00% |

| Europe | 25.00% |

| Asia Pacific | 40.00% |

| Latin America | 8.00% |

| Middle East & Africa | 7.00% |

Germany AdBlue Oil Market Growth Trends

Germany's AdBlue market is experiencing robust growth, driven by strict Euro 6/VI emission standards, a massive, aging diesel commercial vehicle fleet, and impending Euro 7 regulations. As a top European consumer, Germany focuses on expanding infrastructure for AdBlue, with high demand for Selective Catalytic Reduction (SCR) technology in both heavy-duty trucks and passenger cars. The integration of IoT and sensors to monitor AdBlue levels in real-time is growing, improving efficiency, which further fuels the growth and expansion of the market.

Recent Developments

- In December 2024, LIQUI MOLY introduced their latest additive for AdBlue recently. Moreover, this AdBlue supports nitrogen oxide levels in diesel engines as per the company claim. (Source : liquimoly.com)

- In February 2024, BPCL unveiled its mobile MAK AdBlue dispenser in Kolkata, India, recently. The main motive of the launch is to access eco-friendly fuel access. (Source : energy.economictimes.indiatimes)

- In April 2024, BASF introduced its latest product, called AdBlueR ZeroPCF. The company’s motive behind the launch is to reduce its carbon footprint. (Source: fuelsandlubes)

Top Vendors in AdBlue Market & Their Offerings

- Yara International ASA: Yara is one of the largest global producers of AdBlue, leveraging its large-scale urea manufacturing capabilities. The company markets AdBlue under the Air1® brand and supplies diesel exhaust fluid to commercial fleets, fuel stations, and logistics operators worldwide.

- BASF SE: BASF provides high-purity AdBlue solutions and emission control chemicals for diesel vehicles equipped with selective catalytic reduction (SCR) systems.

- CF Industries Holdings, Inc.: CF Industries is a major nitrogen fertilizer and urea producer supplying raw materials and finished diesel exhaust fluid products for transportation and industrial applications.

- BASF SE

- Bosch Limited

- Brenntag S.p.A.

- CF Industries Holdings, Inc.

- CrossChem Limited

- Graco Inc.

- Komatsu

- Mitsui Chemical, Inc.

- Nandan Petrochem Ltd.

- Nissan Chemical Company

- S.C. OMV PETROM S.A.

- Shell plc

- STOCKMEIER Group

- TotalEnergies

- Yara

Segment Covered in the Report

By Application

- Commercial Vehicles

- Passenger Cars

- Railway Trains

- Others

By Region

- North America

- U.S.

- Canada

- Mexico

- Europe

- UK

- Germany

- France

- Italy

- Spain

- Sweden

- Denmark

- Norway

- Asia Pacific

- Japan

- China

- India

- Australia

- South Korea

- Thailand

- Latin America

- Brazil

- Argentina

- The Middle East and Africa

- South Africa

- Saudi Arabia

- UAE

- Kuwait

Report Dashboard

Our Chemicals & Materials Research Solutions

- Comprehensive chemicals & materials market analysis

- Competitive landscape intelligence dashboard

- Material innovation & sustainability development tracker

- Market sizing & demand forecasting tools

- Chemicals & materials trend intelligence reports

- Customer application behavior insights

- Customized chemicals & materials research solutions

Chemical Supplier Solutions

- Supplier identification & capability mapping

- Production capacity & geographic footprint analysis

- Quality & performance monitoring

- Compliance & regulatory insights

- Commercial readiness assessment

- Supplier network relationship mapping

Category Intelligence Solutions

- Chemical category overview & segmentation

- End-use demand patterns & application insights

- Raw material pricing & cost structure analysis

- Industry dynamics & competitive structure

- Supply chain & distribution mapping

- Manufacturing benchmarks & industry standards

- Key reports & strategic deliverables

Customer Insights Analytics

- Buyer profile & overview

- Spend analysis & scope

- Procurement strategy & model

- Vendor criteria & expectations

- Contract terms & policies

- Market entry & engagement strategy

- Pain points & buying triggers

- Research outputs & insights

Pricing Intelligence Solutions

- Chemical price benchmarking & comparisons

- Raw material trends & cost insights

- Indexation models & price adjustment analysis

- Total material cost evaluation

- Commercial agreements & contract terms

Brand Intelligence Solutions

- Brand positioning within markets

- Market share & competitive presence

- Customer perception & brand performance

- Go-to-market effectiveness strategy

- Digital presence & industry reputation

- Performance indicators & growth gaps

FAQ's

Select User License to Buy

Figures (5)